?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

The paper aims to provide an in-depth understanding of the effectiveness of anti-money laundering (AML) regulations in measuring banking sector stability in Western Balkan countries, as well as to explore the possibility of enhancing banking sector policy and performance. The study employs a quantitative methodology created on secondary data from 2012 to 2021. The data analysis methodology incorporates static and dynamic approaches to examine the banking sector stability using OLS and 2SLS. The results of the study show that the tight implementation of both approaches has a positive and statistically significant impact on the banking sector stability (

). The value of the paper is unique in that it applies the most recent data in this field for Western Balkans countries, and it brings benefits for a better understanding of the effectiveness of

regulations. The research will encourage fruitful discussion among policymakers, practitioners, researchers, and financial institution executives.

PUBLIC INTEREST STATEMENT

Stability in the banking sector is critical for long-term development. The development and stability of the banking sector, different factors influence, but anti-money laundering is crucial. Many indicators indirectly interfere with anti-money laundering and have a crucial impact on banking sector stability. The countries of the Western Balkans have been exposed to adverse phenomena of money laundering- (ML) in the transition period, after the turmoil in the region of the transition to the market economy. These countries need to focus on measures to combat ML and the informal economy. Effective anti-money laundering measures will undoubtedly strengthen and stabilize the banking sector and will the preconditions for sustainable economic advancement will be created. With the decision of the reliability of that market economy, they will have more chances to promote their economies and attract investments to solve the big efforts they have in employment and orientation of young people in career and as a result of emigration.

1. Introduction

The last two decades have been marked by the rapid development of sophisticated technology on the one hand, and the process of globalization on the other, which has had an impact on economic integration, capital liberalization, and the speed of financial transactions enabled by fintech created new opportunities. Nevertheless, these innovations have benefited and facilitated the actions of criminal groups on money laundering ().

means camouflaging the origin of illegal property gained via criminal operations and converting them into regular money to preserve the property, to avoid prosecution with the sole purpose of increasing the property and legitimizing it. This money circulates worldwide through the construction business, where corporations are pumped up to five times across the world before they ultimately reach a final destination in property investments, prestige vehicles, and other luxuries (Ferwerda et al., Citation2020). Moreover,

actions are not only threatening to the criminal justice system but these activities can create turmoil in financial organizations and the whole financial system. Therefore,

poses a great risk to the entire global economy (Aluko & Bagheri, Citation2012). Based on this background, policy-making structures have constructed a worldwide legislative framework for money-laundering prevention, and individual states have established relevant authorities to combat these phenomena.

Thus, the Basel Committee on Banking Supervision—BCBS, (1988) released a recommendation on the prevention of criminal use of the banking system to prevent for the first time 1988.Footnote1 Where the fundamental purpose of this guideline was to establish policies and procedures for the preclusion of

, identification or knowledge of the client, the level of compliance with laws, collaboration with law enforcement authorities, and declaration compliance. Considering the degree of risk and the importance that should be given to this phenomenon, BCBS in continuous collaboration with other authorities has issued guidelines that fight this phenomenon, on 20 July 2020, has revised the sound management of risks related to

. Whereas, in the context of the European Union (EU), this issue is regulated by the

Directive issued by the EU on the prevention of

in the banking sector (EU Directive, Citation2015/849), where it is worth noting that the latest changes in anti-money laundering (

) have been proposed by the (European Commission, Citation2021) in the

package published in July 2021.

In light of this focus, the countries treated in the analysis aspire to be part of the EU, and as a result, this strict implementation of regulation contributes in two aspects, meeting the standards set by the EU to combat money laundering and financing of terrorism, and on the other hand in creating financial stability. Based on a comprehensive examination, all countries are carefully enforcing this regulation, and it is worth mentioning that all Western Balkan countries have made updates throughout 2019 and 2020 under the 4AML Directive (EU Directive, 2015/849). Undoubtedly, this legal framework will be subject to changes once again according to the latest recommendations set by the European Commission in the

package published in July 2021. As a result, the objective of this study is to evaluate the effectiveness of AML/TF requirements for the economies of the Western Balkans, their influence on the prevention of these undertakings on the one hand, and the degree of compliance on the other. To reach this objective, the research employed the most recent data using the OLS and 2SLS econometric approaches, which are appropriate in such treatments when the criteria N ≥ T (Beck & Katz, Citation1995). Therefore, this research aims to investigate how AML requirements, asset quality management (as measured by non-performing loans (NPLs)), domestic credit financial sector, inflation, return on assets, Herfindahl–Hirschman index, inflation, unemployment, and GDP affect banking sector stability.

Using the most recent data for the Western Balkan countries, the study contributes to the provision and extension of literature to measure the influence of regulation and other factors in the

. In terms of contribution and originality, this research provides evidence for these countries because it is one of the first empirical efforts, which is considered an added value. Furthermore, panel data were employed to construct the set objectives during the research, and as a result, advantages may be discussed from a range of viewpoints. First, from an academic and scientific point of view, it contributes to the provision of detailed knowledge on the degree of impact of

regulation in the

, this argument is based on econometric findings where it eliminates dilemmas regarding the interconnection of these components. Second, it provides a unique empirical contribution utilizing data from recent years on the economies involved in the analysis, utilizing a combined econometric approach through the OLS and 2SLS estimates of the instrumental variables with an endogenous regressor. Lastly, from the standpoint of policymaking, it contributes to the identification and updating of policies that influence financial stability. The structure of the article is as follows: the second section reflects a legislative and empirical overview of the literature, the third section reflects the research methodology, the fourth section reflects the results and discussions, and the fifth section reflects the conclusion.

