?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

Sub-Saharan Africa (SSA) ranks lowest globally in respect of energy access rates. The resulting high energy poverty impedes sustainable economic growth and aggravates the overall poverty which is prevalent in SSA countries. A better understanding of the relationship between financial development and energy consumption can contribute to enhancing sustainable development in SSA. The existing literature presents conflicting evidence regarding this relationship. Our objective is to investigate the symmetric and asymmetric relationships between financial development and energy consumption in SSA, using annual data from 1990 to 2016. The Autoregressive Distributed Lag (ARDL) panel estimator was employed to test for the linear relationship and symmetric effects of the long-run and short-run coefficients. The asymmetry was determined by decomposing financial development into positive and negative components, employing the non-linear ARDL (NARDL) method. The results reveal that a positive financial development shock is positively linked with energy consumption in the long-run implying that further financial development intensifies energy consumption. Results of the negative shock in financial development is positively linked with energy consumption in the long-run implying that the reduction in financial development could decrease energy consumption.

PUBLIC INTEREST STATEMENT

The relationship between financial development and energy consumption has been extensively discussed in developing countries. However, the results remain inconclusive and ambiguous due to conflicting views from prior researchers. Some researchers consider that increasing financial development increases energy consumption. Contrary, other researchers view that more financial development reduces energy consumption. Therefore, it is crucial that we investigate the asymmetrical link between financial development and energy consumption in SSA. To the best of our knowledge, this study makes the following novel contributions. First, we examine the link between financial development and energy consumption by addressing the issue of poverty being worsened by the lack of energy access in SSA. Second, we analyse the asymmetric nature of the relationship between financial development and energy consumption from an SSA perspective. Third, we incorporate the broad-based financial development index of the IMF in the context of financial development and energy consumption studies in SSA. We hope that our study can assist policymakers in coming one step closer to achieving Sustainable Development Goal (SDG) 7, namely “to ensure access to affordable, reliable, sustainable and modern energy for all” in SSA.

1. Introduction

1.1. Background and significance

The 2021 United Nations Climate Change Conference held in Glasgow (COP26) recognised that climate change has reached a crisis point. The resulting Glasgow Climate Pact represents a renewed commitment by nearly 200 countries to accelerate climate change action, especially for the “phasedown of unabated coal power and phase-out of inefficient fossil fuel subsidies” (UNFCCC, Citation2021). Another outcome was the establishment of the new Global Energy Alliance for People and Planet (GEAPP) to facilitate investments for the green energy transition in developing and emerging economies (African Development Bank [AfDB], Citation2021). In particular, the GEAPP aims to accelerate access to electricity in pursuit of ending global energy poverty (African Development Bank [AfDB], Citation2021).

Broadly defined, energy poverty refers to a level of energy consumption that does not adequately meet specific basic needs (González-Eguino, Citation2015). Globally, sub-Saharan Africa (SSA) countries perform the worst when it comes to energy access rates (Corfee-Morlot et al., Citation2019). The resulting energy poverty impedes sustainable economic growth and aggravates the overall poverty which is prevalent in SSA countries (Michoud & Hafner, Citation2021). In fact, the International Energy Agency (IEA) found that over half of SSA lacks electricity and one-third rely on traditional fuels (International Energy Agency (IEA), Citation2019b).

This severe shortage of energy and difficulties in accessing energy in the region may be attributed to a lack of investments in energy technologies (International Energy Agency (IEA), Citation2019a). Consequently, economic and sustainable development are negatively impacted, which is evident in that the region still relies upon unsustainable energy sources and outdated power generation plants (International Energy Agency (IEA), Citation2019b; Avila et al., Citation2017; Kaunda et al., Citation2012). These poorly maintained and outdated power plants have become weak and unable to meet demand from consumers (Castellano et al., Citation2015), thereby occasioning energy conservation policies such as the load shedding practices that have affected most SSA countries (International Energy Agency (IEA), Citation2020; Electricity Supply Commission [Eskom, Citation2019; Bhatia & Angelou, Citation2015). It is for these reasons that the SSA context is the focus of this study.

Energy dilemmas in SSA are exacerbated by the restriction of power generation from the private sector (Eberhard et al., Citation2011). However, the initiative from Power Africa to allow private investments in African energy markets has improved the energy consumption levels in Ghana, Ethiopia, Kenya, Tanzania, and Nigeria (African Development Bank [AfDB], Citationn.d.). South Africa has also recently relaxed restrictions to allow private investors to generate electricity of up to 100 megawatts (MW; Burkhardt & Mbatha, Citation2021), which can supply energy to about 80 000 households (USAID, Citation2021). These initiatives are an indication that, regardless of the difficulties in accessing energy, SSA is still working towards the United Nations agenda to provide universal, affordable, and clean energy by 2030 (United Nations Development Programme (UNDP), Citation2015).

1.2. Problem statement

Financial development has emerged as an important factor driving countries’ economic progress, alongside rapid production that has increased energy consumption (Kihombo et al., Citation2022). Furthermore, financial development is linked to novel technologies that improve energy consumption (Shahbaz et al., Citation2017), which, in turn, is dependent upon on economic expansion (Danish & Ulucak, Citation2021; Komal & Abbas, Citation2015).

The financial sector is influenced by reform strategies, financial openness, structural changes, financial crises, energy prices, and inflation (Boufateh & Saadaoui, Citation2020; Çoban & Topcu, Citation2013; Mahalik et al., Citation2017), which all play a significant role in the consumption of energy. In that regard, the relationship between financial development and energy consumption is a subject that has been widely discussed in developing countries (Nkalu et al., Citation2020; Ma & Fu, Citation2020; Destek, Citation2018; Odusanya et al., Citation2016; Ali et al., Citation2015; Chang, Citation2015; Islam et al., Citation2013; Sadorsky, Citation2010). The discussion has escalated to an investigation into how the financial system can reduce costs incurred in the financial sector, thereby enabling investments in energy consumption.

The financial industry in SSA—in particular the banking sector—has improved, as is evidenced by a rapid growth in the region’s economic activities in recent years (European Investment Bank (EIB), Citation2016). This could partly be the result of enhanced financial reforms (Danish & Ulucak, Citation2021). Consequently, financial institutions can provide households and businesses with loans to purchase energy-intensive goods, which are used to increase energy consumption (Chang, Citation2015; Danish & Ulucak, Citation2021).

The question then arises as to the nature of the relationship between financial development and energy consumption, i.e. how does a growing economy contribute to energy consumption?

1.3. Research objective and contributions

By focusing our attention on the link between financial development and energy consumption, greater insights might be gleaned as to how policymakers and the financial sector could support sustainable development in SSA. However, as will be seen from the ensuing literature review, the existing body of knowledge presents conflicting evidence regarding the association between financial development and energy consumption.

Accordingly, our objective is to test whether this relationship is symmetric or asymmetric by applying a panel NARDL approach from 1990 to 2016 for 21 SSA countries. This study makes three significant contributions, in that we undertake to address a contextual gap, narrow an empirical gap, and employ a novel measure of financial development.

First, a contextual gap is identified among the studies of Nkalu et al. (Citation2020), Odusanya et al. (Citation2016), and Ali et al. (Citation2015) who investigated the relationship between financial development and energy consumption in SSA. These studies motivated energy efficiency and conservation policies within high industrialised economies. Our study does not consider energy conservation, but instead addresses the issue of poverty being aggravated by a lack of energy access (Michoud & Hafner, Citation2021). To the best of our knowledge, the prior studies ignore the highlighted analysed variables for selected SSA economies.

Second, an empirical gap is ascertained in prior studies that examined financial development and energy consumption, as these only employed symmetric approaches to explore the drivers of energy consumption (see, for example, Nkalu et al., Citation2020; Ma & Fu, Citation2020; Destek, Citation2018; Odusanya et al., Citation2016; Ali et al., Citation2015; Chang, Citation2015; Islam et al., Citation2013; Sadorsky, Citation2010). Ahmed et al. (Citation2021) draw attention to the methodological weakness of studies which only use symmetric methods, as macroeconomic variables can also display asymmetric properties. For example, asymmetries may surface between financial development and economic globalization (Ahmed et al., Citation2021), which could affect energy consumption. This paper therefore uses both symmetric and asymmetric methods to probe the impact of financial development on energy consumption by applying the NARDL model posited by Shin et al. (Citation2014). As best we could determine, this is the first study to analyse the link between financial development and energy consumption in SSA, using both the symmetric and asymmetric ARDL methods.

