?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

We examine the role of female directors on firm cost of equity in the context of US-listed firms, and further explore the mediating impact of debt financing policy on such association. Using a dataset of 4619 non-financial firm-year observations covering the period of 2008–2019, we find that firms with female directors on boards are likely to exhibit a lower cost of equity, through relying on a less risky financing decision. The indirect effect is found to take up around 45% of the female-cost of equity association. In addition, our analysis also indicates that the lower debt financing levels are realised only if female representation reaches a critical mass of around 28%. Our findings provide important implications for firms in balancing the gender ratio within their boards to level out their risk-taking through their financing decisions.

1. Introduction

The extent literature (see among others, Bear et al., Citation2010; Karavitis et al., Citation2019; Srindhi et al., Citation2011) on corporate governance and finance has underlined the importance of improving board diversity, especially gender diversity. They claim that female presence is imperative to create harmony and balance in the board structure as females are punctual, hard workers and critical thinkers. In this manner, they provide better oversight of the managers’ behaviour and their financing decisions. Given the recognition of the value-added contribution of female representation to the quality of firm strategic policies, corporate governance codes in several countries, particularly the US, have begun setting targets for the proportion of female directors to be appointed on boards.Footnote1 Even though investors seek high-risk-taking to maximise their wealth, they have been still pursuing firms to increase the number of females within boards to enhance the monitoring quality mechanisms.

A line of research (e.g., Abad et al., Citation2017; Jizi & Nehme, Citation2017) has been put on female directors and their role in enhancing firm’s financial disclosure, transparency, and stock informativeness, which gives a good indication on the association between female directors and the firm cost of equity. This may subsequently develop a favourable image and reputation of female-led firms in the eyes of shareholders. Notably, previous studies have reported on the role of gender diversity board in increasing voluntary disclosure of firms’ information, which, in turn, reduces the information asymmetry in the equity market (Abad et al., Citation2017); enhancing the informativeness of stock prices (Gul et al., Citation2011); reducing adverse selection problems in security markets (Cai et al., Citation2006); and a firm’s equity risk measuring by stock return volatility (Jizi & Nehme, Citation2017).Footnote2 These studies imply positive effects of board gender diversity on the equity markets, which indirectly signal a lower cost of equity. Other literature (Botosan, Citation1997; Gietzmann & Ireland, Citation2005) point out that the quality of financial reporting is as essential to the equity holders as the debt holders. However, “the value of transparency is a function of a firm’s overall operating environment and organizational structure” (Upadhyay & Sriram, Citation2011, p. 1242). Dobija et al. (Citation2021) find that higher percentage of women on boards is associated with better financial reporting quality. Again, if board gender diversity can improve the transparency of a firm’s financial report, then investors may ask a lower rate of return for their investment. Building on the literature, we argue that the presence of female directors on board lowers the firm cost of equity.

To further investigate the mediating effect of financing decisions made by highly female-represented firms, we steer our attention to the association between the presence of female directors serving on the board of directors and firm capital structure. Till date, extant literature has paid efforts on examining the impacts of female directors on firms’ financing choices, resulting in conclusive findings on the negative female-leverage association (Adams & Funk, Citation2012; Huang & Kisgen, Citation2013; Alves, Couto, and Francisco.; Alves et al., Citation2015; Faccio et al., Citation2016; Adusei & Obeng, Citation2019). They find that the presence of female directors on boards decreases firms’ leverage, hence lower exposures to bankruptcy risks and greater survival chances. This can be explained through the lower risk-aversion of females (Adams & Funk, Citation2012; Croson & Gneezy, Citation2009). Nevertheless, we realise that what remains unclear in the literature is whether this more conservative capital structure (i.e., lower debt levels) of highly female-represented firms is perceived as an optimal or a suboptimal financial decision in the eyes of shareholders (to be explained later). We therefore substantially contribute to the corporate governance and finance literature by investigating both the direct impacts of board gender diversity on the US firm’s cost of equity and the mediating effect of debt financing decision on that association.

Employing a sample of 4,619 US firm-year observations for the period 2008–2019, we initially find that if a firm’s board contains up to approximately 28% of female directors, the increase in the debt level is marginally diminishing and will start to fall when the proportion of females goes beyond that level. However, for the firms with a higher proportion of female directors (≥28%), the rise of the debt financing degree is marginally diminishing and starts falling when the female proportion goes beyond that level. Our findings provide robust evidence for Critical Mass theory (Kanter, Citation1977). Specifically, the theory suggests that for female directors to fully realise their potentials and impacts, the board should have at least three female directors (Adusei & Obeng, Citation2019). This is supported by several studies such as Joecks et al. (Citation2013), Farag and Mallin (Citation2017), and Fan et al. (Citation2019). More interestingly, the results indicate that firms with a more gender-diversified board are more likely to mitigate the total debt levels through long-term debt instruments rather than short-term debts.

We subsequently find significant and negative linear effects of female directors on board on firms’ cost of equity. This implies that market participants should honour these US firms with an increase in stock value, and hence, lower their cost of equity. In this section, we aim to arrange and integrate these two mosaics into one unified framework by examining whether highly female-represented firms achieve a lower cost of equity through their lower debt strategies. The main methodology challenge for our tests here is the measurements of the cost of equity. Therefore, to obtain reliable findings, we have employed alternative proxies for equity cost, which include four cost of equity components and the average of these. Typically, we measure the implied equity cost based on averaging four commonly estimates developed by Claus and Thomas (Citation2001)—RCT; Gebhardt, Lee, and Swaminathan (Citation2001)—RGLS; Ohlson and Juettner-Nauroth (Citation2005)—ROJN; and Modified Easton (Citation2004) module by Gode and Mohanram (Citation2003)—RMPEG. Our results can be justified insofar as shareholders are aware of the value added by the female directors’ risk aversion nature in mitigating the potentially “excessive” risk-taking behaviours of firms and hence lowering their required return rates.

In further analyses, we examine the mediating effect of the debt financing policy on the relationship between female directors and the firm cost of equity. For that, our study aims at inferring the judgements of shareholders on the lower level of debt adopted by firms with high female representation through their rates of required returns (i.e., cost of equity). Various evidence has been reported on the positive contributions of higher female representation on boards in some corporate respects, with many of the advantageous and benefiting the shareholders. Consequently, shareholders may have built up positive representative judgements on highly female-represented firms. According to the representativeness and anchoring biases,Footnote3 shareholders’ faith and trust have been developed over time regarding corporate decisions made by highly female-represented firms, including their lower debt financing decisions (Tversky & Kahneman, Citation1974). As a result, we argue that the firm cost of equity is significantly mediated through the capital structure choice of firms with a high representation of female on their board.

Based on this expectation, we use Baron’s and Kenny’s (Citation1986) four-step mediation models to explore the mediating impacts of firm capital structure on the influences of board gender diversity on the cost of equity. We attempt to arrange and integrate the above two mosaics into one unified framework by examining whether highly female-represented firms achieve a lower cost of equity through their lower debt strategies. As a result, we find a significant mediating effect of firm financing choices with the indirect effect takes up approximately 45%. Indeed, firms with a higher percentage of female directors tend to significantly lower their cost of equity through their lower financial leverage levels.

Our study makes at least three noteworthy contributions. First, our paper contributes to an important topic within the corporate finance literature that links board gender diversity to the cost of equity. Second, we contribute to previous literature (e.g., Adams & Funk, Citation2012; Adusei & Obeng, Citation2019; Alves et al., Citation2015; Faccio et al., Citation2016; Huang & Kisgen, Citation2013) by examining the non-linear effects of board gender diversity on the capital structure or financial leverage levels, as we provide strong evidence of a non-linear result. Accordingly, we are among the first empirical studies that confirm this Critical Mass level of female presence on boards within the financing decision-making process. A few prior studies also support the Critical Mass level of female board representation on other firm outcomes, e.g., financial performance, earnings management and financial fragility (Fan et al., Citation2019; Farag & Mallin, Citation2017; Joecks et al., Citation2013; Terjesen et al., Citation2009). Third, to our best of knowledge, this study is the first to focus on the mediating effect of the capital structure on the relationship between boardroom gender diversity and the cost of equity. Therefore, we have enriched our existing knowledge about the linkages between gender diversity and firm financial outcomes (e.g., J. Chen et al., Citation2017; Dezsö & Ross, Citation2012; Karavitis et al., Citation2019; Liu et al., Citation2014; Strøm et al., Citation2014).