2. Theoretical background

2.1. Banking stability and anti-money laundering

The key objective of the BCBS’s guidelines and standards, as well as EU directives and individual countries’ supervisory agencies, is to create an environment that promotes BSS. As a consequence, the intention of this legislation is for central banks to establish and implement macroprudential policies that will enhance financial stability. The recurrence of financial crises has underscored the importance of a sustainable financial structure that can withstand financial and economic shocks. The issue of has always been in the interest of all central banks as it has direct implications for the sustainability of the banking industry itself. However, the importance of the concept of

does not mean that there is a full agreement (Segoviano & Goodhart, Citation2009; Gersl and Hermanek Citation2010; Creel et al., Citation2015; Swamy, Citation2014). This disagreement between policymakers, scholars, and other stakeholders stems from the usage of a measure that quantifies the banking sector’s stability. Regulatory bodies, such as central bank supervision, evaluate

using financial indicators based on the CAMELSFootnote2 rating, whereas researchers use the Z-score.

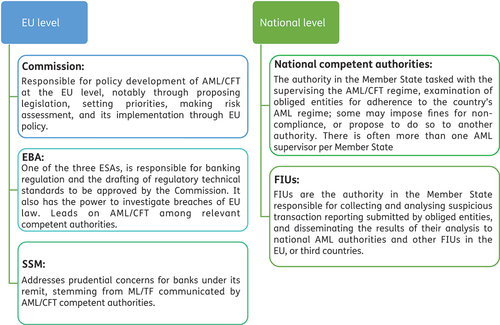

From another perspective, to ensure the policy-making structures at the global level have emphasized their focus on drafting sustainable regulations as well as the bodies in charge of observing and applying these policies on AML/TF. The Basel AML comparisons are made for each country independently based on the following five (5) components to determine the degree of compliance with this regulation: a) property of AML/FT guidelines, b) corruption and bribery risk, c) financial comprehensibility and standards, d) public comprehensibility and responsibility, and e) governmental and legal risk. Gregaite, Magnus, and Pacheco Dias Cristina (Citation2021) evaluated the directive of AML in the banking industry for euro area countries in their paper “In-depth Analysis.” They looked at recent improvements to EU Directive 2018/843, often known as the 5th AML Directive, and in specific AML—relevant EU and national authorities. Figure illustrates the structure of these actors.

Figure 1. Relevant actors to AML/FT.

As a consequence, if legislative enforcement and the designation of responsible actors are consistently applied, they will affect the prevention of AML/TF, and as a result of this prevention, the countries under surveillance will have a more stable . Although there may be resistance from some shareholders in terms of enforceability, stressing the costs of the rigorous application of this regulation. Argument’s pro and contra rigorous application of this guideline, as well as its impact on the creation of the

, will be discussed in the next section.

2.2. Empirical review of literature

In recent years, the stability of the banking sector and the entire financial system, in general, had some very critical moments and as a result, it became at the heart of scholars and policymakers. What can be considered as an added value of this field is that many studies have been conducted by different authors for certain countries or panel countries applying different financial indicators as a specific factor of the bank, but there are studies conducted applying the macroeconomic factors with the sole purpose of evaluating their impact on the . Germany is an instance of specific treatment in terms of financial and non-financial institutions. Non-financial entities have received special attention because money launderers have been influenced by them as a result of the inadequate application of AML legislation (Friedrich & Quick, Citation2019). Cotoc Bodescu et al. (Citation2020) steered comparative research of Romania’s and European nations’ legislative frameworks, assessing reports of suspicious transactions, prohibited transactions, and frozen funds as a consequence of the combat against ML. Moreover, Cotoc et al. (Citation2022) explored the trend of combating ML in the European context using nearly the same methodology as in the study of the legislative framework for Romania and European nations, incorporating data for 2018 to 2019. Furthermore, Ferwerda et al. (Citation2014) concentrated on studying AML in the outline of European Commission guidelines in the frame of European Union jurisdiction, whereas European Union (Citation2015) focused on advanced economies.

Fang et al. (Citation2014) explored transition countries, whereas Creel et al. (Citation2015) examined European Union countries, also Durguti (Citation2020) examined eurozone banks by focusing on particular banks and macroeconomic factors. Furthermore, Mansilla-Fernandez et al. (Citation2020) investigated the link between BSS and non-performing loans for eurozone banks, Ofoeda (Citation2022) examined developed and emerging African countries, as well Issah et al. (Citation2022), studied the link between AML/FT and for African countries. However, according to Galeazzi et al. (Citation2021), attention to AML/TF has risen significantly, with the AML Act being adopted in the United States in 2020, but such attention has been emphasized in Europe following a series of banking frauds (Denmark, Latvia, Cyprus, Malta, Finland, Estonia, the Netherlands, and United Kingdom), and these scandals have reinforced the need to strengthen the legal framework of AML/TF (Kirschenbaum & Véron, Citation2018; Isolauri et al., Citation2021).

