?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

The purpose of this study is to examine the role of options volatility and bid-ask spread as microstructural variables in determining whether the foreign exchange market’s price formation process in response to macroeconomic announcements is characterised by changes in risk perception and transaction costs. The findings suggest that behavioural characteristics of market participants appear to trump macroeconomic considerations. The volatility indices and bid-ask spreads were found more sensitive to announcements than forex returns, which directly imply weak assimilation of common knowledge into exchange rates. The forex returns, bid-ask spread, and volatility indices demonstrated less vulnerability towards Chinese announcements than the USA, UK, Japan, and Euro. Moreover, findings distinctly signify the role of China as a global liquidity provider by reducing trading costs in the foreign exchange markets. The implications suggest that core macroeconomic models should incorporate agents’ heterogeneous expectations based on risk perceptions than the order flow approach.

1. Introduction and background

The microstructure approach states that information content that is unrelated to macroeconomic announcements, like liquidity demands, hedging, and changing risk tolerance, may affect the exchange rate (M.D.D. Evans & Lyons, Citation2002a). Microstructure approaches enriched with order flow dynamics of exchange rates around fundamentals, but other determinants are understudied or uncovered (Abolaji Daniel Anifowose, Citation2018; Du et al., Citation2018; M.D.D. Evans & Lyons, Citation2002a, Citation2002b). However, the present study investigated the information content disclosed through the trade of hedging and changing risk tolerance through “options volatility” in particular and a liquidity component (bid-ask spread) to explain exchange rate dynamics around macroeconomic announcements which is the core novelty and contribution of this research.

This research’s first contribution is using a novel component of options implied volatility to forecast exchange rate movements. This study hypothesized two possible ways to deal with market uncertainty; either market participants sell their underlying assets to avoid future uncertainty, which in turn induces order flow or hedge against future uncertainty via trading of options. This indicates that information content is preserved in private information with the market participants exercised through the trade of assets or hedging through options. Hence, a rise in the trade of buying options demonstrates mounting volatility, influencing the underlying asset prices or currencies. However, this study considered options implied volatility which is the trademark of the Chicago Board of Options Exchange (CBOE), popularly known as the “fear gauge index” (Whaley, Citation2000). Presumably, options implied volatility considers the market’s perceptions of risk or a gauge to measure short-term volatility. The second contribution of this research is using another variable of the bid-ask spread, which plays a substantial role in the valuation of market functioning and behavior and is an essential driving factor in immediate trade executions. The microstructure literature mentions the adjacent association of options implied volatility with market liquidity (bid-ask spread).

Do these options variables imply volatility and bid-ask forecast exchange rate dynamics directly or indirectly around macroeconomic announcements? It seems essential to employ macroeconomic announcements to explore the behavior of options implied volatility and bid-ask spread which is an essential contribution of this research. Moreover, this research includes emerging economies like China and the big four currencies, USD, EUR, JPY, and GBP. Earlier literature on the microstructure approach concentrated on exchange rates of mature markets. In this sense, it will be particularly more fascinating to compare the results applied to an emerging market, in which external factors exert significant influence on the development path of the domestic economy. The forex markets of transition economies may indicate different properties than the major currency markets. However, with the growing importance of China in the world economy, mounting complexity in financial liberalization and recent vulnerability of the CNY exchange rate.

The present study modernized the forecasting mechanism of foreign exchange with the introduction of micro variables, i.e., options implied volatility and transaction cost (bid-ask spread) around macroeconomic announcements of the USA, China, UK, Japan, and Euro area. The study examined whether options implied volatility and bid-ask spread characterize any part of the information to exchange rates in response to macroeconomic announcements, which, in particular, draw valuable information for monetary thinkers, financial markets, and market participants to anticipate the market direction and improve trading efficiency in foreign exchange markets.

The rest of this paper consists of the following sections; the second section discusses the data and methodology, while the third section sheds light on the results and discussions. The fourth section covers the conclusion of the study. Finally, the fifth section addresses the policy implications, limitations and future study directions.

2. Literature review

The failure of conventional macroeconomic models to explain and forecast movements in exchange rates has given rise to two diverse dimensions of research: one concentrating on the implications of asset pricing through the standard present value approach and the other focused on the microstructure approach to the forex market (Flood & Taylor, Citation1996; J. J. Frankel & Rose, Citation1995; J. A. J. A. Frankel & Rose, Citation1994; Meese & Rogoff, Citation1983a, Citation1983b; Taylor, Citation1995). A later approach of microstructure literature of the forex markets attempted to clarify the mechanism inducing deviations from fundamentals (Flood & Taylor, Citation1996; R. K. R. K. Lyons, Citation2001; Taylor, Citation1995). Microstructure approach has taken into account short run dynamics of exchange rates.

