?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

The study aims to provide empirical evidence for a one-way relationship between corporate environmental responsibility (CER) and financial performance (FP) in the banking industry, with special consideration into the moderating role of legal regulations and ownership structures. Net interest margin (NIM), return on assets (ROA), return on equity (ROE) are selected to measure FP while the content analysis method is adopted to examine CER. The study used regression analysis with the two-step system generalised method of moments (Sys-GMM) on a sample of 29 Vietnamese commercial banks from 2012 to 2019, and the positive impacts of CER on banks’ FP were identified. Analysis of these data revealed that listed banks have a higher level of information disclosure than unlisted banks, but the positive relationship between CER and FP is weaker in listed banks. Similarly, while state-owned banks have a higher degree of disclosure than privately-controlled banks, the relationship between their CER and FP is weaker. The paper also provides some recommendations and suggests future research implications.

1. Introduction

Environmental issues have long been an ongoing concern at the national and individual levels. They are mainly driven by abnormal weather phenomena and lead negative natural consequences such as floods, droughts, and sea-level rise (Coulson & Monks, Citation1999). These alarming problems are reported to stem from many causes, and business operations are believed to have some long-term environmental impacts that may not be reversible (Worae & Ngwakwe, Citation2017). Therefore, businesses should realise the importance of acting in a socially and environmentally responsible manner, since going beyond environmental compliance will affect their bottom line and reputation in the long run.

CER or corporate social responsibility towards the environment is considered an integral part of corporate social responsibility (CSR) so that businesses can have sustainable development. According to Lee et al. (Citation2016), 93% of CEOs believe that climate change and sustainability are crucial to the success of their businesses. As a result, an increasing number of empirical studies are investigating why companies undertake environmental responsibility as well as make environmental disclosure, and how these activities are related to the FP of companies (Angelia & Suryaningsih, Citation2015; Dimitropoulos, Citation2021; Lee et al., Citation2016; Wu et al., Citation2020).

Banking is one industry type that needs to take environmental compliance into serious consideration. Although banks are often considered to be eco-friendly (Tran et al., Citation2016) and do not produce toxic chemicals or discharge pollutants into natural environment (Kennedy, Citation1999), they can also have indirect negative impacts by providing loans to companies or projects that cause significant damage to the environment (Zhang et al., Citation2011). On the other hand, environmental issues can affect the bank’s management strategies and day-to-day operations. When eco-unfriendly projects are restricted by environmental policies, banks will have to suffer (Yang, Citation1997). Therefore, it could be said that CER is an essential part of the CSR in the banking industry.

In fact, CER initially did not attract much attention from the banking industry (Yang, Citation1997). The development of CER is mainly due to the increasing pressure that companies face from many stakeholders to comply with legal regulations and community’s environmental concerns (Dimitropoulos, Citation2021). In 1980, the United States Comprehensive Environmental Response and Compensation Liability Act (CERCLA) required the US. banks to be responsible for environmental cleaning costs over asset-based lending. Hence, banks began to pay more attention to the potential regulatory risks associated with the environmental mandate of the loan borrowers such as the ecological impacts of bank credits, wealth management, investments, and insurance. Simultaneously, international organisations, especially the United Nations and the World Bank, have pushed banks in all countries to integrate sustainable development into their operations via their detailed framework and policies for environmental and social safeguard (Zhang et al., Citation2011).

As a developing country implementing a natural resource-driven model for economic growth, Vietnam is also facing environmental and social problems and this issue is becoming more and more serious. This urges the need to have more effective regulatory policies and environmental legislation to balance the bottom line of businesses with environmental responsibility. One example of the government’s endeavours is the National Green Growth Strategy for 2011–2020 with a vision for 2050 (Vietnamese Government, Citation2012), which aimed at building a low carbon economy by using use natural resources effectively with higher added values, reducing greenhouse gas emissions significantly, greening existing business sectors, responding to climate change efficiently, and creating a driving force from green industry for sustainable economic development. Such policies require changes i the banking industry to catch up with the green growth trend. For instance, on 24 March 2015, the State Bank of Vietnam (SVB) issued Directive No. 03/CT-NHNN to promote green credit growth and manage environmental and social risks in credit activities (SBV, Citation2015a). Then, on 30 December 2016, the SBV issued Circular No. 39/2016/TT-NHNN regulating lending activities of credit institutions and foreign bank branches. Accordingly, starting from 15 March 2017, the bank’s lending activities to customers ensure credit relations and comply with regulations on environmental protection (SBV, Citation2016). On 7 August 2018, the SBV signed Decision No. 1604/QD-NHNN approving the Green Bank Development Project in Vietnam (SBV, Citation2018).

In addition to the legal documents regulating business operations for better corporate environmental responsibility and sustainable economic development, statutory regulations have also been promulgated, requiring companies to publicise non-financial information. Directive 2014/95/EU issued by the EC in December 2014 is an example. Accordingly, large companies of public interest (e.g., listed companies, banks, insurance companies, and national authorities) are required to have their non-financial disclosures since 2018 (European Commission, Citation2014). This directive is highly appreciated because it derives from the European Parliament’s recognition of the critical role that non-financial disclosure plays in promoting CSR implementation and disclosure by European businesses. In Vietnam, the Circular 155/2015/TT-BTC of the Ministry of Finance took effect on 1 January 2016, requiring listed enterprises to disclose their non-financial information on environmental and social impacts (Ministry of Finance, Citation2015). In fact, these statutory regulations have created a legal framework for environmental compliance in the banking sector. However, more research is needed to clarify whether and to what extent such policies enable banks to develop effective environmental risk management systems and undertake environmentally responsible practice seriously. Moreover, the question of whether these regulations exert a moderating effect on the relationship between CER and FP of commercial banks should also be addressed.

Another noteworthy issue is that the Vietnamese economy is characterised by a large number of totally state-owned enterprises (with 100% of the charter capital held by the State) and joint-stock companies (with a State share capital ratio of 50% or more). The Vietnamese banking industry is of no exception with four state-owned commercial banks. As of 31 December 2019, the total assets of these four banks reached over VND 5.4 million (US$233.5 million), increasing nearly fourfold within ten years and accounting for over 50% of the total assets of the entire commercial banking system. The influence of these four banks on monetary policies, banking transactions, and other business activities is enormous. They can also undertake environmental responsibility and disclose information a required by the government. According to Wang et al. (Citation2014), decisions of state-controlled enterprises are usually made based on the Government’s objectives. Therefore, the impact of government control in regulating and moderating business activities of commercial banks should also be examined as far as the CER is concerned.

Empirical evidences of CER’s impact on FP in Vietnamese enterprises have been found in some empirical studies. Nguyen and Tran (Citation2019), for example, investigated the relationship between the level of environmental accounting information publication and FP of listed enterprises in Vietnam from 2013 to 2017. The results showed a close relationship between the level of ecological accounting information release and FP. Le et al. (Citation2019) determined factors impacting the application of environmental management accounting (EMA) and the relationship between EMA application and performance efficiency of 418 medium-sized building materials manufacturing enterprises in Vietnam between 2018 and 2019. These results confirm a significant positive relationship between environmental efficiency and FP, stating that innovative solutions to reduce ecological pollution can yield fruitful benefits to business activities.

However, there is a lack of empirical studies on CER and FP within the Vietnam’s banking industry. Therefore, raises several intriguing questions, such as (i) Which activities of commercial banks demonstrate their environmental responsibility? (ii) To what extent do Vietnamese commercial banks disclosure their CER information? (iii) Does the undertaking and disclosure of CER have positive impact on the financial performance of commercial banks? (iv) Can legal documents reinforce the positive influence of CER on the FP of commercial banks? (v) And will the ownership structure increase or weaken CER’s impact on FP in the state-owned commercial banks?

