?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

From an economic prospective, the relationship between financial innovation and economic growth has always been a critical aspect of the financial system. However, this relationship has not recieved extensive attention in academia. Therefore, this study examines the effect of financial innovation on economic growth in the context of developing and developed countries using 92 cross-sectional data over the period of 2002 to 2020, the fixed effect method of panel regression has been applied to examine the relationship between financial innovation and economic growth. This study has compared the results of developing and developed countries using different combinations of explanatory variables. The results of this study depict that various combinations of variables have varied impacts on dependent variable. This study has revealed the negative relationship between financial innovation and economic growth. However, domestic credit to private sector banks has the best proxy for financial innovation. This study suggests that regulators should focus on encouraging and discouraging financial innovation based on its impact on the economy.

1. Introduction

The efficient mobilization of economic resources is a crucial part of developmental economic theories as it ensures the most efficient use of economic resources (Aigbokhan, Citation2000; Huntington, Citation1993; Soyode, Citation1990). Transferring resources with the help of efficient financial intermediation is a link between savers and borrowers in the economy (Adams, Citation2021; Gurley & Shaw, Citation1967). Efficiency in the financial system is established by constant changes and improvements in the current form of existing financial offerings; hence, constant change or innovations in financial institutions are essential and have also grown recently (Berman et al., Citation2022; Wachter, Citation2006). Consequently, this link between financial innovations and economic growth has attracted the attention of researchers and policymakers over the years, especially after the financial crisis of 2007, given the uncertainty around its detrimental impact on GDP (Li & Xu, Citation2021). On the contrary, numerous research examining different financial development proxy variables demonstrate a positive relationship between financial development and economic growth (Adams, Citation2021; Ahmad & Shah, Citation2020; Bibi & Bibi et al., Citation2022; Hasan & Barua, Citation2015; Kyophilavong et al., Citation2016; Ram, Citation1999; Robeena Bibi, Citation2020). Since there is conflicting literature on the theme, new evidence is needed.

When the financial system develops, The economy benefits because it makes it easier to accumulate wealth and encourage saving while also offering a variety of options in the form of new and improved financial products that are more useful and less expensive (Lusardi, Citation2019). Financial innovation is a rapid and ongoing process that involves the creation of new financial products, services, and processes to meet changing market demands and improve existing ones. As a result of this innovation, the financial system is continually evolving and transforming to accommodate new products and technologies. Financial innovation is essential because it provides new opportunities to access financial services and manage risk (Chien, Pantamee, Hussain, Chupradit, Nawaz, Mohsin et al., Citation2021; Djoumessi, Citation2009; Handa & Khan, Citation2008; Simiyu et al., Citation2014). Financial institutions, especially private commercial banks, play an essential part in financial system advancement by innovating various financial goods and services. In the long run, these innovative products and services help to accelerate economic growth by augmenting various economic activities and facilitating financial inclusion, transfer of payment, and remittances (Bara et al., Citation2016; Edquist, Citation2019). These enhanced economic activities create more opportunities, contributing to increased economic growth. As the financial system evolves, so do financial innovations in the economy. Therefore, the financial system becomes more efficient, allowing financial institutions to provide better products and services.

Financial innovation can be defined as the development and dissemination of new financial instruments, financial technologies, institutions, and markets in the financial system in order to overcome the system’s deficiencies. (Frame & White, Citation2004; Lerner & Tufano, Citation2011). Many authors classify financial innovation into product and process innovation. However, the distinction between the two is difficult to make new derivatives contracts, and new types of securities can be classified as new products. In addition, new organizational setups, such as payment banks and India’s UPI system, can be classified as processes (Sharma, Citation2016). Defining a product or process can be complicated, but determining what constitutes innovation is even more challenging, particularly for patent providers, who must contend with counterfeiting and imitation. The main problem they face while assigning the patent to an invention is the classification of what is genuinely new vs merely a replica. Almost nothing is entirely new; originality or novelty is a subjective thing. Innovation comes into being mainly through an evolutionary process in which new products and processes primarily result from changes in the previous products (Khan et al., Citation2021; Tufano, Citation2003).

Financial innovation has been admired and condemned throughout history for its contribution in various areas, particularly to the economy. According to a report released by the World Economic Forum (Citation2012), financial innovation has a broader impact on economic growth and significantly influences the global economic order. A good amount of literature is available on this topic, still less than in other finance areas. The research community focuses more on financial inclusion than innovation (Chibba, Citation2009). Around the world, be it developing or developed, the focus is on including more and more people in the formal financial sector. The financial innovation could facilitate the process more rapidly as it is proven to be an enhancer of economic activities (Maimbo et al., ; Marszk & Lechman, Citation2021). There is an opposite side to financial innovation as well; plenty of literature demonstrates the negative effect as it is criticized for the financial crisis that began in 2007 with the housing bubble (Meier et al., Citation2021). According to critics like John Paul, there is no evidence supporting financial innovation’s positive effect.

Furthermore, some evidence indicates that financial innovations mislead users and drive them to make poor financial decisions. Allen and Gale (Citation1994) point out that only complexity beyond the ordinary person’s understanding is often used to portray oneself as an innovator. Financial institutions purposefully create securities, so inexperienced investors barely comprehend the implications of purchasing them. When these overpriced and undervalued products are circulated in the market, a bubble develops like the housing bubble in 2007 (Ujunwa et al., Citation2021).

Therefore, such innovations which are false and non-genuine are undesirable as they are not natural substitutes for old or existing products; they might cause financial instability and affects users’ feelings, making them have unrealistic expectations from the financial system (Gennaioli et al., Citation2012; Nazir et al., Citation2021).

It is also impractical to prevent these innovations due to fear of financial crises; every system, including the financial system, is characterized by various flaws that are always there in the form of taxes, regulations, information asymmetry, and others (Schoemaker et al., Citation2018; Tufano, Citation2003). These flaws require constant improvement by replacing existing offerings with new and innovative versions and sometimes with entirely new products. It has been noticed that small, less profitable companies invent more to meet the demand for innovative products than large profitable businesses. (Lerner, Citation2006; Soumitra et al., Citation2020). They probably do not care too much about the quality and implications of the innovation during the invention process. They only aim for greater profits. To stop these small enterprises from developing damaging financial innovations, authorities must exercise caution in evaluating them (Idun & Aboagye, Citation2014; Usman et al., Citation2022).

Financial innovation can have a positive or negative impact, but it is hard to ignore since it has existed for a long time and will remain that way as long as there is a financial system. (Allen & Gale, Citation1994) Numerous research has been carried out, the majority of which have concluded that innovations in the financial sector positively influence economic growth (Bara et al., Citation2016; Wu et al., Citation2020). However, few notable cases also point to its adverse effect (Lee et al., Citation2020). Since Goldman first recognized the connection between financial development and economic growth in 1969, it has been the subject of extensive research from various scholarly perspectives. (Laeven et al., Citation2013; Levine, Citation1997) In particular, after the financial crisis of 2007, additional studies have been performed, shifting the focus from a rosy picture to the role of financial innovation in the crises. (Laeven et al., Citation2013; Levine, Citation1997) Based on the research, it is difficult to rule out the effect of financial innovations in influencing economic growth, be it positive or negative (Chien, Pantamee, Hussain, Chupradit, Nawaz, Mohsin et al., Citation2021; Levine, Citation1997).

Consequently, it is essential to investigate this relationship thoroughly from different standpoints and under various conditions. In addition, this study would help resolve the ambiguity around selecting an appropriate proxy for financial innovation, and by appropriate we mean that variable affecting economic growth positively, as indicated by earlier research (Bara et al., Citation2016; Lerner, Citation2006. Tufano, Citation2003). Furthermore, no previous study has attempted to confirm the relationship between financial innovation and economic growth using such a large data set.

The remainder of the paper begins with a theoretical and empirical literature review on financial innovation and economic growth that considers a range of perspectives and opinions. Then it proceeds to the research method, results, and study discussion. Finally, it ends with a conclusion and recommendation.

