Abstract

This study seeks to determine Ghanaians’ perceptions of the new electronic transaction levy (E-levy) and the impact of their perception on their intention to use electronic transactions (ETs) that attract the levy, financial inclusion (FI) and financial well-being (FW). To achieve this, the study employs PLS-SEM with a sample size of 782. Generally, we found Ghanaians have limited knowledge on E-levy. Thus, Ghanaians should be re-educated about E-levy. We again document that the perception of Ghanaians towards E-levy is negative. Also, we found most Ghanaians intend to reduce their patronage of ETs that attract levy. Furthermore, Ghanaians’ perception of the E-levy reduces their intention to use ETs that are affected by the levy and, by extension, adversely affect FI and FW. Hence, based on the perception of Ghanaians, the E-levy introduced is a curse. We recommend that the government of Ghana review the E-levy policy to minimize its negative effects. We specifically suggest that government raise the GH¢100 per day transaction exemption threshold to increase the intention to use ETs and FI; moreover, government can exempt businesses that pay income tax from E-levy to reduce the tax burden on their income. Also, government should re-enlighten the public on the benefits of E-levy to the country, reassuring the public of accountability and honesty in implementing the E-levy policy to increase their intention to patronize ETs that attract levy. Again, we record a significant and positive total effect of FI on FW. Thus, additionally, government should introduce policies that ensure FI.

1. Introduction

On 17 November 2021, during the reading of the 2022 budget, the Minister of Finance (Ghana), Ken Offori-Atta, announced the introduction of a levy on electronic transactions in Ghana (Ministry of Finance, Citation2022). The electronic transaction levy, popularly known as E-levy, was initially said to be pegged at 1.75% and was to take effect from 1 February 2022 (Minister of Finance, Citation2021). Following further consideration, the E-levy charge was reduced to 1.5% and implementation took effect on 1 May 2022 (Oni & Gasparri, Citation2022). The E-levy charge covers mobile money payments, bank transfers, merchant payments, and inward remittances (Ghana Revenue Authority, Citation2022). The originator of the transaction will bear the charge except for the inward remittance, which will be borne by the recipients (Oni & Gasparri, Citation2022). There is, however, an exemption for transactions up to GH¢100 per day (Ghana RevenueAuthority, Citation2022).

Various justifications were given by the government of Ghana on why there is a pressing need for the payment of E-levy in Ghana. According to the government, Ghana’s tax-to-GDP ratio is barely 13%, well below the 15% per GDP threshold. Thus, the introduction of the E-levy would help widen the tax net from 13% to 16%. It argued further that it would widen the tax income generated from the informal sector (The President of Ghana, Citation2022). This is necessary because, for years, the informal sector in Ghana has been said to be poor at tax compliance (Okpeyo et al., Citation2019). Also, government through the Ghana Revenue Authority (Citation2022) and the Minister of Finance (Citation2022), enumerated various activities that the income generated from the E-levy would help undertake. Among them were as follows: first, it would be a driving force for Ghana to battle its high debt; second, it would be used to support and widen entrepreneurship in Ghana; again, it would be employed to finance infrastructure in Ghana; and it would give most Ghanaians the opportunity to contribute toward the nation’s development.

Following the social psychology theory which indicates that, in assessing the citizen’s tax compliance behaviour, one must know how the taxpayer considers the country in his mind (Noguera, Quesada, Tapia & Llacer, Citation2014), the perception of Ghanaian residents is, therefore, paramount to the successful implementation of the E-levy policy. Also, using equity theory, which concentrates on whether the distribution of resources is fair to both relational partners (in the case of this study, levy payers and government; Adam et al., Citation1963), we argued that the possible reason why Ghanaians might not patronize electronic transactions (ETs) with the E-levy payment is the perceived equity (fairness) between earlier taxes paid and the return given back to the public by the government. However, Ghanaians’ reactions to the E-levy on social media have been mixed, with several criticisms from a large portion of the Ghanaian population since its announcement. Most of the arguments have been centred on the possible impact of the introduced E-levy on financial inclusion (FI) and financial well-being (FW) of the people of Ghana (Oni & Gasparri, Citation2022; Sulemana, Citation2022).

For instance, many have argued that the introduction of E-levy would force people to use cash, driving them away from ETs in Ghana (Anokye, Citation2022). This might undermine Ghana’s recent achievement of 100% FI, according to State of Inclusive Instant Payment in Africa 2022 report (AfricaNenda Accelerating Inclusive payment system, Citation2022). However, this achievement was made possible by the increase in mobile money accessibility in Ghana (Hesse, Citation2022). As per other platforms of FI, Sulemana (Citation2022) indicated low FI in Ghana, and the presence of E-levy might increase the already existing issue of low FI. Meanwhile, empirical evidence and supply-leading theories have emphasized the relevance of FI to the economic growth of a country (Van et al., Citation2021; Kim et al., Citation2018). The government of Ghana, however, debunked the possibility that E-levy would result in the reduction of FI in Ghana by arguing that the Ghanaian population is accustomed to ETs and their convenience and would, therefore, find it difficult to revert from them.

Again, when it comes to FW, the people of Ghana indicate that payment of E-levy would eventually affect the cash they have in their pocket and their ability to save and invest (International Center for Tax and Development, Citation2022). In addition, the people argued that E-levy would have an adverse effect on their business income since the E-levy charge would be additional expenses against the income of their business, and thus, the profit would shrink (International Center for Tax and Development, Citation2022; Sulemana, Citation2022). Other Ghanaians also indicated that, contrary to tax benefit theory, which indicates that tax payment should translate into the FW of taxpayers (Wicksell, Citation1896;), the government of Ghana has not been able to channel the previous taxes paid into their FW. Thus, they believe this E-levy too will not be different. However, the government of Ghana insisted that E-levy would rather enhance the financial well-being of Ghanaians because the income generated from E-levy would help provide facilities (such as education and employment) that enhance FW in an economy.

We, therefore, sought the perception of Ghanaians on whether the introduction of the E-levy in Ghana would be a blessing or a curse. Aside from the debates on social media, there is a dearth of empirical evidence on Ghanaians’ perception of E-levy. Thus, the study’s originality lies in being the first to assess Ghanaians’ perception of E-levy. Furthermore, there is a lack of literature on how Ghanaians’ perceptions of E-Levy can affect their intention to use ETs that attract levy, FI, and FW. We focus our attention on the E-Levy for three main reasons: First, passing the E-levy bill would only be successful if residents’ perceptions were supportive. Secondly, a democratic economy like Ghana needs to know what the people in the economy think about the E-levy. Again, it could aid policymakers in deciding whether or not to continue with the E-levy implementation.

The study’s next section provides a succinct review of pertinent literature. Subsequently, the methodology is discussed. Further, the results, discussions, conclusions and recommendations for policy and practice are highlighted.

2. Review of literature, questions and hypothesis development

The social psychology theory is the foundation of this study because it explains that in assessing the citizen’s tax payment behaviour, one must know how the taxpayer considers the country in his mind (Noguera et al., Citation2014). In other words, how a taxpayer reflects on the occurrences in their country inspires their payment behaviour towards the E-levy (Peprah, Mensah & Akosah, Citation2016). Thus, if Ghanaians perceive that E-levy would have an adverse effect on their well-being, they are very likely not to pay. Similarly, Adams’ (1960) equity theory states that there should be fairness between levy payers and the government. We argued that the possible reason why Ghanaians might not comply with the E-levy payment is the perceived equity (fairness) between earlier taxes paid and the returns given to the public by the government. If the residents think what they received back from the earlier tax they paid is not fair, then they are likely to not engage in transactions that would lead to paying the E-levy. Also, in the minds of Ghanaians, does E-levy favour public interest theory of regulation by Pigou (Citation1938) or private interest theory of regulation by Horwitz (Citation1991)? If Ghanaians perceive E-levy to favour the interests of the public, then they are likely to patronize ETs that attract a levy. On the contrary, if Ghanaians perceive the E-levy to satisfy private targets and political ambition, they might not patronize ETs affected by the levy. Moreso, the theory of planned behaviour by Adjen (Citation1991) explains that the behaviours of people are influenced by various factors, for certain reasons and emerge as planned. This theory is employed to support this study because empirical evidence has indicated that perceptions influence actions (Haazebroek et al., Citation2017). Thus, Ghanaians’ perceptions of E-levy will determine their willingness to patronize ETs that attract E-levy charges.

