?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

This study investigates the relationship between central bank independence and financial stability in a global sample covering 56 countries from 1980 to 2012. We find strong and robust evidence that central bank independence and its four dimensions (personnel independence, financial independence, policy independence, and central bank objectives) are negatively associated with bank systemic risk. In addition, the results indicate that the reductive effect of central bank independence on systemic risk is more pronounced during actual episodes of banking crises. Moreover, our results suggest that the democratic environment plays a vital role in moderating the central bank independence − systemic risk nexus.

“Governments that do not respect central bank independence will sooner or later incur the wrath of financial markets, [and] ignite economic fire … ”(Acharya, Citation2018, pp. 31–32)

1. Introduction

The benefits of improving central bank independence (CBI) have attracted considerable attention from scholars and policymakers especially when governments across the globe have actively reformed central bank laws in the past two decades (Bodea & Hicks, Citation2015a; Garriga, Citation2016). There is a broad agreement that the mandates of modern central banks include maintaining price stability and financial stability (Das et al., Citation2004; Oosterloo & de Haan, Citation2004; Padoa-Schioppa, Citation2003; Schinasi, Citation2003). Substantial evidence emphasizes the essential role of CBI to price stability (e.g., Arnone et al., Citation2009; Berger et al., Citation2001; Blancheton & Maveyraud, Citation2018; Cukierman, Citation2008; Garriga & Rodriguez, Citation2019; Klomp & De Haan, Citation2010). Notwithstanding, much less is known about the impact of CBI on financial stability in banking sectors, although such stability has become an important public policy goal (Čihák, Citation2006).

Financial stability is the joint stability of the key financial institutions operating within financial markets and the stability of those markets (Schinasi, Citation2003). The underlying rationale for oversights of central banks in the area of financial stability is the perceived market failure in the form of systemic financial risk (Crockett, Citation1997).Footnote1 Given that (i) banking regulatory and supervisory authorities may be unexpectedly faced with political pressure, and (ii) systemic risk is a major concern of regulators and banking stakeholders (Acharya et al., Citation2017; Silva et al., Citation2017), the CBI − systemic risk nexus is worth investigating.Footnote2

There is a growing consensus that central banks, with their long-term goals, should be free from the political pressure of governments. While the horizon of decision-making of a government is short (surrounding election periods), that of central bankers is much longer (over business and financial cycles). Such difference creates a dilemma that sometimes requires a sacrifice of short-term gains (e.g., politicians’ or governments’ commitments) for long-term achievements (e.g., financial stability). In addition, governments may also intervene central banks functions, including money and credit creation, to pursue short-term strategies which contain potential risk in the long term for the financial system (Acharya, Citation2018).

On the one hand, CBI is critical for financial stability for various reasons. First, such independence frees a central bank from political interference and possible conflicts of interest. This facilitates a central bank’s prompt actions to prevent and correct financial distress or financial institutions’ problems. For example, central banks need to expand lending to financial institutions to alleviate possible liquidity shortage (Bernanke, Citation2010), perform money market operations using various instruments (Goodhart, Citation2008), regulate the credit market (Acharya, Citation2018), or introduce global policy initiatives in response to crises (Praet & Nguyen, Citation2008). In addition, right after identifying emerging disturbances, an independent central bank may alert financial markets, leading to the necessary actions to prevent possible crises (Klomp & de Haan, Citation2009). Against this, a dependent central bank may choose to provide monetary and financial support to institutions with problems, which eventually triggers moral hazards in the system. This is definitely harmful to the stability of the banking sector (Hutchison & McDill, Citation1999).

On the other hand, there is a theoretical perspective against the independence of central banks. Specifically, Berger and Kißmer (Citation2013) present a model showing how policymakers react to the run-up in an asset price. In their settings, policymakers can choose either a “leaning-against-the-wind” strategy (i.e. to raise short-term interest rates in the boom stage) or a “cleaning-up” strategy (i.e. to dissemble potential probability of crisis). Berger and Kißmer (Citation2013) prove that independent central bankers tend to choose the latter approach, consequently raising financial instability in the future. Moreover, Aklin and Kern (Citation2021) show that CBI results in weakened financial regulation, leading to various deregulation approaches related to financial reform, bank entry barriers, liberalization, deposit insurance, and capital openness. Such deregulation may trigger systemic risk since the literature has depicted that deregulation may negatively influence banking stability (e.g, Demirgüç-Kunt & Detragiache, Citation2002; Detragiache & Demirgüç-Kunt, Citation1998; Keeley, Citation1990; Marcus, Citation1984).Footnote3

There are a small number of empirical studies targeting the relation between CBI and financial stability. For instance, Khan et al. (Citation2013) find that higher bank independence is associated with a lower likelihood of experiencing a banking crisis. Klomp and de Haan (Citation2009) investigate the role of CBI on financial instability in a sample of 60 countries spanning the 1985–2005 period. The authors characterize the instability of financial systems using factor analysis on 16 country-level variables. Those variables capture changes in banking systems (e.g., change in bank liabilities to asset ratio, change in credit growth), risk and return of markets (e.g., change in interest rate, change in risk premium), and monetary traits (e.g., change in net foreign assets to GDP). Klomp and de Haan (Citation2009) suggest a negative relation between CBI and financial instability.

The application of the country-level instability indicator in Klomp and de Haan (Citation2009) is criticized by Doumpos et al. (Citation2015) because it results in a small sample and may lead to a loss of bank-level characteristics. Alternatively, Doumpos et al. (Citation2015) target bank-level stability indicated by the Z-score (i.e. insolvency risk). Using a sample of 1,756 commercial banks from 2000 to 2011, the authors show that CBI exerts positive repercussions on banking soundness. Andrieș et al. (Citation2022) aim to investigate the effects of CBI on bank systemic risk using a data sample containing 323 publicly listed banks in 40 countries from 2001 to 2014. Using the index proposed by Bodea and Hicks (Citation2015b) to indicate CBI, the authors document a strong and negative relationship between CBI and systemic risk.

In this research, we explore the relationship between CBI and bank systemic risk, which attracts great attention over the past few years (Silva et al., Citation2017). After the Global Financial Crisis and the Eurozone sovereign debt crisis, the identification of the banks which remarkably contribute to the aggregate risk of the financial system has been an interest of scholars and policymakers (Benoit et al., Citation2013; Dungey et al., Citation2022). Systemic risk can be defined as “broad based breakdown in the functioning of the financial system, which is normally realized, ex post, by a large number of failures of FIs” or “the breadth of its reach across institutions, markets, and countries” (IMF, Citation2009, p. 113). Meanwhile, various studies depict the massive influences of banking distortions on the real economy (e.g., Acharya et al., Citation2018; Chodorow-Reich, Citation2014; Hoggarth et al., Citation2002; Laeven & Valencia, Citation2013).

We employ a systemic risk indicator, namely marginal expected shortfall (MES; Acharya et al., Citation2017), to characterize systemic instability, instead of the country-level indicator as in Klomp and de Haan (Citation2009) or standalone bank risk as in Doumpos et al. (Citation2015).Footnote4 MES measures how exposed a bank is to aggregate tail shocks. Acharya et al. (Citation2017) show that it can quantitatively predict the financial corporations with the worst contributions to the financial system, thereby meeting the definition of systemic risk.

