?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

This study aims to prove the consistency of Agency Theory, Behavioral Consistency Theory and Upper Echelon Theory as a solution to explain the influence of male CEO masculinity on earnings management. This study uses a quantitative approach with a population and research sample using companies on the Indonesia Stock Exchange in 2016–2021. The study collected images of faces identified as male CEOs from data from the Indonesia Stock Exchange website and company websites and using Google searches. The data analysis method in this study uses Ordinary Least Square Regression, Fixed Effects, Random Effects, Robust by using Stata Software which is one of the regression solving procedures that has a high level of flexibility in research that connects theories, concepts and data that can be carried out on research variable. These findings explain that the higher the masculinity of the male CEO’s face has an impact on increasing earnings management, and vice versa, the lower the masculinity of the male CEO’s face has an impact on the decrease in earnings management. The empirical findings have implications for management as a policy maker regarding the face of male masculinity which has an impact on earnings management policies, so that these empirical findings can be used by corporate and government management. The empirical findings provide evidence in the field of behavioral accounting by looking at the face of male masculinity as determinant of company earnings management.

PUBLIC INTEREST STATEMENT

Until now, this empirical research on the topic of male CEO masculinity in Indonesia is still rare. Previous research conducted empirically in developed countries (the United States) was conducted by (Jia Citation2014) with the finding that the face of male CEO masculinity has a positive effect on earnings management. While the empirical findings in Indonesia have a different direction, meaning that the higher the masculinity of the male CEO’s face has an impact on the decline in earnings management, and conversely the lower the masculinity of the male CEO has an impact on the increase in earnings management. These empirical findings have several implications for regulators and corporate governance policy makers regarding male face size as a determinant of earnings management practices.

1. Introduction

Explaining in agency theory explains the relationship or contract between the principal and the agent (Jensen & Meckling, Citation1976); (Nawang Kalbuana et al., Citation2022). The principal employs the agent to perform tasks on behalf of the principal, including the delegation of decision-making authorization from the principal to the agent, where the agent is represented by a male CEO. (Mahiswari & Nugroho, Citation2014); (Susilowati et al., Citation2022). Companies listed on the Indonesia Stock Exchange whose capital consists of shares, shareholders act as principals while male CEOs act as agents. CEO characteristics have an influence on earnings management (Shefer & Frenkel, Citation2005); (Yuhertiana, Arief et al., Citation2020; Yuhertiana et al., Citation2022). Meanwhile, according to the behavioral consistency theory (Epstein, Citation1979); (Yuhertiana, Izaak et al., Citation2020; Yuhertiana, Rochmoeljati et al., Citation2020) explained that the face of male CEO masculinity is correlated with testosterone, aggressiveness and social status have an effect on earnings management.

The decision-making process characteristic of male CEOs is divided into two decision models, rational and incremental models (Fredrickson, Citation1984; Fredrickson & Mitchell, Citation1984; Miller & Friesen, Citation1983). In addition to the two requirements retrieval, there is a need for comprehensiveness model taking process. The process that leads to a rational planning model that is complete with alternatives to the incremental process that relies on intuition and speed in decision-making characteristics of male CEOs, at the end of the decision should be implemented strategic practices. In the implementation process, a measuring tool is needed to assess and evaluate the results of an informational strategy that can help a strategy model that can examine a strategy (Jarzabkowski & Kaplan, Citation2015; Kaplan, Citation2011; Vaara & Whittington, Citation2012). In this case, it certainly affects and determines the quality of decisions made by a leader. Hambrick & Mason (Citation1984); (Yuhertiana, Bastian et al., Citation2019; Yuhertiana, Patrioty et al., Citation2019) explains in the upper echelons theory that the company is a picture of the leaders in the company. Echelon theory explains the differentiating characteristics that are influenced by the characteristics of the CEO on the psychological aspect in terms of cognitive in managing the company, the decision-making process in policy makers related to earnings management practices.

While the use of variable earnings management is based on the opinion of (Scott, Citation2015); (Priono et al., Citation2019; Yuhertiana, Purwanugraha et al., Citation2019) which explains that earnings management is a practice in the process of compiling financial statements that do not violate generally accepted accounting principles, so as to increase or decrease accounting profit as desired by the agent. The agent as the manager of the company knows more data about the state of the company and the company’s prospects in the future than the principal, the agent is the management party represented by the characteristics of the male CEO in managing the company. Earnings management can be seen in the attitude of agents with agency theory (Jensen & Meckling, Citation1976); (Rahma et al., Citation2016; Tatiana & Yuhertiana, Citation2014). So as to provide empirical evidence that the masculinity of the male CEO’s face has an effect on earnings management. The findings are expected to complement the literature to provide empirical evidence of the disclosure of the influence of the masculinity face of male CEOs on earnings management that has not been carried out in Indonesia, so that it can provide empirical evidence in the field of behavioral accounting.

The face of masculinity is a concept of masculine behavior that exists in men which has implications for aggressive nature, has a hard character, tends to be emotional in taking action (Jewitt, Citation1997); (Yuhertiana, Citation2011a, Citation2011b). Male CEO masculinity face is correlated with testosterone, aggressiveness and social status have an influence on earnings management practices (Kamiya et al., Citation2018; Jia et al., Citation2014); (Adi et al., Citation2022). The number of male CEOs of companies listed on the Indonesia Stock Exchange in 2016 to 2021 has grown. This development has become an important issue in companies listed on the Indonesia Stock Exchange. The characteristic role of male CEOs has an impact on the development of companies in Indonesia. The positive impact can be seen from the increase in the number of business units, proving that the economy in Indonesia is getting better and more business units are listed on the Indonesia Stock Exchange (Tanjaya & Santoso, Citation2020); (Sudaryanto et al., Citation2022; Utari et al., Citation2021a).

The face of masculinity has factors that can affect the performance of a male CEO in managing the company (Tanjaya & Santoso, Citation2020); (Aliyyah, Siswomihardjo et al., Citation2021; Prasetio et al., Citation2021). The face of masculinity is a personal aspect, the face of one’s masculinity is carried from birth. Kamiya et al. (Citation2018); (Endarto, Taufiqurrahman, Kurniawan, Indriastuty, Prasetyo, Aliyyah, Endarti, Abadi, Daim, Ismono, Indrawati et al., Citation2021; Rusdiyanto et al., Citation2021) described in the neuroendocrinology literature that facial masculinity in men predicts masculine behavior and aggressive behavior. The face of high masculinity male CEOs can be predicted to be more aggressive in managing the company (Tanjaya & Santoso, Citation2020); (I. Prasetyo et al., Citation2021; Utari et al., Citation2021).

Bertrand and Schoar (Citation2003); (Abadi et al., Citation2021; Endarto, Taufiqurrahman, Suhartono et al., Citation2021) explained that the characteristics of male CEOs have an influence on the company’s decision-making process. Characteristics of male CEOs are confident and often practice earnings management. The nature of excessive trust is characteristic of male CEOs who often practice earnings management (Graham et al., Citation2013; Kamiya et al., Citation2018; Malmendier & Tate, Citation2005), acquisition (Doukas & Petmezas, Citation2007; Kim, 2013; Kamiya et al., Citation2018), innovation (Hirshleifer et al., Citation2012; Kamiya et al., Citation2018). Research in the field of neuroendocrinology explains that a man’s face has an influence on a person’s aggressive behavior. Whereas (Carré & McCormick, Citation2008; Christiansen & Winkler, Citation1992); (Abadi et al., Citation2021; I. Prasetyo et al., Citation2021) explained that the face of male masculinity has an influence on aggressive behavior. Campbell et al. (Citation2011); (N. Kalbuana, Suryati, et al., Citation2021; Rusdiyanto et al., Citation2021) explains that the face of masculinity has an influence on a man’s behavior. Wong et al. (Citation2011); (N. Kalbuana, Prasetyo, et al., Citation2021; I. Prasetyo, Aliyyah, Rusdiyanto, Nartasari, et al., 2021a) explained that the characteristics of male CEOs tend to negotiate for personal gain. Therefore, Stirrat & Perrett, (Citation2010); I. Prasetyo, Endarti et al., (Citation2021); I Prasetyo et al., (Citation2021) explained that men who have a high masculinity face are considered trustworthy. Therefore, Kamiya et al., (Citation2018); Kamiya, & Park, (2017); Wong et al., (Citation2011) provide empirical evidence that the characteristics of male CEOs who have higher masculinity faces have better performance than the characteristics of male CEOs who have lower masculinity faces. Based on the arguments from previous studies, research is the latest issue in Indonesia because previous research was carried out in developed countries (United States), while in Indonesia, as long as observations so far have found research with the masculinity of male CEOs having an impact on earnings management, this study seeks to provide empirical evidence that the masculinity of male CEOs has a positive effect on earnings management in Indonesia, which is actually a developing country.

