?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

Purpose: This paper investigates how entrepreneurial finance in Qatar affects the performance of small and entrepreneurship businesses (SEB). It is the first study examining the financial decisions of SEB in Qatar, illustrating the advantages and disadvantages of traditional and innovative sources of finance. In addition, we investigate the impact of different funding sources on three dimensions of SEB performance: financial, marketing and internal business and development performance. Methodology: Our sample included 300 SEB owners and managers, selected randomly and contacted in January to March 2020. Following the delivery and collection process, the study obtained 161 questionnaires, which were analysed using ordinary least squares regression. Findings: The results suggest that diversity and accessing new and innovative sources of finance affect the performance of SEBs. Meanwhile, this effect varies among different aspects of performance. The study concluded that SEBs prefer equity to debts. The performance of SBEs is mainly derived through accessibility to funds, governmental support, using innovative finance and the availability of collateral. Implications: This study contributes to the literature and industry by being the first to examine the accessibility of innovative sources of funds for SEBs in Qatar and their impact on different dimensions of performance. Our findings can help decision-makers to consider the impact of diverse sources of funds on different performance dimensions, which affect financing decisions made based on the performance priorities. Moreover, we find a negative impact of governmental support and using crowdfunding on internal business and development performance; this implies that less efficient SEBs, in terms of their internal business and marketing performance, are more active in obtaining both governmental support and crowdfunding, as they may be not eligible for other sources of finance. Our work highlights the key role of adapting to the new accessibility of funds in improving the performance of SBEs in Qatar, which is ultimately reflected in the diversification of the economy.

PUBLIC INTEREST STATEMENT

This paper investigates how entrepreneurial finance in Qatar affects the performance of small and entrepreneurship businesses (SEB). We examined the financial decisions of SEB in Qatar, illustrating the advantages and disadvantages of traditional and innovative sources of finance. In addition, we investigate the impact of different funding sources on three dimensions of SEB performance: financial, marketing and internal business and development performance. Our sample included 300 SEB owners and managers, selected randomly and contacted in January to March 2020. The results suggest that diversity and accessing new and innovative sources of finance affect the performance of SEBs. Meanwhile, this effect varies among different aspects of performance. The study concluded that SEBs prefer equity to debts. The performance of SBEs is mainly derived through accessibility to funds, governmental support, using innovative finance and the availability of collateral. Our findings can help decision-makers to consider the impact of diverse sources of funds on different performance dimensions, which affect financing decisions made based on the performance priorities. Moreover, we find a negative impact of governmental support and using crowdfunding on internal business and development performance; this implies that less efficient SEBs, in terms of their internal business and marketing performance, are more active in obtaining both governmental support and crowdfunding, as they may be not eligible for other sources of finance. Our work highlights the key role of adapting to the new accessibility of funds in improving the performance of SBEs in Qatar, which is ultimately reflected in the diversification of the economy.

1. Introduction

Small and entrepreneurship businesses (SEBs) are newly launched firms or entrepreneurial ventures that are at the stage of introduction, development or market research. Usually these enterprises are associated with high-tech projects, because their products are mostly software-based products that can be effortlessly created and mimicked. Modern and innovative firms promote a wide range of positive effects on economic development and wellbeing (Harash et al., Citation2014). More specifically, the intention of these types of companies is to achieve a short-run growth and a long-run profit maximization (Park et al., Citation2019). When it comes to the Arab region, SEBs are considered one of the most essential sectors, as they comprise more than 90% of all businesses, excluding the agricultural sector. In some Arab countries, like Kuwait, the labour force of SEBs makes up approximately half of the country’s total labour force. This suggests that these businesses are not only helping employment rates and job creation (Motta, Citation2020; Vasilescu, Citation2014), but are also contributing greatly to their countries’ GDP. In other words, SEBs play a major role in economic activities, especially in Arab countries (Emine, Citation2012).