The remainder of our study is structured as follows. Section 2 discusses the literature review and hypothesis development. Subsequently, Section 3 presents data sources, sample selection and methodology, and the descriptive analysis. Section 4 reports our main results and robustness checks. Section 5 concludes the research.

2. Literature review and hypothesis development

According to the resource dependence theory, the board of directors contributes to the firm ability to access a critical resource and manage the uncertainty in the external environment (Hillman et al., Citation2009; Pfeffer & Salancik, Citation2003). The appointment of female directors on boards has been argued to bring a greater diversity in terms of skills, knowledge, and experience into the board. Particularly, female directors are different from their male counterparts because of their socialised behaviours, which help them to be more interdependent, nurturing, compassionate, cooperative and focus on developing interpersonal skills (Zelezny et al., Citation2000). Accordingly, they tend to bring different ideas and perspectives, and diverse human capital to the board (Singh et al., Citation2008). They could bring superior benefits to firms, such as an enhanced communication effectiveness within board (Gul et al., Citation2011; Joy, Citation2008), alternative experiences and viewpoints for a better quality of board deliberations and discussions (Clarke, Citation2005; McInerney-Lacombe et al., Citation2008; Zahra & Pearce, Citation1989), and greater firm oversight/monitoring effectiveness (Adams & Ferreira, Citation2009; Carter et al., Citation2010).

Furthermore, Nadeem et al. (Citation2017) discuss that women on boards can provide a better understanding on certain customers and better access to resources. Consequently, women on board may enhance the management of firm risk and uncertainty in the external environment, thus leading to more appropriate risk level being adopted, such as protecting firm from an over-levered position. Consequently, shareholders may have a favourable perception on the financing decisions made by female-presented firms, leading to cheaper financing cost of equity.

2.1. Board gender diversity and firm debt financing decisions

Firms aim to implement sound corporate governance practices through the establishment and maintenance of a healthy corporate culture in which managers are encouraged to behave in line with the shareholders’ interests, i.e., to maximise firms’ performance and to minimise the cost of funds. Corporate financial literature has prevalently claimed that self-interested managers may adopt suboptimal capital structure which is determined “not only by market frictions such as taxes, bankruptcy costs, or refinancing costs (as in Fisher, Heinkel, and Zechner (Citation1989)) but also by the severity of manager-shareholder conflicts” (Morellec et al., Citation2012, p. 803). As a result, academic researchers have paid much attention in learning about the influences of corporate governance on firms’ financing choices (Adusei & Obeng, Citation2019; Berger et al., Citation1997; Friend & Lang, Citation1988; Jensen, Citation1986; Mehran, Citation1992; Wen et al., Citation2002). It has been well established that financing decisions are at least in part influenced by agency conflicts, hence the quality of firms’ corporate governance (Berger et al., Citation1997; Friend & Lang, Citation1988). Particularly, as Aggarwal and Goodell (Citation2014) and Harford et al. (Citation2008) suggest that firms with strong governance with better protections for stakeholders tend to have better access to financing and take on higher debt.

Among many internal and external corporate governance mechanisms being studied to influence firms’ capital structure, board gender diversity remains unexplored despite their significant roles in firms’ financial and investment decisions. Recently, Adusei and Obeng (Citation2019) conduct an international study on microfinance institutions to examine the association of board gender diversity and the capital structure. They find that the presence of female directors on boards decreases firms’ leverage, and hence, their exposure to bankruptcy risk. This may be explained through the lower risk-aversion and risk attitude of females; thereby, they are more concerned about the financial matters, and thus, prefer to take secure financial decision to avoid bankruptcy by taking lower debt (Adams & Funk, Citation2012). Similarly, another global analysis study, but on non-financial firms, was conducted by Alves et al. (Citation2015) by employing data from 33 countries over the 2006–2010 period. They report that firms with stronger female representation on boards tend to issue more external equity in comparison to long-term debt. They justify that diversified gender enhances board efficiency and lower asymmetries in information between company management and shareholders which help capital structure with less short debt and more long debt resources, reducing the bankruptcy risk of firms.

On the same research line, Faccio et al. (Citation2016) intriguingly find that firms managed by CEO females exhibit lower leverage level, greater survival opportunity, and more stable earnings mainly due to the risk-avoidance behaviours of female CEOs. Supporting the same finding, Huang and Kisgen (Citation2013) reveal that female executives are less likely to issue debt financing and engage in merger and acquisition activities. The key justification for this negative female-leverage association is the higher risk-averse nature of females (J. Chen et al., Citation2017; Croson & Gneezy, Citation2009). Taken together, since debt financing is positively linked with the probability of bankruptcy and financial distress, female directors tend to prefer lower debt to equity ratios. Consequently, the following hypothesis will be tested:

H1: Firms with higher proportion of females on board exhibit lower debt financing level.

2.2. Female critical mass

Building on the Critical Mass theory (Kanter, Citation1977), which shows that an increase in the share of females within corporations reaching a Critical Mass level can enhance the contributions of a female minority group that can alter the corporate cultures as well as the impacts of the existing majority male group. Specifically, the theory suggests that for female directors to fully realise their potentials and impacts, the board should have at least three female directors (Adusei & Obeng, Citation2019). A few prior studies also support the Critical Mass level of female board representation on other firm outcomes, e.g., financial performance, earnings management and financial fragility (Fan et al., Citation2019; Joecks et al., Citation2013; Terjesen et al., Citation2009). For example, a study by Joecks et al. (Citation2013) examines the effects of board gender diversity on performance of 151 German-listed firms covering the period from 2000 to 2005. They reported a U-shape relationship between female representation in the boardroom and corporate performance. This indicates that the positive effect of female directors only comes into place if there is at least 30% of females on board (equivalent to 3 female directors on average). Any lower fraction would indeed reduce the firm performance instead. Another study in which female on board effect is also examined to influence bank earnings management (Fan et al., Citation2019). The findings indicate that firms with a boardroom of more women (specifically three or more female directors), the earnings are less likely to be manipulated. Hence, the U-shape has been once again confirmed with a similar “magic number” of three female directors on board. Most recently, a study by Terzani et al. (Citation2020) has also supported the “critical mass” notion of board gender diversity on leverage level. The study was conducted on 268 Italian family firms from 2016 to 2018 and reported that firm’s leverage only reduces with three or more female directors in the boardroom.

To our knowledge, the extant studies have omitted the potential non-linear association of female representation on boards, which is an interest of this study. Accordingly, we are among the first empirical studies that examine this Critical Mass level of female presence on boards within the financing decision-making process. We argue that the effects of female representation on a firm’s capital structure may not come to fruition until a “critical mass” of female proportion on the board is reached, leading to the following hypothesis to be tested:

H2: A critical mass of female directors has a negative influence on debt financing level.

2.3. Board gender diversity and cost of equity

Cost of equity could be understood as either the cost of investors’ funds that firms raise or the returns required by investors for holding shares of companies. Lowering the cost of equity, an imperative component of the overall cost of capital, can greatly assist the achievement of the core shareholders value maximisation goal of corporations. Previous studies have reported the role of gender diversity board in increasing voluntary disclosure of firms’ information, which reduces the information asymmetry in equity market (Abad et al., Citation2017); enhancing the informativeness of stock prices (Gul et al., Citation2011); reducing adverse selection problems in security markets (Cai et al., Citation2006); and firm’s equity risk measuring by stock return volatility (Jizi & Nehme, Citation2017). These studies imply positive influences of board gender diversity on the equity markets, which indirectly signal a lower cost of equity. For example, Beyer et al. (Citation2010, p. 314) suggested that “the cost of equity capital is increasing in the level of information asymmetry”. In other words, increased voluntary disclosure, and reduced information asymmetry are associated with lower cost of equity (Albarrak et al., Citation2019, Citation2020).