MES is a widely recognized indicator of bank systemic risk and is used in various empirical studies.Footnote5 Its use has various benefits. First, MES requires simple data to estimate (Acharya et al., Citation2017), but it has a stronger predictive ability compared to other risk measures (Acharya et al., Citation2017; Engle et al., Citation2014).Footnote6 Second, MES varies at the bank level, thus tackling the disadvantage of the country-level measure of instability employed in Klomp and de Haan (Citation2009). Third, MES requires market-based information to estimate. Thus, it allays concerns regarding manipulation or inconsistencies across regulatory jurisdictions or over time because of changes in accounting policies when using accounting-based measures (Jiang et al., Citation2017). Fourth, using a market-based measure is beneficial for prediction purposes since market information reflects future cash flow and is forward-looking (Fu et al., Citation2014).

Our study complements the recent literature on the effects of CBI on economic outcomes, in which very few studies focus on bank-level risk in general, and systemic risk in particular. In addition, this article differs from Andrieș et al. (Citation2022) in several aspects. First, we retrieve the index of CBI from Garriga (Citation2016), which is the largest dataset on CBI compared to other publicly available databases.Footnote7 By doing so, our final sample data spans more than three decades and thus captures various disturbances in global financial markets such as Black Monday, the Asian financial crisis, the Global Financial Crisis and the European debt crisis. In addition, Garriga (Citation2016) dataset conveniently provides information on whether a central bank is a regional entity (e.g., the European Central Bank or the Bank of Central African States). Thus, we can either include or exclude regional centrals banks to convincingly observe the influence of CBI on bank risk. Importantly, we show that the effect of CBI on systemic risk is not due to the level of CBI per se but rather to the interplay between CBI and democratic environment. In other words, we investigate the moderating role of democracy on the relationship between CBI and systemic risk. Although the democratic environment can facilitate the usefulness of CBI on price stability (Garriga & Rodriguez, Citation2019), its role on the CBI—systemic risk nexus is still an open and unsolved question in the recent literature.

Using a sample of more than 5,000 bank-year observations in 56 countries from 1980 to 2012, we find that lower CBI is associated with higher systemic risk measured by MES (Acharya et al., Citation2017). The impact is economically large: a standard deviation decrease in CBI is associated with 0.499% jump in systemic risk, representing 21% of its standard deviation. Our result is robust when we apply alternative measures of CBI and risk, various subsamples, and alternative estimation techniques which tackle endogeneity issues.

Moreover, Cukierman et al. (Citation1992) state that the independence of central banks results from various factors. Garriga (Citation2016) provides information on four key components of independence (personnel independence, financial independence, policy independence, and central bank objectives). The analysis of components is essential for at least two reasons. First, such analysis provides implications for conceptualizing and measuring CBI and offers insights for policymakers when implementing each dimension of independence (Garriga & Rodriguez, Citation2019). Second, there are arguments about the validity of statistical analysis on the dimensions of CBI (e.g, Banaian et al., Citation1998) and concerns about the possibility that some components may drive the main result (see, Garriga & Rodriguez, Citation2019).

Conceptually, the deterioration of financial independence leads to the higher ability of the government to use central bank loans to finance its expenditures or public sectors, whereas a reduction in personnel independence allows government intervention on the board membership and tenure of central bankers. In addition, the ability of central banks to formulate and implement policies will be altered negatively if policy independence is politically violated (Garriga, Citation2016). Lastly, the independence of central bank objectives will be reduced if banks have various goals in conflict with maintaining price and financial stability (Cukierman et al., Citation1992). Therefore, anything that threatens the CBI dimension could potentially affect central bank function and policy management toward central bank mandates in financial markets, consequently penalizing market players such as banks.Footnote8 The above argument implies that we should expect each dimension to be negatively associated with bank risk. And when decomposing CBI into four components, we find that all components are negatively associated with systemic risk. The results thus indicate that independence in all aspects matters for the systemic stability of banking sectors.

We have argued that CBI is beneficial for systemic stability since it provides corrective actions to markets during times of financial disturbance. Hence, we include banking crises in our model, expecting that the benefits of CBI on bank stability should be more pronounced in times of crises. Using information on banking crises from Laeven and Valencia (Citation2018), the results indicate that CBI exerts a stronger reductive impact on systemic risk when countries experience banking crises, and so do the four components of CBI.

Political science has documented the moderating role of democratic environments on CBI (Bodea & Hicks, Citation2015b; Fazio et al., Citation2018; Garriga & Rodriguez, Citation2019). Bodea and Hicks (Citation2015b) suggest that democracies differ from dictatorships in the degree of political interference because of the existence of political oppositions and freedom to express disagreement and expose government scandals or performance. Therefore, in a more democratic environment, the government cannot freely coerce and intervene in central banking activities. This is because law implementation and amendment in democracies allow an independent central bank to pursue its long-term goals regardless of government interference for short-term interests. In addition, the central bank is more credible in democratic countries with the presence of the free press and free speech (Bodea & Hicks, Citation2015b).

From the above argument, we investigate whether the political environment can explain the variation in the CBI − systemic risk nexus. Following previous studies (Bodea & Hicks, Citation2015b; Garriga & Rodriguez, Citation2019), we employ the democracy score, Polity2, from Marshall et al. (Citation2019). We document that the negative effect of CBI on bank systemic risk is more substantial in a more democratic environment. Notably, we find that there are differences in the effects of CBI dimensions on systemic risk conditioning on the level of democracy. The finding implies that some components are more effective at reducing bank risk when taking democracies into consideration.

The remainder of this paper is structured as follows. Section 2 describes measures and data sampling. Section 3 shows the research method. Section 4 displays empirical results, while section 5 concludes.

2. Measures and data sampling

2.1. Measuring central bank independence

An indicator of CBI is retrieved from Garriga (Citation2016), covering 182 countries from 1970 to 2012. Based on the methodology described in Cukierman et al. (Citation1992), Garriga (Citation2016) constructs the de jure CBI index using more than 800 documents related to central bank charters, constitutions, laws and amendments. According to Garriga (Citation2016), the CBI index appears as an appealing alternative for the de facto CBI retrieved from questionnaires (e.g., Almeida et al., Citation1996; Blinder, Citation2000) or the turnover rate of central bankers (e.g., Cukierman & Webb, Citation1995; De Haan & Siermann, Citation1996). The de facto CBI is criticized for its reliability, coverage and cross-country comparability (Garriga, Citation2016). Meanwhile, the application of the turnover rate suffers from reverse causality issues since central bankers who fail to accomplish missions are replaced more frequently (Dreher et al., Citation2008).

We employ the average of CBI for the main analysis, and the weighted index is used for the robustness test. The CBI index varies from zero to one. Higher values of this index mean greater independence.

Eijffinger and De Haan (Citation1996) and Cukierman et al. (Citation1992) suggest that CBI originates from various factors. Hence, from Garriga (Citation2016), we employ indicators on four components of CBI as follows: (i) personnel independence (appointment, dismissal, and term of office of a central bank’s CEO); (ii) policy independence (the formulation of monetary policy, directives and resolution of conflicts from the government, and the role of the central bank in the budget process); (iii) central bank objectives; and (iv) financial independence (limitations on lending to the government).Footnote9

A shortcoming of data retrieved from Garriga (Citation2016) is that it covers CBI up to 2012. Some may argue that such time coverage prohibits researchers from investigating the role of CBI during more recent banking disturbances. We provide information to allay this concern. According to Laeven and Valencia (Citation2018), there were 151 banking crises from 1970 to 2017, but from 2013 onwards, there were only three banking crises (in 2014, in Guinea-Bissau, Moldova, and Ukraine which are not in our sample).

