?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

Given the skyrocketing returns earned by bitcoin, it has received widespread attention as an investment asset. The shocks experienced by stock and bond markets over time and especially during the COVID-19 pandemic has led to an evaluation of bitcoin as a wealth protection asset, a role that gold has played until now. The current paper tests the hedging and safe haven properties of bitcoin in a broad portfolio of both developed and emerging markets stocks, bonds and real estate over a period of 10 years and during COVID-19 pandemic. Using a DCC-GARCH method, the study finds weak hedge and safe haven benefits of bitcoin. The results of the study establish that there is still a long way to go before bitcoin displays a strong safe haven behavior. However, there is a need for portfolio managers to become more cognizant about bitcoin given its potential to protect their portfolios.

1. Introduction

The introduction of bitcoin, in response to the global financial crisis of 2008, revolutionized financial markets across the world. Since its introduction, bitcoin has emerged as the most widely used cryptocurrency, which is both transparent and safe. Coded by Satoshi Nakamoto, an anonymous entity (Nakamoto, Citation2008), bitcoin is an open-source, software-based decentralized digital currency that functions as a peer-to-peer payment system and does not require any intermediary like a bank or a clearinghouse. The growing popularity of bitcoin has fostered various kinds of research on it. Initially, research on bitcoin focused on its properties, operating mechanism and the related safety, regulatory and ethical issues (Dwyer, Citation2014; Yermack, Citation2015). However, post the European sovereign debt crisis of 2010–2013 and the Cypriot banking crisis of 2012–2013, bitcoin became popular because it offered benefits of investment risk management similar to that offered by a traditional asset like gold. Since then, the focus of research on bitcoin shifted to examining the aspects of its volatility, risk spillover (Derbali et al., Citation2021; Gkillas et al., Citation2020; Yousaf & Ali, Citation2021; Zhang et al., Citation2021), trading dynamics (Dwyer, Citation2014; Yermack, Citation2015), market efficiency (Naeem et al., Citation2021; Yaya et al., Citation2020), etc.

Further, the increasing interdependence between various asset classes has necessitated the search of an asset that possesses diversification and risk mitigation properties. Since times, gold has been considered one such protective asset, as gold has been the first form of money, and past evidence suggests that it continues to serve as an inflation hedge (D. G. Baur & Lucey, Citation2010). Additionally, gold has no correlation with other asset classes and this property makes it an important risk hedging tool (Yousaf et al., Citation2021a) especially during any crises (McCown & Zimmerman, Citation2006; Yousaf et al., Citation2021b). In line with this, D. G. Baur and Lucey (Citation2010) and G. D. Baur and McDermott (Citation2010) study the role of gold as a safe haven in financial markets and find that gold acts as a hedge against stocks during normal market conditions and a safe haven in extreme stock market conditions. Recently, bitcoin has been seen as virtual gold (Dyhrberg, Citation2016) as it displays many similarities with gold such as limited supply, no control of supply by centralized authorities and a weak correlation with other asset classes. Various studies have tested the risk mitigation properties of bitcoin and compared this attribute with gold, which is considered a safe haven asset (Baur et al., Citation2018; Bouri, Azzi et al., Citation2017; Bouri et al., Citation2020; Brière et al., Citation2015; Fang et al., Citation2019; Guesmi et al., Citation2019; Ji et al., Citation2018; Majdoub et al., Citation2021; Shahzad et al., Citation2019; Smales, Citation2019; Urquhart & Zhang, Citation2019).

However, the bulk of these studies serve merely to establish a relation between bitcoin and stock markets alone, ignoring a broad portfolio approach to study the risk-mitigating ability of bitcoin. Nevertheless, the majority of portfolio managers tend to invest in a combination of domestic and international markets and a broad set of asset classes comprising both traditional (such as stocks, bonds and currencies) and alternative assets (namely real assets), which helps in eliminating asset-specific risk and minimizing portfolio variance (Bodie & Marcus, Citation2014).

Additionally, past literature well recognizes the dependence of time-series financial asset returns on historical volatilities and return shocks (Bollerslev, Citation1990). While it is important to have an imperfect correlation between assets, the proposition of a constant correlation across time has been rejected by past research (Bera & Kim, Citation2002; Engle, Citation2002). Hence, it is important to account for the time-varying behavior of the connectedness between various asset classes in a portfolio to ensure a dynamic diversification over time. Bouri et al. (Citation2017) also suggest that bitcoin’s diversification, hedge and safe haven ability does not remain constant over time. Hence, it is important to study the time-varying nature of these properties.

In line with the above facts, we take a broad portfolio approach to study the risk mitigation behavior of bitcoin similar to that possessed by gold. Since bitcoin is driven more by enthusiasm than cash flow, hence, when added to a portfolio of a single asset class, say stocks, some risk reduction might occur. However, it is important to understand whether such a property continues to exist when we add bitcoin to a well-diversified portfolio. Such an analysis has never been done, to the best of our knowledge. One of the studies by Brière et al. (Citation2015) evaluates a broad sample of asset classes; however, their study period is based on initial data (2010–2013) when bitcoin was still in its infancy. In addition, this study takes a constant correlation between bitcoin and other asset classes while ignoring the time-varying behavior of bitcoin versus selected asset classes. Furthermore, Eisl et al. (Citation2015) study the diversification ability of bitcoin against a wider variety of asset classes; however, they use a mean variance approach with conditional value-at-risk (CVaR) framework different from a dynamic conditional correlation (DCC) approach used in the current study.

Apart from diversification, another key aspect of strategic asset allocation is protection of the portfolio against inflation since high inflation can have a damaging effect on the portfolio by wiping out the real returns (Chopra et al., Citation2021). Until now, only gold and inflation-linked bonds have been studied for their inflation-hedging properties (Beckmann & Czudaj, Citation2016; Bodie, Citation1988; Chen & Terrien, Citation2001; Hoang et al., Citation2016; Iqbal, Citation2017). Hence, we study the inflation-hedging ability of bitcoin to explore whether bitcoin exhibits gold-like virtue of protecting the real return or not.

Our study intends to bridge the existing gaps and expand the extant literature by examining the diversifier, hedging and safe haven properties of bitcoin across a wider global asset base of traditional assets (stocks, bonds and currencies) and alternative assets (real estate) across varied time horizons (daily and weekly). We use the DCC-GARCH method to examine the time-varying correlation between bitcoin and selected asset classes.

The current study additionally examines the impact of the COVID-19 pandemic on the behavior of bitcoin. The onset of this pandemic caused a significant negative sentiment in the financial markets, leading the investors to search for credible safe havens (Corbet et al., Citation2020). Considering this fact, we specifically investigate the behavior of bitcoin against the selected asset classes during the COVID-19 crisis.