In short, this paper examines the extent to which Vietnamese commercial banks undertake environmental responsibility as well as disclose their information, and how the one-way impact of CER on FP exists. In addition, it also demonstrates the moderating effects of legal regulations and ownership structures on the relationship between CER and FP of commercial banks. Hence, the study could have significant contributions to the growing line of research literature in the banking and financial sector. First, this study provides empirical evidence on the interrelation between CER and FP. Second, this bridges the literature gap in examining the moderating impact of legal regulations and ownership structures in the Vietnamese context. Finally, as Vietnam is facing increasingly severe environmental problems, this study could inform policymakers on how to better implement more effective government-led initiatives so that an essential leverage for the transformation of corporate environmental responsibility could be constituted. To sum up, this study provides further empirical evidence of CER in one emerging economy where environmental protection and regulatory enforcements are much weaker than in developed countries.

2. Literature review and hypotheses

2.1. Corporate environmental responsibility and its impact on financial performance

In recent years, environmental performance and disclosure have become more critical in the business community. A greener and cleaner environment is a must for every business to survive in the context of sustainable development being promoted in each country. Since the main objective of a company is to maximize shareholder value; therefore, it is essential to know the additional value created for companies by conducting environmentally responsible activities. As a result, many studies have investigated the possible relationship between CER and FP, both theoretically and experimentally.

At the outset, neoclassical agency theory explains the negative relationship between CER and FP (Brouwers et al., Citation2014), stating that CER might not be compatible with the companies’ objective of profit maximization. According to Brouwers et al. (Citation2014), investments in the corporate environment will protect the company well from fines for environmental violations. Still, they are not enough to offset the investment costs the company has spent, which results in reduced profits, reduced business value, or further competitive disadvantage.

On the contrary, Stakeholder theory, Legitimacy theory, and Resource-based theory support the idea of CER’s positive impact on FP (Aggarwal, Citation2013; Brouwers et al., Citation2014). According to the Stakeholder theory, the social and environmental performance of a company aims to meet the demands of relevant stakeholders. If companies fail to meet these requirements, they will face many problematic issues, even serious boycotts or lawsuits. Thus, meeting stakeholders’ demands to some extent is considered an unavoidable cost in business. However, this can also lead to an improvement in the company’s reputation, prestige, and brand image, thereby positively affecting financial performance (Brouwers et al., Citation2014). According to Gangi et al. (Citation2019), the reputation of banks is even more important as it is the basis for building and maintaining customer trust. Banks with strongest reputations and recognition could have more chance to increase customer trust and loyalty as depositors tend to put money in more reputable banks. Besides, banks with high reputations also pay lower interest rates on deposits, thus potentially increasing margins. Brouwers et al. (Citation2014) also added that the resource-based perspective lays a strong foundation to explain the competitive advantage of a company. By taking the needs of their stakeholders into consideration, businesses gain a competitive advantage through the acquisition of additional benefits. In other words, this theory implies that environmental responsibility leads to competitive advantage and enhances corporate value. According to Legitimacy theory, companies need to meet social standards and expectations to ensure long-term survival. In other words, corporate social and environmentally responsible practices will reduce the risk of boycotts and lawsuits and strengthen the company’s license to operate (Aggarwal, Citation2013). Meanwhile, Gangi et al. (Citation2019) argue that banks with environmentally friendly activities and more sensitive customer support for the sake of community interests will gain more business advantage as the social legitimacy of banks supports their economic legitimacy. Besides, banks can inspire stakeholders and thus may get more interest from companies that want to be certified by the most reputable banks. This desirability can offer reputable banks the opportunity to increase market share and charge higher interest rates or commissions than less reputable banks. In short, greater attention to the environment represents the bank’s long-term profitability vision and higher service quality.

Brouwers et al. (Citation2014) also provide arguments to explain the third possible case in the relationship between CER and FP—the ambiguous relationship. Specifically, a company’s optimal level of investment in environmentally responsible activities can be assessed in the same way as any other investment by examining both the supply and demand sources. While companies that do not invest in CER will offer their products at a lower price, those who incur environmental costs will sell their products at a higher price. Therefore, the relationship between CER and FP is ambiguous.

Empirical studies also draw different conclusions about the impact of CER on FP. Most studies find a positive effect of CER on a firm’s FP. For example, Nehrt (Citation1996) investigated 50 pulp-producing companies in eight countries and argues that firms with early investment in pollution reduction technologies have a more significant financial advantage. He argues that such technologies can allow companies to reduce unit production costs and improve sales in the long run. Miles and Covin (Citation2000) examined more closely the relationship between environmental performance, corporate reputation and financial performance, and the results show that reputation is one of the most important intangible assets related to financial performance. Marketing, and financial performance of the business. They conclude that good environmental management provides companies with a reputational advantage and increased financial performance. López-Gamero et al. (Citation2009) argue that the time and intensity of early investment in environmental issues impact the application of environmental management, thereby helping to improve ecological activity. The impact of environmental protection on the financial performance of Spanish enterprises is not direct and may vary depending on the field considered but generally positive. A company’s resources and competitive advantages serve as intermediary variables for the relationship between environmental protection and financial efficiency.

Similarly, by investigating financial services firms from 29 countries, Jo et al. (Citation2015) concluded that by effective investment in CERs could reduce costs environment, thereby improving financial performance. In particular, reducing environmental costs increases financial performance in the long run because it could lead to improved corporate reputation, allowing companies to hire more qualified workers, improving production efficiency and competitiveness, reducing capital costs, and increasing profit opportunities. Lee et al. (Citation2016) studied how environmental responsibility impacted corporate financial performance, as measured by ROE and ROA. By using two different testing methods (OLS and 2SLS) on Korean companies between 2011–2012, the results showed that the relationship between CER and FP was positive and statistically significant. Environmental performance conclusions that substantially affect ROA and ROE are also found in the study of Angelia and Suryaningsih (Citation2015). Recently, Shabbir and Wisdom (Citation2020) conducted a study with Nigerian manufacturing companies to examine how investments in the internal environment and investments in the external environment affect the financial performance of the company. The results show that a positive and significant relationship exists between investments in the internal environment and the financial performance of the company. A positive but insignificant relationship was also found between investments in the external environment and corporate financial performance. Specifically, companies with higher environmental investment have higher returns than companies that are not environmentally conscious. Dimitropoulos (Citation2021) investigated the performance of 7313 corporations in 24 European countries between 2003 and 2018. The experimental analysis results showed that CER created better competitive resources and improved financial efficiency. Similarly, the empirical study of Xu et al. (Citation2021) with a sample of 141 global construction companies showed that CER increased return on equity (ROE) and economic value added (EVA) of companies. Iwata and Okada (Citation2011) draw a mixed conclusion about the impact of environmental activities on FP by using data of Japanese manufacturing firms from 2004 to 2008. Overall, the effect of waste emissions on FP is positive. However, waste emissions have adverse effects on dirty industries as a reduction in greenhouse gas could increase ROE (reflecting long-term financial performance) but has no significant effect on ROS (representing short-term financial performance).

In another geographical context, Nyirenda et al. (Citation2013) did not find a significant relationship between environmental management practices and FP among mining companies in South Africa. Companies’ environmental management practices are primarily driven by a desire to comply with legal regulations and ethical obligations to mitigate the effects of climate change. Similarly, Pintea et al. (Citation2014) also found no significant link between Romanian firms’ corporate environmental performance and financial performance.

Mixed results about the effect of CER on a firm’s FP can also found in the systematic review of Dang (Citation2017), who examined 72 empirical studies. The results showed that 41 studies found a positive effect, 19 studies found a neutral relationship, and 12 studies found a negative impact of CER on a firm’s FP. Although the number of these publications indicates that there are more positive than negative findings, such mixed results prove that additional research is needed to define the actual impact of CER on a firm’s FP, especially in an emerging country like Vietnam.