2.2. Measuring systemic risk

To measure bank-level systemic risk, we follow banking literature (e.g., Engle et al., Citation2014) by employing the MES proposed by Acharya et al. (Citation2017). The utilization of MES is beneficial since it requires simple data to construct. Engle et al. (Citation2014) show advantages of MES over other systemic risk indicators. The authors suggest that MES is the most suitable indicator for predicting bank distress in the 1996 Asian and 2007–2009 financial crises.

A bank’s MES is computed as the average equity return of a bank (ri) when the return of the country banking market (rm) is in its worst 5% return quantile over one year. For ease of interpretation, the negative value of MES is used. Thus, higher values of MES suggest higher systemic risk.

Following Nguyen (Citation2020), we also employ an alternative version of systemic risk for robustness checking. Specifically, MESGlobal is the negative value of the average of bank stock return (ri) when the global market return (rm-global) is in the 5% left tail of its return distribution. The global banking index is provided by Datastream (code: BANKWD).

2.3. Sample construction

Our main source of data is Datastream. Since the estimation of our systemic risk measure requires market data, we focus on publicly listed banks. Our objective is to construct a sample that can represent both country and global banking sectors. To do so, we retrieve banks from the list of global banks provided by Datastream (i.e. constituents of the Datastream global banking index BANKWD).Footnote10 Those banks cover a minimum of 75 to 80% of total market capitalization of countries worldwide.

Because financial information is only available from 1980 from Datastream, we collect data from 1980 onwards. We (i) drop banks that have no data on key characteristics (such as size, deposits, loans, market to book value, provisions), (ii) remove banks in countries where the country stock price index is not available up to 2012, and (iii) drop banks in economies where macroeconomic data is not available (such as Taiwan). Lastly, we delete banks in Hong Kong because CBI data does not cover this economy. We retrieve stock price and accounting data in U.S. dollars to reduce possible bias regarding currency risk. The final sample in an unbalanced panel data, containing 5,509 bank-year observations from 415 active banks in 56 countries.

3. Research method

We employ the following specifications to investigate the relationship between CBI and bank systemic risk:

where i, j and t denote bank, country and year, respectively. The dependent variable is bank systemic risk − MES (%) − while the key independent variable is CBI. The negative sign of suggests that higher CBI is associated with lower systemic risk, and vice versa.

All explanatory variables are lagged by one year to mitigate reverse causality issues. Bank fixed effects and year dummies are included in Equationequation (1)(1)

(1) to control for omitted time invariant heterogeneity at the bank level (such as bank ownership structure) and global business cycle.Footnote11 In addition, we cluster standard errors at the bank level to correct for heteroscedasticity and autocorrelation.

In Equationequation (1)(1)

(1) , B (C) is a matrix of bank-level (country-level) variables. At the bank level, following the recent literature on drivers of bank risk, we include the following controls:

LnTA: the natural logarithm of total assets in thousands of US$ (Laeven et al., Citation2016).

MTB: market to book ratio calculated as market value of common equity divided by book value of common equity (Brunnermeier et al., Citation2012).

LOAN: loans to total assets (Engle et al., Citation2014).

DEPOSIT: deposit to total liabilities (Bostandzic & Weiß, Citation2018).

PROVISIONS: loan loss provisions (expenses set aside as an allowance for uncollectable or troubled loans) deflated by interest income (Beck et al., Citation2013; Bostandzic & Weiß, Citation2018).

DEBT_MATURITY: long-term debts divided by total liabilities (Bostandzic & Weiß, Citation2018).

NIIS: non-interest income divided by total income (Brunnermeier et al., Citation2012; DeYoung & Roland, Citation2001; Saunders et al., Citation2020).

LEVERAGE: total assets divided by total equity (Karolyi et al., Citation2018).

At the country level, we employ the natural logarithm of GDP per capita (constant 2010 US$) (LnGDPPC), the annual growth rate of GDP (GDPGR), and annual change in consumer price index (INFLATION) to control for economic development and conditions. In addition, we use domestic credit to the private sector by banks (PRIVATE) to capture banking sector development. We also use the annual percentage change in Private credit by deposit money banks (CREDITGR) following the calculation in Nguyen et al. (Citation2020). Operationally, CREDITGRt = ln(LOANt/LOANt-1) where LOAN is private credit by deposit money banks.Footnote12 Those country-level variables are retrieved from the World Development Indicator (WDI) and the Global Financial Development Database (GFDD).

Lastly, IMFP is a dummy variable which equals one for years when a country is under the programs of IMF lending.Footnote13 Following Oberdabernig (Citation2013), we consider both Stand-By Arrangement and Extended Fund Facility. The literature offers conflicting predictions on the role of IMF supports. On the one hand, Papi et al. (Citation2015) and Dreher and Walter (Citation2010) find that IMF programs reduce the probability of financial crises. On the other hand, IMF supports lead to the weakened incentives of national policymakers when making their own adjustment efforts, laxer economic policies, and the higher IMF dependency, consequently bearing a negative impact on banking stability (Goldstein, Citation2001; Vaubel, Citation1983). Dreher (Citation2004) and Conway (Citation2006) discuss the creditor moral hazard related to IMF programs. In support, Jorra (Citation2012) find that IMF programs increase the likelihood of subsequent sovereign defaults due to the increased debtor moral hazard. We winsorize dependent and control variables at the first and 99th percentiles to reduce the influence of outliers.

4. Empirical results

4.1. Descriptive statistics

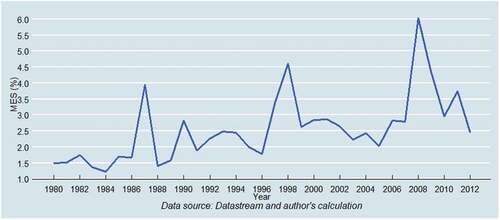

Figure illustrates the evolution of MES from 1980 to 2012. It is observed that values of systemic risk indicator are remarkably high around 1987, 1998 and 2008, which indicate the heavy consequences of Black Monday, the Asian financial crisis and the GFC, respectively.

Figure 1. Systemic risk over time.This figure shows the evolution of MES (%) from 1980 to 2012. To produce this graph, we calculated the mean value of MES by year based on 5,509 observations from 56 countries in our sample.

Table presents the national mean values of CBI index for 56 countries in our data sample. We observe considerable variation in CBI across countries in our sample, ranging from the minimum of 0.166 (Brazil) to the maximum of 0.879 (Romania).

Table 1. Descriptive statistics of CBI index and MES(%) by country

Table presents the descriptive statistics of all variables. The mean (standard deviation) of systemic risk is 3.032% (2.370%). The mean of CBI index is 0.509, which is far less than one, indicating that on average, central banks in our sample have low levels of independence.

Table 2. Descriptive statistics

4.2. The relationship between CBI and systemic risk

Table displays the estimates of Equationequation (1)(1)

(1) using bank and year fixed effects. In column (1), CBI is the only independent variable, while all controls are included in column (2).