Moreover, previous studies have documented that investors require lower cost of capital for firm with better transparency (e.g., Diamond and Verrechhia, Citation1991). Other literature (Botosan, Citation1997; Gietzmann & Ireland, Citation2005) point out that the quality of corporate financial reporting is as important to equity holder as debt holders. However, “the value of transparency is a function of a firm’s overall operating environment and organizational structure” (Upadhyay & Sriram, Citation2011, p. 1242). If gender diversity can improve the transparency of firm financial report, then investors would ask lower rate of return for their investment. Female presence should also provide better management monitoring role (Campbell & Mínguez-Vera, Citation2008; Gull et al., Citation2018). When the firm has better management monitoring, it should lead to management to make better decisions and have lower managerial opportunisms which can improve firm performance (Ashbaugh et al., Citation2004). Therefore, market participants should value these firms with an increase in stock value, and hence, lower their cost of equity. Therefore, we expect a negative association between board gender diversity and firm cost of equity. Consequently, the following hypothesis will be tested:

H3: Firms with higher proportion of females on board exhibit lower cost of equity

2.4. Board gender diversity and cost of equity: Mediating effect of debt financing decision

Nevertheless, what remains unclear in the literature now is whether the more conservative capital structure (i.e., lower debt levels) of female-led firms is perceived as a better and more appropriate financial decision. Hence, the subsequent objective of our study is to investigate the influence of debt financing decisions of female-led firms on their cost of equity. In other words, we examine the mediating effect of debt financing decisions on the relationship between board gender diversity and cost of equity.

It is indeed worth noting that in general, cost of equity may be reduced with higher female representation on board as hinted by the literature. This implies that investors positively value the presence of female on board. Nevertheless, it is not clear whether the investors positively value the financing decisions made by female-led firms, i.e., whether the negative female-equity cost association (fully/partially) functions through female’s financing decisions.

According to cognitive and behavioural studies, individual stakeholders exhibit different beliefs, perceptions, and thoughts which tend to be subjective rather than objective reality (Krueger & Brazeal, Citation1994). Therefore, providing these contradictory interpretations, different stakeholders may possess different judgements on whether to support or go against the lower leverage decisions of female-led firms. There are a number of factors that may influence their judgements comprising both objective and subjective factors. Regarding the former, rational investors should thoroughly analyse all information related to the firms, e.g., financial performance and positions, calibrate the firms’ optimal leverage level, current levels of agency cost and so on, before making judgment on the financial choices of female-led firms. On the other hand, subjective factors can be stakeholders’ attitudes toward risk, risk perceptions, other heuristics such as representativeness and availability (Kahneman and Tversky, Citation1972).

With much recent but extensive empirical evidence reported from academics and practitioners together with the resource dependence theory (e.g., J. Chen et al., Citation2017; Dezsö & Ross, Citation2012; Karavitis et al., Citation2019; Liu et al., Citation2014; Perryman et al., Citation2016; Strøm et al., Citation2014), female directors on corporate boards have been consistently reported to be positively related to firm key decisions. Campbell and Mínguez-Vera (Citation2008) support the critical role of female directors in the risk management process and firm policies. They are found to be more responsible and conscientious (Parrotta & Smith, Citation2013; Schmitt et al., Citation2008), more risk-averse and hence engaging in less risky projects (J. Chen et al., Citation2017; Croson & Gneezy, Citation2009), and less overconfident compared to men (Barber & Odean, Citation2001; Johnson et al., Citation2006).

Provided those among many positive characteristics of female directors, shareholders are subjected to a favourable representative image of highly female-represented firms. According to the representativeness and anchoring biases,Footnote4 shareholders’ faith and trust have been developed over time regarding corporate decisions made by highly female-represented firms, including their lower debt financing decisions (Tversky & Kahneman, Citation1974). Hence, they are likely to support and believe in the value-added contributions of female directors in enhancing the firms’ financing strategies. Consequently, the shareholders may require a lower equity premium to hold the firms’ stakes, leading to a decreased cost of equity. Therefore, the following hypothesis will be tested:

H4: Debt financing decision is significantly mediated the negative association between proportion of female on board and cost of equity

3. Data sources and sample selection

Our sample of US-listed firms is compiled from different sources, including BoardEx, IBES, Compustat, the Center for Research in Security Price (CRSP), and the Wharton Research Data Service (WRDS). Our ultimate sample consists of 4619 firm-year observations of 652 firms that are listed on three US stock markets (i.e., NYSE, NASDAQ, and AMEX) for the period from 2008 to 2019. Following the study of Sila et al. (Citation2016), we do not require the panel sample to be balanced. Also, financial firms and services are excluded from our sample due to their different characteristics (i.e., business models, products, and services), corporate governance mechanisms, and agency problems. To construct the cost of equity measures, we require all firms in our sample to have positive median forecasts of earnings per share for two subsequent years ahead (FEPS1 and FEPS2). These earnings forecasts are collected 6 months after the fiscal year end of each year to ensure that analysts have assimilated in their forecasts all the information from the fiscal year report. Our sample criteria require all firms to have available the cost of equity estimates. We obtain our corporate governance data including board gender diversity from the BoardEx database, which covers NYSE, NASDAQ, and AMEX firms. We then consolidate the data into firm-level variables, which are collected from IBES, Compustat, CRSP, and WRDS.

4. Variable definitions and methodology

4.1. Measurements of cost of equity

We measure the implied cost of equity (COE) based on averaging four commonly implied COE estimates as developed by Claus and Thomas (Citation2001)—RCT; Gebhardt, Lee, and Swaminathan (Citation2001)—RGLS; Ohlson and Juettner-Nauroth (Citation2005)—ROJN; and the Modified Easton (Citation2004) module by Gode and Mohanram (Citation2003)—RMPEG. These measurements of COE are based on analysts’ earnings forecast and current stock prices. In addition, RCT and RGLS models are based on a residual income valuation model, whereas ROJN and RMPEG are based on earnings growth models. The measurements were developed based on different assumptions of future growth, underlying estimated models and forecasting horizons. To conduct these measures, we require the following variables: Pt (Share price after 6 months of a firm’s fiscal year end), FEPSt+i (Forecasted earnings per share for year t + i), FROEt+i (Forecasted return on earnings for year t + i), Payout (Dividend pay-out forecast at year t, this variable is measured using the average of a firm’s dividend payout in the last 3 years. If this number is missing or greater than one or zero, we use the year-industry dividend payout average), Bt (Book value of share for the last fiscal year), Bt+I (Forecasted book value of share for year t + i, this variable is measured by using clean surplus (, LTG (Long-term forecast of earnings growth at year t and, if the value is missing, LTG is equal to

), and Rf (risk free rate, measured by the yield on 10-years treasury bonds).

We require firms to have positive median FEPS1 and FEPS2 and LTG. However, in case the medians of FEPS3, FEPS4 and FEPS5 are missing, we substitute the measures using the following equation:

The specific model descriptions to construct the four implied cost of equity components are explained as follows:

4.1.1. Model 1: Claus and Thomas (Citation2001)—RCT

Claus and Thomas (Citation2001) assume clean surplus accounting. It also allows a share price to be expressed in regard to book value and forecasted residual earnings. This model uses a 5-year horizon of forecasted earnings per shares (FEPS1, FEPS2, FEPS3, FEPS4 and FEPS5) and beyond these years, forecasts earnings residual grows at inflation rate. The forecasted earnings per share for the fourth and fifth years (FEPS4 and FEPS5) are estimated by the forecast earnings per share of the 3rd year (FEPS3) and the growth rate of long-term earnings (LTG). If the long-term growth rate is missing, the growth rate between FEPSt+2 and FEPSt+3 is used. The long-term abnormal earning growth rate is measured as 10 years of Treasury bonds minus 3%.

4.1.2. Model 2: Gebhardt, Lee, and Swaminathan (Citation2001)—RGLS

Gebhardt et al.’s (Citation2001) model assumes clean surplus accounting. The model also expresses share price in regard to book value, forecasted book values and forecasted return on equity (FROE). The model measures FROE by using analyst forecasts for the first 3 years. From the 4th to 12th number of years, FROE is equal to targeted ROE. Afterward, specifically after 12 years, ROE remains constant. However, FROE for the first three years is equal to (). From the 4th year to 12th years, FROE is equal to the year-industry median. If this ratio is negative, we replace it with the year median. The model uses 48 industries as classified by Fama and French (Citation1997).

4.1.3. Model 3: Modified Easton (Citation2004) COE module by Gode and Mohanram (Citation2003)—RMPEG

This model allows the current share price to be expressed with regard to 1 and 2 years of forecasted earnings per share (FEPS1 and FEPS2) and the expected dividend payout. This model assumes forecasted abnormal earnings to grow at a constant level after a 2-year horizon. The model requires RMPEG to be positive.