Motivation in research on the masculinity of male CEOs is the latest issue that is very interesting for research in the field of behavioral accounting to provide justification or motivation as follows: First, this study is supported by agency theory, behavioral consistency theory and upper echelon theory to obtain empirical evidence about the effect of face masculinity of male CEOs on earnings management, Second, this study measures the masculinity of male CEOs using ImageJ software which is not familiar with accounting research. This study was conducted in Indonesia. As long as observations have been made to date, researchers have not found the topic of masculinity of male CEOs associated with the cost of earnings management, Third, the sample of this study is a unique sample, research on the face of male CEO masculinity is associated with earnings management. The sample of this study uses images identified by male CEOs taken from the Indonesia Stock Exchange website, company websites and using Google search. This sample is very interesting to study because it is not yet familiar to be explained empirically in Indonesia. Fourth, the use of ImageJ software is very good quality and reliable software in research, it can be shown from several studies that have been published and accepted by reputable journals (Scopus Q1 and Q2) with Some names of authors who use ImageJ software are as follows: (Lestari & Ningrum, Citation2018; Alrajih & Ward, Citation2014; Jia et al., Citation2014; Kamiya et al., Citation2018; Lewis et al., Citation2012; Alrajih & Ward, Citation2014; Stirrat & Perrett, Citation2010); (Adi et al., Citation2022; Tjaraka et al., Citation2022a)

2. Literature review and hypothesis development

2.1. Agency theory

Agency theory is defined as a consequence of the differentiation of control characteristics of male CEOs as agents having direct access to company information data as compared to shareholders. The relationship between the characteristics of a male CEO as an agent and shareholders delegating authority to the characteristics of a male CEO as an agent to manage the company is explained in (Jensen & Meckling, Citation1976); (I. Prasetyo et al., Citation2021; I. Prasetyo et al., Citation2021b). A male CEO’s as an agent should have the same objective as shareholders do, which is to improve the company through shareholder prosperity, but male CEOs as agents may have their own thoughts that are contrary to what shareholders think (MAYANGSARI, Citation2001); (Prabowo et al., Citation2020; Susanto et al., Citation2021). As a conclusion, agency theory offers an important solution to male CEOs’ decision-making characteristics in the face of corporate earnings management. Jensen and Meckling (Citation1976); (Prabowo et al., Citation2020; Susanto et al., Citation2021) define agency costs in three categories: monitoring, bonding, and residual (Eisenhardt, (Citation1989a); (Adi et al., Citation2022; Sudaryanto et al., 2021). The agency theory consists of three human nature assumptions, namely: (1) humans are generally selfish, (2) humans have limited thinking power in terms of future perceptions, and (3) humans avoid risk at all costs. From the concept of human nature, it can be seen that the usual role of male CEOs affects the company’s earnings management.

2.2. Behavior consistency theory

The facial masculinity of male CEOs correlates with testosterone, aggressive, and social status affects earnings management, seen from the perspective of behavioral consistency theory. He also discusses how behavioral consistency could be used to predict a majority of people within a given time span (Epstein (Citation1979); (Hanim et al., Citation2019; Sudaryanto et al., Citation2020). The theory of behavioral consistency is assumed to be the opinion of a person’s ability to affect issues that trigger emotions to emerge; consistency of behavior can be shown as a particularly selected subject; consistency of behavior is described in the study with the title: “The Stability of Behaviour: I. Predicting Most of the People Much the Time”.

2.3. Upper echelon theory

Upper Echelon theory developed (Hambrick & Mason, Citation1984); (Putri & Sudaryanto, Citation2018; Sudaryanto et al., Citation2019) explain the assumptions that will occur in a company by studying the characteristics of the company’s top management team. Hambrick & Mason, (Citation1984); (N F Asyik et al., Citation2022; Wahidahwati & Asyik, Citation2022) describes the distinguishing characteristics that are influenced by the characteristics of male CEOs on psychological aspects in terms of cognitive in managing the company. The decision-making process was initially divided into two models, namely rational and improvement (Fredrickson, Citation1984; Fredrickson & Mitchell, Citation1984; Miller & Friesen, Citation1983). The rational model focuses on prudence, completeness of information, good planning and analysis, with various alternatives and choosing the best alternative (Camillus, Citation1981; Quinn et al., Citation1988); (Indra Prasetyo et al., Citation2022). On the other hand, the Incremental model relies more on intuition, speed, spontaneity and not in a formal environment because it realizes that there are limitations in terms of rationale or budget (Ismail & Zhao, Citation2017); (Dewianawati & Asyik, Citation2021; Wijaya et al., Citation2020). In the rational model approach, the role of a leader (Selznick, Citation1996) environmental factor (Andrews et al., Citation1971) and strategic decision models developed (Quinn et al., Citation1988); (Ahmed et al., Citation2022; Maulidi et al., Citation2022) impact on the quality of the company’s decision-making. In the incremental model approach, the strategic formulation of the decisions taken is a dynamic that will work (Mintzberg, Citation1978); (D A Nuswantara, Citation2022; D A D A Nuswantara & Maulidi, Citation2021). This rational model process is then used as a starting point to develop a more comprehensive and complete model to conduct a more complete and thorough study (Fredrickson, Citation1984); (IRIANI et al., Citation2021; D A D A Nuswantara et al., Citation2018). A comprehensive approach is considered to provide sharpness in seeing opportunities and provide stability when execution is carried out with caution, thereby reducing the risk of failure (Eisenhardt, Citation1989b; Quinn et al., Citation1988). The holistic approach has its drawbacks when dealing with a dynamic environment, because a dynamic business environment requires speed of decision-making (Eisenhardt & Bourgeois III, Citation1988); (Dian Anita Dian Anita Nuswantara & Maulidi, Citation2017).

2.4. Face, testosterone, and behavior

Previous research has provided empirical evidence of a link between testosterone and masculine behavior. A CEO’s face may be the basis for male facial linkages to topics in this study (Jia et al., Citation2014). Hendrati & Fitrianto, (Citation2020); Hendrati & Taufiqo, (Citation2020) explains that a man’s face can predict masculine behavior. Based on laboratory evidence, Carré & McCormick, (Citation2008); Christiansen & Winkler, (Citation1992) claim that a man’s face predicts aggressive traits. Men’s faces affect masculine behavior (Eisenegger et al., Citation2010; Jia et al., Citation2014). Jia et al., (Citation2014) explain that the relationship between testosterone and male CEOs’ behavior affects the brain both before birth and during growth. A group of nerve cells play a role in the processing of memories and emotional reactions as mediators between testosterone in brain regions to evaluate social interactions (Bos et al., Citation2012; Jia et al., Citation2014); (Indra Prasetyo et al., Citation2022).

Testosterone regulates adolescent spurt (Johnston et al., Citation2001); (Hendrati et al., Citation2019). Adolescents’ development is affected by testosterone (Verdonck et al., Citation1999; Jia et al., Citation2014). Previous research indicates that male and female growth differs in the bizygomatic (the area between the left and right cheeks); however, there is no difference in the growth period for upper facial height (Jia et al., Citation2014). The findings provide empirical evidence that testosterone does affect the development of the male face (Folstad & Karter, Citation1992). Meanwhile, according to (Jia et al., Citation2014; Alrajih & Ward, Citation2014), men’s looks affect masculine behavior during their growth. Further, the findings of Lefevre et al. (Citation2013) provide empirical evidence that there is indeed a connection between testosterone and the ratio of male facial width. Some other studies suggest that the ratio of a man’s face width to testosterone has a beneficial link. In addition, testosterone has a positive relationship with the face, as suggested by previous research (Lefevre et al. (Citation2013). Higher or lower testosterone in men affects the facial masculinity, according to Jia et al. (Citation2014); Pound et al., Citation2009).

2.5. Earnings management

According to (Lestari & Ningrum, Citation2018; Sulistyanto, Citation2008) explained that there are three patterns of earnings management that can be done by the management. First, income increasing raises the company’s profit greater than the actual profit, the management wants the company’s performance to be seen as good. Second, income decreasing, the management wants the company’s performance to be lower than the actual performance, the management can lower the company’s profit. Third, income smoothing, the management performs to control the financial statements, the management wants the profits to remain unchanged from the previous year, so that profits appear stagnant throughout certain periods (Lestari & Ningrum, Citation2018).