Market participants interpret public information differently, which highlights the role of trading. However, one may conceive different information content; First, the information content is publicly available and evaluated similarly by most traders and also maps into prices directly and immediately as in traditional models. Second, information content is not common knowledge or common but is difficult to interpret (Glosten & Milgrom, Citation1985; Kyle, Citation1985; R. R. Lyons, Citation1995). In this case, it is considered as private and dispersed information and transmuted into prices via the trading process (M.D.D. Evans & Lyons, Citation2002a). Third, information content that is unrelated to macroeconomic announcements like liquidity demands, hedging, and changing risk tolerance may affect the exchange rate (M.D.D. Evans & Lyons, Citation2002a).Abolaji Daniel Anifowose (Citation2018), Anifowose et al. (Citation2018) and M.D.D. Evans and Lyons (Citation2002a, Citation2002b) focused on the trading process and considered order flow as core determinant of exchange rate dynamics. However, trade of options (hedging instruments) and the role of transaction or trading cost have not explored yet which could drive valuable outcomes in forecasting exchange rate. The information content preserved in private information with the market participants exercised through the trade of assets or hedging through options as suggested by (Eberbach et al., Citation2021). Hence, a rise in the trade of buying options demonstrates mounting volatility, influencing the underlying assets or currencies.

Earlier literature evidence that the options implied volatility index significantly anticipates exchange rate (Cairns et al., Citation2007; Ishfaq, Qiong, Abbas et al., Citation2018; Ishfaq, Qiong, Rehman et al., Citation2018; Kang, Ki-Hong et al., Citation2014; Kang, Yun-Jung et al., Citation2014). Similarly, Du et al. (Citation2018) reported that the transaction cost (bid-ask spread) play a substantial role in the valuation of market functioning and behavior, and essential driving factor in immediate trade executions. Earlier studies use ex-post and ex-ante foreign exchange risk measures to confirm that both options implied volatility and spread are interrelated and find that the risk measure is associated positively with the width of bid-ask spread (Black, Citation1989; Boothe, Citation1988; Glassman, Citation1987; Wei, Citation1991).

Previous studies have found that options volatility and bid-ask spread are linked to macroeconomic information (DeGennaro & Shrieves, Citation1997; Ederington & Lee, Citation1996; Ishfaq et al., Citation2017; Kim & Kim, Citation2004). However, the role of options volatility and transaction cost in aggregating expectations about macroeconomic fundamentals has not yet been studied in the literature. Table A1 summarizes the findings from the previous study to pave the way for the contribution of this study.

3. Data and methodology

3.1. Data

The daily frequency data conveys the rich structure of announcements effects. The dataset used in this study covers seven years’ period from 16 March 2011Footnote1 to 28 November 2017. The first stream of data includes exchange rates and bid-ask spread of currency pairs of USD/CNY, JPY/CNY, GBP/CNY, and EUR/CNY at a daily frequency from a highly reliable database “Bloomberg.”

The study also used five major options implied volatility indices of VIX, VXFXI, BPVIX, JYVIX, and EUVIX. The data source stems from the Chicago Board of Options Exchange (CBOE) official website. Options implied volatility defined as the market’s expectation for the remaining life of the options (about 30 days), also known as “investor’s fear-gauge index.” In this study, Options implied volatility represents the expectations of the foreign exchange market (Whaley, Citation2000). A high value of Options implied volatility directs that participants expect the market will become more volatile and vice versa. However, Options implied volatility to be calculated for equity exchanges, exchange-traded funds (ETF), currencies, commodities, and so forth. This study considered options implied volatility of Euro Volatility Index (EUVIX), Japanese Yen Volatility Index (JYVIX), and British Pound Volatility Index (BPVIX), options volatility of S&P 500 index (VIX) and China ETF Volatility Index (VXFXI).

The study also considers the dummy variables of the macroeconomic announcements of the USA, China, UK, Euro area, and Japan over the sample on bi-weekly, monthly, and quarterly basis but varies on country basis. As this study uses novel variables of the microstructure approach, it seems necessary to investigate the impacts of all scheduled announcements in the sample, i.e., market participants know the hour and minute of their release in advance except for underlying information content and may react within a short time. The creation of dummy variables of announcements daily hypothesis that daily frequency intervals seem more appropriate to seize their effects on the exchange rate and volatility.