4.1.4. Model 4: Ohlson and Juettner-Nauroth (Citation2005)—ROJN

where

where DEPS t+1 = Dividend per share for the next year computed as payout ratio for firms with positive earning. is the average of the short-term earnings growth rate (

) and the long-term growth rate of analysts’ forecasts (LTG).

subtracts the 10-year treasury bonds yield from 3%. This model is generalized as an extension of Gordon’s constant model. The model also expresses the share price with forecasted earnings per share and perpetual growth rate. The model uses a one-year horizon for forecasted earnings per share and then assumes a growth rate to perpetual rate which is equal to expected inflation rate. This model requires both FEPSt+1 and FEPSt+2 to be greater than zero and have a positive value.

The ex-ante cost of equity has become more popular in academic research, as realised returns consider poor proxies for COE (Boubakri et al., Citation2018; K. C. Chen et al., Citation2009; Dhaliwal et al., Citation2016; El Ghoul et al., Citation2011). Following existing literature (Boubakri et al., Citation2018; Dhaliwal et al., Citation2006; El Ghoul et al., Citation2018), we use the average of four COE estimates to mitigate the measurement error in the COE. This estimate allows growth and cash flow to be differentiated and variation in the time-series of expected returns (Albarrak et al., Citation2020, Citation2019; K. C. Chen et al., Citation2009; Pástor et al., Citation2008).

4.2. Empirical specification

To examine the impacts of board gender diversity on the capital structure and cost of equity, we estimate the two following baseline estimation models:

captures the financing decision of a firm i for year t. We employ three different measures of

, including total debt to total assets (Debt/TA); total long-term debt to total assets (LT_Debt/TA), and total short-term debt to total assets (ST_Debt/TA). These three proxies of the dependent variable focus on the book value of corporate leverage adoption, providing the fraction of debt to firm total value.

is the average cost of equity of firm i at time t. As described in Section 2.2, the main COE measure (

) is the average value of four implied cost of equity components, i.e., COE_OJN, COE_GLS, COE_RCT, and COR_Pout.

represents the proportion of female directors on the board of firm i in year t. It is computed by dividing the number of female directors by the total number of board members. Based on our preliminary univariate tests (discussed in Section 2.4), non-linear effects of board gender diversity are indicated. Therefore, we employ the square term of

, i.e.,

to capture such non-linear effects.

represents a list of control variables which potentially affect the firm capital structure (Model 1) and the cost of equity (Model 2). Finally,

represents year-fixed effects.

We consider some controlling variables that are expected to influence the firm’s capital structures and cost of equity. These variables include stock return beta (denoted as Beta) which is measured based on a market model.Footnote5 We expect a positive association between Beta and COE (El Ghoul et al., Citation2018). Firm size has also suggested to be negatively correlated with the implied cost of equity (Botosan & Plumlee, Citation2005; K. C. Chen et al., Citation2009; El Ghoul et al., Citation2011). That is, bigger sized firms have a lower cost of equity and the inverse is true (Albarrak et al., Citation2020, Citation2019). We measure the firm size (LogTA) by a natural logarithm of total asset values. Our control variables also include book values per share outstanding (BV_Share) and proportion of property, plant, and equipment to total assets (PPE/Assets). We also control for firm performance indicators, including the return on assets (ROA) and turnover ratio (Sale/Assets; Ng & Rezaee, Citation2015). We control for analysts’ forecast dispersion (DISP) which we expect to be positively associated with COE (Dhaliwal, Krull and Li, Citation2005; He et al., Citation2013). DISP is measured as the standard deviation of earnings per share forecast for a year ahead. Furthermore, we control for analysts’ forecast of long-term earnings growth (LTG), which is suggested to be positively associated with the cost of equity (Dhaliwal et al., Citation2005). Other corporate governance variables are also taken into account, including the proportion of independent directors on a board (%IND), the presence of CEO-Chairman duality (B_Dual) and a CEO’s tenure (CEO_BTenure; K. C. Chen et al., Citation2009; Reverte, Citation2009; Setiany et al., Citation2017). Detailed definitions and measures of all variables are provided in Appendix A.

Moreover, to investigate the shareholders’ views on the financing decisions made by firms with high female-represented board, we employ the Baron and Kenny’s (Citation1986) four-step mediation model to examine the mediating effects of the capital structure on the influences of board gender diversity on the cost of equity. We perform the mediating tests using the OLS robust standard error and generalised method of moments (GMM) to tackle potential endogeneity issues. The four steps are described as follows:

Step 1: Board gender diversity on the capital structure

Step 2: Capital structure on the cost of equity

Step 3: Board gender diversity on the cost of equity

Step 4: Board gender diversity and capital structure on the cost of equity

For a mediating effect to be concluded, the key regressors in Equationequations 3(3)

(3) –Equation5

(5)

(5) (i.e., %Female, Debt/TA, and %Female, respectively) should be statistically significant. In step 4 (equation 6), if after controlling for capital structure (Debt/TA) in the same model and the effect of board gender diversity (%Female) becomes insignificant, we can conclude a full mediating effect of the capital structure. On the other hand, if variable %Female remains significant yet with a weaker magnitude, a partial mediating effect of the capital structure is concluded. We further confirm whether the indirect effects of females on the cost of equity through the capital structure are different from zero, using the Sobel, Aroian and Goodman tests (Baron & Kenny, Citation1986; Sobel, Citation1982; Goodman, Citation1960).

5. Empirical results

5.1. Descriptive statistics

provides summary statistics for all variables employed in our empirical models. Regarding measures of the cost of equity, this table shows details on the single COE measure and its components. The t-test analyses on the differences in each variable between firms with and without females on their board are also provided. Female representation in boards takes up around 13.7% on average, with the highest-scoring firms (66.7% and 50%) not appointing any female directors to their boards. On average, the cost of equity of our firm sample is around 7.8% with components’ mean cost of equity ranges from 1.5% (COE_OJN) to 16.7% (CEO_Pout). Firms without females on their board are generally exposed to a higher cost of equity, which is statistically significant at a 1% critical level. The same pattern holds for the single COE measure and its component, except for COE_Pout (but not significant).

Table 1. Descriptive statistics

The summary statistics reveal the full picture of our firm sample by considering other financial and governance characteristics. The mean value of capital structure (Debt/TA) is around 20%, for the full sample. However, the bivariable t-test analysis reveals a significantly higher debt level of firms with a female presence on their board. This may be a result of statistical drawbacks of the t-test as other determinants of leverage are not accounted for and non-linear relationship is disregarded. Therefore, more detailed discussions will be provided based on multivariate analyses in subsequent sections for a clearer picture. Interestingly, firms with (more) female directors are bigger, with a more fixed assets percentage, have a larger board size, a higher independent member percentage, a book value of share, and have a lower market risk, return, and long-term growth rate. The results show that firms with a more powerful CEO (proxied by CEO tenure) do not tend to appoint female members on the board compared to firms with a less powerful CEO.

reports the Pearson correlation matrix among the independent variables which can be used as a preliminary indicator for a multicollinearity issue. The results indicate the absence of a multicollinearity issue, as there is no noticeably strong correlation between the key variables. We further employ the variance inflation factors (VIFs), which also show no multicollinearity problems among the regressors.Footnote6 Our female variable (%Female) is positively correlated with LogBSize, %IND, LogTA, BV_Share, and PPE/Assets, but negatively associated CEO_BTenure.