Table 3. The relationship between CBI and systemic risk

Consistent with Laeven et al. (Citation2016), estimates show that larger banks tend to be systemically riskier. Large banks have more complex operations and a higher degree of interconnectedness when compared to small banks (Bostandzic & Weiß, Citation2018). The “too-big-too-fail” paradigm depicts that regulators are reluctant to close massive banks, leading to the moral hazard behaviour of bank managers. Consequently, large banks are more likely to engage in excessive risk-taking strategies (Farhi & Tirole, Citation2012; Gandhi & Lustig, Citation2015).

Next, we find that the estimate on DEPOSIT is negative and significant. Banks with a lower share of deposits are more fragile in their funding structure, leading to higher risk (Bostandzic & Weiß, Citation2018; Brunnermeier et al., Citation2012). The estimates on NIIS are negative and significant, suggesting that banks in our sample may benefit when diversifying their income stream. Lastly, it is obvious, when observing the positive relation between loan loss provisions and systemic risk, that banks with bad credit portfolios are riskier.

Consistent with Demirgüç-Kunt and Detragiache (Citation1998), we find that banks are systemically riskier in countries with weak macroeconomic environments, indicated by low level of GDP per capita and high inflation. Moreover, complementing the evidence in Demirgüç-Kunt and Detragiache (Citation1998), our results show that banks in economies with larger exposure to private sector borrowers (i.e. higher private credit on GDP ratio) are more fragile. As expected, we find that excessive loan growth is associated with bank systemic risk. The estimate on IMFP dummy is positive and significant, suggesting that the participation in IMF lending programs is associated with higher bank systemic risk. The result support the moral hazard effects documented in prior theories and empirics, such as Jorra (Citation2012), Goldstein (Citation2001) and (Vaubel, Citation1983).

We then place the spotlight on our variable of interest, which is the indicator for CBI. It is observed that the estimates on CBI are negative and significant in specifications (1) and (2). Therefore, the negative relationship between CBI and bank systemic risk is not driven by spurious correlations between other variables.

The coefficient of CBI shows that lower central bank independence is associated with higher systemic risk. The impact is economically meaningful. Using the result in column (2) for interpretation, we find that a one standard deviation drop in CBI index (0.194) is associated with 0.499% increase in value of MES (%), representing about 21% of its standard deviation. The finding is consistent with prior studies on the CBI—financial stability nexus (Andrieș et al., Citation2022; Doumpos et al., Citation2015; Klomp & de Haan, Citation2009), depicting the beneficial role of CBI on financial stability.

To test whether each component is associated with systemic risk, we estimate model (1) and replace the CBI index with personnel independence, financial independence, policy independence, and central bank objectives indices. We find that all components are statistically and negatively associated with bank systemic risk, indicating that independence in all aspects matters for the systemic stability of banking sectors. This result provides evidence for potential initiatives from policymakers to complement and strengthen the four major components of CBI.

4.3. Sensitivity tests

We conduct a battery of sensitivity tests to provide a convincing view of the negative association between CBI and systemic risk. First, we consider alternative sample selection criteria and present the results in Table . Precisely, from the “full” sample containing 56 countries, we form 56 subsamples by removing one country from the full panel. We also exclude each region from the sample and estimate model (1).Footnote14

Table 4. Robustness test: using different subsamples

Moreover, there are regional central banks in some parts of the world, such as the European Central Bank or Bank of Central African States. Thus, some groups of countries have the same CBI value (e.g., Austria, Belgium and Finland from 1998 onwards). We remove regional banks from the sample for robustness checking to ensure their presence does not distort our results (subsample 57).

We employ bank and year fixed effects and cluster standard errors at the bank level for all subsamples. It is observed that all coefficients of CBI are negative and significant. When we remove some countries with the largest number of banks (such as Japan or the U.S.), each region, and regional central banks, the negative association between CBI and systemic risk holds. Therefore, our result is robust to different sample selection criteria.

In the subsequent analysis presented in Table , we employ alternative indicators of CBI and bank risk. In column (1), we apply an alternative version of systemic risk, which is MESGlobal. Next, in column (2), we replace the CBI index with Garriga (Citation2016) weighted CBI index.Footnote15 In the last two columns, we retrieve two measures of CBI (CBI_Bodea and CBI_Bodea_weighted) from Bodea and Hicks (Citation2015b). It is observed that the estimates on CBI variables are negative and significant, confirming that the utilization of alternative measures does not alter our result.

Table 5. Robustness test: using alternative measure of systemic risk and CBI

In Table , we show the results when employing different estimation techniques. In column (1), we use country fixed effects and year dummies. The use of the country fixed effects technique can control unobserved and time-invariant characteristics at the country level. Next, our CBI measure is at the country level, while the outcome variable is at the bank level. Thus, we have multilevel panel data. We employ the hierarchical linear modelling as in Doumpos et al. (Citation2015) and present the result in column (2).Footnote16 Albeit that Hausman statistics support the use of fixed effects, we show the estimate generated from the random effects estimator as a mean of robustness check (column 3). It is observed that the estimated coefficients of CBI are negative and statistically significant in columns (1), (2) and (3).

Table 6. Robustness test: using alternative econometrics techniques

In the main analysis, we use the lagged values of explanatory variables to eliminate endogeneity concerns related to the reverse causality problem. Nonetheless, possible issues of endogeneity, such as omitted variables, may still drive the main finding of our study.Footnote17 We employ two approaches to efficiently tackle endogeneity issues following the econometric setting proposed by Garriga and Rodriguez (Citation2019).Footnote18 First, in column (4), we employ the two-step system generalized method of moments (GMM) estimator (Blundell & Bond, Citation1998) as in Klomp and de Haan (Citation2009) and Garriga and Rodriguez (Citation2019). We observe that the coefficient of CBI is negative and statistically significant in column (4). In addition, statistics from post-estimation tests (AR1, AR2, and Hansen test) validate the use of the system GMM technique for our data sample.

Second, we treat CBI as an endogenous variable and apply the two-stage least squares (2SLS) method. Following Garriga and Rodriguez (Citation2019), we employ the regional CBI (CBI_regional) as an instrument. Using the data from Garriga (Citation2016), the CBI_regional for each country j is the regional average of CBI (excluding country j; see, Garriga & Rodriguez, Citation2019, footnote 29). In our data sample, the correlation coefficient between CBI indicator and CBI_regional is 0.60, which is similar to that in Garriga and Rodriguez (Citation2019). The result of 2SLS is shown in column (5).Footnote19 The estimate on CBI indicator is negative and significant, suggesting that CBI negatively influences bank systemic risk. In addition, the estimate on CBI_regional (the first-stage regression) is positive and significant. It is consistent with Garriga and Rodriguez (Citation2019).

Because we use clustered standard errors, a traditional test for weak instruments such as the Cragg and Donald (Citation2009) statistic is not applicable. Therefore, we employ the Montiel–Pflueger robust weak instrument test (Olea & Pflueger, Citation2013), which is robust to heteroscedasticity, autocorrelation, and clustering. We observe that the effective F-statistic exceeds the critical value (and far exceeds 10), showing that the instrument variable is not weak.

