?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

This study investigates the impact of economic policy uncertainty (EPU) on foreign remittances and whether it affects them symmetrically or asymmetrically. The ARDL model is employed to examine the short-run and long-run symmetric impact of EPU on foreign remittances, while the NARDL model is utilized to examine the short-run and long-run asymmetric impact of EPU on foreign remittances, using monthly data for the BRIC economies (Brazil, Russia, India, and China). The results indicate that in the short-run, EPU has a positive and significant impact only on the inflows of foreign remittances received in Russia. Additionally, the short-run asymmetric impact of EPU on foreign remittances is found in Russia and India. Meanwhile, the long-run asymmetric impact of EPU on foreign remittances is observed in the BRIC economies. In particular, the results show that the non-linear response of EPU varies among the sampled countries. The findings of this study enhance our understanding of the role of policy uncertainty in overseas remittances. This information would be beneficial for policymakers, migrants, and recipients, as they are directly involved in making decisions about policies and the transfer of remittances, respectively.

PUBLIC INTEREST STATEMENT

This research is of interest to the general public as it sheds light on the factors that affect the flow of money from individuals living abroad to their home countries. The results of this study can provide important insights for policymakers and international organizations, as well as for individuals and families who rely on foreign remittances as a source of income. Understanding the impact of economic policy uncertainty on foreign remittances can also inform discussions around immigration policies, economic uncertainty, and international economic cooperation.

1. Introduction

Uncertainty has been a topic of interest in the field of finance since 1997, with numerous events in academia and media drawing attention to its importance. Despite the significance of uncertainty, there is still a lack of a widely accepted definition in the literature, leading to diverse interpretations and approaches (Galbraith, Citation1977). This study focuses on economic uncertainty, which refers to unexpected changes in the economic system and the risk posed by unclear future legislative initiatives and regulatory schemes, respectively (Abel, Citation1983). In recent years, concerns about future government policies in areas such as regulation, spending, taxation, monetary policy, and healthcare have increased among businesses and households due to the impact of the 2008 global financial crisis and the uncertainty surrounding future government actions (Baker et al., Citation2016). The potential delay in investments and purchases due to a volatile economic environment highlights the importance of understanding the impact of uncertainty on the economy.

Economic policy uncertainty (EPU) significantly impacts consumer, corporate, and government expenditures and investments. Several studies have shown the negative effects of policy uncertainty on investment (Cui et al., Citation2021; Ilyas et al., Citation2021; Stokey, Citation2016), individual consumption (Baker et al., Citation2012), economic growth (Bloom, Citation2014; Xue et al., Citation2022), technology and output (Zheng & Zhu, Citation2021), stock prices (Antonakakis et al., Citation2013; Brogaard & Detzel, Citation2015; Ko & Lee, Citation2015), the entry of exporters into international markets (Handley, Citation2014), and the cryptocurrency market (Bouri & Gupta, Citation2021; Colon et al., Citation2021).

The impact of economic policy uncertainty goes beyond just capital markets, affecting bank valuations as prices drop in times of uncertainty (He & Niu, Citation2018). During periods of high economic policy uncertainty, economies often experience slow or negative growth rates and a decline in bank valuations. There is a positive correlation between EPU and oil prices (Fang et al., Citation2018) and it is also a strong predictor of stock and green practices (Balcilar, Bekiros et al., Citation2017; Pham & Nguyen, Citation2022; Qalati et al., Citation2022). The short-term policy changes brought on by EPU can also affect gold prices in terms of returns and volatility (Balcilar, Gupta, Pierdzioch et al., Citation2016; Fang et al., Citation2018). Policy uncertainty also has spillover effects on other countries (Balcilar et al., Citation2017; Ma et al., Citation2022, Citation2022). This is shown by Istiak and Alam (Citation2019), who found that US policy uncertainty increases caused decreases in Mexico’s industrial production, price level, and policy interest rate.

Our main contribution is to examine the symmetric and asymmetric impact of economic policy uncertainty shocks on foreign remittances. In recent decades, international remittances have become increasingly important for countries’ socioeconomic development. Remittances make a significant difference at the household, local, and international levels of a nation. The increase in foreign remittances is due to their role in promoting economic prosperity (Ajide & Osinubi, Citation2020; Bhattacharya et al., Citation2018; Das & Sethi, Citation2020), improving household welfare and reducing poverty (Kumar, Citation2021; Wagle & Devkota, Citation2018), enhancing health conditions (Kumar, Citation2019), and driving sustainable growth (Jushi et al., Citation2021).

While various factors affect foreign remittances as identified in the literature, such as oil price shocks, exchange rate fluctuations, domestic GDP (Jijin et al., Citation2022), real interest rate changes, political stability in both countries, government policy for migrants, inflation, differential income analysis, and ease of remitting funds (Gupta, Citation2006), political stability, government policy, and financial intermediation are significantly influencing remittances (Abbas et al., Citation2017; Faini, Citation1994; Wahba, Citation1991). The economic conditions of both the migrant’s home and destination countries also play a role (Yoshino et al., Citation2020). Furthermore, a high inflation rate and policy uncertainty can decrease the inflow of foreign remittances (Elbadawi & Rocha, Citation1992). Similarly, the rise in prices can destabilize the economy and discourage migrants from making investments in their home countries (Abbas et al., Citation2017). In general, foreign remittances have a positive impact on investment and economic growth (Noushad et al., Citation2020; Pande, Citation2018). Despite this, the relationship between foreign remittances and policy uncertainty has received limited research attention.

Nevertheless, Yayi (Citation2022) noted a variation in remittances made by emigrants from developed to developing nations during uncertain times. Specifically, the author demonstrated that economic policy uncertainty has a lagged, positive, and significant effect on remittances, as opposed to a contemporaneous effect. However, previous studies have emphasized that non-linear impacts add complexity because the effects of economic policy uncertainty can be difficult to predict, as they may depend on other variables (e.g., Alam & Istiak, Citation2020; Bahmani-Oskooee & Maki-Nayeri, Citation2019; Foerster, Citation2014; Hassan et al., Citation2018; Wen et al., Citation2022). This poses a challenge. In this study, we aim to expand the understanding of the relationship between economic policy uncertainty and foreign remittances by examining the non-linear response of economic policy uncertainty to foreign remittances. Furthermore, we anticipate that the empirical investigation of positive and negative policy uncertainty shocks would yield insightful results that could be valuable to policymakers.