2.1. Perceptions of Ghanaians on the 1.5% levy charge on ETs

According to the President of Ghana Revenue Authority (Citation2022), generally, people perceive levies as bad and a burden and, therefore, would not like the introduction of the additional levy. Since the announcement of the E-levy, Ghanaians have been vocal about their perception of the E-levy. From Facebook, Twitter, television, radio stations, and arguments from the parliament of Ghana, some claim that E-levy is a lazy man’s approach to raising money and that the government is finding an easy way to raise money (Bentil, Citation2022; Kumasi traders, Citation2022). Also, Ghanaians argue that the government of Ghana has introduced so many taxes within a short period and therefore, perceive the E-levy in Ghana to be too much of a burden. The masses have again indicated that the levies collected by the government are corruptibly diverted for their personal gain. This confirms an earlier result of a survey by Bortey (Citation2021), which concluded that Ghanaians are not willing to pay taxes due to perceived corruption. Again, the Minority Leader of the Eighth Parliament of the Fourth Republic of Ghana (Haruna Iddrisu) indicated that the E-levy is a form of double taxation. As much as the majority are criticizing the E-levy, others are counting it as a blessing since they claim it will help residents contribute toward the development of Ghana. Also, some Ghanaians are hoping that by introducing the E-levy, the government of Ghana can raise enough funds to finance the hardships in the economy and, therefore, would not have to resort to the International Monetary Fund for help. However, there is no empirical evidence on how Ghanaians perceive E-levy. Thus, the study’s novelty begins with being the first to conduct a scientific examination of Ghanaians’ perceptions of the recently implemented E-levy. To achieve this, we ask:

Q1: What is the perception of Ghanaians towards the introduction of the E-levy?

2.2. Intention to use ETs affected by the levy

Following the law of demand, it cannot be denied that when the cost of using a transaction increases, the demand for that particular transaction is likely to be reduced. The E-levy is indisputably an additional cost to the already existing cost of ETs in Ghana. The E-commerce Association, Citation2021) established a possible reduction of electronic transactions with the inception of E-levy. Statistics from Kenya, which is implementing a similar levy on ETs, indicated that the introduction of the E-levy would cause a reduction in ET in the country. Similarly, in Zimbabwe, the introduction of E-levy has caused a reduction in the use of ETs. Again, the United Nations Capital Development Fund (UNCDF) (2018) indicated that levy on mobile money transactions causes many to move away from mobile money patronage. Specifically, Angela Wamola, the acting head of sub-Saharan Africa at the Global System for Mobile Communication Association (GSMA), indicated that in Uganda, the value of mobile money transactions dropped by nearly a quarter within a month of the levy coming into force. The Mobile Money Agents Association in Ghana reported massive withdrawals from mobile wallets after news of E-levy. Based on the arguments, we indicated that Ghanaians might form an intention not to patronize ETs that attract the levy. Again, Ghanaian literature is deficient in the intention to use ETs that attract levy; thus, this study contributes to literature investigating it. To achieve this, we asked the question:

Q2: What is the intention of Ghanaians towards using ETs that attract levy?

2.3. Perception of Ghanaians on E-levy and intention to use ETs affected by the levy

Logically, how a person perceives a thing determines whether that person will utilise it or not. Thus, the first thing those who perceive E-levy as bad would do is to stop the use of ETs that attract levies. Anokye (Citation2022) stated that if people perceive E-levy as bad, they will reduce electronic transaction activities. According to the GSMA (Citation2018), the E-levy could potentially create an incentive for cash transactions rather than electronic transactions. Ndung’u (Citation2019) also argued that Ghanaians’ perceptions of the E-levy would influence their use of ETs. Following the technology acceptance model by Davis (Citation1989), which indicates that the perceived usefulness or benefit of technology determines whether it will be used or not, we argue that if Ghanaians perceive E-levy as useful to them and the nation, they will patronize ETs that attract E-levy. Hossain et al. (Citation2020) confirm that the perception of individuals affects their intention to use online transactions. Extending from this, if Ghanaians perceive E-levy to be beneficial to them or the nation, then logically they are likely to patronize ETs that attract E-levy and vice versa. In literature, however, existing studies such as Hossain et al. (Citation2020), Nguyen (Citation2020), and Sigar (Citation2016) have concerned themselves with the influence of perceived usefulness and ease of use on intention to use ETs. This study looked at the impact of E-levy perception on the intention to use levy-affected ETs. Corollary to this, we hypothesize that

H1: The perception of Ghanaians on E-levy positively influences their intention to patronize ETs affected by levy.

2.4. Perception of E-levy and financial inclusion

Policymakers and World Bank have long pushed for improving financial inclusion in sub-Saharan Africa since literature suggests financial inclusion can help reduce poverty and boost economic growth in the region (Kim et al., Citation2018; Van et al., Citation2021). It has been recorded recently that one platform that has succeeded in bringing more people into the financial system in Ghana is electronic transactions, with special emphasis on mobile money transactions (Bank of Ghana, Citation2020). Even though financial inclusion in Ghana is generally low, mobile money has succeeded in improving financial inclusion by bringing even the most vulnerable (illiterate and poor) into the financial system (Koomson et al., Citation2020; Osabuohien & Karakara, Citation2018). Therefore, the risk of the E-levy undermining years of work to bring lower-income, illiterate and rural communities into the financial system in Ghana is at stake. According to Ghana’s minority leader and financial experts, imposing the E-levy contradicts policymakers’ goal of increasing financial inclusion in the country. World Bank (Citation2018) reveals that imposing a levy on financial transactions over mobile phones remains a threat to enrolling more people in the financial system because people generally have a negative perception of levies. In addition, the results of Bhuvana and Vasantha (Citation2017) indicated that the perception of Ghanaians could influence FI. Naruetharadhol et al. (Citation2021) also found that the perception of users influences their patronage of mobile banking services. Earlier studies have examined the perceived usefulness of ETs in enhancing FI (Bhuvana & Vasantha, Citation2017; Naruetharadhol et al., Citation2021). Thus, this study differentiated itself by investigating the role of perception of E-levy in boosting FI. Based on this discussion, we hypothesize that

H2: Perception of Ghanaians on E-levy positively affects FI.

2.5. Intention to use ETs affected by E-levy and financial inclusion

When talking of factors that contribute to financial inclusion, ETs cannot be sidelined (Vasile et al., Citation2021). That is, ETs such as mobile money transfers and electronic payments are major means for accessing financial services. Thus, if the intention to use ETs affected by E-levy, it would most likely manifest in financial inclusion because, empirically, ETs affect FI: Guermond (Citation2022) indicated that mobile money and remittances affect FI and Senyo et al. (Citation2022) indicated that financial technology shapes FI in an economy. Mudi Barruetabeña (Citation2020) indicated in his studies that ETs influence financial inclusion. Pacheco and Rojas-Suarez (Citation2017) specifically argued that E-levy is likely to adversely affect financial inclusion since most people avoid transactions that attract tax. The UN Specialized Agency for ICTs (Citation2021) posits that electronic payment causes an expansion in FI. Masino and Niño-Zarazúa (Citation2020) state that electronic payment delivery can improve FI services. The above-reviewed studies looked at the effect of electronic transactions on FI, not the intention to use ETs affected by levy on FI. Thus, this study filled a gap in literature by considering the intention to use ETs affected by levy instead of just ETs on FI. To accomplish this, we hypothesize that

H3: Intention to use ETs affected by E-levy positively affects FI.

