Abstract

This study provides a critical review of the literature that examines and analyses how Fraud Prevention mediates the Effect of Internal Audit, Risk Management, Whistle Blowing System and Big Data Analytics on the Prevention of Financial Crime Behaviour. The problem discussed in this study is the limited strategic formulation in risk management, internal audit, whistleblowing system and big data analytics for early detection for fraud prevention and prevention of financial crime behavior in Indonesia, especially the problem of fraud that occurs in the Sumatra Regional Government, namely in Aceh, North Sumatra, Riau, Kepulauan Riau, South Sumatra, Bangka Belitung, Jambi, West Sumatra, Bengkulu and Lampung. Various kinds of scientific studies that have been carried out provide clues that the skills mismatch on the impact of fraud and financial crime behavior is still a fundamental polemic that will continue to hamper the productivity and competitiveness of various economic and industrial sectors in Regional Governments in Indonesia. To prepare for the emerging discourse, this research refers to 90 articles published in leading academic journals, discussing related topics from the early 1990s to 2021. Therefore, the formulation of the problem in this study: (1) How does Internal Audit influence prevention fraud, (2) How does Risk Management influence fraud prevention, (3) How does Whistleblowing system influence fraud prevention, (4) How big data analytics influence fraud prevention, (5) How fraud prevention mediates the influence of Internal Audit, Risk Management, whistleblowing system and big data analytics to prevent financial crime behavior.

PUBLIC INTEREST STATEMENT

Since 1990, there is a sizable accounting literature on the determinants of fraud prevention and financial crime behaviour.

Several functions within Regional Governments in Indonesia are not carried out obediently and consistently, which leads to unhealthy structural and managerial activities.

Hence, researchers recommend a combined variable approach, the internal audit, risk management, whistleblowing systems and big data analytics on both problems, as the initial determining factors through digital analysis and auditing skills to prevent them in facing dynamics change and development of digital native, intelligent mobility, healthy living arrangements, civil security, and technology in the workplace by regarding economic, socio-cultural challenges and state life aspects to build economic citizens generation affected by cases of them.

This paper output provides a comprehensive understanding of responsibilities for financial statement fraud control in the context of the above theories and contributes recommendations for improvement in financial statement fraud control in public interest entities.

1. Introduction

This study reviews and synthesizes the literature on “Fraud Prevention as Mediating the Effect of Internal Audit, Risk Management, Whistleblowing System and Big Data Analytics on the Prevention of Financial Crime Behavior”. This is supported by the results of previous studies which explained that the development of turbulence of human activities led to criminal behavior such as fraudulent acts undergoing a transformation that has attracted the attention of many researchers around the world (Dan Desi Handayani, Citation2018; Indriani Dan & Titan Terzaghi, Citation2017; Rezaee & Wang, Citation2018; Rusmana & Tanjung, Citation2019). This paper deals with an attempt to summarize the current discussions and findings, regarding how fraud prevention and disclosure is important, and in what ways it can be prevented. Several research results from various institutions and world organizations provide an overview of the shifts that have occurred (Chiu et al., Citation2018). This action is due to the fact that each actor is required to submit accurate and relevant financial information.

The issue of fraudulent practices in Indonesia has become one of the nation’s main problems because of the increasing prevalence of violations. The Association of Certified Fraud Examiners (ACFE) stated that of the 14 institutions that most frequently appeared fraudulent practices, the first place was occupied by the Regency Government (Pemkab) with a total of 246 cases, the second rank was occupied by institutions under the auspices of the City Government (Pemkot) which had 56 cases, third ranked, namely institutions in the Provincial Government (Pemprov) with a total of 23 cases with state losses reaching Rp. 88.1 billion, and the fourth place was occupied by State-Owned Enterprises (BUMN) with 18 corruption cases owned with losses reaching Rp. 249.4 billion, in fifth place, namely KPU/KPUD with 14 cases that cost the state Rp. 26 billion, the sixth is the Ministry with 13 cases that cost the state Rp. 56 billion, and there are many other sequences from the 7th to the fourteenth including BUMD with 12 cases that cost the state as much as Rp. 69 billion, DPRD/DPR with 10 cases that harm as much as Rp. 8 billion, the Agency as many as 8 cases that harm Rp. 15 billion, Universities with 7 cases as much as Rp. 12 billion, the Court with 4 cases that harm as much as Rp. 2 billion, the Prosecutor’s Office with 4 cases that cost Rp. 0.8 billion, NGOs with 2 cases as much as Rp. 24 billion, and Bank Indonesia with 1 case.

The Regional Apparatus Work Unit (SKPD) is part of the public sector which is always under the spotlight because of budget management which often experiences leakage. This is evidenced by a number of cases of misuse of the budget. This opinion is emphasized by Hidayat et al. (Citation2017) that the impact of regional dependence on the centre includes the lack of decentralization of regional finance and the powerlessness of local communities to manage their own households. The same information is shown through an increase in data on cases regarding financial crime behavior resulting from the transformation of information systems in the Digital Age. Good financial management can be seen from quality financial reports. Quality financial reports can be used as a form of accountability to the public in monitoring and evaluating performance, providing a basis for observing trends across time periods, achieving the goals that have been set, and comparing them with previous performance (Enggar Diah et al., Citation2018). This opinion shows that the quality of financial reports is a barometer of the size of the depth of financial statement information presented in providing a true and honest picture Dan Freddie Lasmara (Citation2016).

Various kinds of scientific studies that have been carried out provide clues that the skills mismatch on the impact of fraud and financial crime behavior is still a fundamental polemic that will continue to hamper the productivity and competitiveness of various economic and industrial sectors in Regional Governments in Indonesia (Badan Pusat Statistik Indonesia (BPS), Citation2020; Gropello et al., Citation2011; Iryanti et al., Citation2014; McLaren et al., Citation2019; Naafs & White, Citation2012). Various similar studies also recommend efforts that must be considered to strengthen the relevance of the efforts considered in responding to the polemics that occur, not only regarding economic aspects, but also socio-cultural challenges in social and state life which will later be an effort to build a generation of economic citizens affected by cases of fraud and financial crime behavior (Baytiyeh & Naja, Citation2012; Gillespie & Graham, Citation2014; Landrum et al., Citation2010). For problems related to the prevention of financial crime behavior, the researcher argues that there is a dichotomy of phenomena from legal and economic concepts in the formulations used in the disclosure of financial crime prevention behavior, which causes the process of law enforcement to be unstructured and systematic in the frame in which there is systems theory (Farkhani et al., Citation2018).

The phenomenon of legal development towards legal pressure and specialization tends to ignore system theory, thus creating ambiguity at the level of implementation. Legal aspects should ideally be interpreted and studied comprehensively in a system structure known as the Law Enforcement System (Isharyanto, Citation2016). If the interpretation is carried out separately, it can lead to inequality in the perception of equality and is not comprehensive which can later lead to a miscarriage of justice (Failure to realize justice; Chazawi, Citation2010; Lawrence, Citation1975). The problem discussed in this study is the limited strategic formulation in risk management, internal audit, whistleblowing system and big data analytics for early detection to prevent fraud and financial crime behavior in Indonesia, especially the problem of fraud occurred in Sumatra, namely Aceh, North Sumatra, Riau, Kepulauan Riau, South Sumatra, Bangka Belitung, Jambi, West Sumatra, Bengkulu and Lampung. Seeing this reality, a more systematic effort is needed in preventing fraud and financial crime behavior by using a clear line of thought that combats this. There is a sizeable accounting literature on the determinants of fraud prevention and financial crime behavior (Beasley, Citation1996; Beneish, Citation1997; Brazel et al., Citation2009; Dechow et al., Citation2011, Citation1996; Efendi et al., Citation2007; Entwistle & Lindsay, Citation1994; Schrand & Zechman, Citation2012; Summers & Sweeney, Citation1998). The purpose of this study differs from the previous one, the researcher hopes to develop a model that can accurately predict the prevention of accounting fraud in Indonesia from the available units of analysis.

The first purposive procedure is related to the utilization of the function of the internal audit role. Researchers suspect that organizational fraud in local governments can be reduced in all provinces in Sumatra in Indonesia if they are able to focus their efforts on internal control. This opinion is confirmed by Enggar Diah Puspa Arum dan Ilham Wahyudi (Citation2020) who argue that fraudulent financial reporting is a reported condition related to presenting financial information that contains misstatements to deceive financial statement users. Furthermore, Dan Goel (Citation2012) argue that fraudulent financial reporting occurs when financial reporting contains an intentional misstatement or omission of material facts (numbers, disclosures, or evidence) to deceive users. Some deviations often occurred today regarding financial accountability to local governments in all Sumatra provinces in Indonesia are terminology tendencies regarding the involvement of several elements consisting of misleading facts, violation of rules or abuse of trust, and the commission of critical facts can be reduced or prevented when intensive internal audit activities are carried out and also the function of internal auditors in local governments is still mostly corrective and not preventive in nature, and there are still frozen monitoring results. According to Sri Dan Freddie Lasmara (Citation2016), the current situation clearly indicates that the control system through the implementation of the accounting function has not been implemented proportionally. This has an impact on the role of the local government internal control apparatus, which can be said to be less effective in providing early warning information if this potential occurs. Research conducted by Cattrysse (Citation2011) states that a good internal audit can prevent fraud. Likewise, the study conducted by Gusnardi (Citation2011) the results of the study show that all assessment components in internal audit expertise have a positive influence in detecting and preventing fraud and other potential fraud, similar research is also shown through the results of research conducted through research results by previous researchers, namely Tulus Suryanto (Citation2016), Novita (Citation2019), Suginam (2016), Bagus Dan Ginarta et al. (Citation2017), Essa Dianca (Citation2018) who have also succeeded in proving that the role of internal audit has a positive effect on fraud prevention which shows that the higher the role of internal audit, the greater the prevention of fraud. Different results are shown in research conducted by Lestari and Bernawati (Citation2020) which shows that internal audit is negative towards the tendency of fraud. In addition, Dewi, Yuniarti Rozali and Mohammad (Citation2015) also researched fraud which showed that internal audit had a negative effect on the tendency of fraud.