3.2. Methodology

This section deals with the simple question of whether any part of the exchange rate is characterized through options implied volatility and bid-ask spread in response to the macroeconomic announcements. To inspect this question, it seems natural to explore bid-ask spread and options implied volatility contribution to the overall response to announcements simultaneously employing the Vector Autoregressive model (VAR), imposing a co-integrating vector in the absence of arbitrage. VAR model differs from univariate autoregressive models as these permit feedback to occur among the sample variables in the model. The model allow simultaneous effects of announcements on exchange rates, bid-ask spread, and options implied volatility simultaneously. VAR model seems distinct to explore direct or indirect effects among sample variables through feedback feature. To come up with robust results, the model motivations took from the paper (Chen & Gau, Citation2009). A comprehensive form of multivariate VAR model for our sample analysis presented below;

Where ,

,

and

represent the change in the exchange rate, bid-ask spread, and options volatility indices for

series (VIX, BPVIX, JYVIX, EUVIX and VXFXI) in time

, respectively. The China ETF Volatility Index (VXFXI) remains influential in all four exchange rate parities of the CNY. The dummy variable of macroeconomic announcements of the USA, China, UK, Japan and Euro area turn

=1 on the release date and takes the form

=0 otherwise, for the country

in time

, respectively.

The literature also analyze the effect of public announcements shocks on exchange rate volatility (Andersen & Bollerslev, Citation1998). They find that dummy variable announcement effects are significant than ARCH effects. The impact of announcements are represented by matrix. In addition, the coefficient

symbols for the lead-lag linkages among sample variables and helps in removing the problem of autocorrelation. The coefficient

in the

matrix quantify the impact of spread, VIX, and VXFXI on price movements of exchange rates and others contemporaneously.

The lag lengths are chosen by engaging Akaike Information Criteria (AIC). While evaluating the influence of macroeconomic announcements on foreign exchange markets, the primal should be both home country and foreign country’s economic decisions. For this, the study hypothesized, for instance, when examining USD/CNY behavior, Chinese and the US announcements naturally have a stronger influence on the exchange rate.

4. Empirical analysis

4.1. Descriptive statistics

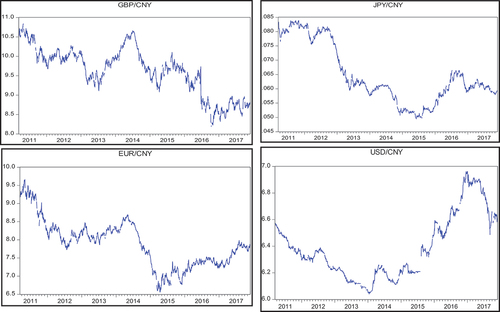

reports summary statistics for the exchange rate returns, bid-ask spread, and volatility indices. The level diagrams exhibit that exchange rates and VIX indices remained volatile and contained a trend. However, the returns are generated by the difference of log price times 100 to make a stationary series for further analysis. The mean values of FX and VIX returns are negative. The mean values of bid-ask spreads are positive except EUR/CNY spread. VIX exhibited the highest standard deviation (market volatility of SPX), which means the highest price change. The positive values of skewness in VIX also show increased volatility. The parity of the USD/CNY exchange rate contains a minor standard deviation (least volatile) and positive skewness (positive returns). This positive skewness is associated with the appreciation trend in later periods of USD/CNY parity, as shown in the level series of exchange rates (). Most sample exchange rates exhibit negative skewness due to the depreciation trend in CNY exchange rates, which is observable in (). However, the bid-ask spread is highly volatile and comprises positive skewness.

Figure 1. Exchange rates at level with extended data.

Table 1. Descriptive statistics

Excess kurtosis coefficients have significant values, specifying that outliers may have arisen with a probability higher than a normal distribution. Accordingly, the Jarque-Bera test rejected the null hypothesis of the normal distribution for all sample returns at the 1% significance level. The lower panel of reports the Augmented Dickey-Fuller test (ADF) results for a unit root. The significant estimates evidenced the absence of unit roots in the return series, implying that their mean returns are around zero. Moreover, the transformation of level series into return series removes the problem of multicollinearity employing the Variance Inflation Factor (VIF) testFootnote2 and consistent (Ishfaq, Qiong, Abbas et al., Citation2018).

reports the results of the Granger causality test in exchange rates, bid-ask spread, and VIX indices. Most estimates reject the null hypothesis that options volatility indices do not cause exchange rates and related bid-ask spread. summarizes that the options volatility indices lead CNY exchange rates and hold a unidirectional relationship except for GBP/CNY parity in panel D, which shows that sample exchange rate and options volatility indices cause each other simultaneously. Second, options volatility indices and bid-ask have a bi-directional association and lead each other except EUR/CNY spread which does not affect options volatility indices in reverse. Finally, options volatility indices interlinked with each other.

