?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

We investigate the asymmetric nonlinear link between foreign direct investment, oil prices, and CO2 emissions for the Gulf Cooperation Council nations, using foreign direct investment and oil price data. As foreign direct investment is positively associated with carbon emissions in the long run and oil prices have positive, significant effects on CO2 emissions, our findings support the pollution-haven hypothesis. Furthermore, these variables have an asymmetric nonlinear relationship, which corresponds to the theoretical expectations of the pollution-haven hypothesis. We also find that negative changes in foreign direct investment have positive, significant impacts on carbon emissions in the short run, implying that foreign enterprises utilize green technologies in their manufacturing processes in the short run. In the long run, however, negative changes in oil prices are positively associated with carbon emissions. These findings should help Gulf Cooperation Council economies focus on policies that encourage foreign direct investment in green rather than dirty industries in order to ensure environmental sustainability.

PUBLIC INTEREST STATEMENT

Over the last three decades, the global economy has experienced significant problems as a result of global warming and environmental degradation. Carbon dioxide (CO2) emissions are thought to be the principal cause of these issues. A large portion of the research on the link between FDI, oil prices, and CO2 emissions ignores the asymmetric or nonlinear nature of the relationship. We analyses the asymmetric nonlinear relationship between oil prices, foreign direct investment and CO2 emissions for Gulf Cooperation Council (GCC) nations. Our findings are align with the pollution theory, which states that corporations who pollute the environment choose to locate their factories and other facilities in developing nations with low environmental restrictions. Negative changes in oil prices, on the other hand, are positively related with carbon emissions in the long term. These findings should help GCC economies in focusing on policies that attract foreign direct investment in green rather than dirty industries to maintain environmental sustainability.

1. Introduction

The global economy has faced considerable challenges as a result of global warming and environmental deterioration over the last three decades. Mounting carbon dioxide (CO2) emissions are considered the primary source of these problems. The environmental Kuznets curve (EKC) hypothesis proposes an inverted-U-shaped relationship between various pollutants and per capita income; that is, as income rises, environmental pressure also rises to a point and then it declines (Dinda, Citation2004). After achieving some threshold income level, economic growth places less pressure on the environment and may even have positive/green impacts (Ozturk & Acaravci, Citation2010). A large section of the literature on environmental pollution and its implications for an economy focuses mainly on the empirical evidence of the environmental Kuznets curve hypothesis and limits its analysis to the relationship between economic growth and carbon emissions. However, economic growth and energy consumption may not be sufficient to account for all of the factors that contribute to increased environmental pollution. The roles of investment, especially foreign direct investment (FDI), and oil prices in enhancing environmental pollution warrant closer scrutiny, especially in relation to Gulf Cooperation Council (GCC) economies.

The net effects of FDI on climate change and pollution have been the subject of continuous discussion. FDI is also a vital component in the development strategies of developing and developed economies. Emerging and developed economies rely on FDI to supplement their domestic savings through capital inflows to promote economic development. More than half of FDI inflows to the Middle East come from the GCC economies. Here, FDI is mainly concentrated in five sectors: oil, coal and natural gas, chemicals, real estate, hotels and tourism, and metals. The voluminous increase in FDI in these sectors can affect CO2 emissions and climate change in different ways. In one set of studies, it is argued that FDI may increase CO2 emissions in countries with relaxed environmental standards (Acharyya, Citation2009; Gokmenoglu et al., Citation2015). Another set of studies reveals that foreign investment has favorable impacts on environmental protection in the form of multinational corporations using efficient technologies and having high environmental standards, which helps economies reduce air pollution (Goldenman, Citation1999; Zarsky, Citation1999; Zeng & Eastin, Citation2012).

A general formulation is that economies may intentionally relax their environmental regulations and standards in order to draw large inflows of FDI as this contributes to economic growth. The pollution-haven hypothesis (PHH) and the assumption of capital flight argue that multinational corporations often seek locations where both labor and resources are relatively cheap. However, these decisions by multinational corporations come at the cost of introducing environmentally degrading practices mainly to developing countries. Polluting multinationals minimize production costs by investing in dirty industries in developing economies with inefficient environmental standards and procedures (Gokmenoglu et al., Citation2015; Lau et al., Citation2014). However, FDI can also have positive direct impacts on environmental pollution when these investment inflows into developing economies encourage increased environmental awareness (Zeng & Eastin, Citation2012). In this study, we analyze the existence of a PHH in relation to the GCC economies. Further, as there is scant evidence on the impact of FDI on CO2 emissions, we undertake an asymmetric analysis to identify the FDI effects on carbon emissions, specifically in the GCC.

The GCC was established on 25 May 1981, in Abu Dhabi. The Gulf Cooperation Council economies, comprising Bahrain, Kuwait, Qatar, the Sultanate of Oman, the United Arab Emirates, and the Kingdom of Saudi Arabia have common characteristics in their histories, language, economic backgrounds, and culture. These countries are the main exporters of oil and gas among Arabian economies whose populations speak the same language (Arabic) and share the same religion (Islam). Oil plays a strategic and crucial role in the structure and pattern of the GCC economies. According to the US Energy Information Agency (Citation2018), in 2006, the GCC economies’ crude oil reserves amounted to 500.7 billion barrels, accounting for 30.42% of total world oil reserves. Oil constituted around 80% of government revenues, 50% of GDP, and 70% of total exports in the GCC that year.

Energy is a vital component and critical driver of modern economic, social, and technological activities (Kebede et al., Citation2010; Oyedepo, Citation2014). The volatile nature of oil prices ultimately affects the economic activities of both oil exporting and importing economies. Large fluctuations in oil prices and their economic impacts are important concerns among researchers and policymakers. Oil is responsible for more than 35% of all global energy consumption. Households use energy in different ways, such as for cooking, lighting, heating purposes and transportation. Industrial and commercial activities heavily depend on energy for communications services, banking, social and economic activities, transportation, and educational and health delivery, among others. However, despite being a driver of economic progress, oil also generates carbon dioxide (CO2), a harmful greenhouse gas. An increase in oil prices will reduce its consumption at both household and industrial levels and encourage consumers and industry to switch to renewable energy sources (Sadorsky, Citation2009; Umar et al., Citation2021).

The importance of crude oil prices in the economic activity of net oil-exporting economies is well documented in the literature (Lescaroux & Mignon, Citation2008; Mehrara & Oskoui, Citation2007; Umar et al., Citation2022). While many studies in the economics literature focus on the effects of oil shocks on GCC economies’ economic activities, and there are few studies on the relationship between oil prices and carbon emissions in GCC economies. Crude oil prices are a key factor in determining these economies’ economic activity and, as a result, they can have an impact on the GCC’s environmental quality by directly influencing energy demand and consumption. As the GCC economies rely heavily on the production of fossil fuels, an increase in economic activity due to higher crude oil prices will lead to an increase in energy consumption in this region; this would imply a decline in environmental quality.