According to (Scott, Citation2015) argues that earnings management is a practice in the process of compiling financial statements that does not violate generally accepted accounting principles, so that it can increase or decrease accounting profit as desired by the management. The management as the manager of the company knows more data about the state of the company and the company’s prospects in the future than the shareholders. Earnings management can be seen in the opportunistic attitude of the management with agency theory (Jensen & Meckling, Citation1976). The management as a manager tries to prioritize his personal interests at the expense of the interests of shareholders reflecting the opportunistic behavior of the management. Conflicts of interest occur between management and shareholders arise because both have different interests (Jensen & Meckling, Citation1976).

Model jones

Model (Jones, Citation1991) propose a model that simplifies the assumption that nondiscretionary accruals are constant. This model seeks to regulate the impact of changes in the company’s economic area on non-discretionary accruals. Model (Jones, Citation1991) for nondiscretionary accruals in the year concerned with the following formula:

(1) Calculating TA (total accrual) i.e. net profit for year t less operating cash flow for yeart with the following formula:

TAC = NIit – CFOit

The following is an estimate of total accrual (TA) using the Ordinary Least Square method:

(2) The NDA (non-discretionary accruals) are calculated using the formula above, which includesthe regression coefficient:

(3) Finally, the formula for determining DA (discretionary accruals) as a metric of EarningsManagement is as follows:

Model (Dechow et al., Citation1995) explained that from the calculation results model (Jones, Citation1991) shows that this model is successful in proving the variation of total accruals. Assumptions implicit in the model (Jones, Citation1991) that income is not discretionary. If revenue is managed through revenue discretionary, then Model (Jones, Citation1991) could remove from earnings managed by proxy discretionary accruals. Model (Jones, Citation1991) explained that total accruals related to revenue can extract discretionary accrual components, earnings management estimates are biased towards zero.

Model Kothari et al., (Citation2005)

In this study, the measurement of earnings management uses the model (Kothari et al., Citation2005) refinement of the model (Jones, Citation1991), by including return on assets to control the company’s financial performance. This model argues that by including the element of return on assets in calculating discretionary accruals, it can minimize specification errors to measure earnings management more accurately, with the formula from the model (Jones, Citation1991) modified model (Kothari et al., Citation2005) with the following formula:

(1) Calculate total accrual (TAC) which is net income in year t minus operating cash flow in year t with the following formula:

TAC = NIit – CFOit

Furthermore, total accrual (TA) is estimated using Ordinary Least Square (OLS) as follows:

(2) With the regression coefficient as in the above formula, nondiscretionary accruals (NDA) are determined by the following formula:

(3) Finally, discretionary accruals (DA) as a measure of earnings management is determined by the following formula:

2.6. Research conceptual framework

The conceptual framework is used to explain the influence between the independent variable and the dependent variable and the control variables used in this study. This study places the face of male CEO masculinity as the independent variable, earnings management as the dependent variable, size, profitability, research & development and leverage as control variables.

Placement of the independent variable on the face of male CEO masculinity, earnings management variable as the dependent variable (Jensen & Meckling, Citation1976) behavioral consistency theory (Epstein, Citation1979) and upper echelon theory (Hambrick & Mason, Citation1984). Agency theory, behavioral consistency theory and upper echelon theory underlie the explanation of the test of the influence of male CEO masculinity faces on earnings management (Jia et al., Citation2014). The placement of control variables of size, profitability, research & development costs and leverage refers to agency theory (Jensen & Meckling, Citation1976) and behavioral consistency theory (Epstein, (Citation1979). Agency theory and behavioral consistency theory underlie the explanation of the test of the effect of variable size, profitability, leverage and research & development costs on earnings management variables (Kadim & Sunardi, Citation2019; Kamiya et al., Citation2018). Based on the explanation above, the conceptual framework of this research can be seen in the following figure .

Figure 1. Research Conceptual Framework.

2.7. Research Hypothesis

This study aims to examine and evaluate the effect of male CEO masculinity faces on Earnings Management.

4.2.1. The face of male CEO masculinity has a positive effect on earnings management

Agency theory basically discusses the form of agreement between shareholders and management in managing the company, the management bears a great responsibility for the success of the company it manages. Jensen and Meckling (Citation1976) explain agency relationships arise when shareholders employ management decision-making. In practice, the management as the manager of the company certainly knows more internal information and the company’s prospects in the future than the shareholders. So that the management has an obligation to provide information about the condition of the company to shareholders. But in this case, the information submitted by the management is sometimes not in accordance with the actual conditions of the company (Jensen & Meckling, Citation1976).

The facial masculinity of male CEOs correlates with testosterone, aggressive, and social status affects earnings management, seen from the perspective of behavioral consistency theory. He also discusses how behavioral consistency could be used to predict a majority of people within a given time span (Epstein (Citation1979); (Hanim et al., Citation2019; Sudaryanto et al., Citation2020). The theory of behavioral consistency is assumed to be the opinion of a person’s ability to affect issues that trigger emotions to emerge; consistency of behavior can be shown as a particularly selected subject; consistency of behavior is described in the study with the title: “The Stability of Behaviour: I. Predicting Most of the People Much the Time”.

Upper Echelon theory developed (Hambrick & Mason, Citation1984); (Putri & Sudaryanto, Citation2018; Sudaryanto et al., Citation2019) explain the assumptions that will occur in a company by studying the characteristics of the company’s top management team. Hambrick & Mason, (Citation1984); (N F Asyik et al., Citation2022; Wahidahwati & Asyik, Citation2022) describes the distinguishing characteristics that are influenced by the characteristics of male CEOs on psychological aspects in terms of cognitive in managing the company. The decision-making process was initially divided into two models, namely rational and improvement (Fredrickson, Citation1984; Fredrickson & Mitchell, Citation1984; Miller & Friesen, Citation1983). The rational model focuses on prudence, completeness of information, good planning and analysis, with various alternatives and choosing the best alternative (Camillus, Citation1981; Quinn et al., Citation1988). On the other hand, the Incremental model relies more on intuition, speed, spontaneity and not in a formal environment because it realizes that there are limitations in terms of rationale or budget (Ismail & Zhao, Citation2017); (Dewianawati & Asyik, Citation2021; Wijaya et al., Citation2020). In the rational model approach, the role of a leader (Selznick, Citation1996) environmental factor (Andrews et al., Citation1971) and strategic decision models developed (Quinn et al., Citation1988); (Ahmed et al., Citation2022; Maulidi et al., Citation2022) impact on the quality of the company’s decision-making. In the incremental model approach, the strategic formulation of the decisions taken is a dynamic that will work (Mintzberg, Citation1978); (D A Nuswantara, Citation2022; D A D A Nuswantara & Maulidi, Citation2021). This rational model process is then used as a starting point to develop a more comprehensive and complete model to conduct a more complete and thorough study (Fredrickson, Citation1984); (IRIANI et al., Citation2021; D A D A Nuswantara et al., Citation2018). A comprehensive approach is considered to provide sharpness in seeing opportunities and provides stability when execution is carried out with caution, thereby reducing the risk of failure (Eisenhardt, Citation1989b; Quinn et al., Citation1988)

Male CEO masculinity face is correlated with testosterone, aggressive, confident has an influence on earnings management, viewed from the perspective of behavioral consistency theory (Epstein, (Citation1979). Strategic leadership is an integral part of the strategy formulation process in a company. The characteristic role of the leader in Upper Echelon Theory is to decide, implement, and ensure the strategy goes well (Hambrick & Mason, Citation1984). Tenggono and Syamlan (Citation2021) explains that an organization is a reflection of the characteristics of its leaders. Strategic leadership is the ability of a leader characteristic to empower his team to anticipate conditions that occur in the business environment, strategic leadership is very closely related to strategic change, the relationship between the two is clearly seen that anticipation of changes in the outside world will be responded by the leader by making strategic changes to achieve sustainability from competitive advantage (Tenggono & Syamlan, Citation2021).

The results of the t-test showed that the facial value of male CEO masculinity had a negative and significant influence on research & development with a p-value level of 0.05 (5%). Furthermore, regarding the magnitude of the influence of the masculinity of male CEOs on research & development, it can be seen from the value of the male CEO masculinity face coefficient of −2.077. The inequality of the findings empirically will have an impact on masculine behavior, thus impacting policy-making and research & development. The results of empirical research findings are consistent with the findings of previous studies conducting empirical research in the United States for the sampling period from 1999 to 2014, with empirical findings revealing that gender has a negative influence on research & development, meaning that the higher the gender has an impact on reducing research & development, vice versa, the lower gender has an impact on increasing research & development (Adi et al., Citation2022).

