?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

This research article explores the mediating role of stock market indexes on the link between exchange rate variations and oil prices by utilizing unrestricted VAR. Previously mainstream research only explained the direct dynamism between the two variables. However, any transmission mechanism for explaining the transmission of shocks from oil prices toward the currency rates has been ignored. Therefore, we have utilized multiple traditional unit root testing procedures followed by a co-integration technique by Johansen (1988). We find that stock market indexes serve as a transmission channel between oil price variability and exchange rate during the pre and post financial recession. Moreover, the dynamic inverse association between the local currency depreciation and stock indices shows the bidirectional return spillover during the pre-contraction period. After the contraction period, the mediating role of stock market indexes is still evident but without the dynamic association between exchange rate and stock indexes. However, during the pre-recession, the transmission mechanism of shocks from the stock indices toward the exchange rate is triggered by oil price negative shocks, whereas after the crisis, the shocks from the stock indices towards the exchange rate are mainly due to positive oil price shocks. This research contributes to the mainstream literature by challenging the theoretical models about the direct dynamism between oil prices and currency and found the mediating role of stock market indexes by utilizing a portfolio balanced approach

1. Introduction

The local exchange rate against US dollars of several developing economies has suffered substantial devaluations as a result of the beginning of the international financial recession, like those of many developed economies (Ltaifa, Kaendera, & Dixit, Citation2009). A disruption in trade and investment inflows resulted in a considerable balance of payment gaps, therefore causing rapid exchange rate devaluation and increased currency instability starting in mid of 2008 (Asad et al., Citation2020; Jebabli et al., Citation2021; Makin, Citation2019; Park & Shin, Citation2020; Zhang & Hamori, Citation2021). The 2008 financial contagion has a wide range of depreciative effects on the currency rate, resulting in exchange rate losses of up to 40% for certain developing nations (Sheikh, Tabash et al., Citation2020). This influence was characterized by domestic and external causes (Sikarwar, Citation2018). The 2008 financial contagion has not only devaluated the local currencies of many developing economies but has also induced impulsiveness in developing and advanced economies’ global oil prices and stock indices (Cheung et al., Citation2019).

The crude oil market was also substantially affected by the international financial recession of 2008. The breakdown of US house prices, in particular, has contributed to the slump in the market for commodities, and particularly the international oil market was significantly fluctuating around 2008. Since the financialization of the commodity market in 2000, the price of crude oil which represents about 50 percent of the total commodity index, rose rapidly after the international financial recession. In particular, West Texas Intermediate prices (WTI) quickly increased before the global financial recession of 2008, from 52.51 USD to145.31 USD a barrel, by over 287 percent. But as of 2008, oil prices have decreased by almost 80 percent to 30.28 US$ a barrel (Cheung et al., Citation2019). Building upon the efficient market hypothesis, it can be reasonably assumed that oil prices may be directly proportional to the stock market indices (SI; Othman et al., Citation2019; Wickremasinghe, Citation2011) and according to the portfolio balanced approach, exchange rate (ER) returns can be impacted by the bullish and bearish effect in the stock market. Therefore, stock indexes may serve as a transmission channel between oil price (OP) shocks and currency fluctuations. This motivates the researchers to investigate the mediating role of stock indexes in-between currency rate variabilities and oil price returns and how the GFC impacted this mediation of stock market indexes and dynamism between the ER, OP, and SI.

The traditional or flow-oriented approach explained that the exchange rate impulsiveness can cause variability in the stock market indexes (Reddy & Sebastin, Citation2008). The depreciative trend in the domestic currency rate against the US dollar can increase the cost-effectiveness of the exporters by reducing their expenses and by increasing their revenues. However, local currency depreciation can have a detrimental impact on the importers because local currency depreciation against the US dollar can increase the expenses of the local importers and thereby decreasing their revenues (Alami, Citation2001; Lewis, Citation1988). According to the portfolio balanced approach, stock market appreciation can have an appreciative impact on the local exchange rate by attracting foreign exchange revenues and by creating a demand for investment in the local stock market indexes (Abdullah et al., Citation2018; Andriansyah & Messinis, Citation2019; Arif et al., Citation2014). If the local stock market indices rise, this might entice overseas investors to invest domestically, increasing capital inflows into the economy (Sheikh, Sheikh, Asad et al., Citation2020). The value of local stocks may increase as a result of the stock index’s growth, allowing local investors to recoup their overseas investments. This is due to the abrupt increase in perceived value of assets in the local stock market. The local exchange rate gains value relative to the US dollar as a result of the local stock market’s appreciation as well as the increased demand for local currency.

Several researchers have found a significant association between oil prices and stock market indices in the already published mainstream research articles. According to the theoretical underpinnings presented by Amano and Van Norden (Citation1998), Basher et al. (Citation2016), Fratzscher et al. (Citation2014), and Habib et al. (Citation2016), the positive terms of the trade shock increased the prices of the non-tradeable goods in the oil-exporting country and this appreciative impact has again resulted into the exchange rate appreciation. On the other side, a positive term of the trade shock decreases the prices of the non-tradeable goods in the oil-consuming economy, and oil price appreciation can have a depreciative impact on the local currency of the oil-importing economy. But according to the arbitrage pricing theory and efficient market hypothesis, the fluctuating oil prices can yield a significant impact on the stock indexes. Therefore, there is a possibility that stock market indexes can act as a mediating variable between the oil prices (OP) and domestic currency rate (ER) unpredictability. In the existing literature, a number of researchers have focused on the direct linkages between the exchange rate fluctuations and oil prices but ignored the role of stock market indexes in mediating the relationship between both variables. The 2008 financial contagion has not only affected the stock indices of developed economies, but has also depreciated the stock market indexes (SI) from 15,000 index points to only 4900 index points in Pakistan. Therefore, it is also important to analyze whether the economic recessionary regime has affected the mediating role of stock indices in between the currency rate fluctuations and oil price. Secondly, it is also pertinent to analyze how to post-economic contraction period changes the dynamic nexus between the OP-SI and ER-SI.