We examine the dynamic asymmetry between economic policy uncertainty and overseas remittances received in the context of the BRIC economies. This group of nations is of particular interest due to their increasing importance in the global economy. With their large population, growth, and trade, these nations have a significant global influence (Yang & Samaké, Citation2011). They are the second-largest economy in the world after the United States and ahead of the Euro Area. The BRIC nations are particularly noteworthy due to their rapidly growing share in world trade over the past few decades (Caporale et al., Citation2017). Furthermore, this group comprises mostly developing countries (with the exception of Russia), which were declared as such by the minister of foreign affairs in March 2022.Footnote1 Remittances are the second-largest source of external financing after foreign direct investment for developing countries (Ratha et al., Citation2012). Additionally, developing countries are more vulnerable to economic uncertainties than developed countries (Yayi, Citation2022). The dynamic nature of the BRIC economies, with their need for foreign remittances and their struggle to cope with economic shocks, highlights the important implications of remittances received during policy uncertainty. Therefore, it is reasonable to draw generalizations from the empirical evidence focusing on the BRIC economies. We employ both linear Autoregressive Distributed Lag (ARDL) by Pesaran et al. (Citation2001) and dynamic non-linear Autoregressive Distributed Lag (NARDL) by Shin et al. (Citation2014) approaches. The former approach is suitable for testing the short- and long-term symmetry, while the latter is used to examine the asymmetry between the foreign remittances’ response to positive and negative policy uncertainty shocks in the short- and long-term.

The findings suggest that economic policy uncertainty has a significant impact on foreign remittances, indicating the importance of having stable and predictable economic policies for attracting and retaining foreign investments. Specifically, policymakers can take measures to reduce policy uncertainty and increase the stability of the economic environment to encourage foreign remittances and attract foreign investment. Moreover, policymakers should also be aware of the impact of policy uncertainty on foreign remittances and take necessary steps to mitigate their negative impact. On the other hand, migrants should be aware of the economic conditions and policy changes in their host countries, and consider these factors when making decisions about sending money back home. Further, recipients of remittances should be aware of the impact of policy uncertainty on the level of remittances they receive and plan accordingly. Overall, the study highlights the importance of a stable and predictable economic environment for attracting and retaining foreign remittances and investments, and the need for policymakers, migrants, and recipients of remittances to take a comprehensive and strategic approach to address the issue.

The rest of the study is organized as: the next section discusses a comprehensive literature review and theory along with the hypothesis, and section three provides data and methodology. Section four discusses the results and section five concludes the study with implications and limitations of the study.

2. Literature review

2.1. The Impact of Economic Policy Uncertainty

The literature nowadays generally agrees that corporate financial management policies and several economic indicators are negatively impacted by economic policy uncertainty. Aye et al. (Citation2018), for instance, demonstrate that policy uncertainty has a significant ability to predict market shocks. EPU hence influences volatility as well as stock returns. EPU specifically has a very poor relationship with the stock market. Additionally, EPU has a markedly adverse link with bond prices, output, and investment in addition to the stock market (Gilchrist et al., Citation2014; Pastor & Veronesi, Citation2013). Also, there is a strong impact of the EPU index on the correlations between the stock and bond markets. Specifically, the increased policy uncertainty can lead to increased correlations between the stock and bond markets, which may have important implications for asset allocation and portfolio management decisions (X.-M. Li et al., Citation2015), along with its long-term association with US equity markets (Fang et al., Citation2017).

The impact of EPU extends beyond capital markets to bank valuations, as prices decline in the face of uncertainty (He & Niu, Citation2018). EPU also has a major impact on volatility, commodity returns (Shahzad et al., Citation2017), and GDP growth (Balcilar, Gupta, Segnon et al., Citation2016). In a similar vein, the relationship of EPU with oil company stock prices over time was positive and relatively significant (Fang et al., Citation2018). Additionally, it has the potential to impact the performance of both stock and oil markets (Balcilar, Bekiros et al., Citation2017). Additionally, Balcilar, Gupta, Pierdzioch et al. (Citation2016) demonstrate how short-term policy changes affect gold prices pertaining to returns and volatility. The EPU influences gold prices, which is consistent with the previous findings (Fang et al., Citation2018).

Therefore, increased policy uncertainty will affect capital investments over the long run and have lengthy repercussions for economic expansion (Barrero et al., Citation2017). In different areas of business, the impact of uncertainty on corporate and financial management decisions varies. Firms, for instance, have significant and rising debt loads, making capital structure one of the most important considerations for any organization, the cost of financing is adversely affected by an increase in EPU (Colak et al., Citation2017; Jens, Citation2017; Kelly et al., Citation2016). The same unfavorable result holds for mergers and acquisitions. When there is a lot of uncertainty, merger, and acquisition agreements become less frequent and take longer to complete (Bonaime et al., Citation2018; Nguyen & Phan, Citation2017). The EPU index has the ability to predict future returns on investments and has some control over the rates of currency conversion (Yin et al., Citation2017).

The impact of economic policy uncertainty on stock markets and economies varies across countries, depending on factors such as the size of the stock market and the state of the economy (Christou et al., Citation2017). Some countries are less affected by uncertainty (X.-L. Li et al., Citation2016), while others experience a stronger impact (Das & Sethi, Citation2020). There is also disagreement on the relationship between stock returns and EPU in developing nations, with some studies suggesting that credit restrictions result in a weaker effect (Carrière-Swallow & Céspedes, Citation2013). Moreover, uncertainty has been known to spread to neighboring countries (Balcilar et al., Citation2017; Christou et al., Citation2017). Further, Holmes and Maghrebi (Citation2016) provide evidence that policy uncertainty may lead to increased stock market volatility and higher unemployment rates, ultimately decreasing employment.

2.2. Uncertainty & Foreign Remittances

According to theoretical literature, there are several ways that uncertainty impacts economic activity. High economic uncertainty is an issue for businesses, financial markets, and households, and causes major delays in spending, investments, and contracts for both households and corporations (Baker et al., Citation2016; Jurado et al., Citation2015; Ozturk & Sheng, Citation2018; Rossi et al., Citation2016; Scotti, Citation2016). Furthermore, macroeconomic instability increases inflation, which increases migration (Elbadawi & Rocha, Citation1992), and migration increases foreign remittances (Nathaniel et al., Citation2017), demonstrating the positive relationship between high inflation rates and remittances from abroad.

However, some studies indicate that price instability negatively links the inflow of foreign remittances (Shahbaz & Aamir, Citation2009). Moreover, real exchange rate fluctuations can hurt remittances (Jijin et al., Citation2022). In the short run, the depreciation of local currency causes remittances to increase, but in the long run, it may reduce immigrants’ confidence in their native country (Bouhga-Hagbe, Citation2006). Likewise, El-Sakka and McNabb (Citation1999) and Helbling et al. (Citation2005) provide evidence that restrictions on exchange rates and black-market charges in the country of origin may prevent remittances and may also prevent transfers from official to unofficial channels. Additionally, political instability and internal conflict are inversely correlated with international remittances (Agbhegha, Citation2006; Helbling et al., Citation2005). Remittances may be discouraged by political unrest or lax laws and regulations in the nation of origin because these risks do not encourage investment.

In addition, the macroeconomic and institutional framework of the nation crucially needs adjustment to support the use of remittances for poverty alleviation, stimulating national investment, and promoting economic growth and sustainable development (Imai et al., Citation2014; Kumar, Citation2021; Noushad et al., Citation2020; Wagle & Devkota, Citation2018; Wei et al., Citation2022). De et al. (Citation2019) found that after a sudden pause and financial crisis, there was an upward trend in remittances, which they observed using a more descriptive technique. Yayi (Citation2022) recently discovered the significant connection between economic policy uncertainty and international remittances. The author showed that the influence of uncertain economic policies on remittances sent by foreign migrants was significantly hindered.