We find that bitcoin possesses weak hedging and safe-haven properties against the selected portfolio of asset classes. These characteristics do not change during the COVID-19 period. However, across the entire time, bitcoin possesses a strong relationship with gold and inflation linked bonds; this relationship becomes even stronger during the COVID-19 period, indicating the inflation-hedging benefits of this virtual currency. Our analysis suggests that, though weak, this virtual currency seems to provide encouraging benefits of portfolio diversification and risk reduction.

The current study is useful for global portfolio managers, crypto traders, individual investors, wealth management professionals and policy-makers in understanding the risk-mitigating properties of bitcoin and making them more mindful towards the benefits of this digital asset class. In order to enable this asset class to bloom fully, all these stakeholders need to become open-minded towards this digital currency.

2. Behaviour of bitcoin as an asset class

The classification of any financial investment as an asset class holds importance from the perspective of strategic asset allocation. We can classify a financial investment as a separate asset class if it is mutually exclusive and diversifying, i.e., it has weak or no correlation with the other asset classes in a portfolio. Such investments are an ideal avenue to park funds during periods of uncertainty or periods of extreme losses in other asset classes like equity, bonds, and commodities (Kaul & Sapp, Citation2007).

An asset class can function as a diversifier, hedge or safe haven in a portfolio. D. G. Baur and Lucey (Citation2010, 219) explicitly defined these three functions of an asset class, based on its correlation with other asset classes, as follows:

“A diversifier is defined as an asset that is positively (but not perfectly correlated) with another asset or portfolio on average.”

“A hedge is defined as an asset that is uncorrelated or negatively correlated with another asset or portfolio on average.”

“A safe haven is defined as an asset that is uncorrelated or negatively correlated with another asset or portfolio in times of market stress or turmoil.”

G. D. Baur and McDermott (Citation2010, 1887) further built on the above definitions to provide a more explicit differentiation between a weak and strong hedge and a weak and strong safe haven property of an asset class as:

“A strong (weak) hedge is defined as an asset that is negatively correlated (uncorrelated) with another asset or portfolio on average.”

“A strong (weak) safe haven is defined as an asset that is negatively correlated (uncorrelated) with another asset or portfolio in certain periods only, e.g., in times of falling stock markets.”

The majority of the studies in the past (Capie et al., Citation2005; G. D. Baur & McDermott, Citation2010; Lucey et al., Citation2004; McCown & Zimmerman, Citation2006; Sherman, Citation1982; Upper, Citation2000) have focused on evaluating the diversifier, hedging and safe haven properties of gold. These works have concluded that gold acts as a hedge and a strong safe haven during periods of extreme market distress. Some researchers have also examined the role of other asset classes as a hedge or safe haven. Kaul and Sapp (Citation2007) consider the US dollar as a safe haven asset and examine the impact of safe haven trading on its liquidity during the Y2K crisis. Ratner and Chiu (Citation2013) examine the hedging and safe haven properties of credit default swaps (CDS) against various sectors of the US stock market. The study finds CDS to be an effective hedge that displays a safe haven property for limited sectors only.

In recent times, bitcoin has emerged as an asset with the ability to provide shelter during any sovereign or financial crisis (Bouri, Azzi et al., Citation2017, Bouri et al., Citation2017; Bouri et al., Citation2020; Majdoub et al., Citation2021; Corbet et al., Citation2020; Conlon et al., Citation2020). A limited number of researchers have evaluated bitcoin as an asset class, and the extant literature has a dearth in terms of evaluating the properties of bitcoin as a risk-mitigating asset against a broad set of asset classes. Among the past studies, few have found bitcoin to be a diversifier due to its weak correlation with traditional assets. Brière et al. (Citation2015) study the diversifying properties of bitcoin in the United States during its early stage of introduction, i.e., 2010–2013, and find that even a small weightage given to bitcoin can significantly reduce the risk-return profile of a well-diversified portfolio. Bouri et al. (Citation2017) further evaluate the data of US firms for the period 2011–2015 and report continued suitability of bitcoin for diversification purposes. Hatemi-J et al. (Citation2021) study a portfolio of bitcoin and a few other assets viz. bonds, equities and US dollar to demonstrate that the diversification benefits of bitcoin become evident only if investors combine risk and return to construct an optimum portfolio of these asset classes. Mokni et al. (Citation2020) study a portfolio of bitcoin and US stocks and observe that economic policy uncertainty (EPU) is an important consideration in deciding on asset allocation and hedging strategies of this portfolio.

Further, a number of researchers examine bitcoin’s capabilities to act as a hedge and safe haven against equity as well as other asset classes. Dyhrberg (Citation2016) find that bitcoin has the explicit potential to act as a hedge against stocks at the FTSE Index. He further shows a short-term hedging capability of bitcoin against the US dollar also. Bouri, Azzi et al. (Citation2017), on the other hand, study the dynamic correlation of bitcoin versus energy commodities. They find that bitcoin acts as a hedge as well as a safe haven against movements in both commodity indices during the pre-crash period of bitcoin (2013), while it plays a role of only a diversifier during the post-crash period. Stensas et al. (Citation2019) evaluate the role of bitcoin in various developed and developing markets. The study finds that bitcoin plays the role of a hedge in developing markets, while it works as a diversifier in developed markets as well as for commodities. Additionally, during periods of global turmoil, bitcoin also exhibit the properties of a safe haven. Wu et al. (Citation2019) study the hedge and safe haven properties of bitcoin during economic policy uncertainty (EPU). They find bitcoin to be more stable as a hedge and safe haven as compared to gold during EPU shocks. Derbali et al. (Citation2020a) find bitcoin to have low correlation and hence diversification benefits against energy commodities. However, Derbali et al. (Citation2020b) find significant dynamic conditional correlation between bitcoin and energy commodities when Fed and ECB monetary policy surprises are accounted for, which they interpret as an indicator of financialization of bitcoin and commodity markets. Bouri et al. (Citation2020) study the safe haven properties of bitcoin along with gold and commodities in developed as well as emerging markets. They find that bitcoin remained superior to gold and commodities, although the benefits of its diversification varied over time-frequency space.

The emergence of COVID-19 has given a new challenge to portfolio managers in terms of maintaining the value of their portfolio. This has brought forward an increasing interest in bitcoin as this asset can offer a new avenue to park funds during times of stress in other asset classes. Corbet et al. (Citation2020) find that bitcoin not only provides diversification benefits, but also acts as a safe haven like gold during the COVID-19 crisis. Derbali et al. (Citation2021) also find a significant association between bitcoin and gold due to COVID-19 news in the USA and China, proving the financialization of bitcoin and gold. Further, Yousaf and Ali (Citation2021) find bitcoin to be a diversifier for oil market during the COVID-19 period. On the contrary, Conlon et al. (Citation2020) find that bitcoin and Ethereum (another popular virtual currency) do not act as safe havens for majority stock indices during the COVID-19 market turmoil. Yousaf and Yarovaya (Citation2022) also find no significant volatility transmission between bitcoin and S&P500 during the COVID-19 period.