Amongst the already published mainstream research articles, most of the researchers have examined the association between exchange rate fluctuations and oil price variability (Huang et al., Citation2020; Jain & Biswal, Citation2016; Jung et al., Citation2020; Roubaud & Arouri, Citation2018; Suliman & Abid, Citation2020). However, there is no evident consistency in the terms of their findings. Firstly, most researchers have found that oil price and exchange rates returns are directly proportional to each other (Delgado et al., Citation2018; Jain & Biswal, Citation2016), whereas others reported an inverse association between both (Bai & Koong, Citation2018; Singhal et al., Citation2019). Previous Researches are unable to determine the exact cause of the relationship between these two significant stock market return factors. Additionally, little attempts have been made to assess if stock market indexes may act as a mediator between the exchange rate and oil prices, despite the fact that most research publications have noted the direct dynamism between the two variables (Albulescu & Ajmi, Citation2021; Nouira et al., Citation2019). Secondly, little attempt has been made to comprehend how the economic downturn has altered the dynamic relationship between non-macroeconomic fundamentals, such as oil prices and stock market indices, and macroeconomic fundamentals, such as the exchange rate.

There are three direct ways through which we can be able to explain the impact of oil price variability on exchange rate fluctuations (Ji et al., Citation2020; Suliman & Abid, Citation2020). The term trade channel is mainly utilized to understand the transmission mechanism of oil prices towards the exchange rate fluctuations (see, Amano & Van Norden, Citation1998; Basher et al., Citation2016; Fratzscher et al., Citation2014; Habib et al., Citation2016). According to the “terms of trade transmission approach” depreciation in the oil prices in the oil-producing economies causes the prices of the non-trading goods to depreciate in the domestic country and thereby driving down the real exchange rate (Amano & Van Norden, Citation1998; Basher et al., Citation2016). The real exchange rate is characterized as the relative price of tradable and non-tradeable goods between the local and international economies. Conversely, in the case of positive terms of trade shock (appreciation in oil prices of the oil-producing economies), the price of non-tradable goods increases and leads to the appreciation of the real exchange rate (Huang et al., Citation2020). Because of the appreciation in the demand for goods, profits, and wages of the preeminence sector of the economy, the prices and the demand for the non-tradeable goods increase which in turn appreciates the real exchange rate in the economy (Basher et al., Citation2016; Fratzscher et al., Citation2014; Habib et al., Citation2016). However, in the case of oil-importing economies, positive oil price shocks lead to the local currency depreciation against the international US dollars (Fratzscher et al., Citation2014). To understand the impact of oil price fluctuations on the exchange rate returns, the wealth and the portfolio channel are also utilized.

By evaluating portfolio decisions and the current account imbalances, the theoretical frameworks presented by Golub (Citation1983) and Krugman (Citation1980) are responsible for the link between oil price returns and currency rate variations. Nevertheless, both frameworks presuppose that there are 3 main economic zones in the global economy: Organization for petroleum exporting economies, the United States, and the Euro Zone (one export-oriented and two import-oriented economies, respectively). An appreciative impact on the oil prices leads to a shift of capital from the oil-consuming to the oil-producing economies. A rise in crude oil prices results in an appreciation in productivity and real wages. These consequences contribute to a rise in the relative prices of service products by equalizing real wages among sectors by moving workers and by increasing oil-sector revenues. Although the real exchange rate is growing, however, the competitiveness in the economy is worsening and long-term economic development is being influenced negatively. Two portfolio-related factors determine the shorter and medium-term influence of the US dollar compared to oil exporters’ currencies. The first is the US’ dependency on the imports of oil compared with the percentage of US exports to the oil-producing economies (Golub, Citation1983; Krugman, Citation1980). The other is the relative preferences of oil exporters for US dollar assets.

2. Literature review: Impact of oil price variability on the exchange rate fluctuations and the mediating role of stock market indices

Lin and Su (Citation2020) investigated the oil-currency nexus by utilizing high-frequency daily data in the BRICS context. Authors have utilized symmetrical ARDL and VAR methodological approaches and found that oil prices impacted the currency rates of oil-producing and importing economies differently. Furthermore, it is also revealed that the impact of oil prices on the currency rates is connected with the type of oil price shocks, oil-importing or exporting economy, and the frequency of data. Oil prices significantly impacted the exchange rate only at higher frequencies but this impact is far more insignificant for China only. Similarly, Olayeni et al. (Citation2020) also explored the dynamic linkages between the oil price variability and domestic currency rate impulsiveness and found that both symmetrical and asymmetrical estimation techniques complement each other in finding the dynamic linkages between the oil and exchange rates. Wen et al. (Citation2020) utilized granger causality and MVMQ-CAViar (1,1) modeling approach to find the spillover of risk between exchange rate and oil price impulsiveness by using daily frequency data from 2000 towards 2018. Results have indicated a strong spillover of risk from currency rate fluctuations of the major oil-producing and importing economies as compared with the risk spillover from oil prices towards the exchange rate.

Khraief et al. (Citation2021) investigated the non-linear impact of oil prices on the exchange rate fluctuations by utilizing the NARDL modeling approach in the domain of emerging economies like China and India. The maximum overlap wavelet approach is utilized to transform the exchange rate and oil prices into non-noisy variables. The exchange rate and oil prices can both exhibit noisy characteristics. Therefore, to remove the element of noisiness from both the variables and for more coherent non-linear detection in the oil-exchange rate nexus, the authors have transformed the two variables into partial sums and then utilized the NARDL approach. Results showed that the non-linearity in the relationship between oil prices and the exchange rate started to reflect the linear distributional behavior for the Indian context in the longer horizons as a result of the modifications. Jain and Biswal (Citation2016) investigated the influence of oil prices on the currency rate fluctuations and Indian stock market indices by utilizing a dynamic conditional correlational GARCH modeling framework and found that oil price declination leads to the depreciation of the local currency. Delgado et al. (2018) utilized an unrestricted VAR modeling framework and found that positive changes in the international oil prices cause an appreciative impact on the exchange rate by using data from 1992 to 2017.

Roubaud and Arouri (Citation2018) utilized Markov switching VAR methodology and found that the relationship exhibited regime dependency characteristics between oil prices and exchange rates changes. Moreover, the relationship between the variables is non-linear as well as became stronger due to the occurrence of a stronger incidence of volatility. In the Mexican context, Singhal et al. (Citation2019) have utilized a symmetrical ARDL framework and found an inverse association between the oil price instability and exchange rate. Kumar (Citation2019) utilized the non-linear ARDL and granger causality approach and found the existence of non-linearity between the relationship of exchange rate and oil prices, as positive and negative shocks in oil prices contrarily impacted the exchange rate. However, non-linearity is determined by the fact that positive shocks in the oil prices have a more profound effect on the exchange rate than the negative shock. Malik and Umar (Citation2019) divided the oil price shocks into different categories and found the impact of oil price shocks arising due to the risk and supply shocks in the currency rate variations. Results have revealed that there is a contributing role of oil price shocks due to the risk and demand shocks on the currency rate. But oil price shocks arising due to the supply shocks didn’t contribute towards the variability in currency rate by utilizing higher frequency data from 1996 towards 2019.

