?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

The study examines the stability of Indonesian Islamic Commercial Bank (ICB) and Islamic Rural Bank (IRB) by employing a Markov Switching Dynamic model of two regimes, stable (tranquil) and unstable (crisis). This study utilizes monthly data between December 2007 and April 2022. Findings show that both ICB and IRB have greater probabilities of remaining in the tranquil regime compared to the period of crisis. Even though ICB Z-scores have a wider range of volatility than IRB Z-scores, the ICB has been shown to recover from crises faster than the IRB. The differences in characteristics between ICB and IRB, as well as swings in the Z-score, do not provide resilience benefits. Thus, both ICB and IRB are equally vulnerable to the crisis. This study’s findings could be used to generate policy for the relevant stakeholders of Islamic banking industries.

JEL Classification:

Public Interest Statement

The stability of the Islamic banking sector contributes significantly to economic expansion. The presence of this sector enables users of financial services to utilize services that adhere to sharia corridors and regulations. A systemic failure of the Islamic banking sector is capable of causing economic failure; consequently, it is necessary to have an early warning system that alerts all stakeholders immediately regarding the causes of the failure. Based on two scenarios—the tranquil and crisis—this study provides an overview of the state of Islamic Commercial and Rural Banks. It is essential to determine whether the distinct characteristics of the two banks (in sizes, assets, regulations, and others) have different effects and repercussions on the crisis.

1. Introduction

Indonesia, as the country with the world’s largest Muslim population, has promising prospects for the development of the Islamic banking industry. According to the Islamic Bank Statistics of the Financial Services Authority (OJK), Islamic banking assets reached IDR 669,006 billion in April 2022, a 12.6% increase over the previous year’s total asset of IDR 593,977 billion. A rising trend can also be seen in net profit; in April 2021, Syariah banking recorded a net profit of 3,350 billion rupiah. This net profit increased by 3,461 billion rupiah, or 3.31%, in April 2022, even during the economic recovery period after the recession caused by Covid-19. The banking sector continues to dominate the structure of the Indonesian financial system. This demonstrates that the banking sector has a significant impact on the stability of the financial system and economic growth. The significant role of Islamic banking to support growth has been documented by many studies including Boukhatem and Ben Moussa (Citation2018), Ledhem and Mekidiche (Citation2022) and Masrizal & Trianto (Citation2022).

The collapse of the banking system can have catastrophic consequences for economic stability. The banking crisis of 1998 and the global financial crisis of 2008 demonstrated the perilous consequences of a financial system crisis. A crisis is essentially a phenomenon that can lead to the collapse of a nation. In extreme cases, crises can cause “irrational” panic. Several studies, including Papanikolaou (Citation2018) have emphasized the significance of early anticipating banking crises. Due to the explosion of public debt, the effort to rescue troubled banks has doubled the impact of bank failure in many economies. Therefore, it is essential to create an early warning system for banking crises. Martin (Citation1977), Meyer and Pifer (Citation1970), and Sinkey (Citation1975) are among the earliest studies to investigate bank failure and establish early warning systems in banking. Tanaka et al. (Citation2016) and Nurfalah et al. (Citation2018) believe that studies on early warnings are particularly valuable for predicting vulnerability to financial crises and might be used to construct a trustworthy financial safety net.

According to Indonesian Law no 21 of 2008 concerning Syariah Banks, there are two types of sharia banks in Indonesia: Islamic Commercial Banks (ICB) and Islamic Rural Banks (IRB), with the fundamental difference being that IRB are barred from collecting demand deposits and providing payment system services. Another notable distinction is that an IRB cannot engage in foreign currency transactions and must be owned by an Indonesian citizen or an Indonesian legal entity. For its establishment, an ICB requires a minimum capital of IDR 3 trillion, whereas an IRB requires a lower capital, namely IDR 5 billion for the operational area of Jakarta, IDR 2 billion for the operational area of the provincial capital on the islands of Java and Bali, IDR 1 billion for operational areas of the provincial capitals outside the islands of Java and Bali, and IDR 500 million for other operational areas. ICB’s large capital allows it to provide various forms of financing for both corporate and individual consumers. Meanwhile, IRB typically focuses on small and micro-scale financing (POJK 66/2016 of the Financial Services Authority (OJK) and provides further information on the comparison of ICB and IRB).

Several studies have been conducted in the Indonesian context to examine the stability and vulnerability of Islamic banks. Wiranatakusuma and Duasa (Citation2017) construct a measurement of Islamic banking’s vulnerability to the crisis and analyze the impact of macroeconomic factors on Islamic banking’s resilience in Indonesia to provide information regarding early warnings. The Markov Switching approach is used by Nurfalah et al. (Citation2018) to compare the stability of Islamic and conventional banking. The Z-score is applied as the proxy for bank stability and the findings show that Islamic banking was more stable than conventional banking from a period of 2004 to 2017. Nurfalah and Rusydiana (Citation2021) expanded on the previous research by comparing the stability of Islamic banking in countries with dual banking system, Indonesia, Malaysia, and Pakistan. When compared to the other two countries, Islamic banking in Malaysia has the best (most stable) performance. Further, the variables that have the greatest influence on the stability model of Islamic banking vary by country. Comparing the performance of Islamic commercial banks to that of rural banks is still not a major concern. Given that these two types of Islamic banking have distinct characteristics, it is in fact worthwhile to conduct additional research.