There is a multidimensional relationship between oil prices, energy consumption and environmental quality. The massive oil reserves in the GCC economies, combined with recent fluctuations in international oil prices have heightened the importance of energy to the region’s economic growth. Energy use in GCC economies is inefficient since these countries are rich in fossil fuels and can provide domestic consumers with fossil-fuels-based energy at relatively lower prices. This phenomenon leads to significant energy consumption and poor levels of energy efficiency (Howarth et al., Citation2017). This, in turn, contributes to an increase in carbon emissions in the GCC economies. The oil price shocks from 2000 to 2016 witnessed an economic downturn in the GCC. This clearly illustrates that oil price shocks may have varying effects on the region’s economic activity. Accordingly, most of the existing literature assumes a linear relationship between oil prices, FDI and environmental quality; however, this may not be the case. Hence, our study focuses on the asymmetric effects of oil prices on carbon emissions. Analyzing the relation between oil prices and carbon emissions with special reference to the GCC countries is important for policymaking.

This study provides an empirical assessment of the asymmetric effects of oil prices and FDI on carbon emissions. As such, it lends further insights into these variables in the context of GCC economies. Our paper is one of the early attempts to use panel nonlinear autoregressive distribution lag (ADRL) analysis to examine the impacts of FDI and oil prices on carbon emissions in the context of GCC economies. We extend the literature by analyzing a unique group of oil-endowed countries and investigating the relationship between oil prices and FDI on carbon emissions. Given the non-linear nature of the underlying relationship between these variables, we employ a novel econometric framework that allows us to analyze this relationship. Our sample consists of six GCC economies. The study period is 1999 to 2016, a time during which the GCC economies faced global turbulence. Our findings confirm the existence of the pollution hypothesis, as FDI has considerable positive impacts on carbon emissions in a region that is an oil producer and exporter. Concurrently, oil prices are also positively associated with carbon emissions.

The paper is structured as follows: Section 2 furnishes some stylized facts, followed by literature review in section 3. Section 4 describes the model and data. Our estimation findings and discussions are presented in section 5, and the paper concludes with section 6.

2. Stylized facts

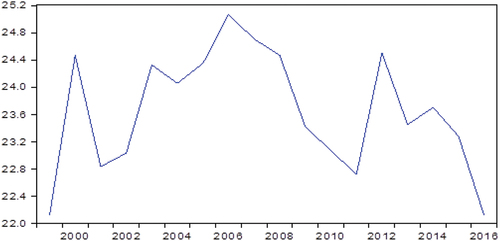

The GCC economies contribute significantly to global CO2 emissions. shows GCC emissions in metric tons per capita, for the period 2000 to 2016. The list of GCC economies is presented in Appendix 1. The share of GCC economies’ CO2 emissions is oscillatory in nature and has witnessed significant increases in absolute terms, from 22.12 metric tons per capita in 1999, to an all-time high of 25.06 metric tons per capita in 2007. The region’s carbon emissions decreased after the 2008 global financial crisis and declined to an all-time low in 2016, perhaps due to greener technologies being introduced after the financial crisis.

Figure 1. CO2 emissions (metric tons per capita) in the Gulf Cooperative Council 2000 to 2016.Source: World Development Indicators, World Bank

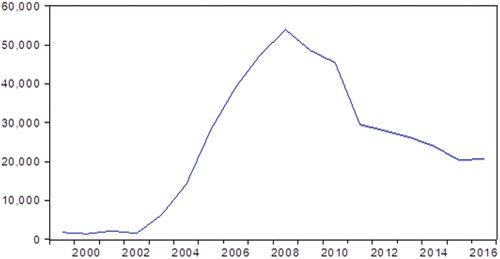

shows FDI inflows to the Gulf Cooperation Council economies. These inflows significantly increased from 1999 to 2008, reached an all-time high in 2008 and the began to decrease, perhaps due to the financial crisis, among other reasons. Saudi Arabia and the United Arab Emirates are the most significant contributors to FDI inflows to the GCC economies. It is interesting to note that the trend line in FDI shows a similar pattern to the trend in the GCC’s CO2 emissions; one could expect a relationship between FDI and CO2 emissions in these oil-producing economies. The sharp decline in FDI inflows after the 2008 financial crisis suggests that, after this event, countries mainly depended on internal finance to supplement domestic savings and promote economic development.

Figure 2. Foreign direct investment inflows to the Gulf Cooperative Council of Countries 2000 to 2016.Source: United Nations Conference on Trade and Development (UNCTAD)

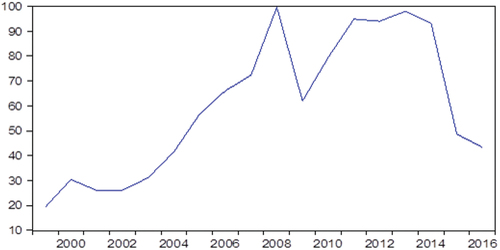

shows oil price trends in the GCC economies over the study period. The graph follows a similar trend to those shown in the previous two figures: oil prices followed a mixed pattern, with many ups and downs over the period, trending upward to $US99.67 per barrel in 2008, decreasing for the next two years, rising again until 2014, plummeting in 2015, and further tapering off to $US42.29 per barrel of West Texas intermediate crude oil in 2016.

Figure 3. West Texas Intermediate crude oil prices 2000 to 2016.Source: Federal Reserve Economic Data

3. Literature review

The literature review is divided into two themes: the research on FDI and carbon emissions, and on oil prices and carbon emissions.

3.1. Foreign direct investment and carbon emissions

The relationship between FDI and CO2 emissions is widely documented. In particular, during the last decade this topic has attracted a lot of attention in the literature (see, Acharyya, Citation2009; Chandran & Tang, Citation2013; Gokmenoglu et al., Citation2015). The debate on the empirical evidence on whether FDI generates positive effects on CO2 emissions in host countries is inconclusive at both micro and national levels. The validity of the PHH has been tested in much of the literature. According to the theory, foreign firms will relocate their dirty industries’ production activities from developed or advanced economies to developing and emerging economies to avoid the environmental costs associated with the higher environmental standards that exist in developed countries. A large number of surveys provide cross-country evidence that is in line with the theoretical expectation that FDI induces carbon emissions (Acharyya, Citation2009; Chandran & Tang, Citation2013; Gokmenoglu et al., Citation2015). Zhang and Zhang (Citation2018) used cointegration and the vector error correction model (VECM) approach to analyze the impacts of FDI, exchange rates, GDP and the trade structure on carbon emissions. They found that FDI has an unfavorable impact on China’s carbon emissions, which supports the existence of the pollution-haven hypothesis in relation to that country. Contrary to the theoretical expectations, some empirical studies either find that FDI does not have significant impacts on carbon emissions or do not have sufficient information to prove the existence of the PHH (Eskeland & Harrison, Citation2003; Kheder & Zugravu, Citation2012; Millimet & Roy, Citation2015; Tang, Citation2015).