In addition to the importance of the internal audit function in the organization, predictive measures of fraud are also needed and even the prevention of financial crime behavior from risk management that occurs through risk assessment which is an advanced procedure that the researcher proposes. Government Regulation Number 60 of 2008 also states that the leadership of Government Agencies is expected to formulate a risk management approach and risk control activities needed to minimize risk. BPKP has also issued Regulation of the Head of BPKP Number Per-1326/K/LB/2009 dated 7 December 2009 concerning Technical Guidelines for the Implementation of the Government Internal Control System (SPIP) for all elements and sub-elements, including risk identification and risk analysis sub-elements. These regulations are used as guidelines and procedural steps for risk management in local governments. Auditors have a responsibility to detect and disclose all types of fraud that can have a material impact on financial statements (Kranacher et al., Citation2012). An effective way to overcome this is by classifying the inherent risks and the impacts caused by this method is known as risk management. Risk management is an effort to systematically implement regulatory policies and practical management efforts in analysing the use and control of risk to protect workers, society and the environment (Dan Freyke Sangari, Citation2011; Sepang et al., Citation2013; Umimper et al., Citation2015). Risk management is able to reduce the possibility of employee opportunities to commit fraud and even financial crime behavior since these actions can identify and close any gaps and weaknesses in the internal control structure (Kassem & Andrew, Citation2012). Research conducted by Crockford (Citation2005) discusses risk as a function of change. As with the results of research by Taleghani and Mehr (Citation2013), Crockford recommends that risk management should be functioned by all units, not just one department within the organization. Snider et al. (Citation2016) have also discussed the objectives of risk management and the importance of clear risk management objectives. In risk management as a solution to the fraud crisis (Constantin et al., Citation2010). A similar study was conducted by Lister (Citation2007) which discussed the importance of antifraud programs in knowing the risks to mitigate fraud. Despite the extensive literature on financial statement fraud, there are still gaps with regard to proactive prevention. Namely, the discovery of gaps in the concept of risk management in current practice in preventing fraud, as well as the auditor’s perspective in detecting fraud and creating a proactive model to detect and prevent fraud.

In addition to anticipating these things through auditing the use of funds, disclosure of parties who play dishonestly in managing these funds is also needed to reveal fraud in the management of funds that may be committed by several parties. One way to prevent fraud is through the whistleblowing system. The 2019 Association of Certified Fraud Examiners (ACFE) survey shows that the whistleblowing system (WBS) method is a fraud prevention tool which is widely considered to be very effective as anti-fraud control with a percentage of 22.6% (ACFE, Citation2020). WBS is a system that manages reporting on all actions or actions that are against the law, regulations and ethics that are reported confidentially, anonymously and independently. Whistleblowing system is one of the effective mechanisms in preventing fraud that really requires commitment in the reporting person’s data, a clear and responsible reporting mechanism and the process of evaluating and improving the system (Wahyuni & Nova, Citation2018; Wardana et al., Citation2017). Research on the effectiveness of the implementation of whistleblowing in fraud prevention has been carried out, but the results found are still mixed. The results of previous studies indicate that the whistleblowing system is one of the factors that influence fraud. Various studies have shown that the whistleblowing system has a positive effect on fraud prevention (Agusyani et al., Citation2016; Gaurina et al., Citation2017; Islamiyah et al., Citation2020; Jayanti & Suardana, Citation2019; Maulida & Bayunitri, Citation2021; Puryati & Febriani, Citation2020; R. Sari et al., Citation2021; Sujana et al., Citation2020; Wahyuni & Nova, Citation2018; Wardana et al., Citation2017). Several studies on whistleblowing suggest that the whistleblowing system has a role in supporting the creation of sound financial management. Empirically, the results of this study are consistent with research conducted by Citation2017, which shows that the whistleblowing system has a positive and significant effect on fraud prevention. This study is in accordance with the research of Nugroho (Citation2015) and Agusyani et al. (Citation2016) which state that the whistleblowing system has a significant effect on fraud prevention. Diverse information is shown through different results that the whistleblowing system has no effect on fraud prevention (Sujana et al., Citation2020). This is thought to have happened because the whistleblowing system has not been implemented properly so that there is no protection for whistle-blowers in reporting fraud or corruption as well as public concerns about dealing with the law related to reporting fraud (Sujana et al., Citation2020). Besides that, research on the effectiveness of the implementation of whistleblowing in fraud prevention was also carried out found that whistleblowing has a negative effect on accounting fraud. Sudarma et al. (Citation2019) found that whistleblowing has a positive effect on fraud detection. The results of research by Sujana et al. (Citation2020) and Nurcahyo and Sulhani who found that whistleblowing did not affect the prevention of fraud in village financial management. Pamungkas et al. (Citation2017) with the implementation of a good whistleblowing system in an organization, integrity and openness will be formed so as to prevent fraud. This indicates that the better the implementation of the whistleblowing system, the higher the level of prevention of fraud or fraudulent behavior. This explains that the role of risk management is so important in helping prevent fraud and prevent financial crime behavior. If whistleblowing is implemented properly by employees, the prevention of fraud will be higher.

The current development of Information Technology provides an illustration that the activities carried out in the Elements of Regional Government are required to be able to apply various statistical algorithm-based analysis models through the use of big data analytics models that apply Computer Assisted Audit Techniques to facilitate the evaluation of their work. This indicates that it is necessary to anticipate the possibility of criminal threats, the unintentional threat of the accounting profession being able to take advantage of various information technologies (ACCA.The Association of Chartered certified Accountants., Citation2013). Since threats are unpredictable, it is important to be able to determine possible threats. All of these can be determined by examining historical data through available big data analytics. Once threats to accounting systems and assets have been identified, a vulnerability assessment should be carried out (Powers & Jack, Citation2013; Wells, Citation2011). The benefits obtained by the use of big data analytics, especially in Local Government Agencies in Indonesia, make it possible to facilitate work in tracing the potential for fraud. Research conducted by Tang and Karim (Citation2019); and Jha and Chen (Citation2015) has provided views and information on the effectiveness of big data analytics as evidence of fraud prevention. The results of this study are strengthened by the results of research by Appelbaum et al. (Citation2015) and Tang and Karim (Citation2017) who share the same opinion that evidence of the use of big data analytics can be optimized for its function in auditing in an effort to prevent potential fraud. Other researchers conducted research on automated methods of preventing fraud (cheating) through big data analytics. The test was carried out regarding the potential for fraud committed by employees, the results obtained that this concept was proven to be effective and efficient in helping to trace fraud that occurred through scanning transactions which were used as evidence of potential fraud occurring. Similar research was also conducted by researchers who made the factor in fraud prevention the dependent variable in their research (Alam, Citation2014; Klynveld et al., Citation2010; Olawake, Citation2013; Ryan, Citation2018)

Several researchers have tested the magnitude of the predictive value generated from each of the internal audit variables, risk management, whistleblowing systems and big data analytics on fraud prevention and financial crime behavior, but empirical evidence shows that no researchers have combined these four variables in preventing fraud. Fraud and empirical research have never been carried out through mediation of fraud prevention in analysing the resulting size, as well as other arguments obtained from the results of the resulting test providing information on the amount of content that varies and is inconsistent since the findings and perspectives of each person are different in each region.

To support the auditor’s ability to prevent occurring fraud in his audit, the auditor needs to understand fraud, its types, characteristics, and ways to detect it. In conducting the examination, each auditor must have audit capability. As well as in routine activities, especially in fraud prevention efforts, an auditor needs to be supported by an attitude of mastery of risk management techniques, the use of the internal audit function, the use of the whistleblowing system and the efficient use of big data analytics. Therefore, this research aimed at extracting information in determining fraud prevention as mediating the influence of internal audit, risk management, whistleblowing system and big data analytics on the prevention of financial crime behavior.

1.1. Formulation of research question

Responding to criticism and concerns about fraud and prevention, this study poses five research questions as follows:

RQ 1: How is the influence of Internal Audit on fraud prevention,

RQ 2: How does Risk Management affect fraud prevention,

RQ 3: How does the Whistleblowing system affect fraud prevention,

RQ 4: How does big data analytics affect fraud prevention,

RQ 5: How fraud prevention mediates the influence of Internal Audit, Risk Management, whistleblowing system and big data analytics on the prevention of financial crime behaviour.