As mentioned before, most studies so far have been majorly focused on the relationship between bitcoin and single asset (stocks) portfolio. To take the existing research forward, we study the diversification, hedging and safe haven benefits of bitcoin against a broad portfolio of traditional and alternative asset classes from the perspective of a global portfolio manager.

3. Methodology

3.1. Data

The data consists of daily and weekly prices of bitcoin and various financial asset classes against which the hedging and safe haven abilities of bitcoin have been tested. We here consider the strategy of a passive portfolio manager who holds a diversified portfolio of traditional and alternative assets. We ignore the case of active stock selection and hence transaction costs, which if considered can result in increased complexity of return computation, given the presence of costs of active management. The purpose of selecting broad asset classes is to check diversification and risk-reduction ability of bitcoin, when added to an already well-diversified portfolio. These asset classes include traditional assets viz., stocks, bonds currencies and alternative investments, i.e., real estate. In light of this, we select various liquid financial indices to represent each asset class. These include MSCI World Index (developed economies equity markets), MSCI Emerging Markets Index (emerging economies equity markets), Bloomberg corporate bond index (global corporate bonds), FTSE world government bond index (developed economies government bonds), JP Morgan emerging economies bonds (emerging economies government bonds), Euro to Dollar spot rate (euro currency), Yen to Dollar spot rate (yen currency) and FTSE Nareit Index (global real estate). The proxy for bitcoin prices is the bitcoin-US dollar exchange rate. Additionally, the inflation hedging properties of bitcoin are tested against inflation-linked bonds (ILBs) and gold. For this purpose, the current study uses Bloomberg Global Inflation Linked Bond Index and Gold Bullion Security Index. The returns of all the indices (total return indices in US dollar) are obtained from the Bloomberg database for the period ranging from 17 July 2010 (first day of bitcoin trading) to 10 March 2021. Each time series comprises 2777 daily observations and 554 weekly observations. For COVID-19 period, we consider data from 1 January 2020 until 10 March 2021 as the COVID-19 was first reported by Wuhan, China, to the WHO on 31 December 2019.

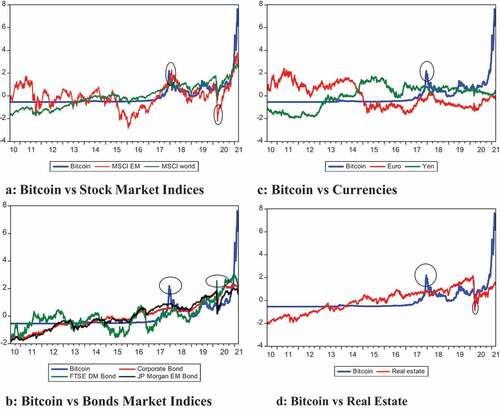

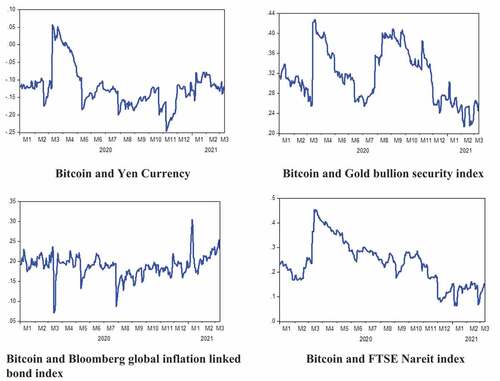

Figure shows plots of normalized historical prices of bitcoin with other asset classes. Bitcoin prices have risen post 2017, and there has been a phenomenal increase in prices of bitcoin during 2020, i.e., the COVID-19 period. This is indicative of the fact that the pandemic generated a significant investor interest in this virtual currency. Tables present the descriptive statistics for daily and weekly returns data for the complete period and daily returns data for the COVID-19 period for bitcoin and selected asset classes viz. stocks, bonds, currencies and real estate. Bitcoin has the highest daily standard deviation across all daily, weekly as well as COVID period data. This property of bitcoin seems similar to its counterpart gold, which, despite its potential safe haven properties, has been found to be riskier than stocks and bonds (D. G. Baur & Lucey, Citation2010). The kurtosis of bitcoin is lower than that of some other asset classes. It must be observed here that in the case of daily and weekly series bitcoin exhibits a positive skewness, which indicates a positive signal for an investor with a probability to offset frequent small losses with large gains.

Figure 1. Performance of bitcoin versus selected asset classes. A bitcoin vs stock market indices. B Bitcoin vs Bonds Market Indices. C Bitcoin vs Currencies. D Bitcoin vs Real Estate.

Table 1. Summary Statistics for daily data for the complete period

Table 2. Summary Statistics for weekly data for the complete period

Table 3. Summary Statistics for daily data for the Covid-19 period

3.2. Empirical Model

It has been widely known that correlation between returns of assets is an important input to determine their hedging properties (Engle, Citation2002). Past volatilities and return shocks drive the returns of these assets (Bollerslev, Citation1990). As a result, many researchers in the past have tried to investigate techniques that can result in reliable estimates of correlation coefficients between investment returns. The simplest methods have been rolling regression and exponential smoothing. However, rolling window estimation is based on the key assumption that the model parameters remain constant over time (Zivot & Wang, Citation2003). Hence, if the parameters change (as in the case of investment returns), this technique does not capture their instability over time. An Exponentially Weighted Moving Average (EWMA) removes this problem to an extent by assigning higher weights to recent return values; however, it does not provide a total solution of an adequate estimate of volatility due to fixed weight of parameters (Ratner & Chiu, Citation2013). A constant correlation model similarly assumes the correlations to be constant over time and ignores nonlinear dependence. These techniques fail to take into account the timing or the nature of possible changes in the correlation between time series. As compared to the above methods, a dynamic conditional correlation (DCC) takes into account time-varying volatility and detects the data-dependent changes in conditional correlation over time (Lee, Citation2006). DCC is a technique given by Engle (Citation2002) who proposed it as a model that has the flexibility of univariate GARCH without the complexity of multivariate GARCH. Ratner and Chiu (Citation2013), Bouri et al. (Citation2017) Stensas et al. (Citation2019) and Majdoub et al. (Citation2021) have also used the DCC model to determine the hedging effectiveness and safe haven properties of various asset classes.

