?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

Corporate restructuring is a widely adopted mode of improving efficiency and firm performance and has been studied in different country contexts such as the US, Australia, and Europe. The aim of this paper is to examine the impact of spin-off announcements on the stock prices of parent firms in the Indian context. In addition, we also investigate the price effect anomaly through two subsamples of high-price scripts and low-price scripts. The study is conducted on a sample of 221 Indian firms listed in BSE (Bombay Stock Exchange) from 2003 to 2020 which have announced the spin-offs. We employ event study methodology and find that spin-offs have a significantly positive impact on the stock prices of the parent firm. We observe the highest abnormal return of 1.35% on +1 day post the event. The interval-wise analysis gives the highest CAAR of 2.64% in (+1, +5) interval. The analysis of the price behavior of stocks at different price levels suggests that the low-price script outperformed the high-price script in each event window with a CAAR of 3.90% in high-price script and 7.16% in low-price script for the event window from −10 to +10.

1. Introduction

The various aspects of corporate restructuring and its implication on firm performance have been a central concern in many studies for approximately three decades (Chemmanur & Yan, Citation2004; Desai & Jain, Citation1999; Schipper & Smith, Citation1983; Singh et al., Citation2009). Restructuring has witnessed considerable research, but the restructuring and the consecutions on a firm and its stakeholders are dubious, and rhetoric of this source of shareholder benefit is challenged by skepticism (Bowman & Singh, Citation1993). However, a general perspective of relevant studies suggests that spin-offs or demergers of business firms create value for its shareholders as a consequence of the positive abnormal return of the stocks (Aggarwal and Garg,Citation2019; Ahn & Denis, Citation2004; Bendre & Apte, Citation2017; Bergh et al., Citation2008; Boreiko & Murgia, Citation2016; Chai et al., Citation2018; Cusatis et al., Citation1993; Hite & Owers, Citation1983; Rosenfeld, Citation1984; Vyas et al., Citation2015).

Corporate restructuring has become an important but common strategic practice among business firms. It encompasses a wide range of transactions such as selling off the existing business lines, altering the firm’s capital structure and internal organization, and others. It can also include acquisitions and divestitures to reconfigure the business lines. The common motives behind restructuring majorly cite maximizing shareholder wealth, cost controls, and productivity enhancements.

A significant number of studies are based on different country contexts that indicate the positive relationship between the announcement of spin-offs and abnormal stock returns. In India, corporate spinning is becoming a prominent mode of restructuring as the past few years have witnessed a large number of spin-offs by Indian companies. Spin-offs are one of the modes of divestitures through which corporates reduce their business portfolio, create value (Kambla, Citation2017), and improve financial performance by reducing information asymmetries (Bergh et al., Citation2008). A spin-off differs from sale divestitures in that it results in an independent firm that causes the reduction in the asset base of the divested firm. The shares of the divested firms may be transferred to the shareholders of the divested firm (Hite & Owers, Citation1983). In this mode, the parent company’s spin-off gets listed on the capital market, and shares of the divested business are distributed to the shareholders of the parent business. The shareholders have the choice to hold a share of either of both entities after the restructuring or sell their stake in divested firm (Puranam & Vanneste, Citation2016). There are various factors that cause the positive association between spin-offs and value creation.

The spinning-off improves the performance of the parent’s stock and increases the number of securities that are traded on the market (Habib et al., Citation1997). The investors believe that post-separation, there will be a decline in the level of information asymmetry in the stock market and an upsurge in the value of the parent firm and its divested subsidiary. Whereas (Krishnaswami & Subramaniam, Citation1999), in their study, concluded that the low positive abnormal returns are associated with the taxable spin-offs and high returns with non-taxable spin-offs. They suggested that firms might undertake spin-off, expecting that reduction in information asymmetry will lead to value unlocking (Bergh et al., Citation2008). In India, the spin-offs are exempted from capital gain tax under section 47(vib) of the Indian Income Tax Act,1961. In addition, there are few provisions to carry forward and set off losses and unabsorbed depreciation in the hand of parent firms.