Since AML/TF has a detrimental influence on the stability of the banking sector, worldwide policymakers have devised adequate instruments and mechanisms to counteract it through recommendations to financial specialists, specific business departments, and, in particular, banks and other stakeholders (Go & Benarkah, Citation2019). However, it is worth mentioning that some thoughts are suspicious about the application of this legislation since strict enforcement of this regulation would result in increased costs for businesses in general. Thus, according to Balani (Citation2019), the adoption of recent revisions in AML/TF legislation is an additional burden for banks since it influences the increase of operational costs. Adopting tangible steps to combat money laundering is critical since these activities are seen as insurmountable barriers to the correct operation of a well-organized financial structure, as well as influencing the entire financial system (Buchanan, Citation2004). In sensitivity to AML/TF effectiveness, Usman-Kemal (Citation2014) emphasizes that the banking industry is highly susceptible to this risk due to banks’ dealing with the deposit, transfer, and withdrawal of funds. As a consequence, authorities and financial organizations must analyze the efficiency of AML/TF regulations before making subjective judgments. Finally, the other explanatory variables are generally discussed in depth in the subsection where the variables are developed.

3. Research methodology

3.1. Data and sample

The research sample consists of six Western Balkan countries (Albania, Kosovo, North Macedonia, Montenegro, Bosnia & Herzegovina, and Serbia), using panel data covering the period 2012 to 2021. The sample was selected based on data availability. The inclusion of this period in the research is determined by the anti-money laundering variable since the Basel Institute for Corporate Governance (BICG) started publishing the “Basel AML index” in 2012. The reason for using data on an annual basis (aggregated at the country level for all variables) is a result of the AML variable. The BICG annually evaluates each country separately according to the defined criteria and those evaluations are published in the “Basel AML Index”. The research to achieve credible results includes the combined variables including those specific to the banking industry as well as macroeconomic ones. The data used are secondary and provided by the World Bank database and International Monetary Fund. This data is processed according to the standards set by the WB and IFM, and as such is used by various researchers. And this fact provides a solid basis that the results that will be generated from this study will be robust and credible.

3.2. Variables

Numerous academics have used different determinants as explanatory or control variables to analyze the influence of certain features in financial organizations as well as macroeconomic factors on the stability of the banking sector. In general, several methodologies have been used to analyze the banking sector stability (), with the majority of the research being evaluated using the Z-score (Cuestas et al., Citation2020; Yiewi et al., Citation2014; Issah et al., Citation2022; Ofoeda, Citation2022). The variables in this study were carefully chosen, including significant banking systems and macroeconomic ratios, as shown in Table .

Table 1. Variable descriptions and data sources

The dependent variable in the context of this research is defined as , where most studies have made this calculation using Z-score. According to the author Cuestas et al. (Citation2020), Z-score enables the degree of comparison between capitalization and returns from risk to identify the degree of riskiness of a financial institution, respectively, a bank. There is a converse association between the likelihood of a financial institution becoming insolvent and the Z-score. The dataset for computing the Z-score was retrieved annually from the IMF library for two bank metrics, ROA and CAR, and then the BSS was computed using the algorithm. The Z-score assessor is calculated by including the return on assets (ROA) plus capital asset ratio (CAR) proportional to the standard deviation of the return on assets and is expressed as in the formula:

The results of the Z-score show that the higher the value of this evaluation we have the higher the stability, and vice versa. A flaw in this estimator is considered to be biased and for this issue, we have applied the natural logarithm of which is usually used as a distribution for measuring

.

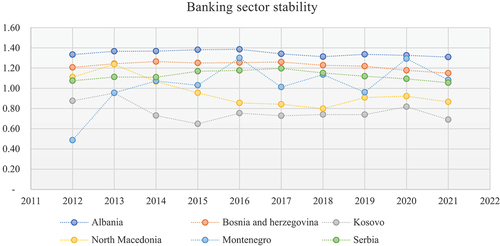

Figure displays the trend for each country involved in the survey. From this reflection, we can conclude that all countries have identical stability, with a small difference excluding Kosovo.

Figure 2. The trend of banking sector stability.

Independent variable: To measure , as the primary objective is the

regulation. This variable will be measured using the Basel anti-money laundering index, which is published on an annual basis by the Basel Institute for Governance. The institute’s methodology for evaluating country rankings is based on the efficiency of institutions, mechanisms, and procedures for combating money laundering. The

index’s ranking is based on five components and varies from 0 to 10, with 0 indicating the lowest level of risk for money laundering and financing terrorism and 10 indicating the highest level of risk. Several prominent researchers have used the same ranking to estimate the level of

‘s significance, and we will highlight some of the most current research in this field (Agoba et al., Citation2019; Isaac et al., Citation2020; Issah et al., Citation2022).

Explanatory variables: non-performing loans, which are directly tied to credit risk and any degradation of the loan portfolio affect the destabilization of the liquidity statements within the bank and the financial structure wide-ranging is another substantial variable that influences the BSS. This banking indicator reflects the ratio of loans that are overdue for more than 90 days divided by total loans, aggregated for each country included in the investigation. The World Bank database was used to obtain the data for this variable. This variable’s use is based on a study by (Mansilla-Fernandez et al., Citation2020). The domestic credit financial sector—, which reflects the size of the bank, will be used to measure the size and stability of the banking sector in the context of this study. It is important to remember that a larger banking sector can also be correlated with instability, since if there is a lot of competitiveness, banks may be tempted to take on even more risk (Ozili., Citation2018). They may incur losses during various intervals as a result of high-risk exposure, leading to the destabilization of the financial system (Ozili., Citation2018). Pietro and Leonida (Citation2018) examined 68 economies throughout the period 1997–2015 from a unique perspective. According to them, a low level of concentration improves the BSS, while a high concentration makes the BSS more fragile due to the cost of loans, expansion, and supervision. Inflation in the simplest sense reduces the value of future money which directly leads to an increase in the interest rate, and at the same time, an increase in the interest rate affects the increase in the cost of capital for various business activities (Isaac et al., Citation2020). In certain instances, the estimators ROA and HHI are used. ROA is one of the three profitability measures, and it indicates the ratio of net income to total average assets or total assets at the end of the period. This ratio reflects a company’s earnings (net income) to the capital invested in assets to determine how well it is operating. Employing panel regression, Xu et al. (Citation2019) investigated how bank profitability influences financial stability in the U.S., advanced European countries, and GSIB countries. Their results indicate that there is a significant link between them.