2.6. Perception of E-levy and financial well-being

Obviously, if a person perceives that a particular levy unfairly takes resources away from levy payers and transfers them to the government, that person might not engage in certain transactions that contribute to his well-being. Levies affect the income level of citizens and reduce the personal income available for savings and investments. According to the World Bank (Citation2022), the tax burden falls on the poor and reduces their comforts and standard of living. One of the main points raised during the E-levy debate on Joy News (Ghana’s leading news channel) was the potential harm to Ghanaians’ financial well-being. The argument was built on the premise that the Ghanaian community is already under financial hardship with the rise in prices of fuel, foodstuffs and accommodation. Thus, government should not worsen the situation by levying their already affected income. Mello (Citation2021) indicated that people perceive government charges to be associated with increasing the financial distress of people in an economy. Andersen et al. (Citation2015) suggested residents’ perception of tax burden could affect their FW because they might not engage in certain transactions that might enhance their well-being because of the tax charge on them. Likewise, Bufe et al. (Citation2022) argued that expense shock is associated with the decline in the FW of households. Moreso, Roll et al. (Citation2021) suggest that negative financial stocks are associated with lower FW and E-levy is a financial shock. Existing studies have focused on government charges, expense shocks, and financial stock on FW rather than perceptions of the E-levy on FW. Thus, the study’s novelty is in introducing the perception of E-levy on FW. Therefore, we hypothesize that

H4: Perception of Ghanaians on E-levy positively affects FW.

2.7. Intention to use ETs affected by levy and FW

Through electronic transactions, people save, invest and even obtain loans (International Center for Tax and Development, Citation2022). Again, people transact business both within and outside Ghana using ETs (Sulemana, Citation2022). Also, ETs help to speed up business and investment transactions. Therefore, if the intention to use ETs is affected by the E-levy, it would in turn affect the FW of residents. Sakyi‐Nyarko, Ahmad, Green et al., Citation2022a) and Adaba et al. (Citation2019) indicated that mobile money presents opportunities for Ghanaians to pursue their FW. Also, Sakyi‐Nyarko argued that electronic transactions such as mobile money enhance well-being. Again, Kraimer (Citation2021) indicated that online transactions improve the FW of customers. In the same vein, Evans (Citation2019) explained that using the internet to transact business helps to improve FW. According to the OECD, Citation2017, ETs make financial services more accessible, convenient, and secure and thus have a positive impact on residents’ FW. From the review, instead of assessing the effect of intention to use ETs affected by levy on FW, existing studies assessed the effect of ETs on FW. Consequently, employing intention to use ETs affected by levy as the independent variable is new. Hence, we hypothesize that

H5: Intention to use ETs affected by levy positively influence FW.

2.8. Financial inclusion and financial well-being

Following the public good theory of financial inclusion, which indicates that regardless of the status and income level of the people in an economy, they will benefit from FI (Ozili, Citation2020), FI influences FW. Financial inclusion is a system where access to affordable financial services is made available in an economy (Selvia et al., Citation2021). FI helps people get access to credit for their business activities (Rashid et al., Citation2022) and also encourages saving and investment, which results in enhancing the FW of citizens (Sisharini et al., Citation2019). This argument is supported empirically by Selvia et al. (Citation2021) indicating that FI influences FW. Nandru et al. (Citation2021) found that FI contributes substantially to the well-being of marginalized street vendors. Since street vendors are mostly part of the vulnerable group in society, we argue therefore that FI enhances the financial well-being of both the rich and poor in an economy. From the discourse, we argued that if the anticipated negative impact of E-levy on financial inclusion by the masses turns out to be true, then the financial well-being of the residents of Ghana is likely to be adversely impacted. Based on this, we hypothesize that

H6: Financial inclusion positively influences FW.

Instead of the previously investigated direct relationship between FI and FW, our study contributes to the literature by assessing complex relationships among perception of E-levy, intention to use ETs affected by levy, FI, and FW. Specifically, we assessed

The mediating role of FI in the relationship between perception of E-levy and FW.

The mediating role of FI in the relationship between intention to use ETs affected by levy and FW.

The mediating role of intention to use ETs in the relationship between perception of E-levy and FW.

The mediating role of intention to use ETs through FI in the relationship between perception of E-levy and FW.

The mediating role of intention to use ETs in the relationship between perception of E-levy and FI.

3. Methodology

This study is a cross-sectional quantitative study, and an explanatory research design was employed. The population of the study comprises all residents in Ghana that use ETs. Since the number of residents that uses ETs in Ghana is large and infinite, we employed Calculator Net to do online calculations of a sample size of unlimited population size with a 95% confidence level and a 5% marginal error and had 385. Since sample size is a scientific minimum representation of a population (Select Statistical Services, Citation2022), 385 or more respondents are needed to provide a reliable result. We were, however, able to collect data from 782 Ghanaians. Extending on the “central limit theory,” which states that as sample size increases, the distribution of sample means approaches a normal distribution (Le Cam, Citation1986), and researchers such as Charlesworth (Citation2022) and Islam (Citation2018), who argue that the larger the sample size, the more precise the results and the smaller the margins of error. We used a sample of 782 because, scientifically, it represents the population of Ghana better than 385.

3.1. Survey instrument

The survey instrument was a questionnaire created in a Google Form with closed-ended questions and distributed through electronic mail and social media, including WhatsApp and Facebook. Closed-ended questions were used because they make it easier for the respondents to choose an answer. On a scale of 1–5, where 1 means strongly disagree, 2 means disagree, 3 means not certain, 4 means agree and 5 means strongly agree, the questionnaire collected information on financial inclusion, financial well-being, financial skills, intentions to use electronic transactions and perception of Ghanaians on E-levy. Also, the questionnaire solicited information on the demographics and knowledge level of respondents to the E-levy. Since E-levy is a new issue and there are no previous question items for collecting data on people’s perceptions of the E-levy and their intention to use electronic transactions affected by the levy, we devised two new constructs and question items based on questions asked by Ghanaians and non-Ghanaians about the E-levy, as well as the benefits enumerated by the government about the E-levy. As required, these new constructs and question items measuring them were submitted to senior researchers and lecturers of University of Cape Coast who have expertise in finance, taxation, and economies to validate the question items generated by the team. On a scale of 1 to 3, where 1 represents “not valid,” 2 is “not certain,” and 3 is “valid,” they were asked to validate the questions. We then adopted the questions that were accepted as valid. Respondents were encouraged to complete the form and share the link with others. Although efforts were made to share the link of the Google Form with our networks across the country, it must be noted that the approach adopted in this survey to reach respondents may not guarantee even distribution across geographical regions in Ghana. This may have an impact on respondents’ background information. At the end of the data collection, the data was downloaded using a Microsoft Excel sheet. The Excel sheet was prepared and imported into the PLS-SEM 4 software for analysis.

3.2. Data analysis

We employed Partial Least Square Structural Equation Modeling (PLS-SEM) to achieve the objectives of this study because it involves a complex relationship where we assessed various mediations (Jeon, Citation2015). Secondly, the reason for using PLS-SEM is that latent variables are used in the study (Sigar, Citation2016). The variables considered in this study include residents’ perception of E-levy, intention to use ETs affected by levy, financial inclusion, financial well-being and financial skills, which are latent variables. Latent variables are constructs that are not observable and thus difficult to measure, and it is unlikely that single indicators can reliably and validly detect complex constructs (Curado, Teles, & Marôco, 2014). Instead, many indicators are required to measure the essence of such variables. Thus, the need for measurement errors in the model. SEM recognizes measurement errors and controls their effect on the empirical result. However, following Bossman and Agyei (Citation2022), before the regression result is obtained from SEM, we ran pre-diagnoses, making sure that the constructs and measure items load sufficiently, are convergently valid, are discriminately valid, are compositely reliable and there is an absence of multicollinearity. We again used frequencies and percentiles to analyze background information, Ghanaians’ perceptions of the 1.5% levy on ETs, Ghanaians’ knowledge of E-levy and intention to use ETs affected by the levy.

4. Results and discussion

This section presents the results of the study. It begins with background information, then moves on to knowledge of the E-levy, Ghanaians’ perception of the E-levy, intention to use ETs affected by the levy, and finally, PLS-SEM results.