Ren et al. (Citation2014) found that FDI is positively associated with carbon emissions, meaning that foreign investors tend to invest in dirty industries in destination economies, especially in developing ones. Kivyiro and Arminen (Citation2014) found that the effects of FDI on carbon emissions varies from one country to another. Baek (Citation2016) validates the relationship between the PHH and FDI and its detrimental effects on the environment. Concurrently, a large section of the literature validates the halo hypothesis, which states that the coefficient of FDI is negatively associated with carbon emissions, or that FDI has some positive impacts on environmental protection (Merican et al., Citation2007; Zeng & Eastin, Citation2012). Shahbaz et al. (Citation2015) found that FDI has adverse effects on the environment in developing economies; this indicates that the outcomes are sensitive to specific econometric models, model specifications, and choice of countries. Huang et al. (Citation2019) studied the effects of exports, imports and FDI on CO2 emissions in Turkey and found that these relationships are asymmetric. These authors also noted that FDI has no long-term effects on CO2 emissions in that country and, as such, does not play a large role in Turkey’s rising CO2 emissions per capita. Kim (Citation2019) examined the causative links between CO2 emissions, energy consumption, GDP and FDI in 57 developing countries from 1980 to 2013. He found that FDI has a negative long-run effect on CO2 emissions, but the very small coefficient implies that FDI does not cause CO2 emissions in developing economies, findings that refute the PHH. Huang et al. (Citation2019) employed panel quantile regression to investigate the effects of FDI and foreign trade on Chinese provincial CO2 emissions for the period 1997 to 2014. They found that FDI has a negative and significant effect on CO2 emissions except in the 5th and 10th quantiles (per capita GDP). At the same time, Hanif et al. (Citation2019) analyzed the relationship between FDI, fossil fuels consumption, and economic growth on the carbon emissions of 15 Asian developing economies. They contended that FDI is a cause of environmental degradation since it increases domestic CO2 emissions, confirming the existence of the pollution-haven hypothesis.

Hamid et al. (Citation2020) reveals that FDI has a positive influence on environmental quality, implying that increased FDI inflows in China would result in higher energy consumption, and therefore higher CO2 emissions. Hamid et al. (Citation2021) find the environmental impacts associated with shocks to the nation’s FDI inflows, capital investment figures, and economic growth is asymmetric. The positive shocks to the economic growth, FDI inflows and capital investments induce the carbon dioxide emissions both in the short and long run. They also validated the environmental Kuznets curve and pollution haven hypothesis as same as Ozgur et al. (Citation2021). According to Mujtaba et al. (Citation2020), economic growth and trade openness have negative and significant effects on carbon dioxide emissions, implying that higher economic growth and openness increase carbon dioxide emissions. A large section of the existing literature (Mujtaba et al., Citation2021; Kongkuah et al., Citation2021, Citation2020) find that there are positive relations between energy consumption, population, economic growth on CO2 emissions.

3.2. Oil prices and carbon emissions

The relationship between oil prices and carbon emissions is another strand of literature that has attracted a lot of attention over the last few decades. The price of energy is critical to the economic growth of any economy. The effects of changes in crude oil prices significantly differ between oil-exporting and importing economies, oil consumption being an important expense for the latter. When oil prices fluctuate, there is a significant negative impact on economies that heavily depend on it for energy. The literature suggests there are large impacts on inflation and output (Backus & Crucini, Citation2000; Hamilton, Citation2003). A large number of studies find that increases in oil prices lead to reductions in the consumption of oil, which in turn results in reductions in carbon emissions (Mensah et al., Citation2019; Wong et al., Citation2013). A rise in energy prices, on the other hand, represents a lack of oil, encouraging oil-importing countries to turn to cheaper alternatives, thereby also reducing carbon emissions (Li et al., Citation2019). Other factors that prompt oil-importing countries to diversify their energy mix by turning to greener alternatives include regulating oil imports from limited suppliers (OPEC) and fears about climate change (Jones & Warner, Citation2016; Troster et al., Citation2018; Umar et al., Citation2021a).

Energy is an essential component of both household consumption and manufacturing production; however, most of the recent research shows a negative relationship between energy (oil) prices and energy use (Li et al., Citation2019; Ohler & Billger, Citation2014). According to Fuinhas and Marques (Citation2013), crude oil has a significant impact on the economic activities of oil-dependent economies by affecting the relationship between energy demand and economic drivers. In a conventional economy, a positive contribution from energy consumption to economic growth is expected. These authors also found that the price of crude oil has a strong and important effect on Algeria’s energy consumption in the long run. In the case of Egypt, however, the price of oil has no discernible effect on energy consumption; on the other hand, there is a strong correlation between oil prices and energy demand (Fuinhas & Marques, Citation2013).

Malik et al. (Citation2020) found that the price of oil has a positive and substantial impact on carbon emissions in the short run. Asymmetric studies suggest that when oil prices increase, emissions decrease in the long run, while a decrease in prices increases emissions. Saboori et al. (Citation2016) show that the ecological footprint is positively associated with oil consumption and economic growth. They also found that there is no significant causal relationship between the ecological footprint, oil prices and oil consumption. Katircioglu (Citation2017) found that there exists a significant negative long-run relationship between oil prices and carbon emissions, which implies that increases in oil prices result in a reduction in the level of carbon emissions. Mensah et al. (Citation2019) found a unilateral cause-and-effect relationship between oil prices, economic development, energy use (fossil fuels) and carbon emissions across all countries in both the long and short term. Alshehry and Belloumi (Citation2015) included crude oil prices in an analysis of the relationship between carbon emissions, energy consumption and economic growth in Saudi Arabia. They discovered that the underlying impact of oil resources on economic activities in oil-resource-dependent economies causes increases in CO2 emissions. Nwani (Citation2017) found that for the Ecuadorean economy crude oil prices have a positive causal impact on carbon emissions in both the short and long run, implying that higher crude oil prices generate economic conditions that lead to increased energy consumption and CO2 emissions in that country. These findings also indicate that there is one-way causality between crude oil prices and energy use. A large stratum of existing literature (Mujtaba et al., Citation2021, Citation2022; Mujtaba & Jena, Citation2021; Ostic et al., Citation2021) finds that the foreign direct investment inflows are negatively associated with carbon dioxide emissions. Mujtaba and Jena (Citation2021) discover that both positive and negative oil price shocks have a positive and substantial effect on CO2 emissions. Furthermore, positive shock energy consumption has a favourable and considerable influence on CO2 emissions. Jijian et al. (Citation2021) find a negative relationship between exports and carbon dioxide emissions, and positive relationship between imports and carbon dioxide emissions.

On reviewing the literature, one possible reason for the inconclusive findings on the effects of FDI on CO2 emissions is the use of symmetric analyses. A vast section of the literature on the relationship between FDI, oil prices and CO2 emissions does not consider the asymmetric or nonlinear relationship between these variables. In fact, the effects of positive and negative changes in FDI and oil prices differ in their impacts on carbon emissions. Reviewing the vast literature in this area, some crucial insights emerge. First, an empirical review indicates that we cannot generalize the impacts of oil prices and FDI on carbon emissions by assuming there is a linear relationship between these variables. Second, studies pertaining to the nonlinear relationship between FDI and carbon emissions as it explicitly relates to GCC economies are conspicuously absent. The present study tries to bridge this gap by analyzing the nonlinear relationship between FDI, oil prices and carbon emissions for the GCC economies. In the process, we also attempt to validate the pollution haven hypothesis for this region. It is evident from the literature that findings on this relationship are inconclusive.