Third, a novel contribution of this study is the use of a broad-based measure of financial development (financial development index) computed by the International Monetary Fund. The index amalgamates the financial development characteristics of depth, access, and efficiency (Svirydzenka, Citation2016).Footnote1 To the best of our knowledge, this study makes a novel contribution by incorporating the broad-based financial development index in the context of financial development and energy consumption SSA studies.

Energy is one of the major input elements in the production, distribution, and consumption of most goods and services and is therefore vital for promoting economic growth (Danish & Ulucak, Citation2021; Hong et al., Citation2019; Liu et al., Citation2018; Sadorsky, Citation2010). As such, analysing the issues that influence energy consumption may assist officials to formulate energy policies that could balance the connection between financial development, economic growth, energy access, energy poverty, and industrialization.

The remainder of the paper is organised as follows. Section 2 provides a review of the pertinent literature. Section 3 describes the methodological approach. In section 4 we report the main results. Lastly, section 5 discusses the policy implications of our main findings and reaches a conclusion.

2. Literature review

2.1. Theoretical literature

SSA is endowed with energy resources—especially renewable energy sources—but these remain largely untapped (”Africa up close,” Citation2018). This shortage of energy access (Corfee-Morlot et al., Citation2019) and inefficient energy utilization (Ozdeser et al., Citation2021) may discourage higher energy consumption levels when compared to the global market (Hafner et al., Citation2018). Energy economics literature presents conflicting views on the relationship between financial development and energy consumption. Some researchers are of the opinion that an increase in financial development increases the consumption of energy. This notion has its origin in the research of Karanfil (Citation2009) and subsequently, Sadorsky (Citation2010) in respect of emerging economies; Sadorsky (Citation2011) pertaining to European frontier economies; Zhang et al. (Citation2011) concerning China; Shahbaz and Lean (Citation2012) in the case of Tunisia; and Ozturk and Acaravci (Citation2013) in consideration of Turkey. Similar views are held by Islam et al. (Citation2013) regarding Malaysia; Al-mulali and Lee (Citation2013) concerning the Gulf Cooperation Council (GCC) countries; and Aslan et al. (Citation2014) in respect of Middle Eastern countries. Similarly, Chang (Citation2015) reached the same conclusion in an examination of 53 low-income countries, as did Ma and Fu (Citation2020) in their global analysis of 120 developed and developing countries.

The consumption of energy rises because a well-developed financial system can allocate low-cost credit to enterprises (Ahmad et al., Citation2022; Danish & Ulucak, Citation2021; Durusu-Ciftci et al., Citation2020; Ma & Fu, Citation2020). Consequently, enterprises use the credit to facilitate the expansion of their production scale and thereby increase energy consumption (Ma & Fu, Citation2020). Financial development can also be achieved directly by financial intermediation. In this case, consumers are assisted to easily access cheap loans to buy energy-intensive goods (Sadorsky, Citation2010). Goods such as cars, machinery, refrigerators, washing machines, and electric stoves use a lot of energy and increase energy consumption. Further, the provision of risk spread for both enterprises and consumers may expand wealth and stability in an economy and lead to an increase in demand for energy-intensive goods (Durusu-Ciftci et al., Citation2020). The financial sector also provides funding to the central government, which can use this money to expand the roll-out of public infrastructure such as hospitals and schools, thereby further boosting energy consumption (Danish & Ulucak, Citation2021).

However, other studies hold the view that an increase in financial development reduces energy consumption. This was the case for Islam et al. (Citation2013) in respect of Malaysia; Chang (Citation2015) in the context of high-income economies, Destek (Citation2015) concerning Turkey; Topcu and Payne (Citation2017) in an examination of 32 high-income countries, and Destek (Citation2018) in an analysis of 17 emerging economies.

Although banks in developing countries prefer short-term debt financing which carries less risk, energy-efficiency projects require long-term debt financing (Danish & Ulucak, Citation2021). The financial system, through the provision of low-cost credit, therefore enables manufacturing sectors to become more energy efficient, aiding them to become less energy intensive and ultimately leading to reduced energy consumption (Ma & Fu, Citation2020). In a similar vein, the adoption of energy efficient technologies in the pursuit of a clean energy transition as advocated for by COP26, could also reduce energy consumption (UNFCCC, Citation2021). In this approach, financial development could help enterprises increase investments into research and development (R&D), and plan and produce progressive, energy-efficient products, thereby decreasing total energy consumption.

Considering the variation in energy consumption, a possible non-linear relationship between financial development and energy consumption is expected. Nonlinearity could be influenced by increased depth in the financial sector, leading to increased energy consumption and thus further development of the financial system. However, once the financial system is developed, energy consumption may decline due to inflation in the economy, leading to fluctuating commodity costs (including energy prices). Thereafter, the financial sector monitors the allocation of resources for investment in energy technologies (Ma & Fu, Citation2020; Mahalik et al., Citation2017). Further, the financial crisis may also stimulate changes and uncertainties in the financial sector, variation in energy prices, and energy policies that can lead to structural changes (Mahalik et al., Citation2017), including a sectorial composition shift from the manufacturing process (Çoban & Topcu, Citation2013).

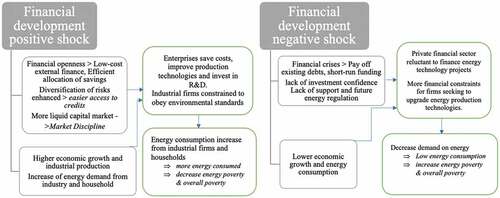

The hypothesis of the asymmetric relationship was established in the positive and negative shocks associated with financial development. A positive shock could be influenced by financial openness, in which foreign capital inflows can improve the financial sector (Boufateh & Saadaoui, Citation2020). This, in turn, encourages the development and diversification of funding sources for firms and financial institutions. The resulting financial stability enhances the allocation of low-cost credit for enterprises (Misati & Nyamongo, Citation2012) to improve and invest in R&D. Capital market liquidity can also be increased by reducing the cost of capital, due to increased competition in the credit market (Boufateh & Saadaoui, Citation2020). This could enable private sector participants to secure enough capital to invest in decentralized power grids, to increase capacity to supply consumers previously excluded from consuming energy. Easier access to credit encourages higher economic growth and more industrial productivity, which strengthens energy demand for industries and households. Access to credit is therefore improved, thereby stimulating energy consumption. As a result, energy poverty (and, eventually, overall poverty) may be lessened.

Further, financial development in SSA is an internal attribute that could be impacted by external shocks derived from reform strategies, structural changes, and other macroeconomic factors, such as economic booms, financial crises, energy prices, and inflation (Boufateh & Saadaoui, Citation2020). These external shocks will probably apply asymmetric effects to the financial development instruments, such as credit capacity for the private sector, liquidity, and stock market capitalization (Chen et al., Citation2020). Thereafter, stimulating financial development can instigate a non-linear asymmetric effect on energy consumption.

Financial crises can also affect a negative shock. This is evidenced by profit-maximizing financial institutions that, in reaction to the crises, employ careful strategies to preserve shareholder’s value and are consequently wary of financing innovative, but risky, projects (Boufateh & Saadaoui, Citation2020). External shocks would therefore economically constrain enterprises, as they fail to secure funds to invest in upgrading energy production technologies. It is assumed that short-term funding may not support the consumption of energy, as instability in the accumulated capital could only be sufficient to pay off the current debt. Due to the deleveraging process, mobilisation of funds becomes inefficient, to such an extent that the financial instability restrains low-cost credit, triggering reduced economic growth and energy production. This reduces energy demand for industries and households, giving rise to lower energy consumption. This, in turn, may intensify energy poverty and ultimately exacerbate overall poverty. below depicts this theorised asymmetric relationship between financial development and energy consumption.

Figure 1. Asymmetry hypothesis between financial development and energy consumption.

Adapted from Boufateh and Saadaoui (Citation2020).

