Abstract

Islam stipulates its adherents to abide by religious principles in their economic transactions. The aim of this study is twofold. First, it accounts for the adherence of Shariah board members of Islamic banks with the Fit and Proper Criteria (FAPC) promulgated by State Bank of Pakistan (SBP). Second, it explores the current state of provision of Islamic finance education in the universities and madaris (i.e., Islamic seminaries) in Pakistan. This is the unique study in a sense because it draws attention of the stakeholders concerned (i.e., SBP, Higher Education Commission, Ittehad-e-Tanzimat Madaris-e-Deeniya & Ministry of Education) to revisit and make strategic milestones in congruent with the demand-supply gap of Islamic professional experts. Total sample consists of 21 banks, out of which the first five are full-fledged Islamic and remaining 16 are the commercial banks with Islamic banking branches. Descriptive research design has been employed to examine the supply of Shariah experts from madaris and universities in Pakistan. Our findings reveal the following: (1) Profiles of all the Shariah board members fully comply with the FAPC of SBP, and more than 50% of members represent multiple boards of Islamic banks. (2) With 26,000 madaris across Pakistan, 75% of the Shariah experts received their education from one Madrisa named Jamia-dar-ul-uloom, Karachi. Notably, province-wise stats highlight Punjab atop in terms of madaris (45% to 56%) in the country, though it produces less than 10% scholars for the Islamic banks’ Shariah boards. A similar situation persists in Khyber Pakhtunkhwa that has 1354 to 3136 madaris and only one Shariah scholar received education from this province. Karachi, the capital of Sindh province and hub of Islamic seminaries, solely contributed more than 85% SB members to the Islamic banks. (3) Among the top fifteen business schools of Pakistan, only four are offering a degree in Islamic finance. Moreover, these four schools have only eight full-time faculty members with a core degree in Islamic finance. This study suggests the practitioners to increase the supply of Shariah scholars and also strengthen the capabilities and skills of human capital regarding Islamic finance education through education, training, social awareness and capacity building.

1. Introduction

The founder and first governor-general of Pakistan Muhammad Ali Jinnah, accentuating the significance of Islamic banking and finance at the inaugural ceremony of State Bank of Pakistan (SBP) in 1948, said:

“I shall watch with keenness the work of your organization in evolving banking practices compatible with Islamic ideas of social and economic life … We must manage our destiny in our own way and present to the World an economic system based on true Islamic concepts of equality of manhood and social justice”.Footnote1

Consistent with the vision of founding father, Council of Islamic Ideology (CII) was constituted in 1957 with aim to orchestrate comprehensive framework, a linchpin to an economic system aligned with Islamic doctrines. In pursuance, in 1969, CII promulgated the country’s current banking structure based on interest (riba)—repugnant to the injunctions of Shariah—and resolved to purge it. In response, in 1980, a committee of fifteen CII members submitted detailed guidelines to reform the economy in accordance with the Islamic stipulations. Consequently, all the commercial banking transactions in Pakistani rupee were made interest free in 1985 and profit and loss sharing deposits reached at a record level of 62% of total deposits in the country (Saleem Ullah et al., Citation2014). However, the country failed to adopt a full-fledged Shariah-compliant regulatory framework because of a serious dearth of Islamic finance experts. The main reason behind this is that at the time of implementation Islamic financial system, face multiple challenges such as conflict between Islamic contract requirements and conventional contract, subtle legal problems, and lack of skilled personnel (Butt et al., Citation2018).

This resulted in devising a few Shariah-compliant products, in juxtaposition of market dynamics, to replace the interest based transactions in the financial markets (Maierbrugger, Citation2016) and spurred complaints against the practices of Islamic Banking and Finance Institutions (IBFIs) in Pakistan. Following these concerns, since 1985 the Federal Shariat Court (FSC) announced to audit the non-Islamic structure of which are executed by banks in Pakistan (Abrar et al., Citation2022). Further, FSC issued a verdict (fatwa) on 14 November 1991, highlighting some of the emerging products and processes of IBFIs linked—directly or indirectly—with interest. Thereby, it ordered the government to take measures to eradicate interest from the economy by June 1992. Instead of honoring the ruling of FSC, the government and financial institutions filed an appeal with the Supreme Court of Pakistan. After a delay of several years, on 23 December 1999, the apex court reaffirmed and sustained the verdict of FSC and directed the government to abolish the interest-based banking system by June 2001. Although the government initiated some tangible measures in this regard, it failed to meet the prescribed deadline to Islamize the entire economic system. The government of that time contended that the well-defined parameters are a prerequisite to establish an Islamic economic and financial system. Accordingly, it decided and reaffirmed resolve to suspend the interest-based system gradually and re-launched the Islamic banking in 2001 (Saleem Ullah et al., Citation2014).

Since the establishment of first full-fledged Islamic bank in 2002, Islamic Banking Industry (IBI) of Pakistan has witnessed a tremendous growth over the past 15 years. By December 2018, five full-fledged Islamic banks and seventeen conventional banks with stand-alone Islamic banking branches were operating in the country. According to SBP (Citation2019) report, the branch network of Islamic banks grew remarkably and reached 2,851 branches. The exemplary ramification of Islamic banking in Pakistan not only notched locally but also distinguished in global Islamic financial assets. For example, in the last five years, IBI of Pakistan observed a growth of about 30% while global cumulative average growth rate hovered around 16.1% (Young, Citation2016). Islamic banking sector in Pakistan roughly makes up 15% of the total banking industry against 1% in 2002 (Saleem Aftab, Citation2016; Ullah et al., Citation2014). Furthermore, SBP is eager to take IBI share to 20% by 2020 with 3300 branches nationwide (Siddiqui, Citation2018). Likewise, Pakistan Stock Exchange also has a Shariah-compliant index called KMI-30 which reflects the performance of 30 leading firms that comply with the criteria of Shairah supervisory board (Akbar et al., Citation2021).