Nevertheless, the research points towards the limited likelihood of the survival of such new organizations as a whole, and for technology-oriented firms in particular, which is mainly due to the lack of financial support. Although Qatar is one of those nations currently experiencing a significant increase in SEBs (Block et al., Citation2017), the most challenging obstacles for such initiatives is the struggle to gather funds (Ullah, Citation2020). The unavailability of finance not only limits SEBs in starting, but also constrains their growth and development (Moscalu et al., Citation2020). The main reasons for financing limitations are information asymmetries, agency problems and lack of collateral (Hall & Lerner, Citation2010; Scherr et al., Citation1993). Furthermore, Harash et al. (Citation2014) argue that a business’s productivity and ability to grow are what decide its accessibility and ease of being financed. Still, Bodlaj et al. (Citation2020) suggest that as the world is developing, with new and innovative techniques for obtaining funds, SEBs could surely bypass financial barriers by obtaining funds through new financial sources, and innovations in particular, such as crowdfunding and peer-to-peer finance.

In this context, this paper expands the literature to highlight the effect of financial sources on certain performance perspectives for SEBs. Studying the market for SEBs in Qatar specifically is interesting, as Qatar has one of the highest average gross domestic product (GDP) per capita in the world, according to World Bank reports (Citation2019): the GDP per capita in Qatar was last recorded at 59,923.96 US dollars in 2020, equivalent to 474% of the world’s average. In addition, the announcement about hosting the football World Cup and the national projects planned for such an event have tempted many investors around the world to invest in Qatar, a country that has already launched hundreds of megaprojects for developing its infrastructure. The high incomes in Qatar also increase savings, which, accompanied by the increase in investment opportunities for small subcontracts in national projects, stimulate small businesses and entrepreneurial initiatives. Moreover, SEBs in the Qatari market are expanding enormously year by year, becoming one of the main cores of the country’s economy. However, Qatar has witnessed many accelerated economic and political events in the last decade, including a major decline in oil prices, political blockades from its neighbours, a decrease of GDP per capita by 40%, a slowdown in governmental spending and the end of infrastructure megaprojects, creating pressures on the financial sources for SEBs.

These financial challenges and investment gaps faced by entrepreneurs have motivated this paper to be the first to investigate and compare all the available sources of financing for SEBs in Qatar. Another major motive is that assessing the various sources of finance in order to examine their effects on the performance of firms could play a complementary role in investors diversifying their capital, either with or without traditional finance. Moreover, although alternative finance sources have come to light, the impact of these financial substitutes is still potentially unclear. Thus, the contribution of this research is to examine the empirical link between various funding sources and the performance of SEBs. We consider three different performance dimensions: financial, internal business and development, and marketing. It is also important to mention the uniqueness of this paper in considering the entrepreneurs’ point of view in favouring a certain source over another, using 161 questionnaires completed by randomly selected SEB owners in Qatar. Therefore, the paper’s contribution is to be the first to assist and examine the ease and accessibility of financing SEBs in the context of Qatar. Secondly, it aims to help with understanding the preferences of Qatari entrepreneurs and their choices of source of finance, in addition to the impact of this choice on the firm’s performance. This research can act as a foundation and the start of extended papers that study in more depth the mechanism of types and sources of funds for SEBs in Qatar.

Previous research has focused on the availability of venture capital and crowdfunding as innovative sources, and have ignored other alternative finance vehicles, while entrepreneurs usually utilize many others financing sources, even traditional ones. There is also a lack of research exploring the effects of alternative finance on the performance of SEBs (Block et al., Citation2018). Another gap is that no work has been carried out to investigate the determinants of finance decisions for SEBs in Qatar. In addition, there is currently no research that has investigated the applications of innovative finance in the Qatari context. Accordingly, this paper aims to fill these gaps by examining the currently available types and sources of finance for SEBs in Qatar, in addition to comparing innovative methods with the conventional lending model and considering their impact on the three different dimensions of performance: financial, marketing and internal business and development performance.