The purpose of this paper is to investigate the Greek firms’ earnings management practices, considering the leverage, taxation and the fiscal debt crisis. Overall, our results indicate that Greek firms are likely to reduce manage earnings via accruals when they face the liquidity risk of leverage, probably because they were more closely controlled by banks and creditors and thus managers had fewer possibilities to engage in earnings management. This study presents useful empirical results about the Greek business environment and offers valuable information to shareholders and investors as they can understand how some main factors, such as leverage, taxation and financial crisis, influence firm’s accounting practices (Mamatzakis et al., Citation2022).

Since the number of companies is more than years, the dynamic panel model and generalized method of moments were employed to enter the lagged dependent variable into the model. It also recommends that capital supervision institutions pass some laws to pave the way for the development and decline of the agency costs and necessitate the establishment of audit committees. The effectiveness of family firms and state ownership on the agency costs is rejected in all three models in terms of statistical significance, so owners cannot prevent agency costs (Salehi, Adibian et al., Citation2021).

In this paper, we examine the voluntary disclosures of female CEOs, which until recently have received very little attention in the literature. In particular, we focus on management earnings forecasts, a major channel involving the communication of voluntary information. These results suggest that female CEOs improve the disclosure environment of their companies by providing high-quality earnings forecasts. Finally, we find that financial analysts rely more on the management forecasts of female CEOs than on those of male CEOs when formulating their forecasts (Francoeur et al., Citation2022).

Stated overconfidence of managers has a positive and significant effect on company’s risk-taking, while it is not consistent with the results of Yang and Kim argue that overconfidence has a negative effect on risk-taking. This study showed that managers’ ethical factors of overconfidence and narcissism as invisible factors could affect managers’ risk-taking. Much research can be of great help to companies because companies can consider their psychological characteristics in selecting managers. Therefore, understanding how narcissism and over-managerial self-confidence can affect the risk and, ultimately, the company’s performance and shareholders' interests, valuable insights in helping companies and organizations in hiring managers with narcissism and overconfidence (Aliyyah, Prasetyo, Rusdiyanto, Endarti, Mardiana, Winarko, Chamariyah, Mulyani, Grahani, Rochman, Hidayat et al., Citation2021).

The results indicated that there is a negative and significant relationship between CEO financial expertise and the logarithm of audit report lag. The results of Kamalluarifin illustrated that there is not relationship between managers’ terms of service and the timeliness of internet reporting. It is obvious that in this stage only the control variable of audit committee is omitted and feature of audit committee, including size, composition, and financial expertise were added (Salehi et al., Citation2018).

Previous research has explained that the masculinity of male CEOs has a positive influence on earnings management (Jia et al., Citation2014). According to (Fee et al., Citation2013; Bolton & Bruunermeier, Markus, Citation2008; Jia et al., Citation2014) explained that the development of research linking accounting practices with the characteristics of top management. The development of research in accounting, finance, and economics extends to the characteristics of male CEOs in the company’s policy making process (Fee et al., Citation2013; Bolton & Bruunermeier, Markus, Citation2008; Jia et al., Citation2014). Bertrand and Schoar (Citation2003) explained that the role of male CEO characteristics has a positive influence on the process of presenting the company’s financial statements. According to (Bamber et al., Citation2010; Brochet et al., Citation2011; Dyreng et al., Citation2010; Feng et al., Citation2011; Ge et al., Citation2011; Jia et al., Citation2014) provide empirical evidence that the characteristics of male CEOs have a positive influence on earnings management. According to Chava et al., (Citation2010); Jia et al., (Citation2014) we provide empirical evidence that the characteristics of male CEOs are the result of the resulting incentives. According to (Dikolli et al., Citation2012; Jia et al., Citation2014) provide empirical evidence that certain characteristics of male CEOs have excessive trust in earnings management practices. According to Jia et al. (Citation2014) it provides empirical evidence that the masculinity of male CEOs has a positive influence on earnings management practices. By combining all the arguments described above, so that the first hypothesis proposed in this study is as follows:

H1: the face of male CEO Masculinity has a positive effect on earnings management

3. Methodology

3.1. Types and approaches to research

This study uses a quantitative approach to give meaning to the interpretation of statistical (Aliyyah, Siswomihardjo et al., Citation2021; Prasetio et al., Citation2021). The research aimed to provide empirical evidence of the effect of male CEO masculinity on earnings management. Explanatory research is used in the design process (Endarto, Taufiqurrahman, Kurniawan, et al., 2021; Indrawati et al., Citation2021). Companies listed on the Indonesia Stock Exchange from 2016 to 2021 were used in the population and research samples. The researchers collected data from the Indonesia Stock Exchange website and company websites, as well as Google searches, to obtain figures of faces identified as male CEOs within a period between 2016 and 2021. The data analysis method in this study uses Ordinary Least Square Regression, Fixed Effects, Random Effects, Robust by using Stata Software which is one of the regression solving procedures that has a high level of flexibility in research that connects theories, concepts and data that can be carried out on research variable. One of the regression completion procedures, Stata has a high degree of flexibility in research that connects theories, concepts, and data that can be done on variables in research.

3.2 Operational definition and measurement

Male CEOs’ masculinity is the independent variable, earnings management is the dependent variable, and the variable of size, profitability, research & development and leverage is the control variable.

3.2.1. Variable independent (fWHR)

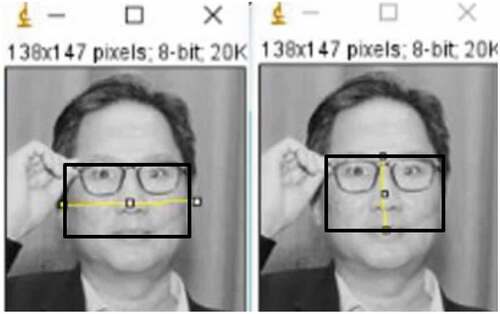

Independent variable is a variable that can affect other variables (Abadi et al., Citation2021; Aliyyah, Prasetyo, et al., Citation2021). This study used male CEO masculinity facial variables as the independent variable. The facial masculinity is a concept of masculine behavior that exists in men having implications on aggressive behavior, having a tough character, having a tendency to be emotional in carrying out their actions (Jewitt, Citation1997). ImageJ software was used to measure male CEOs’ facial masculinity variables, this study changed the male CEO’s face figure to a gray-scale figure with a height of eight bits (Kamiya et al., Citation2018; Alrajih & Ward, Citation2014; Yupping Jia et al., Citation2014; Lewis et al., Citation2012).

For the face of each male CEO inside the ImageJ software, the researchers selected a location in the face figure and dragged the mouse to another location to measure the distance, the vertical line size represents the distance between the upper lip and the highest point of the eyelid. The horizontal line represents the maximum distance between the left and right cheeks, while the vertical line represents the minimum length (Kamiya et al., Citation2018; Alrajih & Ward, Citation2014; Yupping Jia et al., Citation2014; Lewis et al., Citation2012). Therefore, the study independently provided photo quality scores from zero to three based on the following guidelines: 0: Poor posture in which (1) only one ear is visible due to the person’s sideways posture; or (2) the photographer photographed the face figure from below or above, causing face height measurement problematic. 1: One ear seems to be perfect, but because the person is facing to the side, only half of the other ear is visible. 2: The person looks straight ahead and both ears are visible with roots on the face. 3: Perfect posture, with both ears clearly visible to the roots, and the person is looking straight ahead.

Based on the criteria of (Kamiya et al., Citation2018; Alrajih & Ward, Citation2014; Yupping Jia et al., Citation2014; Lewis et al., Citation2012), the study used quality scores of two and three. The measurement scale of this study used the percentage ratio scale which can be seen in the following figure :

Figure 2. Male CEO Masculinity Face Measurements (fWHR).

3.2.2. Dependent Variable (Y)

The dependent variable is a variable whose value cannot be influenced by other variables. The dependent variable in this study uses earnings management with the measurements described as follows:

3.2.2.1. Earnings Management (EM)

Earnings management is a practice in the process of preparing financial statements, so that it can increase or decrease accounting profit as desired by the management. The management as the manager of the company knows more data about the state of the company and the company’s prospects in the future compared to shareholders (Scott, Citation2015). Earnings management in this study uses the measurement model (Kothari et al., Citation2005) refinement of fashion (Jones, Citation1991). By including return on assets, this model adds return on assets in the calculation of discretionary accruals, so as to measure earnings management more accurately. The measurement scale of this study uses a percentage ratio scale. Here is the model equation (Kothari et al., Citation2005) with the following formula:

(1) Calculate total accrual (TAC) which is net income in year t minus operating cash flow in year t with the following formula:

TAC = NIit – CFOit

Furthermore, total accrual (TA) is estimated using Ordinary Least Square (OLS) as follows:

(2) With the regression coefficient as in the above formula, nondiscretionary accruals (NDA) are determined by the following formula:

(3) Finally, discretionary accruals (DA) as a measure of earnings management is determined by the following formula:

3.2.3. Control Variable

The control variable is a variable to control the causal relationship so that it is better to obtain a more complete and better empirical model (Riadi et al., Citation2021). So that this variable can affect the indications being studied. Placement of control variables following previous research (Kamiya et al., Citation2018). The control variables used in this study consist of size, profitability, leverage and research & development.