Financial literacy concerned with Islamic finances is the essential element for financial inclusion in developing economies, because majority of people are familiar with Islamic products but unaware with their functions (Ali et al., Citation2020). Advanced Islamic nations such as Malaysia and Turkey has reformed and adapted their Islamic education institutions to conform with the needs of a contemporary world (Aşlamacı & Kaymakcan, Citation2017). Despite the phenomenal growth in the last decade, IBI in Pakistan has been facing multifaceted challenges, which tend to blur its future. One of the major challenges that IBI is currently facing is roughly the same that hampered its growth in late 1980s: a shortage of well-qualified Islamic finance experts and lack of awareness about Islamic banking system in the country. Although, comparatively, the current IBI of Pakistan is better regulated and identifies a number of qualified Islamic financial experts, there exists a gap worth concern between the supply and demand of these experts. At present, over 25,000 experts are associated with Islamic Finance Industry (IFI) in Pakistan, while additional 3000 to 4000 professionals are required every year to meet the growing needs of this industry. Moreover, majority of IFI professionals believe that the number of entry-level trained experts in Islamic finance is not sufficient (Siddiqui, Citation2018). Earlier this perspective was eluded and endorsed by SBP that Shariah the task of promoting Islamic banking with absence of extensive awareness and paucity of experts regarding Islamic banking practices (Saleem Ullah et al., Citation2014). Although in the 1990s Pakistan put the efforts, it failed to start the Islamic financial system because officials were not familiar with the Islamic financial practices (Abrar et al., Citation2022).

Based on the aforementioned literature, the current study has the following objectives: (1) It assesses the adherence of Shariah board members of Islamic banks with Fit and Proper Criteria (FAPC), specifically the quantitative caluses, promulgated by State Bank of Pakistan (SBP); (2) it explores the current state of Islamic finance education vis-à-vis Islamic banks’ Shariah board members, probing traditional Islamic educational institutions (i.e., madaris) and contemporary higher education institutions (i.e., Universities) in Pakistan. By doing so, the study expands, academically, the literature on Islamic finance education and unveils the focal obstructs impeding growth of Islamic banks, specifically in Pakistan. Practically, it draws attention of the stakeholders concerned (i.e., SBP, Higher Education Commission, Ittehad-e-Tanzimat Madaris-e-Deeniya & Ministry of Education) to revisit and make strategic milestones in congruence with the demand-supply gap of Islamic professional experts. It deserves mentioning that approximately 35,337 madarisFootnote2 in Pakistan are registered with Ittehad-e-Tanzimat Madaris-e-Deeniya Pakistan (ITMDP), an independent umbrella organization of five schools of Islamic jurisprudence (Gishkori, Citation2015). Surprisingly, only three madaris are registered with Pakistan Madrasa Education Board (PMEB), a body established by the government of Pakistan, because ITMDP totally works independently and not wants to work under the guidance of government of Pakistan.

Rest of the paper is organized into four sections. Section 2 provides a review of the relevant literature on the topic, followed by the methodology in section 3. Descriptive analysis is presented in section 4, while the final section concludes the study with a proposed Islamic finance education framework that can spur the growth of this industry in Pakistan.

2. Literature review

2.1. Islamic finance industry in pakistan: an overview

Like any other field, Islamic banking practices require a number of skills, expertise, and qualifications related to the product/service design and development. More precisely, Islamic banking personnel shall have the capability to develop a product in accordance with the Islamic laws (Shariah). Although the Islamic finance industry is growing rapidly for the last two decades (Kayani, Citation2022) and Pakistan is one of the leading centres for preparing Islamic scholars, the major challenge is an acute shortage of human capital which has the requisite professional education and understanding of Shariah principles (Yurizk, Citation2013). Global estimates project that IBI industry needs as much as 1 million Islamic finance professionals by 2020 (O’brien, Citation2016). Moreover, the statistics suggest that nearly 400 renowned Islamic scholars are well versed in Islamic finance theory and practices. Only 15 to 20 of these scholars are deemed to be more experienced and knowledgeable than others. As a result, the top 20 scholars are occupying around 55% of the total board positions worldwide (Davies & Sleiman, Citation2012). The situation of Islamic micro finance industry is even worse in terms of the availability of Islamic finance experts. Despite sharing less than 1% of total Islamic finance assets, the main barrier to the growth of this niche industry is the lack of awareness and absence of specialized educational institutions (Yurizk, Citation2013).

2.2. Islamic finance education in Pakistan

The critical role of education and skills development to improve productivity and create employment opportunities cannot be undermined. Further, human capital theory majorly emphasises to seek the benefit from education and skills training of individuals in the form of investment in human capital (Nafukho et al., Citation2004). Therefore, if human capital is not efficiently utilized, then it will disrupt the business growth (Siswanti & Ganis Sukoharsono, Citation2019). As Levy and Murnane (Citation2013) put it: “For the foreseeable future, the challenge of ‘cybernation’ is not mass unemployment but the need to educate many younger people for the jobs computers cannot do.” In a similar vein, World Bank reported that more than 2 billion working-age people lack the basic literacy skills required for quality jobs. With the emergence of globalization, the growth would crucially depend on skills of better quality to get competitive advantage. The skills development results in resiliency, mastery and core competencies in the relevant fields (Kemal, Citation2005).