Table 2. Pairwise granger causality tests

4.2. Empirical results

The present study hypothesized that market participants buy more options during uncertain circumstances to hedge against future adverse effects. The release of public announcements renders the foreign exchange market more volatile, hence push traders to hedge their investments through option contracts, which, in turn, spurs the options volatility. The Granger causality outcomes in reveal that VIX indices lead to foreign exchange. However, our empirical analysis considered; whether VIX indexes and spread lead foreign exchange around announcements.

contains BPVIX bears significant negative sign at a 3rd lag which causes an appreciation of sample exchange rate, while the positive coefficient of VXFXI reasons depreciation and partially consistent (Ishfaq, Qiong, Abbas et al., Citation2018). The lower panel of presents aggregated announcement coefficients showing a significant impact on BPVIX and VXFIX on the day of release.

Table 3. USD/CNY, spread, VXFXI, VIX and USA announcements

Table 4. USD/CNY, spread, VXFXI, VIX & Chinese announcements

Table 5. GBP/CNY, spread, BPVIX, VXFXI & UK announcements

CNY exchange /CNY exchange rate, bid-ask spread, VXFXI, and VIX around the USA and Chinese announcements respectively. The study followed the hypothesis that announcements may have a direct impact on exchange rates or some part of private information perceived by the market participants and exercised through trading options hence affect the exchange rate indirectly through the movements in spread or VIX indices. The upper panel of both tables shows that VXFXI and VIX both influence the sample exchange rate significantly. The significant negative slope points appreciation of the sample of the exchange rate, while the positive coefficient of VIX implies deterioration.

The lower panel of summarizes that spread and VIX index found sensitive to the public releases on the day of announcement of an aggregated dummy variable (D). The VIX index also shows sensitiveness to the release a day before the aggregated announcements (D-1). The widening spreads in response to unemployment rates and personal income are consistent with the earlier study (Rühl & Stein, Citation2013). The positive coefficient of spread around the US announcements reveals an asymmetry in information content and considers widespread as protection for loss to informed traders from noisy traders in low liquid markets which is consistent (Balduzzi et al., Citation2001; Kyle, Citation1985).

Most individual announcements significantly affect the spread of VXFXI and VIX on the day of release. The negative impact of announcements on options volatility points towards the resolution of uncertainty on the day of release. This result offers some support from earlier studies that the release of information content enclosed in scheduled macroeconomic announcements reduces the expectations of future volatility (DeGennaro & Shrieves, Citation1997; Ederington & Lee, Citation1996; Kim & Kim, Citation2004). The announcements of consumer confidence and personal income explain natural movements in the sample exchange rate. Other announcements seem to impact the exchange rate via VXFXI and VIX indirectly. Our study considers that the variable having a significant correlation with both announcements and exchange rates qualifies to encompass information content effectively and vice versa.

The estimates show that options volatility significantly correlates with both announcements and exchange rates, hence qualifies to assimilate private information content, unlike bid-ask spreads. Likewise, the role of order flow, these results support the importance of options volatility to analyze the movements in the exchange rate (Martin D. D. Evans & Lyons, Citation2005; Love, Citation2005; Love & Payne, Citation2008). The role of the money supply is too small and insignificant as money demand in China is mainly decided by other factors like expected inflation rate, income, and interest rate (Xiangsheng Dou, Citation2019). To best our knowledge, the present study is the first comprehensive study to explore the interaction of exchange rates, spread, and market volatility indices around announcements.

The lower panel of bears significant negative sign at a 3rd lag which causes an appreciation of sample exchange rate, while the positive coefficient of VXFXI reasons depreciation and partially consistent (Ishfaq, Qiong, Abbas et al., Citation2018). The lower panel of presents aggregated announcement coefficients showing a significant impact on BPVIX and VXFIX on the day of release. reports that the effect of aggregated announcements of China has no role in explaining the dynamics of FX returns, spread, and VIX indices. However, directly and indirectly, individual announcements influence exchange rates via market volatility. The results indicated VXFXI and VIX lead price changes in the exchange rate. Additionally, the effects of the announcement of the leading index report a significant direct impact on the sample exchange rate. Other individual announcements display a substantial effect on the exchange rate. The results support our hypothesis that announcements affect exchange rate returns and market volatility.

The BPVIX bears significant negative sign at a 3rd lag which causes an appreciation of sample exchange rate, while the positive coefficient of VXFXI reasons depreciation and partially consistent (Ishfaq, Qiong, Abbas et al., Citation2018). The lower panel of Table presents aggregated announcement coefficients showing a significant impact on BPVIX and VXFIX on the day of release.

The effect of announcements of GDP, unemployment rate, and total business investment significant on FX returns. The rest of the announcements influenced FX returns via market volatility indices. Most announcements indicated the considerable impact on BPVIX and VXFXI but not on FX returns because the impact of announcements reflected in options volatility first, then impounded into FX returns via options volatility which is the market reaction to announcements. analyzed the dynamics of GBP/CNY returns, spread, BPVIX, VXFXI around the UK, and Chinese announcements separately. The upper panel of both Tables indicates that FX returns, BPVIX and VXFXI hold bi-directional association and lead each other to mark the market equilibrium as shown in the Granger causality test (, panel D).