2.3. The Asymmetric Impact of Economic Policy Uncertainty

The EPU index has been demonstrated to have asymmetric impacts on a wide range of variables and indicators by numerous research in the literature. For instance, Foerster (Citation2014) claimed that uncertainty had asymmetric effects on employment and economic activities. According to the author’s findings, significant increases in uncertainty have a detrimental impact on economic activity and can prolong the time it takes for the economy to recover, but significant decreases in uncertainty have no such impact. In the G7 nations, it has been demonstrated that policy uncertainty significantly asymmetrically affects domestic investment as well as money supply and demand. This important relationship persists when there is greater uncertainty but diminishes or might even vanish when there is less uncertainty. Similarly, uncertainty affects numerous economic activities and financial policies in an asymmetrical manner (Bahmani-Oskooee & Maki-Nayeri, Citation2019; Qalati et al., Citation2023).

Istiak and Alam (Citation2019) demonstrated that the impact of EPU on inflation can be asymmetric, depending on whether it occurs before or after a financial crisis. The growing impact of EPU on trade has a stronger impact than a corresponding decrease (Hassan et al., Citation2018). Additionally, uncertainty has asymmetric impacts in the insurance industry, where surges in uncertainty result in higher non-life insurance rates and lower life insurance prices (Gupta et al., Citation2019). Short-run economic growth is negatively impacted by the positive EPU shocks, and the size of the positive shocks is bigger than the magnitude of the negative shocks (Wen et al., Citation2022).

It is interesting to note the suggested ways to lessen the information asymmetry effect that uncertainty in economic policy has on investors. Markets react less strongly to announcements that come with greater dispersion and shock, as assessed by the bid-ask spread when there is more uncertainty. Moreover, uncertainty can lead to an increased risk of low market liquidity and decreased market efficiency. Although managers try to lessen the problems brought on by uncertainties and asymmetries by encouraging more disclosure practices, doing so would address the unfavorable effects of uncertainty (Kumari et al., Citation2022; Nagar et al., Citation2019).

Alternatively, Wellman (Citation2017) hypothesized that political ties possibly will lessen the negative impacts of uncertainty and information asymmetry. The author made the case that in order to reduce the level of uncertainty, businesses must invest in such relationships. Similarly, demonstrated economic uncertainty affects dividends in the US in a non-linear way. Their results showed that companies increase dividend payments during a presidential election because of the uncertainty surrounding future national, fiscal, and monetary policies.

2.4. Conceptual Framework

According to the pull and push factors theory of migration, various political and economic push motives result in migration. Such as war, political independence movements for refugees, and political persecution are all political push factors. Poverty and unemployment are economic factors that influence migration, driving people to seek employment (Alchin, Citation2014). Political unrest compels people to move abroad; as more people move, more remittances will be transferred to the country of origin, since migration increases remittance inflows (Nathaniel et al., Citation2017). Based on this idea, we may demonstrate a convincing connection in the underlying theory of migration between economic policy uncertainty and foreign remittances.

Considering the harm that EPU does to the economy, it is surprising that there is limited research on the effect of EPU on foreign remittances. The dynamics of remittances over the business cycle have not been well studied. Yayi (Citation2022) reports three types of findings regarding the cyclicality of remittances concerning the recipient’s economies. First, remittances are considered to be countercyclical, meaning that they increase during economic downturns and act as a stabilizing force for households, helping to maintain consumption levels (Ebeke & Combes, Citation2013; Singh et al., Citation2011). Second, remittances are also considered procyclical, meaning that they increase during periods of economic growth and decline during recessions (Cooray & Mallick, Citation2013; Durdu & Sayan, Citation2010). Third, some studies have found inconclusive results regarding the relationship between remittances and the business cycle (Akkoyunlu & Kholodilin, Citation2008; Naudé & Bezuidenhout, Citation2012).

Bekaert et al. (Citation2013) noted that monetary policy uncertainty is an important component of economic policy uncertainty. Further, Hayford and Malliaris (Citation2005) suggested in times of uncertainty and market asymmetry, monetary policy can be used as a tool to mitigate financial risk and prevent a financial crisis. Without sound economic rules in place, it is difficult for firms and individuals to decide how much money to save, spend, and invest (Foresti, Citation2018). Monetary and fiscal policies can significantly be considered to reduce market asymmetries and risks (Al-Thaqeb & Algharabali, Citation2019). Economic policies may also make it easier to receive remittances from abroad. Thus, it motivates us to examine the asymmetric impact of economic policy uncertainty on foreign remittances. Given that economic variables react to shocks as a result of typical stochastic trends, a non-linear analysis of EPU would be more important to emphasize its impact on foreign remittances. Therefore, we hypothesize that economic policy uncertainty has an asymmetrical impact on foreign remittances.

3. Data and Methodology

We examine the linear and non-linear impact of EPU on Foreign remittances received in BRIC countries using monthly data for the period from 1998M1 to 2020M12 for Brazil, Russia, and China. While we use the data for India from 2003M1-2020M12 because of the availability of data for India’s EPU index. We measure economic policy uncertainty, composed of news events, monetary and fiscal policy, forecast disagreement, and tax code changes, using a comprehensive EPU index developed by Baker et al. (Citation2016). The EPU index comprehensively captures economic uncertainty about the policy decisions, actions, and the economic effects of current and future policy actions (Baker et al., Citation2016). Further, to match the variables’ frequency, we use the data interpolation process for sample countries. We use the fundamental determinants of foreign remittances as control variables in our study such as real effective exchange rate, inflation, unemployment rate, and per capita GDP (Elbadawi & Rocha, Citation1992; Jackman, Citation2013; Jijin et al., Citation2022; Yayi, Citation2022). Table defines a summary of data sources and the specification of variables.

Table 1. Variables and Measures

3.1. Model Specification

We use the linear ARDL (Pesaran et al., Citation2001) and the non-linear ARDL model (Shin et al., Citation2014) to examine the symmetrical and asymmetrical effects of economic policy uncertainty and foreign remittances. Previously, Pesaran et al. (Citation2001) created a special cointegration and error correction method known as the bound test technique. Although Pesaran et al. (Citation2001)’s ARDL model is more adaptable than other approaches, it predicts a linear adaptation process i.e., policy uncertainty has a symmetrical effect on foreign remittances. The adjustment process may be nonlinear when inflow from foreign remittances responds differently from positive and negative shocks of uncertainty. Nevertheless, the asymmetrical expansion of the Pesaran et al. (Citation2001) linear ARDL model is now referred to as NARDL by Shin et al. (Citation2014). Therefore, first, we define the linear ARDL model because the NARDL model is an asymmetric extension of the linear ARDL model Pesaran et al. (Citation2001). According to Pesaran et al. (Citation2001), the following conditionality-based error correction model can be written:

The ARDL (Autoregressive Distributed Lag) process involves two steps: 1) Evaluation of EquationEquation (1)(1)

(1) using the Ordinary Least Squares (OLS) method. 2) Establishment of cointegration among variables. Then, we compare the null hypothesis of no integration

against the alternative hypothesis of integration

using the F-test Pesaran et al. (Citation2001).