The Herfindahl–Hirschman index, on the other hand, is used to measure market concentration in predicting the intensity of competitiveness, and in our scenario, this predictor will be employed to see if it has any effect on banking stability. Using the GMM method, Noman et al. (Citation2017) investigated whether the dimension of competition enhances financial stability in the banking industry in ASEAN countries. The data for these two predictions were taken from the IFM database and expressed in coefficients. Consequently, they are reliable data for this study. Finally, the unemployment variable, which is a macroeconomic component that obviously affects the . The increase in the unemployment rate progressively affects the probability of non-payment of loan obligations, and as a result, non-payment destabilizes banking stability. The same findings have been reached by the authors in their studies (Boateng et al., Citation2015; Yiewi et al., Citation2014).

3.3. Research question and hypothesis

After defining the factors employed in the econometric approach and validating their influence on the predicted variable, we will propose the research question and key hypothesis in this component. As a result, attempt to achieve this aim, we are considering the underlying research questions:

RQ: Does the adequate implementation of AML regulations in the case of Western Balkan countries affect the creation of banking sector stability?

As a consequence of the research question, we will present the research’s core hypothesis as follows:

Ho: Adequate implementation of AML regulations has a significant positive influence on banking sector stability.

3.4. Empirical model

The main objective of this research is to examine the influence of anti-money laundering legislation, bank-specific factors, and macroeconomic factors on banking sector stability in Western Balkan economies from 2012 to 2021. The study was based on panel data from six (6) countries collected over a ten-year dated, with a total of 60 observations. The study on the contributing aspect of in the countries of the Western Balkans will be based on the above-mentioned treatments, but given the characteristics and specifics of the factors applied in this research. According to Cameron and Trivedi (Citation2005), in conditions when we are dealing with NT (number of panel economies and time series), the linked observations contain less evidence than the independent observations. Therefore, ignoring the possible correlation of disturbance regression over time and between panels can lead to one-sided conclusions. The latest research that incorporates a regression in panel data corrects standard errors of estimated parameters for possible residual dependency to preserve the validity of statistical discoveries (Beck & Katz, Citation1995). In conditions where the N < T criterion with the panel data is suggested to apply 2SLS the approach tends to produce optimistic estimates for SE (Beck & Katz, Citation1995). Thus, our research also applied a mixed approach, using OLS and 2SLS based on the study of Durguti and Kryeziu (Citation2021).

Nevertheless, using the dynamic approach of the panel is more relevant in the situation of this research, as the instrumental variables 2SLS estimator calculates the endogeneity and instrumental weak issues arising from the association between and selected variables. In the following, we will introduce the dynamic panel equation.

Based on the basic construction of the equation, in our concrete situation applying the dynamic panel data estimation would be:

In addition, since the equations presented beyond, we will present the concrete equation for the Banking stability sector—.

Meanwhile, along with more explanatory variables in the study’s paradigm, Equationequation 3(3)

(3) is expanded as follows:

4. Econometric findings and discussion

4.1. General summary statistics

Table presents the descriptive breakdown of the factors examined in the study. The total number of observations is 60 for the six Western Balkan countries (W.B.C), followed by mean, standard deviation, minimum, maximum, and Jarqua Bera. Bank stability sector data generated for W.B.C. are 8.32 with a standard deviation of 5.85. These results give us indications that the W.B.C can be considered to be in the area of financial stability. This argument is based on the Z-score ranking area, where a result of 0–1.8 is deemed unstable, 1.8–3.0 is known as the gray zone and is believed to have a low threat, and a rating of 3 or more is considered to be in a safe zone. The mean rate of regulation is 3.48. The rating is scaled from 0 to 10, where 0 signifies the lowest risk degree of

regulating compliance and 10 indicates the maximum risk level of

regulating compliance. The implication of the mean of 4.78 implies that

legislation effectiveness in W.B.C. seems to be quite low.

Table 2. Summary of descriptive statistics

During the observation period, non-performing loans had a mean value of 10.12, a minimum value of 1.93, and a maximum value of 22.24. The mean amount of domestic credit granted by the financial sector was 54.64%, while inflation was 1.53%. Based on qualitative metrics, the return on assets (ROA) has a mean value of 1.13, indicating that the economies included in the analysis have a high degree of profitability, whereas the standard deviation for this parameter is 0.06. HHI, on the other hand, has an arithmetic mean of 0.14, a maximum value of 0.25, and a standard deviation of 0.07. The investigation continues with the unemployment rate, which has a mean amount of 20.37. Finally, based on the findings, we can infer that the WB economy’s mean GDP value is 2.46, with maximum and minimum values of 12.43 and −15.31, respectively. Table also includes more comprehensive specific data. The Jarque-Bera evaluation was used to determine if the data in the panel had a normal distribution, and the p-value results of this evaluator are statistically insignificant, confirming that the data have a normal distribution.