4.4. CBI and bank systemic risk: banking crises included

To investigate the role of CBI during banking crisis episodes, we add an interaction term between CBI and the banking crisis variable into model (1). Specifically, BANKING_CRISIS is a dummy variable which equals one in a year when a country experiences a banking crisis and zero otherwise. According to Laeven and Valencia (Citation2018), a country is under a banking crisis if there are substantial signs of distress in the banking system (e.g., bank runs, losses) and significant banking policy intervention as responses to banking losses. We retrieve information on actual episodes of banking crises from Laeven and Valencia (Citation2018). Table illustrates the results of this analysis.

Table 7. Central bank Independence and systemic risk: banking crises included

The estimate on the interaction term (BANKING_CRISIS * CBI) is negative and significant at the 1% level, and so are the coefficients associated with the four components (columns 2 to 5). To facilitate interpretation, we present the joint effects of CBI and the interaction term for two scenarios: BANKING_CRISIS = 0 and BANKING_CRISIS = 1 at the bottom of Table .

The simple slope is—9.104 and—2.532 when BANKING_CRISIS = 1 and BANKING_CRISIS = 0, respectively.Footnote20 Using the delta method to obtain the standard errors, we observe that the effect of CBI is statistically significant at the 1% level for the two scenarios. We draw similar conclusions when focussing on personnel independence, central bank objectives, policy independence, and financial independence. Thus, CBI and its dimensions exert a stronger eliminating effect on systemic risk when countries experience banking crises than in normal times.

4.5. CBI and systemic risk: the role of democratic environments

To investigate the conditioning role of democracy, we include the interaction between CBI and Polity2 in Equationequation (1)(1)

(1) . Note that Polity2 varies from—10 to 10, and higher values indicate a more democratic environment. We present the estimates in Table .

Table 8. Central bank Independence and systemic risk: the role of democratic environments

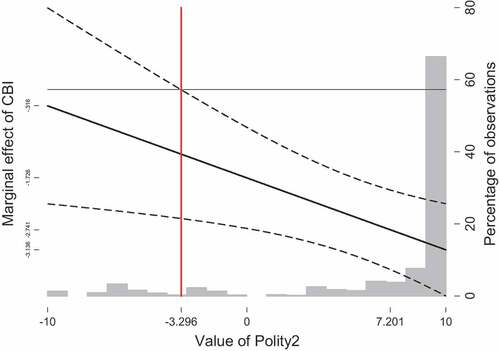

From column (1), it is observed that the estimate on the interaction term is negative and significant. A first glance at the coefficient suggests that CBI has a strong reductive effect on systemic risk when values of Polity2 increase. Nonetheless, merely showing the estimates on CBI indicator, Polity2 and their interaction terms is less informative since it does not show how the marginal effect of CBI changes across the meaningful range of Polity2. Therefore, following Brambor et al. (Citation2006), we visualize the marginal effect of CBI on systemic risk by level of democracy.

In Figure , we show the marginal effect of CBI when Polity2 is at its mean, min and max (the meaningful range). In addition, the 95% confidence intervals provide information on the conditions under which CBI has a statistically significant effect on bank systemic risk (both upper and lower bounds are above or below zero).

Figure 2. The marginal effect of CBI on systemic risk.The sloping line illustrates how the marginal effect of CBI changes with the level of democracy measured by Polity2. Any particular point on this line is . Coefficients are estimated from:

with bank and year fixed effects. The bar chart shows the distribution of Polity2. The two dashed lines indicate the 95% confidence intervals. The red vertical line crosses the value of Polity2 from which the marginal effect of CBI is statistically significant (–3.296).

It is observed that the marginal effect of CBI is statistically insignificant when Polity2 <—3.296, indicating that the moderating role of democracy is irrelevant in countries characterized by low democratic environments. CBI provides a significant reductive effect (at the 5% level) on systemic risk when countries reach a certain level of democracy (i.e. Polity2 ≥—3.296). The distribution of Polity2 shows that the significant reductive effect is applicable for most observations in our sample.

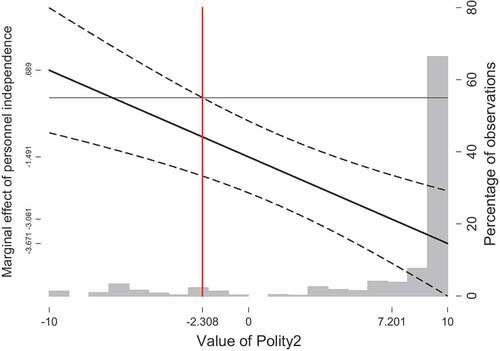

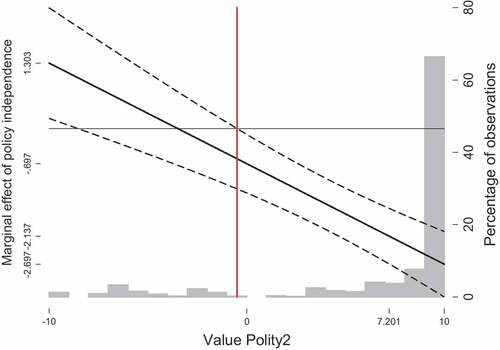

Interestingly, we observe that estimates on the interactions between personnel independence and Polity2 (column 2), and between policy independence and Polity2 (column 4) are statistically significant at the 1% level. Nonetheless, the coefficients associated with the remaining two components are insignificant. Similarly, we visualize the marginal effects of personnel independence and policy independence in Figures , respectively. The thresholds from which personnel independence and policy independence exert significant reductive effects on systemic risk are—2.308 and—0.480, respectively.

Figure 3. The marginal effect of personnel Independence on systemic risk.The sloping line illustrates how the marginal effect of personnel independence changes with the level of democracy measured by Polity2. Any particular point on this line is . Coefficients are estimated from:

with bank and year fixed effects. The bar chart shows the distribution of Polity2. The two dashed lines indicate the 95% confidence intervals. The red vertical line crosses the value of Polity2 from which the marginal effect of personnel independence is statistically significant (–2.308).

Figure 4. The marginal effect of policy Independence on systemic risk.The sloping line illustrates how the marginal effect of policy independence changes with the level of democracy measured by Polity2. Any particular point on this line is . Coefficients are estimated from:

with bank and year fixed effects. The bar chart shows the distribution of Polity2. The two dashed lines indicate the 95% confidence intervals. The red vertical line crosses the value of Polity2 at which the marginal effect of policy independence is statistically significant (–0.480).

5. Conclusion

There have been lively discussions on the threatened independence of central banks (Acharya, Citation2018; Blinder, Citation2010). In parallel, the heavy consequences of the recent crises, including the disappearance of massive financial giants and the huge amounts used to bail out problem institutions, raise the importance of maintaining systemic stability in banking sectors. In this study, we investigate the relationship between CBI and bank systemic risk in a sample of banks in 56 countries from 1980 to 2012. Our study joins a handful of empirical papers addressing the influence of CBI on financial stability.

Using the index constructed by Garriga (Citation2016) to measure CBI and the MES (Acharya et al., Citation2017) to indicate systemic risk, our findings can be summarized as follows. First, we document a strong and negative relationship between CBI and systemic risk. This negative association is confirmed with a battery of robustness tests, including the utilization of alternative sample selection criteria, alternative measures of CBI and systemic risk, and various estimation techniques.