2.2. Empirical literature

In the context of financial development and energy consumption, several studies have conducted an empirical investigation using panel data and time series estimation techniques. These studies can be divided into four sets, based on their main findings.

The first set of studies found that financial development increases the consumption of energy. Sadorsky (Citation2010, Citation2011) examined 22 emerging economies from 1990 to 2006 and nine Central and Eastern European countries from 1996 to 2006, respectively. Komal and Abbas (Citation2015) investigated Pakistan from 1972 to 2012. Kihombo et al. (Citation2021a) considered 11 West Asian and Middle East (WAME) economies from 1990 to 2017. Likewise, two related studies determined that ecological quality is weakened by a rise in financial development. In the first, Ahmed et al. (Citation2021) examined data from Japan over the period 1971 to 2016; in the second, Ahmad et al. (Citation2022) analysed 17 emerging countries from 1984 to 2017. These studies confirmed a positive relationship between financial development and energy consumption.

Other studies that investigated the finance-energy nexus and employed the ARDL approach include Rafindadi and Ozturk (Citation2016), who examined Japan from 1970 to 2012; and Mukhtarov et al. (Citation2017), who analysed Azerbaijan from 1992 to 2015. Moreover, Sbia et al. (Citation2017) conducted a United Arab Emirates (UAE) study for the period 1975 to 2011. In addition, Danish and Ulucak (Citation2021) examined data from Pakistan from 1990 to 2017 and concluded that energy consumption increases with financial development.

Similarly, Dumrul (Citation2018) explored Turkey, spanning from 1961 to 2015. Salahuddin and Ozturk (Citation2015) assessed the same nexus in GCC countries, using mean group (MG) and pool mean group (PMG). Further, Islam et al. (Citation2013) analysed Malaysia from 1971 to 2009, using the ARDL approach. These studies reached the same conclusion, namely that financial development increases the consumption of energy. It is therefore evident that the current economic conditions of a country influence the consumption of energy, despite the variation in estimation techniques used in the various studies.

In contrast, the second group of studies presented different results contending that increasing financial development reduces the consumption of energy. Farhani and Solarin (Citation2017) used the United States (US) quarterly data from 1973 to 2014. They determined that despite financial development improving energy demand in the short-run, the consumption of energy declined in the long-run. Similarly, Ouyang and Li (Citation2018) used quarterly panel data of 30 Chinese provinces from 1996 to 2015 and the results showed that financial development reduces energy consumption significantly. Gómez and Rodríguez (Citation2019) analysed North American Free Trade Agreement (NAFTA) countries from 1971 to 2015 and established a negative association between financial development and energy consumption. Interestingly, Destek (Citation2018) reported that the bond market is the most efficient indicator of reducing energy consumption. Conversely, Chiu and Lee (Citation2020) demonstrated that banking sector development has a larger impact on energy consumption compared with stock market development.

The third group of studies analysed the non-linear relationship between financial development and energy consumption (Shahbaz et al., Citation2016) obtained ambiguous results, and to solve the ambiguity, applied a non-linear model. It is worth noting that Sadorsky (Citation2010) reached a similar outcome, but ignored the existence of a non-linear relationship between financial development and energy consumption. Instead, the study used panel data and considered heterogeneity (differences in study outcome) across countries. It should be cautioned, however, that ignoring the non-linear relationship may result in an estimation bias, and may also lead to an unclear consensus on the relationship between financial development and energy consumption (Chang, Citation2015).

Shahbaz et al. (Citation2016) examined Pakistan from 1985 to 2014 and found a positive non-linear effect. Similarly, Mahalik et al. (Citation2017) affirmed the non-linear relationship between financial development and energy consumption in Saudi Arabia. Further, Baloch et al. (Citation2019) examined 25 Organisation for Economic Co-operation and Development (OECD) countries between 1980 to 2016 and found a positive non-linear (inverted U-shape) relationship. In a study of the Middle East and North African (MENA) countries, Gaies et al. (Citation2019) found financial development increases energy consumption with a non-linear effect. It could be inferred that energy demand first rises alongside financial development, culminates, and subsequently falls.

In addition, Chang (Citation2015) analysed 53 countries from 1999 to 2008 and found that energy consumption increased with financial development in low-income regimes, while it decreased slightly with financial development in high-income countries. However, energy consumption increased in high-income countries of emerging markets. Consequently, a non-linear negative relationship was established. Wang and Gong (Citation2020) found a positive threshold between financial development and energy consumption, with a non-linear effect in 30 Chinese provinces. Similarly, Chiu and Lee (Citation2020) analysed 79 countries from 1984 to 2015, finding a non-linear relationship between financial development and energy consumption.

The fourth group of studies focused their investigation on the association between financial development and energy consumption in SSA. Rafindadi and Ozturk (Citation2017) examined South Africa from 1970 to 2011 and found that financial development increases energy demand. Odusanya et al. (Citation2016) assessed Nigeria from 1971 to 2014, using the ARDL approach in the long-run and the short-run, and found that energy consumption increased with more financial development. This finding is corroborated by Lefatsa et al. (Citation2021) who also used the ARDL approach to investigate South Africa from 1980 to 2018. Kebede et al. (Citation2010) analyzed 20 SSA countries during the period 1980 to 2004, with regional differences leading to mixed results. Commercial and traditional energy demand increased in East, South, and West African countries with economic development, while the demand in Central African countries decreased with more economic development, therefore generating mixed results. Ozdeser et al. (Citation2021) studied Nigeria from 1960 to 2019 and found that increasing financial development (by way of stock market growth) reduces energy consumption. Nkalu et al. (Citation2020) found that financial development and energy consumption have a positive and significant relationship in SSA countries. However, Ali et al. (Citation2015) concluded that an increase in financial development reduced the consumption of energy in Nigeria.

In summary, the nexus between financial development and energy consumption has been examined by several researchers, with mixed results being found. Some researchers conclude that enhancing financial development increases energy consumption, while others contend that financial development reduces energy consumption. The disparity in findings could be initiated by the individual countries’ structural changes and policies in both energy consumption and financial development. The effect of the use of diverse explanatory variables, different indicators, and different estimation methods could also contribute to this inconsistency. Although various studies have investigated the non-linear relationship between financial development and energy consumption (Baloch et al., Citation2019; Chang, Citation2015; Chiu & Lee, Citation2020; Gaies et al., Citation2019; Mahalik et al., Citation2017; Shahbaz et al., Citation2016; Wang & Gong, Citation2020), they did not consider the asymmetric effect of financial development on energy consumption.

3. Methodology

3.1. Empirical model

The focus of this study is to investigate the possible asymmetric relationship between financial development and energy consumption, by controlling for economic growth, energy access, poverty, industrialization, foreign direct investment (FDI), and inflation. The empirical model is based on adaptations from studies of Sadorsky (Citation2010) and Chang (Citation2015) and is specified as follows:

Operational definitions from Equationequation (1)(1)

(1) used in this paper consist of the dependent variable (

which represents energy consumption, while

refers to financial development, which is the main explanatory variable of interest. The control variables (

represent standard explanatory variables of energy consumption. These explanatory variables comprise economic growth (

), energy access (

), poverty (

), industrialization

, FDI

, and inflation

, where

is the error term, and i and t represent the country and the time, respectively. The next section elaborates on these explanatory variables.

3.2. Theoretical underpinning of the model

Following the literature review, it is evident that the relationship between financial development and energy consumption is ambiguous. Some studies observed a negative relationship between financial development and energy consumption (Nkalu et al., Citation2020; Odusanya et al., Citation2016; Rafindadi & Ozturk, Citation2017; Shahbaz et al., Citation2013), whereas others determined a positive link (Ali et al., Citation2015; Al-mulali & Binti Che Sab, Citation2012). Therefore, the relationship between financial development and energy consumption remains unclear.

The relationship between economic growth and energy consumption is highly positively correlated (Mukhtarov et al., Citation2017). GDP—which is a proxy of economic growth—carries a positive component of energy utilization due to economic booms and output expansions (Richard, Citation2012). The a priori expectation between economic growth and energy consumption is positive. It could be asserted that a reduction in energy prices leads to increased energy access, which, in turn, results in more energy consumption (Chang, Citation2015). Thus, the a priori expectation concerning the link between energy access and energy consumption is positive.