Jiang et al. (Citation2020) determined whether the influence of oil price shocks on the currency rate fluctuations of emerging as well as developed economies are different at various quantiles of the oil prices. Results have found the non-linear impact of oil price impulsiveness on the currency rate variations and the impact of oil prices on the currency rate are different under multiple quantiles of the oil price fluctuations. Several other studies have also explored the linkages between oil prices and exchange rate such as Huang et al. (Citation2020), Jain and Biswal (Citation2016). However, these studies have not examined the transmission channel of stock market indexes in between the exchange rate fluctuations and oil prices and whether the GFC influences that transmission channel and dynamism between the variables

3. Data

This study incorporates the monthly data for the exchange rate fluctuations, stock market indices, and international oil prices from January 2003 towards January 2019. Exchange rate fluctuations are represented by the fluctuations in the local currency of Pakistan against international US dollars. Pakistan Stock market indexes are represented by KSE-100 index (100 top-performing companies registered on the Karachi stock exchange with the highest market capitalization than all other registered companies on the Pakistan stock exchange). Oil price fluctuations are represented by West Texas Intermediate (WTI) international crude oil prices per barrel in US $. To explain the dynamism between oil price fluctuations and exchange rate variations, a number of the research articles have utilized the same measures of oil price fluctuations and currency rate variations (see, Basher et al., Citation2016; Jain & Biswal, Citation2016; Jung et al., Citation2020; Kumar, Citation2019; Lin & Su, Citation2020; Malik & Umar, Citation2019; Sheikh, Asad et al., Citation2020; Suliman & Abid, Citation2020). Monthly level data is divided into three-time frames: the period that occurred during the pre-2008 economic contagion, the period after an economic contagion, and the overall time frame. The period before the crisis consisted of 63 observations from Jan 2003 to Dec 2007, and the time frame after the crisis comprised 99 observations from Dec 2009 towards Jan 2019. The overall period covers the period from January 2003 to January 2019 and consisted of 168 total observations. This division of sampling duration before and after the crisis is in line with (Sheikh, Tabash et al., Citation2020).

4. Research methodology

VAR methodology is applied after the estimation of unit root analysis such as Philips Peron PP test by (PHILLIPS & PERRON, Citation1988), Kwiatkowski Philips Schmidt Shin KPSS test statistics by (Kwiatkowski et al., Citation1992) and augmented dickey fuller ADF test by (Dickey & Fuller, Citation1981). These test determined that whether all the variables are integrated at the same order or not. For the VAR method, exchange rate fluctuations, stock market indices and oil prices should exhibit non-stationary characteristics after taking first difference. Zivot Andrew unit root test is also utilized in order to estimate the unit root properties of the variables in the presence of structural breaks (Zivot & Andrews, Citation1992). Traditional unit root test only provides robust, coherent and legitimate results about the stationary properties of the variables in the absence of structure breaks. Decision to implement between the Unrestricted VAR and Restricted VAR is dependent upon the estimated results from Johannsson co-integration analysis (Neveen, Citation2018; Rajesh, 2019). In case of long-run co-integration between the variables, traditional unrestricted VAR model should not be applied (Camilleri et al., Citation2019) and restricted VAR or VECM or Error correction method (ECM) must be applied.

After the estimation of the stationary characteristics of the variables, we have calculated the appropriate lag length criteria. Model with the lowest AIC values will be selected (Abdullah et al., Citation2018). On the other hand, in the presence of structural breaks, the estimated model may exhibit instability and may provide spurious results (Akbar et al., Citation2019; U.A. Sheikh et al., Citation2020; Wei et al., Citation2019). Therefore, we have also utilized Bai- Peron method of the identification of multiple structural breaks within the data series (Olaleke et al., Citation2019a). In order to estimate the transmission mechanism in between the two endogenous variables, for example, exchange rate fluctuations and oil price variability, optimal lag length criteria are determined by estimating the unrestricted VAR modelling approach for the following endogenous variables and simultaneous system of equations can be created.

In the first phase, building upon the efficient market hypothesis, we investigate the impact of oil price fluctuations on the stock market indexes of Pakistan. From the equation no 1, the statistical significance of () determines the influence of OP changes on the Karachi stock indices

. However, in order to establish the transmission mechanism, direct relationship between the oil prices

and exchange rate (

should be statistically insignificant (see, EquationEquation.2)

(2)

(2) . Therefore, following the same procedure, we can test whether there is any influence of stock indexes

on the currency rate

through Equation.no 2. Moreover, in case of insignificant direct impact of OP on the ER (see, EquationEquation.2

(2)

(2) ), but with a direct significant impact of OP on the SI (see, EquationEquation.1

(1)

(1) ), the stock market indexes (SI) may lead towards the fluctuations in exchange rate (see, EquationEquation.2)

(2)

(2) . Therefore, we may conclude that there is a transmission mechanism between oil prices and stock indexes, which then transmits from stock indexes towards exchange rates. We can re-write the above EquationEquation.1

(1)

(1) and EquationEquation.2

(2)

(2) , as EquationEquation.3

(3)

(3) , EquationEquation.4

(4)

(4) , respectively. “k” is the lag orders of independent variables and

are represented as Short run coefficient.

is designated as error term. Dependent variables are represented as lnSI, lnER and lnOP, whereas inclusion of regressand in the EquationEquation1

(1)

(1) , EquationEquation2

(2)

(2) , EquationEquation3

(3)

(3) with one period prior prices, i.e.

,

and

makes the Equationuation autoregressive or dynamic, respectively.

5. Results

The results section is divided into the following 5 sections. The first section explains the descriptive statistics about the variables of interest. Sections 2 and 3 explain the result of unit root estimation, appropriate lag length criteria, and long-run co-integration analysis by Johansen Julius (JJ), respectively. Section no 4 describes the estimated output from multiple structural break point tests purposed by Bai- Peron and VAR model results. Section no 5 is about residual diagnostics.

According to the results reported in Table , the skewness of exchange rate returns is greater during the post-economic contagion as compared with the pre-economic contagion. However, the negative skewness of stock market returns is greater during the pre-crisis sample period when compared with post-crisis and overall sample period. Positive skewness showed that the right tail of the distribution graph was longer than the left, indicating that the left side of the graph is where more values are concentrated. Moreover, high positive (negative) skewness also exhibited the presence of larger positive (negative) values in the data series of exchange rate (stock indices) during the post-economic (pre-economic) contagion than the pre-economic (post economic) contagion. This means that local currency appreciation against the US dollar was more intensive during the post-contagion period as compared with pre-economic contagion time. However, during the pre-crisis regime, oil price movements exhibited greater negative skewness when compared with post-crisis and overall sample period. Negative skewness is an indication of more negative values in the data series and clustering of values towards the right side of the distribution graph.