Following Ratner and Chiu (Citation2013) and Yousaf and Ali (Citation2021), we use DCC-GARCH to produce time-varying estimates of conditional co-movement between assets implemented as given below:

Here is the k × 1 demeaned vector of variables, which is assumed to be the conditionally multivariate normal and is conditional on information

.

is the covariance matrix,

is the k × k diagonal matrix of conditional standardized residuals calculated using univariate GARCH models and

is the k × k time-varying correlation matrix. The likelihood function of the estimator has the general form of the equation given below:

This process has two variable steps. In the first step, the volatility component is maximised by replacing

with a k × k identity matrix. As a result, the log likelihood is reduced to the sums of log likelihoods of the univariate GARCH equations. The Glosten et al. (Citation1993) model is used to estimate first-order univariate GARCH models for bitcoin and each asset class, represented by an index, after allowing for asymmetries:

where is the conditional variance,

is the asymmetry term and

= 1 if

< 0 else I = 0.

In the second step, the , the correlation component is maximized:

where the DCC parameters α and β are provided with their values. When both α and β are zero, changes to

, indicating that the constant correlation model is suitable.

Subsequent to the GARCH estimation, the time varying correlations are derived from model (5) into a separate time series for each asset class. To assess bitcoin as a hedge and safe haven against various asset classes,

are regressed on dummy variables that reflect market turmoil.

Where represents the dynamic conditional correlation between bitcoin and an asset class. The variables

qn represent the returns at the 10%, 5% and 1% quantile, while D denotes the dummy variable that captures extreme swings in the underlying asset classes at the 10%, 5% and 1% quantiles (

qn) of the most negative returns of each asset class, respectively. If

is zero for the specific asset class, bitcoin is a weak hedge; if

is negative, bitcoin is a strong hedge. If

,

, or

coefficients are insignificantly different from zero, bitcoin is a weak safe haven; if they are negative, bitcoin is a strong safe haven.

4. Results

4.1. Dynamic correlation between bitcoin and other asset classes

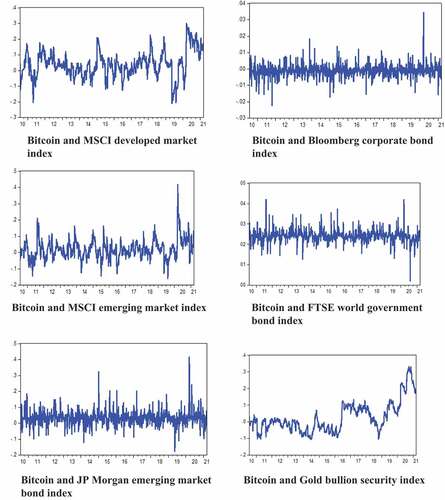

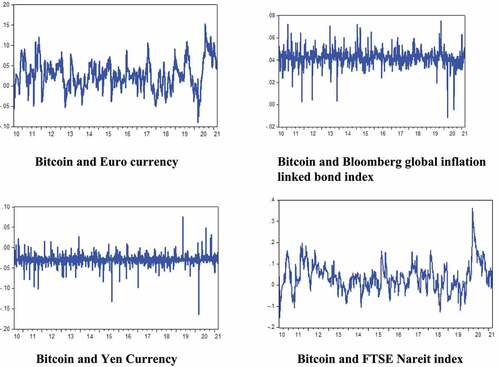

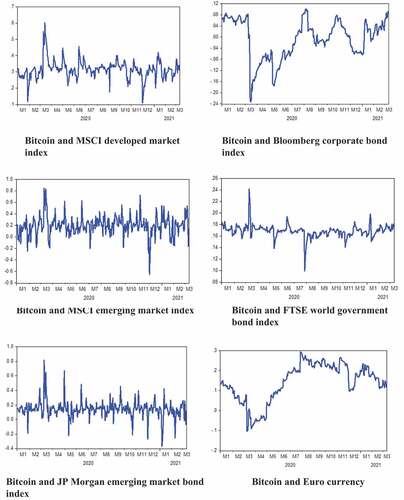

Before evaluating the hedging and safe haven properties of bitcoin in the context of a portfolio, we first assess the time-varying correlation between bitcoin and individual asset classes. For this purpose, we consider three periods—the entire study period, pre-COVID-19 period and COVID-19 period. Table presents the mean DCC coefficient of bitcoin with each asset class for all three periods. When checked individually, each asset class shows a positive but a very low mean correlation with bitcoin except in the case of corporate bonds and Yen, where these coefficients are negative during the entire study period, pre-COVID-19 period and COVID-19 period. The DCC coefficients of corporate bonds and Yen currency, in fact, become more negative during the COVID-19 period, indicating a better hedging ability of bitcoin against these two assets during this pandemic. The table also exhibits that there is a significant difference between the mean DCC coefficients of the pre-COVID-19 and the COVID-19 period as indicated by t-values (significant at 1%). Additionally, the correlation between bitcoin and other asset classes becomes significantly high during the COVID-19 period versus the pre-COVID-19 period, demonstrating a contagion effect between bitcoin and the selected asset classes viz. stocks, bonds, currency and real estate. Figures present the DCC coefficients of bitcoin and the selected asset classes for the entire study period and during COVID-19 period, respectively. The DCC coefficients between bitcoin and all other selected asset classes remain low or negative during the entire period except for gold and ILBs, where it hovers in a positive territory. This positive correlation with gold is low till 2018, but it rises sharply afterwards. During COVID-19 period, this dynamic correlation of bitcoin with most of the selected assets becomes higher and this increase is the highest in the case of gold and ILBs. However, in the case of Yen currency and corporate bonds the DCC coefficients show a steep negative trend during COVID-19 period. These preliminary findings lay down the ground for a detailed analysis of hedging and safe haven properties of bitcoin.

Table 4. DCC coefficient of bitcoin versus other asset classes

Figure 2. Dynamic correlations between bitcoin and the selected assets during the complete period (17 July 2010 to 10 March 2021).

Figure 2. (continued).

Figure 3. Dynamic correlations between bitcoin and other assets during Covid-19 period (1 January 2020 to 10 March 2021).

Figure 3. (continued).