In Table , we record that 782 people responded to the online survey, with 458 (58.57%) representing males and 324 (41.43%) representing females. We again documented that 16 of the respondents were below the age of 20 (2.05%), 300 (38.36%) were between the ages of 21 to 30, 347 (44.37%) were between the ages of 31 to 40, 85 (10.87%) were between the ages of 41 to 50 and 34 (4.35%) were 51 years and above. Also, 4 (0.51%) of the respondents completed JHS., 47 (6.07%) completed SHS and 731(93.48%) completed tertiary. In terms of marital status, 397 (50.77%) are married, 365 (46.68%) are single, and 13 (1.66%) and 7 (0.90%) are widows. When it comes to regional representation, Ahafo were 21 (2.7), Ashanti was 153 (19.57%0, Bono were 74 (9.46%), Bono East were 24 (3.07%), Central were 117 (14.96%), Eastern were 41 (5.24%), Greater Accra were 176 (22.51%), North East were 10 (1.28%), Northern were 19 (2.43%), Oti were 32 (4.09%), Western were 76 (9.72%), Western North were 19 (2.43%) and Volta were 20 (2.56%). Finally, we document the monthly income of the respondents and it revealed that 220 (28.13%) earn below Ghȼ1,000, 221 (28.26%) earn between Ghȼ1,001 to Ghȼ2,000, 190 (24.30%) earn between Ghȼ2,001 to Ghȼ3,000, 59 (7.54%) earn Ghȼ3,001 to Ghȼ4,000, 21 (2.69%) earn between Ghȼ4,001—Ghȼ5,000 and 71 (9.08%) earn more than Ghȼ5,000.

Table 1. Background information

From Table , we report on the knowledge of residents about the E-levy. We realized 711, representing 98.59% of those who participated in this study, have heard of the E-levy planned to be introduced, with only 11 (1.41%) indicating they have not heard of the E-levy. This implies that most Ghanaians have heard of the E-levy. When asked about the projected rate to be charged for the E-levy, 677 (86.57%) were able to choose the correct answer of 1.50%, while 105 (13.43%) got the answer wrong. This again indicates that majority of Ghanaians know of the rate for E-levy. We further asked respondents when the levy is planned to take effect. A total of 313 representing 40.03%, chose May 2022, which was the correct answer, whereas 469 (59.97%) chose the wrong answer. This means that most Ghanaians were unaware of the date ETs would start attracting the levy. We also inquired about the daily MoMo transactions that would be subject to the levy. Of the respondents, 303 (38.75%) chose to transfer Gh120, which was correct because, according to the Minister of Finance, any amount above Ghȼ100 would attract a levy. However, 479 (61.25%) of the respondents, which represents the majority, got the answer wrong. Finally, we asked of the transactions that do not attract a levy and 308, accounting for 39.39 percent, got the answer correct by choosing personal bank transfers. This is because the Minister of Finance indicated that if a transaction is between the accounts of the same person, then that transaction is exempted from E-levy. Yet, 474 respondents, representing majority got the answer wrong.

Table 2. Knowledge on the electronic transaction levy

Five questions were posed to elicit Ghanaians’ knowledge of the E-levy. Out of the five questions, the first two indicated that majority are aware of the E-levy and the rate to be charged. However, in the next three questions, majority of the respondents got the answers wrong. This demonstrates Ghanaians’ low knowledge of the E-ley. This finding is supported by Peprah et al. (Citation2020) who indicated that over the years, the knowledge level of Ghanaians on taxation and levies has been low. Also, Twum et al. (Citation2020) found low knowledge of Ghanaians on taxation. Hence, much education should be made about the E-levy to enhance the public’s knowledge of it.

Table reports on the perception of Ghanaians towards the 1.5% E-levy. It starts by revealing that most of the respondents (615,78.67%) [164 agreed plus 451 strongly agreed] think E-levy is a form of double taxation. Similarly, 540 respondents, representing 69.05 percent, specified that they do not think E-levy will be channeled toward the development of the nation. Again, majority of the respondents, representing 52.68% (412), do not think that the E-levy would go towards assisting local entrepreneurs in Ghana. In addition, most of the respondents (554 out of 782) think that the government will not be fair to Ghanaians when the E-levy is passed. The E-levy, according to the majority (57.41%), will increase poverty. Likewise, 567 out of 782 respondents think E-levy will have an adverse effect on the performance of businesses. Furthermore, more than half (55.37%) agreed that the E-levy would impede Ghana’s economic development.

Table 3. Perception of Ghanaians on the 1.50% levy on the electronic transactions

Overall, the responses to questions about Ghanaians’ perceptions of the 1.5% E-levy show that Ghanaians view the E-levy negatively in terms of its impact on residents, businesses, and the country’s economy as a whole. Inferring from the answer to question one, “what is the perception of Ghanaians towards the introduction of the E-levy?” Ghanaians perceive the E-levy as a negative initiative. Our results support the finding of Bortey (Citation2021), who established that Ghanaians perceive taxes to be bad. It also confirms the argument made by the minority leader (Haruna Iddrisu).

From Table , we solicited the possible effect of the E-levy on the intention to patronise ETs affected by the levy. We realized that majority of the respondents, representing 585 out of 782 [agreed (188, 24.04%) and strongly agreed (398, 50.90%)], indicated that introducing a levy on electronic transfers is likely to reduce their usage of ETs. Similarly, most of the respondents, 451 (137 agreed and 314 strongly agreed), or 57.67%, said they would rather queue at the bank than make a levy-paying transfer. Again, the majority of the respondents (493 out of 63.04) agreed that they will not transfer mobile money above GH¢100 in a day if there was a 1.50% levy charge. Moreso, when the respondents were asked whether they would bear the transportation cost of sending money to their loved ones rather than pay a levy of 1.50%, only 364 (46.54%) agreed, with 142 (18.16%) choosing not certain and 276 (35.29%) choosing disagree. Thus, even though those who choose to agree are not more than half, they are certainly more than those who choose to disagree. The next question sought to know whether they preferred to withdraw money manually and make a direct payment rather than a bank transfer, which would attract a 1.50% levy, and 526 (67.26%) of the respondents agreed. Also, most of them (462 out of 782) agreed that they would only use electronic transactions that come with a levy of 1.50% when they have no option. A little above average of the respondents (394, 50.38%) agreed that they would discourage friends and family from using electronic transfer when the levy of 1.50% is passed; 15.73% were not certain and 33.89% disagreed. With the final question, 551 representing 70.46% agreed that they would rather make a direct deposit at the bank than transfer the money through my mobile money account, which comes with a 1.50% levy.

Table 4. Intention to use electronic transactions affected by the levy

From the responses to the questions asked to solicit information on the intention to use ETs that attract levy, we conclude that when the E-levy is passed, most Ghanaians intend to reduce the patronage of ETs that attract levy. Thus, the answer to question 2, “What is the intention of Ghanaians towards using ETs that attract levy?” is Ghanaians’ intent to reduce the use of ETs that attract levy. Our finding confirms the fears of ECommerce Association, Citation2022)..

Most Ghanaians perceive E-levy as a negative initiative (see Table ) and have agreed that E-levy would affect their intention to use ETs that attract levy (see Table ). Hence, we conclude that Ghanaians’ acceptance of the E-levy is very low.

5. Discussion of PLS-SEM Results

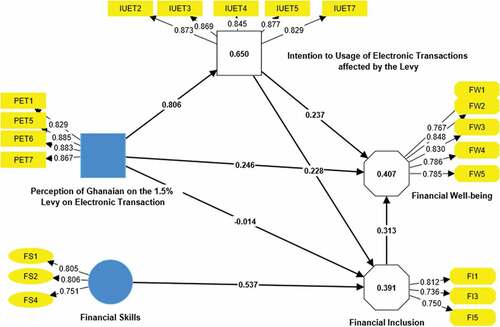

In this section, the regression results from the PLS-SEM estimations are presented and discussed. Table highlights the pertinent diagnoses (construct reliability and validity, as well as discriminant validity) that are required in PLS-SEM. Figure also provides information on factor loading and R-square. Table concentrates on the results of the direct relationships between the variables. Table also gives details on the mediating and total effects. The regression results are presented with the coefficient, T-statistic, and probability value of all the relationships established. The results are detailed below, guided by the hypotheses tested:

Figure 1. Graphical output of the impact of E-levy based on perception.