In relation to the five research questions posed above, it is very important to highlight the role of fraud prevention in mediating the prevention of financial crime behaviour. Researchers combine these four variables in the study as these four attitudes are considered to be the initial determining factors in accordance with related issues and regulations in carrying out their functions as an effort to prevent the occurrence of financial crime behaviour prevention through fraud prevention mediation.

2. Methods

2.1. Methodology of structured systematic literature review

Along with the development of digital technology, fraud detection methods must also continue to be developed hence they can be applied effectively and can detect the indications of fraud using digital technology. According to Donning et al. (Citation2019), the development of a fraud detection system is not an easy thing to do because it involves new technology and requires financial support from those who specifically allocate it for the purpose of fighting fraud. Fraud prevention is a strategy that researchers propose as a preventive measure to prevent financial crime behavior in measuring and managing the presence or absence of the use of human resources through acts of fraud, fraud or errors that are intentionally committed either to individuals or entities through a special method of literature study (i.e., literature review; structured and systematic) used by using a general search on several academic database sources.

This study utilized seminal papers published through the ISI Web of Knowledge database and the Scopus database. This is necessary to appreciate the similarities and differences of fraud prevention in mediating the prevention of financial crime behavior, and fraud issues occurring in the Regional Government SKPD in Sumatra, Indonesia. To eliminate inappropriate searches on studies related to the topic in this study, the researcher conducted a limited retrieval of the Social Science Citation Index (SSCI) and used certain keywords to avoid irrelevant material. Specific keywords used in this study included “Fraud prevention,” “Internal Audit”, “Risk Management”, “Whistleblowing system”, “Big Data Analytics”, and “Prevention of Fraudulent Behavior”. Judging from the time span of the study, the study materials used in this study ranged from the early 1990s to 2021, which were available in the two previous academic databases. Attached is the classification of articles based on their journal groups as follows:

2.2. Empirical research methodology

As a continuation of the systematic study of the literature, this section of this paper attempts to draw on potential empirical methods, which may be useful in conducting empirical tests for future research. The most common methodology used in fraud prevention analysis in mediating the prevention of financial crime behavior uses content analysis. The combination of all these attributions has a stronger relationship with fraud prevention and financial crime behavior than one individual aspect, which suggests a common mechanism between attributions. Although each component has shown discriminant validity across multiple samples when compared to one another (Carifio & Rhodes, Citation2002) there is also evidence to support the overall core construct (Luthans et al., Citation2010).

As described by Guthrie et al. (Citation2017) content analysis concentrates on the codification of qualitative and quantitative information into predetermined categories to obtain patterns in reporting and presenting information. Therefore, a potential data collection procedure can be referred to the study. In the literature study, the procedure was divided into three stages. The first stage focuses on defining the recording unit as one sentence in a paragraph. The second stage concerns the determination of coding rules to capture specific information related to each variable contained in the research, and the third stage is the coding process.

3. Results and discussion

3.1. Theoretical framework

This research is the development of the center of topic of previous research that examines factors related to fraud prevention in mediating the prevention of financial crime behavior based on Fraud Triangle (Cressey, Citation1953) and Diamond Theory (Wolfe & Hermanson, Citation2004) as Grand Theory in an effort to provide an explanation of the phenomenon and formulate research hypotheses, and supported through attribution theory (Fritz, Citation1958) and legal theory from criminology, namely the General Theory Of Crime (Gottfredson & Hirschi, Citation1990) as a supporting theory (supported theory) as well as several concepts that explain in more detail about fraud prevention, behavior prevention financial crime, internal audit, risk management, whistleblowing system and big data analytics. This research is also supported by several descriptions of the results of previous studies that are needed in designing the research concept. Along with the increasingly complex activities occurring in Digital dynamics, the activities and problems faced by the public sector, especially in the Regional Government in the Sumatra Province of Indonesia will be increasingly complex so that it is increasingly more difficult to supervise all service activities, where the greater the possibility for fraud and even potential activities that leads to financial crime behavior.

Table illustrates the theoretical approach to the development of Fraud Prevention mediating the Prevention of Financial Crime Behavior of literature. In this regard, the Fraud Triangle (Cressey, Citation1953) and Diamond Theory (Wolfe & Hermanson, Citation2004) are clearly related to government relations, while attribution theory (Fritz, Citation1958) and legal theory from criminology, namely the General Theory of Crime (Gottfredson & Hirschi, Citation1990) is associated with stakeholder relations. More in detail, the disclosure of Fraud Prevention in mediating the prevention of financial crime behavior can be used to signify the accountability of government performance. The fraud triangle is a framework commonly used in auditing to explain the reason behind an individual’s decision to commit fraud. The fraud triangle outlines three components that contribute to increasing the risk of fraud: (1) opportunity, (2) incentive, and (3) rationalization. The fraud triangle summarizes three elements that are present when an individual commits fraud: opportunity, pressure, and rationalization. Public officials can help prevent fraud by diminishing any one of the triangle’s three elements and, ideally, taking steps to diminish all three elements. Cressey’s fraud triangle helps an organization determine the motives behind an individual’s decision to commit fraud as well as the opportunities enabling him to perpetrate the theft. In this regard, fraud triangle theory and diamond theories are obviously related to the government relation, while legitimacy, stakeholder, and attribution theory (Fritz, Citation1958) and legal theory from criminology, namely the General Theory of Crime (Gottfredson & Hirschi, Citation1990) are associated with the stakeholder relation. This leads to the effort of obtaining and gaining the public legitimacy for the under-performing companies, in which fraud triangle theory, diamond theories, attribution theory, and General Theory of Crime are relevant as the basis of argument development. Table . The Referred Literature Studies From Varible in The Research from the 1990s to 2021.

Table 1. The referred literature studies of internal audit, risk management, whistleblowing system, big data analytics, fraud prevention, and prevention of Financial crime behavior from the 1990s to 2021

Table 2. Relevant theoretical frameworks

3.2. Relationship between variables

a. The Influence of Internal Audit on fraud prevention

Internal audit has an important role in evaluating control system activities, providing input for improvement and also has a significant role in supervising activities. It takes a big responsibility in monitoring activities to ensure that anti-fraud programs and controls are running effectively. Internal audit activities can prevent as well as overcome fraud. Internal audit can be a barometer of behavioral standards within the organization through continuous monitoring activities, which encourage the creation of an efficient work climate. Research by Petra and Tieanu (Citation2014), Oki et al. (Citation2021), Onoja Emmanuel and Usman (Citation2015), R. Sari et al. (Citation2021), Hendri et al. (Citation2020), and Badara and Saidin (Citation2013); (Abdullah et al., Citation2018); Alzeban and Sawan (Citation2013), Widilestariningtyas et al. (Citation2016), Dewi, Yuniarti Rozali and Mohammad (Citation2015), Firmansyah (Citation2020), Mahendra et al. (Citation2021), Wijayanti and Hanafi (Citation2018), Yuniarti (Citation2017), Pua et al. (Citation2017), and Ginanjar and Syamsul (Citation2020) explains that there is a positive and significant influence between internal audit on fraud prevention. From this research, researchers are interested in testing whether there is a direct influence between internal audit on fraud prevention in the Regional Government of Sumatra Province in Indonesia, with the assumption that the better the internal audit capability will be the effective role of internal audit, the fraud prevention can be carried out.

b. The effect of risk management on fraud prevention

Alleyne (Citation2016), Johansson and Carey (Citation2016), Kurniawan Saputra et al. (Citation2020), Lee and Fargher (Citation2013), Mursalim et al. (Citation2021), Pamungkas et al. (Citation2020), Puryati and Febriani (Citation2020), Robinson et al. (Citation2012), Saputra and Sanjaya (Citation2019), Shonhadji and Maulidi (Citation2021), Yulian Maulida and Indah Bayunitri (Citation2021), Sujana et al. (Citation2020), Triantoro et al. (Citation2020), Romadaniati and Nazir (Citation2020), Sudarma et al. (Citation2019), Pramudyastuti et al. (Citation2021), Mersa et al. (Citation2021), and Ariastiani et al. (Citation2018) found that risk management is positively and significantly associated with fraud prevention. Risk management is defined as a relationship of the ways in which each individual uses his knowledge, skills, and behavior at work related to certain types of contextual tasks, namely with regard to what must be done, and how well the work is done. In this study, the authors argue that risk management is a determining factor where the higher the risk that arises, the more things will be done in an effort to prevent fraud, resulting in a lower tendency of individuals to commit fraud.

c. The influence of the whistleblowing system on fraud prevention

The results of research conducted by Alazzabi et al. (Citation2020), Chowdhury and Shil (Citation2019), Harahap and Nengzih (Citation2021), Hussaini et al. (Citation2018), Pangaribuan (Citation2020), Shanmugam et al. (Citation2012), and Sunaryo et al. (Citation2019) shows that partially the whistleblowing system has a positive influence, which means that the higher the whistleblowing system, the less likely there is to be a fraudulent act. In this study, it was concluded that the existence of a whistleblowing system includes those within an agency, and there is compliance with the whistleblowing system in it. The better the whistleblowing system of a government agency, the lower the tendency to fraud. Likewise, the higher the level of compliance with the whistleblowing system, the lower the level of fraud in the government sector.

d. The effect of information technology (big data analytics) on fraud prevention

The use of information technology (big data analytics) in work has radically changed the types of jobs, workers, organizations, and management systems used to manage organizations. The success of investigators and auditors is highly dependent on their ability to contribute value to the organization through the effective use of information technology. The results of this study indicate that understanding the use of information technology through big data analytics has a positive and significant effect on fraud prevention (Broeders et al., Citation2017; Roger Clarke, Citation2016; Herland et al., Citation2018; Vikash Sharma, Citation2016; Zhang et al., Citation2015).