According to Pesaran et al. (Citation2001), two sets of critical values are calculated: the lower limit, which assumes that all variables are I (0), and the upper limit, which implies that all variables are I (1). This creates a band that includes all categories of variables, including integrated variables and I (0) and I (1). If the estimated test statistics are higher than the upper limit of reference, the null hypothesis that there is no cointegration is rejected in the interests of integration. After that long-term rates are estimated if the variables are cointegrated. We follow Shin et al. (2013) and take into account the following asymmetric regression long-run equation to develop the NARDL model:

Where is the initial value,

(

) are the partial sum of positive (increase) and negative (decrease) changes in

defined as:

To distinguish between positive and negative changes in , we assume this is divided into

and

around a single threshold value of zero in the basic form. Shin et al. (Citation2014) contend that the partial sum processes result in economically significant interpretation in many applications with this zero-threshold value. The linear ARDL model in Equationequation (1)

(1)

(1) can be changed to the following NARDL model by substituting

and

as:

The estimation of the NARDL (Non-Linear Autoregressive Distributed Lag) model (5) requires three steps: First, estimation of the equations using the standard OLS method. Second, demonstration of the asymmetric (non-linear) long-term relationship (integration) among the variables. To this end, Shin et al. (Citation2014) follow Pesaran et al. (Citation2001) and give the F-test, which involves testing the null hypothesis of no cointegration against an alternative hypothesis. The standard Wald test is used in the third step to demonstrate long- and short-term symmetry. The applicable null hypothesis for a long-term symmetry is

, where

and

. Short-term symmetry can test by evaluating the null hypothesis

=

. Therefore, short-term corrections in increase and decrease are taken off

,

respectively.

4. Results and Discussion

We first use the linear ARDL model and then the nonlinear ARDL model to examine whether economic policy uncertainty has a symmetric or asymmetric effect on foreign remittances in the BRIC context. The descriptive statistics for the variables used for the empirical analysis are presented in Table . The mean values of EPU are very close to each other for sampled countries. Also, the Jarque-Bera test evidence for EPU data is normally distributed for all cases, except Russia, for which EPU is positively skewed.

Table 2. Descriptive Statistics

The correlation analysis is presented in Table for EPU and control variables to test the correlation between the variables used.

Table 3. Correlation Analysis

The results do not evidence of a high correlation between the variables used and the model is free from the multicollinearity problem. Further, to estimate ARDL models, we need to establish that all variables are not integrated into the order I(2). So, we use the Augmented Dickey-Fuller (ADF) and Phillips and Perron (PP) tests to examine the order of integration of each variable. The unit root test is performed on variables at their level and first differences. According to the results reported in Table , all the variables are stationary in their first differences, meaning they are integrated of order I(1) and not I(2). Based on this, the ARDL model can be applied.

Table 4. Unit-root Tests

4.1. ARDL Results

The short-run and long-run linear ARDL model results are presented in Tables and (6), respectively. Since the ARDL model requires testing the null hypothesis of no-cointegration against the alternative to establish the long-run relationship between the variables (Pesaran et al., Citation2001). The F-test value for Russia 4.13, India 3.67, and China 2.85 are greater than the upper and lower bounds critical values at the 1%, 5%, and 10% significance levels revealing statistically significant evidence of linear cointegration, while the F-test for Brazil 2.76 suggests inconclusive results. The short-run estimated coefficient of EPU in Russia is positive and significant at the 10% level. This suggests that a 1% increase in policy uncertainty would result in a 0.1% increase in foreign remittances received by Russia. In addition, the error correction mechanism (ECMt-1) coefficient size for Brazil (−0.001), Russia (−0.010), India (−0.011), and China (−0.001) indicates that the foreign remittances received achieves their long-run equilibrium with the speed of 0.1 percent per month in Brazil and China, and 1 percent per month in Russia and India in the wake of EPU.

Table 5. Linear ARDL (short-run) and diagnostic results

The diagnostic tests reveal no model instability, no error autocorrelation, and no heteroskedasticity in all cases. The adjusted R2 has also been reported as a good fit of the model, and the adjusted R2 0.99, 0.99, 0.89, 0.85 indicates the model enjoys a good fit for Brazil, Russia, India, and China, respectively. Moving towards long-run results, provided in (Table ), suggests the positive and significant long-run effect of EPU on foreign remittances in Russia. Similarly, the positive and significant coefficient of EPU indicates a 17% increase in foreign remittances received in the long-run presence of policy uncertainty in Russia. However, we find no long-run linear cointegration between EPU and foreign remittances in Brazil, India, and China.

Table 6. Linear ARDL (long-run) results

4.2. NARDL Results

The short-run nonlinear ARDL and diagnostic estimation results are reported in (Table ). The F-test value for Russia 3.87, India 3.50, and China at 3.82 are greater than the upper and lower bounds critical values at the 5% significance levels revealing statistically significant evidence of nonlinear cointegration, while the F-test for Brazil 2.41 suggests inconclusive results. The Wald test provides evidence for the presence of short-run asymmetry, which implies the asymmetric impact of EPU on foreign remittances received in Russia and India. However, the long-run Wald test results indicate the presence of asymmetry in all cases. This implies the long-run asymmetric impact of EPU on foreign remittances received in BRIC economies. The findings are consistent with our hypothesized relationship; EPU has an asymmetrical impact on foreign remittances. The estimated coefficient for the positive shock of EPU is 3.980, −0.000, 0.039, and −0.003 for Brazil, Russia, India, and China respectively but only significant for India. It suggests that a 1% increase in positive shock of EPU is anticipated to increase the foreign remittances received in India by 3.9%. This is consistent with the findings of earlier studies (e.g., Hagen-Zanker & Siegel, 2007; Abbas et al., Citation2017), which suggest that the detrimental effects of political uncertainty and social turmoil increase the requirement for funds to households and migration from the country, and subsequent remittances received in home countries. Whereas, the estimated coefficient for the negative shock of EPU is 0.000, 0.003, 0.000, and −0.001 for Brazil, Russia, India, and China respectively but only significant for Russia. It implies that the negative shock of EPU has a positive impact on foreign remittances received in Russia. The size of ECMt-1 coefficient (−0.001) for Brazil, (−0.011) Russia, (−0.013) India, and (−0.003) China indicates that foreign remittances achieve long-run equilibrium at a speed of 0.1, 1.1, 1.3, and 0.3 percent per month during EPU in Brazil, Russia, India, and China respectively.