Table 5. Diagnostics

Table 6. Path coefficient

Table 7. Mediating and total effect

In this section, we present the diagnosis of the empirical result. First, we report on construct reliability and validity. Cronbach’s alpha (CA), rho_a and composite reliability (CR) measure the reliability of the latent variable. Our CA, rho_a and CR values are more than 7, as recommended by Hair et al. (Citation2014), which implies that the items measuring their constructs are closely related (see, Table ). Also, the average variance extracted (AVE) assesses the convergent validity. As suggested by Alarcón et al., Citation2015, October), AVE value should be greater than 0.5. The values for AVE are more than 0.5, meaning the convergent validity of the constructs is adequate (see, Table ). Thus, construct reliability and validity are established in this study.

Second, we give details on the discriminant validity of the constructs using Fornell–Larcker criterion, Heterotrait–Monotrait ratio, and cross loading. For Fornell and Larcker criterion, it was indicated that the square root of a construct’s AVE between the same construct should surpass its correlation with other constructs (Fornell and Larcker, Citation1981). From Table , we report the correlation of a construct with itself is greater than with other constructs in all the variables employed. Using the cross-loading, it was identified that each item loads higher on itself than others (see Table in the appendix). Additionally, we assess discriminant validity using Heterotrait–Monotrait ratio (HTMT). According to Henseler et al. (Citation2015), HTMT quantifies the level of similarity between latent variables. Normally, if HTMT is less than one, discriminant validity is regarded. However, in recent times, a threshold of 0.85 has been given. Since the similarity between all the variables employed in this study is less than 0.85, we emphasize that discriminating validity is established by HTMT. From all the assessors for discriminant validity, we conclude that items measuring the variables and constructs in this study distinctly represent separate concepts (Henseler et al., Citation2015).

Third, we report on collinearity statistics (VIF) is below the threshold of 0.5, indicating that there is no multicollinearity among the independent variables employed in the models (see Table in the appendix).

5.1. PLS-SEM Graphical output

This section presents a conceptual view of the interaction among the variables involved in this study. From Figure , we see the names of the variables, factor loading, R-square and path coefficients of the direct relationships among the variables.

We continue with the diagnosis of this study by reporting on factor loading and R-square. Factor loading shows how well an item represents the underlying construct. As a result, items must load higher on the constructs they are measuring. Zephaniah et al. (Citation2020) indicated that satisfactory factor loadings should be above 5. The items loading on all the constructs presented in Figure are from 0.736 to 0.885. Hence, measurement items employed for all variables load well. R-Square is comprehended as the variance in the dependent variable explained by the independent variables. In literature, the threshold for R-square is not consensual. However, following Heidari et al. (Citation2018), Lange and Johnston (Citation2020), and Abdel-Fattah et al. (Citation2021), we indicate that below 0.25 is weak, between 0.25 and 0.5 is moderate and between 0.5 and 0.75 is high. Since R-square is 0.391 for FI, 0.407 for FW and 0.650 for intention to use ETs affected by the levy, we indicated that independent variables adequately explain the dependent variables in our study.

5.2. Path coefficient

The dialogue in this section would focus on the direct relationship between the variables. Using a sample bootstrapping of 5000, we obtained our results.

From Table , Model 1 indicates Ghanaians’ perception of the E-levy has a direct positive and significant effect on their intention to use ETs affected by the levy. Thus, an increase in Ghanaians’ perception of E-levy, will increase their intention to use ETs affected by the levy by 0.806. This implies that if Ghanaians have a positive perception of the E-levy, their intention to use ETs affected by levy will increase, whereas a negative perception will decrease their intention to use ETs affected by levy. The findings support the first hypothesis, which states that Ghanaians’ perception of the E-levy influences their intention to patronize ETs affected by the levy. The findings show that Ghanaians’ perception of E-levy influences their use of ETs affected by levy. This confirms the fears of GSMA (Citation2018) and Ndung’u (Citation2019) that E-levy could potentially create an incentive for cash transactions rather than ETs.

In Model 2, we find a direct positive and significant relationship between Ghanaians’ perceptions of E-levy and their financial well-being (FW). This suggests that Ghanaians’ perceptions of the E-levy can influence their FW (β = 0.246). Andersen et al. (Citation2015) indicated that residents’ perception of tax burden could affect their financial well-being because they might not engage in certain transactions that might enhance their well-being because of the tax charge on them. Similarly, World Bank (Citation2022) stated that the tax burden falls on the poor and reduces their comforts and standard of living. The result is in line with our hypothesis 4, perception of Ghanaians on E-levy positively affects FW.

Again, Model 4 reports a direct positive and significant influence of intention to use electronic transactions affected by E-levy on FW. In particular, a reduction in the intention to use ETs affected by levy would reduce FW by 0.180. This is because people transact investments and business activities both within and outside Ghana, using ETs. Hence, intending to reduce ETs would result in a reduction in the financial well-being of the people. Model 4, therefore, agrees with hypothesis 5five, that the intention to use electronic transactions affected by the levy positively influences FW. This finding is supported by Evans (Citation2019) and OECD (Citation2017).

Model 5 also finds a direct positive relationship between the intention to use E-levy-affected ETs and financial inclusion (FI) (=0.228). Through ETs people easily access financial services such as savings, investments and loans. Meaning, if electronic transactions are affected by levy, the purpose of making financial services easily accessible may be hindered. The finding confirms hypothesis 3 which indicates, intention to use ETs affected by levy positively affects financial inclusion in Ghana. It is also supported by Guermond (Citation2022) .

Model 7 demonstrates a significant positive direct relationship between FI and FW. Precisely, a reduction in FI would reduce FW by 0.313. Access to financial services enables a person to save, invest and access credit and these factors are very necessary to the financial well-being of an individual. The result supports hypothesis 6, which states that financial inclusion positively influences financial inclusion. Financial inclusion helps people access credit for their business activities (Rashid et al., Citation2022) and encourages saving and investment, which enhances citizens’ FW (Sisharini et al., Citation2019). Thus, this result is empirically supported.

Model 3, on the other hand, reports an insignificant direct effect of the perception of Ghanaians about E-levy on FI. Model 3, therefore, failed to support hypothesis 2, which states that perception of Ghanaians on E-levy positively affect FI. Logically, this result might not be too strange because perception of E-levy might need to first influence intention to use ETs before it can affect FI. In other words, people’s perception of E-levy might not affect FI unless they form the intention not to patronize ETs that attract levy.

Finally, Model 6 indicated a direct positive relationship between financial skills and FI.

5.3. Mediating and total effect

In this section, we discuss the indirect and total effects of the variables. Before going with this, we would like to highlight that in PLS-SEM, there are two main mediating effects (partial and full). A partial mediating effect is recognized when both the direct and indirect relationships between the dependent variable (DV) and the independent variable (IV) are significant. However, if the direct effect is insignificant, but the indirect effect is significant, then we recognize full mediation.

From Table , Model 4 reports a significant positive indirect effect of perception of Ghanaians on E-levy (PET) on FW. Specifically, Model 7 indicates that PET significantly affects FW through the intention to use ETs affected by levy (IUET). Also, Model 9 indicates the relationship between PET and FW is mediated by both IUET and FI. However, Model 5 reports an insignificant mediating effect of PET on FW when FI is considered in isolation. Since the direct effect of PET on FW is significant (see Table ), we report the following: IUET in isolation mediates PET and FW partially; IUET and FI together partially mediate the link between PET and FW; FI in isolation does not mediate the nexus between PET and FW. Thus, these results justify why we had an insignificant direct relationship between PET and FI in Table , Model 3. Until the intention to use ETs attract levy is affected by PET, it will not reflect in FI.