Table 6. GBP/CNY, spread, BPVIX, VXFXI & Chinese announcements

The Chinese aggregated announcements denoted a significant impact on the day and a day after the announcement in . Particular changes in FX returns are explained by market volatility as announcements significantly affected BPVIX and VXFXI and are consistent with our hypothesis. The macroeconomic announcements from the UK and China significantly reduced the bid-ask spread in exchange rate markets, which implies that both economies play an essential role in providing liquidity and keeping markets active.

reports the association of EUR/CNY, bid-ask spread, EUVIX, VXFXI surrounding the Euro and Chinese announcements correspondingly. The upper panel of both tables displays a significant impact of EUVIX and VXFXI on FX returns. Both volatility indices contained significant negative coefficients pointing towards an appreciation of sample exchange rate and supportive (Ishfaq, Qiong, Abbas et al., Citation2018). The lower panel of shows the substantial effect of aggregated Euro announcement on FX returns a day before the release of announcements D (−1). However, individual announcements exhibit insignificant coefficients to explain the dynamics of FX returns.

Table 7. EUR/CNY, spread, EUVIX, VXFXI & Euro announcements

Table 8. EUR/CNY, spread, EUVIX, VXFXI & Chinese announcements

The individual announcements indicated a significant influence on the spread and both volatility indices that play a role to explore the movements in FX returns. The impact of aggregated Chinese announcements displayed a significant effect on EUVIX before the release in . The announcement of the balance of trade indicated a considerable coefficient to explain changes in FX returns. Other macroeconomic announcements leading index, New Year loans, and GDP influenced spread and VXFXI respectively hence play an essential role in intermediating information content into exchange rate via market volatility. Chinese announcements reduced the bid-ask spread, while the Current Account Balance of the Euro area raised spread during the sample period.

illustrate the results of JPY/CNY, spread, JYVIX, and VXFXI around Japanese and Chinese announcements accordingly. Chinese and Japanese volatility indexes significantly influence underlying exchange rates. The negative slope of JYVIX encourages appreciation while the positive slope of VXFXI urges deprecation and consistency (Ishfaq, Qiong, Abbas et al., Citation2018). Japanese announcements highlight the substantial impact on JYVIX which indicates increased volatility a day before and after the release of announcements in anticipation of macroeconomic announcements (Bauwens et al., Citation2005; Jones et al., Citation1998).

Table 9. JPY/CNY, spread, JYVIX, VXFXI & Japanese announcements

Table 10. JPY/CNY, spread, JYVIX, VXFXI & Chinese announcements

However, some part of the information makes significant revisions in the expectations of future volatility. The effects of GDP and PPI report substantial impact on both announcements on FX returns. Other individual announcements significantly influenced the spread of JYVIX and VXFXI to transmit information content in FX returns.

The sensitivity of spread coefficients to announcements find some support of liquidity and the presence of noisy traders, making the sample market less liquid. describes that aggregated announcements of China have no impact on sample FX returns. Individual announcements affect spread, JYVIX, and VXFXI significantly, which, in turn, assist in examining the dynamics of FX returns.

The study evidenced the behavioral aspects of market participants seem dominant over macro perspectives, which highlight the significance of microstructural approaches in anticipating asset prices, which is in line with the microstructural approach. One of the earlier studies supports our result which stated that risk perception slows down the process of economic growth (Marmolejo & Urquijo, Citation2011). The study evidenced the behavioral aspects of market participants seem dominant over macro perspectives, which highlight the significance of microstructural approaches in anticipating asset prices. Our study provides supportive evidence and recommends including heterogeneous expectations of agents in the core macroeconomic models, which are a crucial argument made in the recent developments on the macroeconomic perspective (Vines & Wills, Citation2018).

However, positive slopes of VXFXI and VIX point towards the depreciation of exchange rates. This devaluation in exchange rates might be linked with an economic backdrop in the stock market crash, a slowdown in real GDP growth rate, stubborn capital outflows from Chinese markets in recent years, and controversies between the US and China in recent years (Peltier, Citation2015). The estimates evidenced the rise in volatility in Chinese financial markets that discouraged investor confidence and seek for “flight to safety” effect. The global risk aversion indicators of developed economies (BPVIX, EUVIX, and JYVIX) are considered as “safe heaven” during volatile regimes.Footnote3 This designates implied volatility indices can play a substantial role in anticipating exchange rates. Investors should consider options volatility indices as a “fear-gauge index” during portfolio evaluation in foreign exchange markets. Our results are consistent with the previous literature (Cairns et al., Citation2007; Ishfaq, Qiong, Abbas et al., Citation2018; Kang, Ki-Hong et al., Citation2014; Kang, Yun-Jung et al., Citation2014).