Islamic finance education has its roots back to the British colonial era (Qadir, Citation2013). In the context of Pakistan, Khan and Bhatti (Citation2006) explored reasons behind the failure of interest-free banking movement of the 1980s. They came up with the conclusion that the evasive attitude of government and bureaucracy, unfavorable socioeconomic environment and a shortage of trained Islamic finance experts in the banking industry were the root causes of this letdown. Subsequently, SBP conducted a nationwide survey and reported that 95% of households and 73% of businesses affirmed their demand for Islamic banking. However, the major challenge is that various potential customers ask questions about the Shariah adherence of a product which are not properly answered by the branch personnel of Islamic banks. Therefore, these customers leave the branch with an assumption that there is not much difference between conventional and Islamic banking system (Saleem Ullah et al., Citation2014). Hanif (Citation2016) contended that mainly two types of human resources are participating in the operations of Islamic financial institutions in Pakistan. First are Shariah experts who are well qualified from orthodox Islamic educational institutions with a little knowledge of contemporary accounting, finance, and banking practices. Second are the bankers with a good knowledge of the profession while having negligible understanding of Islamic Shariah principles. Further, Shaikh et al. (Citation2020) contended that Islamic banks are usually unable to market and promote their available products to the customers.

Further, a wide range of literature shows that employees of IBIs have less knowledge of Islamic banking practices. In this regard, Harun et al. (Citation2015) concluded that there is severe need to train the management staff of IBI concern with Islamic knowledge in the context of Malaysia. A study by Belwal and Al Maqbali (Citation2018) in the context of Oman documented that customers are much confused regarding whether the Islamic banks follow the principles according to Shariah or not due to the less knowledge of employees’ about their products. In addition, Kamarudin and Kassim (Citation2020) contended that professionalism of employees is the key element of the organizational success. They found that customers are much satisfied with the staff of conventional banks with regard to their assurance, empathy, responsiveness, and awareness as compared to Islamic banks. Similarly, another recent research has proven that for the success of IBI, it’s essential to work on the training and development of the employees (Akkas & Asutay, Citation2022). As a result, the product development departments of Islamic financial institutions often keep their focus on the existing products of conventional banks and often attempt to replicate their Islamic version with minute changes to give them a Shariah-compliant outlook. Likewise, once a financial product is conceived it will be presented to Shariah experts who will approve this product and contract design after ensuring its Shariah compliance without assessing its underlying economic value. This lack of knowledge about the true spirit of Islamic financial system restricts the banking staff to think beyond existing practices of conventional banking. Hence, it is essential that staff of Islamic banks shall possess sound knowledge of Shariah principles along with professional qualifications of banking and finance to design efficient products or services in conformity with the Islamic laws. Similarly, Shariah experts should also be trained in the accounting, finance, and banking matters to develop their understanding of the economic value of a product.

The statistics about the provision of Islamic finance education are also not encouraging. For example, in Pakistan only 24 higher educational institutions are offering Islamic finance courses in their curriculum which is far behind other countries such as the UK (68), Malaysia (44), and UAE (39; Thecityuk, Citation2015). Furthermore, among the eight key educational institutions of the world that offer best Islamic finance programs, none is sited in Pakistan (Sengupta, Citation2014). Additionally, if we look at the current state of the provision of Islamic finance education in Pakistan, a huge gap exists between the supply and demand of graduates. This issue was also highlighted by the governor of central bank of Pakistan: “with the high growth of the (Islamic finance) industry, there still prevails a demand supply gap of Shariah scholars” (Bajwa, Citation2017). While Al-Awlaqi and Mohamed Aamer (Citation2022) contended that Islamic financial literacy is one of the major determinants at the time of the preference of banking products. Thus, it is the right time for top universities and professional education providers to roll out Islamic finance-related courses as an essential part of their accounting- and finance-related programs. Further, a vast majority of traditional madrasas are also lagging in rendering background knowledge, basic concepts (Zaki, Citation1982), and application of modern Islamic financial techniques (Siddiqui (Citation2018). Therefore, this paper is shedding some lights on one problem: the production of well-qualified Shariah scholars to respond to the needs of Islamic finance industry of the Pakistan.

2.3. Underlying Theory of Human Capital

Human Capital Theory (HCT), proposed by Becker (Citation1962) and Rosen (Citation1976), advocate that individuals can improve their skills and abilities through education and training that will lead to higher economic output. When human capital is properly utilized then this will ultimately profitable for society at large and for any organization (Nafukho et al., Citation2004). If human capital is not optimized, then it will disrupts the sustainability of businesses (Siswanti & Ganis Sukoharsono, Citation2019). Hence, HCT focused on seeking gain from personnel’s education and training in the form of investment in human capital (Nafukho et al., Citation2004). Human development through education, work productivity, and creativity generates positive externalities. While the provision of education is considered as an investment in human capital and contemplated as more worthwhile than that of physical capital (Woodhall, Citation1997). Further, human capital is also the key factor which significantly boosts the financial performance of the Islamic banks (Siswanti & Ganis Sukoharsono, Citation2019). Hence, HCT is provided the theoretical basis for our inquiry. Further, Ahmad et al. (Citation2020) contended that financial literacy is major predictor of human capital, which influences the individual’s financial behavior and also documented that countries should try to improve Islamic financial literacy that will ultimately enhance knowledge of the people regarding Islamic financial decisions and contribute to their growth in the long-run.