2. Theoretical and empirical literature review

There is limited empirical evidence of a link between financial innovation and economic growth. The study of financial innovation began in 1963, and an average of 23 publications are released yearly. Compared to developed countries, there are fewer studies on the relationship between financial innovation and economic growth in developing countries (Li & Xu, Citation2021).Numerous studies have investigated innovation and economic growth, but there is still a gap in the literature on financial innovation and economic development. Many studies have examined financial settings to determine how they affect economic growth. Only a few have focused on the core of financial innovations. Financial innovation stimulates economic growth by encouraging consumers to save money by constantly providing new products that meet their regularly changing needs. These saved resources are eventually used as an investment through an efficient financial intermediation process. (Pagano, Citation1993) When things are more efficient in an environment of growth, more financial products are generated with fewer resources. Innovative financial products like mobile payment systems help increase financial inclusion by lowering the friction involved in connecting to a formal financial system (Chen & Bellavitis, Citation2020).

These innovations result from innovative market participants seeking to increase their earnings by devising new and more efficient methods of distributing products and services (Bilyk, Citation2006). These innovative methods give the company a stronghold; if they stop innovating, they could lose significant market share. Innovation is the primary instrument through which enterprises can capture or lose significant market share (Utterback & Afuah, 2006). The term “innovation” refers to creating something new through the permutation and combination of existing concepts. It is up to the recipient to accept it as brand new or reject it as a duplicate of an older one. The adoption of a product by market players is the only factor that decides whether or not an innovation is successful (Katz, Citation2021; Van de Ven, Citation1986). Innovation in the financial system is similar to innovation in any other sector. Financial innovation is creating and promoting a new instrument or technology, which can be a product or a process (Al-Dmour, Al-Dmour, Rababeh et al., Citation2020a; Tufano, Citation2003). Financial innovation is sometimes misinterpreted only with the introduction of new financial products. However, it is a much broader term that includes many products, ranging from simply an innovative reporting system to credit scoring (Allen et al., Citation2021; Michalopoulos et al., Citation2009). The emergence of new financial innovation depends on changing customer, supplier, environmental, and technological requirements (Lewis & Mizen, Citation2000; Shao et al., Citation2020). Although not all the innovations are to meet the requirement of society or are economically advantageous, regulators decide their utility (Laeven et al., Citation2015; Stulz, Citation2019). However, there is no doubt that it has been there for a very long, playing a critical role in economic activities (Laeven et al., Citation2015).

Financial intermediaries also play an essential role in developing financial innovation, which boosts economic growth (Bernier & Plouffe, Citation2019; Mishra, Citation2008). Goldsmith (Citation1969) also highlighted the financial structure and economic development bond. The relationship between financial development and economic activity is well-known and well-documented historically (Goldsmith, Citation1969; Gurley & Shaw, Citation1967; Schumpeter & Backhaus, Citation2003). As well as recently (Bibi & Bibi et al., Citation2022; Laeven et al., Citation2015; Lumpkin, Citation2010; Sekhar & Gudimetla, Citation2013). Likewise, indicating the strong relationship between financial innovation and economic growth. It has constantly been regarded as a significant factor in the financial expansion. Throughout history, financial innovation has positively and negatively affected economic growth (Bernier & Plouffe, Citation2019; Arnaboldi & Rossignoli, Citation2013; Beck et al., Citation2015; Olayungbo & Quadri, Citation2019). Those who see its role positively argue that financial innovation turns saved resources into their most productive use and enhances capital accumulation (Mishra, Citation2008; Nazir et al., Citation2021). Moreover, those who oppose or negate its positive contribution argue that these innovations can be used to reap more resources from its ignorant or ill-informed users for the lower-valued product just by making it complex in the sense of comprehension by the typical investor (Allen, Citation2012).

Similarly, financial innovation has increased the volatility of industries that rely on foreign investment because exchange rate fluctuations are nearly impossible to predict (Beck et al., Citation2015; Forbes et al., Citation2018). Allen (Citation2012), more inclined to see the wrong side of it, claimed that the global financial crisis of 2008 resulted from the creation of unnecessary financial products, which generated a financial market bubble that eventually burst. It cannot be denied that this century’s financial innovation has increased the financial system’s vulnerability (Bernier & Plouffe, Citation2019; Gubler, Citation2011). Because these innovations mostly come up with the common problem of information asymmetry, causing a moral hazard to the people who indulge in these innovations (Stiglitz, Citation2010). The ignorant investor made industries more volatile and the financial system more complex and challenging to understand (Henderson & Pearson, Citation2011).

However, when we focus on the positive side of it. In that case, it has enhanced financial inclusion (Qamruzzaman & Wei, Citation2019), mobilization of funds, and infrastructure funding, all of which ultimately contribute to economic growth (Jacolin et al., Citation2019; Prior & Santomá, Citation2010). Michalopoulos et al. (Citation2009) incorporated financial innovation in their model and predicted that the economy would stagnate without it. (Xiong et al., Citation2020; Carbó Valverde et al. (Citation2007) discovered a positive relationship between product and service innovations with regional GDP, investment, and gross savings. In a study by; Chipeta and Muthinja (Citation2018); Mwinzi (Citation2014), financial innovation with mobile transactions has a significant, positive impact on economic growth. Mobile banking has become a critical financial innovation that has expanded financial deepening and intensified accessibility, boosting economic growth (Chukwuma et al., Citation2022). Mobile transactions in the developing world enable users to store value in an account accessible via a handset, convert cash whenever necessary from the store value account and transfer it between accounts (Almuhammadi, Citation2020; Donner & Tellez, Citation2008).

On the other hand, Lindholm-Dahlstrand et al. (Citation2019); Laeven et al. (Citation2015), emphasizing the critical role of financial innovation in economic growth, established a model in which financial and technological entrepreneurs interact to shape economic progress. They conclude that institutions, laws, regulations, and policies designed to constrain financial innovation also become caused to restrict technological change and economic growth. However, their models measure economic development with the financial system other than financial innovation. Therefore, it would not be wrong to say that inefficient and uncalled-for innovation could result in undesirable outcomes (Beck et al., Citation2015; Rishi, Citation2022). In the long run, there is a negative relationship between financial innovation and economic growth, while in the short term, there is a positive relationship (Ansong et al., Citation2011; Chien, Pantamee, Hussain, Chupradit, Nawaz, Mohsin et al., Citation2021). Their findings also show that financial innovation and economic growth have a bidirectional Granger cause relationship. However, Idun and Aboagye (Citation2014) discovered the opposite of (Ansong et al., Citation2011; Pholkerd & Nittayakamolphun, Citation2022). They found a short-term negative correlation between variables like M2/M1 and long-term positive relations in the long run. However, the paper’s main objective was to see the impact of financial innovation on saving, which is also a negative because existing innovations might have a negative perception about it that causes more withdrawal than deposits.

Only a small amount of experimental evidence exists on the relationship between financial innovation and economic growth. The literature from the point of empirically testing the nexus between financial innovation and economic growth shows mixed results, some indicating positive association and others showing negative.

However, as per Chien et al. (Citation2021); Garcia Bassa (Citation2013), despite the lack of empirical data on the impact of financial innovation on the economy, financial innovation can affect more economies dependent on the financial system. If we summarize the entire literature review, we can identify arguments supporting and opposing financial innovation. As a result, it would be desirable to revisit this nexus and see what the freshly obtained data shows.

3. Data and research method

3.1. Data

This study uses panel data analysis in which there are 92 cross-sectional units grouped as developing and developed countries. A wider variety of data-related issues, including unobserved heterogeneity and collinearity, are automatically resolved by having such a high number of observations (Baltagi, Citation2005), leading to better efficiency and more robust conclusions. The study uses data in which 46 cross sections for each group and period ranging from 2002 to 2020. All The data were collected from the World Bank and IMF sites. The division of countries into developed and developing is done based on the World Bank classification of the countries World Bank Country and Lending Groups—World Bank Data Help Desk, Citation2022).

