Abstract

Technology has reshaped how financial services are designed, delivered, and consumed over the past decade. The increased mobile and internet penetration and availability of cheap data combined with the advent of Fintech, digitalization, blockchain technology, machine learning, and artificial intelligence have fast-tracked the digital transformation of economies worldwide. Covid19-induced lockdowns accelerated the digitalization of financial services. This study identifies the main areas and current dynamics of Fintech, digitalization, and financial services and suggests future research directions. Using a bibliometric analysis followed by a thematic literature review, the study examines a sample of 583 journal articles from the Scopus database from 1984 to 2021. Based on the bibliometric analysis, we identified four dominant themes. These themes are further explored through a thematic literature review to gain further insights. We conclude by suggesting potential directions for future research in the field.

1. Introduction

How financial services are designed, created, and consumed has metamorphosed with the advent of technology. Fintech conveys the integration of technology with financial services. According to a comprehensive definition, Fintech is an innovative technology that improves and automates financial services that enable smooth management of firms, investors, and customers using specialized software and applications (Zhang-Zhang et al., Citation2020). The Fintech market initially developed in the US, followed by the UK (Haddad et al., Citation2019). However, the diffusion and adoption of Fintech were faster in Asia. According to a report on Global Fintech Adoption Index in 2019 by Ernst & Young (EY), Asia is the world leader in Fintech adoption, led by China and India. India enjoys the second-highest Fintech adoption rate of 87% compared to the global average of 64% (EY, Citation2021a). Likewise, in 2021, the Americas and the EMEAFootnote1 regions saw 22% and 26% growth in Fintech startups, compared to 31% for the APACFootnote2 region (Statista, Citation2021). Fintech in the Asian region is more of a solution to the lack of banking infrastructure, which is not the case for the USA and European regions (Arner et al., Citation2020). A study (Rabbani et al., Citation2020) reports the quick adoption of Fintech by the Islamic finance industry.

An increase in smartphone penetration and internet users, investments in Fintech startups, and a mindset to leverage technology to create innovative product solutions remain the critical drivers for Fintech growth in emerging economies. Further, the Covid19 pandemic accelerated the speed and scale of Fintech growth and adoption in developing economies (Findexable, Citation2021). With the advent of new business organizations such as internet-only banks, regulators have shown willingness to strike a delicate balance between flexibility and security in financial activities (EY, Citation2021b). The future of the digital economy and financial inclusion depends on the advancements in Fintech business models, digital technology, and changing landscape of how financial services are designed, delivered, and consumed. Hence, as the new era of virtual financial services unfolds, there is a need to consolidate the knowledge in these closely interlinked domains. Such research can be a ready reckoner for scholars to understand the knowledge progression and present status. It offers future research directions in Fintech and the digitalization of financial services.

lists important review papers on Fintech and financial services over the past three years. These studies contribute to the literature and offer future research directions in the following areas.

Some studies are specific to technological applications like big data, artificial intelligence, and blockchain.

Some studies are specific to Fintech products like P2P lending, mobile banking, and digital payments.

Most studies on Fintech have either employed bibliometric methods or conducted a systematic literature review.

Table 1. Methodology of related research topics to see the gap

We apply bibliometric analysis and thematic literature review on Fintech and digitalization in financial services. A hybrid approach using bibliometric analysis followed by a thematic literature review enables us to have a holistic view of the topic and generate thematic future research directions.

This study contributes to the body of literature on Fintech and digital financial services in more than one way. First, we apply a unique two-stage sequential approach by first identifying major research themes using bibliometric analysis followed by a thematic literature review. Such an approach helps cover the breadth and the depth of the field. Second, the study synthesizes knowledge structure by thoroughly analyzing the field’s conceptual and intellectual structures. Third, the study identifies and presents a thematic literature review of four major themes and a descriptive review of the 53 most relevant papers; it serves as a reference for scholars working in this field. Fourth, the study provides future research directions for Fintech and digital financial services, especially in the changing landscape and pace of digitalization of financial services.

This paper aims to understand the knowledge progression and its present status, draw a thematic map, and identify future research directions. We achieve this by looking at the extant literature through an integrated lens of bibliometric analysis and thematic literature review. Accordingly, the following research questions are identified for this study.

RQ1. Which are the most influential documents, authors, sources, institutions, and countries in Fintech (digital) and financial services research?

RQ2. What are the conceptual structure and thematic evolution of the Fintech (digital) and financial services research?

RQ3. What is the existing intellectual structure of Fintech (digital) and financial services research?

RQ4. Which Fintech (digital) and financial services research areas need further research?

The rest of the paper proceeds as follows. Section 2 explains the research methodology, followed by section 3 discusses the bibliometric analysis and findings. Section 4 presents a thematic literature review, and section 5 offers discussion, future research directions, and a conclusion.

2. Research methodology

The study analyses the linkages between Fintech, digitalization, and financial services rather than a review of a specific field (e.g., blockchain (Cai, Citation2018); financial literacy (Goyal & Kumar, Citation2021; Ingale & Paluri, Citation2020); open innovation (Schueffel & Vadana, Citation2015).

The study applies a unique two-stage sequential approach to understanding knowledge progression and eliciting trends through knowledge structure synthesis. The bibliometric analysis provides insights into the field’s intellectual structure and thematic evolution. The thematic literature review provides insights into the progression of knowledge within each theme and helps identify future research directions. Within the bibliometric analysis, the study includes performance analysis and science mapping. Performance analysis reveals essential characteristics of the field of research in terms of sources, authors, and documents; The science mapping, done through the synthesis of the knowledge structure, helps understand the thematic evolution and the current status of research. It also gives insights into future research directions.

The first and the most significant step in any bibliometric study is identifying relevant documents consistent with the study’s objective. To this end, the study used the 1984 to 2021 period in the search strategy and document selection process. While the number of documents from the early years is scanty, and the last decade has seen significant advancement in the field, the logic of using the more extended period is to avoid missing out on any seminal study.

The study uses (“Fintech” OR “Financial Technology” OR “Financial Technologies” OR “Finance Technologies” OR “Blockchain” OR “Cryptocurrency” OR “Crowdfunding” OR “P2P lending” OR “digital” OR “digital transformation”) AND “Financial Services” as keywords for the search in author keywords, abstract, and title to find the articles related to financial services connected with either Fintech or digital technology. We restrict the search to only English articles published in journals. Initially, we found 587 articles with four duplicates. After removing duplicates, the data has 583 documents for bibliometric analysis. Further, we used 53 most cited and influential articles comprising 38 most cited articles from A-A* category ABDC listed journals and 15 curated articles based on abstract and full-text analysis.

depicts the search strategy used for document selection and data analysis techniques used in this study. The study uses the Scopus database. Scopus, along with Web of Science (WoS), is a widely used abstract and citation database, and these are the two widely used indexing databases for bibliometric studies (Zhu & Liu, Citation2020). Scopus has a broader coverage of publications than Web of Science (Echchakoui, Citation2020). Zhu and Liu (Zhu & Liu, Citation2020) advocate using either to complement each other.

Figure 1. Flowchart of search strategy, document selection for Bibliometric analysis.

Following (Donthu, Kumar, Pattnaik, et al. (Citation2020, Citation2020)), we do performance analysis, followed by network analysis to understand the knowledge structure of the field using the Biblioshiny version 3.1.4. Biblioshiny incorporates various techniques as it is the most recently developed software tool.

We screened data to use articles published in journals only. Due to the review process, they are more reliable documents and represent “certified knowledge” (Danvila-del-Valle & of B, Citation2019). Therefore, the database excluded proceedings papers, news, and other document types. We searched the database citation records from scholarly journals across our research areas by searching for keywords in the title, abstract, and topic fields.

3. Bibliometric analysis and findings

3.1. Descriptive analysis

To answer RQ1 (Which are the most influential documents, authors, sources, institutions, and countries in Fintech (digital) and financial services research?), we present descriptive analysis on trends in scientific production, most relevant documents, journals, authors, institutions, and countries, in Fintech and financial services.

3.1.1. Dataset

summarizes the final database used for the analysis after cleaning and filtration for relevance. 583 documents were published between 1984 and 2021 in 385 journals by 1480 authors. However, on average, 2.93 years from publication reveals that most articles were published recently. Over 90% of articles are multi-author documents. A collaboration index of 2.94 shows that the research on Fintech and financial services has high author collaboration.

Table 2. Summary of dataset

3.1.2. Three field plot

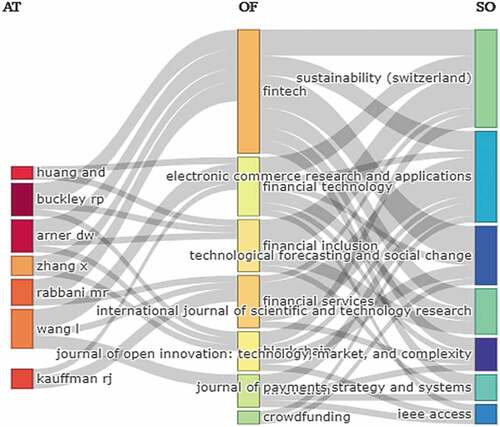

Three field plot () shows the relationship between three fields using Sankey Plots, where the size of the portion represents the node’s value (Riehmann et al., Citation2005). Authors (left), keywords (middle), and sources (right) were the three fields. Wang, Arner and Buckley are important authors. Fintech, financial services and inclusion, digital financial services, blockchain, and artificial intelligence emerged as the primary keywords. Electronic commerce, research and applications, Technology forecasting and social change, Journal of scientific technology and research and Sustainability (Switzerland) remained the preferred journals were the most prominent Fintech and financial services authors published their work.