3.2.3.1. Size (Size)

Size is a value that can classify companies into large or small types that are sourced from total assets, log size. The greater the total asset, the greater the size. So that the transactions carried out are more complete (Kamiya et al., Citation2018). Noviyana and Rahayu (Citation2021) explain the size measurement scale using firm size with the following formula:

SIZE = Ln total asset

3.2.3.2. Profitability (ROA)

Profitability is a tool that can be used to evaluate investments that have been invested by investors and are able to provide the expected returns. Measurement of profitability using Return on assets which describes the distribution of net income divided by total assets (Kamiya et al., Citation2018). The measurement scale of this study uses a percentage ratio scale, with the following formula:

3.2.3.3 . Research & Development (R&D)

Research & development is an investment made by the company on the basis of new knowledge, to produce more efficient product methods based on existing resources. Research cost of research & development is measured using the ratio of research & development intensity (Arifian & Yuyetta, Citation2012; Padgett & Galan, Citation2010) with the following formula:

Research & Development=Total research & development expenditure/Sales

3.2.3.4. Leverage (LEV)

Leverage describes the division of total liabilities by total assets. This financial ratio explains the amount of assets owned by the company which is financed by liabilities. The greater the value of the liability, the greater the impact felt by investors to receive the profits they receive (Kamiya et al., Citation2018). Leverage measurement uses the result of dividing total liabilities by total assets (Kamiya et al., Citation2018). The measurement scale of this study uses a percentage ratio scale with the following formula:

3.3. Data analysis techniques

Data analysis is part of the data testing process after the selection and collection stage of research data. Data analysis is interpreted as estimating or determining the magnitude of the quantitative influence of the change of an event on something else, as well as predicting or estimating other events (Sudaryanto et al., Citation2022; Utari, Sudaryanto, et al., 2021).

3.3.1. Descriptive statistics

Descriptive statistics are statistics that can illustrate the research object through analytical data, without doing analysis (Prasetyo, Aliyyah, Rusdiyanto, Utari et al., Citation2021, Citation2021) from the data of male CEO facial masculinity variable, Earnings management variable, size variable, profitability variable (ROA), Research & Development variable and leverage variable.

3.3.2. Pearson correlation test

Pearson correlation testing is used to look at the relationship between an independent variable and a dependent variable by assuming the Pearson correlation of the data is normally distributed (Prasetyo, Aliyyah, Rusdiyanto, Nartasari, et al., 2021; Rusdiyanto et al., Citation2021). Correlation testing produces positive (+) and negative (-) numbers. If the correlation value is positive, it means that the variables move in the same direction, meaning that when the independent variable is large, the dependent variable is also getting bigger. If the value is negative, it means that the variables move in the opposite directions, meaning that if the value of the independent variable is large, then the dependent variable is getting smaller (Endarto, Taufiqurrahman, Suhartono et al., Citation2021; Prasetyo, Aliyyah, Rusdiyanto, Kalbuana, et al., Citation2021).

3.3.3. Research regression model

Regression analysis is used to find out how close the relationship between one variable and another variable is. The regression analysis has a function to predict the value of independent variable (Y) if the dependent variable (fWHR) is changed (Prasetyo, Aliyyah, Rusdiyanto, Nartasari, et al., 2021; Rusdiyanto et al., Citation2021). The method used in this study was panel data regression analysis. Panel data is also called pool data, longitudinal data, and micro panel data. The panel data regression analysis was used to examine the influence of male CEOs’ facial masculinity (fWHR) on earnings management (Y). Based on the independent variables and dependent variables that have been described, an equation model is obtained that will be used as follows:

To explain the model of the facial masculinity of male CEOs, variables of earnings management, size, profitability, research & development and leverage can be explained as follows Table :

Table 1. Variable Description

4. Research and discussion results

4.1. Descriptive statistics of variables

The results of descriptive statistics can be presented with minimum, maximum, mean, and standard deviation of the variables studied from the sample companies. In addition to presenting based on a sample of all companies listed on the Indonesia Stock Exchange from 2016 to 2021, the figure also shows the testing of this sample based on the company Table :

Table 2. Descriptive Statistics

The table output variables dependent stata above shows the number of observations (N) was 1925. From these 1925 observations, the earnings management value minimum was.000, and the earnings management value maximum was 0.046, the average value of 1925 observations or the mean was of 0.003 with a standard deviation of 0.007. The table variables independent output stata above shows the number of observations (N) was 1781. From these 1781 observations, the value of male CEOs’ facial masculinity minimum was 0.110, and the value of male CEOs’ facial masculinity maximum was 267, the average value of 1781 observations or the mean was of 2.086 with a standard deviation of 6.287. The table variables control output stata above shows the number of observations (N) was 1925. From these 1925 observations, the size value (minimum) was 11.862, and the size value (maximum) was 31.592. The average value of 1925 observations or the mean was of 23.12 with a standard deviation of 5.011. Based on the table output stata above, it can be seen that the number of observations (N) was 1925. From these 1925 observations, the profitability value (ROA) minimum was 000, and the profitability value (ROA) maximum was 0.925, the average value of 1925 observations or the mean was of 0.078 with a standard deviation of 0.108. Based on the table output stata above, it can be seen that the number of observations (N) was 1925. From these 1925 observations, the research & development minimum was 5.234, and the research & development maximum was 21.502, the average value of 1925 observations or the mean was of 15.234 with a standard deviation of 2.549. Based on the table output stata above, it can be seen that the number of observations (N) was 1925. From these 1925 observations, the leverage minimum was 000, and the leverage maximum was 0.990, the average value of 1925 observations or the mean was of 0.482 with a standard deviation of 0.246.

4.2. Pearson correlation test

Pearson’s correlation test was done to see how strong or how weak the relationship between the facial masculinity of male CEOs and earnings management. In this test, if the Pearson correlation value (r) is above 0.05 (5%), it means that there is a strong relationship between the facial masculinity of male CEOs to earnings management, but if the Pearson correlation value is below 0.05 (5%), then it means that the relationship between the facial masculinity of male CEOs and earnings management is said to be weak (Table ).

Table 3. Pearson Correlation Test

Based on the table above, it can be interpreted that the earnings management variable, the facial masculinity of male CEOs, size, Profitability (ROA), Research & development and leverage have a value above 0.05 (5%). Thus, it explains that all variables are declared to be valid to be used in model testing. The reliability test results above explain the value of above 0.05 (5%). This proves that all variables used are reliable and produce the same results when tested.

4.3. Goodness of Fit Model Testing

Hypothesis testing in research is very important, because it can determine whether the research conducted is scientific enough or not. To determine the scientific feasibility of the model, based on the results of four tests that have been carried out put model analysis Ordinary Least Squares (OLS), Fixed Effect Model (FE), Random Effect Model (RE) with the following output (Table ):

Table 4. Goodness-of-Fit Model Testing

4.4. Discussion of Research Results

The probability result of Prob>F was 0.003 ≤ 0.05 (5%), showing that if taken together, the value of regression coefficient is significant, which means that the facial masculinity of male CEOs affects earnings management. The R2 value was 0.139, indicating that the male CEO’s masculinity on the earnings management had a determination level of 0.139. This means that the facial masculinity of male CEOs can be explained by the 0.139 of variability of 0.139. The discussion of the research findings is an analysis of the suitability of previous theories, opinions, or research that has been put forward by the findings of past research to overcome phenomena in this study. The followings are the main parts that can be discussed in the analysis of the findings of this study:

4.4.1. Findings: Male CEO Facial masculinity has a positive effect on earnings management

The masculinity face of the male CEO shows a positive coefficient estimation result in accordance with the initial hypothesis. The results of the t-test explain that the masculine face of male CEOs has a positive and significant effect on earnings management at the significance level of p-value 0.00 ≤ 0.05 (5%). Furthermore, regarding the magnitude of the influence of male CEO masculinity faces on earnings management, it can be seen from the regression coefficient value of male CEO masculinity faces of 0059656. This explains that when the face of male CEO masculinity increases by 1%, earnings management will increase by 0059656.