Table 2. Correlation matrix

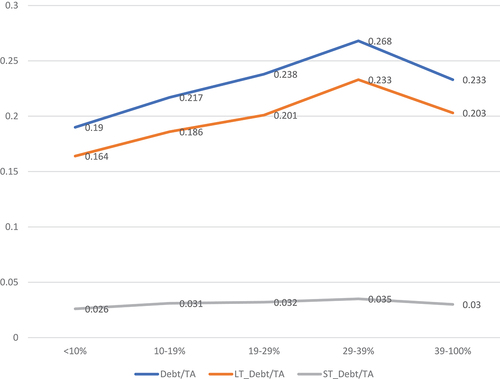

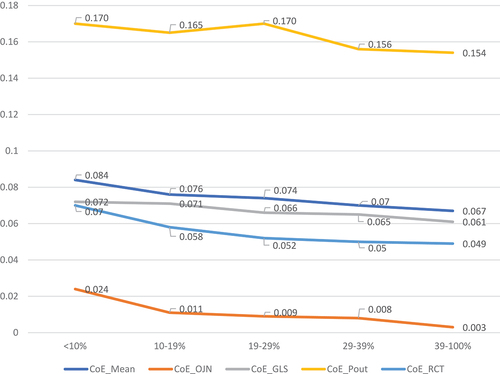

To preliminarily analyse the association between board gender diversity and capital structure and the cost of equity, presents a trend analysis describing the changes in financing structures (i.e., Debt/TA, LT_Debt/TA, and ST_Debt/TA) and cost of equity (i.e., COE_Mean, COE_OJN, COE_GLS, COE_RCT, and COE_Pout). We visually observe a generally non-linear relationship between female representation and debt levels, whilst the measures of cost of equity reveal gradual reductions with the proportions of female on a board. These variation patterns are depicted in , which is provided in Appendix B. Particularly, the debt levels (both total debt and long-term debt) initially increase and then decrease after a quarter of the board size is filled with female directors. The line graph () also shows a relatively stable pattern of short-term debts across different levels of female representation in board. Regarding the cost of equity, depicts general declines in the main cost of equity measure (COE_Mean) and its components across proportions of female directors. This bivariate trend analysis cannot rule out the potential influences of other firm-specific characteristics on firms’ cost of equity and capital structure. Nevertheless, it signifies the relevance of the non-relationships between board gender diversity and our dependent variables, which is controlled for in our main models (Equationequations 1(1)

(1) and Equation2

(2)

(2) ).

Table 3. Trend analysis: Firm capital structure and cost of equity by the interval categories of % female directors

Figure 1. Firm capital structure by the interval categories of % female directors.

Figure 2. Firm cost of equity by the interval categories of % female directors.

5.2. Effects of board gender diversity on firm capital structure

visualises the results for the regressions explaining the firm leverage levels, measured respectively by total debt over total asset (Debt/TA), total long-term debt over total asset (LT_Debt/TA), and total short-term debt over total asset (ST_Debt/TA). We test whether a board with a higher percentage of females is associated with lower leverage level. Panel A presents the findings using the Ordinary Least Square (OLS) robust standard error estimation, whereas Panel B shows the results of examining the board gender diversity impacts on the three debt measures using the Generalised Method of Moments (GMM) to control for any endogeneity problem. In columns 1–2, board gender diversity is significantly and positively related to the first two leverage ratios (i.e., Debt/TA; LT_Debt/TA) at the 1% level or better. Economically, an increase of 1% in the proportion of female directors on a board is associated with a 22% increase in total-debt-to-total-assets ratio (β%Female = 0.221, column 1), and with a 23% increase in the fraction of long-term debt over total asset (β%Female = 0.229, column 2). Our results support the first hypothesis H1.

Table 4. Effects of board gender diversity on firm capital structure

Interestingly, the analysis captures a significant non-linear effect of female representation on a board by revealing the negative significant coefficients of the quadratic terms of the fraction of female directors (%Female).2 This provides evidence supporting our second hypothesis (H2). According to the coefficients of (%Female)2 in column 1 and 2, the results suggest that if a firm’s board contains up to approximately 28% of female directors, the increase in the debt level (for both measures) is marginally diminishing and will start to fall when the proportion of females goes beyond that level. This finding signifies that, as a minority gender group on board, the level of representation is critical in exercising the board control. According to the literature (e.g., Palvia, et al., ,Citation2015), male directors are more risk-friendly compared to female directors; thus, they tend to adopt riskier financing choices. Since firms gradually appoint female directors to boards, it is challenging for a trivial female representation to alter the board cultures and decisions instantly and dramatically. Furthermore, it is possible that the minority female group in the board may increase the exposure to initial conflicts and possible “bullying” within the board (see Eriksen & Einarsen, Citation2004; Lee et al., Citation2013). Therefore, the majority male group may exercise their power and dominance within a board to go against the opinions or views of the minority female group, leading to higher debt levels. Nevertheless, as the proportion of females gradually increases, their influences on a board start being realised through the diminishing marginal debt levels. Eventually, when the female representation increases up to a “critical mass” level and so do their board influences, the debt levels decrease. Similarly, non-linear patterns were obtained for the relationships between female fractions on boards and firm performances such that firms perform worse once female directors are initially appointed on a board and subsequently perform better after female representation reaches about 30% (Joecks et al., Citation2013). Farag and Mallin (Citation2017) and Fan et al. (Citation2019) also find that firms are more financially fragile and earnings prone to manipulation when the proportion of females on a board is trivial. However, the situation is reversed once the female share reaches a critical mass of around 21–30%. As (column 3) importantly suggests, the board gender diversity is not significant in explaining short-term-debt-to-total-assets ratio. In other words, the results indicate that firms with a more gender-diversified board are more likely to mitigate the total debt levels through long-term debt instruments rather than short-term debts.

Panel B in the table is consistent with our main results. The validity tests confirm that our GMM estimator is valid. The first-order serial correlation (AR (1)) confirms that the residuals in the first differences are correlated, as the p-value <5% is significant. Furthermore, the second-order correlation (AR (2)) and Hansen tests of overidentification are not significant, which indicate that there is no serial correlation of second differences and our instruments are valid (see Aljughaiman & Salama, Citation2019; Elnahass et al., Citation2020; VQ Trinh et al., Citation2020a,b,c). Overall, there is strong and consistent evidence supporting our expectation that board gender diversity contributes to the lower debt levels of firms as stated in many prior studies. Nevertheless, instead of an instantaneous influence, we find that the gender effects are realised marginally as the representation of females on boards increases toward a “critical mass” level, i.e., approximately a quarter of the board.

Moving onto the control variables, the results show positive relationships between logTA, PPE/Assets, and debts level indicating that larger firms acquire higher debt levels. This is consistent with previous literature discussing that big firms are less financially constrained, which allow them to take a higher leverage level due to their reputation. In contrast, Beta_Industry, DISP, BV_Share, and Sales/Assets have a significantly negative effect on the leverage level. Importantly, all the corporate governance characteristics are significant. In line with Abobakr and Khairy Elgiziry (Citation2016), we find a negative effect of the board size on the leverage level. We also find that board independence and CEO duality (B_Duality) decrease the leverage level. CEO tenure also has a negative relationship with the firms leverage level. This indicates that more CEO power decreases the debt level at the firm. However, the corporate governance variables assure that stronger monitoring governance mechanism tends to reduce the risk of using excessive leverage levels.

5.3. Effects of board gender diversity on firm cost of equity

contains the results on the influence of board gender diversity on firm cost of equity. The literature within this topic has been overlooked despite the relevance of cost of equity as an imperative component of the firm overall cost of capital. Lowering the cost of equity can greatly assist the achievement of the core value maximisation goal of corporations. Nevertheless, as mentioned, there is an abundance of prior studies that have provided indications on the negative association between board gender diversity and firm cost of equity through many positive equity-related contributions that female directors bring to the firm board (Abad et al., Citation2017; Cai et al., Citation2006; Gul et al., Citation2011; Jizi & Nehme, Citation2017). Columns 1–5 in Panel A of Table present the associations between the female share on boards and five cost of equity measures (i.e., the main measure and its components). Overall, we obtain significant negative linear effects of female directors on board on firms’ cost of equity (β1 = −0.054, p-value < 0.05; β2 = 0.082, n.s), supporting the third hypothesis (H3). In the contexts of a firm’s corporate decisions, female representation needs to be sufficiently critical to alter the board decisions made by the male majority group. The cost of equity is the required return of shareholders which is adjusted based on their perceptions of positive contributions made by female directors. This is to say, shareholders may value the positive contributions of female directors on boards in balancing the board cultures and especially, in preventing the firms to become exposed to excessive risk-taking through their more risk-averse characteristics.

Table 5. Effects of board gender diversity on firm cost of equity

Across the four cost of equity components, the same patterns are obtained for the COE_OJN and COE_GLS, whilst COE_Pout (column 5) does not show significant effects of board gender diversity. For COE_RCT, non-linear effects of female directors are detected. Particularly, the implied cost of equity initially decreases with the proportion of females on boards and subsequently increase after the female ratio reaches roughly 40%. It is possible that shareholders are aware of the added value of female directors’ risk aversion nature in mitigating the potential “excessive” risk-taking behaviours of firms, and thus lowering their required return rates. Nevertheless, as females exceed the critical mass, their risk aversion may lead the firms to operate conservatively, which may not be favourable to shareholders. Particularly, debt financing instruments exhibit the tax shield and ownership retaining property. Too conservative boards may cause the firms to fail in taking advantages of this financing instrument, hence negatively affecting the shareholders’ interests, leading to an increasing cost of equity. Generally, the computations of these cost of equity measures are based on different models and assumptions, leading to different findings. The literature has not agreed on the best measure to be used; therefore, we build our conclusion on the main cost of equity measure (COE_Mean; K. C. Chen et al., Citation2009).