Due to the obvious possible collinearity of the applied statistics, the connection relating to the pairs of explanatory parameters was examined before beginning the design of the econometric model. This situation distorts the measurement of variable values, as well as their level of importance and the direction of the effect on the predicted parameters. In terms of econometrics, there is currently no adequate test for detecting multicollinearity in panel models. According to Baltagi (Citation2015), in empirical works that use panel patterns for the detection of multicollinearity, association constants between pairs of latent explanatory parameters are used (Table ).

Table 3. Correlation matrix

The association examination reveals that pairs of explanatory parameters should not cause multicollinearity since the interaction is extremely weak in all scenarios. According to the results in (Table ), exhibits a moderated confident connection with

,

, and

. Although there is an adverse relationship between the

,

,

,

, and

with the

.

Furthermore, the most popular evaluation utilized for the multicollinearity issue is the VIF evaluation, where the findings are shown in (Table ) in which the mean value is 1.31 and validate the ascertainment discovered by the correlation analysis that the data have no concerns with multicollinearity.

Table 4. VIF analysis

4.2. Empirical findings

This section reports overall issues such as F-test, R-squared, and Wald chi2 (4) test, then proceeds with regression estimates and then confirms the fit and adequacy of the models treated by post-estimation test as Sergan, Durbin chi (1), and Wu-Hausman. The OLS model and the 2SLS model were applied to assess the degree of impact of , and other determinants defined in the

for the Western Balkan countries. The results of the F-test from the OLS model (F = 12.26, with probability ρ = 0.000) show that all the data in the model are unbiased and the model is generally significant at the level of 99% reliability since the value ρ > F is 0.000 and is less than α = 0.01. As well, in the 2SLS model, the reliability level model is 95% since the value ρ > wald chi2 (4) is 0.0303, which means that it is less than α = 0.05. R-squared according to the OLS has a constant of 0.6580% or 65.80% of the banking stability sector is described by the determinants applied in the research, while the rest is described by other determinants, while according to the 2SLS, it has a constant of 0.6516% or 65.16% described by the determinants applied in the research while the rest is described by the determinants which are not included in the research [see table no. 5].

The empirical data reported in Table , applied to the evaluation and degree of effectiveness in , reveal that tight

implementation, proper asset quality management—

, and

have positive effects on both models in the creation of

. Whereas the inflation rate—

and the unemployment rate—

have shown statistically significant effects with negative signs in sustaining the

. An unexpectedly insignificant effect has been discovered to be connected to the variable

,

, and

. The panel analysis’s econometric results indicate that anti-money laundering legislation has a statistically significant and favorable effect on the

in Western Balkan nations. This is stated since coefficient β = 0.09678, and statistical significance ρ = 0.000 according to OLS, while β = 0.03628, and ρ = 0.019 according to 2SLS. These results indicate that the examined economies have a satisfactory rating in terms of the

index, and as such, any increase in the effectiveness of

will affect the stability of the banking sector. As a consequence, the positive association between these two analyzed factors is compatible with the predicted results. In line with our findings, the authors Isaac et al. (Citation2020) and Issah et al. (Citation2022) report a positive link between

and

in African countries. Secondly, from the perspective of

prevention, these findings are compatible with the Basel Committee’s aims for the sound application of

guidelines, which successfully impact the

and preserve its integrity to customers (BIS, Citation2020).

Table 5. Estimation results

The second variable used to explain the impact of in the Western Balkan countries asset quality management, respectively, non-performing loans. The asset quality management variable measures the perception of the ability of the regulatory authorities of countries to create the banking stability sector, which creates a favorable environment for business development. Non-performing loans were found to be important in establishing the stability of the banking sector at a level of 1%. This result gives us indications that any decrease in the non-performing loans rate has a direct impact on the increase of the banking stability sector, and conversely, an increase in this ratio reduces the degree of stability. A study conducted by Ferwerda et al. (Citation2020) confirms the findings of this study by arguing that adequate asset quality management, respectively,

has a significant impact on financial stability by analyzing euro area banks. This phenomenon according to this study in the economic aspect is more significant for unlisted financial institutions, concerning those listed. Furthermore, Atoi (Citation2018) applying the GMM dynamic approach has analyzed the impact of

on the banks’ stability in Nigeria. Econometric results according to this research confirm the hypothesis of moral hazard in the correlation risk versus return of efficient market theory. And the most important finding is that international banks more easily withstand the shocks resulting from the growth of

, compared to national banks.

Additionally, based on the two techniques used, the other component engaged in the research to analyze the effect of the creation of the for the countries of the Western Balkans is domestic private credit from the banking segment, which turns out to be statistically insignificant. This is evidenced from the results presented in Table , where the coefficient β (according to—OLS β = .00262, with ρ = 0.115; and 2SLS—β = .01107, with ρ = 0.234). In this light, our results are consistent with Akpansung’s (Citation2018) conclusion that this component has a favorable but statistically insignificant influence on the

. Other determinants that have proven to be influencers in the

were macroeconomic matters such as inflation and unemployment. At a confidence level of 5%, both of these determinants have a negative influence on the

for Western Balkan countries. These findings indicate that any increase in inflation and unemployment has a direct effect on the banking sector’s stability. Therefore, the policy-making bodies to promote overall financial stability, in addition to specific factors of the banking industry should create stability in macro-fiscal terms, and in particular in inflation as we have continuous price increases as a result of the post-pandemic period and current developments in Ukraine. The findings of the empirical analysis tend to correspond with those of studies by (Feldkircher et al., Citation2021; Carvahlo et al. Citation2018; Pietro & Leonida, Citation2018; Bernal-Verdugo et al., Citation2013), who suggests that when financial and banking crises occur, these two components influence negatively financial stability.