In conclusion, a review of literature proves that more research is needed to examine the impacts of CER on FP in business. Moreover, in-depth investigations are also needed to know how such relationship actually exists in specific contextual business environments such as Vietnam. Therefore, this study is conducted to examine the impact of CER implementation and disclosure on the FP of Vietnamese commercial banks via NIM, ROA, and ROE; thus, contributing to the growing line of research literature in the field.

In Vietnam, the results of studies conducted with the research sample are enterprises (Huynh, Citation2019; Le et al., Citation2019; Nguyen & Tran, Citation2019) or commercial banks (Tran, Citation2016) draw conclusions about the positive impact of CER on FP. This study is different from a previous study conducted with Vietnamese commercial banks in terms of CER measurement method, FP representative variables, research model, and estimation method. It main research objective is to verify the positive impact of CER on FP of banks. Another reason is that the underlying theories used to explain the positive impact of CER on FP in this study are the Stakeholder theory and the Legitimacy theory which are normally used for developed countries. Therefore, this study is of considerable importance to test the relevance of the above theories in developing economies. As a result, the paper develops hypothesis H1 as follows:

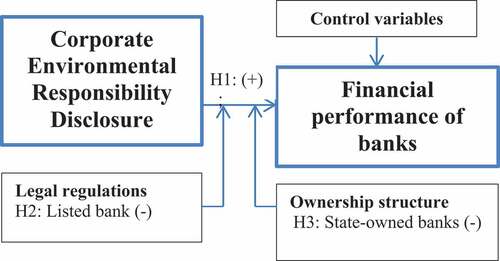

H1: There is a positive impact of the implementation and disclosure of CER on the FP of Vietnamese commercial banks.

2.2. Moderating effect of legal regulation

Businesses in different economic and political-institutional environments operate differently to achieve their business objectives. Institutionalists argue that institutions outside the market are necessary to ensure that firms will seriously take into account stakeholders’ benefits and demands (D. Li et al., Citation2017). One of the common institutions affecting businesses in emerging economies as Vietnam is the law or legal system, and legal pressure exerts a strong influence on the behaviors of firms. In a clearer sense, regulatory agencies develop rules, regulations, and ordinances to monitor corporate environmental behaviors. Strict ecological regulations can force businesses to take responsible initiatives such as actively participating in environmental activities or investing in environmentally-friendly projects. Rules for companies listed on the stock market are even stricter. According to Q. Li et al. (Citation2013), listed companies need to adhere to the pre-defined values or beliefs set by the society and the system of norms to achieve legitimacy on the stock market. Listed enterprises are obliged to provide CSR information, while unlisted enterprises have no such obligation. However, unlisted companies normally implement and disclose CSR information to achieve financial goals. They are more interested in cost-benefit analysis than in institutional pressure. In other words, listed companies can conduct and disclose more CSR information, but the positive association of CSR-FP in listed companies will be weaker than in unlisted companies.

To implement the green growth strategy of the economy, the Government of Vietnam and SBV have issued stricter regulations on the environmental issues. Listed banks are obliged to carry out environmentally responsible activities according to institutional requirements and publish such information in the media. Therefore, there is a difference in the level of CER disclosure between the listed banks and the unlisted ones.

From the above arguments, we propose the following hypotheses:

H2: The positive relationship between CER and FP in listed banks is weaker than in unlisted banks.

2.3. Moderating effect of ownership structures

According to Ali et al. (Citation2019), an ownership structure affects the relationship between the stakeholders of a company. The most potent stakeholder (e.g., the Government) facilitates state-owned enterprises (SOEs) in financial difficulty because of CSR involvement. Therefore, CSR will have a positive impact on the financial performance of these businesses. However, Q. Li et al. (Citation2013) found that the relationship between CSR and FP in state-owned enterprises is weaker than in private enterprises and pointed out some reasons for this difference: (1) The goals of state-owned enterprises include social objectives as well as economic goals; (2), SOEs need to legitimize their position and implement CSR no matter how profitable they are; (3) Government agencies regularly evaluate executives of SOEs, and their promotion level depends on the assessment results in which social orientation is one category to consider. In contrast, non-state-controlled enterprises are not subject to government constraint. They generally implement and disclose CSR information due to the tangible and intangible benefits that CSR offers. Such benefits include attracting new talents and retaining efficient employees, increasing opportunities to penetrate into new markets, enhancing employees’ loyalty and risk management; attracting new investors and customers, fostering labor productivity, preventing legal violations, enhancing the quality of products and services, promoting brand value or corporate reputation, and improve FP (Bui & Huynh, Citation2020).

Liu et al. (Citation2021) argue that state-owned enterprises are closely linked with central and local governments, taking on more social responsibility in environmental and ecological protection, thus they invest more in environmental protection than non-state enterprises. Public companies can acquire significant positive feedback by taking on environmental responsibilities; however, in the current market environment, state-owned companies with more environmental responsibilities will not receive additional compensation. As a result, the financial performance of state-owned companies could not be supported much by these environmental and ecological activities. In contrast, non-state-owned companies can send positive signals to the market through their environmentally responsible practices and receive significantly positive feedback on the company’s financial performance. Similar conclusions are also drawn by Ang et al. (Citation2022), who investigated 6306 Chinese heavily polluting listed companies from 2012 to 2019, the regression results show that CSR promotes CFP in non-state enterprises better than in state-owned enterprises.

In the 90s of the twentieth century, Vietnam’s commercial banking system had only nine banks, including four state-owned commercial banks. However, after the State Council passed two Ordinances on Banking in May 1990, the banking system began a dramatic transformation. By 1996, Vietnamese banks had increased to 76 (including four state-owned commercial banks, 48 private commercial banks, and the rest were joint venture banks and foreign bank branches). Right from the early 2000s, the Government of Vietnam planned to equitize state-owned commercial banks to bring the banking and finance sector to par with other countries in the region. As a result, three state-owned commercial banks were equitized. However, the State still maintains enough shares to retain voting control and political influence over these banks. The Board members and executives of State-owned commercial banks tend to make decisions on behalf of the government’s interests such as social benefits and economic benefits. From the above arguments, we hypothesize:

H3: The positive relationship between CER and FP is weaker in state-owned commercial banks than in private commercial banks.

Combining the assumptions presented above, a theoretical model for the conduct of this research is established as follows:

Figure 1. Research framework.

3. Research design

3.1. Samples and data sources

The research population for this research includes 35 banks Vietnamese commercial banks (excluding Joint venture Banks and Banks with 100% foreign capital). Annual reports and financial statements of banks used for analysis. As a result, there are 29 fully publicized banks in the period 2012–2019. Therefore, the final study sample is 29 banks, and the number of observations is 232.

The data sources of this study includes (i) CERs of commercial banks collected from the content analysis method; and (ii) FP or control variables collected from financial statements of commercial banks and annual reports of SBV.

3.2. Variable measurement

3.2.1. Dependent variable: Financial Performance (FP)

ROA and ROE are the basic profitability metrics used to measure a bank’s FP (Esteban-Sanchez et al., Citation2017; Fijałkowska et al., Citation2018; Wu & Shen, Citation2013). In addition, this study also uses NIM to measure a bank’s FP because it is one of the primary metrics of bank profitability (Matuszaka & Różańskaa, Citation2019), and high profits will assist banks in preserving capital, increase market share, and attract investments. So, this type of revenue influences net income and capital—the factors that decide banks’ financial success. The higher the NIM is, the more the bank’s profitability and the more stable the bank’s operations are (Matuszaka & Różańskaa, Citation2017). NIM has been used as the dependent variable to measure FP in many studies on CSR and the financial performance of the banking industry (Gonenc & Scholtens, Citation2019; Hafez, Citation2015; Matuszaka & Różańskaa, Citation2019). However, in Vietnam, using NIM to assess the FP of commercial banks has not been found.