The arising fraud problems in Government Agencies are a sign of disobediently and inconsistently carried out functions resulting in unhealthy governance. Therefore, it is necessary to mediate fraud prevention in overcoming the prevention of financial crime behavior as early as possible in an effort to avoid fraud. To overcome this, the role of internal audit must be consistently empowered which can trigger the implementation of risk management control and public compliance with the use of the whistleblowing system and big data analytics as well as an important role in various aspects of the organization which include fraud and financial crimes behavior prevention. In this study, fraud prevention refers to an effort, system and reintegration procedure that can suppress the occurrence of factors causing fraud, eliminate the causes of fraud, and prevent fraud. Figure displays the proposed potential research model, which could be the empirical base test of the relationship between main variables of interest. In that model, fraud prevention can mediate the prevention of financial crime behavior are conjectured to contribute to the variation of internal audit, risk management, whistleblowing system and big data analytics. Based on references to theories, concepts, and a number of research results, a schematic framework of thought can be drawn up in the following figure:

Figure 1. Theoretical framework.

Based on the research framework, a research concept can be drawn up that explains the relationship between the variables of this study. The overall conceptual framework model in this study can be described as follows as shown in Figure :

Figure 2. Conceptual framework model.

The results of the literature review on several articles, the authors found related literature in mediating fraud prevention efforts. The result of the article reviews can be checked in the appendix 1.

The summary of the study provides us with various information on how to build a good reputation for government accountability through fraud prevention measures, and how fraud prevention mediates the prevention of financial crime behavior through fraud prevention. Fraud prevention is a strategy that the researcher proposes as a preventive measure to prevent financial crime behavior in measuring and managing the presence or absence of the use of human resources through acts of fraud. Intentionally committed fraud or errors made by a person or entity who knows the results are is not good to the individual or entity.

The researcher chose the study on Regional Governments in Indonesia as the object of research since it is intended to determine the de facto measure of Regional Governments in Indonesia in carrying out professional, intensive, and sustainable prevention efforts related to the problems. Besides, they wanted to analyse as a whole about the potential problems occurring in each Regional Government in Indonesia with the potential for various problems and irregularities of fraud. For those reasons, the researcher analysed how much fraud prevention mediates the influence of internal audit, risk management, whistleblowing system and big data analytics on the prevention of financial crime behavior by presenting new information since the perception of each person in each region is divergent. Based on the literature survey and the synthesis, the research novelties in this study are:

First, increase knowledge by developing new variables in a way through the synthesis of new information that is re-examined using a logical framework of research variables contrasting from previous research conducted by Abdullahi and Mansor (Citation2015) through Fraud Theory and Fraud Diamond Theory which those variables do not have a significant effect. In testing this research, the researcher conducted an update using several different variables which the researcher suspected had their own influence and role and added other unexamined variables in fraud prevention mediating the influence of internal audit, risk management, whistleblowing system and big data analytics on the prevention of financial crime behavior. The argument underlying this research is to be able to synthesize new information in a distinct way which is done in Indonesia. Therefore, researchers applied some of the latest ideas needed to empirically prove the activism carried out and the relationship between these variables by knowing the size parameters of research on fraud in the public sector, especially the magnitude of the predictive value on the use of risk management variables and big data analytics that were previously only researched in the private sector. Some of the reasons for the lack of research on fraud in the public sector through the use of these variables include the difficulty of data on fraud in the public sector, in addition to the assumption that the private sector is more likely to commit fraud than the public sector. Therefore, preventive measures to prevent fraud are a sure-fire strategy in mediating financial crime behavior through these four attitudes through the applicable methods to be used. This statement is in line with research conducted by Dechow et al. (Citation1996) which indicated that the potential for fraud could occur in various organizational units. This finding is reinforced by Dunn (Citation2004) who concludes that fraud is more likely to occur when there is a concentration of power in the hands of insiders accompanied by a predictive model of fraud (Bart et al., Citation2021; Cross, Citation2018; Drie, Citation2018; Mehmet & Ganji, Citation2021).

Second, this study develops a predictive model for the disclosure of fraud prevention and prevention of new financial crime behavior and the magnitude of the resulting value charge between variables from the unit of analysis studied through the use of financial statements and audit evidence obtained publicly (Kapardis & Papastergiou, Citation2016; Schuchter & Levi, Citation2015; Sundarakantham, Citation2019) by following a review of previous research on economic activities in the Regional Government of Sumatra Province in Indonesia. The fraud prediction model that the researcher proposes differs from the benchmark model which can be determined in two main ways. First, researchers used fraud ensemble learning, a sophisticated machine learning paradigm in the form of using big data through strengthening the whistleblowing system, risk management and internal control in the form of using internal audit, to predict fraud (the rarity of fraud). Second, the measurement model used raw financial data items and perceptions of State Civil Apparatus and auditors with Auditor Functional Positions (JFA) who work at BPK Regional Representatives in Indonesia as predictors of fraud. Raw financial data items are the most basic building blocks of accounting systems, researchers are interested in exploring whether these data can be directly used in fraud prediction. Various kinds of potential shifts in the dynamics of fraud prevention as mediating the influence of internal audit, whistleblowing system, risk management, and big data analytics can BE addressed through various anticipatory steps with synergy between Local Governments in Indonesia and the Community as well as preventive efforts in providing information on the impacts and risks involved. resulting from various modes of fraud and actions that lead to financial crime behavior.

Third, this study expands, qualifies or elaborates a number of measurement indicators through a systematic literature review using accounting scientific indicators through the representation of the relationship between disclosure prevention through meta-analysis found regarding fraud prevention and financial crime prevention behavior which is an important predictor of determining the attitude and behavior barometer. Behavior related to the grand theory is used in an effort to provide perspective on phenomena and can trigger research hypotheses through Diamond Theory (Wolfe & Hermanson, Citation2004), with attribution theory (Fritz, Citation1958) and legal theory from criminology, namely the General Theory of Crime Gottfredson and Hirschi (Citation1990) as a supporting theory. For this reason, the researchers combined the four attributions to determine the size of the value, determining and inhibiting factors obtained from the prediction model in generalizing matters in preventing fraud and financial crime behavior in local governments of Sumatra province in Indonesia. Based on the order of the theoretical framework, the researcher finally obtained a reference that could be used as a guide in empirically proving the synergy of these problems through a systematic literature review of research.

4. Conclusion and implications

The conclusion from the literature review as the stated goal is how Fraud Prevention as Mediation for the Effect of Internal Audit, Risk Management, Whistleblowing System and Big Data Analytics on the Prevention of Financial Crime Behavior provide information about the relationship between the magnitude of the influence. The results of the literature review on the article found the importance of Fraud Prevention efforts carried out as Mediating the Influence of Internal Audit, Risk Management, Whistleblowing System and Big Data Analytics.

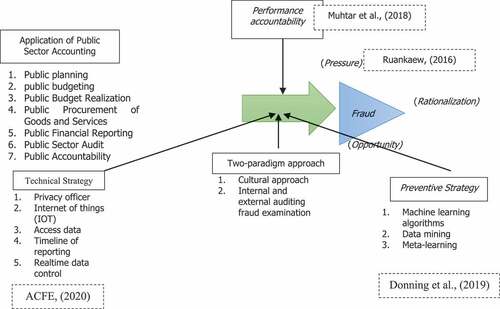

This study contributes to the literature by providing an understanding of how the simultaneity of fraud activity (internal audit and risk management) with organizational predictors (whistleblowing system, and big data). Fraud prevention is a strategy that the researcher proposes as a preventive measure in measuring and managing the presence or absence of the use of human resources through acts of fraud, fraud or errors that are intentionally committed either to individuals or entities. Overall, the model for implementing public sector accounting in preventing fraud and even financial crimes that occur in the Public Sector in the Digital Age can be described as follows as shown in Figure :

Figure 3. Public sector accounting application model in the digital age in preventing fraud.

Based on the application model, it can be stated that the presence of digital technology, especially with its products in the form of big data and cloud computing, will change the method of measuring assets from what was originally done conventionally to using digital technology to measure assets, thereby minimizing the potential for fraud that occurs. It is supported that understanding the use of information technology through big data analytics has a positive and significant effect on fraud prevention (Broeders et al., Citation2017; Roger Clarke, Citation2016; Herland et al., Citation2018; Vikash Sharma, Citation2016; Zhang et al., Citation2015). A large body of literature also documents the large role of fraud prevention in mediating the potential for fraud to occur. In conclusion, this study tries to critically and systematically review literature works in finance, economics, and auditing from a theoretical or conceptual empirical point of view. Thus, this research focuses on providing a structured and systematic literature review accompanied by evidence in academia that can be used as a frame of reference for research models and further empirical tests.

