?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

We assess the effect of the recent royal wedding of Prince Harry and Meghan Markle on various sectors of the UK stock market over the period between November 2017 and May 2018. For this purpose, the event study methodology is used to estimate abnormal returns and conduct several robustness tests such as the Corrado ranking test, the Chesney non-parametric conditional distribution approach, the Fama-French five-factor model, the market model, allowing for market integration, and the removal of firm-specific information. In addition, we use various ARCH-type models to capture changes in systematic risk. The results show that the effect of the royal wedding is limited to few sectors. We also find that a positive national and investor mood does not always boost sectoral stock returns. In addition, we observe that announcements related to the royal wedding led to changes in both short-term and long-term systematic risk.

1. Introduction

A royal wedding has been a significant event for the royal family throughout the history of the monarchy in the United Kingdom as the occasion attracts substantial national and international attention. While royal weddings take place in a traditional manner, the wedding of Prince Harry and Meghan Markle was relatively unconventional in many respects—for example, the wedding was deemed as a family affair rather than an official state event. The wedding was expected to affect various sectors of the UK stock market, such as tourism and fashion. According to Euromonitor Research, the wedding will keep the UK as a desired tourist attraction with its culture and heritage in the coming years due to the media coverage.Footnote1 The wedding was predicted to boost the tourism sector as tourists would visit the UK to celebrate the occasion. Furthermore, the royal wedding was expected to affect the national mood and investor mood positively, which would in turn lead to rising stock prices (Landsall-Welfar, Lampos and Cristianini, Citation2012; Prechter & Parker, Citation2007). The Brand Finance (2018) indicated the wedding of Prince Harry to Meghan Markle benefit the British economy and spread across several sectors, especially for tourism and merchandise sector. However, according to the Bank of England, previous royal events such as Diamond Jubilee in 2012 increase in spending but leading to a total decrease in GDP of 0.5% in the second following the Diamond Jubilee event. The literature has shown little reliable evidence on the impact of Royal Wedding on the UK economy as well as the UK stock market. This study, therefore, will contribute to the literature by measuring the effect of Royal Wedding on the UK stock market.

To assess the “Royal Wedding effect”, we use the event study methodology to estimate abnormal returns and capture, through various risk models, changes in the systematic risk of the UK stock market sectors. In general, we find evidence indicating that the effect of the royal wedding on the UK stock market, but the effect is limited to few sectors. Our results also show that a positive national and investor mood does not always boost sectoral stock returns. In addition, we observe that the royal wedding announcements led to changes in both short-term and long-term systematic risk.

The remainder of the paper is structured as follows. Section 2 provides a brief overview of recent history of Royal Wedding effect and literature surrounding royal events, the data and methodologies are presented in Section 3, Section 4 discusses the results, and Section 5 concludes the paper.

2. Literature review

According to Atkinson (Citation2018), there has always been a strong tie between British royal weddings and stock market performance, known as the “Royal Wedding effect”. In the 1980s and the 1990s, royal weddings were the “magic spell for the market”. During the year of Prince Harry’s parents’ marriage in 1981, for instance, the British stock market (as proxied by FTSE All-Share Index) went up by 7.24% from 291.99 at the beginning of 1981 to 313.12 at the end of the year. Similar trends were associated with the 1986 wedding of Prince Andrew and Sarah Ferguson and the 1999 wedding of Prince Edward and Sophie Rhys-Jones’s.

Royal weddings, however, could not resist the effect of economic crises. In 1973, the wedding of Princess Anne and Captain Mark Phillips could not help the British stock market during the energy crisis as the FTSE All-Share Index ended the year 31.63% lower than the start of the year. The same is true of the wedding of Prince William and Catherine Middleton in 2011 as the market lost 6.7% by the end of the year due to the long-lasting effect of the global financial crisis on the British economy. Given the bright picture of the British economy this year with the lowest unemployment rate, together with an increase in wage growth and jobs, the wedding of Prince Harry and Meghan Markle was expected to boost the British economy. A report by Brand Finance claims that the royal wedding would boost the British economy by more than £1 billion.Footnote2 The sectors that could benefit from the wedding include tourism, retail and restaurants, fashion, merchandise, and public relations. The Brand Finance report predicted a 5.5% surge in non-business visits from the US and the rest of the world as well as an increase in travel and accommodation spending. In addition, the report predicted that the retail and restaurants sectors would bring in £250 million through food, beverages and parties. Another sector, which was anticipated to benefit from the royal wedding, is the fashion sector. It was widely believed that Meghan was a popular and accomplished actress and hence, the “Meghan Effect” was expected to surpass the “Kate Effect” in the fashion industry.