The perception that poverty is associated with energy consumption has not been widely researched. Nonetheless, Nwani and Osuji (Citation2020) found energy consumption to bear a positive and significant impact on poverty reduction in SSA, implying that poverty reduction increases energy consumption. Therefore, this study anticipates a negative relationship between energy consumption and poverty. Kebede et al. (Citation2010) understood that sufficient access to energy could increase industrialization in the production process, thus indicating that industrialization may increase energy consumption. Recent industrial production places greater focus on reducing energy intensity to ensure low carbon emissions (Kebede et al., Citation2010). As a result, the energy consumption level is expected to decrease along with industrialization. Thus, the link between industrialization and energy consumption remains unclear.

The flow of FDI to developing countries can influence energy consumption and control emission standards by applying an advanced technological transfer in host countries (Qamruzzaman & Jianguo, Citation2020). Furthermore, the improvement of energy technologies promotes a reduction in energy consumption (Ma & Fu, Citation2020). Therefore, a negative relationship between FDI and energy consumption is expected. Abbas et al. (Citation2015) contend that inflation is positively correlated to energy consumption. summarises the explanatory variables in the paper with symbols, units of measurements, expected signs, and sources of data.

Table 1. Summary of variable descriptions, data sources, and expected signs

3.3. Data

This paper employed a panel dataset for the empirical analysis of 21 selected SSA countriesFootnote3 spanning the period from 1990 to 2016. Energy consumption is measured in kg of oil equivalent to primary energy sources. Data were extracted from International Monetary Fund (IMF; Citation2018), World Bank Indicators (WDI, Citation2016) and the International Energy Agency (IEA; Citation2016). Financial sector development consists of diverse financial characteristics, including the depth and efficiency of financial institutions and financial markets. The optimal measure of financial development is comprised of a comprehensive Financial Development Index from the IMF.

3.4. Estimation approach

The investigation of the link between financial development and energy consumption was conducted using the ARDL model developed by Pesaran and Shin (Citation1995). To achieve nonlinear asymmetric co-integration among the variables, the current study used the NARDL method developed by Shin et al. (Citation2014) and applied by the related studies of Qamruzzaman and Jianguo (Citation2020) and Boufateh and Saadaoui (Citation2020). This method incorporates a dynamic model and allows for the separation of variables between asymmetries in the short and long run. Additionally, the NARDL method is more reliable due to its advantages over other methods such as the Vector Error Correction Model (VECM) because it is not constrained by the integration order (Khan, Rehman et al., Citation2021; Pesaran et al., Citation2001). As a result, prior investigations that applied VECM were unable to establish an asymmetric link between variables (Kibria et al., Citation2021). Furthermore, the NARDL technique relaxes the integration order limitations, which state that the order for the error correction model must be the same (Kibria et al., Citation2021). Because of its flexibility, NARDL can be employed regardless of the type of integration (Khan, Rehman et al., Citation2021).

Difficulties associated with traditional cointegration techniques such as Engle and Granger (Citation1987) and Johansen and Juselius (Citation1990) are avoided. Furthermore, NADRL not only reveals short and long-run asymmetries but also how to uncover hidden cointegration (Shin et al., Citation2014). Finally, with the right interchange of lag durations in the model, any endogeneity and multicollinearity difficulties are avoided, rendering the method more adaptable than other techniques (Kibria et al., Citation2021; Pesaran et al., Citation2001; Shin et al., Citation2014).

The panel ARDL has become mainstream over the last few years for analyzing relationships among economic variables (Akinsola et al., Citation2017; Asongu et al., Citation2016). Although the model was developed for time series, to apply it to panel data, the financial development must be decomposed into increase and decrease for all countries and adopted for all cross-sections. It is considered the best model to account for long-run and short-run non-linearities introduced in regressors as positive and negative partial sum decompositions (Salisu & Isah, Citation2017; Shin et al., Citation2014). It can be asymmetric, as both the positive and negative partial sums introduced in the specification are unbalanced in instances where both positive and negative shocks are expected to produce a different impact on energy consumption.

3.5. The pool mean group (PMG) and the mean group (MG) estimators

Considering the diversity of SSA in the economic, environmental, and social sectors (GIZ, Citation2013), it is important to assess for possible heterogeneity. The MG estimator adopted by Pesaran and Smith (Citation1995) and the PMG estimator adopted by Pesaran et al., Citation1999) were considered for this study because the time series T and number of cross-sections N are both fairly large, and they also mitigate the endogeneity problem. Despite the positive characteristics in both the MG and PMG estimators, the PMG is further preferred over MG, due to unbiased tendencies resulting in shorter periods. In addition, the Hausman specification test determines the competence and consistency between PMG and MG estimators. If the null hypothesis cannot be rejected, the test suggests that the PMG estimator can be adopted, whereas a rejection of the null hypothesis indicates the adoption of the MG estimator. The basic structure of the model adopted from Pesaran et al. (Citation1999) motivating PMG estimation is represented as ARDL (p,q,q … .q) in Equationequation (2)(2)

(2) .

Where i = 1, 2, …, N; T = 1,2, …, T and N = no. of cross-section units; T = no. of years and is a vector of regressors for cross-section unit i;

represents individual fixed effects; whereas

, j = 1, …,p and

, j = 1,2 …,q represent scalars.

3.6. Stationarity

The next step is to determine the stationarity properties of the applied variables using the unit root tests (URTs) of Levin-Lin-Chu (LLC) and Im-Pesaran-Shin (IPS). These are first-generation URTs that apply homogeneous slopes. The first-generation URTs assume cross-sectional independence across units. The presence of unit roots is tested to warrant the series to be of order I(1) and not exceed order I(2) integration (Samargandi et al., Citation2015).

3.7. Cointegration

Variables in this paper are integrated of order I(1), thus the Pedroni cointegration test is best suited to examine the presence of a cointegrating relationship between energy consumptions and regressors. Pedroni posits a residual-based cointegration test for dynamic panels, in which the short-run and the long-run coefficients are allowed to differ across cross-sections (Akinsola & Odhiambo, Citation2020). The error correction equation, reparametrized from Equationequation (2)(2)

(2) , is specified to structure the long-run and short-run dynamics of the variables in response to the deviation from equilibrium, as provided by:

Where ;

;

(j = 1, 2, …,p-1);

and (j = 1, 2, …,q-1), if a = 1,2, …,N; t = 1,2, …,T,

refers to the first difference operator,

is the error correction used for short-run and long-run dynamics. Variables converge to long-run equilibrium in case of any disturbance. The estimate is deemed to be significantly negative, with the impression that the variables suggest a return to equilibrium if

, with no evidence of a long-run relationship. Equation

is the error correction term, representing the long-run model, whereas equation

signifies the short-run model. To account for energy consumption, financial development, and control variables used in the study, the Akaike Information Criterion (AIC) is used. The AIC of the ARDL (1, 1, 1, 1, 1, 1, 1, 1) is an enforced maximum lag length that uses the equation to establish the appropriate predictor. Therefore, the panel ARDL model is:

where is the energy consumption,

is financial development, ∝ is a vector of constants,

is the vector of explanatory variables of financial development, gross domestic per capita, energy access, poverty, industrialization, FDI, and inflation.

is the white noise error term, and

is the lag length. EquationEquation (5)

(5)

(5) outlines the dependent and independent variables in a model form, in which the general model is estimated for the panel of 21 countries.