In terms of macroprudential evaluation, growth is a key element in determining financial stability, particularly in BSS. As a result, Tabash (Citation2019) explored the correlation between

and

using an econometric approach known as Pooled Ordinary Least Squares (POLS) to evaluate the hypotheses. According to the conclusions of this study, there is substantial interaction between them. Furthermore, Yilmaz et al. (Citation2020) examined the correlation between

growth and

for transition economies in the European Union, examining the causal dynamic impacts between economic development and

from 1998 to 2016. The research used the cointegration test between countries to reach insights, and they conclude that there is a positive link between these two metrics in the long and short term. Therefore, our findings are consistent with previous studies, the coefficient (β = .00323, with ρ = 0.012 according to OLS) and (β = 0.1410; ρ = 0.008 according to 2SLS) demonstrate that there is a significant interaction with the level of reliability 99%.

4.3. Post estimation test

After analyzing the initial general tests, and the coefficients evaluated according to OLS and 2SLS, to further verify the stability and suitability of the applied models, several post-diagnostic tests were used. To test whether the data applied in the model have a problem with heteroskedasticity, Breusch-Pagan/Cook-Weisberg was applied, where the result according to this examination rejects the basic premise since the ρ = 0.2138. This result proves that the applied data have no problems with heteroskedasticity. For the 2SLS model, the following post-diagnostic tests have been applied: Sergan test with ρ = 0.0762 which proves the variables used as instrumental are adequately adjusted since the ρ—value is greater than α = 0.05. This result provides a sufficient indication to refuse the null premise that “instruments are not valid”. Finally, to verify the validity and adequacy of the 2SLS model, the Durbin chi (1) and Wu-Hausman tests, known as the endogeneity test, are presented and the results presented in Table show that both of these tests have been insignificant (ρ = 0.1132, respectively, ρ = 0.1162) that provide solid evidence that the model is perfectly tailored.

5. Conclusion

Considering the continual development of technology and the process of globalization on the one hand, and the ongoing struggle by relevant agencies and money launderers on the other, measuring the impact of AML/TF regulation is essential for the countries under consideration. As a result, the overall aim of this study was to investigate how AML/TF legislation, adequate asset quality management (NPLs), domestic credit to the private sector, ROA, HHI, inflation, unemployment, and GDP influence the BSS. To accomplish this goal, a suitable technique was chosen, beginning with the treatment of data using general statistics, followed by the appropriate tests to prove the robustness of the models, the use of the combined approach, and lastly some post-diagnostic testing. This research yielded several interesting results. First, as an initial conclusion, it was found that all economies involved in the study are already using AML/TF legislation, with recent modifications made in 2019 and 2020. Second, the mean value based on empirical analysis for BSS and AML/TF provides indications that these economies have stable banking stability, and on the other hand, the value of risk according to the AML index is 4.78 points. Third, the study discovered that AML/TF regulations and proper asset quality management as a specific factor in the banking industry had a beneficial impact on the creation of the based on the OLS and 2SLS assessments. Nevertheless, the remaining two macroeconomic indicators, inflation, and unemployment indicate that any increases in them will undermine

. As a result, rigorous compliance with AML/TF legislation can greatly stimulate

in Western Balkan countries. These findings are expected to be a valuable reference for policy-making institutions that, if given sufficient significance and focus on combatting and preventing money laundering at the national and Western Balkans levels, will have an even higher incentive and

. Finally, the competent authorities should collaborate with other international entities such as the World Bank, IMF, and UN to build a database on money laundering and other financial crimes. Numerous researchers avoid performing research on money laundering due to insufficient data on the issue.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

Notes on contributors

Esat Durguti

Esat Durguti has completed his Ph.D. at the University of Tirana, Department of Finance, and is an Associate Professor at the University of Mitrovica. Mr. Durguti has rich experience in the field of public finance and the financial industry.

Erëza Arifi

Erëza Arifi completed Ph.D. studies at the Faculty of Economics, the University of Tirana in the Department of Finance. She has a considerable number of scientific international publications.

Emine Gashi

Emine Gashi had completed a Master of Science in finance and she has advanced experience in the field of research and specializes in data analyses. She has a considerable number of scientific publications and participation in conferences with international reviews, mainly in the field of finance.

Muhamet Spahiu

Muhamet Spahiu has more than two decades of experience in wide economic sectors and has completed his Ph.D. in European “Union Law and International Business Law” at the ECPD of the University of Peace, founded by the United Nation.

Notes

1. Basel Committee on Banking Supervision (1998): Prevention of criminal use of the banking system for the purpose of money-laundering. https://www.bis.org/publ/bcbsc137.htm

2. CAMELS: The system, known as CAMELS, means the use of financial indicators such as C-capital, A-asset quality, M-management, E-earnings, L-liquidity, and S-interest rate sensitivity.