Table 7. Nonlinear ARDL (short-run) and diagnostic results

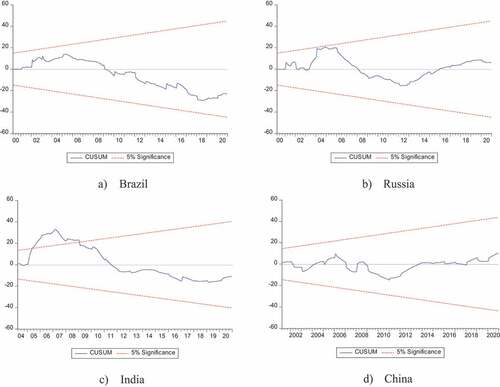

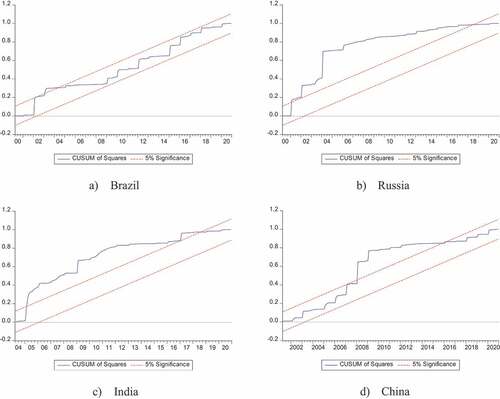

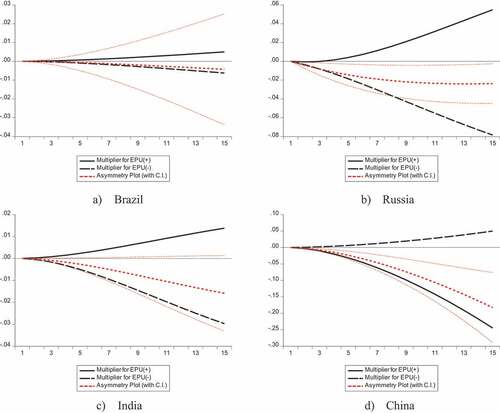

The diagnostic tests reveal no model instability, no error autocorrelation, and no heteroskedasticity in all cases. The adjusted R2 0.99, 0.87, 0.89, and 0.87 indicates a good fit for Brazil, Russia, India, and China, respectively. Moreover, Figure depicts CUSUM, and Figure depicts CUSUMQ estimation of variance stability at a 5% significance level. The CUSUM graphs Figure shows parameters are stable for all cases except India. The dynamic visual impact of positive and negative EPU shock in Figure highlights the correction of asymmetry in the current long-term equilibrium by moving to a new long-term equilibrium. Foreign remittances respond more to negative shocks of EPU than to positive shocks in all cases. We observe an asymmetric slow response of foreign remittances received about the positive and negative shocks of EPU.

Figure 1. CUSUM Graphs.

Figure 2. CUSUMQ Graphs.

Figure 3. Dynamic Multipliers Graphs.

Moving towards long-run results in (Table ), positive (EPU⁺) shocks and negative (EPU⁻) shocks both are positive but not significant in their impact on foreign remittances received. Thus, we find no evidence of positive and negative shocks of EPU on foreign remittances in the long run. Overall the findings are heterogeneous for sample countries. Our findings may be explained by the fact that different nations experience different degrees of economic policy uncertainty (Haq et al., Citation2021). Specifically, some developed nations (e.g., Russia) manage quite well when faced with economic shocks, while emerging nations (e.g., Brazil, India, and China) have the greatest degree of economic uncertainty. This undoubtedly turns into the requirement that overseas migrants send money back to their home nations to ease tough circumstances (Naudé & Bezuidenhout, Citation2012). Consequently, the inflow of remittances received varies subject to economic uncertainties.

Table 8. Nonlinear ARDL (Long-run) results

5. Conclusion

In today’s politically globalized world, the impact of uncertainty on policies relating to economic decisions is greater than ever. Considering the importance of international remittances to the economic development and general well-being of nations, including raising the percentage of investment and education, developing lifestyles, lowering credit constraints and poverty, and expanding business potential. This study specifically examines whether the EPU has a symmetric or asymmetric effect on foreign remittances. The ARDL model is used to analyze the short-run and long-run symmetrical impact of EPU on foreign remittances, while the NARDL model is used to study the short-run and long-run asymmetrical impact of EPU on foreign remittances in BRIC economies. The data used for this analysis is monthly data. The result is evidence for long-run cointegration between EPU and foreign remittances for all cases. However, we find that in the short-run EPU is only positive and significant to the inflows of foreign remittances received in Russia. The possible explanation could justify the need for remittances in the home country when recipients suffer from policy uncertainty. Further, we also find the short-run asymmetric impact of EPU on foreign remittances in Russia and India. Whereas, the long-run asymmetric impact of EPU on foreign remittances in BRIC economies.

The study shows the significance of a steady and predictable economic environment for attracting and maintaining foreign remittances and investments. It also emphasizes the need for a comprehensive and strategic approach by policymakers, migrants, and remittance recipients to address the impact of policy uncertainty on remittances. Policymakers should take measures to reduce policy uncertainty and increase the stability of the economic environment to encourage foreign remittances and attract foreign investment. This can be achieved by having stable and predictable economic policies, designing an effective tax system, promoting financial literacy, developing the domestic financial system, and improving the quality of institutions. These steps will help to increase the benefits of remittances and contribute to the overall economic development of the recipient countries. Further, migrants become aware of the potential risks and uncertainties in their remittances due to the importance of remittances in their home countries. Recipients of remittances should also be aware of the impact of policy uncertainty on the level of remittances they receive.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

Notes

1. Available at: Developing countries, foreign affairs. Retrieved 1 November 2022, from https://www.dfat.gov.au/sites/default/files/list-developing-countries.pdf.

References

- Abbas, F., Masood, A., & Sakhawat, A. (2017). What determine remittances to Pakistan? The role of macroeconomic, political and financial factors. Journal of Policy Modelling, 39(3), 519–20. https://doi.org/10.1016/j.jpolmod.2017.03.006

- Abel, A. B. (1983). Optimal investment under uncertainty. The American Economic Review, 73(1), 228–233. https://www.jstor.org/stable/j.ctv9hj7wb.11

- Agbhegha, V. O. (2006). Does Political Instability Affect Remittance Flows? Vanderbilt University.

- Ajide, F. M., & Osinubi, T. T. (2022). Foreign aid and entrepreneurship in Africa: The role of remittances and institutional quality. Economic Change and Restructuring, 55, 193–224. https://doi.org/10.1007/s10644-020-09305-5

- Akkoyunlu, Ş., & Kholodilin, K. A. (2008). A Link between Workers’ Remittances and Business Cycles in Germany and Turkey. Emerging Markets Finance and Trade, 44(5), 23–40. https://doi.org/10.2753/REE1540-496X440502

- Alam, M. R., & Istiak, K. (2020). Impact of US policy uncertainty on Mexico: Evidence from linear and nonlinear tests. The Quarterly Review of Economics and Finance, 77, 355–366. https://doi.org/10.1016/j.qref.2019.12.002

- Alchin, L. (2014). Pull and Push Factors of Immigration. Retrieved Oct 15, 2018, from http://www.emigration.link

- Al-Thaqeb, S. A., & Algharabali, B. G. (2019). Economic policy uncertainty: A literature review. The Journal of Economic Asymmetries, 20, e00133. https://doi.org/10.1016/j.jeca.2019.e00133

- Antonakakis, N., Chatziantoniou, I., & Filis, G. (2013). Dynamic co-movements of stock market returns, implied volatility and policy uncertainty. Economics Letters, 120(1), 87–92. https://doi.org/10.1016/j.econlet.2013.04.004

- Aye, G. C., Balcilar, M., Demirer, R., & Gupta, R. (2018). Firm-level political risk and asymmetric volatility. The Journal of Economic Asymmetries, 18, e00110. https://doi.org/10.1016/j.jeca.2018.e00110

- Bahmani-Oskooee, M., & Maki-Nayeri, M. (2019). Asymmetric effects of policy uncertainty on domestic investment in G7 countries. Open Economies Review, 30(4), 675–693. https://doi.org/10.1007/s11079-019-09523-z

- Baker, S. R., Bloom, N., & Davis, S. J. (2012). Has economic policy uncertainty hampered the recovery? In Government policies and the delayed economic recovery (pp. 12–16).