Countries that lie in the Lower to the upper-middle-income category are classified as developing; on the other hand, the middle to the high-income category is classified as developed. The analysis has performed on the unbalanced panel data. The study utilizes various variables to measure the impact of financial innovations on economic growth. Three variables have been included in the study to gauge the effect of financial innovation. The first one is Domestic credit to the private sector by banks (% of GDP), following (Idun & Aboagye, Citation2014; Laeven et al., Citation2013); for simplicity, it will be called “DC” as shown in Table . Domestic credit to the private sector refers to financial resources supplied to the private sector by financial corporations, such as loans, non-equity securities purchases, trade credits, and other accounts receivable, creating a claim for repayment. It has been used to capture the improvement in the private sector. More lending to the private sector will result in more development of the economy. (Guidotti & de Gregorio, Citation1992). Since it is hard to run enterprises in this technologically savvy environment without financial technologies or innovations (Rzepka, Citation2019). In this way, this proxy variable would be good enough to capture the true nature of financial innovations. Therefore it is expected to have a positive relationship with GDP, as depicted in Table . The other variable in this line is Mobile cellular subscriptions per 100 people, representing the mobile penetration rate. Mobile subscription per 100 adults represents the number of people who own a mobile phone (though not everyone who owns a mobile engages in mobile banking), increases the probability of using it for mobile banking, facilitating financial inclusion, and thus contributing to economic growth (Klein & Mayer, Citation2011). This variable is taken following (Aker & Mbiti, Citation2010; Asongu, Citation2013; Ondiege, Citation2010); hence it would be a good proxy indicator for financial innovations (Bara et al., Citation2016). The anticipated relationship of this variable is also positive with the dependent variable, as shown in Table . The next indicator is the ratio of the monetary base to broad money following (Ansong et al., Citation2011; Mannah-Blankson & Belnye, Citation2004). Most researchers have taken this variable because broad money represents a wide range of financial resources at one’s disposal. Narrow money is also known as lesser money, so if broad money is more in comparison to narrow money, it shows more comprehensive financial resources are available at the disposal, hence more financial innovations (Ansong et al., Citation2011). This variable has a positive relationship as well as shown in Table . Besides these variables, the researcher has also taken some control variables to have more robust results: general government final consumption expenditure (annual % growth), Gross fixed capital formation (% of GDP). Trade (% of GDP). Finally, for measuring the economic growth out of many variables, GDP per capita growth (Annual %), denoted as GDP, has taken the following (Bara et al., Citation2016).

Table 1. Variables description and expected signs

3.2. Descriptive statistics and correlation analysis

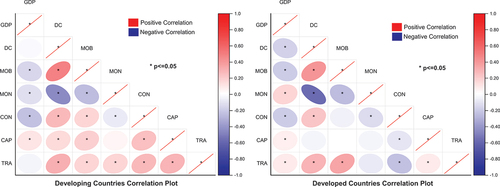

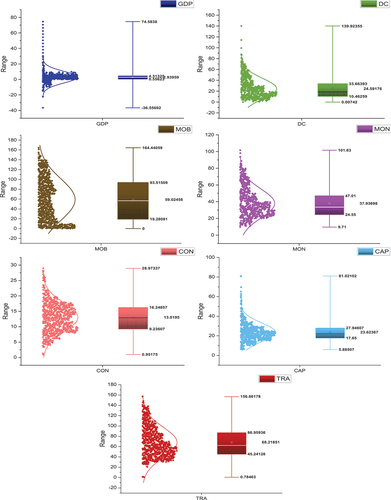

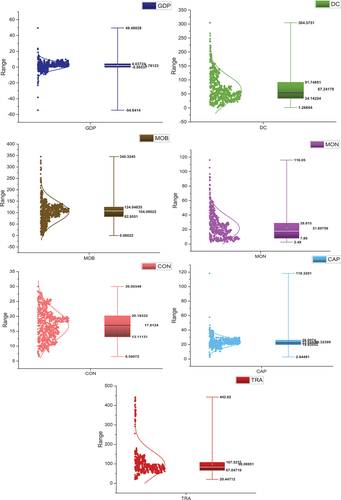

The descriptive statistics are shown in box plots in Figures , where the dependent variable GDP’s Value spans from 36.5 to 74.8 in developing countries and from −54.6 to 49.4 in developed nations. The other independent variables, interchangeably used for financial innovation as DC in model 1, display a value that varies from.00742 to 139.92 in developing countries and from 1.266 to 304.57 in developed nations. The following variable, MOB, display values from 0 to 164.44 and .080 to 345.32 in developing and developed nations, respectively. Finally, the variable, MON, has values ranging from 9.71 to 101.63 and 2.48 to 116.05 in both developing and developed countries, respectively. In addition, other variables CON, CAP, and trade included in all models are depicted in Figures for developing and developed nations, respectively. In addition to the descriptive statistics, the correlation between the variables is depicted in Figure separately for developing and developed countries. The red colour in the figure shows a positive correlation between the variables, and the blue colour highlights the negative correlation. Furthermore, no colour boxes indicate there is no correlation. A 95% confidence level establishes the relationship between the variables.

Figure 1. Correlation plot for developing and developed countries.

Figure 2. Descriptive statistics summary of developing countries (GDP, DC, MOB, MON, CON, CAP and TRA) through box plot.

Figure 3. Descriptive statistics summary of developed countries (GDP, DC, MOB, MON, CON, CAP and TRA) through box plot.

3.3. Research methodology

Analyzing the panel data began by checking whether the data is pool-able or not because if data is pool-able, which means there is no heterogeneity in the data. Simply OLS can be applied, and applying the OLS method would be enough. However, if the data does not support the test requirement of homogeneity, then the OLS cannot be applied. In this case, a different data analysis technique would be more adequate. When the test for pool-ability has run for which the null hypothesis is that the data is pool-able or has the common intercept, the p-value comes out to be less than 5% for both the developing and developed countries, which rejects the possibility of applying OLS here.

The next step after checking the pool-ability is to check the time effect, which is nothing but checking whether cross-sectional units show the same effect over some time. It is done by introducing time dummies in the model, which is done through a Wald joint test on time dummies, for which the null hypothesis is that there is no time effect in the panel. The result of the test shows there is a time effect. Therefore, in this case, the researcher is left with only applying either the fixed effect model or random effect model to begin choosing one of these two methods. Hausman test is applied in each model. This test helps to decide which effect to use, whether the fixed effect model or the random-effect model.

3.4. Model specification: Fixed and random effect

Fixed-effect model is applied when the intercept and slope are different for each cross-sectional unit. To control the difference in intercept values fixed-effect model introduces a common alpha representing each intercept of different individual equations of every cross-section. In this way, it controls unobserved heterogeneity. The fixed effect method allows heterogeneity or individuality among the cross-sectional units by allowing its intercept value.

The intercept of an individual or cross-section unit may differ, but the intercept does not change over time.

The general equation for the fixed effect model includes “y,” representing the value of dependent variables. “i” shows different cross-sections, and “t” is for time series. α and β are the line intercepts and slope, respectively. In the last, there is an error term representing the rest of the variables left to be included in the model; in addition, μ is a common intercept value used to capture unobserved heterogeneity. As it is established that the fixed effect model is more appropriate than the random effect, the study has used four models of fixed effect using different combinations of the variable utilized for financial innovation to measure the effects of different combinations of variables on GDP. Furthermore, it also helps to understand more clearly which variable among them is a more suitable proxy for financial innovation as there is some confusion around the correct proxy variable for financial innovation (Bara et al., Citation2016). The following are the equations for the results of the fixed-effect method.