3.2.2. Explanatory variable: corporate environmental responsibility (CER)

Most empirical research on CER obtained data from Kinder, Lydenberg, Domini Research & Analytics (KLD) database. Other databases frequently employed to measure CER are TRI (Toxic Release Inventory), the Business Ethics “100 Best Corporate Citizens”, and CEP (Council on Economic Priorities; D. Li et al., Citation2017). However, these databases only include companies in developed countries. Almost no Vietnamese companies are ranked by independent rating agencies (Luu, Citation2019). As an alternative, scholars have applied content analysis to measure CER by collecting environmental information published in commercial bank annual reports.

To measure CER by content analysis method, a table of criteria (question items) is needed. There have been many regulations and guidelines on CSR disclosure, including content related to information disclosure on the environment. Therefore, in this study, the criteria to measure the bank’s CER are designed based on Circular 155/2015/TT-BTC, GRI Standards, Corporate Sustainability Index set (CSI), and previous studies (Szegedi et al., Citation2020). The reason is that Vietnamese commercial banks prepare and publish sustainability reports following the provisions of Circular 155/2015/TT-BTC, so the CER measurement criteria have to stick to these categories. Furthermore, GRI is not only applied by enterprises to prepare sustainability reports to integrate with the international community but is also used by scholars to design CSR metrics (Matuszaka & Różańskaa, Citation2017; Taşkın, Citation2015). CSI is a guide for businesses to implement and disclose CSR information. CSI has been updated with many new points to match the requirements of the Free Trade Agreements that Vietnam has signed. In particular, issues related to the seventeen sustainable development goals and the national action plan for implementing the 2030 Agenda for Sustainable Development have been integrated into CSI 2020. In addition, the CSI also launched a program to evaluate, rank, and announce sustainable businesses for their endeavours to protect environment. Many Vietnamese enterprises consider that being listed in this annual report of “sustainable enterprises” by CSI is a proud title as it represents the recognition of the Government, the business community, and the whole Vietnamese society (VBCSD, Citation2020).

Besides, specific regulations and guidelines for the banking industry have also been issued to guide Vietnamese banks in undertaking CSR and disclosing. The most important legal document is the Decision No. 1604/QD-NHNN approving the Green Bank Development Project in Vietnam, which is a guiding document for environmentally responsible activities of commercial banks. For example, this document provides some guidance for commercial banks to gradually transform internal governance processes, modernize infrastructure and information technology, and minimize negative impacts on the environment. Provide credit and payment services in environmentally friendly areas. Proactively develop internal guidelines on green working environment towards implementing measures to save water, printing paper, electricity, fuel, etc. Besides, banks need to combine environmental risk assessment as part of the bank’s credit risk assessment. They also develop green credit policies, organize training courses to raise awareness for employees about sustainable development, organize events and propagate to guests about green banking products and services, introduce products that are friendly or do not adversely affect the environment, etc.

Referring to the above regulations and guidelines, a list of CER measurement indexes for banking activities were designed in this study. Then, a pilot study was carried out in May, 2020 and the questionnaire items were assessed by two experienced executives and one Vietnamese linguist to examine the relevance of the contents of the indexes with the environmental disclosure practice in the annual reports of commercial banks. Afterwards, the content of this list is modified and displayed in .

Table 1. CER grading form for bank

Information about each bank corresponding to a year was collected and marked on a “CER grading form”. Data in the “Proofs” column included words, phrases, sentences, paragraphs, figures, and images related to each criterion. The proofs were collected and processed in either two ways:

using the Microsoft Edge software to copy relevant information in the PDF files and paste it into the form, or

using the Snipping Tool software to save images of related contents in the uncopiable files and paste them into the form

Then, marks were given to each criterion: 1 for criterion with relevant proof(s), and 0 for criterion without any CER evidence.

3.2.3. Moderating variables

3.2.3.1. Legal regulations

In this study, the dummy variable Listed Bank (DLB) was used to represent the legal regulations. The banks in this study were divided into two groups: listed and unlisted ones. The listed group consists of seventeen banks, fifteen of which are listed on the Ho Chi Minh City Stock Exchange and two listed on the Hanoi Stock Exchange. The remaining banks belong to the unlisted group, including a 100% state-owned commercial bank (Agribank) and eleven joint stock commercial banks. Shares of these banks are traded on UpCom (Unlisted public company market) or OTC (Over the counter market). Listed banks were marked “1” and unlisted banks got “0” for indexing.

4. Ownership structure

The state-controlled bank dummy variable (DSOB) is included in the model to test the regulatory impact of ownership structure on commercial banks’ relationship between CER and FP. A commercial bank controlled by the State is a commercial bank established with 100% capital from the state budget or a joint-stock commercial bank with a State share rate greater than 50%. Four state-controlled banks (Agribank, BID, CTG, VCB) will receive the value “1”. In contrast, a privately controlled bank is a type of commercial bank established in a joint-stock company in which businesses, organizations, and individuals contribute capital. This group will receive the value “0”.

4.1. Estimated model

To test hypotheses H1, H3 and H5, we use the following formulas, respectively:

Specifically, the variables in the model are described and have specific formulas in .

Table 2. Description of variables and symbols in the models

4.2. Estimation method

The variables in this study were collected from 2012 to 2019, which are continuous variables. In the analysis of continuous variables, most statistical tests can only be performed with normally distributed variables. Therefore, it is necessary to determine whether a variable is normally distributed or not before conducting tests. Therefore, first, the study will test the normal distribution of the variables in the model. Next, the study examines the model’s defects, such as multicollinearity, autocorrelation, heteroscedasticity, and endogenous variables. The GMM method is proposed to be used as a tool to overcome the model’s defects with panel data. The GMM test results are similar to the Pooled OLS test results if the model is not endogenous, heteroscedasticity, and autocorrelation. When the model has an endogenous phenomenon but does not have heteroscedasticity and autocorrelation, the GMM test results are similar to the 2SLS test results. On the contrary, when the model does not suffer from endogenous phenomena but has heteroscedasticity or autocorrelation, the GMM test results are similar to the GLS test results (Le, Citation2016).

The GMM method has two alternative estimators, Dif-GMM and Sys-GMM. This study chose to use Sys-GMM because it has been improved based on the Dif-GMM version to give a better estimate. The two-step estimator was also chosen because it is more efficient than the single-step version, especially for the Sys-GMM estimator (Huynh et al., Citation2021).

Before discussing the estimation results, the study was conducted to test the suitability of the regression using the Sys-GMM method. F test to check the statistical significance of the estimated coefficients. If P.value < 1%, the estimated coefficients are statistically significant. AR test to determine whether there is a correlation in the model residuals. If the AR (2) test has a P.value > 10%, it means that the model has no quadratic autocorrelation. Sargan test to check for excessive constraints, the reasonableness of the representative variables. If P.value > 10%, the model is correct, the variables are reasonably representative. Hansen test to check the validity of the instrumental variable. If the P.value is greater than 10%, it is reasonable to say that the selected variables as instrumental variables are appropriate. Finally, when the number of instruments is less than or equal to the number of groups, it is concluded that the instrumental variables are not weak.

5. Results and discussion

5.1. Level of CER disclosure

provides the level of CER disclosure among Vietnamese commercial banks during the period of 2012–2019. Data revealed that a constant upward trend could be identified from 2013 to 2019, showing that Vietnamese commercial banks were aware of the importance of undertaking CER and disclosing information to stakeholders. More important, there is a significant increase in the implementation and disclosure of environmental-related information from 2016 onward. The level of environmental disclosure of commercial banks in the period 2012–2015 was only about 21%, but in the period 2016–2019, it doubled at an average of about 39%. The reason is that SBV has issued many legal documents related to the environment in banking activities. In addition, the Circular 155/2015/TT-BTC taking effect on 1 January 2016 required that enterprises listed on the stock market must disclose information on sustainable development related to the environment and society (Ministry of Finance, Citation2015). This is an important milestone marking that CER activities have been regulated by Vietnamese law, and the implementation of CER has been compulsory and consistent rather than at the discretion and preference of each bank. Specifically, each listed company is required to either issue a separate sustainability report or integrate this information into their annual reports including Management of raw materials; Energy consumption; Water consumption; and Environmental legal compliance. Moreover, listed banks also have to report on green capital market activities such as green credit policies or the management of environmental and social risks in credit extension activities.