Furthermore, the benefits of CBI tend to be more pronounced during banking crises. Notably, we show that the reductive effect of CBI on bank systemic risk is more substantial in countries with a higher level of democracy.

When disaggregating CBI, we find that all four components are negatively associated with systemic risk and exert a stronger impact during banking crises. Interestingly, the moderating role of democracy is different for different dimensions of CBI, revealing the importance of personnel independence and policy independence.

Consistent with prior research (Andrieș et al., Citation2022; Doumpos et al., Citation2015; Klomp & de Haan, Citation2009), this study highlights the importance of maintaining and improving central bank independence. Since financial crises originate from bank systemic risk, the degree to which central banks are free from political intervention in order to implement necessary policies and conduct oversights should contribute to the soundness of banking systems.

Acknowledgements

We thank Anil V. Mishra, An Nguyen, Tuan Van Nguyen, Tuan Doan, and participants in a DLU research seminar for insightful comments on an early version of this paper. Duc Nguyen greatly appreciates Robert Faff for his invaluable instruction during the “Pitching Research” section at Western Sydney University, Australia. Duc Nguyen dedicates this article to his two beloved sons (Bond and Pi). Any remaining errors are our own responsibility.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

Notes

1. Acharya and Richardson (Citation2009) define systemic risk as the joint failure of financial institutions and capital markets that considerably shortens the supply of capital to the real market.

2. For example, see Trump vs. FED [at https://www.nytimes.com/2019/11/18/business/economy/trump-powell-fed.html]; Argentina’s central bank chief, Martin Redrado, and the government in Acharya (Citation2018); a case about the Bank of England in Balls et al. (Citation2018); and some cases discussed in Blinder (Citation2010).

3. We thank an anonymous reviewer for suggesting this point.

4. Danı́elsson (Citation2002) suggests that macroprudential regulations targeting individual risk in financial institutions are insufficient to prevent financial crises.

5. MES is used in various empirical studies targeting the systemic stability of not only banks (e.g, Engle et al., Citation2014; Karolyi et al., Citation2018; Nguyen, Citation2020; Silva-Buston, Citation2019) but also non-financial corporations (e.g, Dungey et al., Citation2022).

6. Meanwhile, the ∆CoVaR (Adrian & Brunnermeier, Citation2016) requires various types of market data such as the Chicago Board Options Exchange volatility index (VIX), three-month Treasury bill rate and repo rate, the credit spread between BAA-rated bonds and the Treasury rate (see, Adrian & Brunnermeier, Citation2016; Anginer et al., Citation2018; Laeven et al., Citation2016). Data limitation prevents us from using ∆CoVaR because market-based data are unavailable for most economies, especially during the 1980s and 1990s.

7. Arnone et al. (Citation2006) provide a review of various measures of CBI.

8. See, Acharya (Citation2018) for some examples of how governments undermine the independence of central banks and the consequences of such interventions.

9. See, Garriga (Citation2016) online appendix for the variables used to construct each component.

10. There is a drawback when gathering financial information from Datastream following this procedure as researchers cannot obtain data of inactive banks.

11. We conduct the Hausman test to determine the appropriate technique. The Hausman test outcomes (Chi-squared statistics = 331.42, p-value = 0.0000) support the utilization of the fixed effects technique instead of random effects.

12. The Global Financial Development Database provides data on Private credit by deposit money banks to GDP. Hence, LOANt = Private credit by deposit money banks to GDPt *GDPt.

13. We thank an anonymous reviewer for suggesting this control variable. The data to construct this variable is publicly available at https://www.imf.org/external/np/fin/tad/query.aspx

14. This approach is widely applied in banking literature, for example, Phan et al. (Citation2020).

15. See the rule of thumb to calculate the weighted version of CBI in Garriga (Citation2016).

16. We thank an anonymous reviewer for suggesting this test.

17. For example, banking regulations and other legal frameworks at the country level. Unfortunately, large databases on banking regulations such as Barth et al. (Citation2013) do not fully cover our sample, which spans from 1980 onwards.

18. We thank an anonymous reviewer for recommending this approach.

19. To save space, the full estimates of the first stage are not shown, but they are available on request.

20. The coefficients are the linear combination of CBI (and each component) and the interaction term at two values of crisis variable.

References

- Acharya, V. V., & Richardson, M. (2009). Causes of the financial crisis. Critical Review, 21(2–3), 195–27. 10.1080/08913810902952903

- Acharya, V. V., Pedersen, L. H., Philippon, T., & Richardson, M. (2017). Measuring systemic risk. The Review of Financial Studies, 30(1), 2–47. 10.1093/rfs/hhw088

- Acharya, V. V. (2018). On the Importance of Independent Regulatory Institutions–The Case of the Central Bank. Current Statistics, 67, 21. https://rbidocs.rbi.org.in/rdocs/Bulletin/PDFs/0RBIBULLETIN_F79C0C7C6BA824813B9F651BD63C21176.PDF#page=27

- Acharya, V. V., Eisert, T., Eufinger, C., & Hirsch, C. (2018). Real effects of the sovereign debt crisis in Europe: evidence from syndicated loans. The Review of Financial Studies, 31(8), 2855–2896. 10.1093/rfs/hhy045

- Adrian, T., & Brunnermeier, M. K. (2016). CoVaR. American Economic Review, 106(7), 1705–1741. 10.1257/aer.20120555

- Aklin, M., & Kern, A. (2021). The side effects of central bank Independence. American Journal of Political Science, 65(4), 971–987. 10.1111/ajps.12580

- Almeida, A., Fry, M. J., & Goodhart, C. (1996). Central banking in developing countries: objectives, activities and Independence. Routledge.

- Andrieș, A. M., Podpiera, A. M., & Sprincean, N. (2022). Central bank Independence and systemic risk. International Journal of Central Banking, 18(1), 81–130.

- Anginer, D., Demirguc-Kunt, A., Huizinga, H., & Ma, K. (2018). Corporate governance of banks and financial stability. Journal of Financial Economics, 130(2), 327–346. 10.1016/j.jfineco.2018.06.011

- Arnone, M., Laurens, B., & Segalotto, J.-F. (2006). The measurement of central bank autonomy: survey of models, indicators, and empirical evidence. IMF Working Paper 06/227. https://deliverypdf.ssrn.com/delivery.php?ID=084013121017007091028087096112022109086032061048043044009013013048077018021095068065100085091036047023066103124093083124097079003111083016006018088082005071095121006126019090095009&EXT=pdf&INDEX=TRUE

- Arnone, M., Laurens, B. J., Segalotto, J.-F., & Sommer, M. (2009). Central bank autonomy: lessons from global trends. IMF Staff Papers, 56(2), 263–296. 10.1057/imfsp.2008.25

- Balls, E., Howat, J., & Stansbury, A. (2018). Central bank Independence revisited: after the financial crisis, what should a model central bank look like? M-RCBG Associate Working Paper Series No. 87, Harvard Kennedy School.