Model 3 also indicates an indirect positive significant relationship between PET and FI. However, Model 10 reveals that the indirect effect of PET on FI is through IUET. This implies that, as much as the perception of Ghanaians on E-levy could affect financial inclusion directly in Ghana, the impact of their perception on financial inclusion will depend on the intention to use ETs that attract levy. This is loadable because our finding in Table and others (GSMA, Citation2018 and CitationHossain et al., Citation2020) confirms that perception of Ghanaians influences the intention to use ETs. Also, in Table , a relationship is established between IUET and FI. The result is in line with Vasile et al. (Citation2021). We, therefore, believe that if the perception of Ghanaians toward E-levy is bad it could cause them to stop using ETs affected by levy such as mobile money and bank transfers. And since electronic transactions have an effect on financial inclusion (Guermond, Citation2022), financial inclusion in the country would be adversely affected. We further indicate that since the direct nexus between PET and FI is significant (see Table ), IUET fully mediates PET and FI.

Furthermore, Model 2 discloses a positive indirect significant relationship between IUET and FW. This was further explained by Model 6 that FI mediates the relationship. This means that the intention to use levy-affected ETs has an indirect effect on FW through FI. In other words, if people conceive the intention not to patronize ETs that attract levy, it will initially influence FI (Masino & Niño-Zarazúa, Citation2020), and subsequently, influence FW (Guermond, Citation2022; Senyo et al., Citation2022). According to the OECD, Citation2017), ETs make financial services more accessible, convenient, and secure and thus have a positive impact on residents’ financial well-being. Thus, FI partially mediates the association between IUET and FW because the direct effect of LUET on FW is significant (see Table ).

Moreso, Model 1 reveals that financial skills have a significant indirect effect on FW, with Model 8 indicating that the indirect effect of financial skills on FW is through the intervention of FI. Thus, FI partially mediates financial skills and FW.

Finally, we report positive significant total effects from FI to FW; FS to FI; FS to FW; IUET to FI; IUET to FW; PET to FI; PET to FW; and PET to IUET (see Models 11 to 18). This implies that when the direct and indirect effects are considered together, all relationships considered in this study are significant.

6. Summary and main findings

The government of Ghana has introduced a levy on certain electronic transactions. As a result, there has been much discussion about whether the E-levy is a blessing or a curse. In the debate, however, most of the discussion was centred on how the E-levy would affect the financial inclusion and financial well-being of the people in Ghana. We, therefore, seek to unearth scientifically whether introducing E-levy in Ghana would be a possible curse or a blessing based on the perception of the public. We achieved this by documenting that Ghanaians have a negative perception of E-levy (see Table ). Also, the result revealed that E-levy has a negative effect on the intention to use ETs that attract levy (see Table ). The results again reveal that Ghanaians have low knowledge of E-levy (see Table ). The PLS-SEM results are summarized in Table below:

Table 8. Summary of PLS-SEM findings

7. Conclusions and recommendations

Since total effect is the combined results of direct and indirect effect (Jiang et al., Citation2020), our conclusions were made based on the total effect results because it would be fair to make inferences based on the overall effect (both direct and indirect effect) than just the direct effect. We document Ghanaians have limited knowledge on E-levy (see Table ). As a result, the Ghanaian government should re-educate the public about E-levy. We again document that the perception of Ghanaians towards the 1.5% E-levy is negative (see Table ). We also found that Ghanaians’ perceptions of the E-levy had a significant positive total effect on their intention to use levy-affected ETs, financial inclusion, and financial well-being (see Table ). Since Table indicates Ghanaians have a negative perception of E-levy, then a significant positive total effect of their perceptions on their intention to patronize ETs affected by levy, their financial inclusion, and their financial well-being means a reduction in their intention to patronize ETs affected by levy, their FI and their FW. Also, in Table , we recognized a reduction in the intention to use ETs affected by levy. This presupposes the significant positive total effect of the intention to use ETs affected by levy on FI and FW would result in a decline in financial inclusion and financial well-being in Ghana (see Table ). Based on the discourse and public perception, E-levy is a curse. Hence, we endorse that the government of Ghana should review the E-levy policy to minimize its negative effects. We specifically recommend that the government raise the GH¢100 per day transaction exemption threshold to increase the level of intention to use ETs and financial inclusivity; additionally, government can exempt businesses that use electronic transactions for business activities, particularly if they are already paying income tax, to reduce the tax burden on their income. Again, to increase the intention to patronize ETs that attract levy, the government should re-enlighten the public on the benefits of E-levy to the country, as well as reassure the public of accountability and honesty in implementing the E-levy policy. We further record a significant and positive total effect of FI on FW (see Table ). Thus, in addition to reviewing the E-levy policy to enhance the financial well-being of residents of Ghana, the government of Ghana should introduce policies that ensure financial inclusivity (accessibility and affordability in the financial sectors).

Mobile money vending is a small-scale business that sprang up in Ghana when mobile money transactions became vibrant (Rea & Nelms, Citation2017). It has created jobs and income for a lot of Ghanaians (Rea & Nelms, Citation2017). However, we anticipate that the financial performance of mobile money vendors would be most affected since they are the major electronic transactions partronized by Ghanaians. In light of this, we recommend other researchers explore the impact of E-levy on the financial performance of mobile money vendors in Ghana.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

References

- , A. (1991). The Theory of Planned Behavior. Organizational Behavior and Human Decision Processes, 50, 179–24.

- Abdel-Fattah, M. K., Mohamed, E. S., Wagdi, E. M., Shahin, S. A., Aldosari, A. A., Lasaponara, R., & Alnaimy, M. A. (2021). Quantitative evaluation of soil quality using principal component analysis: The case study of El-Fayoum depression Egypt. Sustainability, 13(4), 1824. https://doi.org/10.3390/su13041824

- Adaba, G. B., Ayoung, D. A., & Abbott, P. (2019). Exploring the contribution of mobile money to well‐being from a capability perspective. The Electronic Journal of Information Systems in Developing Countries, 85(4), e12079. https://doi.org/10.1002/isd2.12079

- Adam, A. M., Frimpong, S., & Boadu, M. O. (2017). Financial literacy and financial planning: Implication for financial well-being of retirees. Business and Economic Horizons (BEH), 13(1232–2017–2418), 224–236. https://doi.org/10.15208/beh.2017.17

- Adams, J. S. (1963). Towards an understanding of inequity. Journal of Abnormal and Social Psychology, 67, 422–436.

- AfricaNenda Accelerating Inclusive payment system. (2022). State of inclusive instant payment in Africa report, 2022. www.africanenda.org on 22nd November, 2022

- Alarcón, D., Sánchez, J. A., & De Olavide, U. (2015, October). Assessing convergent and discriminant validity in the ADHD-R IV rating scale: User-written commands for Average Variance Extracted (AVE), Composite Reliability (CR), and heterotrait-monotrait ratio of correlations (HTMT). In Spanish STATA meeting (pp. 39). Retrieved from https://www.stata.com/meeting/spain15/abstracts/materials/spain15_alarcon.pdf

- Andersen, V., Austin, S., Doucette, J., Drazkowski, A., & Wood, S. (2015). Addressing income volatility of low income populations. In Workshop in Public Affairs (pp. 1-37). La Follette School of Public Affairs .