4.2. Hedge and safe haven analysis of bitcoin

Table presents the estimation results of the GARCH dynamic conditional correlation (DCC) model as stated in Equationequation (6)(6)

(6) using daily data. The DCC coefficients (Ct) are regressed on a constant and three dummy variables, which represent the extreme volatility quantiles, viz., 1%, 5% and 10% of the asset classes under consideration. The C0 coefficients in the “Hedge” column indicate a negative relationship in the case of MSCI Emerging Market Index (−0.0805), Global Corporate Bond Index (−0.5968), Emerging Markets Government Bond Index (−0.4841), Euro currency (−0.0744), Yen currency (−0.1307) and real estate (−0.0529). However, the coefficients are insignificant in all these cases. This indicates that bitcoin acts as a weak hedge against risk in these asset classes. In the case of MSCI Developed Market Index and Developed Market Government Bonds Index, bitcoin acts as a weak diversifier (insignificantly positive C0, i.e., .0.4977 and 0.8290, respectively). These results are similar to the studies conducted by Brière et al. (Citation2015) and Eisl et al. (Citation2015), which find that bitcoin improves diversification when added to a well-diversified portfolio. Additionally, Dyhrberg (Citation2016) proposes that bitcoin can be used as a hedge against the UK equities and the US dollar. Hence, bitcoin can be added to the list of traditional assets like gold as a hedge to minimize portfolio risks (Bouri et al., Citation2020; Dyhrberg, Citation2016)

Table 5. DCC-GARCH: Bitcoin as a hedge and safe haven against global traditional and alternative asset classes using daily data

The quantile regression coefficients (C1, C2, and C3) represent the safe haven characteristics of bitcoin against the risk of the chosen asset classes. It has been observed that bitcoin acts as a strong safe haven only for Developed Market Government Bond Index in the 10% quantile (−2.2986) at 10% level of significance. Bitcoin functions as a weak safe haven in all quintiles, i.e., 1%, 5% and 10% for all the remaining asset classes except for MSCI Developed Market Index, where it shows the properties of a weak safe haven only in the 5% and 10% quantiles (with C2 and C3 being −0.2198 and −0.0344, respectively). This is indicated by insignificant positive or negative coefficients in these quintiles.

The results pertaining to weekly data (presented in Table ) are qualitatively similar to those of daily data and show that bitcoin acts as a weak hedge for all asset classes except for MSCI Developed Market Index, Developed Market Government Bond Index and Emerging Market Government Bond Index. Additionally, it continues to exhibit a weak safe haven property with all asset classes across all three quantiles. Our results find support from various studies done in the past. Bouri et al. (Citation2017) find that bitcoin can serve as a strong safe haven against weekly extreme down movements in Asian stocks. Baur et al. (Citation2018) find hedging and safe haven properties of bitcoin across varying time horizons. Additionally, Brière et al. (Citation2015), Bouri et al. (2019), Bouri et al. (Citation2017), Adrianto and Diputra (Citation2017), Guesmi et al. (Citation2019), and Kajtazi and Moro (Citation2019) highlight the risk-reduction benefits of bitcoin investment against various asset classes viz. developed market equities, investment-grade bonds, US dollar, commodities, ETFs, real estate and alternative investments.

Table 6. DCC-GARCH: Bitcoin as a hedge and safe haven against global traditional and alternative asset classes using weekly data

Table shows the results of hedge and safe haven properties of bitcoin from January 2020 till March 2021, a period when major financial markets were hit by the COVID-19 crises. During this period, bitcoin becomes a strong hedge against emerging market bonds where the coefficient C0 (−1.6392) is significantly negative at 5% level of significance. Bitcoin acts as a weak hedge against global corporate bonds, the Yen and real estate. In the case of the Euro, a small and positive coefficient (C0 being 0.0084), significant at 1% shows strong diversification properties of bitcoin while for MSCI Emerging Market Index, bitcoin functions as a weak diversifier (insignificantly positive C0 coefficient). The results of safe haven properties of bitcoin during the COVID-19 period are consistent with the previous cases of daily and weekly data. This confirms the weak safe haven properties of bitcoin across all asset classes in the majority quintiles with the exception of developed market government bonds where bitcoin came out as a strong safe haven in the 10% quintile (−4.5223) at 10% level of significance. However, in the case of 5% quantile of developed market bonds and 1% quantile of Yen, bitcoin does not show any safe haven property. Our results are in accordance with Conlon et al. (Citation2020) who does not find a safe haven property of bitcoin for major international equity investors except for China where the cryptocurrency provided modest downside risk benefits. In contrast, Corbet et al. (Citation2020) find evidence of cryptocurrencies, including bitcoin, to act as a store of value during the COVID-19 period. Although the returns of cryptocurrencies are significantly affected by negative sentiment, these digital currencies still provide diversification as well as safe haven benefits during the pandemic period similar to that done by precious metals. Hence, there is mixed evidence in the literature regarding the risk reduction benefits of bitcoin during COVID-19.

Table 7. DCC-GARCH: Bitcoin as a hedge and safe haven against global traditional and alternative asset classes using daily data during Covid-19 period

Our study shows that the overall response of bitcoin as a hedge and safe haven against various asset classes is similar for daily and weekly data over the complete data period as well as during the COVID-19 period. Across all these frequencies, bitcoin largely displays weak hedge and weak safe haven properties. These results may be due to the limited trading history of bitcoin versus the other asset classes like gold (D. G. Baur & Lucey, Citation2010), where more than two centuries of data are available. A lack of regulatory acceptance of bitcoin along with the presence of a limited number of traders whose trades are largely driven by enthusiasm rather than portfolio management objectives may also result in the failure of bitcoin to act as a strong safe haven.

In order to check the inflation hedging properties of bitcoin, we conduct a DCC-GARCH between daily and weekly returns of bitcoin, gold and ILBs. The same is also done for daily returns of these assets during the COVID-19 period. The results show a significant positive correlation between bitcoin and gold as well as bitcoin and ILB, across both daily and weekly frequencies. The coefficients of bitcoin’s relationship with gold and ILB are stronger for daily returns during COVID-19 period than the entire period under consideration. Gold and ILBs have proven themselves to be inflation hedges in the past (Andonov et al., Citation2010; Bampinas & Panagiotidis, Citation2015; Chen & Terrien, Citation2001; Ghosh et al., Citation2004; Gracia & Rixtel, Citation2007; Worthington & Pahlavani, Citation2007). Any asset that has a positive relationship with these two asset classes will also have similar properties of insulating a portfolio against inflation. The results in Table show that bitcoin acts as a strong inflation hedge with gold and ILB and the strength of this association has been higher during the COVID-19 period. This evidence is in line with the findings of European Central Bank (ECB; Citation2012) and Harper (Citation2013), who point out the limited supply of bitcoin as the underlying reason for its inflation-hedging properties. These results can also support the view of bitcoin being virtual gold (Dyhrberg, Citation2016).

Table 8. DCC-GARCH: Bitcoin vs gold and ILB

5. Conclusion and implications

Financial innovations have been associated with bubble-like features (Frehen et al., Citation2013) and, hence, it may take some time for bitcoin to establish its stability. Previous studies on hedging and safe haven properties of bitcoin (Brière et al., Citation2015) have been conducted at quite an early stage of evolution of this virtual currency. Studies done earlier may have shown bitcoin to be a hedge and safe haven (Brière et al., Citation2015; Dyhrberg, Citation2016, Bouri et al., Citation2017; Bouri et al., Citation2020) but the majority of them advise to take the results with caution as bitcoin is an evolving asset class and trading data history is still limited. Additionally, recent research (Bouri et al., Citation2020; Majdoub et al., Citation2021) has focused on testing these properties of bitcoin against stocks, which are the most common asset class in an investor’s portfolio. Taking the same research forward, the current study examines the hedging and safe haven properties of bitcoin spanning a longer data period that also includes the exceptional event of the COVID-19 pandemic, which started from the real sector but made its way to the financial sector. Additionally, the study takes into consideration a wide variety of traditional asset classes, viz., developed and emerging market stocks, developed and emerging market bonds, corporate bonds, currencies as well as an alternative asset class, viz., real estate. This fills the previous gap by evaluating the investment characteristics of bitcoin against a broad portfolio of eight asset classes. The hedging capability of bitcoin can be crucial in improving the risk profile of such a portfolio and maximizing the diversification effect. On the other hand, the safe haven property can act as a wealth preserver as well as provider of liquidity in distress situations.