Disclosure statement

No potential conflict of interest was reported by the authors.

Additional information

Funding

Notes on contributors

Iwan Putra

Iwan Putra, a postgraduate student at Economics Study Program, Universitas Jambi, Indonesia who has research interest in the area of financial accounting, economic of education and auditing.

Urip Sulistiyo

Urip Sulistiyo, a lecturer at the Faculty of Teacher Training and Education, Universitas Jambi who has research interest in the area of teacher education and professional development, and language curriculum.

Enggar Diah

Enggar Diah, a lecturer at the faculty of economics and business, Universitas Jambi who has research interest in Fraudulent Financial Reporting, Fraud Disclosure, internal audit, etc.

Sri Rahayu

Sri Rahayu, a lecturer at the faculty of economics and business, Universitas Jambi who has research interest in Financial Constraints and corporate governance, government organization, etc.

Syurya Hidayat

Syurya Hidayat, a senior lecturer at the faculty of economics and business, Universitas Jambi who has research interest in the area of development model and strategies of global economics approach in Indonesia.

References

- Abdullahi, R., & Mansor, N. (2015). Fraud triangle theory and fraud diamond theory. Understanding the convergent and divergent for future research. International Journal of Academic Research in Accounting, Finance and Management Sciences, 5(4).https://doi.org/10.6007/IJARAFMS/v5-3/1823

- Abdullah, R., Ismail, Z., & Smith, M. (2018). Audit committees’ involvement and the effects of quality in the internal audit function on corporate governance. International Journal of Auditing, 22(3), 385–27. https://doi.org/10.1111/ijau.12124

- ACCA.The Association of Chartered certified Accountants. (2013). The business benefits of sustainability reporting in Singapore. Singapore.

- ACFE.,(2020). Report to the nations on occupational fraud and abuse. Online. Global Fraud Study: https://acfepublic.s3-us-west2.amazonaws.com/2020-Report-to-the-Nations.pdf

- Agusyani, K. S., Sujana, E., & Wahyuni, M. A. (2016). Pengaruh whistleblowing system dan kompetensi fraud pada pengelolaan keuangan penerimaan pendapatan asli daerah (studi pada dinas pendapatan daerah kabupaten buleleng). Jurnal Jurusan Akuntansi Program S1, 6(: 3), Tahun 2016. http://dx.doi.org/10.23887/jimat.v6i3.8801

- Alam, M. D. (2014). Persepsi aparatur pemerintah dan anggota dewan perwakilan rakyat daerah kota malang terhadap fraud dan peran whistleblowing sebagai upaya pencegahan dan pendeteksian fraud. Tahun 2014. Jurnal Ilmiah Mahasiswa FEB. 2. 2. https://jimfeb.ub.ac.id/index.php/jimfeb/article/view/1280

- Alazzabi, W. Y. E., Mustafa, H., & Karage, A. I. (2020). Risk management, top management support, internal audit activities and fraud mitigation. Journal of Financial Crime, ahead-of-p(ahead-of-print. https://doi.org/10.1108/jfc-11-2019-0147

- Alles, M., & Gray, G. L. (2016). Incorporating big data in audits : Identifying inhibitors and a research agenda to address those inhibitors. International Journal of Accounting Information Systems, 22, 44–59. https://doi.org/10.1016/j.accinf.2016.07.004

- Alleyne, P. (2016). The influence of organisational commitment and corporate ethical values on non-public accountants’ whistle-blowing intentions in Barbados. Journal of Applied Accounting Research, 17(2), 190–210. https://doi.org/10.1108/JAAR-12-2013-0118

- Alzeban, A., & Sawan, N. (2013). The role of internal audit function in the public sector context in Saudi Arabia. African Journal of Business Management, 7(6), 443–454. https://doi.org/10.5897/AJBM12.1430

- Appelbaum, D., Kogan, A., Yan, Z., & Vasarhelyi, M. (2015). Impact of business analytics and enterprise systems on managerial accounting. International Journal of Accounting Information Systems, 25(March), 29–44. https://doi.org/10.1016/j.accinf.2017.03.003

- Ariastiani, N. K. D., Yuniarta, G. A., & Kurniawan, P. S. (2018). Pengaruh kompetensi sumber daya manusia, sistem pengendalian internal, proactive fraud audit, dan whistleblowing system terhadap pencegahan fraud pada pengelolaan dana BOS se-kabupaten klungkung. JIMAT (Jurnal Ilmiah Mahasiswa Akuntansi), 8(2), 13–69. https://doi.org/10.23887/jimat.v8i2.13291

- Badan Pusat Statistik Indonesia (BPS). (2020). Catalog : 1101001. Statistik Indonesia, 2020. https://www.bps.go.id/publication/2020/04/29/e9011b3155d45d70823c141f/statistik-indonesia-2020.html’

- Badara, & Saidin. (2013). The relationship between audit experience and internal audit effectiveness in the public sector organizations. International Journal of Academic Research in Accounting, Finance and Management Sciences, 3(3), 329–339. https://doi.org/10.6007/ijarafms/v3-i3/224

- Bagus Dan Ginarta, I., Kusuma, A., & Sedana, P. (2017). Pembentukan portofolio optimal pada saham-saham perusahaan sub-sektor konstruksi bangunan di bursa efek indonesia (Pendekatan Markowitz). E-Jurnal. https://erepo.unud.ac.id/id/eprint/16275

- Bart, B., Sebastiaan, H., Oppner, C., & Verdonck. (2021). Data engineering for fraud detection. Decision Support Systems Jurnal. https://doi.org/10.1016/j.dss.2021.113492

- Baytiyeh, H., & Naja, M. (2012). Identifying the challenging factors in the transition from colleges of engineering to employment. European Journal Of Engineering Education, 37(1), 3–14. https://doi.org/10.1080/03043797.2011.644761

- Beasley, M. S. (1996). An empirical analysis of relation between directors and financial fraud. The Accounting Review, 71(4), 443–465. https://www.jstor.org/stable/248566

- Beneish, M. D. (1997). Detecting GAAP violation: Implications for assessing earnings management among firms with extreme financial performance. Journal of Accounting and Public Policy, 16(3), 271–309. https://sci-hub.se/10.2469/faj.v55.n5.2296

- BPKP., (2015). Etika dalam fraud audit. https://pusdiklatwas.bpkp.go.id/

- Brazel, J. F., Jones, K. L., & Zimbelman, M. F. (2009). Using nonfinancial measures to assess fraud risk. Ssrn Electronic Journal, 47(5), 1135–1166. https://www.jstor.org/stable/40389222

- Broeders, D., Schrijvers, E., van der Sloot, B., van Brakel, R., de Hoog, J., & Hirsch Ballin, E. (2017). Big data and security policies: Towards a framework for regulating the phases of analytics and use of big data. Computer Law and Security Review, 33(3), 309–323. https://doi.org/10.1016/j.clsr.2017.03.002

- Carifio, J., & Rhodes, L. (2002). Construct validities and the empirical relationships between optimism, Hope, Self-Efficacy, And Locus Of Control. Journal Of Work, 19(2), 125–136. https://content.iospress.com/articles/work/wor00249

- Cattrysse, J. (2011, January). Reflections on corporate governance and the role of the internal auditor. SSRN Electronic Journal, https://doi.org/10.2139/ssrn.485364

- Chazawi, A. (2010). Pelajaran hukum pidana I (stelsel pidana, tindak pidana, teori-teori pemidanaan & batas berlakunya hukum pidana). PT RajaGrafindo Persada.

- Chiu, T., Huang, F., Liu, Y., & Vasarhelyi, M. A. (2018). The impact of nontimely 10-Q fi lings and audit firm size on audit fees. Managerial Auditing Journal, 33(5), 503–516. https://doi.org/10.1108/MAJ-10-2017-1673

- Chowdhury, A., & Shil, N. C. (2019). Influence of new public management philosophy on risk management, fraud and corruption control and internal audit: Evidence from an Australian public sector organization. Journal of Accounting and Management Information Systems, 18(4). https://doi.org/10.24818/jamis.2019.04002

- Clarke, R. (2016). Big data, big risks. Information Systems Journal, 26(1),77–90. 2016. https://doi.org/10.1111/isj.12088

- Constantin, Pluciennik, A., Dzantiev, L., Iyer, R. R. N., Kadyrov, F. A., & Modrich, P. (2010). PCNA function in the activation and strand direction of MutL α endonuclease in mismatch repair. Proceedings of the National Academy of Sciences, 107(37), 16066–16071. https://doi.org/10.1073/pnas.1010662107

- Cressey, D. R. (1953). Other people’s money, dalam “detecting and predicting financial statement fraud : The effectiveness of the fraud triangle and SAS no 99”. Journal of Corporate Governance and Firm Performance, 13, 53–81. Skousen et al.2009. https://doi.org/10.2139/ssrn.1295494