It is anticipated that a non-linear energy consumption relationship may develop, at which point prior studies by Gaies et al. (Citation2019), Baloch et al. (Citation2019), Shahbaz et al. (Citation2017), Chai et al. (Citation2016), Chang (Citation2015), and Al-mulali and Lee (Citation2013) found inconclusive results when investigating the non-linearity. Therefore, this paper used different estimation methods and a multiple country sample of SSA countries to test for non-linearity. The next equation states the decomposition of financial development as a possible non-linear relationship to energy consumption as follows:

This study used the Wald test to investigate long-run (=

=

) and short-run (

=

=

) asymmetry. The financial development is decomposed in EquationEquation (6)

(6)

(6) as FD+ and FD− to represent the positive and negative components. Other variables remain unchanged, and the theoretical definitions of the decomposed financial development are:

4. Results and discussions

4.1. Descriptive statistics and correlation matrix

This paper measures the coefficient of variation CV (Std. dev/mean), which is the ratio of the standard deviation to the mean, used to interpret the relative magnitude of the standard deviation. Table presents the descriptive statistics of the data used in estimating the empirical model. The minimum and maximum values of the dependent variable in SSA are 1.009 and 31.291, respectively, presenting a significant variation in the consumption of energy. In terms of specific countries, South Africa recorded the highest mean value in energy consumption of 25.940, followed by Gabon with 18.789. In contrast, Senegal and Uganda recorded the lowest mean values of 2.528 and 3.222, respectively, implying that they consume the least energy. Overall, most countries in SSA are still at their initial stages of energy development, showing an average of 6.629. The minimum and maximum values of financial development at the country level are 1.883 and 61.781 for the DRC and South Africa, respectively, indicating that South Africa has progressed in its economic development and shows maturity levels.

Table 2. Summary of descriptive statistics

Skewness measures the lack of symmetry of the normal distribution in a dataset, and kurtosis determines the normality of values in a dataset. presents all variables to be positively skewed, and some variables show a kurtosis value of less than 3, indicating the presence of platykurtic values (fewer values close to the mean). The variables with a value of more than 3 present as leptokurtic (more values close to the mean). This implies that the dataset has a normal distribution, as the kurtosis values are less than 4 and the values are asymmetrical and do not coincide (Mishra et al., Citation2019).

4.2. Cross-sectional dependence test

To determine if the panel time-series data exhibit cross-sectional dependence (CD), the CD test devised by Pesaran (Citation2004) is used. Results from the Pesaran CD tests are presented in . Inspecting the related probability values, the null hypothesis of no cross-sectional dependence for energy consumption, financial development, economic growth, energy access, poverty, industrialization, foreign direct investment, and inflation cannot be rejected. This analysis indicates that the panel times series data exhibit no cross-sectional dependence. The investigation proceeds with panel methods that assume cross-sectional independence.

Table 3. Results from the Pesaran (Citation2004) cross-sectional Independence

4.3. Panel unit root stationarity test

The purpose of URTs for stationarity in variables is to avoid spurious regression in the panel. The URT results shown in reveal that some variables are non-stationary and became stationary at the first difference. Financial development, energy access, FDI, and inflation are of order I(0) and other variables are of order I(1). The order of integration is I(0) and I(1) in all series, indicating the suitability of the panel ARDL approach for estimation purposes. Results of the optimal lag selection were obtained during the first step of finding the lag length from the selected panel ARDL lag structure (1 0 0 0 0 0 0 0), which was determined across units by applying variables of interest to select the most common lag. The test was conducted based on the AIC.

Table 4. Unit root tests

4.4. Pedroni cointegration test

After the stationarity of variables was established from the URTs, the Pedroni cointegration test was conducted and the results are presented in . A total of seven statistics were employed and five of those statistics proved significant. The significant statistics from within-dimension comprise panel v, panel pp, and panel ADF, while between-dimension includes panel pp and panel ADF. Although panel v is significant in this paper, while insignificant in the studies of Akinsola and Odhiambo (Citation2020) and Asongu et al. (Citation2016), it does not change the overall results. As ascertained by Karaman-Örsal (Citation2007), the PP and ADF of the panel and group are the four statistics with the best performance and are further regarded to be more reliable (Asongu et al., Citation2016; Pedroni, Citation2004). Therefore, the panel pp, ADF, and group pp, ADF reject the null hypothesis of no cointegration at a 1% level of significance, indicating that the variables EC, FD, GDPK, EA, POV, IND, FDI, and INFL are cointegrated.

Table 5. Pedroni cointegration test results

4.5. Hausman specification test

The results displayed in indicate that the null hypothesis of the Hausman test cannot be rejected. Ultimately, this supports the PMG estimator as the most efficient and preferred estimator to analyse the linear and non-linear effects of financial development on energy consumption.

Table 6. Hausman test for long-run homogeneity

4.6. Symmetric effect of financial development on energy consumption

The linear transformations in present segments of Part A of the long-run estimates, while Part B represents short-run coefficients, comprised of financial development and its determinants to energy consumption. While the linear regression analysis predicts the value in energy consumption based on financial development, it must be noted that the results in focus on significant long-run estimates. This technique allows linearity and permits the impact variables to maintain their value (Beck & Jackman, Citation1998), to the extent that increasing financial development transforms the consumption of energy with the same value. This can be achieved by applying Equationequation (4)(4)

(4) of the ARDL estimation.

Table 7. Linear effect of financial development on energy consumption in 21 SSA countries

The PMG estimate for the long-run coefficient indicates a positive significant result at a 1% level in financial development to energy consumption. More precisely, a 1% increase in financial development will lead to a 0.12% increase in energy consumption in the long-run. The implication is that an increase in financial development expands economic activities associated with the rising consumption of energy. Increasing the consumption of energy may contribute to human development, which may enhance access to energy (United Nations Development Programme (UNDP), Citation2015). Enhancing energy access could also be perceived as reducing energy poverty, which, in turn, boosts energy security in the form of aggregate energy consumed by SSA countries in the long-run.

The correlation between energy consumption and increased financial development is due to the provision of credit by the financial sector (Danish & Ulucak, Citation2021). This credit is allocated to various sectors of the economy to buy energy-intensive goods (Durusu-Ciftci et al., Citation2020; Sadorsky, Citation2010) and public infrastructure (African Development Bank [AfDB], Citation2018; Danish & Ulucak, Citation2021) to increase energy consumption.

The overall result aligns with the findings of numerous researchers who have contemplated that an increase in financial development leads to an upsurge in energy consumption because an efficient, well-developed financial system has the potential to provide cheap loans to enterprises (see, Chang, Citation2015; Danish & Ulucak, Citation2021; Dumrul, Citation2018; Komal & Abbas, Citation2015; Ma & Fu, Citation2020; Mukhtarov et al., Citation2020, Citation2018; Nkalu et al., Citation2020; Odusanya et al., Citation2016; Sadorsky, Citation2010).

In contrast, energy consumption was found to decrease when financial development improved in China, Malaysia and member states of the South Asian Association for Regional Cooperation (SAARC) (Alam et al., Citation2015; Islam et al., Citation2013; Ouyang & Li, Citation2018). This could be suggestive of the fact that these countries have better access to more energy efficient equipment and technologies than their SSA counterparts.

Economic growth is negative and statistically significant at a 10% level, meaning increasing economic growth reduces energy consumption. The result contradicts the a priori expectation that economic growth is positively related to energy consumption. Among others, the findings of Al-Malkawi et al. (Citation2012), as well as Bernard and Austin (Citation2011), align with the outcome of the present study, namely that economic growth reduces energy consumption. However, according to Kihombo et al. (Citation2021b), this result might be biased. Jaforullah and King (Citation2017) also caution that the consideration of energy consumption and economic growth can lead to unreliable results.

Energy access is positive and statistically significant at a 1% level, meaning increasing energy access increases the consumption of energy. This result satisfies the a priori expectation that increased access positively impacts the consumption of energy.

FDI has a negative significant coefficient, which implies that the pressure on energy consumption is limited by increased access to foreign capital. The finding is that increasing FDI decreases energy consumption in the long-run. The a priori expectation for FDI and energy consumption is met and aligns with the result from Ma and Fu (Citation2020). The inflation coefficient for energy consumption is positive and significant at a 1% level. The result is consistent with the outcome from Abbas et al. (Citation2015). The sign of the error correction term in part B is negative and statistically significant, as expected. The implication is that any shock to the system is temporal and the variables will converge to their long-run equilibrium. Moreover, all short-run coefficients are insignificant.

4.7. Asymmetric effect of financial development on energy consumption

The analysis of the NARDL long-run and short-run estimates is presented in . These estimates indicate segments of Part A for the long-run and Part B for short-run coefficients, comprised of financial development variables that are decomposed for positive and negative shocks. The positive and negative changes in financial development impact energy consumption, indicated by the coefficient sign and size as FD_POS and FD_NEG indexes. The indexes allow for a non-linear relationship, which is vital for the independent variable of interest, as increases or decreases will have a different impact on the dependent variable (Apergis & Gangopadhyay, Citation2020).