In this paper, we attempt to study the discussed phenomena on the Indian companies as corporate restructuring has become a common phenomenon in India after the liberalization policy adopted by the Government of India in the year 1991. Developing countries like India, Korea, China, and others contain and conduce the growth of business groups. These conglomerates grow into a diversified business with related or unrelated diversifications. However, with changes in the business environment and an increase in competition, the large business groups face threats of operational inefficiencies and takeovers by foreign companies. Therefore, to survive the competition in domestic and global markets, Indian conglomerates are spinning-off their business portfolio to focus on their core business and improve operational efficiencies (Ramu, Citation1999).

We study 221 spin-offs by Indian companies from the year 2003–2020 and the impact of their announcement on the stocks return of the parent firms. The result expects to substantiate the findings on Indian companies taking a much larger sample size, which comprises parent firms compared to other studies conducted on Indian firms. To the best of our knowledge and literature in hand, this study provides the first empirical comparative study of low-price and high-price scripts.

2. Literature review

The downsizing of a large company is a response to the dynamic business environment and industry shocks. The restructuring through divesture has a wealth effect on shareholders (Mulherin & Boone, Citation2000). The voluntary spin-offs by the firm are perceived to have a positive impact on the parent company and the spin-off subsidiary. The primary reason behind divestitures is to enhance managerial efficiency and improve firms’ economic value in the capital market and competitive positions (Woo et al., Citation1989). Spinning-off a division or a subsidiary provides strategic and financial advantages to the corporates and results in additional value for the stockholders of the parent firms and causes increases in operating performance (Chemmanur & Yan, Citation2004). Several empirical evidence strengthens the argument made in the paper that spin-offs announcement leads to abnormal return (Refer ). The literature covers the study of different types of restructuring modes and their association with the impact on stock prices of the firms and shareholders’ wealth. These studies differ in-country context and sample size, and period of study. The extant literature cites multiple reasons for companies to undergo spin-offs some of which are mentioned below:

Table 1. Summarises the empirical evidence and their findings and conclusion from different country contexts

2.1. Focus on core business

Corporate strategists find restructuring appealing for an excessively diversified company. It separates the subsidiary that is not aligned with the core business to avert the incoordination of resources and the dilution of core competencies because of firm size (Kambla, Citation2017). Desai & Jain, Citation1999, in their study, examined the explanation of the abnormal return of the stock market on the spin-off announcement based on focus on the core business. Their result suggests that focus-increasing spin-offs show long-run abnormal returns than non-focus-increasing spin-offs. The spin-offs as a restructuring mode are also a low-cost method of transferring control of corporate assets to bidders who will create greater value (Cusatis et al., Citation1993). Spin-offs lead to an increase in corporate focus and thus improve the performance; as a result, spin-off announcement causes an increase in return.

2.2. Increase efficiency of parent and divested firm

(Ahn & Denis, Citation2004), in their study on 106 spin-offs, cited that diversified firms allocate investment funds inefficiently; thus, the spinning creates value by improving investment efficiency. Whereas spinning off a subsidiary helps reduce negative synergies and unlock value by divesting assets or business lines that are not associated with the core business of the firm (Kambla, Citation2017). A comparative study of cross-industry spin-offs and own-industry spin-offs indicated that the operating-return-on-assets ratio, i.e., ROA increased in excess in the case of cross-industry spin-offs. In contrast, ROA change was modest and insignificant for the own-industry spin-offs (Daley et al., Citation1997). In addition, the restructuring allows the divested entity to explore its value by attracting investors and analysts and accessing supplementary funds in the equity and debt markets. Spin-off provides ease for a parent company to divest its subsidiary as, most often, their existing shareholders buy the spin-off subsidiary. Consequently, the spin-off has appealed to a large number of firms as a popular restructuring mode, particularly in the environment where obtaining finance becomes a challenge (Gordon, Citation1992).

2.3. Reduce information asymmetries

(Bergh et al., Citation2008) in their study of spin-offs and sell-offs examined the selection of diversification strategy in relation to the restructured asset and observed the impact on the stock market due to restructuring announcements. Their study concluded that spin-offs effectively reduced information asymmetries and transferred the asset to the capital market when restructured assets remained with primary and related businesses. In contrast, sell-offs proved to be the best restructuring mode when restructured assets remain with the secondary and unrelated business. Firms show high diversification, and sell-offs reduce the information asymmetries through market forces.