Model 1:

Model 2:

Model 3:

Here “i” represent different countries, and “t” is the period. The coefficient values of four regressors showed through β(1 to 5). GDP represents the value of GDP per capita’s annual percentage growth rate based on the constant currency in developing countries. The value of domestic credit to the private sector implies the disbursement of financial resources to the private sector represented through DCit. MOBit captures the value of mobile cellular telephone subscriptions for public services. Variable MONit means the value of the percentage of the monetary base to broad money, and the variable CONit shows the General final consumption expenditures of the government as a percentage of GDP. CAPit is used to denote the value of gross fixed capital formation as a percentage of GDP, and in the same way, TRA exhibits the net value of the sum of exports and imports of goods and services. A DUM_FC variable for the financial crisis of 2007–2008 has been taken a value of 1 and otherwise 0. This variable is used to account for the effect of the financial crisis on the dependent variable in these models and finally denotes Individual Effect,

for Error term, and α is a constant term.

The random effects technique is an alternate estimating technique that treats the constants for every segment as random variables rather than fixed variables. The intercept for every cross sectional component is supposed to be derived from a familiar intercept α (which is identical for every cross sectional components and over time) plus a random variable ϵi that tends to vary cross sectionally although is constant in time, ϵi attempts to measure the random variation of every entity’s intercept term from the global intercept term. The random effects panel technique can be written as

Where,

4. Empirical results

4.1. Hausman test

The values of the test are shown in Table . According to the table, the fixed effect model is more suitable in all cases except in model 2 of developing countries, where the p-value rejects the test’s null hypothesis. The null hypothesis is that the random effect is consistent; therefore, in model 2, the results of the random effect model would be more appropriate.

Table 2. Hausman test for model selection

4.2. Random effect model

When the analysis is done on the random effect model, it shows a significant negative relationship between the different independent variables taken in this study and the dependent variable, except in the case of MON, both in developing and developed countries. However, the primary purpose to run this model, was to check whether this method is usable here or not. This is done through the houseman’s test, as already described above. The results of this test show that in the case of model 2, random effects are more appropriate. In model 2, here, the variable MOB represents financial innovation. The variable bears a negative coefficient, i.e., -0.0293353, which means there is a negative relationship between financial innovation and economic growth. Except for model 2, the housemen test shows results in favour of a fixed effect in all other cases as depicted in Table .

Table 3. Results random effect model

The essential difference between fixed and random effects is that in the random effect model, the difference in the intercept value is not considered due to the difference in cross-sectional units. However, it is considered because of the randomness of the selection trying to represent the region. In the fixed-effect model, we assume that we have chosen all the sample units and that the intercept value difference is due to the individual units.

4.3. Fixed effect model

The analysis of model 1 begins with the fixed effect method by the Hausman test, as shown in Table , by taking the variable DC as an independent variable representing the financial innovations to see its effect on economic growth. Variable DC, negatively relates to the dependent variable. It reacts in the same fashion in developing and developed countries with coefficient values of −0.1097264 and −0.0758177, respectively, at a 1% significance level. In order to check for structural changes during the study period. We have also included the dummy for the global financial crises of 2007–08, and the results reveal that in the case of developing countries, it is positively affecting the dependent variables, but the results are not significant, which is why we cannot conclude anything from this. On the other hand, in the case of developed countries, the results are same as without adding dummy.

The probable reason for this negative relationship between dc and gdp could be due to unnecessary growth in credit to the private sector following flawed policies due to the general impression that credit growth always leads to economic growth. (Cecchetti & Kharroubi, Citation2019). However, this is the same in both the developing and developed world. Therefore, some hidden structural issues might be there and need a focused study because providing credit to the private sector is generally associated positively with economic growth. (De Gregorio & Guidotti, Citation1995; Petkovski & Kjosevski, Citation2014; Yakubu & Abdallah, Citation2021).

In Model 2, MOB has been used as an independent variable instead of DC for financial innovation to see whether the impact on the dependent variable changes. Variable MOB shows the mobile subscription rate representing mobile banking, the expectation from this variable was that, it would have a positive impact on economic growth, as also shown in Table . because in this age of technology, all the necessary means which can be used as money, generates through technology; having mobile devices ensures accessing these FinTech instruments, therefore, owing mobile devices has become an essential part of being the participant of this technology-driven financial system, without mobile device there is no scope for that. The coefficient values were −0.0263439, −0.0164801, in the developing and developed countries, respectively, with a 1% significance level both in the developing and the developed world. This is contrary to the expectation of positive association. The reason for that could be that financial innovation through mobile banking might have improved the efficiency in transferring the money from source to destination but could not have increased the intention or desire to purchase more which ultimately turns into more production and consumption of goods and services, leading to more economic growth (Mirabi et al., Citation2015). Another way of looking at it would be in terms of liquidity; having mobile banking ensures liquidity all the time, which creates Inflationary pressure that is not considered suitable for the economy’s growth (Chu & Chu, Citation2020; Sotiropoulou & Giakoumatos, Citation2019). However, suppose we examine this variable from the perspective of the study’s second goal, determining which variable serves as a good substitute for financial innovation. In that case, it may be a good substitute because the coefficient values are significant at 1% However, when dummy was added for the period of financial crises, the results were slightly altered; during the crisis period, this variable showed a positive association rather than a negative association with the dependent variable, with the coefficient value being 1.289503 in developing countries with a 10% significance level, and a negative relationship with the dependent variable in developed countries with a 1% significance level. The result of the dummy shows that during a crisis, as financial innovation increases, so does economic growth in developing countries, but in developed countries, as financial innovation increases, economic growth decreases. . The overall finding from this variable contradicts the notion that more mobile banking means increased financial deepening, contributing to greater economic activities (Karahan & Yılgör, Citation2011). This relationship between the rates of financial innovation from mobile subscriptions is contrary to expectations as well as contradicts the previous study conducted by Mago and Chitokwindo (Citation2014)

Model 3 runs with the remaining variable, the ratio of the monetary base to broad money, which represents the state of liquidity in the form of cash and cash equivalent. Results are interesting, showing that variable MON is the only variable establishing a positive relationship with the dependent variable, which means if broad money grows in comparison to narrow money, there will be more liquidity in the system in the form of new financial instrument, which makes a transfer of resources easy and efficient which could also contribute in increased purchasing power of the people willing to spend and that ultimately cause the economic growth. In both the cases of developing and developed nations, the coefficient values are 0.0914629 and 0.0548293, respectively, with 1% & 5% significance level in developing countries and developed countries respectively, as shown in Table . These positive results with this proxy variable are aligned with the results of (Petkovski & Kjosevski, Citation2014; Michalopoulos et al., Citation2009; Laeven et al., 2016; Carbó Valverde et al., Citation2007; Garcia Bassa, Citation2013; Mwinzi, Citation2014). In addition, it supports Shaw’s argument from 1973, which said that financial development raises the economy’s saving deposits and thus becomes a reason to grow the economy; this appears to be the case in these circumstances as well. When the dummy is added to this model to examine the impact of financial crises, we discover that the results are insignificant in developing countries, however, in developed countries, they have a negative relationship. Implying that during a financial crisis period, financial innovations actually reduce economic growth.

Table 4. Results of fixed effect model

Other macro-economic variables used in all the models, such as CAP and TRADE, also have positive coefficient values with a 1% significant level in developing and developed nations across all three models. However, one variable, CON, bears negative coefficient values also in all models.

After analysing these three models, it is clear that: all the variables significantly affect the dependent variable. The variable DC has remained significant and shows the same relationship with the dependent variable throughout, except when its dummy is used in developing countries. In the same way, the variable MOB also bears the same sign both in developing and developed countries, but the dummy used for the period of financial crises shows opposite results from the whole period of the study only in case of developing countries. Finally, the variable MON, which only shows a positive sign, is significant in developing countries with a 1% significance level and 5% in developed countries. The dummy in this model depicts that in developing countries, financial innovation positively affects economic growth, although the value is insignificant; contrary to this, there is a negative association in developed countries.