Empirical test results prove that the higher the masculinity of the male CEO’s face has an impact on increasing earnings management, and vice versa, the lower the masculinity of the male CEO has an impact on the decrease in earnings management. These empirical findings support the hypothesis that male CEO masculinity has a positive effect on earnings management, the hypothesis is accepted (p-value 0.00 ≤ 0.05 (5%)). Submission of the direction of the initial hypothesis based on the findings of previous studies that lead to positive (Jia et al. Citation2014; Hendrati et al., Citation2023; Dian Anita Dian Anita Nuswantara et al., Citation2023). The initial hypothesis with empirical findings is the value of the masculinity coefficient of male CEOs in Indonesia in the same direction as the results of the masculinity of male CEOs in the United States. The results of the coefficient of determination indicate that the masculinity face of Indonesian male CEOs is in line with the value of the masculinity face of male CEOs in the United States. These empirical findings have an impact on masculine behavior, so that it has an impact on male CEOs in making policy on earnings management.

The results of this empirical research are consistent with the previous empirical findings (Jia et al., Citation2014; Nur Fadjrih Asyik, Muchlis, Riharjo, et al., 2022; I Prasetyo et al., Citation2022) His empirical study in the United States for the sampling period from 1996 to 2010 with his findings revealed that the face of male CEO masculinity has a positive effect on earnings management, meaning that the higher the masculinity of the male CEO’s face has an impact on the increase in earnings management, and vice versa, the lower the masculinity of the male CEO. impact on the decline in the value of earnings management. While the results of empirical research findings in Indonesia for the sampling period in 2016–2021 with the findings revealing that the masculinity of male CEOs has a positive effect on earnings management, meaning that the higher the masculinity of the male CEO’s face has an impact on the increase in earnings management, and vice versa, the lower the face of male CEOs. Male CEO masculinity has an impact on earnings management.

These findings are supported by behavioral consistency theory which explains that male CEO masculinity is correlated with testosterone, aggressiveness, social status affects earnings management, viewed from the perspective of behavioral consistency theory (Epstein, Citation1979; N Kalbuana et al., Citation2022; Tjaraka et al., Citation2022b). While agency theory basically discusses the form of agreement between shareholders and the characteristics of the male CEO as an agent in managing the company, the characteristics of the male CEO as an agent carry a great responsibility for the success of the company he manages (Jensen and Meckling (Citation1976)). Explaining agency relationships arise when shareholders employ male CEO characteristics as agents to provide services and then delegate authority in decision-making. In practice, the characteristics of male CEOs as agents as company managers certainly know more internal information and company prospects in the future than shareholders. So that the characteristics of male CEOs as agents have the obligation to provide information about the condition of the company to shareholders. While the Upper Echelon Theory (Hambrick & Mason, Citation1984; Indra Prasetyo et al., Citation2023) explains the assumptions that occur in the company by studying the characteristics of the company’s top management team. Hambrick & Mason, (Citation1984) explain the distinguishing characteristics of male CEOs on psychological and cognitive aspects of corporate management. The decision-making process is divided into two rational models and improvements (Fredrickson, Citation1984; Fredrickson & Mitchell, Citation1984; Miller & Friesen, Citation1983). The rational model focuses on caution, completeness of information, planning and analysis with various alternatives and choosing the best alternative (Camillus, Citation1981; Quinn et al., Citation1988).

Jia et al., (Citation2014) provide empirical evidence that the higher the masculinity of the male CEO has an impact on increasing earnings management, and vice versa, the lower the masculinity of the CEO has an impact on the decline in earnings management, financing decisions are focused on earnings management policies, high earnings management can increase company profitability. The higher the value of male CEO characteristics has an impact on increasing learning management, and vice versa, the lower the value of male CEO characteristics has an impact on decreasing earnings management (Cronqvist et al., (Citation2012); Huang et al., (Citation2013); Malmendier et al., (Citation2011); Chava et al., (Citation2010)).

5. Conclusion

Empirical findings conducted in developing countries (Indonesia) explain that the masculinity of the male CEO’s face has a positive effect on earnings management, meaning that the higher the masculinity of the male CEO has an impact on improving earnings management, and vice versa, the lower the masculinity of the male CEO impact on the decline in earnings management. These empirical findings are consistent with their findings (Jia et al., Citation2014) conducted in developed countries (United States of America) with their findings explaining that the face of male CEO masculinity has a positive effect on earnings management, meaning that the higher the masculinity of the male CEO’s face the impact on increasing practice, earnings management, and vice versa, the lower the masculinity of the male CEO has an impact on the decline in old management practices. Based on empirical findings, both developed countries (United States of America) and developing countries (Indonesia) did not experience differences in the face of male CEO masculinity in making policies related to earnings management practices.

5.1. Research implication

This research can provide some implications for theory, practice in policy making. This research provides both theoretical and practical implications:

5.1.1. Theoretical implications

The findings are empirically supported by agency theory, behavioral consistency theory and upper echelon theory explaining that the face of CEO masculinity has an influence on earnings management. While agency theory and upper echelon theory explain the role of male CEO characteristics in earnings management policy making. Empirical findings that ImageJ software supports this empirical finding that the masculinity of male CEOs has an influence on earnings management. The empirical findings provide evidence that the presence of male CEOs has an influence on earnings management decision making, supported by agency theory, upper echelon theory and behavioral consistency theory. The face describes the distinctive style of male CEOs in making earnings management policies, supported by agency theory, upper echelon theory and behavioral consistency theory. Male CEO style can influence masculine behavior and testosterone is supported by behavioral consistency theory. The face of masculinity in the fields of Biology and Psychology explains a person’s masculine behavior supporting the theory of behavioral consistency. The face of masculinity in accounting explains that the masculinity of male CEOs has an influence on earnings management.

5.1.2. Practical implications

These empirical findings provide input on the development and improvement of corporate financial governance practices in Indonesia, specifically, the practical implications: These empirical findings have implications for company management as policy making regarding the face of male masculinity has an impact on earnings management policies, so that the empirical findings can be used by company management and the government. These empirical findings provide evidence in the field of behavioral accounting by looking at the face of masculinity as a determinant of earnings management. Furthermore, it enriches empirical findings in the field of behavioral accounting and becomes a reference for conducting future research

5.2. Research limitations

It is impossible to escape the limitations of this investigation. In order to make this research understandable with a non-misleading interpretation, limitations are disclosed. The goal of the limits disclosure is to allow future research to fill up the gaps left by the constraints of this study: The element of conducting content analysis in determining the measurement of the face value of masculinity of male CEOs using imageJ software cannot distinguish images of male CEOs that have been modified or edited, taking pictures of male CEOs is obtained from the company’s annual report for the 2016–2021 period and the use of search image of male CEO on Google. Because the sample for this study was restricted to using images of male CEOs from firm annual reports published between 2016 and 2021 and from Google image searches of male CEOs, researchers were unable to tell apart images of male CEOs that had undergone changes.

Author Contributions

Conceptualization, N.F.A, R and RDP; investigation, M, R and RDP.; writing preparation of original draft, I.K.B; IGMH, DA.N,S writing reviews and editing, R, RDP and M.; supervision, T; project administration, N.F.A; I.G.M.H, D.A.N,S fund acquisition, N.F.A, and T All authors have read and approved the published version of the manuscript.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Data Availability Statement

The study did not involve any data sets and the articles collected were sourced from https://www.scopus.com/home.uri, accessed on 2022 and https://scholar.google.com/, accessed on 2022.

Additional information

Funding

Notes on contributors

Nur Fadjrih Asyik

Nur Fadjrih Asyik, S.E., M.Si., Ak., CA. is the Chairperson of the Indonesian School of Economics (STIESIA) Surabaya Indonesia, an Assessor of BAN PT and an independent researcher. He obtained his Bachelor’s degree in Accounting from Indonesia School of Economics (STIESIA) Surabaya Indonesia with a degree (S.E), Master of Accounting Postgraduate Program from Universitas Gadjah Mada with a degree (M.Si), Postgraduate Program in Accounting Science with his (Dr.) Degree research interests include financial accounting, corporate finance, corporate governance, behavioral accounting, management accounting and corporate social responsibility. Dr. Rusdiyanto, S. E,. M. Ak,. CH,. CHt Higher Education S1 Universitas Madura Graduated with a Bachelor of Accounting (S.E), Master of Accounting Study Program, Universitas Pembangunan Nasional Veteran Jawa Timur Graduated with Master of Accounting (M. Ak), Postgraduate of Doctoral Program in Accounting, Fakultas ekonomi dan bisnis Universitas Airlangga Surabaya Graduated Doctor of Accounting Science.

References

- Abadi, S., Endarto, B., Taufiqurrahman, A., Kurniawan, R. B., Daim, W., Ismono, N. A., Alam, J., Purwati, A. S., Wijaya, A., Rusdiyanto, A. U., & Kalbuana, N. (2021). Indonesian desirious finality of the community in regard. Journal of Legal, Ethical and Regulatory Issues, 24, 1–27.