Figure 2. Three field plot: Authors (left), Keywords (middle) and Sources (right).

3.1.3. Annual scientific production

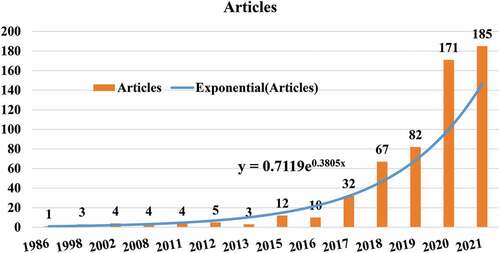

shows the growth in annual scientific production in Fintech and financial services. It is visible that Fintech and digitalization influence how financial services are designed, delivered, and consumed. Increased mobile penetration, internet access, and availability of cheap data accelerated the digitalization of financial services. Covid19 induced restrictions, and lockdowns further accelerated it. The rapid digitalization of financial services and economies has drawn a significant surge in research interest, resulting in a continuous increase in annual publications since 2016. as presented in .

Figure 3. Annual Scientific Production and Publication growth in the field of Fintech and Financial services

3.1.4. Sources

583 articles on Fintech (digital) and financial services appeared in 385 journals. Many journals from different domains cover the research domain, reflecting the research field’s diverse nature in that area (Low & Siegel, Citation2020). International Journal of Web and Grid Services, Electronic Commerce Research and Applications, and Journal of Management Information Systems are the most relevant journals based on total citations (). Sustainability (Switzerland) has the maximum number of publications (18) with 153 total citations, followed by Electronic Commerce Research and Applications, Technological Forecasting and Social Change, and IEE Access are journals with eight publications each. Interestingly, the source with the most citations—the International Journal of Web and Grid Services, has its top position owing to just one article (Zheng et al., Citation2018) with 1109 citations. This significant publication lands all five authors in the top five author positions by citations, and the country China comes out as the top most-cited country.

Table 3. Most relevant sources by total citations

It clearly shows that the journal with the maximum number of articles published is not necessarily the journal with maximum influence in research. That may be because the articles in these journals are more recently published and are yet to move up the ladder of total citations. Among the top-20 most cited sources in , all except Electronic Commerce Research and Applications have started publishing on our area of interest from 2015 or later. Two among the top 20 most-cited journals have a finance focus, and two have economics; the rest all have a technology or sustainability focus or focus on more than one area.

3.1.5. Authors, affiliations, and countries

1480 authors from 851 affiliations and 92 countries have published articles related to Fintech (digital) and financial services from 1984 to 2021. The most relevant authors in the research field were identified based on the total number of publications and citations. While the total number of articles shows the authors’ productivity, the total citations show the authors’ influence on the study field. Buckley R, Kaufmann R, Arner D, and Rabbani are the most productive authors (left panel of ). As discussed earlier, Wang H, Chen X, Zheng Z, Dai H, and Xie S are the top-5 most-cited authors and co-authors of the most-cited article (Zheng et al., Citation2018) (middle panel of ). Makerere University Business School—Uganda, Southwestern University of Finance and Economics—China, and the University of Hong Kong—China are the most relevant affiliations with the maximum number of publications (right panel of ).

Table 4. Most relevant authors and affiliations

China, USA, United Kingdom (UK), India, and South Korea have the highest published articles. On the other hand, China, the USA, UK, Germany, and South Korea are the most-cited countries. New Zealand, China, Sweden, Brazil, and Germany are the most relevant countries in the average articles cited ().

Table 5. Most relevant countries by total articles, total citations, and average citations per article

3.1.6. Documents citation analysis

Citation analysis is an appropriate way to assess the impact of a document (Ding & Cronin, Citation2010). It helps assess the impact and influence of the document in the research domain. Global citations show the number of times a document is cited by other documents in the network of documents and beyond and measure the overall impact. In contrast, the number of local citations shows the number of times the document is cited within the network of documents in the specific field. As shown in , Zheng et al. (Citation2018), Gomber et al. (Citation2018), and Wang et al. (Citation2019) are the most relevant documents with the highest number of global citations, whereas Gomber et al. (Citation2017, Citation2018) and Ozili (Citation2018) are the most local cited documents. Zheng et al. (Citation2018) comprehensively survey blockchain’s technological and application aspects. Gomber et al. (Citation2017) provides future research directions in the field of Fintech; Gomber et al. (Citation2018) investigates the forces driving the Fintech revolution. Wang et al. (Citation2019) shed light on architecture, applications, and future trends of blockchain-enabled smart contracts. Ozili (Citation2018) discusses the impact of digital finance on financial inclusion and stability.

Table 6. Most relevant documents by global citations and local citations

3.2. Conceptual structure

To answer RQ2 (What are the conceptual structure and thematic evolution of the research involving Fintech (digital) and financial services research?), we analyzed the conceptual structure of the field using the most frequent keywords, keywords co-occurrence, and study of thematic evaluation about research in Fintech (digital) and financial services.

3.2.1. Most frequent keywords

Keywords analysis offers insights into popular themes in the domain of research. The word cloud of 50 most relevant keywords shows Fintech, financial services, financial inclusion, blockchain, and financial technology as the most important keywords. In addition, crowdfunding, innovation, mobile money, and artificial intelligence are the most important words. That is consistent with the accelerated pace of digitization worldwide, especially since the breakout of Covid19. The role of AI and ML has been increasing exponentially. The word cloud in also shows other emerging themes such as regtech, cryptocurrency, machine learning, bitcoin, digital currency, and digital economy.

Figure 4. Word cloud of the most frequent authors’ keywords in the field of fintech (digital) and financial services

3.2.2. Co-occurrence analysis of the authors’ keywords

Co-occurrence analysis offers insights into the dominant themes in Fintech (digital) and financial services. Some of the most prominent keyword pairs are financial inclusion and Fintech, blockchain and Fintech, blockchain and financial services, Fintech, financial services and artificial intelligence, financial services and innovation, Fintech and regtech and Fintech and crowdfunding, blockchain and cryptocurrency. Analysis of keyword co-occurrence network following major themes emerged ().

Figure 5. Keyword co-occurrence network.

Fintech (in the context of disruptive innovation, banking and financial services, digital transformation, and decentralized finance enabled by blockchain technology)

Financial Services and Financial Technology (in the context of e-commerce, banking, and the role of e-commerce)

Financial Inclusion (enabled by mobile money, mobile payments, and digital finance)

Application of Big data, AI, and ML (in the context of design, delivery, and consumption of financial services

Regulation of Fintech and mobile payment, and role of digital money and digital currency

3.2.3. Thematic map and thematic evolution

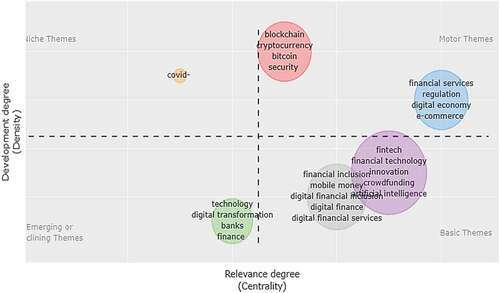

The thematic map prescribed by Callon et al. (Citation1991) offers insights into the thematic evolution of the field. The thematic map places the themes according to Callon centrality (x-axis) and density (y-axis). Centrality measures the theme’s relevance and the strength of its links with the other themes; density measures the strengths of links between the nodes within the theme and shows how well the theme is developed. Based on the relative position of a theme on the development-centrality map, themes are divided into motor themes, Basic themes, Niche themes, and Emerging or declining themes. presents the thematic map.

Figure 6. Thematic map.

Motor Themes: Motor themes are highly developed themes connected to other themes in the first quadrant. They are the most significant themes. Fintech and financial services enabled by blockchain and other technologies have been among the most significant and highly developed themes. E-commerce in the digital economy and regulation of Fintech and financial services and digital economy has become a highly developed theme. Given the rapid pace of digitization and exponential growth in e-commerce, governments and regulators worldwide have been busy putting in place an appropriate regulatory framework to ensure the stability of the banks, financial systems, and e-commerce platforms. The digital economy needs new regulations, and the debate about appropriate regulatory regimes and frameworks for digital financial services and Fintech has gained traction. The theme has become highly developed given its importance and has increasingly become central and well connected to other major themes. The role of blockchain technology and the evolution of cryptocurrencies in financial services and emerging security concerns has been evolving into a motor theme from a niche theme.