In column 6 of Panel A, we further control for the non-linear effect of female director fraction (%Female)2 on COE_Mean. As expected, the coefficient of the quadratic term is not statistically significant (= 0.078) whilst the linear term of %Female remains negatively significant at the 5% level. Overall, this has verified the indications from the literature on the female-COE relationship. Specifically, shareholders tend to require lower required returns for firms with more female-diversified boards. This may be that shareholders acknowledge female directors’ efforts and contributions to the corporations in managing the firm risk to an appropriate lower level even when they only hold a trivial stake within boards. Employing a valid GMM estimator as indicated by AR(1), AR(2) and the Hansen test, Panel B of reveals consistent findings on the linear influences of board gender diversity on firm cost of equity (β%Female = −0.202, p-value = 0.05;

= 0.078, n.s).

5.4. Mediating effects of capital structure on the relationship between board gender diversity and firm cost of equity

We have obtained two mosaics: firms with stronger female-diversified boards tend to (1) adopt less risky financing choice by employing lower debt financing instruments and (2) have lower cost of equity. In this section, we aim to arrange and integrate these two mosaics into one unified framework by examining whether highly female-represented firms achieve a lower cost of equity through their lower debt strategies. presents OLS and GMM regression results for the Baron and Kenny’s (Citation1986) 4-step mediation model (Panel A and Panel B respectively). In step 1 (column 1, ), the Debt/TA is regressed on %Female to test for the indirect effects of female directors.

Table 6. Four-step mediating effects: board gender diversity, capital structure and firm cost of equity

The results indicate that female representation exhibits a significant concave relationship with a firm leverage level at the 1% critical level. This step has been confirmed and discussed in Section 4.2. Proceeding to step 2 of the mediation test (column 2, ), we perform a regression where COE_Mean is the criterion variable in the equation and Debt/TA is the predictor. In this step, the mediating factor Debt/TA is treated as an outcome variable. We found a positive effect of Debt/TA on COE_Mean at the 1% level, indicating that the higher the debt levels firms adopt, the higher the cost of equity (βDebt/TA = 0.030). This direction of influence is supported by the literature as higher debt is associated with a higher bankruptcy risk due to higher periodic payment obligations putting downward pressure on the firm financial budget. Subsequently, the third step measures the direct effect of %Female on the cost of equity (CEO_Mean) that may be mediated.

As reported previously in Section 4.3, higher female representation in boards is likely to lower the firm cost of equity. These first three steps have revealed their statistically significant pathway indicating a mediating effect of the capital structure on the influences of female director presence on the cost of equity. In the final step of the analysis, we regressed the cost of equity (CEO_Mean) on both female fraction (%Female) and firm total-debt-to-assets ratio (Debt/TA) to determine if the mediating effect is full or partial. In column 4 of , the effect of Debt/TA are statistically positively significant at the 1% level or below (βDebt/TA = 0.060), whilst the effects of %Female lost its significance (β%Female = −0.031). This signifies a full mediating effect of firm financing choices and supports our final hypothesis (H4). Particularly, board gender diversity lowers the cost of equity substantially through their lower leverage and the indirect effect takes up approximately 45%.

We further employ the Sobel test, Aroian test and Goodman test to examine if the indirect effect of female representation on boards on the cost of equity via the firm capital structure is significantly different from zero (Baron & Kenny, Citation1986; Sobel, Citation1982; Goodman, Citation1960) All the three tests indicates the indirect effect is statistically significant at the 1% critical level (Statsobel = 2.91, StatAroian = 2.89, and StatGoodman = 2.93). Panel B of repeats the above four steps using the GMM analysis to tackle the potential issue of endogeneity for a more robust result. Generally, all the mediation pathways (columns 5–8) are consistent with the OLS method and all validity tests confirm our GMM estimator. Similarly, we calculate that the indirect effect revealed in this method with β%Female = −0.193 (step 3, column 7) and β%Female = −0.097 (step 4, column 8) reached 50% of the female influence on the cost of equity, which is similar to the results obtained in OLS estimations. This indirect effect appears to be statistically significant at the 1% critical level. GMM results might be more robust as we control for all types of endogeneity problems (i.e., reverse causality, omitted-variables bias, and measurement error in the repressor), and the findings remain unchanged.

5.5. Propensity score matching

To identify a causal effect of the representation of female directors on boards on the capital structure and cost of equity, the analysis exposes a potential issue of sample selection bias and possible endogeneity for the board gender diversity variable. For a better risk management and financial performance, managers are urged to adjust the firm risk through lower leverage and achieve a lower cost of equity. Therefore, they may appoint more female-represented firms due to their well-known nurturing, conscious, and risk-averse natures. In this case, the proportion of female on board may be an endogenous factor. To address this concern, we further employ the propensity score matching (Rosenbaum and Rubin, Citation1983), whereby firm-years with female representation (treatment group) match with those without females on the board (control group) which have relatively matching characteristics.

compares the cost of equity for firms with female directors and firms without female directors that have been matched with the former using the propensity score matching method. To accomplish this, we follow three steps. First, we employ the probit technique to estimate the propensity score for firms having females on their board (treatment group) and those having no females on their board (control group). After the estimated propensity score of the treated and control groups are obtained, we match the samples using four alternative methods: one-to-one nearest neighbour matching with and without replacement and nearest neighbour matching with n = 2 with replacement. Consequently, we can match the observation of the treatment group with the one of controlled group using the previous techniques we discussed previously. Lastly, we investigate the average impact of board gender diversity on the cost of equity and capital structure using the matched sample. Panels A and B in this table report the univariate analysis and panel C presents the multivariate results. Both panels (A and B) indicate that the cost of equity (debt levels) is lower (higher) for firms with female presence on the board than firms without female presence on the board. Panel C confirms our main results in (female-debt) and (female-cost of equity); whilst there is a significantly positive relationship between the female presence on the board and debt levels for the matched sample, such female representation is negatively associated with firm cost of equity.

Table 7. Propensity score matching (PSM) on the effect of board gender diversity on firm cost of equity and capital structure

6. Conclusion

In this study, we employed a sample of firms listed in the NYSE, NASDAQ and AMEX stock exchange markets for the period from 2008 to 2019 with 4,619 firm-year observations to examine the influences of board gender diversity on financing decisions and the cost of equity. We also aimed to unify our findings to confirm if shareholders adjust their cost of equity based on the capital structure adopted by firms with a high female representation. We conduct our analyses on the baseline OLS robust standard error estimation method with further robustness checks using the generalised method of moments (GMM) and propensity score matching (PSM) to consider potential endogeneity issues and sample selection bias. After controlling for governance-related and financial factors, we obtained three main findings. First, we found that firms with more female directors on board tend to adopt lower debt levels due to their risk-averse natures. Nevertheless, such less risky financing decisions only take place after the female representation reaches a critical mass level of around 28%. Before this level, the debt levels are diminishingly increased. This may be because the minority female group does not have sufficient power to make influences on the board decisions. Second, we found that shareholders indeed value the presence of females on boards in general and tend to reduce their required return rates as the proportion of females on the board increases. Third, we examined whether shareholders have positive views on the capital structures of highly female-represented firms by conducting the Baron and Kenny (Citation1986) mediation test. Intriguingly, we found that shareholders’ decisions to lower their required returns are based on the capital structure of firms with greater female representation. This implies that shareholders view positively the financing decisions made by firms with more female directors on board. Possibly, they believe that the more risk-averse, nurturing, and careful natures of (female) directors can prevent firms from adopting excessively risky financing structures.