2.3.1. Theoretical framework

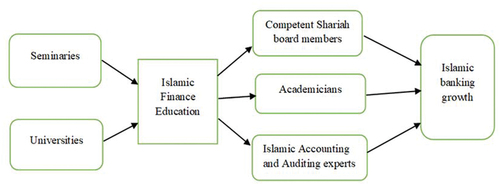

Although for the last two decades Islamic finance has got much attention from researchers, literature has failed to answer the questions, “how to promote Islamic finance globally?” (Alam & Seifzadeh, Citation2020), how to motivate the people to adopt Islamic finance practices? (Azmat, Ali, Brown, & Skully, Citation2021). With these questions in mind, we have developed the above-mentioned framework. The sources of Islamic finance teaching are the Quran, the Hadit, and the consensus of the Muslim jurists. Therefore, to learn the fundamental rules of Islamic finance people go to the seminaries where Muslim jurists teach Quran and Hadith. Similarly, some universities also offer degree programs in Islamic finance and teach contemporary issues and instruments in Islamic finance alongside their permissibility in religious jurisprudence. People who got education from these institutions serve as Shariah board members, academicians, or work as Islamic accounting and auditing experts. Once the Islamic banking industry has needed a number of experts who can ensure that all the transactions of their respective financial institutions are Shariah compliant; this will not only increase the internal efficiency of the institution but also build trust with customers and other stakeholders. This customer trust and loyalty is a key factor for profitability and growth of the Islamic financial institution (Aslam et al., Citation2020); see, Figure . The description of all arabic terms are defined in nd .

Figure 1. Conceptual framework.

Appendix A. Definitions of Arabic terms

Appendix B. List of abbreviations

3. Methodology

3.1. Data collection

Data about total strength, qualification, experience, affiliations, and institutions (i.e., Shariah board members earned their education) Shariah is mainly extracted from the website of respective Islamic bank. The total sample consists of 21 banks, out of which first five are full-fledged Islamic and the remaining 16 are the commercial banks with Islamic banking branches; details are presented in Table . Information about Islamic finance-related degree, specialization, and course offerings in top fifteen business schools—as ranked by Higher Education Commission in 2015—of Pakistan was accessed from the website of each academic institute. To fill up the missing data about Shariah board members and business schools, an email was sent to the respective institutionFootnote3 (e.g., Islamic bank or business school). Finally, data on the number of traditional Islamic institutions (Madrasas) in Pakistan was obtained from “The Madrasa conundrum (2014); the state of religious education in Pakistan”—an annual report published by provincial Auqaf departments and Ministry of Religious Affairs of Pakistan.

Table 1. Profiles of SB members of Islamic and conventional banks with Islamic banking windows and their adherence to FAPC (Oct 2018 to Feb 2019)

3.2. Nature of study

This study is quantitative in nature and uses the descriptive analysis to illustrate the outcomes of the study. Descriptive analyses are employed to present quantitative descriptions in a manageable form. Since, the purpose of present research is to provide some basic-level information about the state of Islamic finance education in Pakistan; the best suited approach we can employ is the “descriptive statistics”.

4. Results and discussion

4.1. Shariah board members’ adherence to FAPC

Fit And Proper Criteria (FAPC) is a set of rules and regulations issued by the SBP and imperative for Islamic banks in Pakistan to follow when appointing Shariah Board (SBP) members. A most recent version of FAPC was issued in 2018 and can be accessed from the SBP website (www.sbp.org.pk). It consists of several quantitative (e.g., education and experience) and qualitative (e.g., integrity and honesty) clauses. The focus of the present research is mainly to examine the quantitative attributes of each SB member.

In pursuit of achieving the study’s objectives, we first analyzed profiles of SB members of all the 21 Islamic banks in terms of their number, qualification, experience, and affiliationFootnote4 to ascertain their adherence with FAPC. Table demonstrates that:

All the Islamic banks have at least three Shariah scholarsFootnote5 on their SB except Bank of Khyber, Summit Bank, and Standard Chartered Bank, which have more than three members.

Each SB member is well qualified and holds an adequate degree (required in FAPC) to be appointed as a Shariah scholar of Islamic bank. FAPC requires that each member should have “Shahadat ul Aalamiyyah Degree (Dars e Nizami) from any recognized Board of Madaris with minimum 70% marks and Bachelor’s Degree with a minimum of 2nd Class” or Post Graduate Degree in Kuliyyatush Shari’ah or Kuliyyah Usooluddin, L.L.M. (Shari’ah) with a minimum GPA of 3.0 or equivalent from any recognized University.Footnote6

All the Shariah board members possess a wide range of experience in Shariah related matters and fulfill the minimum criteria stipulated in FAPC. FAPC stated that each member of shariah board should have “at least four (4) years’ experience of giving Shari’ah rulings including the period of Takhassus fil Ifta; or at least five (5) years post qualification experience in teaching or Research and Development in Islamic Banking and Finance”.v

In accord with the FAPC, Resident Shariah Board Members (RSBM) of all the Islamic banks are not employed by any other Islamic bank in any capacity; neither they are serving on the Shariah boards of more than two Islamic Financial Institutions (IFIs).

Further, the version of FAPC- 2018 is amended by SBP and restricts that Shariah board member will not serves more than three Islamic banking institutions.

Overall, these evidences unveil that Islamic banks are committed to comply with the instructions of the SBP.

Moreover, we examined a number of SB members are affiliated with multiple IFIs. Table illustrate that around 53% of SB members are affiliated with multiple IFIs. However, if we look at the worldwide scenario, in 2017 there were 1162 Shariah scholars representing IFIs, out of which as many as 835 scholars were serving on the board of a single IFI. One possible reason of this overlapping in Pakistan could be the scarcity of trained Shariah scholars. It implies and justifies the SBP relaxation regarding Shariah scholars to appear on multiple SBs. In stark contrast, other Muslim countries, such as Malaysia, strictly prohibit a Shariah scholar representation on Shariah a multiple SBs in the same industry.Footnote7

Among other reasons elaborating shared SB member lies with the reluctance on the part of Islamic banks to hire new and young scholars. Table also shows that among 69 Shariah scholars, 34 have a specialized degree in banking or finance whereas 29 members do not possess any such professional qualification (data on 6 SB members was unavailable). However, FAPC does not explicitly require SB members to have an earned degree in banking or finance and asks that each Shariah scholar must demonstrate an adequate understanding of banking and finance in general and Islamic finance in particular. Thus, it emphasizes the importance of banking and finance knowledge for Shariah scholars. Moreover, in an interview conducted by SBP with 100 top-level and middle-level managers of Islamic banks, it was suggested that Shariah scholars shall be trained in the field of finance so that they can have better knowledge and understanding of contemporary financial practices (Saleem Ullah et al., Citation2014).