Basic Themes: Basic themes are the themes located in the fourth quadrant. They have high relevance for the overall body of research. They are well connected to other themes; however, they see stagnation and do not develop well. Financial inclusion backed by mobile money and digital financial services, innovation in Fintech led by innovation such as crowdfunding and the application of Artificial intelligence emerged as basic themes central to Fintech (digital) and financial services. These are important themes and are closely linked and connected to other themes.

Niche Themes: Niche themes are placed in the top left quadrant, and these are highly developed and specialized themes, not highly relevant and weakly connected to other themes. Covid19 played an important role in accelerating Fintech adaptation and digitalization of financial services; hence, the role of Covid19 has emerged as a niche theme in Fintech and digital financial services research.

Emerging or declining themes: Emerging and declining themes are the marginal themes, neither well developed nor highly relevant and well connected to the other themes. Such themes are either emerging or declining themes. The ever-increasing role of Fintech in digitalizing financial services pushed banks and financial institutions to look for digital transformation, which has emerged as an emerging theme.

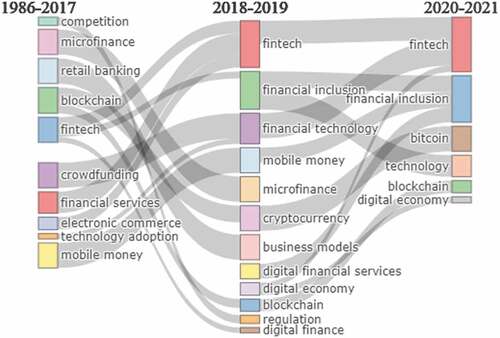

Thematic Evolution: The thematic map provides a snapshot of and categorizes themes as it stands. However, one needs to study relevant themes across different timeframes to see the evolution of themes over the years. It is relevant, especially in the research field that evolved rapidly over the years. Fintech and digital financial services are such fields.

As we see in , mobile penetration and Fintech, mobile banking, and mobile payment have helped narrow down the digital divide, and this theme has lost relevance. Mobile money has transformed itself into a broader digital currency theme. Fintech and digital financial services business models emerged as a significant theme in 2018-19. Regulation of Fintech and financial services in the digital era emerged as another important theme in the same period. Come 2020-21, with the increased pace of digitalization, security of financial transactions has become an emerging theme, and regulatory frameworks that maintain financial stability emerged as a critical concern. AI and ML have found their applications in most fields, and financial services are no exceptions. Big data, artificial intelligence, and blockchain technology in Fintech and digital financial services emerged as important themes in 2020-21 and will evolve further (Sadok et al., Citation2022). Last but not least, mobile and internet penetration, cheap data availability, and government push for digital economy aided by Covid19 induced lockdown led to quick adoption of Fintech and digital financial services.

Figure 7. Thematic evolution map

3.3. Intellectual structure of Fintech (digital) and financial services research

In order to answer RQ3 (What is the existing intellectual structure of Fintech (digital) and financial services research?), we presented a co-citation network and content analysis of the most relevant documents.

3.3.1. Co-citation and content analysis

Co-citation illustrates the number of times two articles are cited together (Small, Citation1973). This analysis is beneficial for illustrating the structure, directions, and developments in a research field (ZLiu et al., Citation2015).

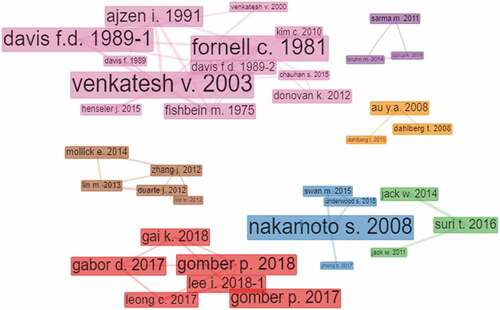

presents the co-citation network of documents in Fintech (digital) and financial services. The node size represents the number of citations, and the link’s thickness between two documents shows the strength of the co-citation. There are seven clusters of co-cited documents that emerged.

Figure 8. Co-citation network of documents.

The largest cluster in pink is dominated by documents providing theoretical or methodological bedrock for Fintech (digital) studies and financial services. Fornell et al. (Citation1991) on Structural Equation Modelling), Ajzen (Citation2002) on the Theory of planned behavior, Venkatesh et al. (Citation2003) on user acceptance of information technology, Davis (Citation1989) on perceived usefulness of Information Technology along with initial studies on mobile money by Donovan (Citation2012) and Chauhan (Citation2015).

The second-largest cluster in red emerges as an important cluster. Gai et al. (Citation2018) study a survey of Fintech; Gomber et al. (Citation2017) article on the literature review of digital finance and Fintech; Gomber et al. (Citation2018) on forces of the Fintech revolution and Gabor and Brooks (Citation2016) on the digital revolution in financial inclusion have been the most influential documents.

Cluster 3 is dominated by mobile money, mobile banking, and digital money articles. Au and Kauffman (Citation2008) on stakeholders’ issues in mobile payments, Bruhn and Love (Citation2014) on the real impact of financial access emerged as the most influential articles.

Analyzing closeness centrality, betweenness centrality, PageRank Analysis of the documents’ co-citation network reveals the documents’ importance and reputation in the network. Closeness centrality shows the dominant position of the document in the network and the influence on the network; Betweenness centrality measures the importance of the documents. Documents with high betweenness centrality might not be the heart of the network. However, these documents are vital connections between two network parts that would have remained isolated otherwise. PageRank analysis measures the article’s prestige. It goes beyond the number of citations and co-citations of the document and measures the quality of the documents citing the article. More citations by quality documents show the high prestige of the article. Hence, page rank analysis helps assess the article’s reputation in a given network. To this end, we use co-citation and content analysis to understand the intellectual structure of product characteristics research.

reports the cluster-wise distribution of the most relevant article in the co-citation network with closeness and betweenness centrality and PageRank analysis scores. Gai et al. (Citation2018), Gomber et al. (Citation2017), Gabor and Brooks (Citation2016) from cluster 2, Au and Kauffman (Citation2008), and Bruhn and Love (Citation2014) from cluster 3 emerged as the most influential articles.

Table 7. Co-citation network of documents and clusters

4. Thematic literature review

Based on word cloud, co-occurrence (of keywords), thematic map, thematic evolution, and co-citation network analysis, and a full-text review of curated most influential journal articles, we identify the following four streams:

Regulation of FinTech and Digital Financial Services

Role of Technology in Digital Transformation of Financial Services

Digital Financial Inclusion (enabled by mobile money, mobile banking, and digital finance)

Technology adoption in digital financial services (niche theme)

Milian et al. (Citation2019), in a review of 179 papers on Fintech, note that 115 papers focused on Fintech in the context of financial services. The prominent areas are the financial institutions’ businesses, operations, and financial services regulations, financial inclusion, and innovations in products, services, and business models.

The thematic review presented below provides insights into major themes.

4.1. Regulation of Fintech and digital financial services

Systemic characteristics of financial institutions change due to implementing fintech innovations and resultant changes in coalitions and market size (Wonglimpiyarat, Citation2017). Gai et al. (Citation2018) support this argument and claim that integrating technology in financial services brings revolutionary changes rather than incremental ones. Given the impact of technology on financial services, it becomes imperative to study the regulatory aspects of financial services dominated by digital and Fintech. Chaudhry et al. (Citation2022) analyze the tail risk and systemic risk of the technology firms vis-a-vis finance firms and conclude that while technology firms face a higher tail risk, finance firms face a higher systemic risk. However, Gozman and Willcocks (Citation2019) note that the fintech revolution requires more robust regulatory frameworks for technology firms similar to financial institutions to ensure financial stability. Fenwick et al. (Citation2019) emphasize the need for platform governance similar to corporate governance in an era wherein most businesses, owing to digitalization, are working as platforms. Yuan (Citation2022) calls for the up-gradation of financial supervision methods by developing a big data supervision platform, improving the technical knowledge of supervisors, and strengthening network security. It is in line with the Arner et al. (Citation2020) call for using regtech for regulatory monitoring, reporting, and compliance. Moreover, as the regulatory frameworks become dynamic, even financial services firms are mandated to modify their technology to comply with the regulations (Currie et al., Citation2018).

Various studies study the risks present in specific fintech products such as digital currency (Latimer & Duffy, Citation2019), cryptocurrency (Dupuis & Gleason, Citation2021; Ukwueze, Citation2021), Initial Coin Offering (ICO) (Gurrea-Martínez, Citation2019; Momtaz, Citation2020), P2P lending (Basha et al., Citation2021; Syamil et al., Citation2020), crowdfunding (Bajakić et al., Citation2021; Soni & Bagchi, Citation2014; Wolfson & Lease, Citation2011) among others. The new regulatory framework needs to strike a delicate balance between protecting the interest of customers and investors and avoiding stifling the innovativeness of Fintech and big-tech firms in revolutionizing the way financial products and services are designed, developed, delivered, and consumed. Tsai and Peng (Citation2017) and Liu et al. (Citation2015) pitch for a light-touch regulatory attitude toward Fintech. Yeoh (Citation2017) finds that the hands-off regulatory approach used in the EU and USA works favorably for innovative technology contributions to financial services. Anagnostopoulos (Citation2018) extends this argument and recommends that the regulator steps into action only when the overall risk posed by the technology surpasses systemic proportions or when red signals are flashed by a change in the systemic status of an individual company. Fenwick et al. (Citation2019) argue that regulators must become participants in the system to build an appropriate regulatory framework. It is fair to conclude that many studies have discussed the need for a new regulatory regime in the era of digital financial services and Fintech. However, there is no consensus on the new regulatory regime’s nature, scope, scale, and shape. presents descriptive review of this theme.