This study formulates several objectives. The first objective is to use the Markov Switching approach to find early signs of the financial crisis in Islamic Commercial Banks (ICB) and Islamic Rural Banks (IRB). The second goal is to use the Markov Switching method to discover which Islamic banks (ICB and IRB) have the longest duration of crisis, and the last goal is to determine which Islamic banks (ICB and IRB) have superior resilience in the face of crisis. This study calculated the Z-Score (a proxy for banking stability or risk of failure) and analyzes it with the Markov Switching approach to address numerous research objectives. Markov Switching model interprets the tendency and the duration of the crisis period based on the likelihood of the transition period. According to Padhan and Prabheesh (Citation2019), the advantages of the Markov Switching model in developing an Early Warning System are, first, the ability to detect a crisis period through regime probability, allowing regime consistency to be analyzed. A two-regime approach was used in this study, namely the stable regime and the unstable regime (crisis). Second, the Markov Switching Model approach can predict the duration of a potential regime period. Furthermore, Markov Switching enables the development of empirical models capable of detecting contagion phenomena and asymmetric effects in various regimes.

This study builds upon Simorangkir (Citation2012), Nurfalah et al. (Citation2018), and Nurfalah and Rusydiana (Citation2021) and is one of the first attempts to compare the stability of the ICB and the IRB. A comprehensive study is needed to analyze the different types of Islamic banks, namely ICB and IRB, in establishing a comprehensive early warning system framework for Islamic banking. Since they both have distinct characteristics, a partial analysis is required to distinguish factors that significantly influence Islamic banking stability in two distinct regimes, namely the period of stability and the period of instability or crisis. It is expected that the results of this study will provide relevant stakeholders with an overview of the factors affecting the stability of Islamic banking, particularly during the crisis, so that a system of decent banking governance can be developed.

2. Literature review

2.1. The Islamic banking industry and financial stability

The Islamic banking industry plays an important role in a country’s economic prosperity, driving the wheels of the economy and facilitating growth (Boukhatem & Ben Moussa, Citation2018; Ledhem & Mekidiche, Citation2022; Masrizal et al., Citation2022). This is due to its function as a fund channeling institution. According to Law no 21 of 2008, Sharia (Islamic) banking is the practice of conducting business in accordance with the Sharia, economic democracy, and prudential principles. The goal of Sharia (Islamic) banking is to aid in the implementation of national development by improving justice, cooperation, and the equitable distribution of people’s welfare. There are numerous distinctions between conventional and Islamic banks. First, the business model of Islamic Banks is invested in halal businesses, whereas conventional banks adhere to value-free investments (does not differentiate between what is halal/permissible and what is haram/impermissible according to sharia). Sharia Bank is a bank that conducts business in accordance with sharia principles, or Islamic legal principles regulated in the fatwa of the Indonesian Ulema Council, such as the principles of justice and balance (‘adl wa tawazun), benefit (maslahah), universalism (alamiyah), and does not contain uncertainty (gharar), gambling (maysir), interest or usury, unjust and unlawful objects. Second, Islamic banks operate on a profit-sharing model in which the amount of profit-sharing varies based on business performance. In contrast, conventional banks operate with a fixed interest rate system (both profits intended for providers of funds and capital costs borne by users of capital). Thirdly, Islamic banks are profit-driven and focused on falah, which is happiness in both this world and the next. Meanwhile, conventional banks are solely motivated by profit. Fourth, the relationship between customers and Islamic financial institutions resembles a partnership. While in conventional banks, the relationship between debtors and creditors exists. Lastly, Islamic banks have a Sharia Supervisory Board whose responsibility is to ensure that all bank operations comply with shariah. However, no such institution exists in conventional banks. In addition, the Sharia Banking Law also mandates Islamic banks to carry out social functions, namely receiving funds from zakat, infaq, alms, grants, or other Islamic social funds.

Financial system stability, as defined by Bank Indonesia Regulation No. 16/11/2014 on macro prudential regulation and supervision, is a condition that enables the national financial system to function effectively and efficiently while also being able to withstand internal and external vulnerabilities, allowing the allocation of funding sources or financing to contribute to growth and stability. A stable financial system can encourage investment and economic growth by expanding and improving the financial intermediation function.

2.2. Bank crisis and “too big to fail” hypothesis

The presence of larger banks, according to the “too big to fail” hypothesis, makes the banking system more vulnerable and exposed to unfavorable shocks. Furthermore, agency issues are more common in large and well-diversified banks, consequently, leading to systematic risk increases (Ibrahim & Rizvi, Citation2017). It may be worsened by the existence of deposit insurance and lender of last resort mechanism. On the one hand, deposit insurance protects depositors from losses caused by a bank’s inability to pay its debts and, thus, reduces bank risk by preventing a bank run and the spread of financial panic (Gropp & Vesala, Citation2004). On the other hand, deposit insurance may reduce market discipline, leading to moral hazard and excessive bank risk taking (Acharya, Citation2009; Demirgüç-Kunt & Huizinga, Citation2004; Ioannidou & Penas, Citation2010). Moutsianas and Kosmidou (Citation2016) argue that large banks with “too big to fail” status played a role in the recent global financial crisis and that stricter requirements should be imposed on them, or that they should be converted into small banks. Banks, on the other hand, can take advantage of economies of scale by growing (in size), resulting in more efficient intermediation, better monitoring, and lower prices (Beccalli et al., Citation2015). Adusei’s and Elliott (Citation2015) study of the rural banking industry in Ghana demonstrates that a bank’s stability increases as its size increases.

There exists a continuing argument about whether Islamic banks with bigger sizes will be more resilient during times of crisis. The study conducted on 45 Islamic banks in 13 countries by Ibrahim and Rizvi (Citation2017) concludes that large Islamic banks, at least when they have reached certain threshold, are more stable comparing to small Islamic banks. This finding opposes Alqahtani and Mayes (Citation2018) who used stability measurements and an accounting-based market to assess 76 Gulf Cooperation Council (GCC) banks and conclude that a small Islamic banking size has higher probability to survive during a crisis period, rather than a larger one. Similar findings were found by Čihák and Hesse (Citation2008) who discovered that small Islamic banks tend to be financially stronger than large Islamic banks, which may be a reflection of higher credit risk exposure in larger Islamic banks.