Table 8. Non-linear effect on financial development & energy consumption in 21 SSA countries

It must, however, be noted that results in focus on significant long-run estimates. The asymmetric effect becomes evident during the initial act of decomposing the financial development into positive and negative components. Thereafter, the formal test of asymmetry confirms the non-linearity. It shows a positive significant statistical effect at a 10% level in the long term, meaning the null hypothesis of no asymmetry is rejected. This confirms the asymmetric effect between financial development and energy consumption. The long-run results show that the positive shock in financial development is positively linked with energy consumption. The implication is that further improvement in financial development will increase demand for energy consumption. The results in the long-run also reveal that the negative shock in financial development is positively linked with energy consumption, which suggests that reduced financial development can ease the energy consumption demand. The effects of the positive and negative shocks in financial development on energy consumption are in line with the findings of Qamruzzaman and Jianguo (Citation2020) for a sample of lower and middle-income countries.

The financial development positive shock positively linked to energy consumption suggests that further financial development should be encouraged. Sources of funding for firms and financial institutions could be improved and diversified, leading to financial stability that enhances the allocation of low-cost credit for enterprises (Misati & Nyamongo, Citation2012). Due to financial intermediation, consumers could receive cheap loans to buy energy-intensive goods such as cars and machinery (Danish & Ulucak, Citation2021; Sadorsky, Citation2010) to increase energy consumption. The provision of credit to finance energy projects could support the private sector in purchasing new power plants and expanding energy access (European Investment Bank (EIB), Citation2018). In turn, enterprises would be able to improve and invest in R&D, observe environmental standards, and increase energy sources. A greater variety of energy sources for both industries and households could, therefore, result in more energy consumption, which ultimately reduces energy poverty and may contribute to poverty reduction in SSA.

The negative financial development shock could be affected by financial crises leading to distress in the financial sector. A negative shock could also lead to a lack of credit access and reduced financial development, which may reduce demand for energy consumption. A negative financial shock further implies financial instability, as credit is not liquid enough to finance countries in SSA with additional total primary energy sources, resulting in decreased energy consumption in the long-run.

As pointed out earlier, a reduction in financial development can negatively affect the consumption of credit-related services and energy-intensive goods (Chang, Citation2015; Danish & Ulucak, Citation2021), as well as impede the provision of public infrastructure (African Development Bank [AfDB], Citation2018; Danish & Ulucak, Citation2021). In the same way, poorly performing stock markets signal delayed growth, thereby eroding investor confidence. In addition, if the COP26 decision to terminate inefficient fossil fuel subsidies and scale down coal usage is implemented, a reduction in energy consumption could follow. Thus, both production and consumption activities are curtailed, resulting in reduced energy consumption.

Within this context, the deleveraging process restricts the mobilisation of funds and restrains low-cost credit, leading to reduced economic growth and energy production. Financial instability inhibits the level of energy consumption, which may, in turn, worsen energy poverty and ultimately overall poverty. These findings support an earlier statement that the lack of access to low credit in SSA (Organisation for Economic Co-operation and Development/The World Bank/UN Environment, Citation2019) restricts the provision of cheap capital rates to improve energy consumption and reduce energy poverty. It is therefore posited that the financial development negative shock instigated by financial crises can lead to an emergence of risks and losses (Boufateh & Saadaoui, Citation2020).

Our findings demonstrate that energy consumption differs significantly depending on whether the financial development is negative or positive. The results also indicate asymmetry in terms of the sign of the coefficients. It can therefore be concluded that financial development has an asymmetric effect on energy consumption in SSA countries. Majeed et al. (Citation2020) supports this notion, and also points out that asymmetry is present with different significance, elasticity direction, and the variation in financial development.

All other variables under study are significant at a 1% level, representing strong evidence of significant coefficients. Economic growth is a strong and significant contributor to increasing energy consumption. This coefficient differs from the one obtained from the ARDL model. A positive and significant economic growth coefficient indicates that, as growth increases, the consumption of energy also increases. This result is in line with the conclusions reached by Chen et al. (Citation2020), Chang (Citation2015), and Sadorsky (Citation2010). The coefficient of energy access is positive and significant, meeting the a priori expectation. It could further be surmised that a reduction in energy prices leads to increased energy access, which allows for greater energy consumption. The previous finding is in line with Chang (Citation2015) and Jacobs and Šlaus (Citation2011). The poverty coefficient is negative and significant, meaning an increase in poverty reduces energy consumption. This meets the a priori expectation of a negative relationship and supports the Nwani and Osuji (Citation2020) finding.

Poverty is a substantial determinant of energy consumption, evidenced by the fact that an increase in energy consumption is associated with the eradication of poverty on the Human Development Index (HDI). The industrialization coefficient is negative and significant at a 1% level, implying an increase in industrialization may result in decreased consumption of energy (Kebede et al., Citation2010).

FDI is found to have a significant negative relationship with energy consumption. Although financial development attracts more FDI, which is invested in the R&D, design, and production of energy technologies (Boufateh & Saadaoui, Citation2020), it does not improve energy consumption in SSA. Inflation is significantly positively related to energy consumption, in line with the finding of Abbas et al. (Citation2015). Regarding cointegration, the error correction term signifying the speed of adjustment is negative and significant, thereby satisfying the theoretical requirement. The outcome shows that the null hypothesis of no cointegration between financial development and energy consumption is rejected.

5. Conclusion, policy implications, and recommendations

Our research objective was to investigate the symmetric and asymmetric relationships between financial development and energy consumption in 21 SSA countries, using annual data from 1990 to 2016. Energy economics literature presents conflicting views, as some researchers suggest that financial development intensifies the consumption of energy, while others contend that energy consumption is reduced. Regarding a possible symmetric relationship, we found that an increase in financial development results in more energy consumption in the long-run.

We also demonstrate findings of a non-linear asymmetric effect of financial development on energy consumption. Financial development positive shock is positively linked with energy consumption in the long-run. The implication is that further improvement in financial development will increase demand for energy consumption which may reduce energy poverty. It also suggests that financial stability influences the availability of credit which, in turn, boosts energy consumption. Results of the negative financial development shock show a positive coefficient in the long-run, which represents a stronger effect on energy consumption than the positive financial development shock. This indicates that financial instability can decrease energy consumption, which may intensify energy poverty. Both the positive and negative results are indicative of an asymmetric relationship between financial development and energy consumption, due to the variation in magnitude of financial development.

Consequently, we discuss various policy implications for SSA governments and put forward several proposals for overcoming barriers to energy access and energy consumption.

First, the playing field between renewable energy and traditional fossil fuel-based generation should be levelled in terms of profitability (”Africa up close,” Citation2018). This can be done by ceasing fossil fuel subsidies, as was aspired to by COP26. Instead, subsidies can be redirected to invest in renewable energy generation projects, which are more beneficial and likely to materialise in the medium to long term and accumulate at the country level (”Africa up close,” Citation2018).

Second, private sector investment in electricity generation should be encouraged. Governments must cut regulatory red tape by providing easy, competitive access to markets and electricity grids (”Africa up close,” Citation2018). Setting strong, national policy targets for renewable energy production will foster confidence among private sector participants and make future public incentive mechanisms more dependable and trustworthy for investors (”Africa up close,” Citation2018). An added benefit is the easing of the present overload on national power grids that struggle to meet consumer demand. Furthermore, the decentralization of power grids will likely improve energy demand and increase energy consumption to acceptable levels (Michoud & Hafner, Citation2021). Investments in solar decentralization, especially, can be used to enhance energy access and domestic capacity (Corfee-Morlot et al., Citation2019). Energy efficient measures can also encourage the transfer of energy-intensive technology that may increase energy consumption and reduce poverty in SSA.