Numerous existing evidence have focused on the effects of female directors on dividends policy (e.g., J. Chen et al., Citation2017; Trinh et al., Citation2020c) and/or those on financial performance and the firm’s risk-taking behaviour (e.g., Adusei & Obeng, Citation2019; Yang et al., Citation2019). However, the linkage between board gender diversity and the firm’s debt financing decision and cost of equity are extremely limited despite their importance in determining firms’ overall cost of capital and in turn, shareholder wealth. To the very best of our knowledge, no research till date has placed on examining such association particularly for US-listed firms, and more importantly, discovering critical underlying channels (debt financing decision, in our study) through which the gender diversity could affect the cost of equity. Consequently, our study has filled this void. We are the first to examine whether the capital structure decisions made by firms with a high share of females on boards are perceived positively by the shareholders. Particularly, risk-averse decisions generally are not favourable to shareholders, especially debt financing exhibits tax shield and ownership concentration properties. Nevertheless, if shareholders believe that the more risk-averse nature of female directors can prevent firms from becoming exposed to excessive bankruptcy risks by taking high debt levels, they are likely to lower their required returns.

Our findings provide several important implications for firms in balancing the gender ratio within their boards to level out their risk-taking through their financing decisions. For example, excessive debt levels can be disastrous for firms within financial turbulence periods such as financial crises, economics recessions and special crises like Covid-19 pandemic. Furthermore, we suggest that a more gender-balanced board can also assist in achieving the maximisation of shareholder’s wealth goal through lower costs of equity. The findings are also relevant for regulators, and investors (both existing and potential). Our study supports the notion of board diversity in the management literature, especially after the enactment of the Sarbanes-Oxley Act (SOX) of 2002, which has emphasized on the corporate board structure, specially, the inclusion of outsiders on board and on the main board committees (Zhang et al., Citation2013). A noticeable fact is that although representation of female directors on board is not exclusively mentioned in the act, the presence of female on board has been found to be substantially increased (Linck et al., Citation2009). This is to say, the post-SOX era has heightened the awareness of investors on the importance of board gender diversity. Further support by this study, our findings enhance the trust and confidence of investors on firms led by high female-represented boards, particularly, on firm cost of equity, and on the general positive perceptions of the market participants on those firms. Additionally, they also encourage regulators to consider enacting similar acts as the SOX focusing on the diversity in board “surface” structure.

Acknowledgements

The authors extend their appreciation to the Deanship of Scientific Research at King Faisal University in Saudi Arabia for funding this research through project number (207013).

Disclosure statement

Declarations of interest: none. This manuscript has not been published and is not under consideration for publication elsewhere.

Additional information

Funding

Notes

1. For example, the UK corporate governance encourages females to represent a third of the UK boardroom positions by the end of 2020 (Austin, Citation2020; V. Trinh et al., Citation2018). Hellier and Chasan (Citation2018) find that Belgium, France, and Norway have passed the laws for the mandatory inclusion of female on corporate boards.

2. An increased voluntary disclosure, and subsequently reduced information asymmetry are associated with a lower cost of equity (Beyer et al., Citation2010; Boubakri et al., Citation2012; Albarrak et al., Citation2019, Citation2020).

3. Employing a short-cut and a benchmark value in judging a matter based on information available to us.

4. Employing a short-cut and a benchmark value in judging a matter based on information available to us.

5. Beta is estimated using the regression of 60 months’ estimation window, with no less than 24 months of stock return and market adjusted excess return. However, when Beta is missing, we use the Beta of the industry in which firms are operating.

6. There is no coefficient higher than 80% among the explanatory variables, also there is no value of VIF higher than 10.

References

- Abad, D., Lucas-Pérez, M. E., Minguez-Vera, A., & Yagüe, J. (2017). Does gender diversity on corporate boards reduce information asymmetry in equity markets? BRQ Business Research Quarterly, 20(3), 192–34. https://doi.org/10.1016/j.brq.2017.04.001

- Abobakr, M. G., & Elgiziry, K. (2015). The effect of board characteristics and ownership structure on the corporate financial leverage. Accounting and Finance Research, 5(1), 1. https://doi.org/10.5430/afr.v5n1p1

- Adams, R. B., & Ferreira, D. (2009). Women in the boardroom and their impact on governance and performance. Journal of Financial Economics, 94(2), 291–309. https://doi.org/10.1016/j.jfineco.2008.10.007

- Adams, R. B., & Funk, P. (2012). Beyond the glass ceiling: Does gender matter? Management Science, 58(2), 219–235. https://doi.org/10.1287/mnsc.1110.1452

- Adusei, M., & Obeng, E. Y. T. (2019). Board gender diversity and the capital structure of microfinance institutions: A global analysis. The Quarterly Review of Economics and Finance, 71, 258–269. https://doi.org/10.1016/j.qref.2018.09.006

- Aggarwal, R., & Goodell, J. (2014). Culture, institutions, and financing choices: How and why are they related? Research in International Business and Finance, 31, 101–111. https://doi.org/10.1016/j.ribaf.2013.09.002

- Albarrak, M. S., Elnahass, M., Papagiannidis, S., & Salama, A. (2020). The effect of twitter dissemination on cost of equity: A big data approach. International Journal of Information Management, 50, 1–16. https://doi.org/10.1016/j.ijinfomgt.2019.04.014

- Albarrak, M. S., Elnahass, M., & Salama, A. (2019). The effect of carbon dissemination on cost of equity. Business Strategy and the Environment, 28(6), 1179–1198. https://doi.org/10.1002/bse.2310

- Aljughaiman, A. A., & Salama, A. (2019). Do banks effectively manage their risks? The role of risk governance in the MENA region. Journal of Accounting and Public Policy, 38(5), 106680. https://doi.org/10.1016/j.jaccpubpol.2019.106680

- Alves, P., Couto, E. B., & Francisco, P. M. (2015). Board of directors’ composition and capital structure. Research in International Business and Finance, 35, 1–32. https://doi.org/10.1016/j.ribaf.2015.03.005

- Ashbaugh, H., Collins, D. W., & LaFond, R. (2004). Corporate governance and the cost of equity capital. Emory, University of Iowa.

- Austin Katy. (2020). Women hold third of board roles at top UK firms. Retrieved 20 March 2020, from https://www.bbc.co.uk/news/business-51417469

- Barber, B. M., & Odean, T. (2001). Boys will be boys: Gender, overconfidence, and common stock investment. Quarterly Journal of Economics, 116(1), 261–292. https://doi.org/10.1162/003355301556400

- Baron, R. M., & Kenny, D. A. (1986). The moderator–mediator variable distinction in social psychological research: Conceptual, strategic, and statistical considerations. Journal of Personality and Social Psychology, 51(6), 1173. https://doi.org/10.1037/0022-3514.51.6.1173

- Bear, S., Rahman, N., & Post, C. (2010). The impact of board diversity and gender composition on corporate social responsibility and firm reputation. Journal of Business Ethics, 97(2), 207–221. https://doi.org/10.1007/s10551-010-0505-2

- Berger, P. G., Ofek, E., & Yermack, D. L. (1997). Managerial entrenchment and capital structure decisions. The Journal of Finance, 52(4), 1411–1438. https://doi.org/10.1111/j.1540-6261.1997.tb01115.x

- Beyer, A., Cohen, D. A., Lys, T. Z., & Walther, B. R. (2010). The financial reporting environment: Review of the recent literature. Journal of Accounting and Economics, 50(2–3), 296–343.

- Botosan, C. A. (1997). Disclosure level and the cost of equity capital. Accounting Review, 72(3), 323–349.

- Botosan, C. A., & Plumlee, M. A. (2005). Assessing alternative proxies for the expected risk premium. The Accounting Review, 80(1), 21–53. https://doi.org/10.2308/accr.2005.80.1.21

- Boubakri, N., El Ghoul, S., Guedhami, O., & Megginson, W. L. (2018). The market value of government ownership. Journal of Corporate Finance, 50, 44–65. https://doi.org/10.1016/j.jcorpfin.2017.12.026

- Boubakri, N., Guedhami, O., Mishra, D., & Saffar, W. (2012). Political connections and the cost of equity capital. Journal of Corporate Finance, 18(3), 541–559. https://doi.org/10.1016/j.jcorpfin.2012.02.005

- Cai, C. X., Keasey, K., & Short, H. (2006). Corporate governance and information efficiency in security markets. European Financial Management, 12(5), 763–787. https://doi.org/10.1111/j.1468-036X.2006.00276.x

- Campbell, K., & Mínguez-Vera, A. (2008). Gender diversity in the boardroom and firm financial performance. Journal of Business Ethics, 83(3), 435–451. https://doi.org/10.1007/s10551-007-9630-y

- Carter, D. A., D’Souza, F., Simkins, B. J., & Simpson, W. G. (2010). The gender and ethnic diversity of US boards and board committees and firm financial performance. Corporate Governance: An International Review, 18(5), 396–414. https://doi.org/10.1111/j.1467-8683.2010.00809.x

- Chen, K. C., Chen, Z., & Wei, K. J. (2009). Legal protection of investors, corporate governance, and the cost of equity capital. Journal of Corporate Finance, 15(3), 273–289. https://doi.org/10.1016/j.jcorpfin.2009.01.001

- Chen, J., Leung, W. S., & Goergen, M. (2017). The impact of board gender composition on dividend payouts. Journal of Corporate Finance, 43, 86–105. https://doi.org/10.1016/j.jcorpfin.2017.01.001

- Clarke, C. J. (2005). The XX factor in the boardroom: Why women make better directors. Directors Monthly, 24, 8–10.