Table 1. Descriptive statistics

Higher kurtosis values for stock market and commodity market returns are generally because of the leptokurtic distribution of the data during the pre-crisis period. During the post-crisis regime, the excess kurtosis for exchange rate exhibits the peakedness of the curve of the distribution graph. Higher kurtosis values of stock and oil price returns during the pre-financial recession regime also resemble the presence of extreme values. The leptokurtic distribution is ideal for most risk taking investors because of the presence of extreme financial risk or volatility during the pre-crisis period. Therefore, the chances of earning higher profitability also increases exponentially. This means that the behavior of both the series such as exchange rate fluctuations and oil prices is different during the pre-crisis and post-crisis period. This has motivated the researchers to reconnoiter the dynamic association between the oil and exchange rate fluctuations and the role of stock market indexes as a transmission channel in between both the variables during 2 different sample settings

Table reports that the coefficient of variation (CoV) of stock market returns and oil returns is higher during the pre-economic contagion timeframe as a contrast with the post-contagion timeframe. Greater values of COV explain the higher incidence of volatility in both the series during the time frame of the pre-recessionary regime. This also shows the volatile behavior of the oil prices and stock market returns during the pre-recession period as compared with post-crisis period. The results reported in Table illustrates that all the variables are non-stationary at level but after taking the first difference, they all display stationary characteristics. All variables are I (1). However, we have also estimated the unit root test by Zivot and Andrews (Citation1992) because of the occurrence of structural breaks in the series. In the occurrence of structural breaks, traditional unit root tests yield spurious outcomes (Tehreem, Citation2018).

Table 2. Coefficient of Variation (CoV)

Table 3. Augmented dickey fuller (ADF) unit root test for three regimes

Table 4. Philips peron unit root test for three regimes

Table 5. KPSS unit root test for three regimes

Table 6. Zivot Andrew (ZA) Unit root test for three regimes

According to the table , Zivot Andrew unit root absolute t-statistics is higher than critical values at 1st difference, which indicates that we can reject the null hypothesis of non-stationarity. According to all unit root testing procedure, all the variables are integrated at the same order. However, Zivot Andrew unit root test indicates the presence of structural break in 2008. We have also included a dummy variable for the stability of the VAR model and to account for the structural breaks.

After detecting the order of integration of the variables and the optimal lag length criteria (see table ), the next step involve is the estimation of Johansson co-integration test. Table reports that there is no long-run co-integrating association between exchange rate, oil prices and stock market indexes. In the absence of long-run co-integration and due to the presence of same order of integration for all the variables, we can estimate unrestricted VAR (Camilleri et al., Citation2019) for detecting the transmission of mechanism of shocks from oil prices towards the currency rate variations.

Table 7. Optimal Lag length criteria

Table 8. Unrestricted Co-Integration Rank test (Trace)

In the first phase, an unrestricted VAR modeling approach is used to determine the direct impact of oil prices on the stock market indexes for three dissimilar time frames, including pre-economic contagion, post-economic contagion, and the entire time frame. The theoretical rationale of efficient market hypothesis (see, Hatemi-J, Citation2012; Othman et al., Citation2019) is utilized for the direct impact of OP on the SI. The unrestricted VAR modeling approach is once more used for the second phase and to estimate the impact of stock market indexes on currency rate variations by using a portfolio balanced approach as an underlying theory (Andriansyah & Messinis, Citation2019). Moreover, during the second phase, the direct impact of oil prices on the domestic exchange rate is also examined. International oil price shocks may not have a direct effect on the exchange rate, but they may nevertheless have a major influence on stock market indexes, which might then have an impact on the exchange rate. In that situation, the stock market indexes serve as a mediator between changes in the exchange rate and oil prices.

According to the table , an increase one-month prior international oil prices have a negative impact on the stock market indexes during the pre-financial recessionary region. These results are in line with (Kumar, Citation2019, Citation2019; You et al., Citation2017). However, the two-month lag period of oil prices positively affects the stock market indexes during the post-economic recessionary period and overall sample period. This shows that the inverse impact of international oil price shocks on the stock market indexes is regime-dependent and shareholders reacted positively to oil price fluctuations after the occurrence of the global financial recession. Building upon the semi-strong form of efficient market hypothesis, all the public level information is already internalized in the stock prices and investors cannot be able to earn greater than the market average based on public information (Othman et al., Citation2019) The negative impact of public information on the stock market indexes means that share prices can be forecasted based on exogenous news and this indicates that the Pakistan stock market is not efficient.

Table 9. Unrestricted Vector Auto regression modelling results: Dependent variable: Stock Indexes

Another possibility of negative impact of oil price on the stock market indexes is the increase in producer prices of most of the products in Pakistan and because of increase in inflation, stock market indexes decreases (Abbas et al., Citation2017; Areli Bermudez Delgado et al., Citation2018; Arfaoui & Ben Rejeb, Citation2017; Pandey et al., Citation2018; Roubaud & Arouri, Citation2018; Salisu & Isah, Citation2017; Wei et al., Citation2019). Another possibility is that appreciation in oil prices may also cause economic instability in Pakistan and which is again reflected by the stock market of a developing economy (You et al., Citation2017). Appreciation in international oil prices also increases the cost of doing business, increase in prices of gasoline-related products, and restrains the overall growth of the economy (You et al., Citation2017). However, there is no adverse impact of oil prices on the stock market indexes during the post-recessionary and overall sample period. Kocaarslan and Soytas (Citation2019) also suggested the positive impact of oil prices on the stock market indices may be due to the increase in demand for oil. Moreover, the positive impact of oil prices during the post-economic contraction regime is due to the indication of economic expansion, industrial production, and overall economic outlook. Therefore, after the recession, investors may have reacted positively to oil price shocks. Oil price positive shocks also cause the local currency depreciation, which is again favorable for export-oriented economies, and shareholders may react positively to oil price increases because of good future economic perspectives associated with Pakistani exporters. Table also shows that local currency depreciation adversely affected the stock market indices during the pre-economic crunch of 2008. However, an inverse association between local currency declination and stock market indices is absent during the post-economic contraction regime. This further purposes practical implications for shorter-term investors to consider the currency fluctuations under different but specific regimes while strategizing investment options.