- Adams, R. B., & Ragunathan, V. (2017). Lehman Sisters. Working Paper, 1–57. https://doi.org/10.2139/ssrn.3046451

- Adi, S., Irawan, B., Suroso, I., & Sudaryanto, S. (2022). Loyalty-Based Sustainable Competitive Advantage and Intention to Choose Back at One Bank. Quality - Access to Success, 23(189), 306–315. https://doi.org/10.47750/QAS/23.189.35

- Ahmed, A. A. A., Komariah, A., Chupradit, S., Rohimah, B., Nuswantara, D. A., Nuphanudin, N., Mahmudiono, T., Suksatan, W., & Ilham, D. (2022). Investigating the relationship between religious lifestyle and social health among Muslim teachers. HTS Teologiese Studies/Theological Studies, 78(4). https://doi.org/10.4102/hts.v78i4.7335

- Aliyyah, N., Prasetyo, I., Rusdiyanto, R., Endarti, E. W., Mardiana, F., Winarko, R., Chamariyah, C., Mulyani, S., Grahani, F. O., Rochman, A. S., Hidayat, W., & Tjaraka, H. (2021). What Affects Employee Performance Through Work Motivation? Journal of Management Information and Decision Sciences, 24, 1–14.

- Aliyyah, N., Prasetyo, I., Rusdiyanto, R., Endarti, E. W., Mardiana, F., Winarko, R., Chamariyah, C., Mulyani, S., Grahani, F. O., Rochman, A. S., Kalbuana, N., Hidayat, W., & Tjaraka, H. (2021). What Affects Employee Performance Through Work Motivation? Journal of Management Information and Decision Sciences, 24, 1–14. https://www.scopus.com/inward/record.uri?eid=2-s2.0-85110461420&partnerID=40&md5=4b5e50800f8866ccdd52682c4b5a73f4

- Aliyyah, N., Siswomihardjo, S. W., Prasetyo, I., Rusdiyanto, P., Rochman, A. S., & Kalbuana, N. (2021). THE EFFECT OF TYPES OF FAMILY SUPPORT ON STARTUP ACTIVITIES IN INDONESIA WITH FAMILY COHESIVENESS AS MODERATION. Journal of Management Information and Decision Sciences, 24, 1–15.

- Alrajih, S., & Ward, J. (2014). Increased facial width-to-height ratio and perceived dominance in the faces of the UK’s leading business leaders. British Journal of Psychology, 105(2), 153–161. https://doi.org/10.1111/bjop.12035

- Andrews, D. F., Gnanadesikan, R., & Warner, J. L. (1971). Transformations of multivariate data. Biometrics, 27(4), 825–840. https://doi.org/10.2307/2528821

- Arifian, D., & Yuyetta, E. N. A. (2012). TERHADAP TANGGUNG JAWAB SOSIAL PERUSAHAAN (CORPORATE SOCIAL RESPONSIBILITY) (Studi Empiris: Perusahaan terdaftar di BEI). Accounting, 1–30.

- Asyik, Fadjrih, N., & Riharjo, I. (2022). The Influence of fWHR Male CEO on Research & Develop- ment. Preprints, August, 1–18. https://doi.org/10.20944/preprints202208.0372.v1

- Asyik, Muchlis, M., Fadjrih, N., Muchlis, M., & Riharjo, I. B. (2022). The impact of a male CEO’ S facial masculinity on leverage The impact of a male CEO’ S facial masculinity on leverage. Cogent Business & Management, 9(1), 1–19. https://doi.org/10.1080/23311975.2022.2119540

- Asyik, Muchlis, M., Fadjrih, N., Muchlis, M., Riharjo, I. B., & Rusdiyanto, R. (2022). The impact of a male CEO’S facial masculinity on leverage. Cogent Business & Management, 9(1), 2119540. https://doi.org/10.1080/23311975.2022.2119540

- Asyik, N. F., Wahidahwati, Laily, N., & Wahidahwati, W. (2022). The Role of Intellectual Capital in Intervening Financial Behavior and Financial Literacy on Financial Inclusion. WSEAS Transactions on Business and Economics, 19, 805–814. https://doi.org/10.37394/23207.2022.19.70

- Bamber, L. S., Jiang, J., & Wang, I. Y. (2010). What’s my style? The influence of top managers on voluntary corporate financial disclosure. Accounting Review, 85(4), 1131–1162. https://doi.org/10.2308/accr.2010.85.4.1131

- Bertrand, M., & Schoar, A. (2003). Managing With Style: The Effect Of Managers On Firm Policies. The Quarterly Journal of Economics, CXVIII(4), 1169–1208. https://doi.org/10.1162/003355303322552775

- Bolton, P., & Bruunermeier, Markus, K. (2008). Economists’ Perspectives on Leadership. Working Paper, 1–33.

- Bos, P. A., Hermans, E. J., Ramsey, N. F., & Van Honk, J. (2012). The neural mechanisms by which testosterone acts on interpersonal trust. NeuroImage, 61(3), 730–737. https://doi.org/10.1016/j.neuroimage.2012.04.002

- Brochet, F., Faurel, L., & McVay, S. (2011). Manager-specific effects on earnings guidance: An analysis of top executive turnovers. Journal of Accounting Research, 49(5), 1123–1162. https://doi.org/10.1111/j.1475-679X.2011.00420.x

- Camillus, J. C. (1981). Corporate strategy and executive action: Transition stages and linkage dimensions. Academy of Management Review, 6(2), 253–259. https://doi.org/10.2307/257881

- Campbell, T. C., Gallmeyer, M., Johnson, S. A., Rutherford, J., & Stanley, B. W. (2011). CEO optimism and forced turnover. Journal of Financial Economics, 101(3), 695–712. https://doi.org/10.1016/j.jfineco.2011.03.004

- Carré, J. M., & McCormick, C. M. (2008). In your face: Facial metrics predict aggressive behaviour in the laboratory and in varsity and professional hockey players. Proceedings of the Royal Society B: Biological Sciences, 275(1651), 2651–2656. https://doi.org/10.1098/rspb.2008.0873

- Chava, S., & Purnanandam, A. (2010). CEOs versus CFOs: Incentives and corporate policies. Journal of Financial Economics, 97(2), 263–278. https://doi.org/10.1016/j.jfineco.2010.03.018

- Christiansen, K., & Winkler, E. (1992). Hormonal, anthropometrical, and behavioral correlates of physical aggression in !Kung San men of Namibia. Aggressive Behavior, 18(4), 271–280. https://doi.org/10.1002/1098-2337(1992)18:4<271::AID-AB2480180403>3.0.CO;2-6

- Cronqvist, H., Makhija, A. K., & Yonker, S. E. (2012). Behavioral consistency in corporate finance: CEO personal and corporate leverage. Journal of Financial Economics, 103(1), 20–40. https://doi.org/10.1016/j.jfineco.2011.08.005

- Dechow, P. M., Sloan, G., & Sweeney, A. P. (1995). Detecting Earnings Management. The Accounting Review, 70(2), 193–225.

- Dewianawati, D., & Asyik, N. F. (2021). The impact of climate on price fluctuations to the income of leek farmers in Sajen village, Pacet, Mojokerto. International Journal of Business Continuity and Risk Management, 11(2–3), 247–262. https://doi.org/10.1504/IJBCRM.2021.116283

- Dikolli, S. S., Mayew, W. J., & Steffen, T. D. (2012). Honoring One’s Word: CEO Integrity and Accruals Quality. Working Paper, 1–41. https://doi.org/10.2139/ssrn.2131476

- Doukas, J. A., & Petmezas, D. (2007). Acquisitions, overconfident managers and self-attribution bias. European Financial Management, 13(3), 531–577. https://doi.org/10.1111/j.1468-036X.2007.00371.x

- Dyreng, S. D., Hanlon, M., & Maydew, E. L. (2010). The effects of executives on corporate tax avoidance. Accounting Review, 85(4), 1163–1189. https://doi.org/10.2308/accr.2010.85.4.1163

- Eisenegger, C., Naef, M., Snozzi, R., Heinrichs, M., & Fehr, E. (2010). Prejudice and truth about the effect of testosterone on human bargaining behaviour. Nature, 463(21), 356–359. https://doi.org/10.1038/nature08711

- Eisenhardt, K. M. (1989a). Agency theory: An assessment and review. Academy of Management Review, 14(1), 57–74. https://doi.org/10.2307/258191

- Eisenhardt, K. M. (1989b). Making fast strategic decisions in high-velocity environments. Academy of Management Journal, 32(3), 543–576. https://doi.org/10.2307/256434

- Eisenhardt, K. M., & Bourgeois III, L. J. (1988). Politics of strategic decision making in high-velocity environments: Toward a midrange theory. Academy of Management Journal, 31(4), 737–770. https://doi.org/10.2307/256337

- Endarto, B., Taufiqurrahman, Kurniawan, W., Indriastuty, D. E., Prasetyo, I., Aliyyah, N., Endarti, E. W., Abadi, S., Daim, N. A., Ismono, J., Aji, R. B., Rusdiyanto, & Kalbuana, N. (2021). GLOBAL PERSPECTIVE ON CAPITAL MARKET LAW DEVELOPMENT IN INDONESIA. Journal of Management Information and Decision Sciences, 24(1), 1–8. https://www.scopus.com/inward/record.uri?eid=2-s2.0-85113411656&partnerID=40&md5=1074bd3526601cda4a86fbdd7b52d1bd

- Endarto, B., Taufiqurrahman, Kurniawan, W., Indriastuty, D. E., Prasetyo, I., Aliyyah, N., Endarti, E. W., Abadi, S., Daim, N. A., Ismono, J., Rusdiyanto, & Kalbuana, N. (2021). GLOBAL PERSPECTIVE ON CAPITAL MARKET LAW DEVELOPMENT IN INDONESIA. Journal of Management Information and Decision Sciences, 24, 1–8.