- Claus, J., & Thomas, J. (2001). Equity Premia as Low as Three Percent? Evidence from Analysts' Earnings Forecasts for Domestic and International Stock Markets. The Journal of Finance, 56(5), 1629–1666. https://doi.org/10.1111/0022-1082.00384

- Croson, R., & Gneezy, U. (2009). Gender differences in preferences. Journal of Economic Literature, 47(2), 448–474. https://doi.org/10.1257/jel.47.2.448

- Dezsö, C. L., & Ross, D. G. (2012). Does female representation in top management improve firm performance? A panel data investigation. Strategic Management Journal, 33(9), 1072–1089. https://doi.org/10.1002/smj.1955

- Dhaliwal, D., Heitzman, S., Zhen, L. I., & R, O. L. I. V. E. (2006). Taxes, leverage, and the cost of equity capital. Journal of Accounting Research, 44(4), 691–723. https://doi.org/10.1111/j.1475-679X.2006.00214.x

- Dhaliwal, D., Judd, J. S., Serfling, M., & Shaikh, S. (2016). Customer concentration risk and the cost of equity capital. Journal of Accounting and Economics, 61(1), 23–48. https://doi.org/10.1016/j.jacceco.2015.03.005

- Dhaliwal, D., Krull, L., Li, O. Z., & Moser, W. (2005). Dividend taxes and implied cost of equity capital. Journal of Accounting Research, 43(5), 675–708. https://doi.org/10.1111/j.1475-679X.2005.00186.x

- Diamond, D. W., & Verrecchia, R. E. (1991). Disclosure, Liquidity, and the Cost of Capital. The Journal of Finance, 46(4), 1325–1359. https://doi.org/10.1111/j.1540-6261.1991.tb04620.x

- Dobija, D., Hryckiewicz, A., Zaman, M., & Puławska, K. (2021). Critical mass and voice: board gender diversity and financial reporting quality. European Management Journal 40 1 29–44 .

- Easton, P. D. (2004). PE Ratios, PEG Ratios, and Estimating the Implied Expected Rate of Return on Equity Capital. The Accounting Review, 79(1), 73–95. https://doi.org/10.2308/accr.2004.79.1.73

- El Ghoul, S., Guedhami, O., Kim, H., & Park, K. (2018). Corporate environmental responsibility and the cost of capital: International evidence. Journal of Business Ethics, 149(2), 335–361. https://doi.org/10.1007/s10551-015-3005-6

- El Ghoul, S., Guedhami, O., Kwok, C. C., & Mishra, D. R. (2011). Does corporate social responsibility affect the cost of capital? Journal of Banking & Finance, 35(9), 2388–2406. https://doi.org/10.1016/j.jbankfin.2011.02.007

- Elnahass, M., Omoteso, K., Salama, A., & Trinh, V. Q. (2020). Differential market valuations of board busyness across alternative banking models. Review of Quantitative Finance and Accounting, 55(1), 201–238. https://doi.org/10.1007/s11156-019-00841-4

- Eriksen, W., & Einarsen, S. (2004). Gender minority as a risk factor of exposure to bullying at work: The case of male assistant nurses. European Journal of Work and Organizational Psychology, 13(4), 473–492. https://doi.org/10.1080/13594320444000173

- Faccio, M., Marchica, M.-T., & Mura, R. (2016). CEO gender, corporate risk-taking, and the efficiency of capital allocation. Journal of Corporate Finance, 39, 193–209. https://doi.org/10.1016/j.jcorpfin.2016.02.008

- Fama, E. F., & French, K. R. (1997). Industry costs of equity. Journal of Financial Economics, 43(2), 153–193. https://doi.org/10.1016/S0304-405X(96)00896-3

- Fan, Y., Jiang, Y., Zhang, X., & Zhou, Y. (2019). Women on boards and bank earnings management: From zero to hero. Journal of Banking & Finance, 107, 105607.

- Farag, H., & Mallin, C. (2017). Board diversity and financial fragility: Evidence from European banks. International Review of Financial Analysis, 49, 98–112. https://doi.org/10.1016/j.irfa.2016.12.002

- Fischer, E. O., Heinkel, R., & Zechner, J. (1989). Dynamic Capital Structure Choice: Theory and Tests. The Journal of Finance, 44(1), 19–40. https://doi.org/10.1111/j.1540-6261.1989.tb02402.x

- Friend, I., & Lang, L. H. (1988). An empirical test of the impact of managerial self‐interest on corporate capital structure. The Journal of Finance, 43(2), 271–281. https://doi.org/10.1111/j.1540-6261.1988.tb03938.x

- Gebhardt, W. R., Lee, C. M., & Swaminathan, B. (2001). Toward an Implied Cost of Capital. J Accounting Res, 39(1), 135–176. https://doi.org/10.1111/1475-679X.00007

- Gietzmann, M., & Ireland, J. (2005). Cost of capital, strategic disclosures and accounting choice. JOURNAL OF BUSINESS FINANCE & ACCOUNTING, 32(3‐4), 599–634. https://doi.org/10.1111/j.0306-686X.2005.00606.x

- Gode, D., & Mohanram, P. (2003). Inferring the cost of capital using the Ohlson–Juettner model. Review of Accounting Studies, 8(4), 399–431.

- Goodman, L. A. (1960). On the exact variance of products. Journal of The American Statistical Association, 55(292), 708–713. https://doi.org/10.1080/01621459.1960.10483369

- Gul, F. A., Srinidhi, B., & Ng, A. C. (2011). Does board gender diversity improve the informativeness of stock prices? Journal of Accounting and Economics, 51(3), 314–338. https://doi.org/10.1016/j.jacceco.2011.01.005

- Gull, A. A., Nekhili, M., Nagati, H., & Chtioui, T. (2018). Beyond gender diversity: How specific attributes of female directors affect earnings management. The British Accounting Review, 50(3), 255–274. https://doi.org/10.1016/j.bar.2017.09.001

- Harford, J., Li, K., & Zhao, X. (2008). Corporate boards and the leverage and debt maturity choices. International Journal of Corporate Governance, 1(1), 3–27. https://doi.org/10.1504/IJCG.2008.017648

- He, W. P., Lepone, A., & Leung, H. (2013). Information asymmetry and the cost of equity capital. International Review of Economics & Finance, 27, 611–620. https://doi.org/10.1016/j.iref.2013.03.001

- Hellier, D., & Chasan, E., 2018, Big investors push harder for more women directors.

- Hillman, A. J., Withers, M. C., & Collins, B. J. (2009). Resource dependence theory: A review. Journal of Management, 35(6), 1404e1427. https://doi.org/10.1177/0149206309343469

- Huang, J., & Kisgen, D. J. (2013). Gender and corporate finance: Are male executives overconfident relative to female executives? Journal of Financial Economics, 108(3), 822–839. https://doi.org/10.1016/j.jfineco.2012.12.005

- Jensen, M. C. (1986). Agency costs of free cash flow, corporate finance, and takeovers. The American Economic Review, 76(2), 323–329.

- Jizi, M. I., & Nehme, R. (2017). Board gender diversity and firms’ equity risk. Equality, Diversity and Inclusion: An International Journal, 36(7), 590–606. https://doi.org/10.1108/EDI-02-2017-0044

- Joecks, J., Pull, K., & Vetter, K. (2013). Gender diversity in the boardroom and firm performance: What exactly constitutes a “critical mass?”. Journal of Business Ethics, 118(1), 61–72. https://doi.org/10.1007/s10551-012-1553-6