4. Data and methodology

The data for the empirical analysis, except for the FDI inflows, oil prices and financial development variables, were sourced from the World Bank’s World Development Indicators. The data on the FDI inflows were obtained from the United Nations Conference on Trade and Development (UNCTAD). The data on financial development come from the International Monetary Fund. The data on oil prices were sourced from the St. Louis Fed, Economic Research Resources. Our balanced panel consists of observations for six Gulf Cooperation Council economies (Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, and United Arab Emirates)

for the period 1999 to 2016. Two considerations mainly guided the selection of the countries and time periods: a) the availability and consistency of the data; and b) incorporating a period during which the world economy experienced both growth and turbulence that were driven by capital flows. We use CO2 emissions as the dependent variable in our analysis. presents descriptions of the variables and their corresponding data sources.

Table 1. Description of the variables used in the study for the period 1999 to 2016

The descriptive statistics in show that the variables vary largely across the GCC. These statistics indicate the heterogeneity between these economies as the dependent and independent variables vary from one country to another.

Table 2. Summary statistics of the variables for the period 1999 to 2016

4.1. Methodology

The long-run characteristics of time series are usually analyzed using estimation techniques such as the unit root and cointegration. Here, we examine the nature and magnitude of the relationship between FDI, oil prices, and CO2 emissions, using a nonlinear autoregressive distributed lag (NARDL) in panel form, according to Shin et al. (Citation2014). The results and discussion are divided into three parts. First, we determine the order in which our main variables are integrated. Second, after determining that the variables are stationary, we examine the relationship between them in both the short and long run, using a panel ARDL model. Third, after defining the linear relationship between these variables, our nonlinear ARDL model is used to examine their asymmetric relationships.

4.1.1. Panel unit root test

Our analysis begins with a panel unit root test, which is well known in the empirical macroeconomics literature for its weak restrictions. On all seven variables, the panel unit root test is used on both the levels and the first difference. Im et al. (Citation2003), Breitung (Citation2001), Harris et al. (Citation1999), Hadri (Citation2000), and Levin et al. (Citation2002) are referred to when using panel unit root test statistics to investigate the integration properties of FDI, oil prices, CO2 emissions, financial development, trade openness, urbanization, and GDP.

To test for stationarity, Breitung (Citation2001) used the following model:

Below are the null hypothesis and the alternative hypothesis for the test statistics.

To formulate the test statistics, we use Breitung’s (Citation2001) method on the transformed vectors below:

The transformed vectors are used to establish the following test statistic:

These vectors follow a standard normal distribution.

To assess the stationarity of the variables, we use a modified Dickey-Fuller regression according to the method of Im et al. (Citation2003) (hereafter, IPS). This method incorporates both time series and cross-section measurements, so few time series are required for the test to be effective. To analyze the long-run relationship in the panel results, the IPS is considered a superior test. An updated augmented Dickey-Fuller regression is also used in the test.

where is the lag length,

is a vector of deterministic terms, and

is the corresponding vector of the coefficients. The hypothesis of the test can be written as

for all i

for at least one i

We use the IPS to test the null and hypothesis 1 with the standardized t-bar statistic:

Since Im et al. (Citation2003) proposed a cross-sectional de-meaned version, their test is superior to other tests when N and T are minimal. This test is also useful when there is a common time-specific variable in the errors across multiple regressions.

The Levin et al. (Citation2002) (hereafter, LLC) panel unit root test has the following form:

where is the first difference operator, k is the lag length,

and

are unit-specific fixed and time effects, respectively. The null hypothesis is

for all i, the alternative hypothesis is

for all i. The rejection of the null hypothesis means that the variable is stationary. Cross-sectional units may have different speeds of adjustment toward long-run equilibrium, but the main assumption of the LLC is that

is homogeneous, meaning that it does not take into consideration the different speeds of adjustment. Harris et al. (Citation1999) used unit root tests with the null hypothesis of the unit root in a common process similar to Breitung (Citation2000) and Levin et al. (Citation2002). Similarly to Im et al. (Citation2003), Maddala and Wu (Citation1999) assumed the unit root with an individual unit root process. Hadri (Citation2000) assumed a null hypothesis of the unit root with individual unit root processes.

The panel unit root results are shown in . Regardless of the panel unit root test type, we discover that the variable for CO2 emissions is integrated of order zero [I (0)] or, alternatively, we have enough information to reject the null hypothesis of non-stationarity. On the other hand, the unit root tests for the remaining variables yield mixed findings. This means that in separate tests, the variables are integrated of either order zero or order one. As a result, we can use both integrated of order zero and order one variables in an ARDL analysis, which reassures the usage of the ARDL model.

Table 3. Panel unit root tests of the variables for the period 1999 to 2016

4.1.2. Panel nonlinear ARDL model

We use Shin et al.’s (Citation2014) panel nonlinear ARDL framework, which is also a representation of a dynamic heterogeneous panel data model and is highly recommended for a panel with a large time dimension. This empirical method was chosen for three reasons: first, it allows us to incorporate the asymmetries in our research in a nonlinear manner. Second, as we saw with oil prices and FDI, it takes into account the data’s inherent variability. Third, whereas cointegration approaches demand that the variables be integrated in order one I (1), we use an ARDL to evaluate the short- and long-run correlations regardless of the order of integration of the variables. Nonetheless, we cannot apply the ARDL when the variables are integrated of order two; that is, I (2). The ARDL offers efficient, consistent estimators since it adjusts the issue of endogeneity by incorporating the lag lengths for the exogenous and endogenous variables.

The NARDL model is suitable for our analysis since we deal with the dynamic heterogeneous panel data with a large T (time period). The pooled mean group (PMG) and mean group (MG) estimators are the two prominent methodologies used in the empirical literature to analyze heterogeneous panels. Pesaran and Smith (Citation1995) modified the PMG estimation from the MG estimation methods. The MG estimator is considered a pooled estimator as it employs the average values of the coefficients for each group and assumes that the slope coefficients and error variances are identical across groups (Pesaran et al., Citation1999).

The PMG estimator provides an error correction term in addition to estimating the short- and long-run relationships between the cointegrated variables. This term indicates the presence of a long-term relationship between the variables. The PMG estimator, in addition to the MG estimator, provides for the short-run heterogeneity in the calculations. The Hausman test, on the other hand, is used to determine whether the estimators have any systematic differences. If the test rejects the null hypothesis, suggesting a systematic difference between the estimators, the MG estimator is the right estimation. Furthermore, the PMG estimator is adequate for the investigation if we do not have enough data to reject the null hypothesis.

The first stage in our research is to look at the link between CO2 emissions, oil prices, and FDI, using a symmetric panel ARDL, assuming that CO2 emissions react symmetrically to changes in the other two variables. Second, by modifying the assumption of a symmetric response, we employ the panel nonlinear ARDL to allow for positive and negative changes in FDI and oil prices. The baseline panel ARDL model is given as

where represents the CO2 emissions (in metric tons per capita) for each emerging economy i over time t

and

are trade as a percentage of GDP and the log GDP, respectively, URBAN is the urban population (% of the total population),

is the group-specific effects

captures the country-specific effects.