Table 8. Descriptive Review of Theme 1—Regulation of FinTech and Digital Financial Services

Fintech-enabled digital financial services have blurred the difference between technology and finance firms. Regulating large technology firms in the fintech and financial services space is essential to ensure financial stability. However, excess regulations often stifle innovations. Therefore, regulators worldwide need to follow soft-touch regulation that strikes the delicate balance between promoting innovation in financial services and ensuring financial stability.

4.2. Role of technology in digital transformation of financial services

This theme covers studies from two sub-streams a) applications of Big Data, AI & ML, Benefits & Limitations, and b) Digital Transformation.

Disruptive innovation has played a vital role in building the fintech ecosystem and has revolutionized the entire range of financial services (Gozman et al., Citation2018; Palmié et al., Citation2020). AI and data science are revolutionizing financial services with the help of smart fintech applications, intelligent and autonomous financial systems, and customized financial services (Cao et al., Citation2021). Pau (Citation1991) documents how AI can deliver financial services, including front-office, general support, and service-specific functions. AI has reshaped banking, insurance, and investment businesses (Qi & Xiao, Citation2018). Similarly, big data applications facilitate frequent and meaningful monitoring of real-life phenomena cost-effectively and improve financial services (Awan et al., Citation2021; R. M. R. M. Chang et al., Citation2014). The application of blockchain technology in financial services has been an area of interest for scholars and practitioners. Studies depict blockchain applications in record-keeping, innovative product offerings, and the resultant positive impact on operational efficiency, decision-making processes in terms of saving in time and cost, improved accuracy levels, and resultant benefits for all key stakeholders of the financial industry. Blockchain allows innovation and decentralization of financial services (Chen & Bellavitis, Citation2020). Wang et al. (Citation2019) emphasize the effective usage of blockchain in making smart contracts, while V. Chang et al. (Citation2020) call for blockchain application in structured knowledge sharing in the financial services industry.

Despite the varied applications and benefits of new technologies in the digital transformation of the financial services landscape, some studies caution against the potential demerits of technology-driven financial services. AI can be a potential source of systemic risk for organizations (Ashta & Herrmann, Citation2021; Kabza, Citation2020). Lu et al. (Citation2020) document a series of positive and negative effects of utilizing chatbots on customer experiences and employees regarding productivity, autonomy, work burden, and more. Fanning and Centers (Citation2016) caution financial institutions about the costs and risks attached to blockchain. Osmani et al. (Citation2021) document increased operational costs like transaction costs, energy costs, and storage costs related to blockchain technology.

Hence, given the costs and risks scholars indicate a need for financial institutions to formulate a clear digital strategy and analyze the costs and benefits before integrating technology into their business models (Au & Kauffman, Citation2008; Chanias et al., Citation2019; Kumar et al., Citation2020). Niemand et al. (Citation2021) further observe that a bank’s clear vision of digitalization is more important in predicting the performance of the bank. Mogaji et al. (Citation2021) support this by claiming that successful AI implementation requires understanding ethical implications, data, and modeling challenges. The timing of entry, design, and order of entry and expansion plays a vital role in the success of digital financial services providers (Staykova & Damsgaard, Citation2015).

Despite the risks, decentralized digital finance has potential to create robust and transparent financial structures and make a positive difference to the performance of financial services firms (Schär, Citation2021). Digital innovation adaptation and technology-empowered relationship marketing orientation (RMO) positively impact the long-term performance of banks (Scott et al., Citation2017; Wongsansukcharoen et al., Citation2015). Further, technology in finance provides opportunities to second-tier financial institutions (Hendrikse et al., Citation2020). Manser Payne et al. (Citation2021) emphasize identifying proper linkages between customers, financial institutions, and Fintech to co-create value propositions while offering AI-enabled banking services. Hence, banks and other financial institutions must collaborate with Fintech and create a new ecosystem (Hornuf et al., Citation2021; Zalan & Toufaily, Citation2017). reports the descriptive review of the articles pertaining to this theme.

Table 9. Descriptive Review of Theme 2—Role of Technology in Digital Transformation of Financial Services

Hence, while it is evident that blockchain big data, AI & ML, and related digital technologies will find myriad applications in financial services, they come with pros and cons. The financial service providers are advised to conduct a cost-benefit analysis before offering technology-based solutions. Further, the financial institutions must be strategically prepared to integrate technology into their operations and measures to mitigate the risks stemming from the same.

4.3. Digital financial inclusion

Financial inclusion is a starting point for the financial well-being of society. However, the debate about what exactly means by financial inclusion is yet to settle. According to Sarma (Citation2012), financial inclusion means the accessibility, availability, and use of the formal financial systems by all agents of the economy. Siddik and Kabiraj (Citation2018) argue that mere access is insufficient for financial inclusion. Wojcik (Citation2021) argues that Fintech improves credit accessibility and positively influences financial inclusion. Financial inclusion is an important goal in most economies as it is a mediator between financial technology and income inequality, and Fintech helps reduce income inequality (Chinoda & Mashamba, Citation2021; Demirgüç-Kunt et al., Citation2020). The evidence suggests that Fintech and the digitalization of financial services have imported financial inclusion worldwide (Fernandes et al., Citation2021).

Financial system and innovation, financial stability, financial literacy, and regulatory frameworks are important factors that influence financial inclusion (Ozili, Citation2018). Fintech is the panacea for financial inclusion and, thereby, the reduction of income inequality (Demirgüç-Kunt et al., Citation2020; Lagna & Ravishankar, Citation2021). Larios-Hernández (Citation2017) examines the role of non-monetary factors and informal financial practices in the habit formation of financially excluded. He concludes that blockchain would be very effective with its disintermediation feature. Kauffman and Riggins (Citation2012) argue that microfinance institutions have the dual goal of outreach and sustainability, and ICT is both the cause and the solution. The spread of the internet and mobile and digital financial services have significantly contributed to poverty alleviation and bridging the gender gap in financial inclusion (Adegbite & Machethe, Citation2020; Demirgüç-Kunt et al., Citation2020; Senou et al., Citation2019). The favorable impact of digitization in financial services on financial inclusion is a repetitive message emerging from several studies (Leong et al., Citation2017; Sadok, Citation2021; Senyo & Osabutey, Citation2020. In the Indian context, Ranade (Citation2017) states how the Jan Dhan-Aadhar-Mobile phone trinity shall help Fintech serve the remotest regions. Kandpal and Mehrotra (Citation2019) add that technology companies shall permeate rural areas with government support and mobile-led solutions. Digital financial inclusion has become possible due to the various benefits of convenience, affordability, and time-effectiveness of innovative fintech solutions (Ravikumar, Citation2019). Galvez-Sanchez et al. (Citation2021) claim that Fintech as a means of promoting financial inclusion will likely attract much research interest.

However, Ozili, Citation2018) argues that lack of proper infrastructure, education bias, and high cost may deter even the digital financial service providers from entering specific markets. While Information and communication technology (ICT) can alleviate poverty by providing greater access to financial services, it can also result in a digital divide (Cecchini & Scott, Citation2003; Yartey, Citation2008). Hughes (Citation2021) sheds light on the fact that the implications of Fintech on financial inclusion are two-fold: On one hand, it makes financial services accessible and affordable and hence, accelerates the pace of financial inclusion; on the other hand, it might be a potential source of systemic risk to the financial stability of the system. Finally, Joia and Cordeiro (Citation2021) identify the four pillars of fintech growth, which facilitate financial inclusion: Expansion and modernization of the mobile and internet infrastructure, the spread of digital and financial education, creation of an environment of trust while using Fintech, and development and implementation of laws and regulatory framework for Fintech. (See for descriptive review)

Table 10. Descriptive Review of Theme 3—Digital Financial Inclusion (enabled by mobile money, mobile banking, and digital finance)

There is overwhelming evidence that the digitalization of financial services and the advent of Fintech have contributed to improved financial inclusion. However, there are concerns surrounding the possibility of a digital divide and increased systemic risk due to overreliance on technology.