In order to run a fixed-effect model efficiently, some assumptions must be checked beforehand. The first one may be the error term’s mean value, which should be zero. When it is checked in all the three models with different variables in the developing and developed world, it comes out to be zero. The next assumption could be to see whether the error term is normally distributed or not; in that case, the Jarque Bara test is used, with the null hypothesis that the error term is normally distributed. Although the error term in this data set is not normally distributed in developing and developed countries, this is not a major concern, especially in such a large data set (Baltagi, Citation2005). When it comes to checking the autocorrelation, the test that is famously applied is Durbin Watson and Wooldridge. In the case of developing countries, when the model is run with the variable DC, there is no autocorrelation, with the Durbin Watson value being 1.19456 in the developed world and 0.89042 in the developing world. This is also cross-checked with Wooldridge with the first-order difference that also turns out to be no first-order autocorrelation. The same procedure was applied in other models, and the autocorrelation results were more or less identical, as shown in Table . The other thing to check is multi-collinearity between the variables, as we can see, in Figures ; that showed variables in both the developing and developed countries are not correlated because no variable shows a correlation of more than 0.80 above that value; it is considered highly correlated. The next thing to check before running the model is homoscedasticity in the Variance of error terms; the Breusch-Pagan test is applied to check that the Null hypothesis. The Variance of the unit-specific error is 0, and in all three models, the test fails to reject the null hypothesis, which means there is homoscedasticity in the model. And finally, to know the overall fitness of the model’s joint test on the named regressor is applied in all the models of developing and developed countries. The p values are less than 0.05 in all cases, so the null hypothesis that the model is not fit is rejected.

5. Conclusion and recommendations

An efficient financial system utilizes economic resources effectively, facilitating the transfer of resources and fostering economic growth (Qamruzzaman & Jianguo, Citation2018a). With the introduction of the new product, services and organizations in the financial system, known as financial innovations, the financial system sometimes experiences substantial expansion as well as contraction as some of the innovations have been beneficial to the economy, as Merton (Citation1992) pointed out and called these innovations the engine for growth, while others indicated its negative aspect and blamed it for the disaster in the economy.

This study re-examines the relationship between financial innovation and economic growth in developing and developed countries’ perspectives and clarifies the appropriate proxy for financial innovation using 96 cross-sectional units.

There are mainly three variables used for financial innovation. Accordingly, three Models were constructed. Model 1 utilizes “DC” as the main variable for financial innovation along with other macroeconomic variables; similarly, “MOB” is used in model 2 and “MON” in model 3. According to the nature of the study, the fixed effect method of panel data was used. The methodology used in this study reveals that, in general, financial innovation has a negative impact on economic growth; the negative results are in line with a study conducted by Qamruzzaman & Jianguo (Citation2018b); Bernier & Plouffe (Citation2019). The variable DC has been significant throughout all the models at a 1% significance level both in developing and developed countries, and the variables MOB shows constant negative relation with the economic growth, same as the DC., and finally variable MON shows a consistent positive association with the economic growth irrespective of the group indicating that it could be the right proxy for financial innovation. Because only through this variable, we have seen the positive relationship of financial innovation on economic growth that’s why it fits in our definition of best proxy variables.

The negative association between DC and GDP might be due to excessive or undue growth in private sector credit. The reason for excessive growth in credit could be to follow inappropriate policies which are based on the notion that credit growth always leads to economic growth. (Cecchetti & Kharroubi, Citation2019) Furthermore, a wide range of literature shows that credit growth leads to economic growth (De Gregorio & Guidotti, Citation1995; Petkovski & Kjosevski, Citation2014; Yakubu & Abdallah, Citation2021) although we found negative relationship between domestic credit and economic growth in both developing and developed countries therefore this relationship might be rechecked in future studies.

Financial innovation through mobile banking would have enhanced the efficiency of transferring money from source to destination, but it might not have raised the intention or desire to purchase more, which leads to higher production and consumption of goods and services, resulting in economic growth (Mirabi et al., Citation2015). Mobile banking ensures constant liquidity, which causes inflationary pressure unsuitable for economic progress (Chu & Chu, Citation2020; Sotiropoulou & Giakoumatos, Citation2019). This contradicts the idea that mobile banking increases financial depth and economic activity (Karahan & Yılgör, Citation2011). This association between financial innovation and mobile subscriptions contradicts the findings of Mago and Chitokwindo’s (Citation2014)

The ratio of the monetary base to broad money is the only variable that has a positive relationship with the dependent variable. This means that if broad money grows relative to narrow money, there will be more liquidity in the system in the form of new financial instruments, which makes it convenient and efficient to move resources. This could also increase the purchasing power of people who are willing to spend, which would lead to economic growth. Petkovski and Kjosevski (Citation2014), Michalopoulos et al. (Citation2009), Laeven et al. (2016), Carbó Valverde et al. (Citation2007), Garcia Bassa (Citation2013), and Mwinzi (Citation2014) all found positive results with this proxy variable. It also backs up Shaw’s argument from 1973, which said that financial development raises the economy’s savings deposits and gives a reason to grow the economy. This seems to be the case here as well. In order to examine the effects of financial innovations on economic development during the global financial crises, we introduced dummy for the financial crises in each model. The results are similar for the entire period of the study with the exception of the dummies of model 1 and model 2 in developing nations and model 3 in developed countries, which demonstrate an opposite relationship.

The study results are aligned with the theory developed by Arnaboldi and Rossignoli (Citation2013), which indicates that innovation is a double-edged sword with both positive and negative side effects. The good side drives the economy to positive growth, and the bad side takes it to negative (Beck et al., Citation2015). However, results contradict the studies pointing out that the positive role is much higher than the negative side of it (Bara et al., Citation2016). The poorer financial system development can explain the negative effects in some developing countries. Therefore it is important to mention that there are noteworthy differences in the financial system of developing countries from those of developed countries. The results might have differed if these countries had been taken separately.

Mainly the negative relationship between financial innovation and economic growth points out possibly two implications, one on the part of regulators, to not allow such innovation that does not prove to be good for the economy. To do that, a separate study can be done to chalk out features of those innovations that have proven to be good for the economy; the second one we can take from this could be to facilitate more and more innovation in terms of the financial system because not allowing any innovation is not an option but encouraging those innovations which adds value to the society should be the main focus of the policies and policymakers

Furthermore policymakers should focus more on supply side of financial innovation rather its demand side because innovations that are not actually beneficial can be demanded by the society. In addition to this, policymaker can also work on the approach of regulating financial innovations because most of the innovation, in this edge, are based on the information technology which are precisely called FinTech. Furthermore, current study also suffers with certain limitations. There are various new edged methodologies and approaches that can be used but we have used rather simple technique when measuring financial innovation’s impact on economic growth. Future researcher can replicate the same study using new techniques like GMM or panel ARDL methods with different set of control variables.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

Notes on contributors

Mohd Hammad Naeem

Mohd Hammad Naeem Department of Commerce, Aligarh Muslim University, Aligarh, India Mohd Hammad Naeem is currently a Ph.D candidate at the Faculty of commerce Aligarh Muslim University Aligarh, under the supervision of Prof. Mohd Yameen. Mohd Hammad Naeem has done his master degree in commerce. His main research Interest include financial innovations, financial development and economic growth.

Mohammad Subhan

Mohammad Subhan Department of Commerce, Aligarh Muslim University, Aligarh, India. Mohammad Subhan currently pursuing a PhD from Department of Commerce, Aligarh Muslim University, Aligarh, India. His areas of research are energy economics, financial management and international trade. He completed his bachelor’s and master’s degree from Aligarh Muslim University. He published more than two research papers in reputed indexed journals. Besides, He attended and presented four Conferences/ Seminars /Symposium. His expertise in secondary data analysis techniques mainly; NARDL model, ARDL model, wavelet coherence analysis and other econometrics models.