2.3. Early warning system in financial industry

Companies require an early warning system (EWS) to detect early and measurable (based on comprehensive risk modeling) the emergence of a risk that has the potential to cause a corporate disaster (catastrophe). EWS enables businesses to take preventative measures in a timely manner that can prevent or avert company failure or fatal losses. EWS is also useful for monitoring the achievement of various company objectives and target key performance indicators (KPI) by employing several early indicators to detect potential significant deviations in the success-influencing factors. The urgency of early warning system to anticipate the occurrences of crisis has been highlighted by many scholars including Papanikolaou (Citation2018), Martin (Citation1977), Meyer and Pifer (Citation1970), Sinkey (Citation1975), Tanaka et al. (Citation2016), and Nurfalah et al. (Citation2018). Padhan and Prabheesh’s (Citation2019) research calls for the existence of an early warning model that can effectively predict and anticipate crises; consequently, reforms and an agenda are required to develop more effective early warning models. Failure to predict the occurrence of a crisis will have catastrophic consequences for the local and global economies. Samitas et al. (Citation2020)attempted to establish Early Warning Systems (EWS) by analyzing potential contagion risks based on structured financial networks. Alshater et al. (Citation2022) attempted to establish EWS for the high-volatility energy industry by employing artificial intelligence and market learning. The EWS aims to stabilize market swings in an uncertain context (such as the Russian invasion of Ukraine) and leverage the capacity to control operating costs and pave the way for a smooth economic recovery.

It is necessary to conduct additional research to look into the different characteristics of Islamic banks on their stability. In the Indonesian context, the difference between ICB and IRB can be optimized to further investigate the impact of different characteristics on banking stability, as the ICB is generally larger (in terms of asset size, capital, and disbursed financing) than the IRB.

3. Research method

There have been times when the behavior of the financial industry, and banking in particular, appears to have changed significantly. Their susceptibility to such unforeseen shocks (i.e. 1997 Asian Financial Crisis and 2008 global financial crisis) can drastically alter the profitability of the banking business, particularly the Islamic banking industry, which has a far smaller market share than its conventional equivalents and so cannot benefit from economies of scale as their conventional counterparts do. All of these eras necessitate the utilization of regime-switching models. Several requirements have been recommended in the literature. Depending on the regimes, the appropriate model class must be chosen. Due to their leaps (spike regime) and base regime, the literature frequently employs regime-switching techniques for the banking sector. For example, two Markov regimes are used to discriminate between stable and explosive phases; that is, regimes of “risky” and “stable” energy market as described by Huang et al. (2011). Nurfalah et al. (Citation2018) and Nurfalah and Rusydiana (Citation2021) also employ two Markov regimes of quiet (tranquil) and crisis, and stable and unstable periods to characterize the Islamic banking regimes.

The Markov-Switching (MS) Autoregressive models are utilized extensively to capture the behavior of regime transitions. Beginning with Hamilton’s (1989, 1990) research, the MS time series models define particular characteristics of the business cycle. This econometric framework is utilized to model the fluctuation behavior of economic variables. The MS model can detect shifts in returns, quantify durations in each state, and aid in measuring the correlations between parameter movements in each state. The purpose of a regime-switching model is to account for distinct behavior in distinct states of nature while concurrently calculating the time of transition between states. The basic equations of MS are as follows:

Where is the dependent variable,

is a state-dependent intercept (intercept that changes with the regime),

is a vector of exogenous variables with state-invariant coefficients (coefficients that do not change with the regime),

is a vector of exogenous variables with state-dependent coefficients (coefficients that do not change with the regime), and

is an independent error and normally distributed.

In order to achieve the aims of the study, the Markov Switching Dynamic Regression Model is utilized (MSDR). MSDR models allow quick adjustment following a process state change. These models are frequently applied to monthly and higher-frequency data (Galyfianakis et al., Citation2016). This method employs a latent variable that follows the first derivative from two-stage Markov, namely {St} where St = 1 is a state of regime and St = 0 is another state of regime. This state can be periods of stable, tranquil or growth and risky or unstable. Although St is not directly observed in this model, the behavior of the dependent variable Yt is independent of St, as stated below:

The two regimes in this study are explained as follows. Regime 0 represents a stable or tranquil regime, while regime 1 represents an unstable regime, with the more unstable regime indicating a greater likelihood of a crisis and bank bankruptcy. The accuracy of model predictions depends on the specification and use of time varying parameters. The process of forming the probability regime is usually described by the movement of the variables. In this banking stability model, constant and variance are involved in the process of forming a regime. Therefore, this model will detect a crisis if there is a significant change, shocks, or vibration of the Z-score.

The dependent variable Yt is used as an early warning indicator of Islamic bank failure and is the Z-Score. This study utilizes the Z-score as calculated by Čihák and Hesse (Citation2008). The Z-score is derived by adding Return on Earnings (ROA) and Shareholder Equity Ratio (SER) divided by the standard deviation of ROA. The MSDR equation utilized in this investigation is shown in Equation 3 and 4. There are four equations since it employs two regimes (2 for ICB and 2 IRB). The lag has been omitted from the equations for simplicity. Lag 1 has been selected, the choice of lag is based on the results of the optimal lag test.

The MSDR assumption employed in this model is switching variance, as the occurrence of Z-Score fluctuations in some crisis times (high-volatility state) cannot be equated with Z-Score fluctuations in the ordinary period (low-volatility state). MSDR suggests a crisis when there is a substantial shift in Z-score fluctuation (through variance), in other word, MSDR uses variance to establish the probability regime.