2.4. Impact on bondholder’s cash flow

Another justification of positive return is based on how the spin-off impacts the bondholders. If spin-offs cause a reduction in the cash flows, then restructuring announcement may lead to a decline in bond prices as the probabilities of cash inflow are revised. Thenceforth, expropriating the bondholder’s wealth is defined by the loss of assets and cash flows (Maxwell & Rao, Citation2003). In addition, the shareholders of the parent firm will get the benefit of shareholdings in both the resulting company and demerged firm at the cost of bondholders of the parent firm due to the decline in collateral value of the parent firm (Galais & Masulis, Citation1976). Alternatively, if spin-offs do not cause a reduction in cash inflows to bondholders, then the spin-off announcement would not initiate a price reaction. An alternative explanation suggests that spin-offs cause an increase in future contracting flexibility as firms are constituted by various optimal contracts depending upon the nature of operation, assets, and investment opportunities. This set of contracts influences the shareholders’ wealth. Therefore, spin-off enables the parent and subsidiary to engage in the contracts in which they have the advantage as per their specialisation and opportunities (Hite & Owers, Citation1983)

A number of studies present a contrasting view regarding the spin-off’s announcement and the abnormal stock return (Boreiko & Murgia, Citation2016). The only exception observed in the study by Murray (Citation2000) was on UK firms. The result reported an insignificant negative abnormal return for the event window from day −1 to day 1.

3. Data

The Bombay Stock Exchange (BSE) is the oldest stock exchange in India. As per the information memorandum of listed companies available on the BSE website, the record of 351 schemes of arrangement and spin-offs is available from 2000 to 2021. Out of these 351 records, 26 were excluded as announced prior to 2003, or their board approval was given before 2003. Out of the remaining, 93 were removed because the record contains other schemes of arrangements other than spin-offs such as amalgamation, buybacks, acquisitions, bonus issue, consolidation of shares, reduction of share capital, name change, and rest others. In addition, these 93 records are also comprised of duplicate entries and firms whose board approval date is not available. Due to some inconsistency in data, 11 companies were removed from the sample. The final sample comprises data of 221 parent firms. The year-wise spin-offs data is given in . We considered the event date, the date on which the company intimated the approval of the announcement of a spin-off by the Board of Directors to the stock exchanges. We obtain the daily frequency stock price data of individual securities for 17 years from 2003 to 2020 from the Bloomberg database. The Nifty 50 index has been considered to capture the movement of the market. Nifty 50 index is a standard stock market index in India. It represents the weighted average of 50 diversified stocks. It is used for benchmarking portfolios, derivative products, and index funds.

Table 2. Year wise observations of parent firms which have announced spin-offs by their board

4. Methodology

The event study methodology has widely been used and accepted in the finance literature to determine the stock price movement around the event. It is evident from the extant literature that event study methodology is the standard method used to study the impact of divestiture announcements on stock price behaviour (Binder, Citation1998). The event can be the announcement of dividends, mergers, the resignation of auditors, etc. Therefore, we have used the standard event study methodology outlined in the paper by Brown and Warner (Citation1985). The first step for conducting an event study is to determine the event window, event date, estimation period, and event of interest. The event of interest in this study is the announcement of a spin-off by the board. For estimating normal return with the use of the market model, we have used 240 days estimation window. The estimation period starts from 250 days before the event day to 10 days of event days. We have taken 21 days event window for an event study. The event window consists of event day, 10 days a pre-event day, and 10-days post-event day.

The second step is to calculate the stock return from the stock price, which is calculated by the following formula:

where is the stock return for firm i on day t, and

is the share price for day t.

The third step is to calculate the normal market return. To calculate, we have selected the market model method to find out alpha and beta values for the sample firms. The values are calculated by applying an ordinary least square regression on the firm return to market return of the estimation period. With the help of the following formula, we calculate the normal return:

where is a measure of average return over the calculation period, which is not explained by the market, the

is the measure of a company’s sensitivity to the market risk component.

is the return on a market index, and the Nifty50 index is selected as the market index for calculating normal market return.

is an error term and

.