4.4. Technology adoption in digital financial services

The final theme focuses on the state of technology adoption in digital financial services in the fintech era. Financial inclusion would be possible if customers adopt the changes while consuming financial services, given the new technological developments. Studies in this theme focus on usage intention or adoption levels of varied fintech services, especially digital payments like mobile banking, internet banking, digital wallets, and more. Most of these studies focus on Asia and the Middle East, followed by African countries (Shaikh & Karjaluoto, Citation2015; Souiden et al., Citation2021). Souiden et al. (Citation2021), in a systematic literature review of the adoption of mobile banking, noted that the Technology Adoption Model (TAM) followed by Unified Theory of Acceptance and Usage of Technology (UTAUT/UTAUT2) are the most prominent theories used by various studies. They identify perceived usefulness, ease of use and individual attitude, social influence, and trust as antecedents for intention to use and adopt a specific technology. Kitchen and Panopoulos (Citation2010) document that age, trialability, and work experience are important factors for adopting the internet for public relations in financial services. Alkhowaiter (Citation2020) documents that trust, perceived security, and perceived usefulness are the best predictors of mobile banking. Perry and Ferreira (Citation2018) look into the behavior of digital currency users that supports mobile device payments and their understanding of the underlying system and its impact on usage. Performance and perceived efforts drive the intention to use mobile money services (Senyo & Osabutey, Citation2020). It is in line with empirical findings by Lutfi et al. (Citation2021), Hu et al. (Citation2019), Huei et al. (Citation2018), Mortimer et al. (Citation2015), Zhou (Citation2011). Similarly, studies by Abu Daqar et al. (Citation2021) and Jünger and Mietzner (Citation2020) find trust, reliability, transparency, and ease of use as significant factors in the adoption of fintech services as a whole.

Further, Karjaluoto et al. (Citation2019) suggest that banks’ investment in mobile financial services apps improves customer relationships and drives business growth. Li and Xu (Citation2021) observe that customer satisfaction in internet banking services is driven by cloud services, security, e-learning, and service quality. However, lack of connectivity, social awareness, and financial literacy continues to prove as barriers to the actual use of accessible financial services in countries like Bangladesh (Aziz & Naima, Citation2021). However, customer relationship management strategies need realignment for better customer experience due to technological disruptions in the financial sector (Kotarba, Citation2016). Similarly, in the context of P2P lending and crowdfunding platforms, it is evident that more borrowers can be attracted by offering convenience and process transparency as these borrowers are not dissatisfied with the services offered by conventional banks but are also looking for flexible alternatives (Maier, Citation2016). On the supply side, while the same collaterals as offline lending are not available in the above mechanisms, investors can rely on collective wisdom initially and then shift to personal judgment as more information is available (Estrin et al., Citation2021; Yum et al., Citation2012). (See for descriptive review).

Table 11. Descriptive Review of Theme 4—Technology adoption in digital financial services (niche theme)

Hence, as the supply side of Fintech increases with a growing number of traditional financial institutions indulging in enhanced technology, there is no doubt that the demand is also on the rise. Customers and investors embrace the new fintech services, albeit with some caution. Thus, we find much research on influencing users’ intentions or adoption levels and customer satisfaction. It has implications for the financial service providers on gaining traction by using digitalized modes of providing services.

5. Discussion, future research directions, and conclusion

The study shows that despite ever increasing research activity in Fintech and the digitalization of financial services, some research gaps remain. To answer RQ4 (Which Fintech (digital) and financial services research areas need further research?), we analyzed the areas of research that need further investigation and are presented in .

Table 12. Future research directions emerging out of each theme and article

5.1. Regulatory frameworks

While many papers have discussed the need to design a regulatory framework to address technology integration in financial services, there is still a need to review the existing rules and regulations and how risks are managed. It could be country-specific as different countries have different rules. At a broader level, one needs to study the efficacy of The Basel framework in dealing with digital and internet-only banking challenges. Future studies can focus on unique systemic risks from digital financial services and identify approaches to mitigate the same. Such studies could have policy implications for the financial regulators of the countries.

Secondly, the Thematic map shows that while the regtech theme is gaining currency, it lacks a strong connection with other themes to draw more relevance. Hence, one might need to explore the impact of regulations on the innovativeness of digital financial service providers or their business models. Further, the scholars must study the impact of regulations on digital financial inclusion and technology adoption going forward.

5.2. Adoption of digital financial services

While the theme of digital financial services adoption has almost stagnated, it is interesting to note that most studies focused on banking and payment services. There is a need to study the same in the context of insurance, wealth management, and other financial services also seeing a digital transformation, especially in developing countries, which can be studied for usage intention and actual adoption.

5.3. Addressing aspects of “security” and “trust”

Studies claim “security” and “trust” are the main factors affecting financial services’ usage. The same factors may act as proponents or deterrents in the case of digital financial services. Hence, future studies may utilize trust-based models and explore customers’ adoption intention, especially in the under-researched areas of insurance, wealth management, and more. At the same time, the security aspect can be looked at in conjunction with the design of the regulatory framework for such digital financial services.

5.4. Inter-disciplinary research

Since Fintech as a topic itself is inter-disciplinary, there is potential for researchers from Finance and technology domains to join hands in future studies. They can contribute to the theme of technology (AI, ML, Blockchain, etc.) applications and their impact on a financial product or service design, model of financial service providers, customers, and regulatory agencies.

5.5. Longitudinal studies

There is a dearth of longitudinal studies on all the themes discussed in Section 4. A sudden spurt in the use of digital financial services triggered by the Covid19 pandemic has warranted such studies. However, customers may revert to traditional practices as the restrictions are lifted. Hence, a longitudinal study would help discover whether Fintech leads to financial inclusion or digital financial inclusion in its true sense.

5.6. Use of the different combinations of keywords

The study identified the intellectual structure and the conceptual structure of Fintech or Digital financial services with the help of bibliometric analysis. Moreover, the thematic map drawn using bibliometric analysis gets further elaborated by a thematic literature review. Such an approach offers an extensive idea about focal points of various studies on the respective themes and their contribution to the body of literature in the field. It also paved the way for understanding the research gaps for future studies.

Hence, our study provides a clear picture of research on Fintech using bibliometric analysis and a thematic literature review. However, it has certain limitations. The literature from 1984 to 2021 is considered. While there is a minimal possibility of ignoring prominent papers in the field due to the time duration, this filter applies to the present study. The keywords used were specific to the topic under investigation. One might also look at a combination of other keywords to gain further insights.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Notes on contributors

Amola Bhatt

Amola Bhatt, Ph.D.Amola Bhatt an Assistant Professor in the faculty of Finance at the Institute of Management, Nirma University, Ahmedabad, India. Her research interests lie in fintech, financial services, and financial literacy. She can be reached at [email protected].

Mayank Joshipura

Mayank Joshipura, Ph.D.Mayank Joshipura is an Associate Dean, Research and Ph.D. program, and Professor of Finance at the School of Business Management, NMIMS University, Mumbai, India. His research interests lie in financial markets, behavioral Finance, and crypto-assets. He has authored a book titled Cases in Financial Management with SAGE India. His ORCID is 0000-0001-7711-6229. He can be reached at [email protected].

Nehal Joshipura

Nehal Joshipura, Ph.D.Nehal Joshipura is an Associate Professor of Finance, Assistant Dean – New Initiatives at Durgadevi Saraf Institute of Management Studies, Mumbai, India. Her research interests lie in financial markets, portfolio management, investment strategies, and quantitative investing. Her ORCID is 0000-0001-7150-2751. She can be reached at [email protected].

Notes

1. EMEA is an acronym for Europe, Middle East, and Africa regions.

2. APAC is an acronym for Asia Pacific region.

References

- A.Basha, S., Elgammal, M.M., & Abuzayed, B.M. (2021). Online Peer-To-Peer Lending: A Review of the Literature. ResearchGate.NetElectronic Commerce Research and Applications, 48(July–August), 101069. https://doi.org/10.1016/j.elerap.2021.101069

- Adegbite, O. O., & Machethe, C. L. (2020). Bridging the financial inclusion gender gap in smallholder agriculture in Nigeria: An untapped potential for sustainable development. World Development, 127. https://doi.org/10.1016/j.worlddev.2019.104755

- Ajzen, I. (2002). Perceived behavioral control, self-efficacy, locus of control, and the theory of planned behavior. Journal of Applied Social Psychology, 32(4), 665–50. https://doi.org/10.1111/J.1559-1816.2002.TB00236.X

- Alkhowaiter, W. A. (2020). Digital payment and banking adoption research in Gulf countries: A systematic literature review. International Journal of Information Management, 53. https://doi.org/10.1016/j.ijinfomgt.2020.102102

- Anagnostopoulos, I. (2018). Fintech and regtech: Impact on regulators and banks. Journal of Economics and Business, 100(November-December), 7–25. https://doi.org/10.1016/j.jeconbus.2018.07.003

- Arner, D. W., Buckley, R. P., Zetzsche, D. A., & Veidt, R. (2020). Sustainability, FinTech and financial inclusion. European Business Organization Law Review, 21(1), 7–35. https://doi.org/10.1007/s40804-020-00183-y

- Ashta, A., & Herrmann, H. (2021). Artificial intelligence and fintech: An overview of opportunities and risks for banking, investments, and microfinance. Strategic Change, 30(3), 211–222. https://doi.org/10.1002/JSC.2404