2. Literature Review

2.1. Accessing Different Sources of Finance

Accessing various sources of finance is one of the major barriers facing SEBs (Harash et al., Citation2014). Funding sources can be divided into two main categories: internal and external financing. As the scope of the financing strategy is wide, it may begin by obtaining funds from relatives and friends, growing into a broader range of finance from public investors and institutions in the market. The first choice for SEBs in the beginning is through capital provided by the owner, which usually means starting through internal financing/equity (Aiello et al., Citation2020). This is mainly due to the difficulty in approaching external financial sources, especially at the introduction stages (Motta & Sharma, Citation2020). Another major alternative source of funding is venture capital (VC), which works as an effective financial source of equity for SEBs in many markets. Wonglimpiyarat (Citation2015) suggests that VC is one of the most appropriate external sources for SEBs, especially for businesses that expect to be growing significantly. In addition, Donald (Citation2020) notes that VC enables funds provided to such SEBs to be easily converted into tradable financial instruments, rather than sticking to a strict form of loan. The presence of a secondary market such as venture capital provides an opportunity for traditional lenders to turn debts into other tradable equity contracts and instruments, rather than investing in the early life of SEBs with a high interest rate, that compensates their high risk. This gives lenders the chance to exit the relationship if they do not wish it to be a long one, flexibility that encourages the flow of loans to SEBs.

The second common source of funds for SEBs is through commercial, merchant and development banks. Eniola and Entebang (Citation2015) classify debt financing into two main groups: formal and informal. Financial institutions are the main formal source of finance, while informal financial sources can include borrowing loans from family and friends. Usually, when it is time to pay the loan back, SEBs are required to return the debt plus a large sum of interest. Unfortunately, this outcome is due to their high exposure to risk, which consequently could have a negative effect on funds providers such as banks. Because of this, requirements such as customers’ credit history, collateral and stable financial indicators are essential to maintain the fund providers’ risk tolerance (Rupeika-Apoga & Saksonova, Citation2018). For example, lending institutions such as banks usually ask for tangible collateral to guarantee loans to SEBs, but this is rarely available for newly established businesses (Motta & Sharma, Citation2020). Meanwhile, it is more logical to establish the requirements of collateral according to the characteristics of the businesses and entrepreneurs. Schmalz et al. (Citation2017) note that collateral should be consistent with the size, assets, sales, performance, wealth, age and other characteristics of businesses. This theory is also supported by Zhang et al. (Citation2018), who discuss the importance of governments considering the diversification of SEBs’ attributes in designing financial packages to support them. Although innovative sources of financing may seem unstable, traditional sources are also affected by regulations and market fluctuations, such as changes in risks, availability and costs. Hence, Schenk (Citation2015) very much supports the idea of entrepreneurs considering combining or diversifying between both traditional and innovative sources of capital.

Due to the extensive drawbacks of traditional methods of finance in meeting the needs of SEBs, plus the unavailability of or difficulty in accessing new sources, the argument between favouring one source over another has not reached an end. For example, Robb and Robinson (Citation2014) demonstrated that the capital structure of new firms depends largely on external debt sources. Contrarily, Baker et al. (Citation2020) state that new firms normally tend to rely on their own equity rather than liability commitments. Moreover, the conception that SEBs are usually dependent on the beneficence of an unfastened coalition of family and friends appears misleading (Robb & Robinson, Citation2014). However, it is imperative to note that firms that depend on external equity at their introduction phase tend to significantly appreciate the role of informal investors. This illustrates that the decision between internal and external financing is still unclear (Aiello et al., Citation2020).

In addition, the owner’s risk preferences and business characteristics, plus the cost of finance are essential factors that affect the decision about capital structure from the perspectives of both business owners and finance providers (Baker et al., Citation2020). Usually, business owners are risk-averse, since the capital is their own wealth and suppliers charge them more because they are risky (Scherr et al., Citation1993). For example, the “pecking order” theory states that potential funders usually require higher rates of return as compensation for the asymmetric information in new businesses (Myers & Majluf, Citation1984), while such businesses are only eligible to offer low internal rates of return due to their incapability (Oláh et al., Citation2019). Thus, Park et al. (Citation2019) suggest that this dilemma could be mitigated by the government’s involvement, as it is able to improve the resources of SEBs. Similarly, Ullah (Citation2020) suggests that government support is the usual solution, especially in developing countries, in order to ease the path and create a suitable environment for SEBs.