This study employs monthly data from December 2007 through April 2022 of Islamic Commercial Banks (ICB) and Islamic Rural Banks (IRB), see Appendix 1 and 2 for an overview of ICB and IRB. The study examines seven variables which include Z-Score (as a measure of financial institution stability), external factors such as Bank Indonesia Rate (BI Rate) and Inflation, and internal factors such as Assets, Non-Performing Financing (NPF), Financing to Deposit Ratio (FDR), and Capital Adequacy Ratio (CAR). Monthly data on the Bank Indonesia 7 days repo rate (BI Rate) variable is obtained from Bank Indonesia’s official website, while monthly inflation data is obtained from Indonesian Statistics (Badan Pusat Statistik/BPS) using the Consumer Price Index approach. The internal variable data is derived from publicly available Islamic banking statistics from the Financial Services Authority (Otoritas Jasa Keuangan/OJK), see, Table . Oxmetric was used to execute the Markov Switch model, whereas Stata was employed for differential statistics.

Table 1. Summary of variable

4. Result and analysis

4.1. Movement and trend of Z-scores

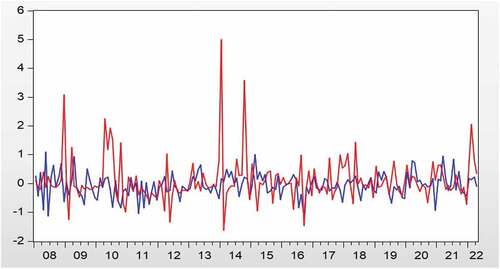

Figure depicts the Z-score for Islamic Commercial Banks (ICB) and Islamic Rural Banks (IRB) from December 2007 to April 2022. Z-score fluctuations for the IRB appear to be more volatile than Z-score fluctuations for the IRB, which are more stable. The Z-score of ICB is found to have higher standard deviation than IRB. Further, the IRB’s Z-score (with an average score of 30.60) outperforms the ICB’s Z-score (with an average score of 15.97). The higher average Z-score on the IRB can be explained by the higher level of profitability. First, the IRB provides the majority of credit to the Small and Medium-Sized Enterprises (SME) sector, with a higher profit-sharing rate than commercial banks. Microfinancing entails a greater risk; consequently, a higher expected rate of return is required. Second, Bank Indonesia (BI) regulations do not govern the determination of profit sharing for IRB. In the absence of such regulation, IRB is able to offer margins that are frequently higher than the benchmark interest rate of Bank Indonesia. In addition, because IRBs typically acquire savings and provide direct financing to consumers, their overhead expenses are relatively high, as more employees are required to provide individualized service. This also increases monitoring costs.

Figure 1. Z-score of ICB (Red Line) and IRB (Blue Line) (Source: Authors’ calculation).

The ICB Z-score of this model is higher than those obtained by Nurfalah et al. (Citation2018) and Nurfalah and Rusydiana (Citation2021). This is because the period utilized in this model is longer and includes extreme events such as the global financial crisis of 2008. Upon closer inspection, there were outliers or extreme events for ICB during the observation period; see, Table for descriptive statistics. A statistical differentiation test will be carried out to find out the statistical difference between the Z-scores on the ICB and IRB (see, Table ).

Table 2. Descriptive statistics

Table 3. Differential statistics of Z-score

The t statistics of the differentiation test between Z-score ICB and IRB are less than its critical values. This indicates that there is sufficient evidence to reject the null hypothesis stating that the average Z-score ICB and IRB are identical and to accept the alternative hypothesis stating that the average Z scores are not identical; therefore, there is a difference between the Z-scores of ICB and IRB.

4.2. Analysis of the estimated model

Table displays the coefficients of each variable that affect the Z-score of the ICB and IRB in two periods, regimes 0 and 1. When the value of constant regime 0 exceeds the value of constant regime 1, it indicates that regime 0 is a period of stability or tranquil, whereas regime 1 is a period of instability or crisis.

Table 4. Coefficient of ICB and IRB (Markov switching—dynamic regression)

In different regimes, the benchmark interest rate (BI 7-days repo rate) has different effects on the stability of the ICB and IRB. In theory, increasing interest rates during stable and crisis periods makes investors and business owners reluctant to seek bank financing. The interest rate represents the cost of obtaining capital; consequently, higher interest rates result in higher overall costs for obtaining capital. Thus, reducing the demand for capital. Nonetheless, there is an unusual aspect to the positive link between the BI Rate and the Z-score, and that aspect is the fact that a rise in the BI rate is positively correlated with an increase in Islamic banking stability. This may be explained by the fact that profit-sharing rates (nisbah) in Islamic banking move in tandem with interest rates. Higher interest rates will raise the expected profit sharing of Islamic banks. Moreover, according to the theory of money demand, higher interest rates encourage individuals to save their money in banks, hence strengthening the capital buffer of banks.

Although interest rates are not considered in Islamic banking operations, the profit-sharing ratio used in Islamic banking is heavily influenced by the market interest rate. A majority of Islamic banks utilize interest-based benchmarks as a pricing reference, due in part to the lack of independent, stable, and widely published alternatives. This is because Islamic banking does not want to set excessive profit-sharing margins, which would make them less competitive with conventional banks. In addition, currently, Islamic banks use various interest-based benchmark rates to determine their cost of funds and, as a result, the prices of their financing products, such as the London Interbank Offered Rate (LIBOR), the Kuala Lumpur Interbank Offered Rate (KLIBOR), the Karachi Interbank Offered Rate (KIBOR), and the Cost of Funds Index (COFI), among others (Ahmed et al., Citation2018; Archer & Abdel Karim, Citation2019; Ghauri, Citation2015; Nouman et al., Citation2022).