- Au, Y. A., & Kauffman, R. J. (2008). The economics of mobile payments: Understanding stakeholder issues for an emerging financial technology application. Electronic Commerce Research and Applications, 7(2), 141–164. https://doi.org/10.1016/J.ELERAP.2006.12.004

- Awan, M. J., Rahim, M. S. M., Nobanee, H., Munawar, A., Yasin, A., & Zain, A. M. (2021). Social media and stock market prediction: A big data approach. Computers, Materials and Continua, 67(2), 2569–2583. https://doi.org/10.32604/cmc.2021.014253

- Aziz, A., & Naima, U. (2021). Rethinking digital financial inclusion: Evidence from Bangladesh. Technology in Society, 64. https://doi.org/10.1016/j.techsoc.2020.101509

- Bajakić, I., Božina Beroš, M., & Grdović Gnip, A. (2021). Regulating crowdfunding in the eu – Same rules, same results? Case study of Croatia. Balkan Social Science Review, 17, 7–25. https://doi.org/10.46763/BSSR2117007B

- Bruhn, M., & Love, I. (2014). The real impact of improved access to finance: Evidence from Mexico. The Journal of Finance, 69(3), 1347–1376. https://doi.org/10.1111/JOFI.12091

- Cai, C. W. (2018). Disruption of financial intermediation by FinTech: A review on crowdfunding and blockchain. Accounting & Finance, 58(4), 965–992. https://doi.org/10.1111/ACFI.12405

- Callon, M., Courtial, J. P., & Laville, F. (1991). Co-word analysis as a tool for describing the network of interactions between basic and technological research: The case of polymer chemsitry. Scientometrics, 22(1), 155–205. https://doi.org/10.1007/BF02019280

- Cao, L., Yang, Q., & Yu, P. S. (2021). Data science and AI in FinTech: An overview. International Journal of Data Science and Analytics, 12(2), 81–99. https://doi.org/10.1007/S41060-021-00278-W

- Cecchini, S., & Scott, C. (2003). Can information and communications technology applications contribute to poverty reduction? Lessons from rural India. Information Technology for Development, 10(2), 73–84. https://doi.org/10.1002/itdj.1590100203

- Chang, V., Baudier, P., Zhang, H., Xu, Q., Zhang, J., & Arami, M. (2020). How Blockchain can impact financial services – The overview, challenges and recommendations from expert interviewees. Technological Forecasting and Social Change, 158, 120166. https://doi.org/10.1016/j.techfore.2020.120166

- Chang, R. M., Kauffman, R. J., & Kwon, Y. (2014). Understanding the paradigm shift to computational social science in the presence of big data. Decision Support Systems, 63, 67–80. https://doi.org/10.1016/J.DSS.2013.08.008

- Chanias, S., Myers, M. D., & Hess, T. (2019). Digital transformation strategy making in pre-digital organizations: The case of a financial services provider. Journal of Strategic Information Systems, 28(1), 17–33. https://doi.org/10.1016/j.jsis.2018.11.003

- Chaudhry, S. M., Ahmed, R., Huynh, T. L. D., & Benjasak, C. (2022). Tail risk and systemic risk of finance and technology (FinTech) firms. Technological Forecasting and Social Change, 174, 121191. https://doi.org/10.1016/j.techfore.2021.121191

- Chauhan, S. (2015). Acceptance of mobile money by poor citizens of India: Integrating trust into the technology acceptance model. Info, 17(3), 58–68. https://doi.org/10.1108/INFO-02-2015-0018/FULL/XML

- Chen, Y., & Bellavitis, C. (2020). Blockchain disruption and decentralized finance: The rise of decentralized business models. Journal of Business Venturing Insights, 13, e00151. https://doi.org/10.1016/j.jbvi.2019.e00151

- Chinoda, T., & Mashamba, T. (2021). Fintech, financial inclusion and income inequality nexus in Africa. Cogent Economics and Finance, 9(1). https://doi.org/10.1080/23322039.2021.1986926

- Christidis, K., & Devetsikiotis, M. (2016). Blockchains and Smart Contracts for the Internet of Things. IEEE Access, 4, 2292–2303. https://doi.org/10.1109/ACCESS.2016.2566339

- Currie, W. L., Gozman, D. P., & Seddon, J. J. M. (2018). Dialectic tensions in the financial markets: A longitudinal study of pre- and post-crisis regulatory technology. Journal of Information Technology, 33(4), 304–325. https://doi.org/10.1057/s41265-017-0047-5

- Danvila-del-Valle, I., Estévez-Mendoza, C., & Lara, F. (2019). Human resources training: A bibliometric analysis. Elsevier, 101, 627–636. https://doi.org/10.1016/j.jbusres.2019.02.026

- Daqar, M. A., Arqawi, S., & Karsh, S. A. (2021). Fintech in the eyes of Millennials and Generation Z (the financial behavior and Fintech perception). Banks and Bank Systems, 15(3), 20–28 doi:10.21511/bbs.15(3).2020.03. https://doi.org/10.21511/bbs.15(3).2020.03

- Davis, F. D. (1989). Perceived usefulness, perceived ease of use, and user acceptance of information technology. MIS Quarterly: Management Information Systems, 13(3), 319–339. https://doi.org/10.2307/249008

- Demirgüç-Kunt, A., Klapper, L., Singer, D., Ansar, S., & Hess, J. (2020). The global findex database 2017: Measuring financial inclusion and opportunities to expand access to and use of financial services. The World Bank Economic Review, 34(Suppl_1), S2–S8. https://doi.org/10.1093/wber/lhz013

- Ding, Y., & Cronin, B. (2010). Popular and/or Prestigious? Measures of scholarly esteem. Information Processing & Management, 47(1), 80–96. https://doi.org/10.1016/j.ipm.2010.01.002

- Donovan, K. P. (2012). Mobile money more freedom? The impact of M-PESA’s network power on development as freedom. International Journal of Communication, 6, 2647–2669. https://open.uct.ac.za/handle/11427/19274

- Donthu, N., Kumar, S., & Pattnaik, D. (2020). Forty-five years of journal of business research: A bibliometric analysis. Journal of Business Research, 109, 1–14. https://doi.org/10.1016/j.jbusres.2019.10.039

- Donthu, N., Kumar, S., Paul, J., Pattnaik, D., & Strong, C. (2020). A retrospective of the journal of strategic marketing from 1993 to 2019 using bibliometric analysis. Journal of Strategic Marketing, 501, 1–21. https://doi.org/10.1080/0965254X.2020.1794937

- Duarte, J., Siegel, S., & Young, L. (2012). Trust and Credit: The Role of Appearance in Peer-to-peer Lending. The Review of Financial Studies, 25(8), 2455–2484. https://doi.org/10.1093/RFS/HHS071

- Dupuis, D., & Gleason, K. (2021). Money laundering with cryptocurrency: Open doors and the regulatory dialectic. Journal of Financial Crime, 28(1), 60–74. https://doi.org/10.1108/JFC-06-2020-0113/FULL/HTML

- Echchakoui, S. (2020). Why and how to merge Scopus and Web of Science during bibliometric analysis: The case of sales force literature from 1912 to 2019. Journal of Marketing Analytics, 8(3), 165–184. https://doi.org/10.1057/s41270-020-00081-9

- Emekter, R., Tu, Y., Jirasakuldech, B., & Lu, M. (2014). Evaluating credit risk and loan performance in online Peer-to-Peer (P2P) lending, 47(1), 54–70. https://doi.org/10.1080/00036846.2014.962222

- Estrin, S., Khavul, S., & Wright, M. (2021). Soft and hard information in equity crowdfunding: Network effects in the digitalization of entrepreneurial finance. Small Business Economics, 58, 1761–1781. https://doi.org/10.1007/s11187-021-00473-w

- EY. (2021a). The winds of change Trends shaping India’s FinTech sector.

- EY. (2021b). Where will wealth take clients next? 2021 Global Wealth Research Report (pp. 1–44). https://assets.ey.com/content/dam/ey-sites/ey-com/en_gl/topics/wealth-and-asset-management/ey-2021-global-wealth-research-report-optimized-for-web-v2.pdf

- Fanning, K., & Centers, D. P. (2016). Blockchain and its coming impact on financial services. Journal of Corporate Accounting & Finance, 27(5), 53–57. https://doi.org/10.1002/jcaf.22179

- Fenwick, M., McCahery, J. A., & Vermeulen, E. P. M. (2019). The end of ‘Corporate’ governance: Hello ‘Platform’ governance. European Business Organization Law Review, 20(1), 171–199. https://doi.org/10.1007/s40804-019-00137-z

- Fernandes, C., Borges, M. R., & Caiado, J. (2021). The contribution of digital financial services to financial inclusion in Mozambique: An ARDL model approach. Applied Economics, 53(3), 400–409. https://doi.org/10.1080/00036846.2020.1808177

- Findexable. (2021). The 2021 Global Fintech Ranking. https://www.fintechmundi.com/2021-global-fintech-rankings/

- Fishbein, M., & Ajzen, I. (1977). Belief, Attitude, Intention, and Behavior: An Introduction to Theory and Research. Contemporary Sociology, 6(2), 244. https://doi.org/10.2307/2065853

- Fornell, C., & Larcker, D. F. (1981). Evaluating Structural Equation Models with Unobservable Variables and Measurement Error. Journal of Marketing Research, 18(1), 39–50. https://doi.org/10.1177/002224378101800104

- Fornell, C., Rhee, B.-D., & Yi, Y. (1991). Direct regression, reverse regression, and covariance structure analysis. Marketing Letters, 2(3), 309–320. https://doi.org/10.1007/BF00554134

- Gabor, D., & Brooks, S. 2016. The digital revolution in financial inclusion: International development in the fintech era. New political economy, 22(4), 423–436. https://doi.org/10.1080/13563467.2017.1259298.