To observe the anticipated price effect resulting from an event announcement, the abnormal return in stocks during the event window is calculated by comparing actual stock returns with the normal market return. The abnormal return for the event window is calculated by using the following formula:

where is the abnormal return for t day, and

is the actual stock return of t day, and

the normal return for day t.

In the subsequent step, we calculate Cumulative Abnormal Return (CAR), which measures abnormal return throughout the event period. It is estimated to determine the total abnormal return during the event window. CAR is calculated by summing up the abnormal return of stock throughout the event window using the formula:

We also calculate some other abnormal return measures to draw the statistical inference: Average Abnormal Return (AAR) and Cumulative Average Abnormal Return (CAAR). AAR is calculated as share prices are impacted by other information. Hence, it makes share prices noisy. To overcome this problem, we average all the firms’ abnormal returns, which constitute our sample. The formula to calculate AAR is:

where N is the number of firms that constitute our sample of the study. is an abnormal return of an individual firm’s share price.

Cumulative Average Abnormal Return (CAAR) is calculated by summing up the average abnormal return of stock throughout the event window. The CAAR is calculated to determine the total average abnormal return during the event window. The formula to calculate CAR is:

where p is the number of days, we want to cumulate the average abnormal return. is an average abnormal return.

In the final step, we determine the statistical significance of abnormal return measures by using the parametric test. Statistical significance means to examine whether the abnormal returns are different from zero or not. The parametric test is done using a cross-sectional t-test which has higher power over standard time-series t-tests (Brown & Warner, Citation1980). Cross-sectional t-test assumes the null hypothesis that the average abnormal returns (averaged over all the firms) is equal to zero and is calculated by the following formula:

where, is the estimated cross-sectional variance of the abnormal returns, calculated as under

5. Empirical results & analysis

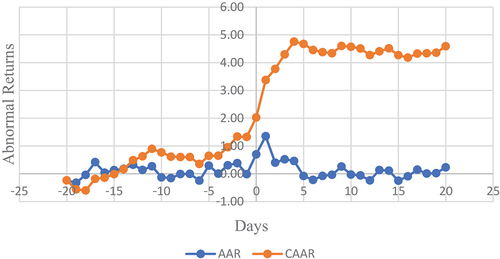

presents the average abnormal return (AAR) and cumulative average abnormal returns (CAAR) of each day during the 41 days event window around the announcement of spin-offs by the board. N stands for the sample size, which is 221. We observe the highest abnormal return of 1.35% on +1 day post the event. The results are significant in the parametric test with a t-value of 5.74. The second highest abnormal return is reported at 0.69% on the event day, significant at a 1 percent level. The cumulative average abnormal return (CAAR) results show that on day +4, the abnormal return is highest with a 4.75% return.

Table 3. AAR and CAAR results of each day during event window: announcement of spin off

Further, we show in the interval-wise abnormal return. The interval (−1,+1) and (0,+1) reports 0.68% and 1.02% CAAR, respectively, which verifies the day-wise analysis. The highest CAAR of 2.64% is reported in (+1,+5) interval. The parent firms show no significant abnormal return after day +5. This signifies, after day +5, the stock price of the firms does not respond to the event announcement. Brown and Warner (Citation1980), the cross-sectional t-test is used for the parametric t-test. Thus, it is evident from the results that the stock prices of the parent firms positively respond to the spin-off announcement. In addition, it can be concluded that spin-offs add to the shareholder’s wealth.

Table 4. AAR and CAAR results over different intervals during event window: announcement of spin off

The results presented in all the above tables are summarised in .