3. European Court of Auditors (2020); The EU’s anti-money laundering policy in the banking sector. June, 2020. https://www.eca.europa.eu/Lists/ECADocuments/AP20_05/AP_anti-money-laundering_EN.pdf

References

- Agoba, A. M., Abor, J. Y., Osei, K., Sa-Aadu, J., Amoah, B., & Dzeha, G. C. O. (2019). Central bank Independence, elections and fiscal policy in Africa: Examining the moderating role of political institutions. International Journal of Emerging Markets, 14(5), 809–16. https://doi.org/10.1108/IJOEM-08-2018-0423

- Akpansung, A. O. (2018). Analysis of the impacts of domestic debts on private sector credit, lending rate, and real output: Evidence from nigeria. Journal of Finance and Economics, 6(3), 111–123. https://doi.org/10.12691/jfe-6-3-5

- Aluko, A., & Bagheri, M. (2012). The impact of money laundering on economic and financial stability and on political development in developing countries: The case of Nigeria. Journal of Money Laundering Control, 15(4), 442–457. https://doi.org/10.1108/13685201211266024

- Atoi, N. V. (2018). Non-performing Loan and its effects on banking stability: Evidence from National and International Licensed Banks in Niger, CBN.Journal of Applied Statistics (JAS), 9, 2. https://dc.cbn.gov.ng/jas/vol9/iss2/3

- Balani, H. (2019). Assessing the introduction of anti-money laundering regulations on bank stock valuation: An empirical analysis. Journal of Money Laundering Control, 22(1), 76–88. https://doi.org/10.1108/JMLC-03-2018-0021

- Baltagi, B. H. (2015). The Oxford handbook of panel data (4th ed.). Oxford University Press.

- Beck, N., & Katz, J. N. (1995). What to do (and not to do) with time-series cross-section data. The American Political Science Review, 89(3), 634–647. https://doi.org/10.2307/2082979

- Bernal-Verdugo, L. E., Furceri, D., & Guillaume, D. (2013). Banking crises, labor reforms, and unemployment. Journal of Comparative Economics, 41(4), 1202–1219. https://doi.org/10.1016/j.jce.2013.03.001

- BIS. (2020). Guidelines: Sound management of risk related to money laundering and financing of terrorism. Bank for International Settlements. https://www.bis.org/bcbs/publ/d505.pdf (accessed 03 June 2022)

- Boateng, A., Hua, X., Nisar, S., & Junjie, W. (2015). Examining the determinants of inward FDI: Evidence from Norway. Economic Modelling, 47, 118–127. https://doi.org/10.1016/j.econmod.2015.02.018

- Buchanan, B. (2004). Money laundering—a global obstacle. Research in International Business and Finance, 18(1), 115–127. https://doi.org/10.1016/j.ribaf.2004.02.001

- Cameron, A. C., & Trivedi, P. K. (2005). Microeconometrics: Methods and Applications. Cambridge University Press. http://dx.doi.org/10.1017/CBO9780511811241

- Commission, E. (2021). Preventing money laundering and terrorist financing across the EU. How does it work in practice? European Commission. https://www.europarl.europa.eu/thinktank/en/document/IPOL_IDA(2021)659654

- Cotoc Bodescu, C. N., Șcheau, M. C., & Achim, M. V. (2020). Anti money laundering effectiveness from a legal framework perspective in Romania and European Countries. In Proceedings of 19th RSEP CONFERENCES (pp. 16). Anglo-American University, Prague, Czechia.

- Cotoc, B. C., Șcheau, M. C., & Achim, M. V. (2022). TRENDS IN COMBATING MONEY LAUNDERING IN THE EUROPEAN CONTEXT. DIEM, 7(1), 142–152. https://doi.org/10.17818/DIEM/2022/1.14

- Creel, J., Hubert, P., & Labondance, F. (2015). Financial stability and economic performance. Economic Modelling, 266800, 1–26. https://doi.org/10.1016/j.econmod.2014.10.025

- Cuestas, J. C., Lucotte, Y., & Reigl, N. (2020). Banking sector concentration, competition and financial stability: The case of the Baltic countries. Post-Communist Economies, 32(2), 215–249. https://doi.org/10.1080/14631377.2019.1640981

- de Carvalho, A. R., Rafael, S., & Ribeiro, M. (2018). Economic development and inflation: A theoretical and empirical analysis. International Review of Applied Economics, 32(4), 546–565. https://doi.org/10.1080/02692171.2017.1351531

- Durguti, E. (2020). Challenges of banking profitability in eurozone countries: Analysis of specific and macroeconomic factors. Naše gospodarstvo/Our Economy, 66(4), 1–10. https://doi.org/10.2478/ngoe-2020-0019

- Durguti, E. A., & Kryeziu, N. (2021). Importance of Corporate Governance: Evidence from Kosovo’s Banking Sector. Croatian Economic Survey, 23(2), 5–32. https://doi.org/10.15179/ces.23.2.1

- European Union. (2015). Directive (EU) 2015/849 on the prevention of the use of the financial system for the purposes of money laundering or terrorist financing, amending Regulation (EU) No 648/2012 of the European Parliament. http://data.europa.eu/eli/dir/2015/849/oj

- Feldkircher, M., Huber, F., & Pfarrhofer, M. (2021). Measuring the effectiveness of US monetary policy during the COVID-19 recession. Scottish Journal of Political Economy, 00, 1–11. https://doi.org/10.1111/sjpe.12275

- Ferwerda, J., van Saase, A., Unger, B., & Getzner, M. (2020). Estimating money laundering flows with a gravity model-based simulation. Scientific Reports, 10(1), 1–11. https://doi.org/10.1038/s41598-020-75653-x

- Friedrich, C., & Quick, R. (2019). An analysis of anti-money laundering in the German non-financial sector. Journal of Management and Governance, 23(4), 1099–1137. https://doi.org/10.1007/s10997-019-09453-5

- Galeazzi, M.-A., Mendelson, B., & Levitin, M. (2021). The anti-money laundering act of 2020. Journal of Investment Compliance, 22(3), 253–259. https://doi.org/10.1108/JOIC-05-2021-0023

- Gersl, A., & Hermanek, J. (2010). Financial Stability Indicators: Advantages and Disadvantages of their Use in the Assessment of Financial System Stability. Occasional Publications-Chapters in Edited, 69–79. Occasional Publications-Chapters in Edited http://ideas.repec.org/h/cnb/ocpubc/fsr06-2.html.