Table 3. Level of CER disclosure among Vietnamese commercial banks from 2012 to 2019 Unit: %

The data in also show that state-controlled commercial banks have higher levels of environmental disclosure than privately-controlled banks since they are always at the forefront of the development strategies of the Vietnamese banking industry. As a result, building a green working environment and implementing environmental protection activities towards sustainable development is of no exception. Listed banks thus have a higher level of CER disclosure than unlisted banks and are bound by legal regulations on non-financial information provision such as CER disclosure.

It could be said that the two criteria with the highest information disclosure level are Env 3 and 4, including Deploy the electronic office systems; Application of technology in internal operations of the bank (Env 3), and Transform business activities into a digital banking model related to customer service products (Env 4). One reason for this result is because these activities could help the bank save resources, reduce costs, and protect the environment. Besides, when automation in internal operations is promoted, the bank could save more time for processing and operating costs, thereby increasing operational efficiency and reducing risks. Finally, when internet banking, mobile banking, and digital bank cards are widely used, this could significantly reduce the use of natural and human resources (e.g., paper, time, delivery) within the bank’s operations. Therefore, Vietnamese banks deploy e-banking operations to diversify products, support other financial products (capital mobilization, lending, etc.), and increase revenue. However, it is also worth noting that the disclosure level of Env 4 is only about 64% (2012–2015) or 80% (2016–2019) because some commercial banks do not publish this information in their annual reports. Those are commercial banks that have not been listed on the stock exchange, so they are not required to provide non-financial information following Vietnamese law.

The criteria with the third-highest information disclosure rate is Env 9, averaging 42.4%/year over the entire study period. Env 9 is a unique indicator because a few banks, mainly unlisted banks, in addition to Env 3 and 4, only announced this indicator with a short sentence, “Compliance with regulations and laws on environmental protection.” In contrast, listed banks, especially state-controlled banks and those that prepare reports under the GRI guidelines, have detailed environmental content. In that case, environmental protection activities outside the bank will be searched and assigned to this indicator, such as beach cleanup, forestation, or public toilet projects, etc.

Results also reveals that very few commercial banks managing environmental and social risks in credit granting (Env 6). In 2012, there was only Sacombank, and in 2013 SHB was added. The number of banks applying environmental and social risk management has gradually increased over time, especially after 2016 when Directive No. 03/CT-NHNN was issued. By 2019, eleven commercial banks apply environmental and social risk assessment into their credit process, including ABB, Agribank, BID, EIB, HDB, MBB, PGB, STB, SHB, VCB, and VPB. These banks (except EIB), together with BAB, MSB, and CTG, also adopt green credit policies by sponsoring environmentally friendly projects (Env 5). Furthermore, it could be seen that the number of commercial banks building an environmentally-friendly workplace (Env 1) or implementing policies to save energy and reduce greenhouse gas emissions (Env 2) has continuously increased during the period of 2012–2019, although this number is not really high. In addition, the environmental responsibility of commercial banks is also reflected in their schemes to provide training to employees (Env 7) or the community (Env 8) to raise more awareness about environmental protection. Finally, the last criteria showing the recognition of the community on the environmental responsibility of commercial banks (Env 10) got the lowest figure at 6.3% from 2012 to 2019. This means very few banks receive prizes related to environmental protection. In 2012 it was 0%, but in 2019 it was 14.3%, there has been a major improvement.

Table 4. Level of CER disclosure based on criteria Unit: %

5.2. Descriptive statistics of research samples

describes statistics based on a sample of 29 commercial banks; the study period is from 2012 to 2019. The maximum value of NIM is 0.09325, the minimum value is 0.00549, and the mean value is 0.02996. There is a significant difference in financial performance among banks in the sample. Similar results are seen when observing ROA and ROE. The average ROE of Vietnamese banks is 0.08537. The lowest ROE was only 0.00062 belonging to National Joint Stock Commercial Bank in 2012. In contrast, the highest was Asian Joint Stock Commercial Bank in 2018 (0.2773).

Table 5. Statistics of variables used in research model

The average CER score of Vietnamese commercial banks is 0.2961. The lowest score is 0, and the highest is 1. Thus, there are commercial banks that do not publish any information related to the environment. In contrast, there are commercial banks that fully implement and provide all ten information indexes.

The commercial bank with the most significant total assets is BID in 2019; the lowest is Baovietbank in 2012. The loan-to-deposit ratio of Vietnamese commercial banks is nearly 0.79, of which the bank has the lowest percentage of only nearly 0.43, and the bank with the highest ratio reached 1.12. The average ratio of equity to total assets of Vietnamese banks is about 9%. At the same time, there is a massive difference in the maximum value (29.3%) and the minimum value (3.89%). Management quality of commercial banks is shown by the ratio of operating expenses to total income. The lower this ratio, the better the quality of management. The average CIR of Vietnamese banks is 55.6%. The bank with the lowest CIR is only 28.7%, while the highest is up to 129.2%.

Regarding market concentration, the average HHI index of Vietnamese commercial banks is 0.05, indicating a high level of competition in the banking industry. Vietnam’s gross domestic product (GDP) growth rate is relatively high, averaging 6.3% in the period 2012–2019. However, accompanied by a high GDP growth rate is a high inflation rate (INF), averaging 3.8%.

5.3. Regression testing

shows the histogram plots of variables in the research model. It can be seen that the variables in the model have a standard distribution, thus further investigation could be performed.

Figure 2. Histogram plots of variables.

presents the correlation matrix of the variables, revealing that these variables are not highly correlated with each other. In addition, the values of the variance inflation factor (VIF) were below 5, implying that the multicollinearity conclusion was small and did not affect the regression results.

Table 6. Variable correlation matrix and results of multi-collinearity test using VIF

Since the Prob is less than 0.05 in the Wooldridge test from , it can be concluded that the regression model has an autocorrelation phenomenon.

Table 7. Autocorrelation test results

shows that the test has Prob <0.05, implying that all estimation methods (Pooled OLS, FEM, REM) detect the presence of heteroscedasticity.

Table 8. Heteroscedasticity test results

In addition, several studies showed a bidirectional relationship between FP and CER. For example, Worae and Ngwakwe (Citation2017) found a two-way causal relationship between emissions intensity and the market value of declining equity with revenue. The experimental results of Dimitropoulos (Citation2021) also confirm the bidirectional association between CER and CFP. In particular, companies with high profitability are associated with higher environmental performance due to an enhanced ability to finance such activities. In return, higher CER performance contributes to FP enhancement.

In summary, the research model detects the presence of such defects as autocorrelation, heteroscedasticity, and endogenous variables.

5.4. Hypothesis testing

5.4.1. Hypothesis H1

presents the regression results of how CER impacted the FP of Vietnamese commercial banks. The three models have three corresponding dependent variables including NIM, ROA, and ROE respectively. The results show that the F-test results in three models have a low P.value (< 1%), indicating the model’s suitability. The AR (2) test has a P.value of more than 10%, which means that the model has no second-order correlation. The Sargan test results show that the model is correct and the variables are reasonably represented. The P.values of the Hansen test of all three models are greater than 10%, indicating that the variables selected as instrumental variables are reasonable. Finally, the number of instruments in three models is less than or equal to the number of groups, so it means that the instrumental variables are not weak.