Figure 1. Day-wise AAR and CAAR results during event window of 41 days: announcement of spin off

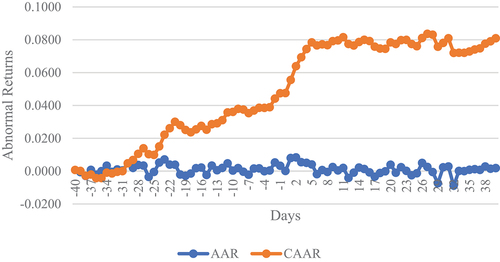

We conduct another event study with an extended event window of 81 days for the robustness of our results. The prime motive of taking an extended event window is to test whether the stocks regress to their previous level as before the announcement. The announcement might be interpreted simply as a short-term opportunity for speculative traders who shortly after the announcement will sell off their trades again.

We report robustness results in and . We find that our results are robust and the abnormal returns persist in the extended event window which implies that there is no evidence of speculative trades. This result signifies that investors realize the synergies that a spin-off of a firm creates. Therefore, the investors maintain their position in the spin-off company and invest for the purpose of long-term returns and maximization of their wealth.

Figure 2. Day-wise AAR and CAAR results during event window of 81 days: announcement of spin off

Table 5. AAR and CAAR results over different intervals during extended event window: announcement of spin off

6. Further analysis

Academicians and practitioners claim that there is a different price reaction of any events on the basis of their price scripts (Lamoureux & Poon, Citation1987). According to Maloney and Mulherin (Citation1992), the firms with low-price scripts have a higher shareholders base as these stocks are more affordable than the high-price scripts. In addition, the attraction of the small retail investors tends to decline in high-price scripts as they can’t afford those stocks. Further, in the advanced stock market such as the US, low-priced stocks are preferred by individual investors which leads to higher liquidity and a better price discovery process (Schultz, Citation2000). Therefore, companies with different levels of share price often have a different level of price reaction. The low-price scripts show volatile behavior as these tend to belong to less established firms (Branch & Chang, Citation1990). According to Fritzemeier (Citation1936), low-price scripts show more fluctuation as compared to high-price scripts. In addition, low-price industrial stocks provide greater opportunities for speculation gains than high-price industrial stocks. If the high and low-price scripts are likely to have equal anticipated profit then investors tend to invest in low-price scripts. Therefore, these stocks are likely to have less loyal investors as compared to high-price scripts. (Bhardwaj & Brooks, Citation1992) also provide evidence that low-price scripts have more abnormal returns than high-price scripts.

Thus, we have explored the price effect on the spin-off announcement on low-price script and high-price script. We have conducted the event study to study the price effect on two subsamples: high-price scripts and low-price scripts.

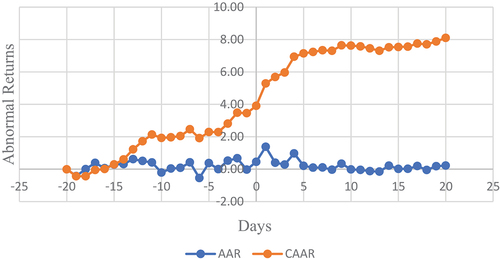

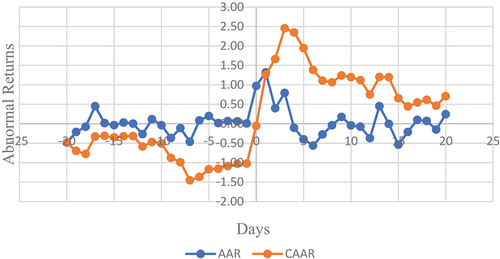

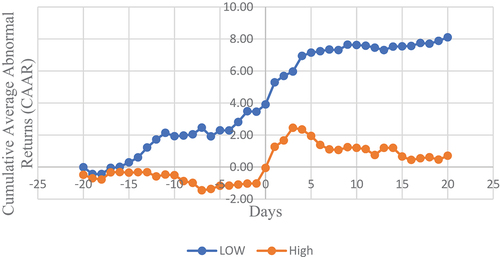

The subsample results are consistent with the complete sample result. It can be analysed from that on the announcement of spin-offs, the abnormal returns of low-price scripts were significantly positive and showed a greater increase, whereas high scripts showed a smaller increase in the post-event period. In the high-price script, the highest CAAR of 2.50% is reported on (+1,+3) interval with significance at 1 percent level. In the low-price script, the highest 3.23% of CAAR is reported on (+1,+5) interval with significance at 1 percent level. It can be concluded from the result of the abnormal return that the low-price scripts show more significant positive returns than high-price scripts for up to 5 days post the announcement. This confirms that spin-offs have a substantial impact on low-price scripts. This confirms that spin-offs have a substantial impact on low-price scripts. The results presented in all the above tables are summarised in for low- and high-price scripts, respectively. We also provide a comparison between the low- and high-price scripts in . It provides a higher understanding and comparability of the results.