- Banaian, K., Burdekin, R. C. K., & Willett, T. D. (1998). Reconsidering the principal components of central bank Independence: the more the merrier? Public Choice, 97(1/2), 1–12. 10.1023/A:1004942714368

- Barth, J. R., Caprio, G., & Levine, R. (2013). Bank regulation and supervision in 180 countries from 1999 to 2011. Journal of Financial Economic Policy, 5(2), 111–219. 10.1108/17576381311329661

- Beck, T., De Jonghe, O., & Schepens, G. (2013). Bank competition and stability: cross-country heterogeneity. Journal of Financial Intermediation, 22(2), 218–244. 10.1016/j.jfi.2012.07.001

- Benoit, S., Colletaz, G., Hurlin, C., & Pérignon, C. (2013). A theoretical and empirical comparison of systemic risk measures. HEC Paris Research Paper No. FIN-2014-1030. https://halshs.archives-ouvertes.fr/halshs-00746272/file/Systemic_Risk_June_2013.pdf

- Berger, H., De Haan, J., & Eijffinger, S. C. W. (2001). Central bank Independence: an update of theory and evidence. Journal of Economic Surveys, 15(1), 3–40. 10.1111/1467-6419.00131

- Berger, W., & Kißmer, F. (2013). Central bank Independence and financial stability: A tale of perfect harmony? European Journal of Political Economy, 31, 109–118. 10.1016/j.ejpoleco.2013.04.004

- Bernanke, B. S. (2010). Central bank Independence, transparency, and accountability [Press release]. https://www.federalreserve.gov/newsevents/speech/bernanke20100525a.htm

- Blancheton, B., & Maveyraud, S. (2018). Central bank Independence and inflation: The government debt and inflation targeting channel. Finance Bulletin, 1(2), 13–33. 10.20870/fb.2018.1.2.2128

- Blinder, A. S. (2000). Central-bank credibility: why do we care? How do we build it? American Economic Review, 90(5), 1421–1431. 10.1257/aer.90.5.1421

- Blinder, A. S. (2010). How central should the central bank be? Journal of Economic Literature, 48(1), 123–133. 10.1257/jel.48.1.123

- Blundell, R., & Bond, S. (1998). Initial conditions and moment restrictions in dynamic panel data models. Journal of Econometrics, 87(1), 115–143. 10.1016/S0304-4076(98)00009-8

- Bodea, C., & Hicks, R. (2015a). International finance and central bank independence: institutional diffusion and the flow and cost of capital. The Journal of Politics, 77(1), 268–284. 10.1086/678987

- Bodea, C., & Hicks, R. (2015b). Price stability and central bank independence: discipline, credibility, and democratic institutions. International Organization, 69(1), 35–61. 10.1017/S0020818314000277

- Bostandzic, D., & Weiß, G. N. F. (2018). Why do some banks contribute more to global systemic risk? Journal of Financial Intermediation, 35, 17–40. 10.1016/j.jfi.2018.03.003

- Brambor, T., Clark, W. R., & Golder, M. (2006). Understanding interaction models: improving empirical analyses. Political Analysis, 14(1), 63–82. 10.1093/pan/mpi014

- Brunnermeier, M., Dong, G. N., & Palia, D. (2012). Banks’ non-interest income and systemic risk. AFA 2012 Chicago meetings paper. https://ssrn.com/abstract=1786738

- Chodorow-Reich, G. (2014). The employment effects of credit market disruptions: firm-level evidence from the 2008–9 financial crisis *. The Quarterly Journal of Economics, 129(1), 1–59. 10.1093/qje/qjt031

- Čihák, M. (2006). Central banks and financial stability: a survey of financial stability reports. Paper presented at the Presentation: Seminar on Current Developments in Monetary and Financial Law.

- Conway, P. (2006). The international monetary fund in a time of crisis: a review of Stanley fischer’s IMF essays from a time of crisis: the international financial system, stabilization, and development. Journal of Economic Literature, 44(1), 115–144. 10.1257/002205106776162690

- Cragg, J. G., & Donald, S. G. (2009). Testing identifiability and specification in instrumental variable models. Econometric Theory, 9(2), 222–240. 10.1017/S0266466600007519

- Crockett, A. D. (1997). Why is financial stability a goal of public policy? Paper presented at the proceedings-economic policy symposium-Jackson Hole, Wyoming August 28–30, 1997.

- Cukierman, A., Web, S. B., & Neyapti, B. (1992). Measuring the Independence of central banks and its effect on policy outcomes. The World Bank Economic Review, 6(3), 353–398. 10.1093/wber/6.3.353

- Cukierman, A., & Webb, S. B. (1995). Political influence on the central bank: international evidence. The World Bank Economic Review, 9(3), 397–423. 10.1093/wber/9.3.397

- Cukierman, A. (2008). Central bank Independence and monetary policymaking institutions — Past, present and future. European Journal of Political Economy, 24(4), 722–736. 10.1016/j.ejpoleco.2008.07.007

- Danı́elsson, J. (2002). The emperor has no clothes: limits to risk modelling. Journal of Banking & Finance, 26(7), 1273–1296. 10.1016/S0378-4266(02)00263-7

- Das, U., Quintyn, M., & Chenard, K. (2004). Does regulatory governance matter for financial system stability? An empirical analysis. IMF Working Paper 04/89. International Monetary Fund.

- De Haan, J., & Siermann, C. L. J. (1996). Central bank Independence, inflation and political instability in developing countries. The Journal of Policy Reform, 1(2), 135–147. 10.1080/13841289608523360

- Demirgüç-Kunt, A., & Detragiache, E. (1998). The determinants of banking crises in developing and developed countries. Staff Papers, 45(1), 81–109. 10.2307/3867330

- Demirgüç-Kunt, A., & Detragiache, E. (2002). Does deposit insurance increase banking system stability? An empirical investigation. Journal of Monetary Economics, 49(7), 1373–1406. 10.1016/S0304-3932(02)00171-X

- Detragiache, M. E., & Demirgüç-Kunt, A. (1998). Financial liberalization and financial fragility. International Monetary Fund.

- DeYoung, R., & Roland, K. P. (2001). Product mix and earnings volatility at commercial banks: evidence from a degree of total leverage model. Journal of Financial Intermediation, 10(1), 54–84. 10.1006/jfin.2000.0305

- Doumpos, M., Gaganis, C., & Pasiouras, F. (2015). Central bank Independence, financial supervision structure and bank soundness: An empirical analysis around the crisis. Journal of Banking & Finance, 61, S69–S83. 10.1016/j.jbankfin.2015.04.017

- Dreher, A. (2004). Does the IMF cause moral hazard? A critical review of the evidence. International Finance.

- Dreher, A., Sturm, J.-E., & de Haan, J. (2008). Does high inflation cause central bankers to lose their job? Evidence based on a new data set. European Journal of Political Economy, 24(4), 778–787. 10.1016/j.ejpoleco.2008.04.001

- Dreher, A., & Walter, S. (2010). Does the IMF help or hurt? The effect of IMF programs on the likelihood and outcome of currency crises. World Development, 38(1), 1–18. 10.1016/j.worlddev.2009.05.007

- Dungey, M., Flavin, T., O’Connor, T., & Wosser, M. (2022). Non-financial corporations and systemic risk. Journal of Corporate Finance, 72, 102129. 10.1016/j.jcorpfin.2021.102129

- Eijffinger, S. C., & De Haan, J. (1996). The political economy of central-bank Independence. Special Papers in International Economics 19. Princeton, NJ: Economics Department, Princeton University.