In theory, it is expected that inflation will have a negative impact on the stability of Islamic banking. High inflation diminishes people’s purchasing power by increasing the cost of acquiring goods and services; hence, when inflation is high, people become reluctant to seek for sources of funds, one of which from Islamic banks.

Assets influence the stability of Islamic banks. Z-scores are influenced negatively by assets. This demonstrates that increasing asset value reduces its stability. Increasing assets is not a recommended strategy, especially during a crisis. The cost of acquiring assets will reduce banks’ efficiency in managing their funds, reducing their stability.

The Capital Adequacy Ratio (CAR) demonstrates a bank’s ability to provide funds that can be used as reserves to anticipate loss. Higher CAR indicates that the bank can finance operational activities while contributing significantly to profitability. Increasing CAR can improve customer security and, as a result, customer confidence in the bank, which can help increase bank profitability. CAR has a significant positive relationship with the stability of ICB in the crisis period (regime 1) and a significant positive relationship in the stable period (regime 0) for IRB. One of the strategies implemented during the growth period is to increase CAR as a capital buffer in the face of future crisis cycles so that an increase in CAR will increase the stability of Islamic banking. The importance of capital as buffers is also highlighted by Daher et al. (Citation2015) for risk mitigation of Islamic banking. This logic also applies in times of crisis.

Financing to Deposit Ratio (FDR) compares the amount of financing provided to the amount of funds and capital owned or used. Higher FDR indicates that a bank is liquid. This implies that the bank has many idle funds and fails to function as a financial intermediary. During unstable periods, higher FDR and liquidity lead to a decrease in the bank’s stability. To compare, FDR has a substantial positive effect on the IRB’s Z-score during tranquil times. This suggests that higher idle funds and liquidity will enhance the IRB’s stability during a crisis.

Further examination reveals that the average FDR of ICB is low. In contrast, it is very high, exceeding 100% at the IRB, indicating that all deposits have been made for financing purposes. At ICB, the deposit is not used entirely to provide financing. This also implies that deposits are used to create diversification.

Non-Performing Financing (NPF) is one indicator of the health of bank asset quality. The inability of the customer to pay the principal installments and profit sharing (margin) of financing affects its collectability. Increased NPF heightens the possibility of a decline in profitability and stability. The effect of NPF on ICB and IRB stability is different in each regime. The increase in NPF is responded positively to the increase in the Z-score.

4.3. Regime transition and differential statistics between regimes

Table provides an overview of the Markov Switching—Dynamic Regression model’s regime transition matrix for the ICB. The probability of ICB remaining in a Stable Regime (regime 0) when it was also in a Stable Regime one period ago is 69.29%. Meanwhile, the probability of ICB surviving in an Unstable Regime when last month was also in an Unstable Regime is 61.21%. The likelihood that ICB will shift to the stable period (regime 0) when the previous month was an unstable regime (regime 1) is 38.79%. Further, the probability that ICB will shift to a crisis period (regime 1) when last month was a stable regime (regime 0) is 30.71%.

Table 5. ICB regime transition probabilities

Table provides an overview of the regime transition matrix on the IRB. The probability of IRB surviving in the stable period (regime 0), assuming it was also in a Stable Regime one period ago, is 78.82%. Meanwhile, the probability of IRB staying in a crisis (regime 1), assuming that last month was also in an Unstable Regime, is 74.78%. The possibility of transition in IRB from tranquil (regime 0) to crisis (regime 1) is 21.19%. On the other hand, the transition probability for IRB from regime 1 to regime 0 is 25.23%.

Table 6. IRB Regime Transition Probabilities

Further analysis reveals that ICB, and IRB are more likely to remain in the stable period (regime 0) than in a crisis, with a more significant probability of staying in the stable phase. In addition, for ICB and IRB, the transition from regime 0 to regime 1 is less than the transition from regime 1 to regime 0. This suggests that the chance of declining (toward a crisis) is smaller than the probability of recovering (from a crisis) or, alternatively, that the likelihood of recovering (from a crisis) is greater than the probability of falling (toward a crisis). Moreover, both ICB and IRB have an unpredictable cycle between regimes in which regime 1 (unstable period) and regime 0 (stable period) have a nearly identical probability. Therefore, policymakers should investigate more precisely the indicators that trigger the crisis for both Islamic banks.

Moreover, this study examines the level of difference in Z scores in each period by applying a two-sample t-test with unequal variances (using ttest sgr and ttest sdp functions); this test is applied to determine the probability of an increase in Z-score during tranquil (regime 0) and a decrease in Z-score during a crisis (regime 1). Table gives the results of Regime 0 differential statistics, where there is a 55.98% possibility of an increase in ICB Z-score in the stable period (Regime 0). At the same time, there is a 54.40% possibility of an increase in IRB Z-score in Regime 0. Further inspection reveals that the probability of the Difference Test of Stable Regime between ICB and IRB is greater than 5%, indicating that Regime 0 probabilities for ICB and IRB are not statistically different.

Table 7. Regime 0 differential Statistics

Table displays the results of Regime 1 differential statistics, which indicate a 44.02% probability that the ICB Z-score will decrease during the crisis (Regime 1). At the same time, there is a 45.6% chance that the IRB Z-score will drop in the same regime. Further review indicates that the probability of the Difference Test of Crisis Regime between ICB and IRB is greater than 5%, meaning that ICB and IRB have a Regime 1 probabilities that are not statistically different.

Table 8. Regime 1 differential Statistics

Despite different behavior and trend of Z-Scores for ICB and IRB, both Z-scores have nearly equal probabilities of tranquil and crisis events, with the IRB being more consistent than the ICB in crisis. The differences in characteristics between ICB and IRB and fluctuation in Z-Score do not provide resilience benefits. Both are equally vulnerable to the crisis and have nearly identical growth prospects.