Figure 3. Day-wise AAR and CAAR results during event window of 41 days for Low-Price Scripts: announcement of spin off

Figure 4. Day-wise AAR and CAAR results during event window of 41 days for High-Price Scripts: announcement of spin off

Figure 5. Day-wise AAR and CAAR results during event window of 41 days for comaprison between High and Low-Price Scripts: announcement of spin off

Table 6. AAR and CAAR results of each day during event window for low-price script: announcement of spin off

Table 7. AAR and CAAR results of each day during event window for high-price script: announcement of spin off

Table 8. AAR and CAAR results over different intervals during event window for low-price script: announcement of spin off

Table 9. AAR and CAAR results over different intervals during event window for high-price script: announcement of spin off

This study also adds to the price-return literature by providing evidence that investor’s choice of low-priced stocks could generate more profitable trades. If stock prices follow long-run average nominal price, as evidenced by Weld et al. (Citation2009), trading in low-priced spin-offs can reap the benefit of this appreciation of prices.

7. Conclusion

The study on spin-off announcements and their price effect can now be widely seen in the literature in a different country context, such as the US, Australia, and Europe. However, the findings from different country contexts cannot be generalised as the institutional settings in advanced economies differ from emerging economies and underdeveloped economies. For instance, in India, the percentage of retail investors is higher among total market participants, whereas institutional investors have a higher share in the US. Therefore, we have supplemented the existing studies on the Indian market, taking a much larger sample size as compared to other studies conducted on Indian firms. The result obtained from the sample of 221 spin-offs announcements is consistent with the previous findings. We observe the highest CAAR of 4.75% on day +4 and 2.64% on the interval (+1,+5).

Further, to analyse the price behaviour of stocks having different price levels, we calculated the CAAR by dividing the whole sample into two sub-samples- low-price and high-price scripts. We observe that the low-price script outperformed the high-price script. In the high-price script, the highest CAAR of 2.50% is reported on (+1,+3) interval with significance at 1 percent level. In the low-price script, the highest 3.23% of CAAR is reported on (+1,+5) interval with significance at 1 percent level. Thus, it is evident that parent companies with low share prices gain more than companies with high share prices from the announcement of spin-offs and that investor’s choice of low-priced stocks could generate more profitable trades. The findings of the study open further research avenues regarding the factors associated with a firm level, industry level, and country-level that contribute to the price reaction after the spin-off announcement by a firm. Further research may focus on exploring the impact of taxable and non-taxable spin-offs on the firm’s stock performance and the impact of regulatory frameworks in different country contexts to capture the contextual factors. Due to the scant literature, another interesting research may focus on a more comprehensive study on bondholders’ wealth creation due to spin-off announcements and factors associated with price reaction.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

Notes on contributors

Deeksha Gupta

Deeksha Gupta is a Doctoral Fellow in the area of Strategic Management at the Indian Institute of Management, Ranchi. Her research interests lie in Corporate Restructuring, Business Models, Entrepreneurial Ecosystem.

Rahul Kumar

Rahul Kumar is a Doctoral Fellow in the area of Accounting and Finance at the Indian Institute of Management, Ranchi. His research interests lie in Corporate Finance, Derivatives, Investment management, Corporate Governance etc.

Subir Chattopadhyay

Subir Chattopadhyay is a professor by practice in the Accounting and Finance area at the Indian Institute of Management Ranchi. His research interests include financial Accounting, Management Accounting, Corporate Finance. He teaches Financial Reporting and Analysis, Managerial Accounting.