The nonlinear panel ARDL model, as previously indicated, assists us in nonlinearly capturing the asymmetric impacts of oil prices and FDI on CO2 emissions. Changes in FDI and oil prices, both positive and negative, may have differing effects on CO2 emissions. In the estimate, the nonlinear ARDL integrates the differential implications of these positive and negative changes. As a result, the panel nonlinear ARDL element of the estimation is divided into two sections: the first examines the nonlinear link between FDI and CO2 emissions, while the second investigates the nonlinear relationship between oil prices and CO2 emissions (metric tonnes per capita). Hence, the nonlinear panel models are given as

Where ,

are the positive and negative changes in the FDI.

where ,

are the positive and negative shocks in oil prices.

5. Results and discussions

Our findings show that there is insufficient evidence to reject the null hypothesis; that is, there are no systematic differences between the estimators; this confirms the pooled mean group estimator’s suitability. In other words, our findings justify the use of the PMG estimator to investigate the short- and long-term link between FDI, oil prices, and carbon emissions. The PMG assumes that all cross sections have the same long-run coefficient or long-run connection between the variables. The PMG estimator will coincide with the mean group estimator if our cross sections are homogeneous.

The panel ARDL results, presented in , indicate the short- and long-term effects of FDI and oil prices on CO2 emissions. As for the negative coefficient of the error correction term, we find the existence of a significant long-run link between FDI, oil prices, and CO2 emissions. Our findings also show that trade has a long-term negative relationship with CO2 emissions, implying that trade has some environmentally benign consequences (If an economy is opening more and more, there is a tendency to reduce CO2 emissions). The linear ARDL results show a positive, substantial link between economic growth and carbon emissions, implying that GCC economies’ economic progress has some negative long-term environmental consequences. Our results are in tandem with the existing literature of Behera and Dash (Citation2017) for middle-income countries, Naz et al. (Citation2019) and Malik et al. (Citation2020) for Pakistan, and Zhang and Zhang (Citation2018) for China.

Table 4. Linear panel ARDL results of the variables for the period 1999 to 2016

We find a significant positive effect of increased shares of FDI on CO2 emissions, implying that foreign direct investment has a large positive impact on CO2 emissions. The pollution-haven hypothesis can better explain the phenomenon where significant inflows in FDI lead to an increase in CO2 emissions as this implies that investment inflows are mainly oriented toward “dirty” industries. The GCC economies’ environmental policies (or lack thereof) along with their poor implementation of environmental standards could explain these trends. These results are consistent with previous research by Zhang and Zhang (Citation2018) for China and Malik et al. (Citation2020) for Pakistan, which found a positive relationship between FDI and carbon emissions. In the short and long run, there are differences in the link between oil prices and carbon emissions. Oil prices are inversely proportional to CO2 emissions in both the short and long term. Jewell et al. (Citation2018) reveal that changes in oil subsidies have significant impacts on the consumption of oil-exporting countries compared to oil-importing economies. Our findings are consistent with a large body of literature that also finds that crude oil prices influence the interaction between energy consumption and the drivers of economic activity in oil-dependent economies; in other words, there is a positive relationship between oil prices and carbon emissions (e.g., Agbanike et al., Citation2019; Fuinhas & Marques, Citation2013; Nwani, Citation2017).

For the rest of the control variables, financial development and urbanization do not significantly affect carbon emissions in either the short or long run.

5.1. Foreign direct investment and CO2 emissions (panel NARDL analysis)

To determine the impact of FDI on CO2 emissions, we assign asymmetric nonlinearity to foreign direct investment. We use the Wald test to assess the asymmetric nonlinear relationship between FDI and carbon emissions, and we conclude that FDI has nonlinear asymmetry in the short run. This indicates that a nonlinear relationship between FDI and carbon emissions exists in the short run. We employ a panel nonlinear ARDL model to analyze the asymmetric relationship between FDI and carbon emissions. The results of the nonlinear ARDL, presented in , demonstrate that economic growth, trade, and carbon dioxide emissions all have the same relationship. In the short run, negative changes in FDI exert positive and significant impacts on carbon emissions. This implies that negative changes in FDI have adverse effects on the environment in the GCC economies in the short run. FDI, on the other hand, has a long-term positive and significant influence on carbon emissions. Combining these two findings, one may conclude that the pollution-haven theory holds true for the GCC economies in the long run. Our results are in line with a large section of the literature (Acharyya, Citation2009; Chandran & Tang, Citation2013; Gokmenoglu et al., Citation2015; Hamid et al., Citation2020; Kheder & Zugravu, Citation2012; Millimet & Roy, Citation2015) that validates the pollution haven hypothesis.

Table 5. Foreign direct investment and CO2 emissions (panel NARDL analysis results) of the variables for the period 1999 to 2016

Table 6. Oil pricesOil prices and CO2 emissions and CO2 emissions (panel NARDL analysis results) of the variables for the period 1999 to 2016

In the short run, however, foreign companies may use greener technologies but domestic companies may use environmentally degrading technologies in their production processes and this may be the prime reason for the positive effects of negative changes in FDI. Concurrently, the rest of the variables also provide the same results as those we observed in the linear panel ARDL model, except that oil prices do not significantly affect carbon emissions in the long run. In the short run, apart from the FDI variable, the results are more or less the same as those in the linear panel ARDL model. Concurrently, the control variables also provide the same results as those we observed in the linear panel ARDL in the short run.

5.2. Oil prices and CO2 emissions (panel NARDL analysis)

In this section, we assign asymmetric nonlinearity to oil prices. We use the Wald test to assess the nonlinear link between oil prices and carbon emissions and discover a nonlinear relationship in the long run. We also use a panel nonlinear ARDL model to investigate their asymmetric relationship.

The coefficient value of the positive changes in oil prices is positive but not significant in the long run. A decrease in oil prices, on the other hand (negative shocks in the partial sum of oil prices) increases carbon emissions. Oil prices do not have significant impacts on carbon emissions in the short run. In the long run, however, the negative coefficient linked to oil prices means that lower oil prices lead to increased consumption of fossil fuels in industrial and manufacturing processes. The resulting inefficient use of energy contributes to an increase in carbon emissions in the GCC economies. Our findings are consistent with some previous research (Hammoudeh et al., Citation2014; Katircioglu, Citation2017) that found that oil prices have a long-term negative and considerable impact on carbon emissions. Lower oil prices will lead to increased energy consumption by both households and industries, while higher oil costs will lead to a shift to renewable energy sources (Sadorsky, Citation2009). The remaining variables produce findings that are identical to those of the panel ARDL model ().

6. Conclusions

The literature shows a linear link between foreign direct investment, oil prices, and carbon emissions. However, is noticeably devoid of discussions on the nonlinear asymmetric link between these elements in the context of the GCC economies. In this study, we provide an empirical investigation of the asymmetric nonlinear effects of FDI and oil prices on carbon emissions. Using data for six GCC economies, covering the period 1999 to 2016, and applying a panel nonlinear ARDL model, we establish a long-run relationship between FDI, oil prices, and carbon emissions. At the same time, we uncover evidence of the asymmetric nonlinear impacts of FDI on carbon emissions in the short term, as well as a long-run nonlinear relationship between oil prices and carbon emissions.