- Anokye, K. (2022). E-levy inimical to financial inclusion and digital transformation. https://thebftonline.com/2021/12/22/e-levy-inimical-to-financial-inclusion-and-digital-transformation/ on 13st June, 2022

- Appiah, B. O. (2022). “It’s a lazy tax”: Why African governments’ obsession with mobile money could backfire. https://restofworld.org/2022/how-mobile-money-became-the-new-cash-cow-for-african-governments-but-at-a-cost/#:~:text=Kenya%2C%20Nigeria%2C%20South%20Africa%2C%20Egypt%20and%20Mauritius%20are,their%20tax%20rates%2C%20after%20businesses%20and%20users%20complained. on 22nd June, 2022

- Bank of Ghana. (2020). Payment system reports. https://www.bog.gov.gh/wp-content/uploads/2022/02/Payment-Systems-Annual-Report-2020.pdf on 25th July, 2022

- Barruetabeña, E. (2020). Impact of new technologies on financial inclusion. Banco de Espana Article, 5, 20. https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3678000

- Bentil, K. (2022). E-Levy is lazy man’s approach to collect revenue. https://www.myjoyonline.com/e-levy-is-a-lazy-mans-approach-to-collect-revenue-kofi-bentil/

- Bhuvana, M., & Vasantha, S. (2017). A structural equation modeling (SEM) approach for mobile banking adoption-a strategy for achieving financial inclusion. Indian Journal of Public Health Research and Development, 8(2), 175–181. https://doi.org/10.5958/0976-5506.2017.00106.1

- Bortey, I. N. (2021). Ghanaians willing to pay taxes but find it difficult to know how tax revenues are used. https://lafollette.wisc.edu/images/publications/workshops/2015-income.pdf

- Bossman, A., & Agyei, S. K. (2022). Technology and instructor dimensions, e-learning satisfaction, and academic performance of distance students in Ghana. Heliyon, 8(4), e09200.

- Bufe, S., Roll, S., Kondratjeva, O., Skees, S., & Grinstein-Weiss, M. (2022). Financial shocks and financial well-being: What builds resiliency in lower-income households? Social Indicators Research, 161(1), 379–407. https://doi.org/10.1007/s11205-021-02828-y

- Charlesworth. (2022). The importance of having Large Sample Sizes for your research. https://www.cwauthors.com/article/importance-of-having-large-sample-sizes-for-research on 23rd November, 2022

- Davis, F. D. (1989). Perceived usefulness, perceived ease of use, and user acceptance of information technology. MIS Quarterly, 319–340. https://doi.org/10.2307/249008

- E-commerce Association. (2021). E-levy will result in loss of jobs in eCommerce and fintech space. https://www.myjoyonline.com/e-levy-will-result-in-loss-of-jobs-in-ecommerce-and-fintech-space-e-commerce-association/ on 13th June, 2022

- Evans, O. (2019). Repositioning for increased digital dividends: Internet usage and economic well-being in sub-saharan Africa. Journal of Global Information Technology Management, 22(1), 47–70. https://doi.org/10.1080/1097198X.2019.1567218

- Fornell, C., & Larcker, D. F. (1981). Evaluating Structural Equation Models with unobservable variables and measurement error. Journal of Marketing Research, 18(1), 39–50.

- Ghana Revenue Authority (2022). Electronic Transfer Levy. https://gra.gov.gh/e-levy/ on 1st June, 2022

- GSMA. (2018), “The mobile economy Sub-Saharan Africa 2018”, Policy measures to support mobile ecosystem development, www.gsmaintelligence.com/research/?file on 2nd July, 2022

- Guermond, V. (2022). Whose money? Digital remittances, mobile money and fintech in Ghana. Journal of Cultural Economy, 1–16. https://doi.org/10.1080/17530350.2021.2018347

- Haazebroek, P., Raffone, A., & Hommel, B. (2017). HiTEC: A connectionist model of the interaction between perception and action planning. Psychological Research, 81(6), 1085–1109. https://doi.org/10.1007/s00426-016-0803-0

- Hair, J. F., Ringle, C. M., Sarstedt, M., Hair, J. F., Ringle, C. M., & Sarstedt, M. (2014). PLS-SEM: Indeed a silver bullet PLS-SEM: Indeed a silver bullet. January, 2015, 37–41. https://doi.org/10.2753/MTP1069-6679190202

- Heidari, A., Kolahi, M., Behravesh, N., Ghorbanyon, M., Ehsanmansh, F., Hashemolhosini, N., & Zanganeh, F. (2018). Youth and sustainable waste management: A SEM approach and extended theory of planned behavior. Journal of Material Cycles and Waste Management, 20(4), 2041–2053. https://doi.org/10.1007/s10163-018-0754-1

- Henseler, J., Ringle, C. M., & Sarstedt, M. (2015). A new criterion for assessing discriminant validity in variance-based structural equation modeling. Journal of the Academy of Marketing Science, 43(1), 115–135. https://doi.org/10.1007/s11747-014-0403-8

- Hesse, A. (2022). MWC22: Ghana makes strong showing in Africa Inclusive instant payment report. https://thebftonline.com/2022/10/31/mwc22-ghana-makes-strong-showing-in-africa-inclusive-instant-payment-report/ on 22nd November, 2022

- Horwitz, R. B. (1991). The irony of regulatory reform: The deregulation of American telecommunications. Oxford University Press on Demand.

- Hossain, S. A., Bao, Y., Hasan, N., & Islam, M. F. (2020). Perception and prediction of intention to use online banking systems: An empirical study using extended TAM. International Journal of Research in Business and Social Science(2147-4478), 9(1), 112–126. on 12th June, 2022. https://www.youtube.com/watch?v=u5SWDMPb_UE

- International Center for Tax and Development. (2022). How will E-Levy impact the informal sector in Ghana. https://www.ictd.ac/blog/how-e-levy-impact-informal-sector-ghana/ on 13st June, 2022

- Islam, M. R. (2018). Sample size and its role in Central Limit Theorem (CLT). Computational and Applied Mathematics Journal, 4(1), 1–7.

- Jeon, J. (2015). The strengths and limitations of the statistical modeling of complex social phenomenon: Focusing on SEM, path analysis, or multiple regression models. International Journal of Economics and Management Engineering, 9(5), 1634–1642.

- Jiang, Y., Zhao, X., Zhu, L., Liu, J. S., & Deng, K. (2021). Total-effect test is superfluous for establishing complementary mediation. Statistica Sinica, 31(4), 1961–1983.

- Kim, D. W., Yu, J. S., & Hassan, M. K. (2018). Financial inclusion and economic growth in OIC countries. Research in International Business and Finance, 43, 1–14. https://doi.org/10.1016/j.ribaf.2017.07.178

- Koomson, I., Villano, R. A., & Hadley, D. (2020). Effect of financial inclusion on poverty and vulnerability to poverty: Evidence using a multidimensional measure of financial inclusion. Social Indicators Research, 149(2), 613–639. https://doi.org/10.1007/s11205-019-02263-0

- Kraimer, C. (2021). The impact of online banking on financial. Well-Being.

- Kumasi traders. (2022). E-Levy is a ‘lazy man’s approach’, sit and plan again. https://www.ghanaweb.com/GhanaHomePage/business/E-Levy-is-a-lazy-man-s-approach-sit-and-plan-again-Kumasi-traders-to-government-1455004#:~:text=The%20association%20which%20has%20described,more%20people%20to%20pay%20taxes. On 12th June, 2022

- Lange, G. S., & Johnston, W. J. (2020). The value of business accelerators and incubators–an entrepreneur’s perspective. Journal of Business & Industrial Marketing, 35(10), 1563–1572. https://doi.org/10.1108/JBIM-01-2019-0024

- Le Cam, L. (1986). The central limit theorem around 1935. Statistical Science, 78–91.