References

- Aggarwal, P., & Garg, S. (2019). Restructuring through spin-off: Impact on shareholder wealth. Managerial Finance, 45(10/11), 1458–20. https://doi.org/10.1108/MF-11-2017-0487

- Ahn, S., & Denis, D. J. (2004). Internal capital markets and investment policy: Evidence from corporate spin-offs. Journal of Financial Economics, 71(3), 489–516. https://doi.org/10.1016/S0304-405X(03)00165-X

- Bendre, M., & Apte, N. (2017). Study of impact of spin-offs on shareholders wealth in India. International Research Journal Of Multidisciplinary Studies, 3(10), 1–7.

- Bergh, D. D., Johnson, R. A., & Dewitt, R. L. (2008). Restructuring through spin‐off or sell‐off: Transforming information asymmetries into financial gain. Strategic Management Journal, 29(2), 133–148. https://doi.org/10.1002/smj.652

- Bhardwaj, R. K., & Brooks, L. D. (1992). The January anomaly: Effects of low share price, transaction costs, and Bid–ask bias. The Journal of Finance, 47(2), 553–575. https://doi.org/10.1111/j.1540-6261.1992.tb04401.x

- Binder, J. (1998). The event study methodology since 1969. Review of Quantitative Finance and Accounting, 11(2), 111–137. https://doi.org/10.1023/A:1008295500105

- Boreiko, D., & Murgia, M. (2016). Corporate governance and restructuring through spin-offs: European evidence. In T. Azarmi & W. Amann (eds.), The financial crisis (pp. 7–47). Springer, Cham. https://doi.org/10.1007/978-3-319-20588-5_2

- Bowman, E. H., & Singh, H. (1993). Corporate restructuring: Reconfiguring the firm. Strategic Management Journal, 14(S1), 5–14. https://doi.org/10.1002/smj.4250140903

- Branch, B., & Chang, K. (1990). Low price stocks and the January effect. Quarterly Journal of Business and Economics, 29(3), 90–118. http://www.jstor.org/stable/40472999

- Brown, S. J., & Warner, J. B. (1980). Measuring security price performance. Journal of Financial Economics, 8(3), 205–258. https://doi.org/10.1016/0304-405X(80)90002-1

- Brown, S. J., & Warner, J. B. (1985). Using daily stock returns: The case of event studies. Journal of Financial Economics, 14(1), 3–31. https://doi.org/10.1016/0304-405X(85)90042-X

- Chai, D., Lin, Z., & Veld, C. (2018). Value-creation through spin-offs: Australian evidence. Australian Journal of Management, 43(3), 353–372. https://doi.org/10.1177/0312896217729728

- Chemmanur, T. J., & Yan, A. (2004). A theory of corporate spin-offs. Journal of Financial Economics, 72(2), 259–290. https://doi.org/10.1016/j.jfineco.2003.05.002

- Cusatis, P. J., Miles, J. A., & Woolridge, J. R. (1993). Restructuring through spin-offs: The stock market evidence. Journal of Financial Economics, 33(3), 293–311. https://doi.org/10.1016/0304-405X(93)90009-Z

- Daley, L., Mehrotra, V., & Sivakumar, R. (1997). Corporate focus and value creation evidence from spin-offs. Journal of Financial Economics, 45(2), 257–281. https://doi.org/10.1016/S0304-405X(97)00018-4

- Desai, H., & Jain, P. C. (1999). Firm performance and focus: Long-run stock market performance following spin-offs. Journal of Financial Economics, 54(1), 75–101. https://doi.org/10.1016/S0304-405X(99)00032-X

- Fritzemeier, L. H. (1936). Relative price fluctuations of industrial stocks in different price groups. The Journal of Business of the University of Chicago, 9(2), 133–154. https://doi.org/10.1086/232428

- Galais, D., & Masulis, R. W. (1976). The option pricing model and the risk factor of stock. Journal of Financial Economics, 3(1–2), 53–81. https://doi.org/10.1016/0304-405X(76)90020-9

- Gordon, J. M. (1992). Spin–Offs: A way to increase shareholder value. Journal of Business Strategy, 13(1), 61–64. https://doi.org/10.1108/eb039472