4.4. Regime period

One of the benefits of using the Markov Switching method is the ability to predict economic cycle changes, such as recession, boom, or crisis. In addition, this method can estimate the durations of the periods of stable and crisis (instability period) described by regimes 0 and 1, respectively. The analysis of ICB and IRB will provide the idea of which bank models have high duration and probability during a period of stability and crisis. Estimating the stable and crisis periods for both models was based on the adaptation of the research variables.

After observing 171 months, the model observed 106 months of ICB in a stable period (Regime 0), with a probability of 16.99% and an average length of 3.66 months. Comparatively, the result revealed 65 months of observations in an unstable period (Regime 1), with a probability of 38.01% and an average duration of 2.24 months (see, Table ).

Table 9. Regime Period for ICB

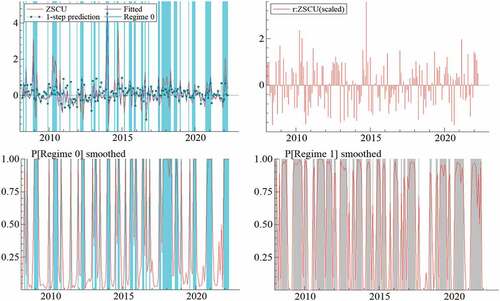

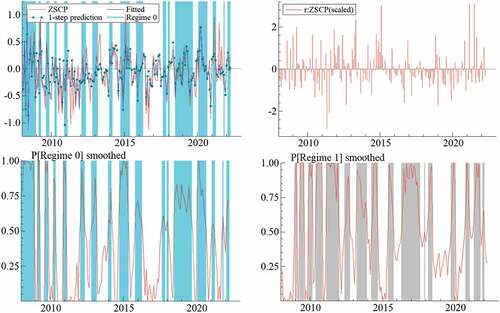

The average duration of IRB in Regime 0 is 5.56 months, with a probability of 52.05%, 89 months were observed in stable period. In comparison, the average duration in Regime 1 (state of instability) is 4.82 months, with 82 months observed to be in a volatility period and a probability of 47.95% (see, Table ). The finding suggests that the IRB has a more extended period of stability and remains in an unstable condition for longer than the ICB. Upon closer inspection, the ICB rebounds from crises more quickly than the IRB. The risk of a crisis arising in ICB is just 38.01%, with a duration of only 2.24 months, after which it will return to stability. On the other hand, IRB has a crisis likelihood higher than 47% and requires around 4.82 months to recover. Although IRB has a longer average duration than ICB, the possibility of being in a stable period (Regime 0) is more significant for ICB than IRB. Figure depicts the regime transition for ICB, while Figure depicts the IRB regime transition. The highlighted area represents a period with high fluctuations, or an unstable period (regime 1), whereas the area that is not highlighted represents a period of stability (regime 0). These two figures show a significant difference of fluctuation of Z-scores. The ICB Z-scores are found to have higher volatility range than IRB. In the event of financial shocks, the ICB is more likely to incur greater losses than the IRB. ICBs are typically larger in size than IRB, thus, “too big to fail” hypothesis is a logic explanation why ICB Z-Scores have a greater variance in volatility than IRB Z-Scores. Despite ICB’s large fluctuation range, IRB exhibits more frequent fluctuations. More frequent swings increase the IRB’s susceptibility to fall into unstable regime (crisis).

Figure 2. ICB Regime Transition (Source: Authors’ calculation).

Figure 3. IRB Regime Transition (Source: Authors’ calculation).

Table 10. Regime period for IRB

5. Managerial relevancy

Following the analysis of the findings, several recommendations are proposed. The government is expected to support the development of Islamic banking in Indonesia. This assistance can be provided by establishing development strategies and economic policies that take into account the crisis in the sharia banking industry, allowing for the formation of an early warning system. Despite the fact that Islamic banking still has a small market share in comparison to its conventional bank competitors, the failure of Islamic banks has the potential to create systemic risk and cause the financial industry to collapse. The wide fluctuation range of ICB confirms the “too big to fail” view; therefore, the government and related regulators should be more vigilant to the fluctuation on the stability of Islamic banks.

For banking industry, Islamic banking managers can easily monitor banking stability by using the Z-scores approach used in this study (by adding ROA and SER divided by the standard deviation of ROA). This monitoring is necessary so that Islamic banking can respond quickly to shocks or economic disruptions. The sharia banking crisis can be mitigated using this approach. Furthermore, IRB managers must be more vigilant because IRBs have been found to be more sensitive to crises and to recover more slowly. In the event of unstable regimes, several strategies for ensuring IRB sustainability must be developed.

6. Conclusion

This study aims to develop a Markov switching-based early warning system that can be used to analyze the factors that affect banking stability. By employing the Markov Switching Dynamic model, this study seeks to identify the Islamic banks (Islamic Commercial Bank/ICB or Islamic Rural Bank/IRB) that are most susceptible to the crisis and the Islamic banks that are expected to experience rapid recovery after the crisis.

Both ICB and IRB have higher probabilities of remaining in the stability period (regime 0) compared to the crisis period. The results further indicate that the IRB has a lengthier time of falling in instability or crisis state and a longer period of stability than the ICB. Even though ICB Z-scores have a higher volatility range than IRB, the ICB has been observed to recover from crises faster than the IRB.