Third, efforts to develop the financial sector within the SSA region should be ramped up. As previously pointed out, external shocks have obstructed financial development (Boufateh & Saadaoui, Citation2020; Chen et al., Citation2020) and have hampered the consumption of energy-intensive goods and curtailed spending on public infrastructure (African Development Bank [AfDB], Citation2018; Chang, Citation2015; Danish & Ulucak, Citation2021; Durusu-Ciftci et al., Citation2020; Sadorsky, Citation2010). Concomitantly, growth is delayed in poor-performing stock markets, which hinders investors. As such, the majority of SSA countries should develop their financial systems by improving stock market capitalization in terms of size and liquidity, as neither are close to reaching their full potential (Demirgüç-Kunt & Maksimovic, Citation1996). More inclusive financial systems are required to increase the availability of funding sources. Deepening and accessing capital markets is likely to increase liquidity by reducing the cost of capital (Boufateh & Saadaoui, Citation2020).

In this regard, enhanced collaboration with international development corporations, such as the European Investment Bank (EIB; Citation2018), could provide the necessary impetus. Enterprises will be able to save costs and encourage higher economic growth, which will allow them to easily access low-cost credit that can be used to improve production in energy technologies and investment in R&D. Thereafter, energy demand for industries and households may expand, leading to increased energy consumption.

Fourth, the risk of political interference and regulatory uncertainty should be mitigated (“Africa up close,” Citation2018). This will provide robust policies that support the stability and development of their financial systems during periods of financial crisis. Incidences of financial crises can impact financial openness since they are linked to growth de-acceleration in SSA countries (Beck et al., Citation2011). Regulations should cautiously balance the development, policy changes, and openness of financial systems to manage the frequency of financial crises, as recommended by Tyson (Citation2021). Moreover, SSA countries should strengthen their governments’ governance capabilities and continue to build high-quality institutions to structure and regulate long-term development frameworks.

The scope of the current study is limited to 21 countries and over a period of 27 years. Also, the detrimental aspect of increased energy consumption on the environment is not addressed. Future research could therefore extend our study by including more SSA countries over a longer period and exploring the effect of FDI and energy consumption on environmental pollution.

Ultimately, the eradication of energy poverty should be a top priority for policymakers, otherwise, it is unlikely that the Sustainable Development Goal (SDG) 7, namely “to ensure access to affordable, reliable, sustainable, and modern energy for all” will be achieved for SSA.

CRediT authorship contribution statement

Winnie Thebuho: Conceptualization, Methodology, Formal analysis, Writing – original draft

Pieter Opperman: Supervision, Methodology, Writing – review & editing

Lee-Ann Steenkamp: Supervision, Project administration, Writing – review & editing

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

Notes on contributors

Winnie Thebuho

Winnie Thebuho is a PhD candidate at the Stellenbosch University Business School. She works for the Office of the Prime Minister in Namibia. She is also a part-time Lecturer at the University of Namibia. Her academic interest lies with sustainable development, with earlier research on Smallholder farmer’s perception of adaptations to climate change. She is currently in the final phase of her thesis, which focuses on Financial Globalisation, Energy Consumption and Environmental Sustainability.

Pieter Opperman

Pieter Opperman lectures on the MBA and Development Finance programmes at the Stellenbosch University Business School.

Lee-Ann Steenkamp

Lee-Ann Steenkamp is a tax lecturer at the Stellenbosch University Business School, where she teaches on the MBA and the Postgraduate Diploma in Financial Planning. She is also an Extraordinary Professor in Tax at the University of South Africa. Lee-Ann is a National Research Foundation (NRF) rated researcher – a rare accolade which is bestowed on academics with exceptional research output. She conducts multi-disciplinary research in the fields of taxation and environmental law. Her current research focuses on developing best practice guidelines for the implementation of carbon pricing schemes on the African continent. Dr Steenkamp has published in numerous peer-reviewed international journals.

Notes

1. According to Sahay et al. (Citation2015), “depth” points to market size and liquidity; “access” refers to individuals and companies having the aptitude to access financial services; and “efficiency” means the capability of institutions in providing low-cost financial services together with maintainable revenues, as well as the activity level of capital markets.

2. Gross domestic product per capita (GDPK).

3. List of SSA countries used in the investigation of this paper: Angola, Benin, Botswana, Cameroon, Congo Republic, Côte d’Ivoire (Ivory Coast), Dem. Rep of Congo, Ethiopia, Gabon, Ghana, Kenya, Mauritius, Mozambique, Namibia, Nigeria, Senegal, South Africa, Tanzania, Togo, Uganda and Zambia.

References

- Abbas, N., Saeed, S., Manzoor, S., Arshad, M., & Bilal, U. (2015). The relationship between electricity consumption, employment rate, inflation and economic growth in five developing countries. British Journal of Economics, Management & Trade, 5(2), 164–26. https://doi.org/10.9734/bjemt/2015/10569

- Africa up close. (2018). Electrifying Sub-Saharan Africa Sustainably with Renewable Energy. https://africaupclose.wilsoncenter.org/electrifying-sub-saharan-africa-sustainably-with-renewable-energy/

- African Development Bank [AfDB]. (2018). 4: financing Africa’S infrastructure: New strategies, mechanisms, and instruments. in African Economic outlook. https://search.proquest.com/docview/2073254171?accountid=14609

- African Development Bank [AfDB]. (2021). Historic Alliance Launches at COP26 to Accelerate a Transition to Renewable Energy, Access to Energy for All, and Jobs. https://www.afdb.org/en/news-and-events/historic-alliance-launches-cop26-accelerate-transition-renewable-energy-access-energy-all-and-jobs-46557

- African Development Bank [AfDB]. (n.d.). Power Africa Initiative. https://www.afdb.org/en/topics-and-sectors/initiatives-partnerships/power-africa-initiative

- Ahmad, M., Ahmed, Z., Yang, X., Hussain, N., & Sinha, A. (2022). Financial development and environmental degradation: Do human capital and institutional quality make a difference? Gondwana Research, 1051, 299–310. https://doi.org/10.1016/j.gr.2021.09.012

- Ahmed, Z., Zhang, B., & Cary, M. (2021). Linking economic globalization, economic growth, financial development, and ecological footprint: Evidence from symmetric and asymmetric ARDL. Ecological Indicators, 121(February), 107060. https://doi.org/10.1016/j.ecolind.2020.107060

- Akinsola, F. A., Odhiambo, N. M., & McMillan, D. (2017). The impact of financial liberalization on economic growth in sub-Saharan Africa. Cogent Economics & Finance, 5(1), 1338851. https://doi.org/10.1080/23322039.2017.1338851

- Akinsola, M. O., & Odhiambo, N. M. (2020). Asymmetric effect of oil price on economic growth: Panel analysis of low-income oil-importing countries. Energy Reports, 6(November), 1057–1066. https://doi.org/10.1016/j.egyr.2020.04.023

- Al-Malkawi, H. A. N., Marashdeh, H. A., & Abdullah, N. (2012). Financial development and economic growth in the UAE: Empirical assessment using ARDL approach to co-integration. International Journal of Economics and Finance, 4(5), 105–115. https://doi.org/10.5539/ijef.v4n5p105

- Al-mulali, U., & Binti Che Sab, C. N. (2012). The impact of energy consumption and CO2 emission on the economic growth and financial development in the Sub-Saharan African countries. Energy, 39(1), 180–186. https://doi.org/10.1016/j.energy.2012.01.032

- Al-Mulali, U., & Lee, J. Y. M. (2013). Estimating the impact of the financial development on energy consumption: Evidence from the GCC (Gulf Cooperation Council) countries. Energy, 60, 215–221. https://doi.org/10.1016/j.energy.2013.07.067

- Alam, A., Malik, I. A., Abdullah, A. B., Hassan, A., Faridullah, A. U., Awan, U., Ali, G., Zaman, K., & Naseem, I. (2015). Does financial development contribute to SAARC’S energy demand? From energy crisis to energy reforms. Renewable and Sustainable Energy Reviews, 41(January), 29–818. https://doi.org/10.1016/j.rser.2014.08.071

- Ali, H. S., Yusop, Z., & Hook, L. S. (2015). Financial development and energy consumption nexus in Nigeria: An application of the autoregressive distributed lag bound Testing Approach, International Journal of Energy Economics and Policy, Econjournals, 5(3), 816–821