- Masino, S., & Niño-Zarazúa, M. (2020). Improving financial inclusion through the delivery of cash transfer programmes: The case of Mexico’s progresa-oportunidades-prospera programme. The Journal of Development Studies, 56(1), 151–168. https://doi.org/10.1080/00220388.2018.1546845

- Mello, S. (2021). Fines and financial wellbeing. Working paper. Retrieved from https://mello.github.io/files/fines.pdf

- Minister of Finance. (2021). Highlights of the 2022 budget and economic policy. https://mofep.gov.gh/sites/default/files/budget-statements/2022-Budget-Highlights.pdf on 1st June, 2022

- Ministry of Finance. (2022). The National Budget. https://mofep.gov.gh/publications/budget-statements on 1st June, 2022

- Nandru, P., Chendragiri, M., & Velayutham, A. (2021). Examining the influence of financial inclusion on financial well-being of marginalized street vendors: An empirical evidence from India. International Journal of Social Economics, 48(8), 1139–1158. https://doi.org/10.1108/IJSE-10-2020-0711

- Naruetharadhol, P., Ketkaew, C., Hongkanchanapong, N., Thaniswannasri, P., Uengkusolmongkol, T., Prasomthong, S., & Gebsombut, N. (2021). Factors affecting sustainable intention to use mobile banking services. SAGE Open, 11(3), 21582440211029925. https://doi.org/10.1177/21582440211029925

- Ndung’u, N. (2019). Could taxation of mobile banking in Africa stall financial inclusion? Brookings institution http://www.brookings.edu/blog/africa-in-focus/2019/02/21 on 2nd July, 2022

- Nguyen, O. T. (2020). Factors affecting the intention to use digital banking in Vietnam. The Journal of Asian Finance, Economics and Business, 7(3), 303–310. https://doi.org/10.13106/jafeb.2020.vol7.no3.303

- Noguera, J. A., Quesada, F. J. M., Tapia, E., & Llàcer, T. (2014). Tax compliance, rational choice, and social influence: An agent-based model. Revue française de sociologie, 55(4), 765–804.

- OECD. (2017). G20/OECD INFE report on adult financial literacy in G20 countries. OECD. (2016).

- Okpeyo, E. T., Musah, A., & Gakpetor, E. D. (2019). Determinants of tax compliance in Ghana. Journal of Applied Accounting and Taxation, 4(1), 1–14. https://doi.org/10.30871/jaat.v4i1.935

- Oni, O., & Gasparri, A. (2022). Ghana announces electronic levy: Possible scenarios on the progress of digital financial inclusion. In Unlocking public and private finance. Retrieved from UN Capital Development Fund. https://www.uncdf.org/article/7408/ghana-electronic-levy#:~:text=E%2Dlevy%20can%20result%20in,major%20contributor%20to%20national%20income. on 13th January, 2023

- Osabuohien, E. S., & Karakara, A. A. (2018). ICT usage, mobile money and financial access of women in Ghana. Africagrowth Agenda, 15(1), 14–18. https://journals.co.za/doi/abs/10.10520/EJC-dc947bee3

- Ozili, P. K. (2020). Theories of financial inclusion. In Uncertainty and challenges in contemporary economic behaviour. Emerald Publishing Limited. https://doi.org/10.1108/978-1-80043-095-220201008

- Pacheco, L., & Rojas-Suarez, L. (2017). An index of regulatory practices for financial inclusion in Latin America (No. 17/15).Mello, S. (2021) Fines and financial wellbeing. Working paper.

- Peprah, C., Abdulai, I., Agyemang-Duah, W., & McMillan, D. (2020). Compliance with income tax administration among micro, small and medium enterprises in Ghana. Cogent Economics & Finance, 8(1), 1782074. https://doi.org/10.1080/23322039.2020.1782074

- Peprah, J. A., Mensah, A. O., & Akosah, N. B. (2016). Small and medium sized enterprises (SMEs) accessibility to public procurement: SMEs entity perspective in Ghana. European Journal of Business and Social Sciences, 4(11), 25–40.

- Pigou, A. C. (1938). Money wages in relation to unemployment. The Economic Journal, 48(189), 134–138.

- Rashid, S., Bowra, Z. A., & Hussain, A. (2022). An empirical investigation of financial inclusion on financial wellbeing of working women: A mediating role of financial capability. Bulletin of Business and Economics (Bbe), 11(1), 14–23. https://doi.org/10.5281/zenodo.6341579

- Rea, S. C., & Nelms, T. C. (2017). Mobile money: The first decade. Institute for Money, Technology and Financial Inclusion Working Paper, 1. https://www.imtfi.uci.edu/files/docs/2017/Rea_Nelms_Mobile%20Money%20The%20First%20Decade%202017_2a.pdf

- Roll, S., Kondratjeva, O., Bufe, S., Grinstein-Weiss, M., & Skees, S. (2021). Assessing the short-term stability of financial well-being in low-and moderate-income households. Journal of Family and Economic Issues, 1–28. https://link.springer.com/article/10.1007/s10834-021-09760-w

- Sakyi‐Nyarko, C., Ahmad, A. H., & Green, C. J. (2022a). Investigating the well‐being implications of mobile money access and usage from a multidimensional perspective. Review of Development Economics, 26(2), 985–1009. https://doi.org/10.1111/rode.12848

- Select Statistical Services. (2022). Population mean – Sample size. https://select-statistics.co.uk/calculators/sample-size-calculator-population-mean/ on 30th November, 2022

- Selvia, G., Rahmayanti, D., Afandy, C., & Zoraya, I. (2021). The effect of financial knowledge, financial behavior and financial inclusion on financial well-being. 12–45.

- Senyo, P. K., Karanasios, S., Gozman, D., & Baba, M. (2022). FinTech ecosystem practices shaping financial inclusion: The case of mobile money in Ghana. European Journal of Information Systems, 31(1), 112–127. https://doi.org/10.1080/0960085X.2021.1978342

- Sigar, J. F. (2016). The influence of perceived usefulness, perceived ease of use and perceived enjoyment to intention to use electronic money in Manado. Jurnal EMBA: Jurnal Riset Ekonomi, Manajemen, Bisnis Dan Akuntansi, 4, 2. https://doi.org/10.35794/emba.4.2.2016.13083

- Sisharini, N., Hardiani, S., & Ratnaningsih, C. S. (2019). Increasing financial literacy and financial inclusion model to achieve MSMEs financial well being. Int J Sci Technol Res, 8(10), 314–317. https://lppm.unmer.ac.id/webmin/assets/uploads/lj/LJ202006111591847909337.pdf

- Sulemana, H. (2022). Ghana’s new E-levy will weaken its financial system. https://www.africanliberty.org/2022/02/14/ghanas-new-e-levy-policy-will-weaken-the-countrys-financial-system/ on 13st June, 2022

- The President of Ghana,. (2022). President Nana Akufo-Addo defends Ghana’s ‘not terrible’ economy. In An interview at British Broadcasting Corporation-Africa. https://www.youtube.com/watch?v=BO4uTZvTKMo

- Twum, K. K., Amaniampong, M. K., Assabil, E. N., Adombire, M. A., Edisi, D., & Akuetteh, C. (2020). Tax knowledge and tax compliance of small and medium enterprises in Ghana. South East Asia Journal of Contemporary Business, Economics and Law, 21(5), 222–231. https://doi.org/10.2753/MTP1069-6679190202

- UN Specialized Agency for ICTs. (2021). Expanding financial inclusion through electronic payments. https://www.itu.int/hub/2021/07/expanding-financial-inclusion-through-electronic-payments/

- Van, L. T. H., Vo, A. T., Nguyen, N. T., & Vo, D. H. (2021). Financial inclusion and economic growth: An international evidence. Emerging Markets Finance and Trade, 57(1), 239–263. https://doi.org/10.1080/1540496X.2019.1697672

- Vasile, V., Panait, M., & Apostu, S. A. (2021). Financial inclusion paradigm shift in the postpandemic period. digital-divide and gender gap. International Journal of Environmental Research and Public Health, 18(20), 10938. https://doi.org/10.3390/ijerph182010938

- Wicksell, K. (1896). Taxation in the monopoly case. Readings in the Economics of Taxation, 156–177.

- World Bank. (2018). Financial inclusion”: Financial inclusion is a key enabler to reducing poverty and boosting prosperity, the world bank brief.

- World Bank. (2022). How do taxes and transfers impact poverty and inequality in developing countries? How do taxes and transfers impact poverty and inequality in developing countries? (worldbank.org) on 13th July, 2022.

- Zephaniah, C. O., Ogba, I. E., & Izogo, E. E. (2020). Examining the effect of customers’ perception of bank marketing communication on customer loyalty. Scientific African, 8, e00383. https://doi.org/10.1016/j.sciaf.2020.e00383

Appendix

Table A1. Cross loading

Table A2.

Collinearity statistics