- Go, L., & Benarkah, N. (2019). Quo Vadis legal profession participation in anti-money laundering. Journal of Money Laundering Control, 22(4), 764–769. https://doi.org/10.1108/JMLC-12-2018-0072

- Gregaite, K., Magnus, M., & Pacheco Dias, C. S. (2021). Preventing money laundering in the banking sector - reinforcing the supervisory and regulatory framework. European Parliament. https://www.europarl.europa.eu/thinktank/en/document/IPOL_IDA(2021)659654

- Isaac, O., Agbloyor Elikplimi, K., Abor Joshua, Y., & Osei Kofi, A. (2020). Anti-money laundering regulations and financial sector development. International Journal of Finance & Economics, 1–20. https://doi.org/10.1002/ijfe.2360

- Isolauri, E. A., Zettinig, P., & Nummela, N. (2021). Emerging international compliance: Policy implications of a money laundering case. Journal of International Business Policy. https://doi.org/10.1057/s42214-021-00127-4

- Issah, M., Antwi, S., Antwi, S. K., Amarh, Amarh, P., & Amarh, P. (2022). Anti-Money laundering regulations and banking sector stability in Africa. Cogent Economics & Finance, 10(1), 2069207. https://doi.org/10.1080/23322039.2022.2069207

- Kemal, M. U. (2014). Anti-money laundering regulations and its effectiveness. Journal of Money Laundering Control, 17(4), 416–427. https://doi.org/10.1108/JMLC-06-2013-0022

- Kirschenbaum, J., & Véron, N. (2018). A better European Union architecture to fight money laundering. Bruegel Policy Contribution Issue N°19, Policy Paper. http://bruegel.org/2018/10/a-better-european-union

- Levi, M. (2012). How well do anti-money laundering controls work in developing countries? In: Reuter P (ed) Draining development? The World Bank, Washington, pp 373–413. https://doi.org/10.1596/978-0-8213-8869-3

- Manuel Mansilla-Fernández, J. (2020). Non-Performing Loans, financial stability, and banking competition: Evidence for listed and non-listed Eurozone banks. Hacienda Pública Española Review of Public Economics, 232(1), 29–52. https://doi.org/10.7866/HPE-RPE.20.1.2

- Noman, A. H. M., Gee, C. S., Isa, C. R., & Hernandez Montoya, A. R. (2017). Does competition improve financial stability of the banking sector in ASEAN countries? An empirical analysis. PLoS ONE, 12(5), e0176546. https://doi.org/10.1371/journal.pone.0176546

- Ofoeda, I. (2022). Anti-money laundering regulations and financial inclusion: Empirical evidence across the globe. Journal of Financial Regulation and Compliance, 30(5), 646–664. https://doi.org/10.1108/JFRC-12-2021-0106

- Ozili, P. K. (2018). Banking stability determinants in Africa. International Journal of Managerial Finance, 14(4), 462–483. https://doi.org/10.1108/IJMF-01-2018-0007

- Pietro, C., & Leonida, L. (2018). Concentration in the Banking Sector and Financial Stability: New Evidence (English). Policy Research working paper, no. WPS 8615 Washington, D.C.: World Bank Group. http://documents.worldbank.org/curated/en/953311539698216215/Concentration-in-the-Banking-Sector-and-Financial-Stability-New-Evidence.

- Segoviano, M. A., & Goodhart, C. (2009). Banking stability measures. IMF Working Paper - International Monetary Fund, 1–56. https://doi.org/10.5089/9781451871517.001

- Swamy, V. (2014). Testing the interrelatedness of banking stability measures. Journal of Financial Economic Policy, 6(1), 25–45. https://doi.org/10.1108/JFEP-01-2013-0002

- Tabash, M. I. (2019). Banking Sector performance and economic growth: An empirical evidence of UAE Islamic Banks. Creative Business and Social Innovations for a Sustainable Future. Advances in Science, Technology & Innovation https://doi.org/10.1007/978-3-030-01662-3_6

- Xu, T., Hu, K., & Das, U. S. (2019). Bank Profitability and Financial Stability. Monetary Economics: International Financial Flows - International Monetary Fund. Retrieved July 21, 2022, https://www.imf.org/en/Publications/WP/Issues/2019/01/11/Bank-Profitability-and-Financial-Stability-46470

- Yiewi, F., Iftekhar, H., & Marton, K. (2014). Institutional development and bank stability: Evidence from transition countries. Journal of Banking & Finance, 39, 160–176. https://doi.org/10.1016/j.jbankfin.2013.11.003

- Yilmaz, B., Djula, B., Gavriletea, D., & Marius. (2020). Banking sector stability and economic growth in post-transition European Union countries. International Journal of Finance & Economics, 26(1), 949–961. https://doi.org/10.1002/ijfe.1829