- Gai, K., Qiu, M., & Sun, X. (2018). A survey on FinTech. Journal of Network and Computer Applications, 103, 262–273. https://doi.org/10.1016/j.jnca.2017.10.011

- Gálvez-Sánchez, F. J., Lara-Rubio, J., Verdú-Jóver, A. J., & Meseguer-Sánchez, V. (2021). Research advances on financial inclusion: A bibliometric analysis. Sustainability (Switzerland), 13 (6), 3156. https://doi.org/10.3390/su13063156

- Ghandour, A. (2021). Opportunities and Challenges of Artificial Intelligence in Banking: Systematic Literature Review. https://digitallibrary.aau.ac.ae/handle/123456789/651

- Gimpel, H., Rau, D., & Röglinger, M. (2018). Understanding FinTech start-ups – a taxonomy of consumer-oriented service offerings. Electronic Markets, 28(3), 245–264. https://doi.org/10.1007/S12525-017-0275-0

- Gomber, P., Kauffman, R. J., Parker, C., & Weber, B. W. (2018). On the Fintech revolution: Interpreting the forces of innovation, disruption, and transformation in financial services. Journal of Management Information Systems, 35(1), 220–265. https://doi.org/10.1080/07421222.2018.1440766

- Gomber, P., Koch, J. A., & Siering, M. (2017). Digital finance and FinTech: Current research and future research directions. Journal of Business Economics, 87(5), 537–580. https://doi.org/10.1007/S11573-017-0852-X

- Goyal, K., & Kumar, S. (2021). Financial literacy: A systematic review and bibliometric analysis. International Journal of Consumer Studies, 45(1), 80–105. https://doi.org/10.1111/ijcs.12605

- Gozman, D., Liebenau, J., & Mangan, J. (2018). The Innovation mechanisms of Fintech Start-Ups: Insights from SWIFT’s innotribe competition. Journal of Management Information Systems, 35(1), 145–179. https://doi.org/10.1080/07421222.2018.1440768

- Gozman, D., & Willcocks, L. (2019). The emerging Cloud Dilemma: Balancing innovation with cross-border privacy and outsourcing regulations. Journal of Business Research, 97, 235–256. https://doi.org/10.1016/j.jbusres.2018.06.006

- Gurrea-Martínez, A. N. R. (2019). The law and finance of initial coin offerings. In Brummer, Chris (Ed.), Cryptoassets: Legal, Regulatory, and Monetary Perspectives (pp. 117–C6.P133). Oxford Academic. https://doi.org/10.1093/oso/9780190077310.003.0006

- Haddad, C., Hornuf, L., Haddad, C., & Hornuf, L. (2019). The emergence of the global fintech market: Economic and technological determinants. Small Business Economics, 53(1), 81–105. https://doi.org/10.1007/S11187-018-9991-X

- Hendrikse, R., van Meeteren, M., & Bassens, D. (2020). Strategic coupling between finance, technology and the state: Cultivating a Fintech ecosystem for incumbent finance. Environment & Planning A, 52(8), 1516–1538. https://doi.org/10.1177/0308518X19887967

- Henseler, J., Ringle, C. M., & Sarstedt, M. (2015). A new criterion for assessing discriminant validity in variance-based structural equation modeling. Journal of the Academy of Marketing Science, 43(1), 115–135. https://doi.org/10.1007/S11747-014-0403-8/FIGURES/8

- Hornuf, L., Klus, M. F., Lohwasser, T. S., & Schwienbacher, A. (2021). How do banks interact with fintech startups?. Small Business Economics, 57(3), 1505–1526. https://doi.org/10.1007/s11187-020-00359-3

- Hu, Z., Ding, S., Li, S., Chen, L., & Yang, S. (2019). Adoption intention of fintech services for bank users: An empirical examination with an extended technology acceptance model. Symmetry, 11(3), 340. https://doi.org/10.3390/sym11030340

- Huei, C. T., Cheng, L. S., Seong, L. C., Khin, A. A., & Leh Bin, R. L. (2018). Preliminary study on consumer attitude towards fintech products and services in Malaysia. International Journal of Engineering and Technology(UAE), 7(2), 166–169. https://doi.org/10.14419/ijet.v7i2.29.13310

- Hughes, H. (2021). The Complex Implications of Fintech for Financial Inclusion. LAW AND CONTEMPORARY PROBLEMS, 84(115), 115–128. http://lcp.law.duke.edu/

- Ingale, K. K., & Paluri, R. A. (2020). Financial literacy and financial behaviour: a bibliometric analysis. Review of Behavioral Finance, 14(1), 130–154. https://doi.org/10.1108/RBF-06-2020-0141

- Jack, W., & Suri, T. (2011). Mobile Money: The Economics of M-PESA. https://doi.org/10.3386/W16721

- Jack, W., & Suri, T. (2014). Risk Sharing and Transactions Costs: Evidence from Kenya's Mobile Money Revolution. The American Economic Review, 104(1), 183–223. https://doi.org/10.1257/AER.104.1.183

- Joia, L. A., & Cordeiro, J. P. V. (2021). Unlocking the Potential of Fintechs for Financial Inclusion: A Delphi-Based Approach. Sustainability, 13(21), 11675. https://doi.org/10.3390/SU132111675

- Jünger, M., & Mietzner, M. (2020). Banking goes digital: The adoption of FinTech services by German households. Finance Research Letters, 34. https://doi.org/10.1016/j.frl.2019.08.008

- Kabza, Milena. (2020). Artificial intelligence in financial services-benefits and costs. In Gąsiorkiewicz, Lech, Monkiewicz, Jan (Eds.), Innovation in financial services: Balancing public and private interests (ed. 1, pp. 183–198). https://doi.org/10.4324/9781003051664-14/ARTIFICIAL-INTELLIGENCE-FINANCIAL-SERVICES-BENEFITS-COSTS-MILENA-KABZA

- Kandpal, V., & Mehrotra, R. (2019). Financial inclusion: The role of fintech and digital financial services in India. Indian Journal of Economics and Business, 18(1), 95–104. https://ssrn.com/abstract=3485038

- Karjaluoto, H., Shaikh, A. A., Saarijärvi, H., & Saraniemi, S. (2019). How perceived value drives the use of mobile financial services apps. International Journal of Information Management, 47, 252–261. https://doi.org/10.1016/j.ijinfomgt.2018.08.014

- Kauffman, R. J., & Riggins, F. J. (2012). Information and communication technology and the sustainability of microfinance. Electronic Commerce Research and Applications, 11(5), 450–468. https://doi.org/10.1016/j.elerap.2012.03.001

- Kitchen, P. J., & Panopoulos, A. (2010). Online public relations: The adoption process and innovation challenge, a Greek example. Public Relations Review, 36(3), 222–229. https://doi.org/10.1016/j.pubrev.2010.05.002

- Kotarba, M. (2016). New factors inducing changes in the retail banking customer relationship management (CRM) and their exploration by the FinTech industry. Foundations of Management, 8(1), 69–78. https://doi.org/10.1515/fman-2016-0006

- Kumar, A., Liu, R., & Shan, Z. (2020). Is blockchain a silver bullet for supply chain management? Technical challenges and research opportunities. Decision Sciences, 51(1), 8–37. https://doi.org/10.1111/deci.12396

- Lagna, A., & Ravishankar, M. N. (2021). Making the world a better place with fintech research. Information Systems Journal, 32(1), 61–102. https://doi.org/10.1111/isj.12333

- Larios-Hernández, G. J. (2017). Blockchain entrepreneurship opportunity in the practices of the unbanked. Business Horizons, 60(6), 865–874. https://doi.org/10.1016/j.bushor.2017.07.012

- Latimer, P., & Duffy, M. (2019). Deconstructing digital currency and its risks: Why ASIC must rise to the regulatory challenge. Federal Law Review, 47(1), 121–150. https://doi.org/10.1177/0067205X18816237

- Lee, I. (2018). Social media analytics for enterprises: Typology, methods, and processes. Business Horizons, 61(2), 199–210. https://doi.org/10.1016/J.BUSHOR.2017.11.002