- Baker, S. R., Bloom, N., & Davis, S. J. (2016). Measuring economic policy uncertainty. The Quarterly Journal of Economics, 131(4), 1593–1636. https://doi.org/10.1093/qje/qjw024

- Balcilar, M., Bekiros, S., & Gupta, R. (2017). The role of news-based uncertainty indices in predicting oil markets: A hybrid nonparametric quantile causality method. Empirical Economics, 53(3), 879–889. https://doi.org/10.1007/s00181-016-1150-0

- Balcilar, M., Gupta, R., & Pierdzioch, C. (2016). Does uncertainty move the gold price? New evidence from a nonparametric causality-in-quantiles test. Resources Policy, 49, 74–80. https://doi.org/10.1016/j.resourpol.2016.04.004

- Balcilar, M., Gupta, R., & Segnon, M. (2016). The role of economic policy uncertainty in predicting US recessions: A mixed-frequency Markov-switching vector autoregressive approach. Economics, 10, 1. https://doi.org/10.5018/economics-ejournal.ja.2016-27

- Barrero, J. M., Bloom, N., & Wright, I. (2017). Short and long run uncertainty (No. w23676). National Bureau of Economic Research.

- Bekaert, G., Hoerova, M., & Lo Duca, M. (2013). Risk, uncertainty and monetary policy. Journal of Monetary Policy, 60(7), 771–788. https://doi.org/10.1016/j.jmoneco.2013.06.003

- Bhattacharya, M., Inekwe, J., & Paramati, S. R. (2018). Remittances and financial development: Empirical evidence from heterogeneous panel of countries. Applied Economics, 50(38), 4099–4112. https://doi.org/10.1080/00036846.2018.1441513

- Bloom, N. (2014). Fluctuations in uncertainty. Journal of Economic Perspectives, 28(2), 153–176. https://doi.org/10.1257/jep.28.2.153

- Bonaime, A., Gulen, H., & Ion, M. (2018). Does policy uncertainty affect mergers and acquisitions? Journal of Financial Economics, 129(3), 531–558. https://doi.org/10.1016/j.jfineco.2018.05.007

- Bouhga-Hagbe, M. J. (2006). Altruism and Workers’ Remittances: Evidence from Selected Countries in the Middle East and Central Asia (EPub) (No. 6-130). International Monetary Fund.

- Bouri, E., & Gupta, R. (2021). Predicting Bitcoin returns: Comparing the roles of newspaper-and internet search-based measures of uncertainty. Finance Research Letters, 38, 101398. https://doi.org/10.1016/j.frl.2019.101398

- Brogaard, J., & Detzel, A. (2015). The asset-pricing implications of government economic policy uncertainty. Management Science, 61(1), 3–18. https://doi.org/10.1287/mnsc.2014.2044

- Caporale, G. M., Spagnolo, F., & Spagnolo, N. (2017). Macro news and exchange rates in the BRICS. Finance Research Letters, 21, 140–143. https://doi.org/10.1016/j.frl.2016.12.002

- Carrière-Swallow, Y., & Céspedes, L. F. (2013). The impact of uncertainty shocks in emerging economies. Journal of International Economics, 90(2), 316–325. https://doi.org/10.1016/j.jinteco.2013.03.003

- Christou, C., Cunado, J., Gupta, R., & Hassapis, C. (2017). Economic policy uncertainty and stock market returns in PacificRim countries: Evidence based on a Bayesian panel VAR model. Journal of Multinational Financial Management, 40, 92–102. https://doi.org/10.1016/j.mulfin.2017.03.001

- Çolak, G., Durnev, A., & Qian, Y. (2017). Political uncertainty and IPO activity: Evidence from US gubernatorial elections. The Journal of Financial and Quantitative Analysis, 52(6), 2523–2564. https://doi.org/10.1017/S0022109017000862

- Colon, F., Kim, C., Kim, H., & Kim, W. (2021). The effect of political and economic uncertainty on the cryptocurrency market. Finance Research Letters, 39, 101621. https://doi.org/10.1016/j.frl.2020.101621

- Cooray, A., & Mallick, D. (2013). International business cycles and remittance flows. The BE Journal of Macroeconomics, 13(1), 515–547. https://doi.org/10.1515/bejm-2013-0030

- Cui, X., Wang, C., Liao, J., Fang, Z., & Cheng, F. (2021). Economic policy uncertainty exposure and corporate innovation investment: Evidence from China. Pacific-Basin Finance Journal, 67, 101533. https://doi.org/10.1016/j.pacfin.2021.101533

- Das, A., & Sethi, N. (2020). Effect of foreign direct investment, remittances, and foreign aid on economic growth: Evidence from two emerging South Asian economies. Journal of Public Affairs, 20(3), e2043. https://doi.org/10.1002/pa.2043

- De, S., Islamaj, E., Kose, M. A., & Reza Yousefi, S. (2019). Remittances over the business cycle: Theory and evidence. Economic Notes: Review of Banking, Finance and Monetary Economics, 48(3), e12143. https://doi.org/10.1111/ecno.12143

- Durdu, C. B., & Sayan, S. (2010). Emerging market business cycles with remittance fluctuations. IMF Staff Papers, 57(2), 303–325. https://doi.org/10.1057/imfsp.2009.3

- Ebeke, C., & Combes, J. L. (2013). Do remittances dampen the effect of natural disasters on output growth volatility in developing countries? Applied Economics, 45(16), 2241–2254. https://doi.org/10.1080/00036846.2012.659347

- Elbadawi, I. A., & Rocha, R. (1992) Determinants of Expatriate Workers’ Remittances in North Africa and Europe. Working Paper WPS 1038, Country Economics Department, The World Bank, Washington, DC.