The results of our panel ARDL model reveal that, in the long run, FDI has a positive and considerable influence on carbon emissions. This proves the existence of the pollution-haven hypothesis in regard to the Gulf Cooperation Council countries. The positive coefficient sign associated with oil prices, in the long run, implies that oil prices are positively associated with carbon emissions also in the long run. Concomitantly, oil prices also have adverse impacts on carbon emissions in the short run. The nonlinear panel ARDL results show an asymmetric relationship between FDI, oil prices, and carbon emissions. In the short term, there is nonlinear asymmetry between FDI and carbon emissions, while in the long run, a nonlinear asymmetry exists between oil prices and carbon emissions. We find that, in the short run, negative changes in FDI have positive, significant impacts on reducing carbon emissions, which implies that, in the short run, foreign companies may use green technologies for their production processes. However, the positive coefficient associated with FDI in the long run indicates that after establishing production units in one country, foreign firms gradually become dirty industries, which is evidence for the pollution-haven hypothesis in the GCC economies. Concomitantly, negative changes in oil prices are positively associated with carbon emissions, which shows that reductions in oil prices lead to the overuse of energy, mainly energy from fossil fuels, which increases carbon emissions in the GCC economies.

6.1. Policy implications

Our findings have several policy implications for market participants, policymakers and investors. There is a global demand for sustainable development and sustainable financing alternatives. Fossil fuels such as oil have been documented to have adverse environmental impacts. We extend this discussion by accounting for the underlying relation between oil prices and CO2 emissions in the world’s most oil-endowed region. Most of the GCC countries are looking for alternatives to their oil-intensive economies. Our findings on the nonlinear relationship between oil prices, FDI, and CO2 emissions implicitly point to the need to emphasize on policies that divert FDI from dirty industries to the green ones, thus, underscoring the need to find ways to divert economies from their existing fossil-fuels-based strategies toward green ones. According to our study, since oil prices are negatively related to carbon emissions, policies for innovation in the alternative energy sector should be prioritized and introduced in the GCC economies. However, green policies are difficult to devise because they require clear recognition of the characteristics of economic activities.

These findings are important for devising sustainable fuel sources as well for investors interested in hedging against environmental risks. For investors, these findings are useful for developing cross-country and cross-assets hedging strategies, which are highly desirable objectives for sustainable financing solutions. Our nonlinear empirical methodology underscores the importance of accounting for asymmetry and nonlinearity in the underlying relationships between these variables. Overall, our findings support the extant strand of the literature that seeks alternatives to fossil fuels and that asserts that emissions reduction is important for all countries and more so for oil-endowed ones.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

Notes on contributors

Sania Ashraf

Sania Ashraf is a young professor having 5 years of teaching and research experience handling core Finance and Accounting courses to undergraduates and master level students. A PhD holder in Finance and Accounting with several peer reviewed publications in Finance including studies on conventional and Islamic stock market, sea port efficiency analysis and environmental degradation. She has also been the reviewer for several Scopus and ABDC indexed journals like Brazilian Administrative Review and International Journal of Islamic and Middle Eastern Finance and Management. Dr. Sania is currently working on many syllabus development programs including Fin Tech with ADGM and CFA as part of the curriculum committee for Abu Dhabi University. Sania’s research interest are in the area of Islamic-Conventional Banking & Finance, Fintech and AI, Behavioral Finance, Risk Management & Evaluation, Financial Modelling and International Financial Markets and Energy Economics. Dr. Sania was one of the panelists of Bloomberg GCC symposium in collaboration with ADNOC and Ministry of Education representing UAE.

References

- Acharyya, J. (2009). FDI, growth and the environment: Evidence from India on CO2 emission during the last two decades. Journal of Economic Development, 34(1), 43. https://doi.org/10.35866/caujed.2009.34.1.003

- Agbanike, T. F., Nwani, C., Uwazie, U. I., Anochiwa, L. I., Onoja, T. G. C., & Ogbonnaya, I. O. (2019). Oil price, energy consumption and carbon dioxide (CO 2) emissions: Insight into sustainability challenges in Venezuela. Latin American Economic Review, 28(1), 1–20. https://doi.org/10.1186/s40503-019-0070-8

- Alshehry, A. S., & Belloumi, M. (2015). Energy consumption, carbon dioxide emissions and economic growth: The case of Saudi Arabia. Renewable and Sustainable Energy Reviews, 41, 237–247. https://doi.org/10.1016/j.rser.2014.08.004

- Backus, D. K., & Crucini, M. J. (2000). Oil prices and the terms of trade. Journal of International Economics, 50(1), 185–213. https://doi.org/10.1016/S0022-1996(98)00064-6

- Baek, J. (2016). A new look at the FDI–income–energy–environment nexus: Dynamic panel data analysis of ASEAN. Energy Policy, 91, 22–27. https://doi.org/10.1016/j.enpol.2015.12.045

- Behera, S. R., & Dash, D. P. (2017). The effect of urbanization, energy consumption, and foreign direct investment on the carbon dioxide emission in the SSEA (South and Southeast Asian) region. Renewable and Sustainable Energy Reviews, 70, 96–106. https://doi.org/10.1016/j.rser.2016.11.201

- Breitung, J. (2000) The Local Power of Some Unit Root Tests for Panel Data. Advances in Econometrics, 15, 161–177. http://dx.doi.org/10.1016/S0731-9053(00)15006-6

- Breitung, J. (2001). Rank tests for nonlinear cointegration. Journal of Business and Economic Statistics, 19(3), 331–340. https://doi.org/10.1198/073500101681019981

- Chandran, V. G. R., & Tang, C. F. (2013). The impacts of transport energy consumption, foreign direct investment and income on CO2 emissions in ASEAN-5 economies. Renewable and Sustainable Energy Reviews, 24, 445–453. https://doi.org/10.1016/j.rser.2013.03.054

- Dinda, S. (2004). Environmental Kuznets Curve Hypothesis: A Survey. Ecological Economics, 49(4), 431–455. https://doi.org/10.1016/j.ecolecon.2004.02.011

- Eskeland, G. S., & Harrison, A. E. (2003). Moving to greener pastures? Multinationals and the pollution haven hypothesis. Journal of Development Economics, 70(1), 1–23. https://doi.org/10.1016/S0304-3878(02)00084-6

- Fuinhas, J. A., & Marques, A. C. (2013). Rentierism, energy and economic growth: The case of Algeria and Egypt (1965–2010). Energy Policy, 62, 1165–1171. https://doi.org/10.1016/j.enpol.2013.07.082

- Gokmenoglu, K., Azin, V., & Taspinar, N. (2015). The relationship between industrial production, GDP, inflation and oil price: The case of Turkey. Procedia Economics and Finance, 25, 497–503. https://doi.org/10.1016/S2212-5671(15)00762-5

- Goldenman, G. (1999). The environmental implications of foreign direct investment: Policy and institutional issues. Foreign Direct Investment and the Environment, 1, 75–91.