4.2. State of traditional Islamic finance education in Pakistan

This section demarcates the names and locations of traditional Islamic educational institutions (madrasas) from where all 69 Shariah board members of IBs have obtained their education. Subsequently, this information was compared with the total number of madrasas functioning in each province of Pakistan. Madrasa is an umbrella term used for all kinds of religious schools in Pakistan. Based on the level of education, these madrasas can be divided into three categories equivalent to their contemporary counterparts. The first category, called Madrasa, teaches students from first to tenth grades which is equivalent to the primary and secondary schools. The second category, known as Dar-ul-uloom, normally encapsulates eleventh and twelfth grades, equivalent to a college education. The highest category is Jamia that has a status of university (Khalil, Citation2015). However, surprisingly, this categorization of madrasas, based on educational level, could vary significantly across various Islamic Sects. For example, Table reflects that 10 Shariah scholars do not attend any traditional Islamic educational institution whereas data of 4 scholars was not available. Similarly, Table indicates that among rest of the 55 SB members 41 (74.54%) received their religious education from only one madrasa: Jamia-dar-ul-uloom, Karachi. Besides, out of these 41 scholars 13 were those who have also attended another madrasa to advance their Islamic education. Madrasa Jamiatul-uloom al-Islamia, Jamia-tur-Rasheed, and Wifaq-ul-madaris al Arabia, Pakistan produced 8, 7, and 5 SB members, respectively. It is noteworthy that Wifaq-ul-madaris al-Arabia Pakistan is an umbrella organization and has 17,952 madrasas, including those mentioned above that are registered with this organization (www.wifaqulmadaris.org). Only few attended more than one madrasa to pursue and advance their religious education. Shariah.

Table 2. Number of SB members graduated from various madrasas

We also probed the province-wise representation of madrasa and relevant representation on the SB members. In this respect, we found that more than 85% of scholars attended madrasas that were located in Karachi city, the capital of Sindh province. Four scholars obtained their religious education from Punjab province, while one was from Khyber Pakhtunkhwa province. Table exhibits the total number of madrasas serving in the provinces of Pakistan. Various government departments have reported varying number of madrasas in the country. Data provided by provincial Auqaf departments demonstrate that 35,337 madrasas are working in Pakistan. On the contrary, the ministry of religious affairs shows 26,131 madrasas in its records (Khalil, Citation2015).

Table 3. Total number of madrasas in different provinces of Pakistan

We compared the total number of madrasas with the number of Shariah scholars from each province. Punjab province represents the highest share of madrasas (45% to 56%) in the country, yet contributes less than 10% scholars to the Shariah boards of Islamic banks. In Balochistan, there are 2704 to 13,000 seminaries, but not even a single SB member was qualified from these institutions. A similar situation persists in Khyber Pakhtunkhwa that has 1354 to 3136 madrasasm and only one Shariah scholar received education from this province. Karachi, the capital of Sindh, as a hub of madrasas solely contributed more than 85% SB members to the Islamic banks. The possible explanation of this unusual distribution of Shariah scholars among different seminaries could be the passive attitude of some madrasas as they are somehow skeptical about the country’s Islamic banking industry. This mistrust between madrasa establishment and the government further compounded this situation regarding appointments of only privileged people of the top positions (Butt, Citation2012). Consequently, 95% madrasas of different sects are affiliated with the non-governmental organization Ittehad-e-Tanzimat Madaris-e-Deeniya, and the role of government in regulating these seminaries is very limited. With exception, Jamia dar-ul-uloom Karachi has been providing some pioneering Islamic finance experts to the country (e.g., Mufti Taqi Usmani). The institute is striving hard to produce Islamic finance experts in accordance with the market needs as it has established its own separate “Centre for Islamic Economics.”

4.3. State of contemporary Islamic finance education in Pakistan

In this section, we analyze the ratio of SB members who possess a degree in conventional banking or finance parallel to their religious education. In addition, we have explored the motivation of top fifteen business schools towards the provision of Islamic banking and finance education in Pakistan. The rationale behind selecting top fifteen business schools is the high academic ranking of these institutes; thus, they are the top priority of business students. Moreover, it is generally perceived that the degree, specialization, and course offerings of these schools are highly aligned with the current job market requirements.

We also categorize the top 15 business schools in Pakistan based on their motivation towards Islamic banking and finance education. The first category (highly motivated) consists of those schools offering a full-fledged degree in Islamic finance. The second category (moderately motivated) institutes specialization in Islamic finance. Subsequently, the third category (least motivated) consists of those business schools which merely offer a single course in Islamic finance. Table indicates that four business schools (26%); ranked 3rd, 4th, 12th, and 13th (i.e., HEC ranking) are offering a comprehensive degree in Islamic finance. While one is offering specialization and rest of the 12 schools are offering a single course on Islamic finance. It is worth mentioning that the majority of the least motivated business schools offer courses related to Islamic finance as an optional subject. It was also observed that the curriculum of college-level (grade 11th, 12th, 13th, and 14th) business students (enrolled in Intermediate in commerce or bachelor in commerce) in Pakistan does not encompass any Islamic banking- and finance-related subject. On the other side, the curriculum of madrasas is highly different from educators. In madrasas religious scholars or leaders teach the students and most of the madrasas do not teach the secular subjects and religious leaders who decided the syllabus argued that a Muslim only needs to know the aspects which are provided by Quran and Sunnah; hence, madrasas do not produce students for employment (Bhattacharya, Citation2014).