Moreover, the volatility indices and bid-ask spreads were found more sensitive to announcements than forex returns, which directly imply weak assimilation of public information into exchange rates. This indicates that low or longer-term frequency announcements are unmatchable with China’s high frequency and volatile exchange rate regimes. Although the forex markets of China are partially flexible, even then, the assimilation of public information seems poor. However, the high-frequency or comparatively matching frequency indicators seem more appropriate to encompass the short-term effects. Our results support the microstructural approaches that information content influences the exchange rate through wide-ranging interpretations of public information.

The forex returns, bid-ask spread, and volatility indices demonstrated less vulnerability towards Chinese announcements as compared to the USA, UK, Japan, and Euro. However, China’s announcements like GDP, FDI, leading index, foreign reserves, and activity index are more influential to volatility indices and bid-ask spreads. The release of announcements reduces the volatility in foreign exchange markets on the day of the announcement. This result offers some support from earlier studies that the release of information content enclosed in scheduled macroeconomic announcements reduces the uncertainty of future expectations (DeGennaro & Shrieves, Citation1997; Ederington & Lee, Citation1996; Ishfaq et al., Citation2017; Kim & Kim, Citation2004). The study also found that the US announcements containing asymmetric information widen the bid-ask spread and consider widespread as protection for loss to informed traders from noisy traders in low liquid markets which is consistent with earlier studies (Balduzzi et al., Citation2001; Kyle, Citation1985). The quick reversion of bid-ask spread in most samples can be attributed to the supremacy of informed traders. The spread consequences do not help to impound any part of information into exchange rates. However, bid-ask spread found sensitive to the release of macroeconomic announcements.

In contrast, announcements related to China and the UK keep foreign exchange markets liquid by reducing bid-ask spread to boost economic activity. These outcomes prove the subjective evidence that “Bernanke and China Send World Stocks Lower” by CNN on 20 June 2013. Likewise, the Bloomberg BusinessWeek headlines that “Copper Weakens for Second Day as China’s Manufacturing Slows” on 30 April 2013. The volatility indices found more sensitive to announcements than forex returns and spreads, which implies weak assimilation of public information into exchange rates consistent with the microstructural approach. The return series of spread and volatility indices demonstrate less vulnerability towards Chinese announcements than the USA, UK, Japan, and Euro. However, the bid-ask spread outcomes do not help to impound any information into exchange rates. Options implied volatility represents investor behavior as a “fear gauge” for future uncertainty.

5. Conclusion

The purpose of this study is to examine the role of options implied volatility and bid-ask spread as microstructural variables in the price formation process of foreign exchange markets in response to macroeconomic announcements. The findings of this study indicated that changes in one’s perception of option implied volatility affect exchange rates and, more precisely, on the private portion of information content associated with announcements likewise order flow in previous literature. The findings indicate that behavioral characteristics of market participants appear to be more influential than macroeconomic perspectives, emphasizing the importance of microstructural approaches in anticipating asset prices, which is consistent with the microstructural approach.

The heterogeneous expectations of agents in core macroeconomic models demonstrated the increase in volatility in Chinese financial markets, which eroded investor confidence and induced a “flight to safety” response. Additionally, the findings demonstrated that US announcements containing asymmetric information increase the bid-ask spread and are widely regarded as a form of protection for informed traders against noisy traders in low-liquid markets. Finally, volatility indices and bid-ask spreads were more sensitive to macroeconomic announcements than forex returns, implying that public information is not directly incorporated into exchange rates.

6. Policy implications, limitations and future study direction

The study recommends that monetary and financial institutions of China require gaining more confidence of global investors emerging as “safe heaven” during volatile regimes through transparent economic policy mechanisms and letting the natural forces of supply and demand to settle market equilibrium. Otherwise, the rising uncertainty in Chinese markets will put pressure on RMB’s financial openness and internationalization. Monetary thinkers and investors should consider China’s GDP, FDI, leading index, foreign reserves, and activity index while evaluating forex markets. Investors should also consider options implied volatility as a fear gauge index during portfolio evaluation.

The limitations of this research include the non-availability of high-frequency data on the minute basis of options volatility and exchange rates which can explore more insights to support microstructure models. Therefore, prospective researchers can consider this limitation as a future study direction.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

Notes

1. As CBOE started to calculate China Exchange Traded Fund’s Volatility Index (VXFXI) since 16 March 2011 which is our core variable.