Table 9. Estimation results of the impacts of CER on FP

The estimated results show a statistically significant relationship between the environmental responsibility index and the FP, which is consistent with previous empirical studies (Angelia & Suryaningsih, Citation2015; Ashraf et al., Citation2017; Buallay, Citation2019; Dimitropoulos, Citation2021; Lee et al., Citation2016). However, this study contrast with the result of Gonenc and Scholtens (Citation2019), who claims that environmental responsibility significantly reduces NIM, or in other words environmental performance reduces the efficiency of banks.

These experimental results prove that the hypothesis H1 is accepted, which means that environmentally responsible implementation and disclosure will improve banks’ FP. The bank’s environmental responsibility is reflected in its carbon reduction activities both inside and outside the bank. Activities conducted inside the bank include online banking, ATM system transactions, card services, or digital information exchanges can minimize the use of stationery products which are environmentally unfriendly when they are disposed. Vietnamese banks are also encouraged to build an eco-friendly working environment such as setting the thermostats at the reasonable temperature to balance comfort and cost savings, using appropriate office lighting, turning off lights when not in use, or checking water equipment regularly to detect damage or leakage. In addition, commercial banks have promoted the implementation of a special program to raise more awareness of banking employees to use things economically and create a green working environment. In terms of activities to reduce carbon dioxide emissions outside the bank’s boundary, green credit policies and environmental-social risk management in credit granting activities are implemented. All of these activities cannot only bring about improved environmental effects but also result in better financial performance because they help commercial banks to reduce costs, increase employee productivity, concentrate on better loan screening and monitoring standards, limit risks, and improve the quality of credit activities. As a result, banks with better environmentally responsible implementation and disclosure will have better financial performance.

5.4.2. Hypothesis H2

This subsection continues to assess the moderating impacts of legal regulations on Vietnamese banks’ relationship between CER and FP. presents the estimation results of three models corresponding to three dependent variables, including NIM, ROA, ROE respectively. Overall, the tests for the robustness of the GMM regression in all three models show that the model has no second-order autocorrelation, the selected variables as instrumental variables are reasonable, the number of tools is less than or equal to the number of groups indicated, and the instrumental variables are not weak.

Table 10. Estimation results of the effect of CER on FP when considering the moderating effect of legal regulations

The estimation results show that no statistically significant relationship could be found between the independent variable (CER), the interactive variable (CERxDLB), and the dependent variable (represented by NIM and ROA) because the P.values all larger than 0.1. However, in the model with ROE as the dependent variable, the regression results show that the CER variable positively affects FP at the 1% significance level, and the CERxDLB variable has a negative effect on FP at the 5% significance level. This result indicates that CER increases the bank’s FP, namely the return on equity; however, listed banks have a lower increase in financial efficiency than unlisted banks. Such a result is consistent with the conclusion of Ali et al. (Citation2019), who examined the moderating role of listed and unlisted companies on the relationship between CSR and FP of Chinese companies. Their empirical results confirm a more robust connection in unlisted firms.

Furthermore, results from can be combined with results on the CER disclosure in Table to state that the hypotheses H2 are accepted. This means listed banks have a higher level of CER disclosure than unlisted banks. However, the positive relationship between CER and FP in listed banks is weaker than in unlisted banks. This is attributed to the fact that listed banks are obliged to undertake CER and disclose information as required by Vietnamese legal regulations while unlisted banks carry out CER activities entirely voluntarily. In addition, the CER disclosure of listed banks are higher than unlisted ones because these listed entities want to create better brand image and improve their reputation on the stock market. Meanwhile, unlisted banks are not legally bound on providing non-financial information such as CER disclosure. They can also any undertake environmentally responsible and socially responsible activities to achieve financial targets. Thus, they are more interested in cost-benefit analysis. In short, it can be concluded that the positive relationship between CER and FP in unlisted banks is more robust than in listed banks.

5.4.3. Hypothesis H3

presents the estimation results of ownership structures on the impact of CER on FP of Vietnamese commercial banks. The F, AR(2), Sargan, Hansen tests show that the regression coefficients of the independent variables are statistically significant, efficient, and unbiased. In all three models, the number of instruments is less than or equal to the number of groups, indicating that the instrumental variables are not weak. For the regression model with dependent variables ROA and ROE, no statistical significance of the variable CERxDSOB could be found. However, the NIM model reveals that the regression coefficient of the CER variable has a positive impact at the 5% level of significance, while the CERxDSOB variable has a negative regression coefficient with a statistical significance of 1%. These results, therefore, confirm that the hypothesis H5 is accepted. This means that environmental responsibility can increase the bank’s financial performance by increasing the net interest margin. However, state-controlled banks have lower levels of economic efficiency gains than private banks. In other words, the positive relationship between CER and FP is weaker in state-controlled banks than in private banks.

Table 11. Estimation results of ownership structures on the impact of CER on FP

Results from this study are consistent with data from the study of Ali et al. (Citation2019), who found that the relationship between FP and CSR disclosure in Chinese state-owned SOEs is weaker than in private enterprises. This group of researchers argue that Chinese SOEs are required to engage in CSR activities under the government’s supervision while private enterprises can freely choose their own CSR strategies based on cost-benefit analysis.

As CER is a component of CSR, so the evidence and conclusions drawn from the relationship between CSR and FP are entirely compatible with the CER-FP relationship. Thus, it can be concluded that private commercial banks can enjoy more financial benefits than state-owned banks because the undertaking of CER within private banks is totally a voluntary activity and based on an analysis of benefits and costs. Meanwhile, the implementation of CER by state-owned commercial banks is compulsory under the strict guidance and supervision of the government. State-managed banks need to take the lead in the development strategies of the banking industry. Developing green banking is one of the important strategies to increase awareness and social responsibility of the banking system for environmental protection, actively contributing to promoting green growth and sustainable development. Therefore, commercial banks controlled by the State encourage the implementation and disclosure of environmentally responsible activities to orient, lead, and model the whole Vietnamese banking system. Together with the data in , these arguments are the rationale for the conclusion that state-owned commercial banks have a higher level of environmental disclosure than private commercial banks; however, the positive relationship between CER and FP in state-owned commercial banks is weaker.

6. Conclusion

This study examines how CER impacted the FP of commercial banks under the adjustments of legal regulations within various ownership structures. Using a sample of 29 Vietnamese commercial banks during the period 2012–2019 and a two-step systematic GMM estimator in a dynamic panel model, the study reveals the relationship between CER and FP and how NIM, ROA, and ROE are impacted within the financial performance of Vietnamese commercial banks. CER is measured by the content analysis method, the dummy variables of listed banks are included in the model to illustrate the regulatory impacts, and the list of state-controlled and non-state-controlled banks represents the moderating variables of ownership structure. After testing the defects of the models, the study shows that there is an autocorrelation, heteroscedasticity, and the existence of endogenous variables. Therefore, the regression analysis was chosen according to the Sys-GMM method. Results from the goodness of fit test shows that the regression coefficients of the independent variables are statistically significant, efficient, and unbiased.

Analysis of the CER disclosure among Vietnamese commercial banks reveals that there has been a significant increase in the level of environmental information disclosure, especially after the provisions of the law have been passed. Listed commercial banks have a higher level of environmental disclosure than unlisted commercial banks, and higher levels in state-owned banks can also be witnessed when comparing them with private banks. These results indicate a positive effect of CER on FP represented by NIM and ROE; therefore, it can be concluded that undertaking and disclosing CER could allow Vietnamese commercial banks improve their financial performance. Moreover, the regression coefficients of the interaction variable prove that the positive relationship between CER and FP in state-controlled commercial banks is weaker than in private commercial banks. Similar conclusion was also found when listed and unlisted banks are examined.