Table 4. Islamic finance-related degree, specialization or course offering by top 15 business schools of Pakistan

Table provides the number of permanent faculty members affiliated with highly motivated business schools and hold a specialized degree in Islamic finance. These numbers reveal and project a grave picture of qualified faculty members in this area as no institute owned more than 4 permanent staff members with core qualification in Islamic finance. It depicts that business schools either rely on other faculty members who are not qualified to teach Islamic finance courses or hire visiting faculty members to fill up this gap. In the seminal study, Warsame (Citation2016) found that shortage of qualified scholars, lack of coordination among Islamic finance education providers, and a dearth of high-quality teaching material are the biggest hindrances in the way of Islamic finance industry. Therefore, based on underpinning theory of this study “HCT” needs to take measures concern with the education and training of human capital because human capital is one of the fundamental elements which will not only enhance the performance of Islamic banks also improves the country’s growth (Siswanti & Ganis Sukoharsono, Citation2019).

Table 5. Number of permanent faculty members with core degree in Islamic finance in highly motivated business schools

4.4. Proposal of Islamic finance education framework for Pakistan

Figure shows the proposed Islamic finance education framework for Pakistan. It reveals the need for two-tier harmonization, both at the top (among regulatory bodies) and lower level (among institutions), where SBP could act as a bridge between IFIs and educational bodies.

Figure 2. Proposed Islamic finance education framework for Pakistan.

The key recommendations of this framework for policy makers and regulators are as follows:

First, State Bank of Pakistan (SBP), Higher Education Commission, Ittehad-e-Tanzimat Madaris-e-Deeniya (ITMD), and Ministry of Education (MOE) should jointly form a committee to oversee and regulate the demand, supply, and growth of Islamic finance education in the country.

SBP being the regulatory authority should instruct IFIs to hire candidates only with a proper degree in Islamic finance. This practice will provide dual benefits; an increase in the demand for Islamic finance graduates and a rapid growth in Islamic finance industry with more satisfied customer base.

SBP should collaborate with HEC and encourage universities to offer specialized Islamic finance courses and programs in line with the market demand. More Islamic finance graduates at university level mean that IFIs would be able to fulfill their specific HR requirements.

HEC and ITMD should sit together to devise Islamic finance programs, specializations, and courses for undergraduate and postgraduate students. ITMD should also direct madaris to launch Islamic economics and finance related specialized programs. At the institutional level, university and madrasa officials should collaborate and refer competent students to each other as well as swap specialized faculty members for different subjects. This practice will produce competent Shariah scholars with comprehensive knowledge of contemporary banking and finance practices. It will also bridge the gap between traditional and contemporary educational Institutions.

This study suggests the practitioners to strengthen the capabilities and skills of human capital regarding Islamic finance education through education, training, social awareness, and capacity building.

HEC and ITMD should assist MOE to devise and incorporate compulsory Islamic finance courses in the curriculum of college-level business programs (i.e., intermediate degree in commerce, diploma in commerce, and bachelor’s degree in commerce). Likewise, (MOE) should direct schools and colleges to include Islamic finance-related courses in the degree programs as a compulsory subject. In this way, students would be able to understand the basic concepts of Islamic banking system and will get the aspiration to make their career in this field. More courses at the college level would mean that more students will be interested to take this course at the university level and a better understanding of Islamic finance at large. Besides, seminaries and universities should assist the colleges in hiring and training qualified staff members.

Last but not the least, at the institutional level, universities and madaris should assist schools and colleges in finding and training faculty members who can teach foundation courses on Islamic finance to the students. The following model pursues the practitioners to facilitate the Islamic finance education, which in turns ultimately will produce the expert officials because if the officials are not much familiar with term “Islamic Finance” then their developed products are not much in accordance with Shariah.

5. Conclusions

This paper synthesizes and cordon off the ground situation of Islamic finance education in Pakistan. It explores the adherence of Shariah board members to FAPC issued by State Bank of Pakistan, the inclination of traditional Islamic schools (madrasas) in producing well-versed Shariah scholars for Islamic finance industry, the motivation of contemporary higher educational institutions (universities) towards the provision of Islamic finance education, and the availability of qualified faculty members. Hence, it captures a holistic perspective of supply and demand of Shariah scholars as the underlying factor impeding the growth of Islamic banking and finance in Pakistan. The study finds that all the SB members of Islamic banks strictly adhere to the criteria issued by the SBP. However, it is observed that 53% of Shariah scholars were affiliated with the Shariah boards of more than one IFI. Likewise, about 45% of IFIs do not possess a specialized degree in contemporary banking or finance.

The study also reveals that the overall capacity of madrasas in producing competent Shariah scholars, who can actually make a career in Islamic finance, is very limited. In a country that has around 35,000 madrasas, more than 74% of Shariah board members of Islamic banks holding a degree in religious education were coming from only one madrasa: Jamia-Darul-Uloom Karachi. This surprising fact reflects a serious lack of commitment on the part of religious schools toward the promotion of Islamic banking and finance in the country.

In the context of Islamic finance education in contemporary higher educational institutions, the results are not much satisfactory either. Among the top fifteen business schools of the country, only four are offering a full-fledged degree program in Islamic finance. Besides, two of them have launched this program only recently (i.e., 2016 and 2017). Moreover, one business school offers Islamic finance specialization and twelve are offering just one course on Islamic finance. It was also noted that there is a serious shortage of highly qualified Islamic finance academics in business schools of Pakistan. In addition, Islamic finance-related courses are not a part of the curriculum at college level.