Several reasons can explain this occurrence. First, the ICB is typically larger than the IRB, allowing it to gain economies of scale in handling financial activities. In contrast, the IRB is smaller in size; therefore, it cannot leverage the potential of economies of scale. Second, ICB’s banking operations are typically more efficient than IRB’s. ICB has a wider variety of financial sources and a cheaper cost of capital than IRB. The structure of third-party funds at ICB is mainly characterized by Time deposits with lengthy maturities; thus, depositors cannot withdraw their money at any moment. Similarly, the financing provided by ICB is diverted towards long-term and high-denomination of financings. ICB also provides current account savings facilities with low-cost capital. IRB, in contrast, manages short-term funding for smaller denominations. The available funding sources are restricted because they are prohibited from offering some saving options, such as current account savings. IRB provides a higher rate of return than ICB. This is because IRB focuses on niche markets and has a small market share or scale. Dispersed finance is more flexible and focuses on microfinancing. This results in a higher rate of return as IRBs are exposed to more risks. Third, the public has greater faith in ICB; therefore, there are fewer concerns about rush money when shocks occur. This is different from the IRB. Due to the tiny size and focus on a niche sector with a smaller market share, consumers have a higher level of skepticism; hence the likelihood of a rush on the IRB will be greater when financial crises arise.

Furthermore, the different behavior and trend of Z-Scores, both ICB and IRB have an unpredictable cycle between regimes, thus making it difficult to forecast future trends. The differences in characteristics between ICB and IRB and fluctuations in Z-score do not provide resilience benefits. Both are equally susceptible to the crisis, and their growth prospects are nearly identical.

7. Limitation and study forward

As for the research limitations, the proposed model was limited to Islamic banking, specifically Islamic commercial and rural banks. The outcome cannot be applied to the entire banking industry. This is due to Islamic banks’ small market share in comparison to their conventional counterparts. During the last decade, Islamic banks’ market share cannot exceed 7% of the total banking market. As a result, the model may differ if used to examine the conventional banks. The recommendation for future research is to conduct a more in-depth comparison of factors and regimes in conventional and Islamic banks. Such research is deemed critical in order to develop a more comprehensive early warning system for the Indonesian banking industry. This recommendation was made because it is possible to capture the phenomenon and produce a quality analysis by employing Markov Switching model.

Further reading

(1) Law Number 21 of 2008 concerning IslamicBanking

(2) POJK 66/2016 of the Financial Services Authority(OJK)

(3) Bank Indonesia Regulation No. 16/11/2014 on macro prudential regulation and supervision.

(4) Data of Islamic Bank Statistics from the officialwebsite of OJK

Acknowledgements

The researcher would like to acknowledge the Research and Community Service Institution (LPPM) of Universitas Airlangga for supporting this study. The authors would also like to commend Mr Muhammad Shalhan Assalam, Mr Dzikri Nurrohman and Miss. Nuria Latifah for their support with data collection and processing.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

Notes on contributors

Imron Mawardi

Imron Mawardi is an associate professor at Universitas Airlangga’s Faculty of Economics and Business. Islamic Finance, Banking, and Microfinance are areas of research interest for him. He is currently the vice dean of the Faculty of Advanced Technology and Multidiscipline.

Muhammad Ubaidillah Al Mustofa

Muhammad Ubaidillah Al Mustofa is a lecturer and researcher at Institut Teknologi Sepuluh Nopember’s Development Studies Department, Faculty of Creative Design and Digital Business. His areas of expertise include Islamic Economics and Finance, as well as Islamic Development Studies.

Tika Widiastuti

Tika Widiastuti is a senior lecturer and researcher at the Universitas Airlangga’s Faculty of Economics and Business. She has a doctorate in Islamic Economics. Her research interests include zakat governance and Islamic economics.

Wahyu Wibisono Wahid

Wahyu Wibisono Wahid Wahid is a doctoral student of Islamic Economics at Universitas Airlangga’s Faculty of Economics and Business.

References

- Acharya, V. V. (2009). A theory of systemic risk and design of prudential bank regulation. Journal of Financial Stability, 5(3), 224–21. https://doi.org/10.1016/j.jfs.2009.02.001

- Adusei, M., & Elliott, C. (2015). The impact of bank size and funding risk on bank stability. Cogent Economics and Finance, 3(1), 1. https://doi.org/10.1080/23322039.2015.1111489

- Ahmed, E. R., Islam, M. A., Alabdullah, T. T. Y., & Bin Amran, A. (2018). Proposed the pricing model as an alternative Islamic benchmark. Benchmarking: An International Journal, 25(8), 2892–2912. https://doi.org/10.1108/BIJ-04-2017-0077

- Alqahtani, F., & Mayes, D. G. (2018). Financial stability of Islamic banking and the global financial crisis: Evidence from the gulf cooperation council. Economic Systems, 42(2), 346–360. https://doi.org/10.1016/j.ecosys.2017.09.001

- Alshater, M. M., Kampouris, I., Marashdeh, H., Atayah, O. F., & Banna, H. (2022). Early warning system to predict energy prices: The role of artificial intelligence and machine learning. Annals of Operations Research. https://doi.org/10.1007/s10479-022-04908-9

- Archer, S., & Abdel Karim, R. A. (2019). When benchmark rates change: The case of Islamic banks. Journal of Financial Regulation and Compliance, 27(2), 197–214. https://doi.org/10.1108/JFRC-11-2017-0104

- Beccalli, E., Anolli, M., & Borello, G. (2015). Are European banks too big? Evidence on economies of scale. Journal of Banking and Finance, 58(January), 232–246. 2014. https://doi.org/10.1016/j.jbankfin.2015.04.014

- Boukhatem, J., & Ben Moussa, F. (2018). The effect of Islamic banks on GDP growth: Some evidence from selected MENA countries. Borsa Istanbul Review, 18(3), 231–247. https://doi.org/10.1016/j.bir.2017.11.004

- Čihák, M., & Hesse, H. (2008). Islamic banks and financial stability: An empirical analysis. In IMF Working Paper WP/08/16. International Monetary Fund. https://doi.org/10.1007/s10693-010-0089-0

- Daher, H., Masih, M., & Ibrahim, M. (2015). The unique risk exposures of Islamic banks’ capital buffers: A dynamic panel data analysis. Journal of International Financial Markets, Institutions and Money, 36, 36–52. https://doi.org/10.1016/j.intfin.2015.02.012

- Demirgüç-Kunt, A., & Huizinga, H. (2004). Market discipline and deposit insurance. Statistics and Probability Letters, 66(4), 375–399. https://doi.org/10.1016/j.jmoneco.2003.04.001

- Galyfianakis, G., Drimbetas, E., & Sariannidis, N. (2016). Modeling Energy Prices with a Markov-Switching dynamic regression model: 2005-2015. Bulletin of Applied Economics, 3(1), 11–28.