Examining both these characteristics against the selected eight asset classes lends support to the proposition of bitcoin having hedging and safe haven properties against a portfolio of a wide variety of asset classes. The findings of the current study suggest that bitcoin acts as a diversifier, hedge and safe haven against various asset classes over both daily and weekly data periods as well as during the COVID-19 period. However, all these characteristics of bitcoin are mixed and are in weak form.

The study of risk mitigation properties of bitcoin in the current paper has several implications for crypto traders, policy-makers as well as investors. Crypto traders face a risk of high volatility and hence increased probability of crashes in bitcoin. The results of the current study can be useful for crypto traders in understanding the correlation between bitcoin and other asset classes, particularly currencies like Yen and Euro, and accordingly use the co-movements as an indicator for predicting future trends in the bitcoin market. In view of the findings of this study, policymakers can think of reducing the curbs on this virtual currency. The findings can be considered as supporting evidence for regulators and governments who seek to make bitcoin either as an official cryptocurrency or include it as a part of their forex reserves (Zhang et al., Citation2021). The findings also give an insight to policymakers on the impact of policy uncertainty on crypto assets in influencing financial market stability given the correlation of this cryptocurrency with other asset classes. The study has useful implications for portfolio managers in the design and implementation of portfolio management strategies where bitcoin can offer additional advantage to the already existing rich list of hedging tools and improve the portfolio risk-return characteristics.

As stated before, bitcoin, though a most promising asset in current times, is subject to various restrictions. The investor class associated with this asset is more interested in its skyrocketing returns rather than using it as a risk hedge. Portfolio managers with various restrictions related to maintaining client wealth do not still have the confidence to put their clients’ money in this asset class. Further, there are no virtual currency-specific funds still available in the market due to the lack of well-defined regulatory mechanisms. However, the results obtained by the current study are encouraging and point towards a promising future for bitcoin. It must be noted that as bitcoin is not regulated by any central authority, it remains insulated from economic shocks. This can also make it less prone to financial market shocks in these economies. Additionally, this high-speed virtual currency is not subject to devaluation by any government action. It is free, independent, traded continuously and purely investor driven. Given the increasing popularity of this digital currency, the results indicate that it will appear as an asset class that can prove to be a strong safeguard against major market downside. Overall, portfolio managers need to become more cognizant of bitcoin as a hedging and portfolio protection tool.

With still a long way to go in terms of getting on par with gold, there is scope for evolving research in this asset class. Besides an empirical investigation, any data from the primary view of portfolio managers, high net worth individuals, regulators crypto traders and active retail investors from multiple geographies can add a lot of value to the behavioral aspects of investment in this virtual currency. The key to developing a conclusive investment strategy in bitcoin is the availability of data. Bitcoin’s golden constant behavior is difficult to prove given the limited data available as compared to gold that has centuries of data. Additionally, there has been an emergence of new asset classes such as non-fungible tokens (NFT) and decentralized finance (DeFi). Yousaf and Yarovaya (Citation2022) study the role of bitcoin with other assets like NFTs and Defis. They suggest adding of newer assets along with bitcoin to the portfolio for achieving diversification benefits.

With more data for bitcoin coming in, the impact of COVID-19 getting clearer, and the emergence of new digital asset classes, future research can take this idea forward so that the investment community becomes clearer and more confident about the role of bitcoin and other cryptocurrencies before adding them to their portfolios.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

References

- Adrianto, Y., & Diputra, Y. (2017). The effect of cryptocurrency on investment portfolio effectiveness. Journal of Finance and Accounting, 5(6), 229–21. https://doi.org/10.11648/j.jfa.20170506.14

- Andonov, A., Bardong, F., & Lehnert, T. (2010). TIPS, inflation expectations, and the financial crisis. Financial Analysts Journal, 66(6), 1–13. https://doi.org/10.2469/faj.v66.n6.1

- Bampinas, G., & Panagiotidis, T. (2015). Are gold and silver a hedge against inflation? A two century perspective. International Review of Financial Analysis, 41, 267–276. https://doi.org/10.1016/j.irfa.2015.02.007

- Baur, D. G., Hong, K., & Lee, A. D. (2018). Bitcoin: Medium of exchange or speculative assets? Journal of International Financial Markets Institutions and Money, 54, 177–189. https://doi.org/10.1016/j.intfin.2017.12.004

- Baur, D. G., & Lucey, B. (2010). Is gold a hedge or a safe haven? An analysis of stocks, bonds, and gold. The Financial Review, 45(2), 217–229. https://doi.org/10.1111/j.1540-6288.2010.00244.x

- Baur, G. D., & McDermott, T. K. (2010). Is gold a safe haven? International evidence. Journal of Banking & Finance, 34(8), 1886–1898. https://doi.org/10.1016/j.jbankfin.2009.12.008

- Beckmann, J., & Czudaj, R. (2016). Gold as an inflation hedge in a time-varying coefficient framework. The North American Journal of Economics and Finance, 24, 208–222. https://doi.org/10.1016/j.najef.2012.10.007

- Bera, A., & Kim, S. (2002). Testing constancy of correlation and other specifications of the BGARCH model with an application to international equity returns. Journal of Empirical Finance, 9(2), 171–195. https://doi.org/10.1016/S0927-5398(01)00050-0

- Bodie, Z. (1988). Inflation, index-linked bonds and asset allocation. Journal of Portfolio Management, 16(2), 48–53. https://doi.org/10.3905/jpm.1990.409260

- Bodie, Z. A. K., & Marcus, A. J. (2014). Investments (10th) ed.). McGraw-Hill Education.