- Leong, C., Tan, B., Xiao, X., Tan, F. T. C., & Sun, Y. (2017). Nurturing a FinTech ecosystem: The case of a youth microloan startup in China. International Journal of Information Management, 37(2), 92–97. https://doi.org/10.1016/j.ijinfomgt.2016.11.006

- Li, F., Lu, H., Hou, M., Cui, K., & Darbandi, M. (2021). Customer satisfaction with bank services: The role of cloud services, security, e-learning and service quality. Technology in Society, 64. https://doi.org/10.1016/j.techsoc.2020.101487

- Lin, M., Prabhala, N. R., & Viswanathan, S. (2012). Judging Borrowers by the Company They Keep: Friendship Networks and Information Asymmetry in Online Peer-to-Peer Lending. Management Science, 59(1), 17–35. https://doi.org/10.1287/MNSC.1120.1560

- Liu, J., Kauffman, R. J., & Ma, D. (2015). Competition, cooperation, and regulation: Understanding the evolution of the mobile payments technology ecosystem. Electronic Commerce Research and Applications, 14(5), 372–391. https://doi.org/10.1016/j.elerap.2015.03.003

- Liu, Z., Yin, Y., Liu, W., & Dunford, M. (2015). Visualizing the intellectual structure and evolution of innovation systems research: A bibliometric analysis. Scientometrics, 103(1), 135–158. https://doi.org/10.1007/s11192-014-1517-y

- Li, B., & Xu, Z. (2021). Insights into financial technology (FinTech): A bibliometric and visual study. Financial Innovation, 7(1), 69. https://doi.org/10.1186/S40854-021-00285-7

- Low, M. P., & Siegel, D. (2020). A bibliometric analysis of employee-centred corporate social responsibility research in the 2000s. Social Responsibility Journal, 16(5), 691–717. https://doi.org/10.1108/SRJ-09-2018-0243

- Lutfi, A., Al-Okaily, M., Alshirah, M. H., Alshira’h, A. F., Abutaber, T. A., & Almarashdah, M. A. (2021). Digital financial inclusion sustainability in Jordanian context. Sustainability (Switzerland), 13(11), 6312. https://doi.org/10.3390/su13116312

- Lu, V. N., Wirtz, J., Kunz, W. H., Paluch, S., Gruber, T., Martins, A., & Patterson, P. G. (2020). Service robots, customers and service employees: What can we learn from the academic literature and where are the gaps?. Journal of Service Theory and Practice, 30(3), 361–391. https://doi.org/10.1108/JSTP-04-2019-0088/FULL/HTML

- Maier, E. (2016). Supply and demand on crowdlending platforms: Connecting small and medium-sized enterprise borrowers and consumer investors. Journal of Retailing and Consumer Services, 33, 143–153. https://doi.org/10.1016/j.jretconser.2016.08.004

- Manser Payne, E. H., Dahl, A. J., & Peltier, J. (2021). Digital servitization value co-creation framework for AI services: A research agenda for digital transformation in financial service ecosystems. Journal of Research in Interactive Marketing, 15(2), 200–222. https://doi.org/10.1108/JRIM-12-2020-0252

- Milian, E. Z., Spinola, M. D. M., & Carvalho, M. M. D. (2019). Fintechs: A literature review and research agenda. Electronic Commerce Research and Applications, 34, 100833. https://doi.org/10.1016/J.ELERAP.2019.100833

- Mogaji, E., Soetan, T. O., & Kieu, T. A. (2021). The implications of artificial intelligence on the digital marketing of financial services to vulnerable customers. Australasian Marketing Journal, 29(3), 235–242. https://doi.org/10.1016/j.ausmj.2020.05.003

- Mollick, E. (2014). The dynamics of crowdfunding: An exploratory study. Journal of Business Venturing, 29(1), 1–16. https://doi.org/10.1016/J.JBUSVENT.2013.06.005

- Momtaz, P. P. (2020). Initial coin offerings. PLoS ONE, 15(5), e0233018. https://doi.org/10.1371/JOURNAL.PONE.0233018

- Morkunas, V. J., Paschen, J., & Boon, E. (2019). How blockchain technologies impact your business model. Business Horizons, 62(3), 295–306. https://doi.org/10.1016/j.bushor.2019.01.009

- Mortimer, G., Neale, L., Hasan, S. F. E., & Dunphy, B. (2015). Investigating the factors influencing the adoption of m-banking: A cross cultural study. International Journal of Bank Marketing, 33(4), 545–570. https://doi.org/10.1108/IJBM-07-2014-0100/FULL/WWW.BANGKOKPOST.COM/MIDYEAR2002/BANKING

- Msweli, N. T., & Mawela, T. (2020). Enablers and Barriers for Mobile Commerce and Banking Services Among the Elderly in Developing Countries: A Systematic Review. Lecture Notes in Computer Science (Including Subseries Lecture Notes in Artificial Intelligence and Lecture Notes in Bioinformatics), 12067 LNCS, 319–330. https://doi.org/10.1007/978-3-030-45002-1_27/FIGURES/1

- Nakamoto, S. (2008). Bitcoin: A peer-to-peer electronic cash system. Decentralized Business Review. https://www.debr.io/article/21260.pdf

- Nasir, A., Shaukat, K., Khan, K. I., Hameed, I. A., Alam, T. M., & Luo, S. (2021). Trends and Directions of Financial Technology (Fintech) in Society and Environment: A Bibliometric Study. Applied Sciences, 11(21), 10353. https://doi.org/10.3390/APP112110353

- Niemand, T., Rigtering, J. P. C., Kallmünzer, A., Kraus, S., & Maalaoui, A. (2021). Digitalization in the financial industry: A contingency approach of entrepreneurial orientation and strategic vision on digitalization. European Management Journal, 39(3), 317–326. https://doi.org/10.1016/j.emj.2020.04.008

- Osmani, M., El-Haddadeh, R., Hindi, N., Janssen, M., & Weerakkody, V. (2021). Blockchain for next generation services in banking and finance: Cost, benefit, risk and opportunity analysis. Journal of Enterprise Information Management, 34(3), 884–899. https://doi.org/10.1108/JEIM-02-2020-0044/FULL/HTML

- Ozili, P. K. (2018). Impact of digital finance on financial inclusion and stability. Borsa Istanbul Review, 18(4), 329–340. https://doi.org/10.1016/j.bir.2017.12.003

- Ozili, P. K. (2018). Impact of digital finance on financial inclusion and stability. Borsa Istanbul Review, 18(4), 329–340. https://doi.org/10.1016/j.bir.2017.12.003

- Palmié, M., Wincent, J., Parida, V., & Caglar, U. (2020). The evolution of the financial technology ecosystem: An introduction and agenda for future research on disruptive innovations in ecosystems. Technological Forecasting and Social Change, 151. https://doi.org/10.1016/j.techfore.2019.119779

- Patrício, L. D., & Ferreira, J. J. (2021). Blockchain security research: Theorizing through bibliographic-coupling analysis. Journal of Advances in Management Research, 18(1), 1–35. https://doi.org/10.1108/JAMR-04-2020-0051

- Pau, L. F. (1991). Artificial intelligence and financial services. IEEE Transactions on Knowledge and Data Engineering, 3(2), 137–148. https://doi.org/10.1109/69.87994

- Perry, M., & Ferreira, J. (2018). Moneywork: Practices of use and social interaction around digital and analog money. ACM Transactions on Computer-Human Interaction, 24(6 1–32). https://doi.org/10.1145/3162082

- Polasik, M., Piotrowska, A. I., Wisniewski, T. P., Kotkowski, R., & Lightfoot, G. (2015). Price fluctuations and the use of bitcoin: An empirical inquiry. International Journal of Electronic Commerce, 20(1), 9–49. https://doi.org/10.1080/10864415.2016.1061413

- Qi, B. Y., & Xiao, J. (2018). Fintech: AI powers financial services to improve people’s lives. Communications of the ACM, 61(11), 65–69. https://doi.org/10.1145/3239550

- Rabbani, M. R., Khan, S., & Thalassinos, E. I. (2020). FinTech, blockchain and Islamic finance : An extensive literature review. International Journal of Economics and Business Administration, VIII(2), 65–86. doi:10.35808/ijeba/444

- Ranade, A. (2017). Role of “Fintech” in Financial inclusion and new business models. Economic and Political Weekly, 52(12), 125–128. https://www.epw.in/journal/2017/12/money-banking-and-finance/role-‘fintech’-financial-inclusion-and-new-business-models

- Ravikumar, T. (2019). Digital financial inclusion: A payoff of financial technology and digital finance uprising in India. Article in International Journal of Scientific & Technology Research, 8(11), 3434–3438. www.ijstr.org

- Riehmann, P., Hanfler, M., & Froehlich, B. (2005). Interactive Sankey diagrams. Proceedings - IEEE Symposium on Information Visualization, INFO VIS, Minneapolis, Minnesota, United States, 233–240. https://doi.org/10.1109/INFVIS.2005.1532152

- Sadok, H. (2021). How can inclusive growth be enabled from financial technology?. International Journal of Business Performance Management, 22(2–3), 159–179. https://doi.org/10.1504/IJBPM.2021.116410