Md Shabbir Alam

Md Shabbir AlamDepartment of Economics and Finance, College of Business Administration, University of Bahrain, Sakhir, Bahrain. Dr. Md Shabbir Alam joined University of Bahrain as an Assistant Professor in Department of Economics & Finance in 2021. Prior to this, Dr Md Shabbir Alam served as an Assistant Professor at Dhofar University, Oman, Saudi Electronic University, Saudi Arabia, Bakhtar University Afghanistan, and Jyoti Vidyapeeth Women’s University India, Etc. He worked as Post Doctorate Fellow in the Department of Economics Aligarh Muslim University India. He has a doctorate in economics from Aligarh Muslim University. Dr Md Shabbir Alam an author of one book and published more than sixty research papers in reputed indexed journals. Dr Alam evaluated Four Ph.D. thesis as an external examiner, supervised dissertations of more than Twenty Master and Thirty-Two Bachelor students. Besides, He attended and presented Sixteen Conferences/ Seminars /Symposium.

Mamdouh Abdulaziz Saleh Al-Faryan

Mamdouh Abdulaziz Saleh Al-Faryan Department of Accounting and Financial Management, Faculty of Business and Low, University of Portsmouth, United Kingdom. Mamdouh Abdulaziz Saleh Al-Faryan, a visiting Researcher at the University of Portsmouth, Department of Accounting and Financial Management, Faculty of Business and Law. Mamdouh is a member of forty national and international professional associations. He has worked tirelessly to expand his experience and financial acumen, which would guide him down the path into leadership and higher level of responsibility. So far, he has several publications in the field of economics, finance, corporate governance, and accounting, which have been published in top international journals. Mamdouh also serves as a reviewer for a number of international journals and holds academic and research distinction.

Mohammad Yameen

Mohammad Yameen Department of Commerce, Aligarh Muslim University, Aligarh, India. Prof. Mohammad Yameen is presently working as Professor in the Department of Commerce, Aligarh Muslim University, Aligarh (U.P.). He has above twenty years of teaching experience. His area of specialization is Management Accounting and Financial Management. Under his guidance a large number of students have completed their Dissertations/Projects at Post Graduate level. He has also guided many research scholars for the award of Ph.D. degree. He has attended several national & international conferences and written many research papers in refereed and reputed journals.

References

- Adams, D. W. (2021). Effects of finance on rural development. In Adams, D.W, Graham, D.H, Von Pischke, J.D. (Eds.) Undermining rural development with cheap credit (pp. 11–20). Routledge.

- Ahmad, M., & Shah, S. Z. A. (2020). Overconfidence heuristic-driven bias in investment decision-making and performance: Mediating effects of risk perception and moderating effects of financial literacy. Journal of Economic and Administrative Sciences.

- Aigbokhan, B. E. (2000). Poverty, growth and inequality in Nigeria: A case study.

- Aker, J. C., & Mbiti, I. M. (2010). Mobile phones and economic development in Africa. The Journal of Economic Perspectives, 24(3), 207–232.

- Al-Dmour, A., Al-Dmour, R., & Rababeh, N. (2020a). The impact of knowledge management practice on digital financial innovation: The role of bank managers. VINE Journal of Information and Knowledge Management Systems, 51(3), 492–514. https://doi.org/10.1108/VJIKMS-01-2020-0006

- Allen, F. (2012). Trends in financial innovation and their welfare impact: An overview. European Financial Management, 18(4), 493–514. https://doi.org/10.1111/j.1468-036X.2012.00658.x

- Allen, F., & Gale, D. (1994). Financial innovation and risk sharing. MIT press.

- Allen, F., Gu, X., & Jagtiani, J. (2021). A survey of FinTech research and policy discussion. Review of Corporate Finance, 1(3–4), 259–339. https://doi.org/10.1561/114.00000007

- Almuhammadi, A. (2020). An overview of mobile payments, FinTech, and digital wallet in Saudi Arabia. 2020 7th International Conference on Computing for Sustainable Global Development (INDIACom), 271–278

- Ansong, A., Marfo-Yiadom, E., & Ekow-Asmah, E. (2011). The effects of financial innovation on financial savings: Evidence from an economy in transition. Journal of African Business, 12(1), 93–113. https://doi.org/10.1080/15228916.2011.555271

- Arnaboldi, F., & Rossignoli, B. (2013). Financial Innovation in Banking. University of Milan.

- Asongu, S. A. (2013). How has mobile phone penetration stimulated financial development in Africa? Journal of African Business, 14(1), 7–18. https://doi.org/10.1080/15228916.2013.765309

- Baltagi, B. H. (2005). Econometric Analysis of Panel Data. In 3rd ed (pp. 1-293). John Wiley & Sons.

- Bara, A., Mugano, G., & Le Roux, P. (2016). Financial innovation and economic growth in the SADC. African Journal of Science. Technology, Innovation and Development, 8(5), 483–495.

- Beck, T., Senbet, L., & Simbanegavi, W. (2015). Financial inclusion and innovation in Africa: An overview. Journal of African Economies, 24(suppl_1), i3–i11. https://doi.org/10.1093/jae/eju031

- Berman, A., Cano-Kollmann, M., & Mudambi, R. (2022). Innovation and entrepreneurial ecosystems: FinTech in the financial services industry. Review of Managerial Science, 16(1), 45–64. https://doi.org/10.1007/s11846-020-00435-8

- Bernier, M., & Plouffe, M. (2019). Financial innovation, economic growth, and the consequences of macroprudential policies. Research in Economics, 73(2), 162–173. https://doi.org/10.1016/j.rie.2019.04.003

- Bibi, R., Bibi, R. others (2022). Banking sector development and economic growth in south Asian countries: Dynamic panel data analysis. Journal of Environmental Science and Economics, 1(1), 52–57. https://doi.org/10.56556/jescae.v1i1.10

- Bilyk, V. (2006). Financial Innovations and the Demand for Money in Ukraine. National University

- Carbó Valverde, S., López del paso, R., & Rodrı́guez Fernández, F. (2007). Financial innovations in banking: Impact on regional growth. Regional Studies, 41(3), 311–326. https://doi.org/10.1080/00343400600928350

- Cecchetti, S. G., & Kharroubi, E. (2019). Why does credit growth crowd out real economic growth? The Manchester School, 87(S1), 1–28. https://doi.org/10.1111/manc.12295

- Chen, Y., & Bellavitis, C. (2020). Blockchain disruption and decentralized finance: The rise of decentralized business models. Journal of Business Venturing Insights, 13, e00151. https://doi.org/10.1016/j.jbvi.2019.e00151

- Chibba, M. (2009). Financial inclusion, poverty reduction and the millennium development goals. The European Journal of Development Research, 21(2), 213–230. https://doi.org/10.1057/ejdr.2008.17

- Chien, F., Pantamee, A. A., Hussain, M. S., Chupradit, S., Nawaz, M. A., & Mohsin, M. (2021). Nexus between financial innovation and bankruptcy: Evidence from information, communication and technology (ict) sector. In The Singapore Economic Review (pp. 1–22). World Scientific Publishing Co Pte Ltd.

- Chipeta, C., & Muthinja, M. M. (2018). Financial innovations and bank performance in Kenya: Evidence from branchless banking models. South African Journal of Economic and Management Sciences, 21(1), 1–11. https://doi.org/10.4102/sajems.v21i1.1681

- Chu, L. K., & Chu, H. V. (2020). Is too much liquidity harmful to economic growth? Quarterly review of economics and finance, 76, 230–242. https://doi.org/10.1016/j.qref.2019.07.002

- Chukwuma, O. V., Ugwu, J. I., & Babalola, D. S. (2022). Application of forensic accounting in predicting the financial performance growth of MTN mobile communication in Nigeria. Journal of Environmental Science and Economics, 1(1), 67–76. https://doi.org/10.56556/jescae.v1i1.86

- de Gregorio, J., & Guidotti, P. E. (1995). Financial development and economic growth. World Development, 23(3), 433–448. https://doi.org/10.1016/0305-750x(94)

- Djoumessi, E. C. K. (2009). Financial development and economic growth: a comparative study between Cameroon and South Africa ( Doctoral dissertation). University of South Africa, Pretoria.