- Crockford, G. N. (2005). The changing face of risk management (first published in 1976 in the Geneva Papers). Geneva Papers on Risk and Insurance: Issues and Practice, 30(1), 5–10. https://doi.org/10.1057/palgrave.gpp.2510019

- Cross, C. (2018). Victims’ motivations for reporting to the ‘Fraud Justice Network’. Police Practice and Research, 19(6), 550–564. https://doi.org/10.1080/15614263.2018.1507891

- Dan Desi Handayani, Y. S. (2018). Mendeteksi kecurangan laporan keuangan dengan analisis fraud pentagon. Jurnal Akuntansi, Keuangan Dan Bisnis, 11(1), 11–23. https://jurnal.pcr.ac.id/index.php/jakb/article/view/1701

- Dan Freddie Lasmara, S. R. (2016). Pengaruh kompetensi sumberdaya manusia, perangkat pendukung dan peran auditor internal terhadap kualitas laporan keuangan pemerintah daerah kabupaten Kerinci. Jurnal Perspektif Pembiayaan Dan Pembangunan Daerah, 3(4), 2338–4603 (print); 2355-8520 (online). April-Juni 2016. https://doi.org/10.22437/ppd.v3i4.3525

- Dan Freyke Sangari, J. T. (2011). Analisis Resiko Pada Proyek Konstruksi Perumahan Di Kota Manado. Jurnal Ilmiah MEDIA ENGINEERING, 1(1), 29–37. 2087-9334 (29-37). https://ejournal.unsrat.ac.id/index.php/jime/article/view/4207

- Dan Goel, G. (2012). Intelligent systems in accounting. Finance And Management Vol. 19(2), 75–89.

- Dechow, DECHOW, P. M., GE, W., Larson, C. R., & SLOAN, R. G. (2011). Predicting material accounting misstatemen. Journal Contemporary Accounting Research, 28(1), 17–82. https://doi.org/10.1111/j.1911-3846.2010.01041.x

- Dechow, P. M., G.Sloan, R., & Sweeney, A. P. (1996). Causes and consequences of earnings manipulation: An analysis of firms subject to enforcement actions by the SEC. Contemporary Accounting Research, 13(1), 1–36. Spring 1996. https://doi.org/10.1111/j.1911-3846.1996.tb00489.x

- Dewi, Yuniarti Rozali, R., & Mohammad, J. (2015). Pengaruh pelaksanaan risk based internal auditing terhadap pencegahan fraud. Jurnal Riset Akuntansi Dan Keuangan, 3(3), 831. https://doi.org/10.17509/jrak.v3i3.6623

- Dianca, E. (2018). Pengaruh Peran Audit Internal Terhadap Pencegahan Fraud (Studi Kasus Pada PT Semen Padang). Jurnal Ekonomi & Bisnis Dharma Andalas , 20(2), 1693 −3273 E-2527–3469. https://ojs.unidha.ac.id/index.php/edb_dharmaandalas/article/view/97/78

- Donning, H., Erikkson, M., Martikainen, M., & Lehner, O. M. (2019). Prevention and detection for risk and fraud in the digital age – the current situation. ACRN Oxford Journal of Finance and Risk Perspectives, 8, 86–97. https://www.acrn-journals.eu/resources/SI08_2019g.pdf

- Drie, H. V. L. (2018). Financial fraud, scandals, and regulation: A conceptual framework and literature review. Business History, 61(8), 1259–1299. https://doi.org/10.1080/00076791.2018.1519026

- Dunn, P. (2004). The impact of insider power on fraudulent financial reporting. Journal of Management, 30(3), 397–412. https://doi.org/10.1016/j.jm.2003.02.004

- Efendi, J., Srivastava, A., & Swanson, E. P. (2007). Why do corporate managers misstate financial statements? The role of option compensation and other factors. Journal Of Financial Economics, 85(3), 667–708. https://doi.org/10.1016/J.Jfineco.2006.05.00

- Enggar Diah, P. A., Eriani, V., & Dan Zamzami. (2018). Pengaruh kompetensi pegawai dan sistem pengendalian internal terhadap kualitas laporan keuangan pemerintahan daerah kabupaten batang Hari. Jurnal Akuntansi & Keuangan Unja, 3(6), Hal.1–13. https://doi.org/10.22437/jaku.v3i6.6039

- Enggar Diah Puspa Arum dan Ilham Wahyudi. (2020). Fraudulent financial reporting detection in banking sector: Evidence from Indonesia. International Journal of Psychosocial Rehabilitation, Conference Special Issue 1475-7192. https://doi.org/10.37200/IJPR/V24SP2/PR201301

- Entwistle, G., & Lindsay, D. (1994). An archival study of the existence, cause, and discovery of income‐affecting financial statement misstatements. Contemporary Accounting Research, 11(1), 271–296. https://doi.org/10.1111/j.1911-3846.1994.tb00444.x

- Farkhani. (2018). On the effectiveness of type-based control flow integrity,Proceedings Of The 34th annual computer security applications conference on – acsac 18, December 3–7, 2018, San Juan, PR, USA. ACM, New York, NY, USA, 12 pages. https://doi.org/10.1145/3274694.3274739

- Firmansyah, I. (2020). Pengaruh audit internal dan pengendalian internal terhadap pencegahan kecurangan (Fraud) di PT perkebunan nusantara VIII. Journal of Chemical Information and Modeling, 53(9), 1689–1699. https://doi.org/10.47491/landjournal.v1i2.705

- Fritz, H. (1958). The Psychology of Interpersonal Relations. Wiley.

- Gaurina, N. P. M., Purnamawati, G. A., & Atmadja, A. T. (2017). Pengaruh persepsi karyawan mengenai perilaku etis dan whistleblowing system terhadap pencegahan fraud (Studi Kasus Pada Bali Hai Cruises). Jurnal Ilmiah Mahasiswa Akuntansi UNDIKSA, 8. 2 Tahun (2017) http://dx.doi.org/10.23887/jimat.v8i2.10450

- Gillespie, A., & Graham, S. (2014). A meta-analysis of writing interventions for students with learning disabilities. Exceptional Children, 80(4), 454–473. https://doi.org/10.1177/0014402914527238

- Ginanjar, Y., & Syamsul, E. M. (2020). Peran auditor internal dalam pendeteksian dan pencegahan fraud pada bank syariah di kota bandung. Jurnal Ilmiah Ekonomi Islam, 6(3), 529. . https://dx.doi.org/10.29040/jiei.v6i3.1392

- Gottfredson, M. R., & Hirschi, T. (1990). A General Theory of A Crime. Stanford University Press.

- Gropello, E., Kruse, A., & Tandon, P. (2011). Skills for the labor market in Indonesia: Trends in demand, gaps, and supply. https://elibrary.worldbank.org/doi/book/10.1596/978-0-8213-8614-9

- Gusnardi. (2011). Pengaruh peran komite audit, pengendalian internal, audit internal dan pelaksanaan tata kelola perusahaan terhadap pencegahan kecurangan. Jurnal Ekuitas, 15(1), 130–146. Maret 2011. https://doi.org/10.24034/j25485024.y2011.v15.i1.196

- Guthrie, J., Manes-rossi, F., & Orelli, R. L. (2017). Integrated reporting and integrated thinking in Italian public sector organisations Meditari Accountancy Research. https://doi.org/10.1108/MEDAR-06-2017-0155

- Harahap, P. S., & Nengzih, N. (2021). The effect of the implementation of enterprise risk management integrating with strategy and performance on fraud prevention. United Arab Emirates Journal, 9414, 141–147. https://doi.org/10.36348/sjef.2021.v05i04.002

- Hendri, H., Yuliantoro, Y., & Ama, M. K. (2020). Determinants of fraud prevention and financial performance as an intervening variable. International Journal of Economics and Financial Issues, 10(1), 19–26. https://doi.org/10.32479/ijefi.8955

- Herland, M., Khoshgoftaar, T. M., & Bauder, R. A. (2018). Big data fraud detection using multiple medicare data sources. Journal of Big Data, 5(1), 1–21. https://doi.org/10.1186/s40537-018-0138-3

- Hidayat, S., Hardiani, & Dan Junaidi, M. (2017). Determinan sosial ekonomi pengeluaran rumah tangga untuk kebutuhan preventif kesehatan di provinsi jambi. Desember 2017. Jurnal Piramida. XIII. 2. https://repository.unja.ac.id/id/eprint/15006

- Hussaini, U., Abu Bakar, A., & Yusuf, M.-B. O. (2018). The effect of the implementation of enterprise risk management integrating with strategy and performance on fraud prevention. United Arab Emirates Journal, 9414, 141–147. https://doi.org/10.36348/sjef.2021.v05i04.002

- Indriani Dan, P., & Titan Terzaghi, M. (2017). Fraund diamond dalam mendeteksi kecurangan laporan keuangan. I- Finance: a Research Journal on Islamic Finance, 3(2), Desember 2017. https://doi.org/10.19109/ifinance.v3i2.1690

- Iryanti, I., Rini, I., & Pangestuti, D. (2014). Pengaruh corporate governance terhadap struktur modal (studi pada perusahaan manufaktur yang terdaftar di BEI periode 2011-2014). Jurnal Akuntansi Bisnis, 9(1), 2014. https://dx.doi.org/10.30813/jab.v9i1.873

- Isharyanto. (2016). Hukum Kebijakan Ekonomi Publik.