- Endarto, B., Taufiqurrahman, Suhartono, S., Setyadji, S., Abadi, S., Aji, R. B., Kurniawan, W., Daim, N. A., Ismono, J., Alam, A. S., Rusdiyanto, & Kalbuana, N. (2021). The Obligations Of Legal Consultants In The Independent Legal Diligence Of The Capital Market Supporting Proportion Of Legal Prepparement. Journal of Legal, Ethical and Regulatory, 24, 1–8.

- Epstein, S. (1979). The stability of behavior: I. On predicting most of the people much of the time. Journal of Personality and Social Psychology, 37(7), 1097–1126. https://doi.org/10.1037/0022-3514.37.7.1097

- Fee, C. E., Hadlock, C. J., & Pierce, J. R. (2013). Managers with and without Style: Evidence using exogenous variation. Review of Financial Studies, 26(3), 567–601. https://doi.org/10.1093/rfs/hhs131

- Feng, M., Ge, W., Luo, S., & Shevlin, T. (2011). Why do CFOs become involved in material accounting manipulations? Journal of Accounting and Economics, 51(1–2), 21–36. https://doi.org/10.1016/j.jacceco.2010.09.005

- Folstad, I., & Karter, A. J. (1992). Parasites, bright males, and the immunocompetence handicap. American Naturalist, 139(3), 603–622. https://doi.org/10.1086/285346

- Francoeur, C., Li, Y., Singer, Z., & Zhang, J. (2022). Earnings forecasts of female CEOs: Quality and consequences. Review of Accounting Studies. https://doi.org/10.1007/s11142-021-09669-7

- Fredrickson, J. W. (1984). The comprehensiveness of strategic decision processes: Extension, observations, future directions. Academy of Management Journal, 27(3), 445–466. https://doi.org/10.2307/256039

- Fredrickson, J. W., & Mitchell, T. R. (1984). Strategic decision processes: Comprehensiveness and performance in an industry with an unstable environment. Academy of Management Journal, 27(2), 399–423. https://doi.org/10.2307/255932

- Ge, W., Matsumoto, D., & Zhang, J. L. (2011). Do CFOs Have Style? An Empirical Investigation of the Effect of Individual CFOs on Accounting Practices. Contemporary Accounting Research, 28(4), 1141–1179. https://doi.org/10.1111/j.1911-3846.2011.01097.x

- Graham, J. R., Harvey, C. R., & Puri, M. (2013). Managerial attitudes and corporate actions. Journal of Financial Economics, 109(1), 103–121. https://doi.org/10.1016/j.jfineco.2013.01.010

- Hambrick, D. C., & Mason, P. A. (1984). Upper echelons: The organization as a reflection of its top managers. Academy of Management Review, 9(2), 193–206. https://doi.org/10.2307/258434

- Hanim, A., Zainuri, A., & Sudaryanto, S. (2019). Rationality of gender equality of Indonesian women migrant worker. International Journal of Scientific and Technology Research, 8(9), 1238–1242. https://www.scopus.com/inward/record.uri?eid=2-s2.0-85073422762&partnerID=40&md5=4ea7c8f29260175800e799cf7bce0936

- Hendrati, I. M., & Fitrianto, A. R. (2020). Environmental Development and Empowerment from Industrial Impact. IOP Conference Series: Earth and Environmental Science, 519(1). https://doi.org/10.1088/1755-1315/519/1/012025

- Hendrati, I. M., Muljaningsih, S., Sishadiyati, S., Nadia Sasri, W., & Ekawijaya, S. (2019). Surabaya city export expansion policy analysis. Humanities and Social Sciences Reviews, 7(1), 137–146. https://doi.org/10.18510/hssr.2019.7117

- Hendrati, I. M., Soyunov, B., Prameswari, R. D., Suyanto, R. D., Rusdiyanto, R. D., & Nuswantara, D. A. (2023). The role of moderation activities the influence of the audit committee and the board of directors on the planning of the sustainability report. Cogent Business and Management, 10(1). https://doi.org/10.1080/23311975.2022.2156140

- Hendrati, I. M., & Taufiqo, F. (2020). Creative industry development model as an economic support in Surabaya. Opcion, 35(22), 1121–1134. https://www.scopus.com/inward/record.uri?eid=2-s2.0-85083102044&partnerID=40&md5=38a28c0cb84b42a496b25bbdbbc1e172

- Hirshleifer, D., Low, A., & Teoh, S. H. (2012). Are Overconfident CEOs Better Innovators? Journal of Finance, 67(4), 1457–1498. https://doi.org/10.1111/j.1540-6261.2012.01753.x

- Huang, J., & Kisgen, D. J. (2013). Gender and corporate finance: Are male executives overconfident relative to female executives? Journal of Financial Economics, 108(3), 822–839. https://doi.org/10.1016/j.jfineco.2012.12.005

- Indrawati, M., Utari, W., Prasetyo, I., Rusdiyanto, & Kalbuana, N. (2021). HOUSEHOLD BUSINESS STRATEGY DURING THE COVID 19 PANDEMIC. Journal of Management Information and Decision Sciences, 24, 1–12.

- Iriani, S. S., Nuswantara, D. A., Kartika, A. D., & Purwohandoko, P. (2021). The Impact of Government Regulations on Consumers Behaviour during the COVID-19 Pandemic: A Case Study in Indonesia. Journal of Asian Finance, Economics and Business, 8(4), 939–948. https://doi.org/10.13106/jafeb.2021.vol8.no4.0939

- Ismail, K. M., & Zhao, X. (2017). Comprehensiveness in strategic decision making: Toward clarifying the construct. American Journal of Management, 17(4), 133–142.

- Jarzabkowski, P., & Kaplan, S. (2015). Strategy tools‐in‐use: A framework for understanding “technologies of rationality” in practice. Strategic Management Journal, 36(4), 537–558. https://doi.org/10.1002/smj.2270

- Jensen, M. C., & Meckling, W. H. (1976). Theory of The Firm : Managerial Behavior, Agency Costs and Ownership Structure. Journal of Financial Economics, 3(4), 305–360. https://doi.org/10.1016/0304-405X(76)90026-X

- Jewitt, C. (1997). Images of men: Male sexuality in sexual health leaflets and posters for young people. Sociological Research Online, 2(2), 23–34. https://doi.org/10.5153/sro.64

- Jia, Y., Lent, L., Van, & Zeng, Y. (2014). Masculinity, Testosterone, and Financial Misreporting. Journal of Accounting Research, 3, 1–63. https://doi.org/10.1111/1475-679X.12065

- Johnston, V. S., Hagel, R., Franklin, M., Fink, B., & Grammer, K. (2001). Male facial attractiveness: Evidence for hormone-mediated adaptive design. Evolution and Human Behavior, 22(4), 251–267. https://doi.org/10.1016/S1090-5138(01)00066-6

- Jones, J. J. (1991). Earnings Management During Import Relief Investigations. Jour Nal of Accounting Reserch, 29(2), 193–228.

- Kadim, A., & Sunardi, N. (2019). Pengaruh Profitabilitas, Ukuran Perusahaan Terhadap Leverage Implikasi Terhadap Nilai Perusahaan Cosmetics and Household yang terdaftar di Bursa Efek Indonesia. Jurnal SEKURITAS (Saham, Ekonomi, Keuangan Dan Investasi), 3(1), 22–32. https://doi.org/10.32493/skt.v3i1.3270