Nowadays, lending technologies can potentially partially offset the lack of information provided by new companies, where mitigating the asymmetry of information not only enhances the role of financial providers, but also encourages them to contribute to funding SEBs (Motta, Citation2020). In addition, from the perspective of businesses, controlling data and initiating a database would surely enhance relations with lenders, and thus enhance their creditworthiness (Donald, Citation2020). Moreover, considering debt as an affordable source is logical if we assume that interest rates are governmentally regulated, which should be the usual case for public banks and institutions (Wellalage & Fernandez, Citation2019). Åstebro and Bernhardt (Citation2003) argue that bank loans could positively affect the survival rate of SEBs. However, Hendon and Bell (Citation2011) disagree, claiming that entrepreneurs prefer credit cards as these mitigate their risk. Similarly, De Kort and Vermeulen (Citation2010) state that entrepreneurs seek funding from equity sources regardless of whether they are weak-ties (venture capital, banks, etc.) or strong-ties (family and friends). Mostly, entrepreneurs prefer equity to debt, where funds are commonly obtained through venture capitalists (Fraser et al., Citation2015; Schäfer et al., Citation2004). Subsequently, Wellalage and Fernandez (Citation2019) suggest that the financing choice of entrepreneurs varies between both types of sources and cannot be confirmed as a certain type of source alone.

Although the literature discussed above demonstrates the impact of financial access and sources on the success and growth of SBEs, very few papers in the literature have investigated the impact of finance on the performance of SBEs. Fraser et al. (Citation2105) stress the need for research to better understand the role of entrepreneurial characteristics in financing decisions, noting a silence in examining the pivotal relationship between access to external finance and growth. In particular, there is a need to explore the relationship between non-bank sources of finance and growth (Fraser et al., Citation2105). Some studies have documented that using venture capital enhances different measures of the performance of small businesses, including higher growth rates (Rosenbusch et al., Citation2013), faster sales (Puri & Zarutskie, Citation2012), better assets, employment growth (Chemmanur et al., Citation2011), better productivity and high income (Ahmed & Cozzarin, Citation2009).

Moreover, a significant proportion of the literature in developed countries highlights the positive effects of private equity finance on growth (Boucly et al., Citation2011; Gilligan & Wright, Citation2012) across a variety of measures, such as labour productivity, employment and operating profitability. Furthermore, other studies have indicated that financial constraints affect survival (Musso & Schiavo, Citation2008), sales and asset growth (Carpenter & Petersen, Citation2002; Musso & Schiavo, Citation2008), employment growth (Haynes & Brown, Citation2009) and business performance in general (Cowling et al., Citation2015). However, there is a lack of such studies in the context of developing markets.

2.2. Innovative Sources of Finance

More recently, there has been an immense change in the entrepreneurial finance scene; new innovative models have come to light, including crowdfunding, peer-to-peer (P2P) business lending and business angels. Block et al. (Citation2021) explains that these platforms connect investors and businesses together to exchange information and receive benefits. In addition, modern financing approaches have emerged due to both supply and demand factors (Block et al., Citation2018). Supply factors include restrictive regulations, undeveloped business information bases and insufficient governmental support for entrepreneurship. In the same context, the demand side (the firm’s characteristics) of small businesses could also affect their ability to be financially supported. For example, demand factors could include a weak business plan, inefficient use of funds and negative performance. As a result, Vasilescu (Citation2014) notes that financial institutions and other funding sources are discouraged from opening up to such businesses. The lack of financial aid has also occurred due to factors that firms might face through no fault of their own, such as adverse selection, moral hazards, inadequate assets and high transaction costs (Vasilescu, Citation2014). This has led to the introduction of innovative financial techniques that allow borrowers and investors to diversify their financing and investment, mainly online and through different types of both debt and equity (Morse, Citation2015). Therefore, these newly established innovations have become a main, dependable source of finance over time, as they are filling the gaps that formal organizations have left. Financial alternatives such as crowdfunding, P2P lending and business angels are thus moving out of their original “box” (Bruton et al., Citation2015). Since the fintech (financial technology) evolution began in 2013 (Stern et al., Citation2017), new and innovative sources of finance have played vast roles in helping SEBs to have the opportunity to begin and in pushing the economy to a new level of growth (Vasilescu, Citation2014).