While the Brand Finance report provides a favourable and optimistic picture of the British economy following the royal wedding, Petroff (Citation2018) disputes the view that the wedding would attract tourists to the UK. She argued that the royal wedding would not affect the British tourism sector in the short run as there is no abnormal increase in the number of bookings for the UK. However, she adds that the wedding could have a positive impact on the tourism sector in the long run as it would keep the UK as a desired destination for tourists. However, the ability of the royal family to attract tourism is a controversial issue on which the jury is still out.

If royal weddings have a positive impact on the national mood, that will subsequently affect the stock market performance (Landsall-Welfare et al., Citation2012). Many studies in behavioural finance investigate the link between the public mood and stock market performance. Prechter (Citation1979, Citation1999) and Prechter and Parker (Citation2007) suggest that social mood can be reflected in stock market indices as investors tend to react in accordance with the mood prevailing in the aftermath of an event. Nofsinger and Kim (Citation2003) and Prechter et al., (Citation2012) find that a negative social mood can cause a substantial decline in stock prices whereas a positive social mood can lead to a significant increase in stock prices. Bollen et al. (Citation2011) and Gilbert and Karahalios (Citation2010) support this proposition by showing how responsive financial markets are to changes in social sentiment.

Several other studies find a positive relationship between investor mood and stock returns. Saunders (Citation1993) and Hirshleifer and Shumway (Citation2003), for instance, find evidence indicating that the NYSE produces positive returns on sunny days and negative returns on cloudy days. Moreover, Kamstra et al. (Citation2000) note that negative returns are associated with the switch from standard time to daylight savings time. These findings imply that negative (positive) investor mood can affect the stock market negatively (positively).

The royal wedding is one of the most important events in the UK. The elevation of the national mood during a royal wedding is expected to affect investor mood and consequently stock market performance. In addition, the evidence of on the effect on a royal wedding on the stock market at the sectoral level is limited. We, therefore, investigate how the sectors of the UK stock market respond to the royal wedding announcements in terms of risk and return.

3. Methodology

The event study methodology is employed to examine the “royal wedding effect” on the stock market. First, we estimate the ex post abnormal returns of each company using the following equation:

where is the abnormal return of firm i at time t,

is the daily return of firm i, calculated as the first log difference of the stock price index,

is the intercept of the CAPM line,

is the slope of the CAPM line,

is the market return, proxied by FTSE100, and

is the risk-free rate, proxied by 10-year bond yield. Daily abnormal returns of all firms within a sector are averaged to obtain a daily abnormal return of that sector, and a t-statistic is used to determine if the reaction is statistically significant for each event date.

To control for the event when the efficient market hypothesis (EMH) does not hold and to find out if the market continues to react following an event, we estimate cumulative abnormal returns (CAR) of 2, 5 and 10 days after the event date and use the t-statistic to check if the results are statistically significant. These event windows are widely accepted in event study methodology (Vikash et al., Citation2017). In addition, we suspect that few sectors may react before the event date as the wedding had been announced several months before it took place—for this reason, we estimate cumulative abnormal returns of 2 and 5 days before the event date to find out if the market anticipates events.

The event study methodology has several drawbacks such as non-normality of abnormal returns and firm-specific effects, the impact of stock market integration and spillover effects. In addition, the parametric t statistics may be affected by abnormal returns, which are often not normally distributed and exhibit high kurtosis and positive skewness. Therefore, we conduct several robustness tests to address these problems. We use the Corrado (Citation1989) non-parametric ranking test to remove the effect of non-normality and the non-parametric conditional distribution approach proposed by Chesney et al. (Citation2011) to estimate the probability of an event having an extreme effect on a sector. Furthermore, we remove all firms that release firm-specific news within a window of days from the announcement day to ensure that abnormal returns are solely driven by the royal wedding-related events. To control for asynchronicity, stock market integration, and spillover effects, we modify the CAPM by incorporating three market risk premia representing Asia

, Europe

and the U.S.

into the model. We also use the Fama-French 5-factor model of Fama and French (Citation2015) (which includes several factors controlling for size, value, profitability and investment) to re-estimate expected returns and abnormal returns and use these results for robustness.