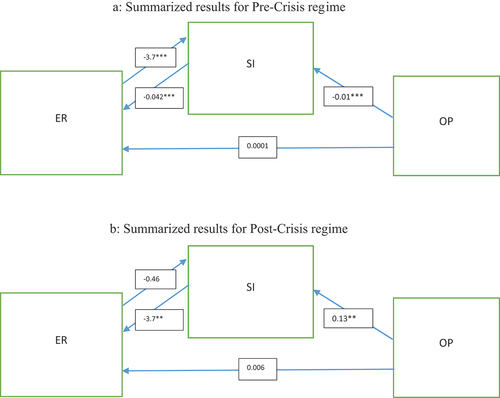

According to the results reported in Tables , stock market indexes played an important role of mediation in between the oil price and exchange rate fluctuations for both the regimes: pre and post-economic recessionary regimes. Building upon the efficient market hypothesis, findings suggested the negative impact of one month prior prices of oil on the stock market indexes (see, Table ) and in return, stock price appreciation formulated a negative association with local currency depreciation (USD/PKR upward movement) during the pre-2008 crisis. Because of the negative impact of oil prices, stock market indexes are inversely associated with exchange rate depreciation (see Table ). This means that with a one-percent increase in the stock market index with one month and two-month lag period, USD/PKR (local currency depreciation) decreases by 0.006% and 0.042 %, respectively (see table ). However, the direct impact of oil prices on the exchange rate is found to be statistically insignificant during the pre-crisis regime (see, Table ). This shows that—ve shocks from the international oil prices are transmitting towards the exchange rate fluctuations by using stock market indexes as a transmission mechanism only during the pre-crisis regime. These results are in contrast with the number of recently published researches because these studies have only explored the direct dynamism between the exchange rate and oil prices (Bai & Koong, Citation2018; Basher et al., Citation2016; Chkir et al., Citation2020, Citation2020; Fratzscher et al., Citation2014; Ingalhalli et al., Citation2016; Jain & Biswal, Citation2016; Jung et al., Citation2020; Khraief et al., Citation2021; Kumar, Citation2019; Wen et al., Citation2020). This is the first study that has explored the role of stock market indexes as a mediator between both. According to the portfolio balanced approach, appreciation in local stock market indexes attracts international investments (FDI) within the country and thereby increases the demand for local currency (Reddy & Sebastin, Citation2008). However, because of the increase in local stock market indexes, local investors are also willing to invest in local stock market indexes by selling their foreign assets (Andriansyah & Messinis, Citation2019; Arif et al., Citation2014).

Table 10. Unrestricted Vector Auto regression modelling results: Dependent variable: Exchange rate

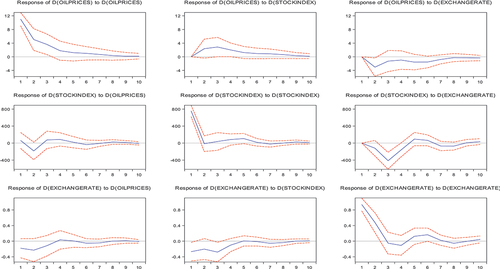

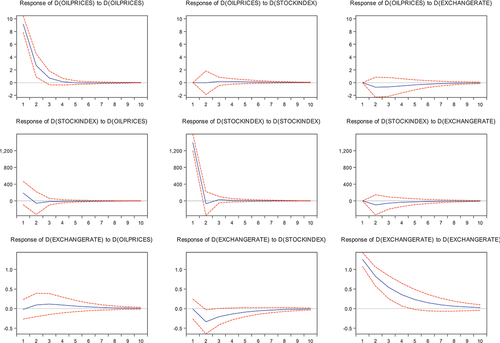

Similarly, during the post-economic contraction period, positive shocks in oil prices lead to appreciation in the stock market indices and this appreciation also leads to local currency appreciation. During the post-economic recessionary regime, the dynamic association between the exchange rate and stock market indices is not evident. On the contrary, the exchange rate and stock market formulated a dynamic nexus during the pre-economic recession. This shows that the global financial crisis has not only affected the dynamism between SI and ER but also affect the reaction of investors toward the oil price shocks. During the pre-2008 recession, investors reacted adversely to oil price shocks and these OP shocks lead to the appreciation in local currency by utilizing SI as a transmission channel. However, after the 2008 economic recession, investors reacted positively to OP positive shocks due to the symbolization of economic expansion and increased industrial output. These positive shocks lead towards the appreciation in stock market indices. Therefore, positive stock market indices also appreciate the local exchange rates. The impluse reponse fundtion during Pre-Crisis and Post Crisis period can be seen in , respectively. Whereas, explains the symmerised results of the tranmission of shocks from oil prices towards the exchange rate.

Figure 1. Impulse response function for pre-crisis period.

Figure 2. Impulse response function after crisis.

Figure 3. Mediating role of stock market indices between exchange rate and oil price retunes. a) Summarized results for Pre-Crisis regime, b) Summarized results for Post-Crisis regime.

6. Conclusion, practical implications and future research direction

The purpose of this research article is to investigate the mediating role of stock market indexes in between the exchange rate fluctuations and oil prices during multiple regimes. In the existing literature, researchers have only investigated the direct dynamism between the oil price shocks and exchange rate and ignored the important transmission mechanism of shocks from the oil prices towards the exchange rate. We have utilized multiple unit root testing procedures followed by the Johannsson co-integration test and lag selection criteria on the basis of the lowest AIC, HQ, and SIC and Unrestricted Vector autoregression modeling framework (VAR) for multiple regimes. Furthermore, this research also explores the role of the economic recessionary period in affecting the dynamism between ER-SI-OP and whether the economic crunch of 2008 affected the mediation of stock market indices between the OP and ER. Results rejected the taken-for-granted assumption of a direct association between oil price and exchange rate fluctuation but this association is mediated by stock market indices. However, the nature of shocks from oil prices towards the stock market indices and the dynamic association between exchange rate and stock market indices is typically different in both the regimes: Pre-financial contraction period and post-financial contraction.