Accordingly, one of the most recognized innovative financing models is crowdfunding, whereby funds are pooled together by group of individuals in order to invest in a project (Ahlers et al., Citation2015). Another innovative method of lending is P2P, which is similar to crowdfunding in that investors gather, share and diversify their investments over numerous loans, although the investment in P2P is considered as a form of loan obligated to be fully returned or partially compensated by the firm’s owner. Crowdfunding, however, could take either route, as it can be treated as a form of donation or as the original form of lending. The classifications of crowdfunding can also extend to more types, such as reward- and equity-based (Cho et al., Citation2019). It is important to highlight the fact that most innovative models gather investors via the World Wide Web, and the internet technologies have benefits in terms of lowering costs, enhancing efficiency and positively affecting social aspects (Ashta & Assadi, Citation2009; Conlin, Citation1999). In addition, such platforms could be useful in the sense of using several techniques to establish interest rates, including automatic allocation based on demand and supply, and pre-set screening. Therefore, these innovative sources of finance are not only acting as alternatives to traditional financing channels, but they can also improve efficiency compared to other traditional channels. Furthermore, the new and innovative channels can provide access to non-monetary resources such as gathering feedback, building loyal customer bases, and connecting experts, ideas and companies together (Eldridge et al., Citation2019).Thus, SEBs are not the only users who benefit from crowdsourcing; large, established corporations are also using various types of innovation to develop their outputs (Qin et al., Citation2016).

Because such types of funding have no geographical barriers, SEBs usually attract many investors to invest a relatively trivial amount of money. This innovation can be an effective way for entrepreneurs to raise funds. On the other hand, Qin et al. (Citation2016) note that a barrier standing against crowdfunding is that the innovation can be considered riskier compared to traditional sources. Moving away from the usual finance sources requires courage and acceptance of benefiting from people’s ideas and money. Moreover, the costs and effort of SEBs in using innovative finance channels can be higher compared to using traditional techniques. Trust and confidentiality issues with crowdsourcing can prevent businesses from using such sources. This is quite reasonable, especially for developing countries that have loose regulations when organizing the use of innovative funding sources, even in their financial markets (Wellalage & Fernandez, Citation2019). The situation is just the opposite for highly regulated countries that are used to such techniques, like the USA, UK and Canada. The old-style system works based on a contract, while innovations are carried out anonymously, so considering others to be trustworthy is difficult. Overall, expectations assume that innovation’s impact on performance should be positive and effective; Effiom and Edet (Citation2020) suggest that using innovative sources of finance might enhance SEBs’ efficiency and growth.

Basha et al. (Citation2021) highlight the fact that although traditional lending for small businesses has declined due to the global financial crisis and restricted financial regulations, P2P lending has increased in volume and number (see also, Segal, Citation2015). Similar annual global trends have appeared in comprehensive geographical reports issued by the Centre for Alternative Finance at Cambridge University for the years 2013–2020 (Basha et al., Citation2021). It was also documented that P2P comprises 17% of the alternative market share in Europe (Ziegler et al., Citation2018), confirming the findings of Wardrop et al. (Citation2016), which showed that business lending via alternative online channels had grown exponentially in the USA and the rest of the Americas from 2014 to 2016.