Many studies have investigated the effect of news (both firm-specific and general) on systematic risk. Engelberg et al. (Citation2018), for instance, show that betas are higher on earnings announcement days. In addition, Vikash et al., Citation2017) find that political events such as Brexit can have various effects on sectoral systematic risk. On 27 November 2017, Clarence House announced that the wedding of Prince Harry and Meghan would take place in the spring of 2018. According to CNNMoney (2018), the wedding would keep the UK in focus and positively affect the British tourism industry in the long run. Furthermore, this event might have spillover effects on the systematic risk of other sectors. We capture aggregate, short-term and long-term changes in systematic risk by using a modified CAPM with interaction variables.

To capture the aggregate change in systematic risk, we create a dummy variable (D) that takes a value of 1 on the announcement day and 0 otherwise. Following Ramiah et al. (Citation2013), we multiply the dummy variable by the market risk premium to create an interaction variable. The model takes the following form:

where is the return of sector S at time t,

is the risk-free rate at time t,

is market return at time t,

is a dummy variable that takes the value of one on the first day of trading following an announcement and zero otherwise,

is the error term,

is the intercept of the regression equation where E(

) is equal to zero,

is the average short-term systematic risk of sector S,

captures the change in the sectoral risk, and

is a measure of the change in the intercept of equation (1).

According to Ramiah et al. (Citation2013), the problem with Equationequation (1)(1)

(1) is that it cannot be used to capture the individual effect on systematic risk of each announcement. We, therefore, use the following equation to estimate the short-term change in systematic risk:

where is the individual dummy variable that takes a value of 1 on event j and zero otherwise,

captures the change in systematic risk of sector S following event j. In addition, we estimate the long-term change in systematic risk following an announcement by replacing

by

which takes the value of 1 from the event date onwards and zero before the event date.

We use the Chow test to detect structural breaks following an event and the Wald test to check for redundant variables. Moreover, we introduce appropriate AR and MA terms to control for autocorrelation. Finally, we use various GARCH specifications to correct the ARCH effects including GARH, TARCH, EGARCH and PARCH models.Footnote3

4. Data and results

We downloaded daily data over the period between June 2010 and June 2018 from Thomson Reuter Eikon Datastream. The time series data include (i) individual daily closed stock prices of listed firms on the London stock exchange in 41 sectors, (ii) Financial Times Stock Exchange Group (FTSE 100) (as a proxy for the market portfolio) and (iii) the 10-year bond yield (as a proxy for the risk-free rate). FTSE100 is an index composed by shares from 100 biggest listed capitalisation companies on the London Stock Exchange. We collected daily observations on the Fama-French five factors from the Kenneth French data library at Dartmouth CollegeFootnote4 and firm-specific announcements from the London Stock Exchange. Announcements on the royal wedding of Prince Harry and Meghan are presented in .

Table 1. Announcements around the royal wedding

In general, we observe that the royal wedding announcements affected the stock market, but the effect was limited to certain sectors. The only two sectors over 41 observed sectors that exhibited abnormal returns are mobile telecommunication and personal goods. The mobile telecommunications witnessed positive reaction meanwhile the personal goods reacted negatively. The mobile telecommunication sector, for instance, experienced an abnormal return of 4.10% (with a t-statistic of 2.15) following the announcement of Kensington Palace that the wedding would be on 12 February 2018. The finding is supported by the market integration model and the Fama-French 5-factor model and market model (). This reaction could be due to the preparation for the wedding, which required extensive communication among the relevant stakeholder, which in turn would boost the revenue of mobile operators such as Vodafone.

Table 2. Abnormal returns around the royal wedding and the robustness checks

Furthermore, 13 sectors experienced delayed reactions following announcements, most of which can be attributed to the first event when Clarence House announced that Prince Harry would marry Meghan Markle. The reaction, however, is not in uniform. Sectors such as automobiles and parts and tobacco show negative cumulative abnormal returns while other sectors—including food and drug retailers, general retailers and life insurance—exhibit positive cumulative abnormal returns. Food and drug retailers, for example, had a 2-day cumulative abnormal return of 3.75% (with a t-statistic of 3.77) following the first announcement. Another example is the general retail sector which produced a 2-day cumulative abnormal return of 1.78% (with a t-statistic of 2.65; ).

Table 3. Delayed reactions following the announcements around the royal wedding

The estimation of market anticipation shows that food and drug retailers and general retailers had statistically significant cumulative abnormal returns two days before the wedding day (). The food and drug retailers sector experienced a CAR(−2) of 5.84% (with a t-statistic of 4.18) while the general retailers sector had a CAR(−2) of 1.89% (with a t-statistic of 2.01). An explanation for these reactions is that the public tends to spend more on clothes and dining during royal events, which reflects positively on the stock prices of the underlying sectors. At least two of the robustness tests support the findings.