- Islamiyah, F., Made, A., & Sari, A. R. (2020). Pengaruh kompetensi aparatur desa, moralitas, sistem pengedalian internal, dan whistleblowing terhadap pencegahan fraud dalam pengelolaan dana desa di kecamatan wajak (studi empiris pada desa sukoanyar, desa wajak, desa Sukolilo, desa blayu dan desa patok. Jurnal Riset Mahasiswa Akuntansi (JRMA), 8(1), 1–3. 2715 - 7016. https://doi.org/10.21067/jrma.v8i1.4452:

- Jayanti, L. S. I. D., & Suardana, K. A. (2019). Pengaruh kompetensi SDM, moralitas, whistleblowing dan SPI terhadap pencegahan fraud dalam pengelolaan keuangan desa. E-Jurnal Akuntansi, 29(3), 1117–1131. https://doi.org/10.24843/EJA.2019.v29.i03.p16

- Jha, A., & Chen, Y. (2015). Audit fees and social capital. Accounting Review, 90(2), 611–639. https://doi.org/10.2308/accr-50878

- Johansson, E., & Carey, P. (2016). Detecting fraud: The role of the anonymous reporting channel. Journal of Business Ethics, 139(2), 391–409. https://www.jstor.org/stable/44164230

- Kapardis, M. K., & Papastergiou, K. (2016). Fraud victimization in Greece: Room for improvement in prevention and detection. Journal of Financial Crime, 23(2), 481–500. https://doi.org/10.1108/JFC-02-2015-0010

- Kassem, R. A. H., & Andrew. (2012). The New Fraud Triangle Model. Journal Of Emerging Trends In Economics And Management Sciences (Jetems), 3(3), 191–195. https://doi.org/10.10520/EJC132216

- Klynveld, P., Marwick, & Goerdeler, (KPMG), (2010). India Fraud Survey Report. KPMG.

- Komite Nasional Kebijakan Governance (KNKG)., (2011). Draft Pedoman Penerapan Manajemen Risiko Berbasis Governance. www.knkgindonesia.com

- Kranacher, M., Dorminey, J., Fleming, A. S., & Riley, R. A. (2012). The evolution of Fraud Theory. Accounting Education, (27 (2): 555–57927 (2), 555–579. https://doi.org/10.2308/iace-50131

- Kurniawan Saputra, K. A., Subroto, B., Rahman, A. F., & Saraswati, E. (2020). Issues of morality and whistleblowing in short prevention accounting. International Journal of Innovation, Creativity and Change, 12(3), 77–88. https://doi.org/10.1016/j.aebj.2017.06.001

- Landrum, R. E., Hettich, P. I., & Wilner, A. (2010). Alumni perceptions of workforce readiness. Teaching of Psychology, 37(2), 97–106. https://doi.org/10.1080/00986281003626912

- Lawrence, M. F. (1975). The legal system. New York: Russell Sage.

- Lee, G., & Fargher, N. (2013). Companies’ use of whistle-blowing to detect fraud: An examination of corporate whistle-blowing policies. Journal of Business Ethics, 114(2), 283–295. https://www.jstor.org/stable/23433892

- Lestari, Y. A., & Bernawati, Y. (2020). Efektifitas Peran Internal Audit Dalam Mencegah dan Mendeteksi Kecurangan. Jurnal Akuntansi Dan Pajak, 20(2), 184–191. . https://dx.doi.org/10.29040/jap.v20i2.740

- Lister, R. (2007). Inclusive citizenship: Realizing the potential. Citizenship Studies, 11(1), 49–61. https://doi.org/10.1080/13621020601099856

- Luthans, F. J. B., Avey, J. B., Avolio, B. J., & Peterson, S. J. (2010). The development and resulting performance impact of positive psychological capital. Human Resource Development Quarterly, 21(1), 41–67. https://doi.org/10.1002/hrdq.20034

- Mahendra, K. Y., Erna Trisna Dewi, A. A., & Rini, G. (2021). pengaruh audit internal dan efektivitas pengendalian internal terhadap pencegahan kecurangan (Fraud) Pada Bank Bumn di Denpasar. Jurnal Riset Akuntansi Warmadewa, 2(1), 1–4. https://doi.org/10.23887/jimat.v8i2.13355

- Maulida, W. Y., & Bayunitri, B. I. (2021). The influence of whistleblowing system toward fraud prevention. International Journal of Financial, Accounting, and Management, 2(4), 275–294. https://doi.org/10.35912/ijfam.v2i4.177

- McLaren, M. R., Willis, A. D., & Callahan, B. J. (2019). Consistent and correctable bias in metagenomic sequencing experiments. ELife, 8. https://doi.org/10.7554/eLife.46923

- Mehmet, H., & Ganji, F. (2021). Investigate the supportive role of management and the independence of the internal auditor in the effectiveness of internal audit. PalArch’s Journal of Archaeology of Egypt/Egyptology, 18(6), 241–251. 567-214X. https://archives.palarch.nl/index.php/jae/article/view/8851

- Mersa, N. A., Sailawati, & Malini, N. E. L. (2021). Pengaruh whistleblowing system sistem pengendalian internal budaya organisasi dan keadilan organisasi trhadap pencegahan kecurangan. Jurnal Akuntansi Keuangan Dan Bisnis, 14(1), 85–92. . https://doi.org/10.35143/jakb.v14i1.4613

- Mursalim, M., Su, M., Ahmad, H., & Hajering, H. (2021). Point of view research accounting and auditing whistleblowing’s effectiveness in preventing fraud through forensic audit and investigative audit. Point of View Research Accounting and Auditing, 2(1), 81–91. https://journal.accountingpointofview.id/index.php/povraa

- Naafs, S., & White, B. (2012). The Asia Pacific journal of intermediate generations : Reflections on Indonesian youth studies intermediate generations : Reflections on Indonesian youth studies. The Asia Pacific Journal of Anthropology, 37–41. https://doi.org/10.35143/jakb.v14i1.4613

- Novita. (2019). Pengaruh Audit Internal Terhadap Pendeteksian Financial Statement Fraud dan Implikasinya Pada Good Government Governance (Studi Pada Dinas Se-Kota Bandung. Jurnal Aktiva: Riset Akuntansi Dan Keuangan, 1(1), 1–12. 2019, 2686-1054. https://doi.org/10.23887/jimat.v13i01.38827

- Nugraha, Y. (2015). Security Assurance Requirements Engineering (STARE) for trustworthy service level agreements. IEEE 23rd International Requirements Engineering Conference, RE 2015-Proceedings, 398–399. https://doi.org/10.1109/RE.2015.7320458

- Nugroho, V. O. (2015). Pengaruh Persepsi Karyawan Mengenai Whistleblowing System Terhadap Pencegahan Fraud Dengan Perilaku Etis Sebagai Variabel Intervening Pada PT Pagilaran. Fakultas Ekonomi Universitas Negeri Yogyakarta. Journal Hasil Riset AKuntansi, 14(1), 85–92. . https://ejournal.unira.ac.id/index.php/jurnal_aktiva/article/view/1333/861

- Oki, I., Brata, D., & Arnan, S. G. (2021). The Influence Of Internal Audit Toward Fraud Prevention In One Of Banks In Bandung. Turkish Journal of Computer and Mathematics Education, 12(8), 840–845. https://turcomat.org/index.php/turkbilmat/article/view/2914

- Olawake, F. (2013). Internal whistleblowing intentions of accounting students in South Africa: the impact of fear of retaliation, materiality and gender. Journal of Social Science, 37(1), 31–44. 2013. https://doi.org/10.1080/09718923.2013.11893202

- Onoja Emmanuel, E., & Usman, H. (2015). Internal audit techniques and fraud prevention: A case study of selected Local Government Councils in Bauch State. Mediterranean Journal of Social Sciences, 6(4), 232–244. https://doi.org/10.5901/mjss.2015.v6n4p232

- Pamungkas, I. D., Ghozali, I., & Achmad, T. (2017). The effects of the whistleblowing system on financial statements fraud: Ethical behavior as the mediators. International Journal of Civil Engineering and Technology, 8(10), 1592–1598. . https://www.iaeme.com/IJCIET/issues.asp?JType=IJCIET&VType=8&IType=10

- Pamungkas, I. D., Wahyudi, S., & Achmad, T. (2020). Whistleblowing system and fraud early warning system on village fund fraud: The Indonesian experience. International Journal of Environmental Science, 5. https://doi.org/10.5430/ijfr.v10n6p211

- Pangaribuan, D. (2020). Governance practices government, of accountability performance and implementation of risk management and implications for fraud detection and prevention. International Journal of Contemporary Accounting, 1(2), 77. https://dx.doi.org/10.25105/ijca.v1i2.6167

- Permenpan, R. B., 2020, Peraturan Menteri Pendayagunaan Aparatur Negara dan Reformasi Birokrasi No 5 Tahun 2020 tentang