- Bollerslev, T. (1990). Modeling the coherence in short-run nominal exchange rates: A multivariate generalized ARCH model. The Review of Economics and Statistics, 72(3), 498–505. https://doi.org/10.2307/2109358

- Bouri, E., Azzi, G., & Dyhrberg, A. H. (2017). On the return-volatility relationship in the Bitcoin market around the price crash of 2013. Economics: The Open-Access, Open-Assessment E-Journal, 11(2), 1–16. http://dx.doi.org/10.5018/economics-ejournal.ja.2017-2

- Bouri, E., Molnar, P., Azzi, G., Roubaud, D., & Hagfors, L. I. (2017). On the hedge and safe haven properties of Bitcoin: Is it really more than a diversifier? Finance Research Letters, 20, 192–198. https://doi.org/10.1016/j.frl.2016.09.025

- Bouri, E., Shahzad, S. J. H., Roubaud, D., Kristoufek, L., & Lucey, B. (2020). Bitcoin, gold, and commodities as safe havens for stocks: New insight through wavelet analysis. The Quarterly Review of Economics and Finance, 77(C), 56–164. https://doi.org/10.1016/j.qref.2020.03.004

- Brière, M., Oosterlinck, K., & Szafarz, A. (2015). Virtual currency, tangible return: Portfolio diversification with bitcoin. Journal of Asset Management, 16(6), 365–373. https://doi.org/10.1057/jam.2015.5

- Capie, F., Mills, T. C., & Wood, G. (2005). Gold as a hedge against the dollar. Journal of International Financial Markets, Institutions and Money, 15(4), 343–352. https://doi.org/10.1016/j.intfin.2004.07.002

- Chen, P., & Terrien, M. (2001). TIPS as an asset class. Journal of Investing, 10(2), 73–81. https://doi.org/10.3905/joi.2001.319464

- Chopra, M. C., Srivastava, A., & Mehta, C. (2021). Inflation-linked bonds as a separate asset class: Evidence from emerging and developed markets. Global Business Review, 22(1), 219–235. https://doi.org/10.1177/0972150918807015

- Conlon, T., Corbet, S., & McGee, J. R. (2020). Are cryptocurrencies a safe haven for equity markets? An international perspective from the COVID-19 pandemic. Research in International Business and Finance, 54, 101248. https://doi.org/10.1016/j.ribaf.2020.101248

- Corbet, S., Hou, G. Y., Hu, Y., Larkin, C., & Oxley, L. (2020). Any port in a storm: Cryptocurrency safe havens during the COVID-19 pandemic. Economics Letters, 194, 109377. https://doi.org/10.1016/j.econlet.2020.109377

- Derbali, A., Jamel, L., Ltaifa, M. B., & Elnagar, A. K. (2020b). Return, volatility and shock spillovers of bitcoin with energy commodities. International Journal of Finance, Insurance and Risk Management, 4(3), 157–170. https://doi.org/10.35808/ijfirm/228

- Derbali, A., Jamel, L., Ltaifa, M. B., Elnagar, A. K., & Lamouchi, A. (2020a). Fed and ECB: Which is informative in determining the DCC between bitcoin and energy commodities? Journal of Capital Markets Studies, 4(1), 77–102. https://doi.org/10.1108/JCMS-07-2020-0022

- Derbali, A., Naoui, K., & Jamel, L. (2021). COVID-19 news in USA and in China: Which is suitable in explaining the nexus among Bitcoin and Gold? Pacific Accounting Review, 33(5), 578–595. https://doi.org/10.1108/PAR-09-2020-0170

- Dwyer, G. P. (2014). The economics of Bitcoin and similar private digital currencies. Journal of Financial Stability, 17, 81–91. https://doi.org/10.1016/j.jfs.2014.11.006

- Dyhrberg, A. H. (2016). Hedging capabilities of bitcoin. Is it the virtual gold? Finance Research Letters, 16, 139–144. https://doi.org/10.1016/j.frl.2015.10.025

- Eisl, A., Gasser, S. M., & Weinmayer, K. (2015). Caveat emptor: Does bitcoin improve portfolio diversification? SSRN Electronic Journal. https://doi.org/10.2139/ssrn.2408997

- Engle, R. F. (2002). Dynamic conditional correlation: A simple class of multivariate generalized autoregressive conditional heteroscedasticity models. Journal of Business & Economic Statistics, 20(3), 339–350. https://doi.org/10.1198/073500102288618487

- European Central Bank (ECB). (2012). Virtual currency schemes. http://www.ecb.int/pub/pdf/other/virtualcurrencyschemes201210en.pdf accessed 26 July 2013

- Fang, L., Bouri, E., Gupta, R., & Roubaud, D. (2019). Does global economic uncertainty matter for the volatility and hedging effectiveness of Bitcoin? International Review of Financial Analysis, 61, 29–36. https://doi.org/10.1016/j.irfa.2018.12.010

- Frehen, R., Goetzmann, G. P., N, W., & Rouwenhorst, K. G. (2013). New evidence on the first financial bubble. Journal of Financial Economics, 108(3), 585–607. https://doi.org/10.1016/j.jfineco.2012.12.008

- Ghosh, D., Levin, E. J., Macmillan, P., & Wright, R. E. (2004). Gold as an inflation hedge? Studies in Economics and Finance, 22(1), 1–25. https://doi.org/10.1108/eb043380

- Gkillas, K., Bouri, E., Gupta, R., & Roubaud, D. (2020). Spillovers in higher-order moments of crude oil, gold and bitcoin. The Quarterly Review of Economics and Finance. https://doi.org/10.1016/j.qref.2020.08.004

- Glosten, L., Jagannathan, R., & Runkle, D. (1993). On the relation between the expected value and the volatility of the nominal excess return on stocks. Journal of Finance, 48(5), 1779–1801. https://doi.org/10.1111/j.1540-6261.1993.tb05128.x

- Gracia, J. A., & Rixtel, A. V. (2007). Inflation-linked bonds from a central bank perspective. European Central Bank Occasional Paper Series No. 62. https://www.ecb.europa.eu/pub/pdf/scpops/ecbocp62.pdf?6805d5ee66586d2efad88494ba01012c

- Guesmi, K., Saadi, S., Abid, I., & Ftiti, Z. (2019). Portfolio diversification with virtual currency: Evidence from bitcoin. International Review of Financial Analysis, 63, 431–437. https://doi.org/10.1016/j.irfa.2018.03.004

- Harper, J. (2013). What is the value of bitcoin? Cato Institute. http://www.cato.org/blog/what-value-bitcoin

- Hatemi-J, A., Hajji, M. A., Bouri, E., & Gupta, R. (2021). The benefits of diversification between bitcoin, bonds, equities and the US dollar: A matter of portfolio construction. Asia-Pacific Journal of Operational Research. https://doi.org/10.1142/S0217595920400242

- Hoang, T., V, H., Lahiani, A., & Heller, D. (2016). Is gold a hedge against inflation? New evidence from a nonlinear ARDL approach. Economic Modelling, 54, 54–66. https://doi.org/10.1016/j.econmod.2015.12.013

- Iqbal, J. (2017). Does gold hedge stock market, inflation and exchange rate risks? An econometric investigation. International Review of Economics & Finance, 48, 1–17. https://doi.org/10.1016/j.iref.2016.11.005