Table 4. Market anticipation 2 days before the wedding day and the robustness checks

We also find evidence indicating that royal wedding-related events do not necessarily boost in stock returns at the sectoral level. The personal goods sector, for instance, shows an AR of −2.20% on the first trading day after the royal wedding (with a t-statistic of −2.19), a result that is supported by the market integration model and the Fama-French 5 factors model (). Moreover, several sectors experienced negative CARs in reaction to the royal wedding announcements, including automobiles and parts, food and drug retailers, non-life insurance, technology hardware equipment, and services and tobacco. These findings suggest that the effect of the royal wedding varies sector by sector and that sectoral stock returns do not necessarily reflect national mood and investor mood.

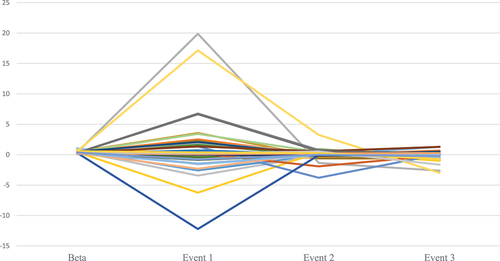

We find that announcements related to the royal wedding had an almost symmetric aggregate effect on the systematic risk of sectors. A total of 21 sectors experienced a decline in systematic risk while 20 sectors exhibited an increase in systematic risk (). When Equationequation (2)(2)

(2) is used to assess the individual effect of each announcement, we discover that the first announcement led to a diamond risk phenomenon (see Ramiah et al., Citation2013) whereby the automobiles and part sector experienced the highest increase in systematic risk (from 0.37 to 20.25) while the industrial transportation sector had the biggest decline in systematic risk (from 0.31 to −11.90; see ). Other notable findings pertain to food and drug retailers, general retailers, and the travel and leisure sectors, which experienced a decline in systematic risk following the first announcement regarding the royal wedding, which means that the royal announcement represented positive news for those sectors. Furthermore, when we replace

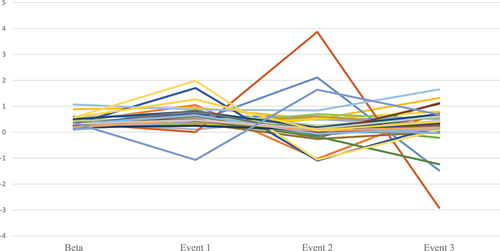

with

and re-estimate Equationequation (2)

(2)

(2) , we observe that the long-term effect of the royal wedding day varies across sectors (see ). Our results confirm that the travel and leisure sector continue to show a decrease in systematic risk in the long run, which perhaps supports the proposition that royal events attract tourists.

Figure 1. Aggregate change in systematic risk following the royal wedding announcements.

Figure 2. Short-term change in systematic risk following the royal wedding announcements.

Figure 3. Long-term change in systematic risk following the royal wedding announcements.

In comparison with the literature review, it can be seen that royal marriages have a different impact on the stock market at different times. Whereas prior studies revealed a positive association between royal weddings in the twentieth century, the impact of marriages in the twenty-first century is unclear. Only two sectors, mobile telecommunications and personal goods, experience a significant impact on Prince Harry’s wedding, with personal goods having a negative reaction. Furthermore, unfavourable reactions are observed in most of sectors within 2 days, 5 days, and 10 days after the event announcement.

5. Conclusion

Although a royal wedding is an important event, its effect on the sectors of the UK stock market is unclear. According to the behavioural school of thought, the event is expected to help the stock market produce positive returns due to an increase in the national level of joy. Our findings confirm the existence of the “Royal Wedding effect”, but this effect only shows in few sectors. In addition, we find that a positive national and investor mood does not necessarily lead to positive stock returns, particularly at the sectoral level. The results also show that the recent royal wedding was most beneficial to the travel and leisure sector, which experienced a decline in both short-term and long-term risk. Our findings also suggest that the Royal family can make financial sense for the UK economy by boosting in some particular sectors such as travel and leisure, hence an appropriate policy must be in place to maintain and promote the image of the Royal family.

The evidence from our study indicates that Royal Wedding event, as a part of royal events, generates abnormal returns in the UK stock market. However, it does not show the spill-over effect of these events on other countries in the Commonwealth. Future research should therefore investigate the impact of royal events on those countries.

Availability of data and materials

The data is collected from Eikon.