- Donner, J., & Tellez, C. A. (2008). Mobile banking and economic development: Linking adoption, impact, and use. Asian Journal of Communication, 18(4), 318–332. https://doi.org/10.1080/01292980802344190

- Edquist, C. (2019). Towards a holistic innovation policy: Can the Swedish National Innovation Council (NIC) be a role model? Research Policy, 48(4), 869–879. https://doi.org/10.1016/j.respol.2018.10.008

- Forbes, K., Hjortsoe, I., & Nenova, T. (2018). The shocks matter: Improving our estimates of exchange rate pass-through. Journal of International Economics, 114, 255–275. https://doi.org/10.1016/j.jinteco.2018.07.005

- Frame, W. S., & White, L. J. (2004). Empirical studies of financial innovation: Lots of talk, little action? Journal of Economic Literature, 42(1), 116–144. https://doi.org/10.1257/002205104773558065

- Garcia Bassa, G. (2013). Application of theoretical models to financial innovation. Universitat Pompeu Fabra. https://repositori.upf.edu/bitstream/handle/10230/21130/Gerbert%20Garcia.pdf?sequence=1&isAllowed=y

- Gennaioli, N., Shleifer, A., & Vishny, R. (2012). Neglected risks, financial innovation, and financial fragility. Journal of Financial Economics, 104(3), 452–468. https://doi.org/10.1016/j.jfineco.2011.05.005

- Goldsmith, R. (1969). New Haven: Yale University Pres (pp. 114-123). National Bureau of Economic Research. http://www.nber.org/chapters/c4417.pdf

- Gubler, Z. J. (2011). The Financial Innovation Process: Theory and Aplication. Delaware Journal of Corporate Law 36 (1). http://ssrn.com/abstract=1905458

- Guidotti, P., & de Gregorio, J. (1992). Financial development and economic growth. IMF Working Papers, 92 (101),i. https://doi.org/10.5089/9781451852455.001

- Gurley, J. G., & Shaw, E. S. (1967). Financial structure and economic development. Economic Development and Cultural Change, 15(3), 257–268. https://doi.org/10.1086/450226

- Handa, J., & Khan, S. R. (2008). Financial development and economic growth: A symbiotic relationship. Applied Financial Economics, 18(13), 1033–1049. https://doi.org/10.1080/09603100701477275

- Hasan, R., & Barua, S. (2015). Financial development and economic growth: Evidence from a panel study on South Asian countries. Asian Economic and Financial Review, 5(10), 1159–1173. https://doi.org/10.18488/journal.aefr/2015.5.10/102.10.1159.1173

- Henderson, B. J., & Pearson, N. D. (2011). The dark side of financial innovation: A case study of the pricing of a retail financial product. Journal of Financial Economics, 100(2), 227–247. https://doi.org/10.1016/j.jfineco.2010.12.006

- Huntington, S. P. (1993). If not civilizations. What? Paradigms of the post-cold War World. Foreign Affairs, 186-194.

- Idun, A. A. A., & Aboagye, A. Q. (2014). Bank competition, financial innovations and economic growth in Ghana. African Journal of Economic and Management Studies.

- Jacolin, L., Massil Joseph, K., & Noah, A. (2019). Informal sector and mobile financial services in developing countries: Does financial innovation matter? Banque de France Working Paper, May 2019, WP #721.

- Karahan, O., & Yılgör, M. (2011). Financial deepening and economic growth in Turkey. MIBES Transactions, 5(2), 19–29.

- Katz, M. L. (2021). Big Tech mergers: Innovation, competition for the market, and the acquisition of emerging competitors. Information Economics and Policy, 54, 100883. https://doi.org/10.1016/j.infoecopol.2020.100883

- Khan, S., Khan, M. K., & Muhammad, B. (2021). Impact of financial development and energy consumption on environmental degradation in 184 countries using a dynamic panel model. Environmental Science and Pollution Research, 28(8), 9542–9557. https://doi.org/10.1007/s11356-020-11239-4

- Klein, M. U., & Mayer, C. (2011). Mobile banking and financial inclusion: The regulatory lessons. World Bank Policy Research Working Paper, (5664).

- Kyophilavong, P., Uddin, G. S., & Shahbaz, M. (2016). The nexus between financial development and economic growth in Lao PDR. Global Business Review, 17(2), 303–317. https://doi.org/10.1177/0972150915619809

- Laeven, L., Levine, R., & Michalopoulos, S. (2013). Financial Innovation and Endogenous Growth. SSRN Electronic Journal. https://doi.org/10.2139/ssrn.2382748

- Laeven, L., Levine, R., & Michalopoulos, S. (2015). Financial innovation and endogenous growth. Journal of Financial Intermediation, 24(1), 1–24. https://doi.org/10.1016/j.jfi.2014.04.001

- Lee, C. C., Wang, C. W., & Ho, S. J. (2020). Financial inclusion, financial innovation, and firms’ sales growth. International Review of Economics & Finance, 66, 189–205. https://doi.org/10.1016/j.iref.2019.11.021

- Lerner, J. (2006). The new new financial thing: The origins of financial innovations. Journal of Financial Economics, 79(2), 223–255. https://doi.org/10.1016/j.jfineco.2005.01.004

- Lerner, J., & Tufano, P. (2011). The consequences of financial innovation: A counterfactual research agenda. In The Rate and Direction of Inventive Activity Revisited (pp. 523–575). University of Chicago Press.

- Levine, R. (1997). Financial development and economic growth: Views and agenda. Journal of Economic Literature, 35(2), 688–726.

- Lewis, M. K., & Mizen, P. D. (2000). Monetary economics. OUP Catalogue.

- Lindholm-Dahlstrand, A., Andersson, M., & Carlsson, B. (2019). Entrepreneurial experimentation: A key function in systems of innovation. Small Business Economics, 53(3), 591–610. https://doi.org/10.1007/s11187-018-0072-y

- Li, B., & Xu, Z. (2021). Insights into financial technology (FinTech): A bibliometric and visual study. Financial Innovation, 7(1), 1–28. https://doi.org/10.1186/s40854-021-00285-7

- Lumpkin, S. (2010). Regulatory issues related to financial innovation. OECD Journal: Financial Market Trends, 2009(2), 1–31.

- Lusardi, A. (2019). Financial literacy and the need for financial education: Evidence and implications. Swiss Journal of Economics and Statistics, 155(1), 1–8. https://doi.org/10.1186/s41937-019-0027-5

- Mago, S., & Chitokwindo, S. (2014). The impact of mobile banking on financial inclusion in Zimbabwe: A case for Masvingo Province. Mediterranean Journal of Social Sciences, 5(9), 221.

- Maimbo, S., Saranga, T., & Strychacz, N. (2010). Facilitating Cross-Border Mobile Banking in Southern Africa. Economic Premise; No. 26. World Bank, Washington, DC.

- Mannah-Blankson, T., & Belnye, F. (2004). Financial innovation and the demand for money in Ghana. In Accra: Bank of Ghana (pp. 1–23). Routledge.

- Marszk, A., & Lechman, E. (2021). Reshaping financial systems: The role of ICT in the diffusion of financial innovations–Recent evidence from European countries. Technological Forecasting and Social Change, 167, 120683. https://doi.org/10.1016/j.techfore.2021.120683

- Meier, S., Gonzalez, M. R., & Kunze, F. (2021). The global financial crisis, the EMU sovereign debt crisis and international financial regulation: Lessons from a systematic literature review. International Review of Law and Economics, 65, 105945.

- Merton, R. C. (1992). Financial innovation and economic performance. Journal of Applied Corporate Finance, 4(4), 12–22. https://doi.org/10.1111/j.1745-6622.1992.tb00214.x

- Michalopoulos, S., Laeven, L., & Levine, R. (2009). Financial innovation and endogenous growth (No. w15356). National Bureau of Economic Research.

- Mirabi, V., Akbariyeh, H., & Tahmasebifard, H. (2015). A study of factors affecting on customers purchase intention. Journal of Multidisciplinary Engineering Science and Technology (JMEST), 2, 1.