- Engle, R. F., Moshirian, F., Sahgal, S., & Zhang, B. (2014). Banks non-interest income and global financial stability. CIFR Paper(015), 1–56.

- Farhi, E., & Tirole, J. (2012). Collective moral hazard, maturity mismatch, and systemic bailouts. American Economic Review, 102(1), 60–93. 10.1257/aer.102.1.60

- Fazio, D. M., Silva, T. C., Tabak, B. M., & Cajueiro, D. O. (2018). Inflation targeting and financial stability: Does the quality of institutions matter? Economic Modelling, 71, 1–15. 10.1016/j.econmod.2017.09.011

- Fu, X., Lin, Y., & Molyneux, P. (2014). Bank competition and financial stability in Asia Pacific. Journal of Banking & Finance, 38, 64–77. 10.1016/j.jbankfin.2013.09.012

- Gandhi, P., & Lustig, H. (2015). Size anomalies in U.S. bank stock returns. The Journal of Finance, 70(2), 733–768. 10.1111/jofi.12235

- Garriga, A. C. (2016). Central bank independence in the world: A new data set. International Interactions, 42(5), 849–868. 10.1080/03050629.2016.1188813

- Garriga, A. C., & Rodriguez, C. M. (2019). More effective than we thought: Central bank Independence and inflation in developing countries. Economic Modelling, 85, 87–105. 10.1016/j.econmod.2019.05.009

- Goldstein, M. (2001). IMF structural conditionality: how much is too much?: Tech. rep., Peterson Institute for International Economics.

- Goodhart, C. A. E. (2008). The regulatory response to the financial crisis. Journal of Financial Stability, 4(4), 351–358. 10.1016/j.jfs.2008.09.005

- Hoggarth, G., Reis, R., & Saporta, V. (2002). Costs of banking system instability: some empirical evidence. Journal of Banking & Finance, 26(5), 825–855. 10.1016/S0378-4266(01)00268-0

- Hutchison, M., & McDill, K. (1999). Are all banking crises alike? The Japanese experience in international comparison. Journal of the Japanese and International Economies, 13(3), 155–180. 10.1006/jjie.1999.0427

- IMF. (2009). Global financial stability report: Responding to the financial crisis and measuring systemic risks. https://www.imf.org/en/Publications/GFSR/Issues/2016/12/31/Global-Financial-Stability-Report-April-2009-Responding-to-the-Financial-Crisis-and-22583

- Jiang, L., Levine, R., & Lin, C. (2017). Does competition affect bank risk? National Bureau of Economic Research Working Paper Series, No. 23080. http://www.nber.org/papers/w23080

- Jorra, M. (2012). The effect of IMF lending on the probability of sovereign debt crises. Journal of International Money and Finance, 31(4), 709–725. 10.1016/j.jimonfin.2012.01.010

- Karolyi, G. A., Sedunov, J., & Taboada, A. G. (2018). Cross-border bank flows and systemic risk. Available at SSRN 2938544.

- Keeley, M. (1990). Deposit insurance, risk, and market power in banking. The American Economic Review, 80 (5), 1183–1200. http://www.jstor.org/stable/2006769

- Khan, A. H., Khan, H. A., & Dewan, H. (2013). Central bank autonomy, legal institutions and banking crisis incidence. International Journal of Finance & Economics, 18(1), 51–73. 10.1002/ijfe.456

- Klomp, J., & de Haan, J. (2009). Central bank independence and financial instability. Journal of Financial Stability, 5(4), 321–338. 10.1016/j.jfs.2008.10.001

- Klomp, J., & De Haan, J. (2010). Inflation and central bank independence: A meta-regression analysis. Journal of Economic Surveys, 24(4), 593–621. 10.1111/j.1467-6419.2009.00597.x

- Laeven, L., & Valencia, F. (2013). Systemic banking crises database. IMF Economic Review, 61(2), 225–270. 10.1057/imfer.2013.12

- Laeven, L., Ratnovski, L., & Tong, H. (2016). Bank size, capital, and systemic risk: some international evidence. Journal of Banking & Finance, 69, S25–S34. 10.1016/j.jbankfin.2015.06.022

- Laeven, L., & Valencia, F. (2018). Systemic banking crises revisited. International Monetary Fund working paper.

- Marcus, A. J. (1984). Deregulation and bank financial policy. Journal of Banking & Finance, 8(4), 557–565. 10.1016/S0378-4266(84)80046-1

- Marshall, M., Gurr, T. R., & Jaggers, K. (2019). Polity IV project: political regime characteristics and transitions, 1800-2018. dataset. Center for Systemic Peace. Accessed October, 20, 2019 http://www.systemicpeace.org/polityproject.html

- Nguyen, C. P., Le, T.-H., & Su, T. D. (2020). Economic policy uncertainty and credit growth: evidence from a global sample. Research in International Business and Finance, 51, 101118. 10.1016/j.ribaf.2019.101118

- Nguyen, D. N. (2020). Bank competition and financial soundness. Thesis (Ph.D.)Western Sydney University,

- Oberdabernig, D. A. (2013). Revisiting the effects of IMF programs on poverty and inequality. World Development, 46, 113–142. 10.1016/j.worlddev.2013.01.033

- Olea, J. L. M., & Pflueger, C. (2013). A robust test for weak instruments. Journal of Business and Economic Statistics, 31(3), 358–369. 10.1080/00401706.2013.806694

- Oosterloo, S., & de Haan, J. (2004). Central banks and financial stability: A survey. Journal of Financial Stability, 1(2), 257–273. 10.1016/j.jfs.2004.09.002

- Padoa-Schioppa, T. (2003). Central banks and financial stability: Exploring the land in between. Second ECB Central Banking Conference, “The transformation of the European financial system”, 25, 269–310.

- Papi, L., Presbitero, A. F., & Zazzaro, A. (2015). IMF lending and banking crises. IMF Economic Review, 63(3), 644–691. 10.1057/imfer.2015.16

- Phan, D. H. B., Iyke, B. N., Sharma, S. S., & Affandi, Y. (2020). Economic policy uncertainty and financial stability–Is there a relation? Economic Modelling, 94, 1018–1029. 10.1016/j.econmod.2020.02.042

- Praet, P., & Nguyen, G. (2008). Overview of recent policy initiatives in response to the crisis. Journal of Financial Stability, 4(4), 368–375. 10.1016/j.jfs.2008.09.008

- Saunders, A., Schmid, M., & Walter, I. (2020). Strategic scope and bank performance. Journal of Financial Stability, 46, 100715. 10.1016/j.jfs.2019.100715

- Schinasi, G. J. (2003). Responsibility of central banks for stability in financial markets. IMF working paper 03/121. Washington: International Monetary Fund.

- Silva, W., Kimura, H., & Sobreiro, V. A. (2017). An analysis of the literature on systemic financial risk: A survey. Journal of Financial Stability, 28, 91–114. 10.1016/j.jfs.2016.12.004

- Silva-Buston, C. (2019). Systemic risk and competition revisited. Journal of Banking & Finance, 101, 188–205. 10.1016/j.jbankfin.2019.02.007

- Vaubel, R. (1983). The Moral Hazard of IMF Lending. The World Economy, 6(3), 291–304. 10.1111/j.1467-9701.1983.tb00015.x