- Ji, Q., Bouri, E., Gupta, R., & Roubaud, D. (2018). Network causality structures among Bitcoin and other financial assets: A directed acyclic graph approach. The Quarterly Review of Economics and Finance, 70, 203–213. https://doi.org/10.1016/j.qref.2018.05.016

- Kajtazi, A., & Moro, A. (2019). The role of bitcoin in well diversified portfolios: A comparative global study. International Review of Financial Analysis, 61(C), 143–157. https://doi.org/10.1016/j.irfa.2018.10.003

- Kaul, A., & Sapp, S. (2007). Y2K fears and safe haven trading of the U.S. dollar. Journal of International Money and Finance, 25(5), 760–779. https://doi.org/10.1016/j.jimonfin.2006.04.003

- Lee, J. (2006). The comovement between output and prices: Evidence from a dynamic conditional correlation GARCH model. Economics Letters, 91(1), 110–116. https://doi.org/10.1371/journal.pone.0123923

- Lucey, B. M., Poti, V., & Tully, E. (2004). International portfolio formation, skewness and the role of gold. https://www.tcd.ie/triss/assets/PDFs/iiis/iiisdp30.pdf

- Majdoub, J., Sassi, B. S., & Bejaoui, A. (2021). Can fiat currencies really hedge Bitcoin? Evidence from dynamic short‑term perspective. Decisions in Economics and Finance, 44(2), 789–816. https://doi.org/10.1007/s10203-020-00314-7

- McCown, J. R., & Zimmerman, J. R. (2006). Is gold a zero-beta asset? Analysis of the investment potential of precious metals. https://papers.ssrn.com/sol3/papers.cfm?Abstract_id=920496

- Mokni, K., Ajmi, A. N., Bouri, E., & Vinh Vo, X. (2020). Economic policy uncertainty and the Bitcoin-US stock nexus. Journal of Multinational Financial Management, 57–58, 100656. https://doi.org/10.1016/j.mulfin.2020.100656

- Naeem, M. A., Bouri, E., Peng, Z., Shahzad, S. J. H., & Vinh Vo, X. (2021). Asymmetric efficiency of cryptocurrencies during COVID19. Physica A, 565, 125562. https://doi.org/10.1016/j.physa.2020.125562

- Nakamoto, S. (2008). Bitcoin: A peer-to-peer electronic cash system. http://pdos.csail.mit.edu/6.824/papers/bitcoin.pdf.

- Ratner, M., & Chiu, J. C. C. (2013). Hedging stock sector risk with credit default swaps. International Review of Financial Analysis, 30, 18–25. https://doi.org/10.1016/j.irfa.2013.05.001

- Shahzad, S. J. H., Bouri, E., Roubaud, D., Kristoufek, L., & Lucey, B. (2019). Is bitcoin a better safe haven investment than gold and commodities? International Review of Financial Analysis, 63, 322–330. https://doi.org/10.1016/j.irfa.2019.01.002

- Sherman, E. (1982). Gold: A conservative, prudent diversifier. Journal of Portfolio Management, 8(3), 21–27. https://doi.org/10.3905/jpm.1982.408850

- Smales, L. A. (2019). Bitcoin as a safe haven: Is it even worth considering? Finance Research Letters, 30, 385–393. https://doi.org/10.1016/j.frl.2018.11.002

- Stensas, A., Nygaard, M. F., Kyaw, K., & Treepongkaruna, S. (2019). Can bitcoin be a diversifier, hedge or safe haven tools? Cogent Economics & Finance, 7(1), 1–17. https://doi.org/10.1080/23322039.2019.1593072.

- Upper, C. (2000). How safe was the “safe haven”? Financial market liquidity during the 1998 Turbulences. Deutsche Bundesbank. Working Paper No. 1/00. http://dx.doi.org/10.2139/ssrn.219132

- Urquhart, A., & Zhang, H. (2019). Is bitcoin a hedge or safe haven for currencies? An intraday analysis. International Review of Financial Analysis, 63, 49–57. https://doi.org/10.1016/j.irfa.2019.02.009

- Worthington, A. C., & Pahlavani, M. (2007). Gold investment as an inflationary hedge: Cointegration evidence with allowance for endogenous structural breaks. Applied Financial Economics Letters, 3(4), 259–262. https://doi.org/10.1080/17446540601118301

- Wu, S., Tong, M., Yang, Z., & Derbali, A. (2019). Does gold or bitcoin hedge economic policy uncertainty? Finance Research Letters, 31(3), 171–178. https://doi.org/10.1016/j.frl.2019.04.001

- Yaya, O. S., Ogbonna, A. E., Mudida, R., & Abu, N. (2020). Market efficiency and volatility persistence of cryptocurrency during pre- and post-crash periods of Bitcoin: Evidence based on fractional integration. International Journal of Finance & Economics, 26, 2. https://doi.org/10.1002/ijfe.1851

- Yermack, D. (2015). Is bitcoin a real currency? an economic appraisal in: Handbook of digital currency: Bitcoin, innovation, financial instruments, and big data (1st) D. L. K. Chuen.Academic Press. https://doi.org/10.1016/B978-0-12-802117-0.00002-3

- Yousaf, I., & Ali, S. (2021). Linkages between stock and cryptocurrency markets during the COVID-19 outbreak: An intraday analysis. The Singapore Economic Review, 1–20. https://doi.org/10.1142/S0217590821470019

- Yousaf, I., Ali, E. B. S., Azoury, N., & Azoury, N. (2021b). Gold against Asian stock markets during the COVID-19 outbreak. Journal of Risk and Financial Management, 14(4), 186. https://doi.org/10.3390/jrfm14040186

- Yousaf, I., Bouri, S. A. E., & Saeed, T. (2021a). Information transmission and hedging effectiveness for the pairs crude oil-gold and crude oil-bitcoin during the COVID-19 outbreak. Economic Research-Ekonomska Istraživanja. 1–22. https://doi.org/10.1080/1331677X.2021.1927787

- Yousaf, I., & Yarovaya, L. (2022). Static and dynamic connectedness between NFTs, Defi and other assets: Portfolio implication. Global Finance Journal, 100719. https://doi.org/10.1016/j.gfj.2022.100719

- Zhang, Y., Bouri, E., Gupta, R., & Ma, S. (2021). Risk spillover between bitcoin and conventional financial markets: An expectile-based approach. The North American Journal of Economics and Finance, 55(C), 101296. https://doi.org/10.1016/j.najef.2020.101296

- Zivot, E., & Wang, J. (2003). Rolling analysis of time series. In Modeling financial time series with S-Plus® (2nd) (pp.299-346). Springer. https://doi.org/10.1007/978-0-387-32348-0