Author contribution

Huy Pham: Conceptualization; Project administration; Supervision, Formal analysis, Methodology; Resources; Software; Vikash Ramiah: Formal analysis, Investigation, Roles/Writing – original draft Hanh Le: Revise and Rewrite Manuscript, Data Analysis Nisreen Moosa: Formal analysis, Investigation, Writing – review & editing Osama Al Hares: Validation, Data Curation and Visualization

Disclosure statement

No potential conflict of interest was reported by the authors.

Additional information

Funding

Notes

3. We do not report these results for brevity, but they are available upon request.

References

- Atkinson, D. (2018, May 18). Harry and Meghan: Royal wedding impact on markets. Capital.com. https://capital.com/harry-and-meghan-what-could-their-marriage-mean-for-markets

- Bollen, J., Mao, H., & Zeng, X. (2011). Twitter mood predicts the stock market. Journal of Computational Science, 2(1), 1–12. https://doi.org/10.1016/j.jocs.2010.12.007

- Chesney, M., Reshetar, G., & Karaman, M. (2011). The impact of terrorism on financial markets: An empirical study. Journal of Banking and Finance, 35(2), 253–267. https://doi.org/10.1016/j.jbankfin.2010.07.026

- Corrado, C. J. (1989). A non-parametric test for abnormal security price performance in event studies. Journal of Financial Economics, 23(2), 385–395. https://doi.org/10.1016/0304-405X(89)90064-0

- Engelberg, J., McLean, R. D., & Pontiff, J. (2018). Anomalies and news. Journal of Finance. Rapid Publication, 73(5), 1971–2001. https://doi.org/10.1111/jofi.12718

- Fama, E. F., & French, K. R. (2015). A five-factor asset pricing model. Journal of Financial Economics, 116(1), 1–22. https://doi.org/10.1016/j.jfineco.2014.10.010

- Gilbert, E., & Karahalios, K. 2010. “Widespread worry and the stock market.” In The Proceedings of the Fourth International AAAI Conference on Weblogs and Social Media, Washington, edited by Association for the Advancement of Artificial Intelligence, 58–65. California: AAAI Press.

- Hirshleifer, D., & Shumway, T. (2003). Good day sunshine: Stock returns and the weather. Journal of Finance, 58(3), 1009–1032. https://doi.org/10.1111/1540-6261.00556

- Kamstra, M. J., Kramer, L. A., & Levi, M. D. (2000). Losing sleep at the market: The daylight-savings anomaly. American Economic Review, 90(4), 1005–1011. https://doi.org/10.1257/aer.90.4.1005

- Lansdall-Welfare, T., Lampos, V., & Cristianini, N. (2012). Nowcasting the mood of the nation. Significance, 9(4), 6–8. https://doi.org/10.1111/j.1740-9713.2012.00588.x

- Nofsinger, J., & Kim, K. (2003). Regaining Investor Confidence. In John R. Nofsinger & Kenneth A. Kim (Eds.), Chapter 14 in infectious greed: Restoring confidence in America’s companies. Pearson.

- Petroff, A. 2018. “Royal wedding: Tourists won’t flock to UK for Harry and Meghan”. CNN. money.cnn.com, March 13. https://money.cnn.com/2018/03/13/news/royal-wedding-uk-travel-tourism/index.html

- Prechter, R. R., Jr. (1979). What’s going on? In P. Robert (Ed.), The elliot wave theorist. New Classics Library.

- Prechter, R. R., Jr. (1999). The wave principle of human social behavior and the new science of socionomics. New Classics Library.

- Prechter, R. R., Jr., Goel, D., Parker, W. D., & Lampert, M. (2012). Social mood, stock market performance, and US presidential elections: A socionomic perspective on voting results. Sage Open, 2(4), 2158244012459194. https://doi.org/10.1177/2158244012459194

- Prechter, R. R., Jr., & Parker, W. D. (2007). The financial/economic dichotomy in social behavioral dynamics: The socionomic perspective. Journal of Behavioral Finance, 8(2), 84–110. https://doi.org/10.1080/15427560701381028

- Ramiah, V., Martin, B., & Moosa, I. (2013). How does the stock market react to the announcement of green policies? Journal of Banking and Finance, 37(5), 1747–1758. https://doi.org/10.1016/j.jbankfin.2013.01.012

- Saunders, E. M. J. (1993). Stock prices and wall street weather. American Economic Review, 83(5), 1337–1345. https://www.jstor.org/stable/2117565

- Vikash, R., Pham, H. N. A., & Moosa, I. (2017). The sectoral effects of Brexit on the British economy: Early evidence from the reaction of the stock market. Applied Economics, 49(26), 2508–2514. https://doi.org/10.1080/00036846.2016.1240352