- El-Sakka, M. I., & McNabb, R. (1999). The macroeconomic determinants of emigrant remittances. World Development, 27(8), 1493–1502. https://doi.org/10.1016/S0305-750X(99)00067-4

- Faini, R. (1994). Workers remittances and the real exchange rate. Journal of Population Economics, 7(2), 235–245. https://doi.org/10.1007/BF00173621

- Fang, L., Chen, B., Yu, H., & Qian, Y. (2018). The importance of global economic policy uncertainty in predicting gold futures market volatility: A GARCH‐MIDAS approach. Journal of Futures Markets, 38(3), 413–422. https://doi.org/10.1002/fut.21897

- Fang, L., Chen, B., Yu, H., & Xiong, C. (2018). The effect of economic policy uncertainty on the long-run correlation between crude oil and the US stock markets. Finance Research Letters, 24, 56–63. https://doi.org/10.1016/j.frl.2017.07.007

- Fang, L., Yu, H., & Li, L. (2017). The effect of economic policy uncertainty on the long-term correlation between US stock and bond markets. Economic Modelling, 66, 139–145. https://doi.org/10.1016/j.econmod.2017.06.007

- Foerster, A. (2014). The asymmetric effects of uncertainty. Economic Review, 99, 5–26.

- Foresti, P. (2018). Monetary and fiscal policies interaction in monetary unions. Journal of Economic Surveys, 32(1), 226–248. https://doi.org/10.1111/joes.12194

- Galbraith, J. K. (1977). The Age of uncertainty. Houghton Mifflin.

- Gilchrist, S., Sim, J. W., & Zakrajšek, E. (2014). Uncertainty, financial frictions, and investment dynamics (No. w20038). National Bureau of Economic Research.

- Gupta, P. (2006). Macroeconomic determinants of remittances: Evidence from India. In Economic and Political Weekly (pp. 2769–2775). https://www.jstor.org/stable/4418406

- Gupta, R., Lahiani, A., Lee, C. C., & Lee, C. C. (2019). Asymmetric dynamics of insurance premium: The impacts of output and economic policy uncertainty. Empirical economics, 57, 1959–1978. https://doi.org/10.1007/s00181-018-1539-z

- Handley, K. (2014). Exporting under trade policy uncertainty: Theory and evidence. Journal of International Economics, 94(1), 50–66. https://doi.org/10.1016/j.jinteco.2014.05.005

- Haq, I. U., Maneengam, A., Chupradit, S., Suksatan, W., & Huo, C. (2021). Economic policy uncertainty and cryptocurrency market as a risk management avenue: A systematic review. Risks, 9(9), 163. https://doi.org/10.3390/risks9090163

- Hassan, S., Shabi, S., & Choudhry, T. (2018). Asymmetry, uncertainty and international trade. Swansea University, School of Management.

- Hayford, M. D., & Malliaris, A. G. (2005). Recent monetary policy in the US: Risk management of asset bubbles. The Journal of Economic Asymmetries, 2(1), 25–39. https://doi.org/10.1016/j.jeca.2005.01.002

- Helbling, T., Batini, N., & Cardarelli, R. (2005). Globalization and external imbalances. IMF World Economic Outlook (April 2005) (pp. 109–156). International Monetary Fund.

- He, Z., & Niu, J. (2018). The effect of economic policy uncertainty on bank valuations. Applied Economics Letters, 25(5), 345–347. https://doi.org/10.1080/13504851.2017.1321832

- Holmes, M. J., & Maghrebi, N. (2016). Financial market impact on the real economy: An assessment of asymmetries and volatility linkages between the stock market and unemployment rate. The Journal of Economic Asymmetries, 13, 1–7. https://doi.org/10.1016/j.jeca.2015.10.003

- Ilyas, M., Khan, A., Nadeem, M., & Suleman, M. T. (2021). Economic policy uncertainty, oil price shocks and corporate investment: Evidence from the oil industry. Energy Economics, 97, 105193. https://doi.org/10.1016/j.eneco.2021.105193

- Imai, K. S., Gaiha, R., Ali, A., & Kaicker, N. (2014). Remittances, Growth and Poverty: New Evidence from Asian countries. Journal of Policy Modelling, 36(3), 524–538. https://doi.org/10.1016/j.jpolmod.2014.01.009

- Istiak, K., & Alam, M. R. (2019). Oil prices, policy uncertainty and asymmetries in inflation expectations. Journal of Economics Studies, 46(2), 324–334. https://doi.org/10.1108/JES-02-2018-0074

- Jackman, M. (2013). Macroeconomic determinants of remittance volatility: An empirical test. International Migration, 51, e36–e52. https://doi.org/10.1111/imig.12100

- Jens, C. E. (2017). Political uncertainty and investment: Causal evidence from US gubernatorial elections. Journal of Financial Economics, 124(3), 563–579. https://doi.org/10.1016/j.jfineco.2016.01.034

- Jijin, P., Mishra, A. K., & Nithin, M. (2022). Macroeconomic determinants of remittances to India. Economic Change and Restructuring, 55(2), 1229–1248. https://doi.org/10.1007/s10644-021-09347-3

- Jurado, K., Ludvigson, S. C., & Ng, S. (2015). Measuring uncertainty. American Economic Review, 105(3), 1177–1216. https://doi.org/10.1257/aer.20131193

- Jushi, E., Hysa, E., Cela, A., Panait, M., & Voica, M. C. (2021). Financing growth through remittances and foreign direct investment: Evidences from Balkan Countries. Journal of Risk and Financial Management, 14(3), 117. https://doi.org/10.3390/jrfm14030117

- Kelly, B., Pástor, Ľ., & Veronesi, P. (2016). The price of political uncertainty: Theory and evidence from the option market. The Journal of Finance, 71(5), 2417–2480. https://doi.org/10.1111/jofi.12406

- Ko, J.-H., & Lee, C.-M. (2015). International economic policy uncertainty and stock prices: Wavelet approach. Economics Letters, 134, 118–122. https://doi.org/10.1016/j.econlet.2015.07.012

- Kumar, B. (2019). The impact of international remittances on education and health in Bangladesh. International Journal of Science and Qualitative Analysis, 5(1), 6–14. https://doi.org/10.11648/j.ijsqa.20190501.12

- Kumar, B. (2021). Construction of household welfare index and welfare impact of international remittances in Rural Bangladesh. Preprints 2021, 20210505512021050551. https://doi.org/10.20944/preprints202105.

- Kumari, S., Oad Rajput, S. K., Hussain, R. Y., Marwat, J., & Hussain, H. (2022). Optimistic and pessimistic economic sentiments and US Dollar exchange rate. International Journal of Financial Engineering, 9(4), 2150043. https://doi.org/10.1142/S2424786321500432

- Li, X.-L., Balcilar, M., Gupta, R., & Chang, T. (2016). The causal relationship between economic policy uncertainty and stock returns in China and India: Evidence from a bootstrap rolling window approach. Emerging Markets Finance and Trade, 52(3), 674–689. https://doi.org/10.1080/1540496X.2014.998564

- Li, X.-M., Zhang, B., & Gao, R. (2015). Economic policy uncertainty shocks and stock–bond correlations: Evidence from the US market. Economics Letters, 132, 91–96. https://doi.org/10.1016/j.econlet.2015.04.013

- Ma, Y., Wang, Z., & He, F. (2022). How do economic policy uncertainties affect stock market volatility? Evidence from G7 countries. International Journal of Finance & Economics, 27(2), 2303–2325. https://doi.org/10.1002/ijfe.2274