The above discussion therefore invites us to suggest that innovative sources of finance such as crowdfunding and P2P could affect firms’ performance and growth. Estrin et al. (Citation2018) have found that the benefits of using innovative sources exceed financial support, as entrepreneurs and investors are utilizing such platforms for further product development. In a similar manner, Stanko and Henard (Citation2016) have examined the contribution of crowdfunding to the improvement of products and found that crowdfunding is used as a communication tool between business owners and loyal customers, allowing them to engage, share ideas and create a “wisdom-of-crowd” effect (Eldridge et al., Citation2019). Moreover, Paschen (Citation2017) suggests that using crowdfunding enhances SEBs’ success and growth. In addition to the multiple enhancements to which crowdfunding can contribute, Cumming et al. (Citation2021) highlight how problems such as adverse selection could be significantly mitigated, as such innovative platforms allow firms to provide information, thus developing transparency and paving the way towards building customers’ confidence.

From the perspective of crisis, specifically during the COVID-19 pandemic, while traditional bank lending had multiple drawbacks, fintechs such as peer-to-peer and crowdfunding platforms were more stable. A possible explanation could be that, counter to traditional banks, the digitalization of innovative platforms eased the process of coping immediately with the disease-spread situation. Cumming et al. (Citation2022) explain that the requirement of the physical presence of the loan applicant reduced access to finance sources for many investors. As a result, bank loans decreased twice as much as P2P loans, especially at the start of the crisis. This finding is supported by Najaf et al. (Citation2022), who illustrate that during the pandemic, online P2P platforms attracted many borrowers with little or no access to financial sources. Even when traditional banks offered online loan services, only a few had a verified lending application with the actual presence of investors. Because of this, innovative platforms became an accessible credit option for entrepreneurs, especially during the COVID-19 pandemic. From the perspective of traditional finance sources, Zhao et al.’s (Zhao et al., Citation2021) study demonstrated that the lending behaviour of banks in the post-COVID-19 period did not vary for SEBs that already had a strong relationship with their financers. For businesses that had already gained banks’ credit and trust before the pandemic, the impact on their accessibility and relationship would be logically diminishing even during the lockdown. Therefore, the COVID-19 period may have highlighted the importance of maintaining a trustworthy relationship towards banks, thus mitigating the unfavourable impacts caused by pandemics.

In another vein, there is a lack of studies that examine the impact of using innovative sources of finance on the SEBs of the Gulf Cooperation Council (GCC), even though SEBs are one of the main engines of the Arab economy. A few studies have considered the nexus between financial innovation and the SEBs in the Arab region. Khan et al. (Citation2021) suggest that governments play a noticeable mediative role between SEBs and innovations. This can be through regulation, as Abdeldayem and Aldulaimi (Citation2022) have illustrated that the lack of regulation of crowdfunding as an innovative source of fund has hindered using this source in the GCC. Still, countries in the Gulf region are taking steps toward establishing well-regulated financial innovations that boost SEBs towards success. For example, the UAE’s central bank manages lending-based crowdfunding, and Bahrain is following accordingly (Abdeldayem & Aldulaimi, Citation2022). In general, this is evidence to prove that governments are introducing some financial alternatives to narrow the gap. Not only that, but the Islamic countries of the GCC are planning to establish a collaborative system between Islamic banks, fintech players and SEBs. They have strong potential to become leaders in this specific core, especially given the fact that some Islamic operations can be more practical when aligning with innovative sources, such as musharakah contracts under peer-to-peer deals (Sa’ad et al., Citation2019). However, no previous studies have examined the impact of using innovative sources of finance on the performance of SEBs. The current paper is addressing this gap by examining the impact of using innovative sources of finance on the financial, marketing and internal business and development performance of SBEs in Qatar.