- Habib, M. A., Johnsen, B. D., & Naik, N. Y. (1997). Spin-offs and information. Journal of Financial Intermediation, 6(2), 153–176. https://doi.org/10.1006/jfin.1997.0212

- Hite, G. L., & Owers, J. E. (1983). Security price reactions around corporate spin-off announcements. Journal of Financial Economics, 12(4), 409–436. https://doi.org/10.1016/0304-405X(83)90042-9

- Kambla, V. (2017). Do spin-offs really create value? Evidence from India. In S. Raghunath & E. Rose (Eds.), International business strategy (pp. 129–141). London: Palgrave Macmillan. https://doi.org/10.1057/978-1-137-54468-1_6

- Krishnaswami, S., & Subramaniam, V. (1999). Information asymmetry, valuation, and the corporate spin-off decision. Journal of Financial Economics, 53(1), 73–112. https://doi.org/10.1016/S0304-405X(99)00017-3

- Lamoureux, C. G., & Poon, P. (1987). The market reaction to stock splits. The Journal of Finance, 42(5), 1347–1370. https://doi.org/10.1111/j.1540-6261.1987.tb04370.x

- Maloney, M. T., & Mulherin, J. H. (1992). The effects of splitting on the ex: A microstructure reconciliation. Financial Management, 21(4), 44–59. https://doi.org/10.2307/3665840

- Maxwell, W. F., & Rao, R. P. (2003). Do spin–offs expropriate wealth from bondholders? The Journal of Finance, 58(5), 2087–2108. https://doi.org/10.1111/1540-6261.00598

- Mulherin, J. H., & Boone, A. L. (2000). Comparing acquisitions and divestitures. Journal of Corporate Finance, 6(2), 117–139. https://doi.org/10.1016/S0929-1199(00)00010-9

- Murray, L. (2000). An assessment of the wealth effects of spin-offs on the London Stock Exchange. Working paper, University College Dublin.

- Puranam, P., & Vanneste, B. (2016). Corporate strategy: Tools for analysis and decision-making. Cambridge University Press.

- Ramu, S. S. (1999). Restructuring and break-ups: Corporate growth through divestitures, splits, spin-offs and swaps. SAGE.

- Rosenfeld, J. D. (1984). Additional evidence on the relation between divestiture announcements and shareholder. The Journal of Finance, 39(5), 1437–1448. https://doi.org/10.1111/j.1540-6261.1984.tb04916.x

- Schipper, K., & Smith, A. (1983). Effects on recontracting on shareholder wealth –– The case of voluntary spin-offs. Journal of Financial Economics, 12(4), 437–467. https://doi.org/10.1016/0304-405X(83)90043-0

- Schultz, P. (2000). Stock splits, tick size, and sponsorship. The Journal of Finance, 55(1), 429–450. https://doi.org/10.1111/0022-1082.00211

- Sin, Y. C., & Ariff, M. (2006). Corporate spin-offs and the determinants of stock price changes in Malaysia. Working Paper, Monash University, February.

- Singh, R., Bhowal, A., & Bawari, V. (2009). Impact of demerger on shareholders’ wealth. Enterprise Risk Management, 1(1), 44–59. https://doi.org/10.5296/erm.v1i1.64

- Vijh, A. M. (1994). The spin-off and merger ex-date effects. The Journal of Finance, 49(2), 581–609. https://doi.org/10.1111/j.1540-6261.1994.tb05153.x

- Vyas, P., Pathak, B. V., & Saraf, D. (2015). Impact of demerger announcement on shareholder value evidences from India (December 15, 2015). Journal of Management & Public Policy, 7(1). https://ssrn.com/abstract=2717020

- Weld, W., Michaely, R., Thaler, R., & Benartzi, S. (2009). The nominal share price puzzle. Journal of Economic Perspectives, 23(2), 121–142. https://doi.org/10.1257/jep.23.2.121

- Woo, C. Y., Willard, G. E., & Beckstead, S. M. (1989). Spin-offs: What are the gains? The Journal of Business Strategy, 10(2), 29. https://doi.org/10.1108/eb039292