- Hadri, K. (2000). Testing for stationarity in heterogeneous panel data. The Econometrics Journal, 3(2), 148–161. https://doi.org/10.1111/1368-423X.00043

- Hamid, I., Jena, P. K., & Mukhopdhyay, D. (2020). Should China prefer more foreign direct investment inflows to environmental change? Journal of Public Affairs, 22(2), 1–18. https://doi.org/10.1002/pa.2466

- Hamid, I., Shabbir, A., Murshed, M., Jena, P. K., Sha, N., & Alam, M. N. (2021 1-17). The roles of foreign direct investments, economic growth, and capital investments in decarbonizing the economy of Oman. Environmental Science and Pollution Research, 29(15), 22122–22138. https://doi.org/10.1007/s11356-021-17246-3

- Hamilton, J. D. (2003). What is an oil shock? Journal of Econometrics, 113(2), 363–398. https://doi.org/10.1016/S0304-4076(02)00207-5

- Hammoudeh, S., Nguyen, D. K., & Sousa, R. M. (2014). Energy prices and CO2 emission allowance prices: A quantile regression approach. Energy Policy, 70, 201–206. https://doi.org/10.1016/j.enpol.2014.03.026

- Hanif, I., Raza, S. M. F., Gago-de-Santos, P., & Abbas, Q. (2019). Fossil fuels, foreign direct investment, and economic growth have triggered CO2 emissions in emerging Asian economies: Some empirical evidence. Energy, 171, 493–501. https://doi.org/10.1016/j.energy.2019.01.011

- Harris, R., Tzavalis, D., & E. (1999). Inference for unit roots in dynamic panels where the time dimension is fixed. Journal of Econometrics, 91(2), 201–226. https://doi.org/10.1016/S0304-4076(98)00076-1

- Howarth, N., Galeotti, M., Lanza, A., & Dubey, K. (2017). Economic development and energy consumption in the GCC: An international sectoral analysis. Energy Transitions, 1(2), 1–19. https://doi.org/10.1007/s41825-017-0006-3

- Huang, Y., Chen, X., Zhu, H., Huang, C., & Tian, Z. (2019). The heterogeneous effects of FDI and foreign trade on CO2 emissions: Evidence from China. Mathematical Problems in Engineering, 2019, 1–14 .

- Im, K. S., Pesaran, M. H., & Shin, Y. (2003). Testing for unit roots in heterogeneous panels. Journal of Econometrics, 115(1), 53–74. https://doi.org/10.1016/S0304-4076(03)00092-7

- Jewell, J., McCollum, D., Emmerling, J., Bertram, C., Gernaat, D. E., Krey, V., Riahi, K., Berger, L., Fragkiadakis, K., Keppo, I., Saadi, N., Tavoni, M., van Vuuren, D., Vinichenko, V., & Riahi, K. (2018). Limited emission reductions from fuel subsidy removal except in energy-exporting regions. Nature, 554(7691), 229–233. https://doi.org/10.1038/nature25467

- Jijian, Z., Twum, A., Agyemang, A., Kofi, E., & Ayamba, E. (2021). Empirical study on the impact of international trade and foreign direct investment on carbon emission for belt and road countries. Energy Reports, 7, 7591–7600. https://doi.org/10.1016/j.egyr.2021.09.122

- Jones, G. A., & Warner, K. J. (2016). The 21st century population-energy-climate nexus. Energy Policy, 93, 206–212. https://doi.org/10.1016/j.enpol.2016.02.044

- Katircioglu, S. (2017). Investigating the role of oil prices in the conventional EKC model: Evidence from Turkey. Asian Economic and Financial Review, 7(5), 498–508. https://doi.org/10.18488/journal.aefr/2017.7.5/102.5.498.508

- Kebede, E., Kagochi, J., & Jolly, C. M. (2010). Energy consumption and economic development in Sub-Saharan Africa. Energy Economics, 32(3), 532–537. https://doi.org/10.1016/j.eneco.2010.02.003

- Kheder, S. B., & Zugravu, N. (2012). Environmental regulation and French firms location abroad: An economic geography model in an international comparative study. Ecological Economics, 77, 48–61. https://doi.org/10.1016/j.ecolecon.2011.10.005

- Kim, S. (2019). CO2 emissions, foreign direct investments, energy consumption, and GDP in developing countries: A more comprehensive study using panel vector error correction model. Korean Economic Review, 35(1), 5–24. http://keapaper.kea.ne.kr/RePEc/kea/keappr/KER-20190101-35-1-01.pdf.

- Kivyiro, P., & Arminen, H. (2014). Carbon dioxide emissions, energy consumption, economic growth, and foreign direct investment: Causality analysis for Sub-Saharan Africa. Energy, 74, 595–606. https://doi.org/10.1016/j.energy.2014.07.025

- Kongkuah, M., Yao, H., Fonjong, B., & Agyemang, A. (2021). The role of CO2 emissions and economic growth in energy consumption: Empirical evidence from Belt and Road and OECD countries. Environmental Science and Pollution Research, 28, https://doi.org/10.1007/s11356-020-11982-8.

- Lau, L. S., Choong, C. K., & Eng, Y. K. (2014). Investigation of the environmental Kuznets curve for carbon emissions in Malaysia: Do foreign direct investment and trade matter? Energy Policy, 68, 490–497. https://doi.org/10.1016/j.enpol.2014.01.002

- Lescaroux, F., & Mignon, V. (2008). On the influence of oil prices on economic activity and other macroeconomic and financial variables. OPEC Energy Review, 32(4), 343–380. https://doi.org/10.1111/j.1753-0237.2009.00157.x

- Levin, A., Lin, C. F., & Chu, C. S. J. (2002). Unit root tests in panel data: Asymptotic and finite-sample properties. Journal of Econometrics, 108(1), 1–24. https://doi.org/10.1016/S0304-4076(01)00098-7

- Li, X., Zhou, Y., Yu, S., Jia, G., Li, H., & Li, W. (2019). Urban heat island impacts on building energy consumption: A review of approaches and findings. Energy, 174, 407–419. https://doi.org/10.1016/j.energy.2019.02.183

- Maddala, G. S., & Wu, S. (1999). A comparative study of unit root tests with panel data and a new simple test. Oxford Bulletin of Economics and Statistics, 61(S1), 631–652. https://doi.org/10.1111/1468-0084.0610s1631

- Malik, M. Y., Latif, K., Khan, Z., Butt, H. D., Hussain, M., & Nadeem, M. A. (2020). Symmetric and asymmetric impact of oil price, FDI and economic growth on carbon emission in Pakistan: Evidence from ARDL and non-linear ARDL approach. Science of the Total Environment, 726, 138421. https://doi.org/10.1016/j.scitotenv.2020.138421

- Mehrara, M., & Oskoui, K. N. (2007). The sources of macroeconomic fluctuations in oil exporting countries: A comparative study. Economic Modelling, 24(3), 365–379. https://doi.org/10.1016/j.econmod.2006.08.005

- Mensah, I. A., Sun, M., Gao, C., Omari-Sasu, A. Y., Zhu, D., Ampimah, B. C., & Quarcoo, A. (2019). Analysis on the nexus of economic growth, fossil fuel energy consumption, CO2 emissions and oil price in Africa based on a PMG panel ARDL approach. Journal of Cleaner Production, 228, 161–174. https://doi.org/10.1016/j.jclepro.2019.04.281

- Merican, Y., Yusop, Z., Noor, Z. M., & Hook, L. S. (2007). Foreign direct investment and the pollution in five ASEAN nations. International Journal of Economics and Management, 1(2), 245–261.