During the pre-2008 economic crunch, negative oil price shocks cause the exchange rate fluctuations by using the stock market indexes as a mediating variable. Furthermore, an inverse association is also established between the stock market decline and local currency appreciation. Before the economic recession, a positive shock to the depreciation in the Pakistani currency caused the stock prices to decline and the stock market decline yields a negative effect on currency devaluation. However, after the economic recession, this dynamic association between the currency-stock market is not evident and only positive shocks in stock prices negatively impacted the local currency devaluations. Furthermore, during the post-recessionary period, oil price positive shocks formulate an indirect association with currency fluctuations by utilizing the stock market indices as a “transmission channel”. This shows that during a turbulent free environment like the pre-2008 financial recession, investors should focus on the oil price negative shocks as these shocks yield an appreciative influence on the KSE-100 index. However, after the recovery from the crisis, investors should consider positive shocks in oil prices as more value relevant for profit maximization. Therefore, the association between oil price and stock indices is regime-dependent and investors may respond differently to oil price shocks under different regimes. Short-term forex traders should put much emphasis on the transmission of shocks from oil prices towards the stock market fluctuations because of the mediating role of stock prices in effecting local currency devaluation. Moreover, exporters and importers must also consider the fluctuations in the stock market before making purchase decisions, as positive shocks in the stock market lead to local currency appreciation. Local currency appreciation may increase the profits margins for exporting businesses but adverse impacts can be seen for import-oriented firms. These practical implications are still helpful for Pakistani investors and exporters as inflation inducted due to the Covid-19 crisis may also give rise to another financial crisis similar to that of 2008.

The context of our research is currently restricted to a single developing economy, future researchers can focus on the whole region like the South Asian region for analyzing the mediating role of stock market indexes in between the exchange rate and oil prices. By examining the role of SI as an oil price shock absorber throughout three different regimes, the panel-based VAR and panel-based VECM modelling framework can also be used to identify the indirect transmission of shocks from the oil prices towards exchange rate variations.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

Notes on contributors

Mosab I Tabash

Mosab I Tabash is acting as Director of the MBA program at Al Ain University, UAE. He is also the author of various number of impact factor publications in well-known journals

Muzaffar Asad

Muzaffar Asad is working as an Assistant Professor at the College of Commerce and Business Administration, Dhofar University, Oman. He completes his Ph.D. in Entrepreneurial Finance and has supervised several research projects in the field of entrepreneurship, finance, and business management

Ather Azim Khan

Ather Azim Khan is a well-known professor of finance and currently working as a Dean of faculty of management and administrative sciences at University of Sialkot. Previously, he has performed many administrative and teaching responsibilities as a dean of faculty of management studies at UCP.

Umaid A Sheikh

Umaid A Sheikh has also published previously in Journals indexed in Scopus, Web of Science Core Collection and Australian Business Dean Council. He has completed several academic degrees including Master of Philosophy in Finance with 87% overall aggregate average and taught at M.Phil. level. His research interest includes Financial Economics, financial time series and Panel data modelling.

References

- Abbas, G., McMillan, D. G., & Wang, S. (2017). Conditional volatility nexus between stock markets and macroeconomic variables: Empirical evidence of G-7 countries. Journal of Economic Studies, 45(1), 77–19. https://doi.org/10.1108/JES-03-2017-0062

- Abdullah, O. A. H., Aziz, H. A., & Kassim, S. (2018). Identification of macroeconomic determinants for diversification and investment strategy for Islamic unit trust funds in Malaysia. International Journal of Emerging Markets, 13(4), 653–675. https://doi.org/10.1108/IJoEM-03-2017-0074

- Akbar, M., Iqbal, F., & Noor, F. (2019). Bayesian analysis of dynamic linkages among gold price, stock prices, exchange rate and interest rate in Pakistan. Resources Policy, 62, 154–164. https://doi.org/10.1016/j.resourpol.2019.03.003

- Alami, T. H. (2001). Currency substitution versus dollarization: A portfolio balance model. Journal of Policy Modeling, 23(4), 473–479. https://doi.org/10.1016/S0161-8938(01)00063-1

- Albulescu, C. T., & Ajmi, A. N. (2021). Oil price and US dollar exchange rate: Change detection of bi-directional causal impact. Energy Economics, 100, 105385. https://doi.org/10.1016/j.eneco.2021.105385

- Amano, R. A., & Van Norden, S. (1998). Exchange rates and oil prices. Review of International Economics, 6(4), 683–694. https://doi.org/10.1111/1467-9396.00136

- Andriansyah, A., & Messinis, G. (2019). Stock prices, exchange rates and portfolio equity flows: A Toda-yamamoto panel causality test. Journal of Economic Studies, 46(2), 399–421. https://doi.org/10.1108/JES-12-2017-0361

- Areli Bermudez Delgado, N., Bermudez Delgado, E., & Saucedo, E. (2018). The relationship between oil prices, the stock market and the exchange rate: Evidence from Mexico. The North American Journal of Economics and Finance, 45, 266–275. https://doi.org/10.1016/j.najef.2018.03.006

- Areli Bermudez Delgado, N., Bermudez Delgado, E., & Saucedo, E. (2018). The relationship between oil prices, the stock market and the exchange rate: Evidence from Mexico. The North American Journal of Economics and Finance, 45, 266–275. https://doi.org/10.1016/j.najef.2018.03.006

- Arfaoui, M., & Ben Rejeb, A. (2017). Oil, gold, US dollar and stock market interdependencies: A global analytical insight. European Journal of Management and Business Economics, 26(3), 278–293. https://doi.org/10.1108/EJMBE-10-2017-016

- Arif, B. D., Aasif, S., Niyati, B., & Amaresh, S. (2014). The relationship between stock prices and exchange rates in Asian markets: A wavelet based correlation and quantile regression approach. South Asian Journal of Global Business Research, 3(2), 209–224. https://doi.org/10.1108/SAJGBR-07-2013-0061

- Asad, M., Tabash, M. I., Sheikh, U. A., Al-Muhanadi, M. M., Ahmad, Z., & McMillan, D. (2020). Gold-oil-exchange rate volatility, Bombay stock exchange and global financial contagion 2008: Application of NARDL model with dynamic multipliers for evidences beyond symmetry. Cogent Business and Management, 7(1), 1849889. https://doi.org/10.1080/23311975.2020.1849889

- Badry, H. (2019). Can conventional energy be replaced by renewable energy without harming economic growth in non-oil-MENA? Evidence from Granger causality in VECM. World Journal of Entrepreneurship, Management and Sustainable Development, 15(2), 159–168. https://doi.org/10.1108/WJEMSD-11-2018-0098

- Bai, S., & Koong, K. S. (2018). Oil prices, stock returns, and exchange rates: Empirical evidence from China and the United States. The North American Journal of Economics and Finance, 44, 12–33. https://doi.org/10.1016/j.najef.2017.10.013