This study also has some limitations. Firstly, as this study is limited to the descriptive analysis, research may be extended by collecting the data from other sources about Islamic banking industry and Islamic finance education and may employ other analysis techniques. Secondly, this study only focused on the Pakistan. A cross-country comparison may provide more pronounced information about Islamic banking industry and Islamic finance education structure. Further, not considering the role of Islamic insurance institutions is also a drawback of this study.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

Notes

2. It is plural of madrasa

3. In some cases, email was directly sent to the concerned Shari’ah board member to obtain the necessary information

4. We have also examined whether Resident Shari’ah Board Member (RSBM) is affiliated with the SB’s of more than three Islamic financial institutions, because this practice is not allowed as per the FAPC.

5. According to SBP regulations every bank shall have an SB which is comprised of at least three Shari’ah scholars

6. Shari’ah Governance Framework for Islamic Banking Institutions (Updated Until June, 2018); Available Online at: https://www.sbp.org.pk/ibd/2018/C1-Annex-A.pdf.

7. Guidelines on the governance of Sharia’ah committee for the Islamic financial institutions are available at Bank Negara Malaysia’s website http://www.bnm.gov.my/guidelines/01_banking/04_prudential_stds/23_gps.pdf.

References

- Abrar, M., Abbas, S., Kousar, S., & Mushtaq, M. (2022). Investigation on the effects of customer knowledge, political support, and innovation on the growth of Islamic banking system: A case study of Pakistan. Journal of the Knowledge Economy, 1–29. https://doi.org/10.1007/s13132-022-00933-y

- Aftab, M. (2016). Islamic banking, modes moving up in Pakistan. https://www.khaleejtimes.com/business/banking-finance/islamic-banking-modes–moving-up-in-pakistan [accessed 3 September 2017]

- Ahmad, G., Widyastuti, U., Susanti, S., & Mukhibad, H. (2020). Determinants of the Islamic financial literacy. Accounting, 6(6), 961–966. https://doi.org/10.5267/j.ac.2020.7.024

- Akbar, M., Akbar, A., & Draz, M. U. (2021). Global financial crisis, working capital management, and firm performance: Evidence from an Islamic market index. SAGE Open, 11(2), 21582440211015705. https://doi.org/10.1177/21582440211015705

- Akkas, E., & Asutay, M. (2022). Intellectual capital disclosure and financial performance nexus in Islamic and conventional banks in the GCC countries. International Journal of Islamic and Middle Eastern Finance and Management, 1–24. https://doi.org/10.1108/IMEFM-01-2021-0015

- Alam, I., & Seifzadeh, P. (2020). Marketing Islamic Financial Services: A Review, Critique, and Agenda for Future Research. Journal of Risk and Financial Management, 13(1), 1–19. https://doi.org/10.3390/jrfm13010012

- Al-Awlaqi, M. A., & Mohamed Aamer, A.(2022). Islamic financial literacy and Islamic banks selection: An exploratory study using multiple correspondence analysis on banks’ small business customers. International Journal of Emerging Markets, ahead-of-print https://doi.org/10.1108/IJOEM-09-2021-1354

- Ali, M. M., Devi, A., Furqani, H., & Hamzah, H. (2020). Islamic financial inclusion determinants in Indonesia: An ANP approach. International Journal of Islamic and Middle Eastern Finance and Management, 13(4), 727–747. https://doi.org/10.1108/IMEFM-01-2019-0007

- Aşlamacı, İ., & Kaymakcan, R. (2017). A model for Islamic education from Turkey: The Imam-Hatip schools. British Journal of Religious Education, 39(3), 279–292. https://doi.org/10.1080/01416200.2015.1128390

- Aslam, E., Haron, R., & Ahmad, S. (2020). A comparative analysis of the performance of Islamic and conventional banks: Does corporate governance matter?. Int. J. Business Excellence, 20(3), 1–13. https://www.researchgate.net/profile/Ejaz-Aslam-3/publication/335456533_

- Azmat, S., Ali, H., Brown, K., & Skully, M. (2021). Persuasion in Islamic finance. Australian Journal of Management, 46(2), 272–286. https://doi.org/10.1177/0312896220926556

- Bajwa, M. T. (2017). Islamic banking & finance awareness drive- 2017. https://www.bis.org/review/r171003e.pdf [accessed 8 June 2019]

- Becker, G. S. (1962). “Investment in human capital: A theoretical analysis. Journal of Political Economy, 70(5, Part 2), 9–49. https://doi.org/10.1086/258724

- Belwal, R., & Al Maqbali, A. (2018). A study of customers’ perception of Islamic banking in Oman. Journal of Islamic Marketing, 10(1), 150–167. https://doi.org/10.1108/JIMA-02-2016-0008

- Bhattacharya, S. (2014). Madrasa education in Pakistan: In the context of government policy. Global Education Magazine, 9, 2. https://dialnet.unirioja.es/servlet/articulo?codigo=7345473

- Butt, T. M. (2012). Social and political role of madrassa: Perspectives of religious leaders in Pakistan. South Asian Studies, 27(2), 387. https://journals.pu.edu.pk/journals/index.php/IJSAS/article/view/2859

- Butt, I., Ahmad, N., Naveed, A., & Ahmed, Z. (2018). Determinants of low adoption of Islamic banking in Pakistan. Journal of Islamic Marketing, 9(3), 655–672. https://doi.org/10.1108/JIMA-01-2017-0002

- Davies, A., & Sleiman, M. (2012). “Insight-”Rock star” scholars a risk for islamic finance”. https://www.reuters.com/article/finance-islamic-scholars/insight-rock-star-scholars-a-risk-for-islamic-finance-idUSL5E8DG31N20120229 [accessed 19 August 2017]