2.3. Financing Choices of SEBs

The literature examines different factors that influence the financing choices of SEBs. Many funding sources are only accessible for SEBs with the existence of certain criteria. Even in the case of acquiring funds from innovative sources such as crowdfunding, this is highly affected by the features of the SEBs (Eldridge et al., Citation2019). In other words, the decision of how and whether to be financed varies according to the firm’s characteristics, such as the business age and life cycle, the owner’s gender, the industry, size, geographical location, the entrepreneur’s risk appetite, information and collateral availability, and, most importantly, the ease and accessibility of businesses to alternative sources of finance (Berger & Udell, Citation1998; La Rocca et al., Citation2011). The idea that the company’s age affects its capital structure and financing decisions is supported by the pecking order theory. SBEs in the introduction stage suffer from a lack of information and tracking history (Watson & Wilson, Citation2002). Conversely, mature entrepreneurs who have a successful history of being financed and have efficiently utilized those funds are more likely to convince funding providers to support their business again (Mamonov & Malaga, Citation2020).

Scherr et al. (Citation1993) argue that personal attributes could affect someone’s risk preference, which in turn affects the type of funds. For instance, Hendon and Bell (Citation2011) mention that gender could play a role in financing decisions. Female entrepreneurs usually avoid dependence on external funds and tend to rely more on internal finance. In contrast, Scherr et al. (Citation1993) argue that males hold more debt because women are more risk-averse or because there might be discrimination in loan decisions. However, Mamonov and Malaga (Citation2020) have observed that equity-funding platforms do not discriminate loan granting based on gender.

Scherr et al. (Citation1993) also suggest that industry type plays an essential role in debt position, as more loans can be given to some industries and not others. Correspondingly, Michaelas et al. (Citation1999) and MacKay and Phillips (Citation2005) state that SBEs’ industry affects funding preferences and capital structure. The entrepreneur’s point of view of risks in certain industries affects their financing options and decisions, which may limit new businesses’ usage of external finance sources due to the high risk to which the entrepreneur will be exposed. Some SEBs have vague plans, especially at the early stages, but accessing banks without a clear plan or realistic revenue expectation is challenging if not impossible. Furthermore, Erdogan (Citation2018) argues that high-volatility businesses, particularly in sales, would reasonably face more difficulties in obtaining capital. For example, food industries have easier access to funds due to their stable circumstances. In a similar way, many SEBs in the manufacturing industries are able to convince loan providers if their operations are backed up by experienced consultants and a well-prepared business plan. This conversely increases the role of banks in funding new SBEs in certain industries (Scholtens, Citation1999). In addition, investors may avoid supporting micro businesses due to the inability of measuring their success, especially in certain industries. Vasilescu (Citation2014) states that such firms usually produce intangible products, which makes it much more difficult for money contributors to assess their monetary value. The financial decision of entrepreneurs therefore does not rely on a single factor. Finance providers are also hesitant to fund SEBs operating in industries that are highly affected by seasonal downturns. Pedauga et al. (Citation2022) found that SEBs in tourism and transportation industries suffered more than SEBs working in other industries during the COVID-19 pandemic. Thus, businesses interact differently if they are operating in industries that are more exposed to external multidimensional shocks. Erdogan (Citation2018) summarizes by suggesting that when firms are not generating sufficient sales revenue, their lending capacity will be negatively affected.