2. Variance Inflation Factor (VIF) is employed to authenticate results but not presented in the paper to conserve the space.

3. Chinese instability has appreciated the yen because Japanese fixed income is seen as “safe haven” in the face of global risk aversion.

References

- Abolaji Daniel Anifowose, I. I., and Mohd Edil, Abd Sukor. (2018). Currency order flow and exchange rate determination: Empirical evidence from the Malaysian foreign exchange market. Global Business Review, 19(14), 11–27. https://doi.org/10.1177/0972150918772925

- Andersen, T. G., & Bollerslev, T. (1998). Deutsche Mark-Dollar volatility: intraday activity patterns, macroeconomic announcements, and longer run dependencies. Journal of Finance, 53(1), 219–265. https://doi.org/10.1111/0022-1082.85732

- Anifowose, A. D., Ismail, I., & Sukor, M. E. A. (2018). Currency order flow and exchange rate determination: Empirical evidence from the Malaysian foreign exchange market. Global Business Review, 19(4), 902–920. https://doi.org/10.1177/0972150918772925

- Balduzzi, P., Elton, E. J., & Green, T. C. (2001). Economic news and bond prices: Evidence from the U.S. treasury market. Journal of Financial and Quantitative Analysis, 36(34), 523–543. https://doi.org/10.2307/2676223

- Bauwens, L., Omrane, W. B., & Giot, P. (2005). News announcements, market activity and volatility in the euro/dollar FX market. Journal of International Money and Finance, 24(7), 1108–1125. https://doi.org/10.1016/j.jimonfin.2005.08.008

- Black, S. W. (1989). Transaction costs and vehicle currencies. IMF working paper, WP/89/96. International Monetary Fund (IMF).

- Boothe, P. (1988). Exchange rate risk and the Bid-ask spread: A seven country comparison. Economic Inquiry, 26(3), 485–492. https://doi.org/10.1111/j.1465-7295.1988.tb01510.x

- Cairns, J., Ho, C., & McCauley, R. (2007, March). Exchange rates and global volatility: Implications for Asia-Pacific currencies. BIS Quarterly Review, 41–52. https://www.bis.org/publ/qtrpdf/r_qt0703.htm

- Chen, Y., & Gau, Y.-F. (2009). Impacts of news announcements to order flow and price discovery in the foreign exchange market. Paper presented at the Annual Conference of Taiwan Finance Association. Taiwan.

- DeGennaro, R. P., & Shrieves, R. E. (1997). Public information releases, private information arrival and volatility in the FX market. Journal of Empirical Finance, 4(4), 295–315. https://doi.org/10.1016/S0927-5398(97)00012-1

- Du, B., Fung, S., & Loveland, R. (2018). The informational role of options markets: Evidence from FOMC announcements. Journal of Banking & Finance, 92, 237–256. https://doi.org/10.1016/j.jbankfin.2018.05.013

- Eberbach, J., Uhrig-Homburg, M., & Yu, X. (2021). Information processing in the option market around earnings and macroeconomic announcements. Karlsruhe: Karlsruhe Institute of Technology (KIT).

- Ederington, L. H., & Lee, J. H. (1996). The creation and resolution of market uncertainty: The impact of information releases on implied volatility. Journal of Financial and Quantitative Analysis, 31(34), 513–539. https://doi.org/10.2307/2331358

- Evans, M. D. D., & Lyons, R. K. (2002a). Informational Integration and FX Trading. Journal of International Money and Finance, 21(6), 807–831. https://doi.org/10.1016/S0261-5606(02)00024-4

- Evans, M. D. D., & Lyons, R. K. (2002b). Order flow and exchange rate dynamics. Journal of Political Economy, 110(1), 170–180. https://doi.org/10.1086/324391

- Evans, M. D. D., & Lyons, R. K. (2005). Do currency markets absorb news quickly? Journal of International Money and Finance, 24(2), 197–217. https://doi.org/10.1016/j.jimonfin.2004.12.004

- Flood, R. P., & Taylor, M. P. (1996). Exchange rate economics: What’s wrong with the conventional macro approach? National Bureau of Economic Research, 261–302.

- Frankel, J. A., & Rose, A. K. (1994). A survey of empirical research on nominal exchange rates, Working Paper No. 4865. Cambridge: National Bureau of Economic Research, Inc.

- Frankel, J., & Rose, A. (1995). Empirical research on nominal exchange rates. In G. M. Grossman & K. Rogoff (Eds.), Handbook of International Economics (Vol. 3, pp. 1689–1729). Elsevier.