- Gishkori, Z. (2015). Reforming madrassas: The revolution within. https://tribune.com.pk/story/825216/the-revolution-within/ [accessed 12 June 2017]

- Hanif, M. (2016). Economic substance or legal form: An evaluation of Islamic finance practice. International Journal of Islamic and Middle Eastern Finance and Management, 9(2), 277–295. https://doi.org/10.1108/IMEFM-07-2014-0078

- Harun, T. W. R., Rashid, R. A., & Bakar Hamed, A. (2015). Factors influencing products’ knowledge of Islamic banking employees. Journal of Islamic Studies and Culture, 3(1), 23–33. https://doi.org/10.15640/jisc.v3n1a4

- Kamarudin, A. A., & Kassim, S. (2020). An analysis of customer satisfaction on employee professionalism: A comparison between Islamic and conventional banks in Malaysia. Journal of Islamic Marketing, 12(9), 1854–1871. https://doi.org/10.1108/JIMA-03-2020-0063

- Kayani, U. N. (2022). Islamic Finance an alternative mode for short term financing–working capital management. International Journal of Islamic and Middle Eastern Finance and Management. https://doi.org/10.1108/IMEFM-07-2021-0290

- Kemal, A. R. (2005). Skill development in Pakistan. The Pakistan Development Review, 44(4), 349–357. https://doi.org/10.30541/v44i4Ipp.349-357

- Khalil, U. (2015). The madrasa conundrum. HIVE.

- Khan, M. M., & Bhatti, M. I. (2006). Why interest-free banking and finance movement failed in Pakistan. Humanomics, 22(3), 145–161. https://doi.org/10.1108/08288660610703320

- Levy, F., & Murnane, R. (2013). Dancing with robots: Human skills for computerized work Third Way.

- Maierbrugger, A. (2016). Islamic finance: Pakistan ready for big growth? https://gulfnews.com/travel/destinations/islamic-finance-pakistan-ready-for-big-growth-1.1877378 [accessed 17 March 2017]

- Nafukho, F. M., Hairston, N., & Brooks, K. (2004). Human capital theory: Implications for human resource development. Human Resource Development International, 7(4), 545–551. https://doi.org/10.1080/1367886042000299843

- O’brien, J. (2016). A new generation of islamic finance experts is required in the Middle East. https://www.entrepreneur.com/article/285821 [accessed 23 March 2017]

- Qadir, A. (2013). Between secularism/s: Islam and the institutionalisation of modern higher education in mid-nineteenth century British India. British Journal of Religious Education, 35(2), 125–139. https://doi.org/10.1080/01416200.2012.717065

- Rehman, Z. (2015). Fresh efforts being made to affiliate madrassas with Pmeb. https://www.thenews.com.pk/print/47930-fresh-efforts-being-made-to-affiliate-madrassas-with-pmeb [accessed 3 April 2018]

- Rosen, S. (1976). A theory of life earnings. Journal of Political Economy, 84(4, Part 2), S45–S67. https://doi.org/10.1086/260532

- SBP. (2019). “Islamic bulletin “. Islamic Banking Department State Bank of Pakistan.

- Sengupta, C. (2014). Consider a career in Islamic finance. https://gulfnews.com/business/personal-finance/consider-a-career-in-islamic-finance-1.1316636 [accessed 5 May 2017]

- Shaikh, I. M., Asif Qureshi, M., Noordin, K., Mehboob Shaikh, J., Khan, A., & Saeed Shahbaz, M. (2020). Acceptance of Islamic financial technology (FinTech) banking services by Malaysian users: An extension of technology acceptance model. Foresight, 22(3), 367–383. https://doi.org/10.1108/FS-12-2019-0105

- Siddiqui, A. A. (2018). Islamic finance education in Pakistan – Challenges and growth. http://www.pakistaneconomist.com/2018/11/12/islamic-finance-education-in-pakistan-challenges-and-growth/ [accessed 17 May 2019]

- Siswanti, I., & Ganis Sukoharsono, E. (2019). Intellectual capital and financial performance of Islamic banks in Indonesia. Institutions and Economies, 11(4), 31–49. https://ijps.um.edu.my/index.php/ijie/article/view/19661

- State Bank of Pakistan. (2019). Islamic banking bulletin. http://www.sbp.org.pk/ibd/bulletin/2019/Mar.pdf [accessed 2 July 2019]

- Thecityuk. (2015). The Uk: Leading western centre for Islamic finance. https://www.thecityuk.com/assets/2015/Reports-PDF/bd4af364ee/The-UK-Leading-Western-Centre-for-Islamic-Finance.pdf [accessed 17 September 2019].

- Ullah, S., Haq, M. F., & Shafique, B. (2014). Knowledge attitude and practices of Islamic banking in Pakistan. State bank of Pakistan.

- Warsame, M. H. (2016). Absence of rigorous educational programs as one of the biggest challenges. Journal of Islamic Banking and Finance, 4(1), 1–9. https://doi.org/10.15640/jibf.v4n1a1

- Woodhall, M. (1997). In H. A. B. P. & A. Wells, (Eds.), Human Capital in Education, Culture. Economy and Society. Open University Press Oxford.

- Young, E. (2016). World Islamic banking competitiveness report 2016. New Realities New Opportunities, 1–68. https://ceif.iba.edu.pk/pdf/EY-WorldIslamicBankingCompetitivenessReport2016.pdf

- Yurizk. (2013). Global Islamic Finance Education. http://reports.yurizk.com/GIFE2013/wp-content/uploads/2013/11/GIFE-2013-Look-Inside.pdf. [accessed 19 May 2017].

- Zaki, Y. (1982). The teaching of Islam in schools: A Muslim viewpoint. British Journal of Religious Education, 5(1), 33–38. https://doi.org/10.1080/0141620820050108