- Petra, D., & Tieanu, A. (2014). The Role of Internal Audit in Fraud Prevention and Detection. 21st International Economic Conference 2014, IECS 2014, 16-17 May 2014, Sibiu,Romania Procedia Economics and Finance ( 2014) 16(May), 489–497. https://doi.org/10.1016/S2212-5671(14)00829-6

- Powers, T. L., & Jack, E. P. (2013). The influence of cognitive dissonance on retail product returns. Psychology & Marketing, 30(8), 724–735. https://doi.org/10.1002/mar.20640

- Pramudyastuti, O. L., Rani, U., Nugraheni, A. P., & Susilo, G. F. A. (2021). Pengaruh Penerapan Whistleblowing System terhadap Tindak Kecurangan dengan Independensi sebagai Moderator. Jurnal Ilmiah Akuntansi, 6(1), 115. https://doi.org/10.23887/jia.v6i1.32335

- Pua, B. Y., Sondakh, J. J., & Pangerapan, S. (2017). Evaluasi Fungsi Auditor Internal Dalam Pendeteksian Dan Pencegahan Fraud Pada Pdam Airmadidi. Going Concern?, Jurnal Riset Akuntansi, 12(2), 452–469. https://doi.org/10.32400/gc.12.2.17881.2017

- Puryati, D., & Febriani, S. (2020). The consequence of whistleblowing system and internal control toward fraud prevention: A study on Indonesian state owned enterprise. International Journal of Business and Technology Management, 2(3), 35–48. . https://myjms.mohe.gov.my/index.php/ijbtm/article/view/10810

- Rezaee, Z., & Wang, J. (2018). Relevance of big data to forensic accounting practice and education. Managerial Auditing Journal, 268–288. https://doi.org/10.1108/MAJ-08-2017-1633

- Robinson, S. N., Robertson, J. C., & Curtis, M. B. (2012). The effects of contextual and wrongdoing attributes on organizational employees’ whistleblowing intentions following fraud. Journal of Business Ethics, 106(2), 213–227. https://doi.org/10.1007/s10551-011-0990-y

- Romadaniati, T., & Nazir, A. (2020). Pengaruh kompetensi aparatur desa, sistem pengendalian internal, dan whistleblowing system terhadap pencegahan fraud pada pemerintah desa dengan moralitas individu sebagai variabel moderasi. Bilancia: Jurnal Ilmiah Akuntansi, 4(3), 227–237. . https://www.ejournal.pelitaindonesia.ac.id/ojs32/index.php/BILANCIA/article/view/734

- Rusmana, O. D., & Tanjung, H. (2019). Identifikasi Kecurangan Laporan Keuangan Dengan Fraud Pentagon Studi Empiris BUMN yang Terdaftar di Bursa Efek Indonesia. Jurnal Ekonomi, Bisnis Dan Akuntansi (JEBA), 21(4). https://doi.org/10.32424/jeba.v21i4.1545

- Ryan, M. (2018). Ethics of public use of AI and Big Data. ORBIT Journal, 2(1). https://doi.org/10.29297/orbit.v2i1.101

- Sadiq, S., & Shyu, M. (2019). Cascaded Propensity Matched Fraud Miner: Detecting Anomalies in Medicare Big Data. Journal of Innovative Technology, 1(1), 51–61. March 2019. https://doi.org/10.29424/JIT.201903_1(1).0007

- Saputra, K. A. K., & Sanjaya, I. K. P. W. (2019). Whistleblowing and tri hita karana to prevent village fund fraud in Bali. International Journal of Religious and Cultural Studies, 1(2), 68–73. https://doi.org/10.34199/ijracs.2019.10.03

- Sari, R., Su’un, M., & Nurwanah, A. (2021). Effect of internal control, whistleblowing role and data asymmetry against fraud prevention. Point of View Research Accounting and Auditing, 2(1), 92–99. https://doi.org/10.47090/povraa.v2i1.118

- Schrand, C. M., & Zechman, S. L. C. (2012). Executive overconfidence and the slippery slope to financial misreporting. Journal of Accounting and Economics, 53(1–2), 311–329. https://dx.doi.org/10.1016/j.jacceco.2011.09.001

- Schuchter, A., & Levi, M. (2015). Beyond the Fraud Triangle: Swiss and Austrian Elite Fraudsters. Accounting Forum, 39(3), 176–187. https://doi.org/10.1016/j.accfor.2014.12.001

- Sepang, F., Gunawan, S., & Pateda, V. (2013). Faktor-faktor yang berhubungan dengan tingkat pengetahuan tentang leukemia anak pada petugas kesehatan puskesmas manado 744. Jurnal E-Biomedik (Ebm), 743–747. https://doi.org/10.35790/ebm.1.1.2013.4629

- Shanmugam, J. K., Ali, A., Hassan, M., & Haat, C. (2012). Internal Control, Risk Management and Fraud Prevention Measures on Smes :Reliability and Validity of Research Instrument, 3rd International conference on business and economic Research, March, 475–494.

- Shapiro, L. W. (1976). A Catalan Triangle. Diwreft Mafhcrndtics Vol. 14 North-tiollmd Publishing Company. 1976) 83 .9rb.63

- Sharma, V. (2016). Importance of Big Data in financial fraud detection. International Journal of Automation and Logistics, 2(4),332. 2016. https://doi.org/10.1504/IJAL.2016.080339

- Shonhadji, N., & Maulidi, A. (2021). The roles of whistleblowing system and fraud awareness as financial statement fraud deterrent. International Journal of Ethics and Systems, 37(3), 370–389. https://doi.org/10.1108/IJOES-09-2020-0140

- Snider, G. L., Chang, L. D., & Hu, E. L. (2016). A self consistent solution of schrocunger-Poisson equations using a nonuniform mesh. 68(October 1990), 4071–4076. https://doi.org/10.1063/1.346245

- Suastawan, I. M. I. D. P., Sujana, E., & Sulindawati, N. L. G. E. (2017). Pengaruh budaya organisasi, proactive fraud audit,dan whistleblowing terhadap pencegahan kecurangan dalam pengelolaan dana bos. e-Journal S1 Ak Universitas Pendidikan Ganesha, 7(1). https://doi.org/10.33086/amj.v6i1.2378

- Sudarma, K. A., Purnamawati, I. G. A., & Herawati, N. T. (2019). Pengaruh persepsi karyawan mengenai budaya kejujuran dan whistleblowing system dalam pencegahan fraud pada PT. BPR Nusamba Kubutambahan. JIMAT (Jurnal Ilmiah Mahasiswa Akuntansi) Undiksha, 10(3), 435–446. https://doi.org/10.23887/jimat.v10i3.22815

- Sujana, I. K., Suardikha, I. M. S., & Laksmi, P. S. P. (2020). Whistleblowing system, competence, morality, and internal control system against fraud prevention on village financial management in denpasar. E-Jurnal Akuntansi, 30(11), 2780. https://doi.org/10.24843/EJA.2020.v30.i11.p06

- Summers, S. L., & Sweeney, J. T. (1998). Fraudulently misstated financial statements and insider trading: An empirical analysis. Accounting Review, 73(1), 131–146. https://www.jstor.org/stable/248345

- Sunaryo, K., Astuti, S., & Zuhrohtun, Z. (2019). The role of risk management and good governance to detect fraud financial reporting. Journal of Contemporary Accounting, 1(1), 38–46. https://doi.org/10.20885/jca.vol1.iss1.art4

- Sundarakantham, K. (2019). Machine Learning Based Intrusion Detection System. 3rd international conference 2019 on trends in electronics and informatics (ICOEI). https://doi.org/10.1109/icoei.2019.8862784

- Taleghani, M., & Mehr, R. R. (2013). The relationship between servant leadership and organizational citizenship behavior in executive organizations of guilan province. Journal of Basic and Applied Scientific Research, 3(1), 910–917.

- Tang, J., & Karim, K. E. (2017). Big data in business analytics: Implications for the audit profession. The CPA Journal, 87(6), 34–39.

- Tang, J., & Karim, K. E. (2019). Financial fraud detection and big data analytics – implications on auditors’ use of fraud brainstorming session. Managerial Auditing Journal, 34(3), 324–337. https://doi.org/10.1108/MAJ-01-2018-1767

- Triantoro, H. D., Utami, I., & Joseph, C. (2020). Whistleblowing system, Machiavellian personality, fraud intention: An experimental study. Journal of Financial Crime, 27(1), 202–216. https://doi.org/10.1108/JFC-01-2019-0003

- Tulus Suryanto, R. R. (2016). The shariah financial accounting standards: How they prevent fraud in Islamic Banking. European Research Studies, XIX(4). https://doi.org/10.35808/ersj/587

- Tunggal, A. W. (2016). Pencegahan dan Pendeteksian Kecurangan. Harvaindo.

- Umimper, R. R., Sompie, B. F., & Sumajouw, M. D. J. (2015). Analisis risiko pada proyek konstruksi perumahan di kabupaten minahasa utara. Jurnal Ilmiah Media Engineering, 5(2). https://ejournal.unsrat.ac.id/index.php/jime/article/view/9966/9552

- Valentine, S., & Godkin, L. (2019). Moral intensity, ethical decision making, and whistleblowing intention. Journal of Business Research, 98, 277–288. https://doi.org/10.1016/j.jbusres.2019.01.009