- Glassman, D. (1987). Exchange rate risk and transactions costs: Evidence from bid-ask spreads. Journal of International Money and Finance, 6(4), 479–490. https://doi.org/10.1016/0261-5606(87)90024-6

- Glosten, L. R., & Milgrom, P. R. (1985). Bid, ask and transaction prices in a specialist market with heterogeneously informed traders. Journal of Financial Economics, 14(1), 71–100. https://doi.org/10.1016/0304-405X(85)90044-3

- Ishfaq, M., Qiong, Z. B., & Shah, S. M. R. (2017). Global macroeconomic announcements and foreign exchange implied volatility. International Journal of Economics and Financial Issues, 7(5), 119–127. https://www.econjournals.com/index.php/ijefi/article/view/5364

- Ishfaq, M., Qiong, Z. B., & Rehman, A. U. (2018). Global volatility spillover in Asian financial markets. Mediterranean Journal of Social Sciences, 9(2), 109–116. https://doi.org/10.2478/mjss-2018-0031

- Ishfaq, M., Qiong, Z. B., & Abbas, G. (2018). Global volatility spillover, transaction cost and CNY exchange rate parities. Mediterranean Journal of Social Sciences, 9(2), 161–171. https://doi.org/10.2478/mjss-2018-0036

- Jones, C. M., Lamont, O., & Lumsdaine, R. L. (1998). Macroeconomic news and bond market volatility. Journal of Financial Economics, 47(43), 315–337. https://doi.org/10.1016/S0304-405X(97)00047-0

- Kang, S. H., Ki-Hong, C., & Yoon, S.-M. (2014). The impact of global volatility on Asian financial markets. National Research Foundation.

- Kang, S. H., Yun-Jung, L., Ki-Hong, C., & Sungkyun, P. (2014). The impact of global volatility on Korean financial markets. Paper presented at the International Conference on Trends in Economics, Pattaya (Thailand). Korea: National Research Foundation.

- Kim, M., & Kim, M. (2004). Implied volatility dynamics in the foreign exchange markets. Journal of International Money and Finance, 22(4), 511–528. https://doi.org/10.1016/S0261-5606(03)00018-4

- Kyle, A. (1985). Continuous auctions and insider trading. Econometrica, 53(56), 1315–1335. https://doi.org/10.2307/1913210

- Love, R. (2005). A microstructural analysis of the effects of news on order flows and price discovery: PhD dissertation, London School of Economics.

- Love, R., & Payne, R. (2008). Macroeconomic news, order flow and exchange rates. Journal of Financial and Quantitative Analysis, 43(2), 467–488. https://doi.org/10.1017/S0022109000003598

- Lyons, R. (1995). Tests of microstructural hypotheses in the foreign exchange market. Journal of Financial Economics, 39(2–3), 321–351. https://doi.org/10.1016/0304-405X(95)00832-Y

- Lyons, R. K. (2001). The microstructure approach to exchange rates. MIT Press.

- Marmolejo, A. L., & Urquijo, I. M. (2011). Exchange rate, fundamental level and the influence of global volatility (pp. 1–6). Banco Bilbao Vizcaya Argentaria’s (BBVA).

- Meese, R., & Rogoff, K. (1983a). The out-of-sample failure of empirical exchange rate models: Sampling error or misspecification? National Bureau of Economic Research, 67–112.

- Meese, R., & Rogoff, K. (1983b). The out-of-sample failure of empirical exchange rate models: Sampling error or misspecification? In Jacob A. Frenkel (ed.), Exchange rates and international macroeconomics (pp. 67–112). University of Chicago Press.

- Peltier, C. (2015). China: A new exchange rate policy. BNP PARIBAS.

- Rühl, T. R., & Stein, M. (2013). The cost of new information-ECB macro announcement impacts on bid-ask spreads of European blue chips ( pp. Ruhr Economic Papers, No. 452, 86710.84419/86788509): Ruhr Economic Papers, No. 452. Ruhr-Universität Bochum (RUB), Germany.

- Taylor, M. P. (1995). The economics of exchange rates. Journal of Economic Literature, 33(31), 13–47. http://www.jstor.org/stable/2728909

- Vines, D., & Wills, S. (2018). The rebuilding macroeconomic theory project: An analytical assessment. Oxford Review of Economic Policy, 34(31–32), 31–42. https://doi.org/10.1093/oxrep/grx062

- Wei, S. J. (1991). Anticipation of foreign exchange volatility and bid-ask spread (pp. 409): International Finance Discussion Papers, Federal Reserve System.

- Whaley, R. E. (2000). The investor fear gauge. The Journal of Portfolio Management, 26(23), 12–17. https://doi.org/10.3905/jpm.2000.319728

- Xiangsheng Dou, S. R. (2019). The determinants of money demand in China. Cogent Economics & Finance, 6(1), 1–17. https://doi.org/10.1080/23322039.2018.1564422