- Nagar, V., Schoenfeld, J., & Wellman, L. (2019). The effect of economic policy uncertainty on investor information asymmetry and management disclosures. Journal of Accounting and Economics, 67(1), 36–57. https://doi.org/10.1016/j.jacceco.2018.08.011

- Nathaniel, A. O., Tetteh, J., & Opoku, S. (2017). Remittance, Migration and Development: Investigating African Diaspora in Germany. International Journal of Innovative Research and Development, 6, 6. https://doi.org/10.24940/ijird/2017/v6/i6/JUN17009

- Naudé, W., & Bezuidenhout, H. (2012). Remittances provide resilience against disasters in Africa. Maastricht Economic and social Research institute on Innovation and Technology (UNU‐MERIT). http://www.merit.unu.edu

- Nguyen, N. H., & Phan, H. V. (2017). Policy uncertainty and mergers and acquisitions. Journal of Financial and Quantitative Analysis, 52(2), 613–644. https://doi.org/10.1017/S0022109017000175

- Noushad, A. P., Parida, J. K., & Raman, R. K. (2022). Low-skilled emigration, remittances and economic development in India. Migration and Development, 11(3), 389–419. https://doi.org/10.1080/21632324.2020.1787099

- Ozturk, E. O., & Sheng, X. S. (2018). Measuring global and country-specific uncertainty. Journal of International Money and Finance, 88, 276–295. https://doi.org/10.1016/j.jimonfin.2017.07.014

- Pande, A. (2018). India’s experience with remittances: A critical analysis. The Round Table, 107(1), 33–43. https://doi.org/10.1080/00358533.2018.1424078

- Pastor, L., & Veronesi, P. (2013). Political uncertainty and risk premia. Journal of Financial Economics, 110(3), 520–545. https://doi.org/10.1016/j.jfineco.2013.08.007

- Pesaran, M. H., Shin, Y., & Smith, R. J. (2001). Bounds testing approaches to the analysis of level relationships. Journal of Applied Econometrics, 16(3), 289–326. https://doi.org/10.1002/jae.616

- Pham, L., & Nguyen, C. P. (2022). How do stock, oil, and economic policy uncertainty influence the green bond market? Finance Research Letters, 45, 102128. https://doi.org/10.1016/j.frl.2021.102128

- Qalati, S. A., Kumari, S., Soomro, I. A., Ali, R., & Hong, Y. (2022). Green supply chain management and corporate performance among manufacturing firms in Pakistan. Frontiers in Environmental Science, 10(873837), 540.

- Qalati, S. A., Kumari, S., Tajeddini, K., Bajaj, N. K., & Ali, R. (2023). Innocent devils: The varying impacts of trade, renewable energy and financial development on environmental damage: Nonlinearly exploring the disparity between developed and developing nations. Journal of Cleaner Production, 135729. https://doi.org/10.1016/j.jclepro.2022.135729

- Ratha, D., Mohapatra, S., & Silwal, A. (2012). Remittances to developing countries will surpass $400 billion in 2012. World Bank, (Migration and Development Brief No. 17)

- Rossi, B., Sekhposyan, T., & Soupre, M. (2016). Understanding the sources of macroeconomic uncertainty. Available at SSRN 2816841.

- Scotti, C. (2016). Surprise and uncertainty indexes: Real-time aggregation of real-activity macro-surprises. Journal of Monetary Economics, 82, 1–19. https://doi.org/10.1016/j.jmoneco.2016.06.002

- Shahbaz, M., & Aamir, N. (2009). Determinants of workers’ remittances: Implications for poor people of Pakistan. European Journal of Scientific Research, 25(1), 130–144.

- Shahzad, S. J. H., Raza, N., Balcilar, M., Ali, S., & Shahbaz, M. (2017). Can economic policy uncertainty and investors sentiment predict commodities returns and volatility? Resources Policy, 53, 208–218. https://doi.org/10.1016/j.resourpol.2017.06.010

- Shin, Y., Yu, B., & Greenwood-Nimmo, M. (2014). Modelling asymmetric cointegration and dynamic multipliers in a nonlinear ARDL framework. In Sickles, R., & Horrace, W. (Eds.), Festschrift in Honor of Peter Schmidt (pp. 281–314). Springer. https://doi.org/10.1007/978-1-4899-8008-3_9

- Singh, R. J., Haacker, M., Lee, K. W., & Le Goff, M. (2011). Determinants and macroeconomic impact of remittances in Sub-Saharan Africa. Journal of African Economies, 20(2), 312–340. https://doi.org/10.1093/jae/ejq039

- Stokey, N. L. (2016). Wait-and-see: Investment options under policy uncertainty. Review of Economic Dynamics, 21, 246–265. https://doi.org/10.1016/j.red.2015.06.001

- Wagle, U. R., & Devkota, S. (2018). The impact of foreign remittances on poverty in Nepal: A panel study of household survey data, 1996–2011. World Development, 110, 38–50. https://doi.org/10.1016/j.worlddev.2018.05.019

- Wahba, S. (1991). What determines workers’ Remittances? Finance and Development, 28(4), 41.

- Wei, C., An-Wei, W., & Kumari, S. (2022). Do more get more: Monopoly appropriation of labor income in manufacturing companies. Frontiers in Environmental Science, 10, 2275. https://doi.org/10.3389/fenvs.2022.1037615

- Wellman, L. A. (2017). Mitigating political uncertainty. Review of Accounting Studies, 22(1), 217–250. https://doi.org/10.1007/s11142-016-9380-0

- Wen, J., Khalid, S., Mahmood, H., & Yang, X. (2022). Economic policy uncertainty and growth nexus in Pakistan: A new evidence using NARDL model. Economic Change and Restructuring, 55(3), 1701–1715. https://doi.org/10.1007/s10644-021-09364-2

- Xue, C., Shahbaz, M., Ahmed, Z., Ahmad, M., & Sinha, A. (2022). Clean energy consumption, economic growth, and environmental sustainability: What is the role of economic policy uncertainty? Renewable Energy, 184, 899–907. https://doi.org/10.1016/j.renene.2021.12.006

- Yang, Y., & Samaké, I. (2011). Low-Income Countries’ BRIC Linkage: Are There Growth Spillovers? IMF Working Papers, 1–35.

- Yayi, C. L. (2022). The lag effect of economic policy uncertainty on remittances. Applied Economics Letters, 1–6. https://doi.org/10.1080/13504851.2022.2086681

- Yin, D. A. I., Zhang, J. W., Yu, X. Z., & Xin, L. I. (2017). Causality between economic policy uncertainty and exchange rate in China with considering quantile differences. Theoretical & Applied Economics, 24(3). 29–38.

- Yoshino, N., Taghizadeh-Hesary, F., & Otsuka, M. (2020). Determinants of international remittance inflow in Asia-Pacific middle-income countries. Economic Analysis and Policy, 68, 29–43. https://doi.org/10.1016/j.eap.2020.08.003

- Zheng, G., & Zhu, S. (2021). Research on the effectiveness of China’s macro control policy on output and technological progress under economic policy uncertainty. Sustainability, 13(12), 6844. https://doi.org/10.3390/su13126844