- Basher, S., Haug, A., & Sadorsky, P. (2016). The impact of oil shocks on exchange rates: A Markov-switching approach. Energy Economics, 54(C), 11–23. https://doi.org/10.1016/j.eneco.2015.12.004

- Ben Ltaifa, N., Kaendera, S., & Dixit, S. V. S. (2009). Impact of the Global Financial Crisis on Exchange Rates and Policies in Sub-Saharan Africa. International Monetary Fund, 1- 25, 1. https://www.imf.org/en/Publications/departmental-papers/Issues/2022/06/06/Impact-of-the-Global-Financial-Crisis-on-Exchange-Rates-and-Policies-in-Sub-Saharan-Africa-23445

- Camilleri, S. J., Scicluna, N., & Bai, Y. (2019). Do stock markets lead or lag macroeconomic variables? Evidence from select European countries. The North American Journal of Economics and Finance, 48, 170–186. https://doi.org/10.1016/j.najef.2019.01.019

- Cheung, Y.-W., Fatum, R., & Yamamoto, Y. (2019). The exchange rate effects of macro news after the global Financial Crisis. Journal of International Money and Finance, 95, 424–443. https://doi.org/10.1016/j.jimonfin.2018.03.009

- Chkir, I., Guesmi, K., Brayek, A. B., & Naoui, K. (2020). Modelling the nonlinear relationship between oil prices, stock markets, and exchange rates in oil-exporting and oil-importing countries. Research in International Business and Finance, 54, 101274. https://doi.org/10.1016/j.ribaf.2020.101274

- Dickey, D. A., & Fuller, W. A. (1981). Likelihood ratio statistics for autoregressive time series with a unit root. Econometrica, 49(4), 1057–1072. https://doi.org/10.2307/1912517

- Fratzscher, M., Schneider, D., & Robays, I. V. (2014). Oil prices, exchange rates and asset prices. Issue 1689, European Central Bank (ECB). http://hdl.handle.net/10419/154122

- Golub, S. (1983). Oil prices and exchange rates. Economic Journal, 93(371), 576–593. https://doi.org/10.2307/2232396

- Habib, M. M., Bützer, S., & Stracca, L. (2016). Global exchange rate configurations: Do oil shocks matter? IMF Economic Review, 64(3), 443–470. https://doi.org/10.1057/imfer.2016.9

- Hatemi-J, A. (2012). Asymmetric causality tests with an application. Empirical Economics, 43(1), 447–456. https://doi.org/10.1007/s00181-011-0484-x

- Huang, B.-N., Lee, -C.-C., Chang, Y.-F., & Lee, -C.-C. (2020). Dynamic linkage between oil prices and exchange rates: New global evidence. Empirical Economics, 60(1), 487–512. https://doi.org/10.1007/s00181-020-01979-0

- Ingalhalli, V., G, P. B., & Reddy, Y. V. (2016). A study on dynamic relationship between oil, gold, forex and stock markets in indian context. Paradigm, 20(1), 83–91. https://doi.org/10.1177/0971890716637706

- Jain, A., & Biswal, P. C. (2016). Dynamic linkages among oil price, gold price, exchange rate, and stock market in India. Resources Policy, 49, 179–185. https://doi.org/10.1016/j.resourpol.2016.06.001

- Jebabli, I., Kouaissah, N., & Aroudri, M. (2021). Volatility spillovers between stock and energy markets during Crises: A comparative assessment between the 2008 global financial crisis and the covid-19 pandemic crisis. Finance Research Letters, 102363. https://doi.org/10.1016/j.frl.2021.102363

- Jiang, Y., Feng, Q., Mo, B., & Nie, H. (2020). Visiting the effects of oil price shocks on exchange rates: Quantile-on-quantile and causality-in-quantiles approaches. The North American Journal of Economics and Finance, 52, 101161. https://doi.org/10.1016/j.najef.2020.101161

- Ji, Q., Shahzad, S. J. H., Bouri, E., & Suleman, M. T. (2020). Dynamic structural impacts of oil shocks on exchange rates: Lessons to learn. Journal of Economic Structures, 9(1), 20. https://doi.org/10.1186/s40008-020-00194-5

- Jung, Y. C., Das, A., & McFarlane, A. (2020). The asymmetric relationship between the oil price and the US-Canada exchange rate. The Quarterly Review of Economics and Finance, 76, 198–206. https://doi.org/10.1016/j.qref.2019.06.003

- Khraief, N., Shahbaz, M., Mahalik, M. K., & Bhattacharya, M. (2021). Movements of oil prices and exchange rates in China and India: New evidence from wavelet-based, non-linear, autoregressive distributed lag estimations. Physica A: Statistical Mechanics and Its Applications, 563, 125423. https://doi.org/10.1016/j.physa.2020.125423

- Kocaarslan, B., & Soytas, U. (2019). Dynamic correlations between oil prices and the stock prices of clean energy and technology firms: The role of reserve currency (US dollar). Energy Economics, 84, 104502. https://doi.org/10.1016/j.eneco.2019.104502

- Krugman, P. (1980). Oil and the Dollar (NBER Working Papers, Issue 0554). National Bureau of Economic Research, Inc. https://econpapers.repec.org/RePEc:nbr:nberwo:0554

- Kumar, S. (2019). Asymmetric impact of oil prices on exchange rate and stock prices. The Quarterly Review of Economics and Finance, 72, 41–51. https://doi.org/10.1016/j.qref.2018.12.009

- Kwiatkowski, D., Phillips, P. C. B., Schmidt, P., & Shin, Y. (1992). Testing the null hypothesis of stationarity against the alternative of a unit root: How sure are we that economic time series have a unit root? Journal of Econometrics, 54(1), 159–178. https://doi.org/10.1016/0304-4076(92)90104-Y

- Lewis, K. K. (1988). Testing the portfolio balance model: A multi-lateral approach. Journal of International Economics, 24(1), 109–127. https://doi.org/10.1016/0022-1996(88)90024-4

- Lin, B., & Su, T. (2020). Does oil price have similar effects on the exchange rates of BRICS? International Review of Financial Analysis, 69, 101461. https://doi.org/10.1016/j.irfa.2020.101461

- Makin, A. J. (2019). Lessons for macroeconomic policy from the Global Financial Crisis. Economic Analysis and Policy, 64, 13–25. https://doi.org/10.1016/j.eap.2019.07.008

- Malik, F., & Umar, Z. (2019). Dynamic connectedness of oil price shocks and exchange rates. Energy Economics, 84, 104501. https://doi.org/10.1016/j.eneco.2019.104501