Several implications could be drawn upon the conduct of this study. First, the research results confirm that commercial banks can simultaneously achieve both environmental performance and financial performance. Therefore, Vietnamese banks need to pay more attention to environmental protection while still ensuring economic development. Second, they should also take more initiatives for environmental responsibility and improve their social and environmental risk management system in credit activities. Third, environmentally responsible activities have helped commercial banks reduce costs and increase operational efficiency, but normally these costs have not been recorded in their financial documents. Therefore, a specialized department should be established to take charge of environmental and social risk management, monitor green banking services as well as green credit activities, and carry out environmental accounting. Besides, The National Assembly of Vietnam and SVB should further improve environmental legislation, strengthen government supervision, and urge commercial banks to undertake more CER. Finally, Vietnamese policymakers should look beyond the rigor of environmental rules and pay more attention to enacting effective environmental policies.

There are several limitations encountered throughout this empirical research. First, the study has not exploited all variables that can be used to represent a bank’s financial performance, such as the variables representing accounting profits or market returns. Therefore, future studies can use a combination of these variables to represent the FP of Vietnamese commercial banks (e.g., Tobin’s Q). Second, the study only measures the level of environmental responsibility disclosure. Therefore, further studies are needed to describe the quality of CER disclosure such as publication location and disclosed contents. These two factors should be used interactively to shed light on how the quality of the company’s environmental responsibility is (Liu et al., Citation2021). Third, because of budgetary and time constraints, the research was limited to the use of regression model and the two-step systematic GMM estimator, while other methods can also be used to measure the FP of Vietnamese commercial banks. Finally, the study has not taken into account the bank size. As a result, further research is needed to explore the relationship between CER and FP when the impacts of bank size are considered.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

References

- Aggarwal, P. (2013). Relationship between environmental responsibility and financial performance of firm: A literature review. IOSR Journal of Business and Management, 13(1), 13–28. https://doi.org/10.9790/487X-1311322

- Ali, S., Zhang, J., Usman, M., Khan, F. U., Ikram, A., & Anwar, B. (2019). Sub-national institutional contingencies and corporate social responsibility performance: Evidence from China. Sustainability, 11(19), 5478. https://doi.org/10.3390/su11195478

- Ang, R., Shao, Z., Liu, C., Yang, C., & Zheng, Q. (2022). The relationship between CSR and financial performance and the moderating effect of ownership structure: Evidence from Chinese heavily polluting listed enterprises. Sustainable Production and Consumption, 30, 117–129. https://doi.org/10.1016/j.spc.2021.11.030

- Angelia, D., & Suryaningsih, R. (2015). The effect of environmental performance and corporate social responsibility disclosure towards financial performance (Case study to manufacture, infrastructure, and service companies that listed at Indonesia stock exchange). Procedia-Social and Behavioral Sciences, 211, 348–355. https://doi.org/10.1016/j.sbspro.2015.11.045

- Ashraf, M., Khan, B., & Tariq, R. (2017). Corporate social responsibility impact on financial performance of bank’s: Evidence from Asian countries. International Journal of Academic Research in Business and Social Sciences, 7(4), 618–632. https://doi.org/10.6007/ijarbss/v7-i4/2837

- Brouwers, R., Schoubben, F., Van Hulle, C., & Van Uytbergen, S. (2014). The link between corporate environmental performance and corporate value: A literature review. Review of Business and Economic Literature, 58(4), 343–374. https://feb.kuleuven.be/drc/AFI/research/AFIInsuranceFolder/InsurancePapers/rebel-2013-4-proef1bis.pdf#page=59

- Buallay, A. (2019). Is sustainability reporting (ESG) associated with performance? Evidence from the European banking sector. Management of Environmental Quality: An International Journal, 30(1), 98–115. https://doi.org/10.1108/MEQ-12-2017-0149

- Bui, T. T. H., & Huynh, T. M. D. (2020). Benefits and methods of measuring corporate social responsibility: An analytical review. Paper presented at the International Conference on Finance, Accounting and Auditing (ICFAA 2020), Hanoi City Vietnam.

- Coulson, A. B., & Monks, V. (1999). Corporate environmental performance considerations within bank lending decisions. Eco‐Management and Auditing: The Journal of Corporate Environmental Management, 6(1), 1–10. https://doi.org/10.1002/(SICI)1099-0925(199903)6:1<1::AID-EMA93>3.0.CO;2-M

- Dang, T. H. (2017). Theoretical studies on corporate social responsibility to the environment and its influence on the financial performance of enterprises. Paper presented at the International scientific conference Sustainable production and consumption, Ha Noi.

- Dimitropoulos, P. (2021). Corporate environmental responsibility, accounting and corporate finance in the EU: A quantitative analysis approach. Springer Nature.

- Esteban-Sanchez, P., Cuesta-Gonzalez, M. D. L., & Paredes-Gazquez, J. D. (2017). Corporate social performance and its relation with corporate financial performance: International evidence in the banking industry. Journal of Cleaner Production, 162, 1102–1110. https://doi.org/10.1016/j.jclepro.2017.06.127

- European Commission. (2014). Directive 2014/95/EU of the European parliament and of the council. https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=%20CELEX%3A32014L0095

- Fijałkowska, J., Zyznarska-Dworczak, B., & Garsztka, P. (2018). Corporate social-environmental performance versus financial performance of banks in Central and Eastern European countries. Sustainability, 10(3), 772–794. https://doi.org/10.3390/su10030772

- Gangi, F., Meles, A., D’Angelo, E., & Daniele, L. M. (2019). Sustainable development and corporate governance in the financial system: Are environmentally friendly banks less risky? Corporate Social Responsibility and Environmental Management, 26(3), 529–547. https://doi.org/10.1002/csr.1699

- Gonenc, H., & Scholtens, B. (2019). Responsibility and performance relationship in the banking industry. Sustainability, 11(12), 3329. https://doi.org/10.3390/su11123329

- Hafez, H. (2015). Corporate social responsibility and financial performance: An empirical study on Egyptian banks. Corporate Ownership and Control, 12(2), 107–127. https://doi.org/10.22495/cocv12i2p9

- Huynh, J., Dang, V. D., & McMillan, D. (2021). Loan portfolio diversification and bank returns: Do business models and market power matter? Cogent Economics & Finance, 9(1), 1891709. https://doi.org/10.1080/23322039.2021.1891709

- Huynh, Q. L. (2019). The impact of environmental responsibility on financial performance. Economy & Forecast Review, 9, 8–12. https://sti.vista.gov.vn/tw/Lists/TaiLieuKHCN/Attachments/286912/CVv139S92019008.pdf

- Iwata, H., & Okada, K. (2011). How does environmental performance affect financial performance? Evidence from Japanese manufacturing firms. Ecological Economics, 70(9), 1691–1700. https://doi.org/10.1016/j.ecolecon.2011.05.010

- Jo, H., Kim, H., & Park, K. (2015). Corporate environmental responsibility and firm performance in the financial services sector. Journal of Business Ethics, 131(2), 257–284. https://doi.org/10.1007/s10551-014-2276-7

- Kennedy, W. (1999). Environmental impact assessment and multilateral financial institutions. In J. Petts (Ed.), Handbook of environmental impact assessment (Vol. 2). Blackwell Science Ltd.