- Ghauri, S. M. K. (2015). Why interest-rate cannot benchmark for Islamic financial product pricing? Benchmarking: An International Journal, 22(7), 1417–1428. https://doi.org/10.1108/BIJ-04-2013-0049

- Gropp, R., & Vesala, J. (2004). Deposit insurance, moral hazard and market monitoring. Review of Finance, 8(4), 571–602. https://doi.org/10.1093/rof/8.4.571

- Ibrahim, M. H., & Rizvi, S. A. R. (2017). Do we need bigger Islamic banks? An assessment of bank stability. Journal of Multinational Financial Management, 40, 77–91. https://doi.org/10.1016/j.mulfin.2017.05.002

- Ioannidou, V. P., & Penas, M. F. (2010). Deposit insurance and bank risk-taking: Evidence from internal loan ratings. Journal of Financial Intermediation, 19(1), 95–115. https://doi.org/10.1016/B978-0-12-815859-3.00026-3

- Ledhem, M. A., & Mekidiche, M. (2022). Islamic finance and economic growth: The Turkish experiment. ISRA International Journal of Islamic Finance, 14(1), 4–19. https://doi.org/10.1108/IJIF-12-2020-0255

- Martin, D. (1977March). American finance association a multivariate statistical analysis of the characteristics of problem banks author (s): Joseph F. Sinkey, Jr. Source: The Journal of Finance 1975), pp. 21–36 Published by: Wiley for the Am. Journal of Banking and Finance, 1(3), 249–276, 30(1), . https://doi.org/10.1016/0378-4266(77)90022-X

- Masrizal, Trianto, B., & Masrizal, M. (2022). the role of pls financing on economic growth: Indonesian case. Journal of Islamic Monetary Economics and Finance, 8(1), 49–64. https://doi.org/10.21098/jimf.v8i1.1378

- Meyer, P. A., & Pifer, H. W. (1970). Prediction of bank failures. The Journal of Finance, 25(4), 853–868. https://doi.org/10.1111/j.1540-6261.1970.tb00558.x

- Moutsianas, K. A., & Kosmidou, K. (2016). Bank earnings volatility in the UK: Does size matter? A comparison between commercial and investment banks. Research in International Business and Finance, 38, 137–150. https://doi.org/10.1016/j.ribaf.2016.03.013

- Nouman, M., Hashim, M., Trifan, V. A., Spinu, A. E., Siddiqi, M. F., & Khan, F. U. (2022, July 7). Interest rate volatility and financing of Islamic banks. PLoS ONE, (17), 1–21. https://doi.org/10.1371/journal.pone.0268906

- Nurfalah, I., & Rusydiana, A. S. (2021). the regime switching of cycle instability of Islamic banking and the economy: evidence from Indonesia, Malaysia, and Pakistan. Journal of Islamic Monetary Economics and Finance, 7(2), 233–262. https://doi.org/10.21098/jimf.v7i2.1362

- Nurfalah, I., Rusydiana, A. S., Laila, N., & Cahyono, E. F. (2018). Early warning to banking crises in the dual financial system in Indonesia: The Markov switching approach. JKAU: Islamic Economics, 31(2), 135–156. https://doi.org/10.4197/Islec.31-2.10

- Padhan, R., & Prabheesh, K. P. (2019). Effectiveness of early warning models: A critical review and new agenda for future direction. Buletin Ekonomi Moneter Dan Perbankan, 22(4), 457–484. https://doi.org/10.21098/bemp.v22i4.1188

- Papanikolaou, N. I. (2018). A dual early warning model of bank distress. Economics Letters, 162, 127–130. https://doi.org/10.1016/j.econlet.2017.10.028

- Samitas, A., Kampouris, E., & Kenourgios, D. (2020). Machine learning as an early warning system to predict financial crisis. International Review of Financial Analysis, 71(May), 101507. https://doi.org/10.1016/j.irfa.2020.101507

- Simorangkir, I. (2012). Early warning indicators study of bank Runs in Indonesia: Markov-switching approach. Buletin Ekonomi Moneter Dan Perbankan, 15(1), 3–40. https://doi.org/10.21098/bemp.v15i1.414

- Sinkey, J. F. (1975). A multivariate statistical analysis of the characteristics of problem banks. The Journal of Finance, 30(1), 21–36. https://doi.org/10.1111/j.1540-6261.1975.tb03158.x

- Tanaka, K., Kinkyo, T., & Hamori, S. (2016). Random forests-based early warning system for bank failures. Economics Letters, 148, 118–121. https://doi.org/10.1016/j.econlet.2016.09.024

- Wiranatakusuma, D. B., & Duasa, J. (2017). Building an Early Warning Towards The Resilience of Islamic Banking in Indonesia. Al-Iqtishad: Journal of Islamic Economics, 9(1), 13–32. https://doi.org/10.15408/aiq.v9i1.3881

Appendix 1.

Number of Banks and Offices

Appendix 2.

Brief Data on Indonesian Islamic Banks