- Neveen, A. (2018). The effect of the financial crisis on the dynamic relation between foreign exchange and stock returns: Empirical evidence from MENA region. Journal of Economic Studies, 45(5), 994–1031. https://doi.org/10.1108/JES-10-2017-0308

- Nouira, R., Hadj Amor, T., & Rault, C. (2019). Oil price fluctuations and exchange rate dynamics in the MENA region: Evidence from non-causality-in-variance and asymmetric non-causality tests. The Quarterly Review of Economics and Finance, 73, 159–171. https://doi.org/10.1016/j.qref.2018.07.011

- Olaleke, F. I., Odudu, T. F., & Adekoya, O. (2019a). Oil and agricultural commodity prices in Nigeria: New evidence from asymmetry and structural breaks. International Journal of Energy Sector Management, 13(2), 377–401. https://doi.org/10.1108/IJESM-07-2018-0004

- Olayeni, O. R., Tiwari, A. K., & Wohar, M. E. (2020). Global economic activity, crude oil price and production, stock market behaviour and the Nigeria-US exchange rate. Energy Economics, 92, 104938. https://doi.org/10.1016/j.eneco.2020.104938

- Othman, A. H. A., Alhabshi, S. M., & Haron, R. (2019). The effect of symmetric and asymmetric information on volatility structure of crypto-currency markets: A case study of bitcoin currency. Journal of Financial Economic Policy, 11(3), 432–450. https://doi.org/10.1108/JFEP-10-2018-0147

- Pandey, V., & Vipul, V. (2018). Volatility spillover from crude oil and gold to BRICS equity markets. Journal of Economic Studies, 45(2), 426–440. https://doi.org/10.1108/JES-01-2017-0025

- Park, C.-Y., & Shin, K. (2020). Contagion through National and Regional Exposures to Foreign Banks during the Global Financial Crisis. Journal of Financial Stability, 46, 100721. https://doi.org/10.1016/j.jfs.2019.100721

- PHILLIPS, P. C. B., & PERRON, P. (1988). Testing for a unit root in time series regression. Biometrika, 75(2), 335–346. https://doi.org/10.1093/biomet/75.2.335

- Reddy, Y. V., & Sebastin, A. (2008). Interaction between forex and stock markets in India: An entropy approach. Vikalpa: The Journal for Decision Makers, 33(4), 27–46. https://doi.org/10.1177/0256090920080403

- Roubaud, D., & Arouri, M. (2018). Oil prices, exchange rates and stock markets under uncertainty and regime-switching. Finance Research Letters, 27, 28–33. https://doi.org/10.1016/j.frl.2018.02.032

- Salisu, A. A., & Isah, K. O. (2017). Revisiting the oil price and stock market nexus: A nonlinear Panel ARDL approach. Economic Modelling, 66, 258–271. https://doi.org/10.1016/j.econmod.2017.07.010

- Sheikh, U. A., Asad, M., Ahmed, Z., Mukhtar, U., & McMillan, D. (2020). Asymmetrical relationship between oil prices, gold prices, exchange rate, and stock prices during global financial crisis 2008: Evidence from Pakistan. Cogent Economics & Finance, 8(1), 1757802. https://doi.org/10.1080/23322039.2020.1757802

- Sheikh, U. A., Asad, M., Israr, A., Tabash, M. I., Ahmed, Z., & McMillan, D. (2020). Symmetrical cointegrating relationship between money supply, interest rates, consumer price index, terroristic disruptions, and Karachi stock exchange: Does global financial crisis matter? Cogent Economics and Finance, 8(1), 1838689. https://doi.org/10.1080/23322039.2020.1838689

- Sheikh, U. A., Tabash, M. I., Asad, M., & McMillan, D. (2020). Global financial crisis in effecting asymmetrical co-integration between exchange rate and stock indexes of South Asian region: Application of panel data nardl and ardl modelling approach with asymmetrical granger causility. Cogent Business & Management, 7(1), 1843309. https://doi.org/10.1080/23311975.2020.1843309

- Sikarwar, E. (2018). Exchange rate fluctuations and firm value: Impact of global financial crisis. Journal of Economic Studies, 45(6), 1145–1158. https://doi.org/10.1108/JES-02-2017-0048

- Singhal, S., Choudhary, S., & Biswal, P. C. (2019). Return and volatility linkages among International crude oil price, gold price, exchange rate and stock markets: Evidence from Mexico. Resources Policy, 60, 255–261. https://doi.org/10.1016/j.resourpol.2019.01.004

- Suliman, T. H. M., & Abid, M. (2020). The impacts of oil price on exchange rates: Evidence from Saudi Arabia. Energy Exploration & Exploitation, 38(5), 2037–2058. https://doi.org/10.1177/0144598720930424

- Tehreem, F. (2018). An aggregate and disaggregate energy consumption, industrial growth and CO2 emission: Fresh evidence from structural breaks and combined cointegration for China. International Journal of Energy Sector Management, 12(1), 130–150. https://doi.org/10.1108/IJESM-08-2017-0007

- Wei, Y., Qin, S., Li, X., Zhu, S., & Wei, G. (2019). Oil price fluctuation, stock market and macroeconomic fundamentals: Evidence from China before and after the financial crisis. Finance Research Letters, 30, 23–29. https://doi.org/10.1016/j.frl.2019.03.028

- Wen, D., Liu, L., Ma, C., & Wang, Y. (2020). Extreme risk spillovers between crude oil prices and the U.S. exchange rate: Evidence from oil-exporting and oil-importing countries. Energy, 212, 118740. https://doi.org/10.1016/j.energy.2020.118740

- Wickremasinghe, G. (2011). The Sri Lankan stock market and the macroeconomy: An empirical investigation. Studies in Economics and Finance, 28(3), 179–195. https://doi.org/10.1108/10867371111141954

- You, W., Guo, Y., Zhu, H., & Tang, Y. (2017). Oil price shocks, economic policy uncertainty and industry stock returns in China: Asymmetric effects with quantile regression. Energy Economics, 68, 1–18. https://doi.org/10.1016/j.eneco.2017.09.007

- Zhang, W., & Hamori, S. (2021). Crude oil market and stock markets during the COVID-19 pandemic: Evidence from the US, Japan, and Germany. International Review of Financial Analysis, 74, 101702. https://doi.org/10.1016/j.irfa.2021.101702

- Zivot, E., & Andrews, D. W. K. (1992). Further Evidence on the Great Crash, the Oil-Price Shock, and the Unit-Root Hypothesis. Journal of Business & Economic Statistics, 10(3), 251–270. https://doi.org/10.2307/1391541