- Mishra, P. K. (2008). Financial innovation and economic growth-a theoretical approach

- Mwinzi, M. D. 2014. The Effect of Financial Innovation on Economic Growth in Kenya. Nairobi: School of Business, University of Nairobi. http://erepository.uonbi.ac.ke/handle/11295/7484

- Nazir, M. R., Tan, Y., & Nazir, M. I. (2021). Financial innovation and economic growth: Empirical evidence from China, India and Pakistan. International Journal of Finance & Economics, 26(4), 6036–6059. https://doi.org/10.1002/ijfe.2107

- Olayungbo, D., & Quadri, A. (2019). Remittances, financial development and economic growth in sub-Saharan African countries: Evidence from a PMG-ARDL approach. Financial Innovation, 5(1), 1–25. https://doi.org/10.1186/s40854-019-0122-8

- Ondiege, P. (2010). Mobile banking in Africa: Taking the bank to the people. Africa Economic Brief, 1(8), 1–16.

- Pagano, M. (1993). Financial markets and growth: An overview. European Economic Review, 37(2–3), 613–622. https://doi.org/10.1016/0014-2921(93)90051-B

- Petkovski, M., & Kjosevski, J. (2014). Does banking sector development promote economic growth? An empirical analysis for selected countries in Central and South Eastern Europe. Economic Research-Ekonomska Istraživanja, 27(1), 55–66. https://doi.org/10.1080/1331677x.2014.947107

- Pholkerd, P., & Nittayakamolphun, P. (2022). Nexus Financial Innovation and Economics Growth in Thailand. ABAC Journal, 42(3), 148–161.

- Prior, F., & Santomá, X. (2010). Banking the unbanked using prepaid platforms and mobile telephones in the United States. IESE Business School – University of Navarra, Working Paper WP-839 January, 2010.

- Qamruzzaman, M., & Jianguo, W. (2018a). Investigation of the asymmetric relationship between financial innovation, banking sector development, and economic growth. Quantitative Finance and Economics, 2(4), 952–980.

- Qamruzzaman, M., & Jianguo, W. (2018b). Nexus between financial innovation and economic growth in South Asia: Evidence from ARDL and nonlinear ARDL approaches. Financial Innovation, 4(1), 1–19. https://doi.org/10.1186/s40854-018-0103-3

- Qamruzzaman, M., & Wei, J. (2019). Financial innovation and financial inclusion nexus in South Asian countries: Evidence from symmetric and asymmetric panel investigation. International Journal of Financial Studies, 7(4), 61. https://doi.org/10.3390/ijfs7040061

- Ram, R. (1999). Financial development and economic growth: Additional evidence. The Journal of Development Studies, 164–174. https://doi.org/10.1080/00220389908422585

- Rishi, P. (2022). Frugality and Innovation for Sustainability. In Managing Climate Change and Sustainability through Behavioural Transformation (pp. 79–104). Palgrave Macmillan Singapore.

- Robeena Bibi, S. (2020). The effect of Foreign direct investment and financial development on economic growth: Evidence from global income countries. Journal of Environmental Science and Economics. https://doi.org/10.56556/jescae.v1i1.5

- Rzepka, A. (2019). Innovation, inter-organizational relation, and co-operation between enterprises in Podkarpacie region in Poland. Procedia Manufacturing, 30, 642–649. https://doi.org/10.1016/j.promfg.2019.02.091

- Schoemaker, P. J., Heaton, S., & Teece, D. (2018). Innovation, dynamic capabilities, and leadership. California Management Review, 61(1), 15–42. https://doi.org/10.1177/0008125618790246

- Schumpeter, J., & Backhaus, U. (2003). The theory of economic development. In Joseph Alois Schumpeter (pp. 61–116 doi:10.1007/0-306-48082-4_3). Springer, Boston, MA.

- Sekhar, S., & Gudimetla, V. (2013). Theorems and theories of financial innovation: Models and mechanism perspective. Financial and Quantitative Analysis. FQA, 1(2), 26–29. https://doi.org/10.12966/fqa.05.02.2013

- Shao, S., Hu, Z., Cao, J., Yang, L., & Guan, D. (2020). Environmental regulation and enterprise innovation: A review. Business Strategy and the Environment, 29(3), 1465–1478. https://doi.org/10.1002/bse.2446

- Sharma, A. (2016). Unified payments interface: The recent Indian financial innovation demystified. Apeejay Journal of Management & Technology, 11(2), 17–27. https://doi.org/10.29385/APEEJAY.11.2.2016.21-33

- Simiyu, R. S., Ndiang’ui, P. N., & Ngugi, C. C. (2014). Effect of financial innovations and operationalization on market size in commercial banks: A case study of Equity Bank, Eldoret branch. International Journal of Business and Social Science, 5, 8.

- Sotiropoulou, T., & Giakoumatos, S. G. (2019). Financial development, financial stability and economic growth in European Union: A panel data approach. 9(3), 55–69.

- Soumitra, D., Lanvin, B., & Wunsch-Vincent, S. (Eds.). (2020). Global innovation index 2020: who will finance innovation?. WIPO.

- Soyode, A. (1990). The Role of Capital in Economic Development. Security Market Journal Nigeria, 6.

- Stiglitz, J. E. (2010, February-March). Financial Innovation Boosts Economic Growth. The Economist.

- Stulz, R. M. (2019). FinTech, bigtech, and the future of banks. Journal of Applied Corporate Finance, 31(4), 86–97. https://doi.org/10.1111/jacf.12378

- Tufano, P. (2003). Financial innovation. Handbook of the Economics of Finance, 1, 307–335.

- Ujunwa, A. I., Ujunwa, A., Onah, E., Nwonye, N. G., & Chukwunwike, O. D. (2021). Extending the determinants of currency substitution in Nigeria: Any role for financial innovation? South African Journal of Economics, 89(4), 590–607. https://doi.org/10.1111/saje.12300

- Usman, M., Kousar, R., Makhdum, M. S. A., Yaseen, M. R., & Nadeem, A. M. (2022). Do fnancial development, economic growth, energy consumption, and trade openness contribute to increase carbon emission in Pakistan? An insight based on ARDL bound testing approach. In Environment, Development and Sustainability (pp. 1–30). https://doi.org/10.1007/s10668-021-02062-z

- Van de Ven, A. H. (1986). Central problems in the management of innovation. Management Science, 32(5), 590–607. https://doi.org/10.1287/mnsc.32.5.590

- Wachter, J. A. (2006). A consumption-based model of the term structure of interest rates. Journal of Financial Economics, 79(2), 365–399. https://doi.org/10.1016/j.jfineco.2005.02.004

- World Bank Country and Lending Groups – World Bank Data Help Desk. (2022). THE WORLD BANK. Retrieved March 2022https://datahelpdesk.worldbank.org/knowledgebase/articles/906519-world-bank-country-and-lending-groups (i don’t know what to do in this)

- World Economic Forum. 2012. “The Financial Development Report 2012.” Geneva, Switzerland, New York, USA. www3.weforum.org/docs/WEF_FinancialDevelopmentReport_2012.pdf

- Wu, C.-F., Huang, S.-C., Chang, T., Chiou, -C.-C., & Hsueh, H.-P. (2020). The nexus of financial development and economic growth across major Asian economies: Evidence from bootstrap ARDL testing and machine learning approach. Journal of Computational and Applied Mathematics, 372, 112660. https://doi.org/10.1016/j.cam.2019.112660

- Xiong, A., Xia, S., Ye, Z. P., Cao, D., Jing, Y., & Li, H. (2020). Can innovation really bring economic growth? The role of social filter in China. Structural Change and Economic Dynamics, 53, 50–61. https://doi.org/10.1016/j.strueco.2020.01.003

- Yakubu, I. N., & Abdallah, I. (2021). Modelling the financial intermediation function of banks and economic growth in sub-Saharan Africa. Journal of Money and Business, 1(1), 1–7. https://doi.org/10.1108/jmb-04-2021-0005