- Apergis, N., & Gangopadhyay, P. (2020). The asymmetric relationships between pollution, energy use, and oil prices in Vietnam: Some behavioural implications for energy policy-making. Energy Policy, 140(May), 111430. https://doi.org/10.1016/j.enpol.2020.111430

- Aslan, A., Apergis, N., & Topcu, M. (2014). Banking development and energy consumption: Evidence from a panel of Middle Eastern countries. Energy, 72, 427–443. https://doi.org/10.1016/j.energy.2014.05.061

- Asongu, S., El Montasser, G., & Toumi, H. (2016). Testing the relationships between energy consumption, CO2 emissions, and economic growth in 24 African countries: A panel ARDL approach. Environmental Science and Pollution Research, 23(7), 6563–6573. https://doi.org/10.1007/s11356-015-5883-7

- Avila, N., Carvallo, J., Shaw, B., & Kammen, D. M. (2017). The energy challenge in sub-Saharan Africa: Generating energy for sustainable and equitable development. Oxfam Research Backgrounder Series, . Retrieved August, 17, 2019 from. https://www.oxfamamerica.org/static/media/files/oxfam-RAEL-energySSA-pt1.pdf

- Baloch, M. A., Danish, & Meng, F. (2019). Modelling the non-linear relationship between financial development and energy consumption: Statistical experience from OECD countries. Environmental Science and Pollution Research, 26(9), 8838–8846. https://doi.org/10.1007/s11356-019-04317-9

- Beck, N., & Jackman, S. (1998). Beyond linearity by default: generalized additive models. American Journal of Political Science, 42(2), 596–627. https://doi.org/10.2307/2991772

- Beck, T., Munzele Maimbo, S., Faye, I., & Triki, T. (2011). Financing Africa: Through the crisis and beyond. World Bank Publications.

- Bernard, A. U., & Austin, A. (2011). The role of stock market development on economic growth in Nigeria: A time-series analysis. African Research Review, 5(6), 213–230. https://doi.org/10.4314/afrrev.v6i1.5

- Bhatia, M., & Angelou, N. (2015). ESMAP Technical Report. https://openknowledge.worldbank.org/handle/10986/24368

- Boufateh, T., & Saadaoui, Z. (2020). Do asymmetric financial development shocks matter for CO2 emissions in Africa? A nonlinear panel ARDL–PMG approach. Environmental Modeling and Assessment, 25(6), 809–830. https://doi.org/10.1007/s10666-020-09722-w

- Burkhardt, P., & Mbatha, A. (2021, June 10). Ramaphosa cuts red tape to ease blackout hobbling South Africa. Boomerang. Retrieved June, 30, 2021, from www.bloomberg.com/news/articles/2021-06-10/south-Africa-allows-more-private-power-generation-to-ease-crisis

- Castellano, A., Kendall, A., Nikomarov, M., & Swemmer, T. (2020). Brighter Africa: The growth potential of the sub-Saharan electricity sector. McKinsey & Company. Retrieved February 17, 2020, from http://www.mckinsey.com/~/media/mckinsey/dotcom/insights/energy

- Chai, J., Xing, L., Lu, Q., Liang, T., Lai, K. K., & Wang, S. (2016). The non-linear effect of Chinese financial developments on energy supply structures. Sustainability (Switzerland), 8(10), 1–21. https://doi.org/10.3390/su8101021

- Chang, S. C. (2015). Effects of financial developments and income on energy consumption. International Review of Economics and Finance, 35(January), 28–44. https://doi.org/10.1016/j.iref.2014.08.011

- Chen, H., Hongo, D. O., Ssali, M. W., Nyaranga, M. S., & Nderitu, C. W. (2020). The Asymmetric influence of financial development on economic growth in Kenya : Evidence from NARDL. Original Research, (January–March), 1–17. https://doi.org/10.1177/2158244019894071

- Chiu, Y., & Lee, C. (2020). Effects of financial development on energy consumption: The role of country risks. Energy Economics, 90(C),104833. https://doi.org/10.1016/j.eneco.2020.104833104833

- Çoban, S., & Topcu, M. (2013). The nexus between financial development and energy consumption in the EU: A dynamic panel data analysis. Energy Economics, Elsevier, 39(C), 81–88. https://doi.org/10.1016/j.eneco.2013.04.001

- Corfee-Morlot, J., Parks, P., Ogunleye, J., & Ayeni, F. 2019. Organisation for economic co-operation and development. France. Retrieved on October, 2, 2021. from https://www.oecd.org/environment/cc/climate-futures/case-study-achieving-clean-energy-access-in-sub-saharan-africa.pdf

- Danish, & Ulucak, R. (2021). A revisit to the relationship between financial development and energy consumption: Is globalization paramount? Energy, 227, 120337. https://doi.org/10.1016/j.energy.2021.120337

- Demirgüç-Kunt, A., & Maksimovic, V. (1996). Stock market development and financing choices of firms. World Bank Economic Review, 10(2), 341–369. https://doi.org/10.1093/wber/10.2.341

- Destek, M. A. (2015). Energy consumption, economic growth, financial development, and trade openness in Turkey: maki cointegration test. Bulletin of Energy Economics, 3(4), 162–168. https://www.tesdo.org/journaldetail.aspx?Id=4

- Destek, M. A. (2018). Financial development and energy consumption nexus in emerging economies. Energy Sources, Part B: Economics, Planning, and Policy, 13(1), 76–81. https://doi.org/10.1080/15567249.2017.1405106

- Dumrul, Y. (2018). Estimating the impact of financial development on energy consumption: A co-integration analysis. International Journal of Energy Economics and Policy, 8(5), 294–299. http:www.ecconjournals.com

- Durusu-Ciftci, D., Soytas, U., & Nazlioglu, S. (2020). Financial development and energy consumption in emerging markets: Smooth structural shifts and causal linkages. Energy Economics, 87, 104729. https://doi.org/10.1016/j.eneco.2020.104729

- Eberhard, A., Rosnes, O., Shkaratan, M., & Vennemo, H. (2011). Africa’s power infrastructure: investment, integration, efficiency. directions in development; infrastructure. World Bank. https://openknowledge.worldbank.org/handle/10986/2290License:CCBY3.0-IGO

- Engle, R. F., & Granger, C. W. (1987). Co-integration and error correction: Representation, estimation, and testing. Econometrica: J Econ Soc, 55(2), 251–276. https://doi.org/10.2307/1913236

- Eskom. (2019). Loadshedding, Retrieved August, 12, 2019, from http://www.eskom.co.za/documents/LoadSheddingFAQ.pdf

- European Investment Bank (EIB). (2016). Banking in sub-Saharan Africa - recent trends and digital financial inclusion (Vol. 178). The European Investment Bank. https://www.eib.org/attachments/efs/economic_report_banking_africa_digital_financial_inclusion_en.pdf

- European Investment Bank (EIB). (2018). Energy Finance in Sub-Saharan Africa. https://www.eib.org/attachments/country/energy_finance_in_sub_saharan_africa_en.pdf

- Farhani, S., & Solarin, S. A. (2017). Financial development and energy demand in the United States: New evidence from combined cointegration and asymmetric causality tests. Energy, 134, 1029–1037. https://doi.org/10.1016/j.energy.2017.06.121

- Fernandez, M. (2019). BioEnergy consult powering clean energy future. Biomass energy in China, https://www.bioenergyconsult.com/biomass-energy-china/2019

- Gaies, B., Kaabia, O., Ayadi, R., Guesmi, K., & Abid, I. (2019). Financial development and energy consumption: Is the MENA region different? Energy Policy. Elsevier.

- GIZ. (2013). Deutsche Gesellschaft Für Internationale Zusammenarbeit (GIZ) Gmb. https://www.greengrowthknowledge.org/sites/default/files/downloads/resource/green_economy_in_sub-saharan_Africa_GIZ

- Gómez, M., & Rodríguez, J. C. (2019). Energy consumption and financial development in NAFTA countries, 1971-2015. Applied Sciences (Switzerland), 9(2), 9020302. https://doi.org/10.3390/app9020302

- González-Eguino, M. (2015). Energy poverty: An overview. Renewable and Sustainable Energy Reviews, 47(July), 377–385. https://doi.org/10.1016/j.rser.2015.03.013