- Millimet, D. L., & Roy, J. (2015). Multilateral environmental agreements and the WTO. Economics Letters, 134, 20–23. https://doi.org/10.1016/j.econlet.2015.05.035

- Mujtaba, A., Jena, P. K., & Mukhopdhyay, D. (2020). Determinants of CO2 emissions in upper middle-income group countries: An empirical investigation. Environmental Science and Pollution Research, 27(30), 37745–37759. https://doi.org/10.1007/s11356-020-09803-z

- Mujtaba, A., & Jena, P. K. (2021). Analyzing asymmetric impact of economic growth, energy use, FDI inflows and oil prices on CO2 emissions through NARDL approach. Environmental Science and Pollution Research, 28(24), 30873–30886. https://doi.org/10.1007/s11356-021-12660-z

- Mujtaba, A., Jena, P. K., & Joshi, D. P. P. (2021). Growth and determinants of CO2 emissions: Evidence from selected Asian emerging economies. Environmental Science and Pollution Research, 28(29), 39357–39369. https://doi.org/10.1007/s11356-021-13078-3

- Mujtaba, A., Jena, P. K., Bekun, F. V., & Sahoo, P. (2022). Symmetric and asymmetric impact of economic growth, capital formation, renewable and non renewable energy consumption on environment in OECD Countries. Renewable and Sustainable Energy Reviews, 160(112300), 1–13. https://doi.org/10.1016/j.rser.2022.112300

- Naz, S., Sultan, R., Zaman, K., Aldakhil, A. M., Nassani, A. A., & Abro, M. M. Q. (2019). Moderating and mediating role of renewable energy consumption, FDI inflows, and economic growth on carbon dioxide emissions: Evidence from robust least square estimator. Environmental Science and Pollution Research, 26(3), 2806–2819. https://doi.org/10.1007/s11356-018-3837-6

- Nwani, C. (2017). Causal relationship between crude oil price, energy consumption and carbon dioxide (CO2) emissions in Ecuador. OPEC Energy Review, 41(3), 201–225. https://doi.org/10.1111/opec.12102

- Ohler, A. M., & Billger, S. M. (2014). Does environmental concern change the tragedy of the commons? Factors affecting energy saving behaviors and electricity usage. Ecological Economics, 107, 1–12. https://doi.org/10.1016/j.ecolecon.2014.07.031

- Ostic, D., Twum, A. K., & Agyemang, A. O. (2021). Assessing the impact of oil and gas trading, foreign direct investment inflows, and economic growth on carbon emission for OPEC member countries. Environ Sci Pollut Res. https://doi.org/10.1007/s11356-021-18156-0

- Oyedepo, S. O. (2014). Towards achieving energy for sustainable development in Nigeria. Renewable and Sustainable Energy Reviews, 34, 255–272. https://doi.org/10.1016/j.rser.2014.03.019

- Ozturk, I., & Acaravci, A. (2010). CO2 emissions, energy consumption and economic growth in Turkey. Renewable and Sustainable Energy Reviews, 14(9), 3220–3225. https://doi.org/10.1016/j.rser.2010.07.005

- Pesaran, M. H., & Smith, R. (1995). Estimating long-run relationships from dynamic heterogeneous panels. Journal of Econometrics, 68(1), 79–113. https://doi.org/10.1016/0304-4076(94)01644-F

- Pesaran, M. H., Shin, Y., & Smith, R. P. (1999). Pooled mean group estimation of dynamic heterogeneous panels. Journal of the American Statistical Association, 94(446), 621–634. https://doi.org/10.1080/01621459.1999.10474156

- Ren, S., Yuan, B., Ma, X., & Chen, X. (2014). International trade, FDI (foreign direct investment) and embodied CO2 emissions: A case study of China's industrial sectors. China Economic Review, 28, 123–134. https://doi.org/10.1016/j.chieco.2014.01.003

- Saboori, B., Sulaiman, J., & Mohd, S. (2016). Environmental Kuznets curve and energy consumption in Malaysia: A cointegration approach. Energy Sources, Part B: Economics, Planning, and Policy, 11(9), 861–867. https://doi.org/10.1080/15567249.2012.662264

- Sadorsky, P. (2009). Renewable energy consumption and income in emerging economies. Energy Policy, 37(10), 4021–4028. https://doi.org/10.1016/j.enpol.2009.05.003

- Shahbaz, M., Loganathan, N., Zeshan, M., & Zaman, K. (2015). Does renewable energy consumption add in economic growth? An application of auto-regressive distributed lag model in Pakistan. Renewable and Sustainable Energy Reviews, 44, 576–585. https://doi.org/10.1016/j.rser.2015.01.017

- Shin, Y., Yu, B., & Greenwood-Nimmo, M. (2014). Modelling asymmetric cointegration and dynamic multipliers in a nonlinear ARDL framework. In Festschrift in honour of Peter Schmidt (pp. 281–314). Springer. ISBN : 978-1-4899-8007-6.

- Tang, J. (2015). Testing the pollution haven effect: Does the type of FDI matter? Environmental and Resource Economics, 60(4), 549–578. https://doi.org/10.1007/s10640-014-9779-7

- Tirgil, A., Acar, Y., & Özgür, Ö. (2021). Revisiting the environmental Kuznets curve: Evidence from Turkey. Environment, Development and Sustainability, 23, 1–20. https://doi.org/10.1007/s10668-021-01259-6

- Troster, V., Shahbaz, M., & Uddin, G. S. (2018). Renewable energy, oil prices, and economic activity: A Granger-causality in quantiles analysis. Energy Economics, 70, 440–452. https://doi.org/10.1016/j.eneco.2018.01.029

- Umar, Z., Gubareva, M., Tran, D. K., & Teplova, T. (2021). Impact of the Covid-19 induced panic on the Environmental, Social and Governance leaders equity volatility: A time-frequency analysis. Research in International Business and Finance, 58. https://doi.org/10.1016/j.ribaf.2021.101493

- Umar, Z., Trabelsi, N., & Zaremba, A. (2021a). Oil shocks and equity markets: The case of GCC and BRICS economies. Energy Economics, 96, 105155. https://doi.org/10.1016/j.eneco.2021.105155

- Umar, Z., Aharon, D. Y., Esparcia, C., & AlWahedi, W. (2022). Spillovers between sovereign yield curve components and oil price shocks. Energy Economics, 109, 105963. https://doi.org/10.1016/j.eneco.2022.105963

- US Energy Information Agency. (2018). US crude oil and natural gas proved reserves (EIA). Year-end 2016.

- Wong, S. L., Chia, W. M., & Chang, Y. (2013). Energy consumption and energy R&D in OECD: Perspectives from oil prices and economic growth. Energy Policy, 62, 1581–1590. https://doi.org/10.1016/j.enpol.2013.07.025

- Zarsky, L. (1999). Havens, halos and spaghetti: Untangling the evidence about foreign direct investment and the environment. Foreign Direct Investment and the Environment, 13(8), 47–74.

- Zeng, K., & Eastin, J. (2012). Do developing countries invest up? The environmental effects of foreign direct investment from less-developed countries. World Development, 40(11), 2221–2233. https://doi.org/10.1016/j.worlddev.2012.03.008

- Zhang, Y., & Zhang, S. (2018). The impacts of GDP, trade structure, exchange rate and FDI inflows on China’s carbon emissions. Energy Policy, 120, 347–353. https://doi.org/10.1016/j.enpol.2018.05.056