- Le, H. D. C. (2016). Effects of cash flow, systematic risk, unsystematic risk and securities liquidity on investment of Vietnamese enterprises [Doctoral dissertation, Ho Chi Minh City University of Economics]. https://digital.lib.ueh.edu.vn/handle/UEH/54705

- Le, T. T., Nguyen, T. M. A., & Phan, T. T. H. (2019). Environmental management accounting and performance efficiency in the Vietnamese construction material industry—A managerial implication for sustainable development. Sustainability, 11(19), 5152. https://doi.org/10.3390/su11195152

- Lee, K. H., Cin, B. C., & Lee, E. Y. (2016). Environmental responsibility and firm performance: The application of an environmental, social and governance model. Business Strategy and the Environment, 25(1), 40–53. https://doi.org/10.1002/bse.1855

- Li, D., Cao, C., Zhang, L., Chen, X., Ren, S., & Zhao, Y. (2017). Effects of corporate environmental responsibility on financial performance: The moderating role of government regulation and organizational slack. Journal of Cleaner Production, 166, 1323–1334. https://doi.org/10.1016/j.jclepro.2017.08.129

- Li, Q., Luo, W., Wang, Y., & Wu, L. (2013). Firm performance, corporate ownership, and corporate social responsibility disclosure in China. Business Ethics: A European Review, 22(2), 159–173. https://doi.org/10.1111/beer.12013

- Liu, Y., Xi, B., & Wang, G. (2021). The impact of corporate environmental responsibility on financial performance—based on Chinese listed companies. Environmental Science and Pollution Research, 28(7), 7840–7853. https://doi.org/10.1007/s11356-020-11069-4

- López-Gamero, M. D., Molina-Azorín, J. F., & Claver-Cortés, E. (2009). The whole relationship between environmental variables and firm performance: Competitive advantage and firm resources as mediator variables. Journal of Environmental Management, 90(10), 3110–3121. https://doi.org/10.1016/j.jenvman.2009.05.007

- Luu, T. T. T. (2019). Transparency of corporate social responsibility listed on Vietnam’s stock exchange. Journal of Financial (Online). http://tapchitaichinh.vn/kinh-te-vi-mo/minh-bach-trach-nhiem-xa-hoi-cua-cong-ty-niem-yet-tren-thi-truong-chung-khoan-viet-nam-309341.html

- Matuszaka, Ł., & Różańskaa, E. (2017). An examination of the relationship between CSR disclosure and financial performance: The case of Polish banks. Accounting And Management Information Systems, 16(4), 522–533. https://doi.org/10.24818/jamis.2017.04005

- Matuszaka, Ł., & Różańskaa, E. (2019). A non-linear and disaggregated approach to studying the impact of CSR on accounting profitability: Evidence from the Polish banking industry. Sustainability, 11(1), 1–21. https://doi.org/10.3390/su11010183

- Miles, M. P., & Covin, J. G. (2000). Environmental marketing: A source of reputational, competitive, and financial advantage. Journal of Business Ethics, 23(3), 299–311. https://doi.org/10.1023/A:1006214509281

- Ministry of Finance. (2015). Circular guiding information disclosure on the stock market. 155/2015/TT-BTC. http://vbpl.vn/botaichinh/Pages/vbpq-print.aspx?ItemID=91233

- Nehrt, C. (1996). Timing and intensity effects of environmental investments. Strategic Management Journal, 17(7), 535–547. https://doi.org/10.1002/(SICI)1097-0266(199607)17:7<535::AID-SMJ825>3.0.CO;2-9

- Nguyen, L., & Tran, M. (2019). Disclosure levels of environmental accounting information and financial performance: The case of Vietnam. Management Science Letters, 9(4), 557–570. https://doi.org/10.5267/j.msl.2019.1.007

- Nyirenda, G., Ngwakwe, C. C., & Ambe, C. M. (2013). Environmental management practices and firm performance in a South African mining firm. Managing Global Transitions, 11(3), 243. http://www.fm-kp.si/zalozba//1581-6311/11_243-260.pdf

- Pintea, M.-O., Stanca, L., Achim, S.-A., & Pop, I. (2014). Is there a connection among environmental and financial performance of a company in developing countries? Evidence from Romania. Procedia Economics and Finance, 15, 822–829. https://doi.org/10.1016/S2212-5671(14

- SBV. (2015a). Directive No. 03/CT-NHNN on promoting green credit growth and managing environmental and social risks in credit extension. https://thuvienphapluat.vn/van-ban/Tien-te-Ngan-hang/Chi-thi-03-CT-NHNN-2015-tang-truong-tin-dung-xanh-quan-ly-rui-ro-moi-truong-xa-hoi-269326.aspx

- SBV. (2016). Circular No. 39/TT-NHNN regulating lending activities of credit institutions and foreign bank branches to customers. https://thuvienphapluat.vn/van-ban/tien-te-ngan-hang/thong-tu-39-2016-tt-nhnn-hoat-dong-cho-vay-cua-to-chuc-tin-dung-chi-nhanh-ngan-hang-nuoc-ngoai-338877.aspx

- SBV. (2018). Decision No. 604/QD-NHNN approving the Green Bank Development Project in Vietnam. https://thuvienphapluat.vn/van-ban/Tien-te-Ngan-hang/Quyet-dinh-1604-QD-NHNN-2018-phe-duyet-De-an-phat-trien-ngan-hang-xanh-tai-Viet-Nam-411378.aspx

- Shabbir, M. S., & Wisdom, O. (2020). The relationship between corporate social responsibility, environmental investments and financial performance: Evidence from manufacturing companies. Environmental Science and Pollution Research, 27(32), 39946–39957. https://doi.org/10.1007/s11356-020-10217-0

- Szegedi, K., Khan, Y., & Lentner, C. (2020). Corporate social responsibility and financial performance: evidence from Pakistani listed banks. Sustainability, 12(10), 4080. https://doi.org/10.3390/su12104080

- Taşkın, D. (2015). The relationship between CSR and banks’ financial performance: evidence from Turkey. Journal of Yaşar University, 10(39), 21–30. https://doi.org/10.19168/jyu.97694

- Tran, T. H. Y. (2016). Nghiên cứu tác động trách nhiệm xã hội của doanh nghiệp đến kết quả hoạt động tài chính tại các NHTM Việt Nam. (Luận án Tiến sĩ), Trường Đại học Kinh Tế, Đại học Quốc gia Hà Nội.

- Tran, T. T., Nguyen, H. A., & Nguyen, V. D. (2016). Environmental policy in credit activities of commercial banks in Vietnam. https://nature.org.vn/vn/wp-content/uploads/2017/03/230717_Vietnam-Banking-and-Env-Policy.pdf

- VBCSD. (2020). Corporate sustainability index set. http://vbcsd.vn/csi.asp

- Vietnamese Government. (2012). Decision No. 139/QD-TTg approving the national strategy on green growth. https://thuvienphapluat.vn/van-ban/Tai-nguyen-Moi-truong/Quyet-dinh-1393-QD-TTg-nam-2012-phe-duyet-Chien-luoc-quoc-gia-tang-truong-xanh-148498.aspx

- Wang, Y., Chen, C. R., & Huang, Y. S. (2014). Economic policy uncertainty and corporate investment: Evidence from China. Pacific-Basin Finance Journal, 26, 227–243. https://doi.org/10.1016/j.pacfin.2013.12.008

- Worae, T. A., & Ngwakwe, C. C. (2017). Environmental responsibility and financial performance nexus in South Africa: Panel Granger causality analysis. Environmental Economics, 8(3), 29–34. https://doi.org/10.21511/ee.08(3).2017.03

- Wu, M. W., & Shen, C. H. (2013). Corporate social responsibility in the banking industry: Motives and financial performance. Journal of Banking & Finance, 37(9), 3529–3547. https://doi.org/10.1016/j.jbankfin.2013.04.023

- Wu, W., Ullah, R., & Shah, S. J. (2020). Linking corporate environmental performance to financial performance of Pakistani firms: The roles of technological capability and public awareness. Sustainability, 12(4), 1446. https://doi.org/10.3390/su12041446

- Xu, Q., Lu, Y., Lin, H., & Li, B. (2021). Does corporate environmental responsibility (CER) affect corporate financial performance? Evidence from the global public construction firms. Journal of Cleaner Production, 315, 128131. https://doi.org/10.1016/j.jclepro.2021.128131

- Yang, X. (1997). Environmental risk management of banks in America. World Market, 1, 32–33.

- Zhang, B., Yang, Y., & Bi, J. (2011). Tracking the implementation of green credit policy in China: Top-down perspective and bottom-up reform. Journal of Environmental Management, 92(4), 1321–1327. https://doi.org/10.1016/j.jenvman.2010.12.019