In terms of size, SEBs receive less financing compared to large firms, whether through bank loans or through different lines of credit (Abraham & Schmukler, Citation2017). Due to this, entrepreneurs tend to rely on their own savings as a foundation for their start-up stage (Storey, Citation1994). As the firm grows, the ability to engage with banks for finance will increase. Petersen and Rajan (Citation1994) introduced evidence to demonstrate that the engagement with credit institutions is nearly twice as much for large firms in comparison to SEBs. This confirms that most enterprises that face difficulties are those that are just being launched and at their early stages. Uncertainty may be the leading issue facing SEBs, as creditors are discouraged from lending to them because these companies do not generate information about their performance, as opposed to what other large and established businesses are used to (Berger & Udell, Citation1998). SEBs would therefore be more financially constrained (Beck et al., Citation2008). Even though there are multiple options for external equity funding, these are limited and cannot be easily obtained by these types of enterprises. This is called the equity gap, which is the main reason leading SEBs to rely on debt financing rather than external equity financing (Fatoki, Citation2014). Still, it is not that easy for small enterprises to even access debt. The problem spreads not only from a monetary perspective, as the contribution of diverse supporters can be utilized in many areas. In addition to finance, financial bodies provide other organizational services that can help SEBs along their path, including monitoring, bargaining and improving their legal agreements—the list is infinite (Park et al., Citation2019). An additional obstacle that increases funding constraints is the difference in rates, premiums and collateral applied to SEBs in comparison to large firms, which receive lower rates when acquiring loans from banks. This gap in the cost of finance is usually expected, as finance providers compensate for the risk to which they might be exposed when funding small enterprises (Wellalage & Fernandez, Citation2019), and such issues lead to an increase in the banks’ administrative rigidity when lending to small businesses, startups and entrepreneurs (Rossi, Citation2014).

In the GCC countries, the small-business-financing problem is even worse. Loans provided to SEBs by banks in GCC countries comprise only 2% of the whole lending system, while in non-GCC countries the share of SEB loans is 13% (Beck et al., Citation2008). Additionally, because regulations do not provide enough protection for small business lenders, investors and creditors are less encouraged to lend to SEBs. It would be effective if henceforth governments put some effort into finding the best solutions to finance newly launched enterprises, as their contribution to the economy is major and essential to all sides. Specifically, the most important factor on which to focus is providing information. Through this, many issues could be solved, thus reducing the financial barriers and constraints facing small, start up, and entrepreneurship businesses. After all, the method of accessing funds for recently introduced businesses can strongly affect their performance in terms of achieving their marketing, organizational and financial objectives (Harash et al., Citation2014). Firms perform better when their path towards being financed is supported, eased and facilitated (Harash et al., Citation2014).

To summarize, a significant proportion of the literature examines the challenges faced by SEBs in obtaining funds from traditional sources of finance and how these affect the businesses’ success (e.g., Aiello et al., Citation2020; Baker et al., Citation2020; Donald, Citation2020; Motta & Sharma, Citation2020; Oláh et al., Citation2019; Park et al., Citation2019; Rupeika-Apoga & Saksonova, Citation2018). A second area of the literature demonstrates the impact of financial access and sources on the SBEs’ success and growth, although very few papers in the literature have investigated the impact of finance on SBEs’ performance (Fraser et al., Citation2105; Chemmanur et al., Citation2011; Cowling et al., Citation2015; Puri & Zarutskie, Citation2012; Rosenbusch et al., Citation2013). However, there is a lack of such studies in the context of developing markets. Even, limited research directly examines the link between the sources of finance and the three dimensions of performance; namely financial, marketing and internal business and development performances. The third strand of the literature examines the impact of using innovative sources of finance on limited measures of performance (e.g., Ashta & Assadi, Citation2009; Effiom & Edet, Citation2020; Eldridge et al., Citation2019; Qin et al., Citation2016). However, there are no explicit attempts to examine such relationships in the emerging market or even to consider the three dimensions of performance in the developed market. This paper will address this gap in the literature by examining the impact of using different sources of finance (traditional and innovative) on the three dimensions of performance in Qatar as an emerging market.

This paper considers the importance of SEBs in diversifying Qatar’s economy, the current challenges that are faced in financing SEBs and the impact of these challenges on their performance. We therefore add to the literature by being the first research to investigate the impact of using innovative and traditional sources of finance on the different performance dimensions of SEBs. By doing this, we position our work on three strands of literature. We build on the accumulated literature on small business finance and its challenges (e.g., Beck et al., Citation2008; Harash et al., Citation2014; Park et al., Citation2019; Rossi, Citation2014; Wellalage & Fernandez, Citation2019). We also utilize the literature on small business performance (e.g., Berger & Udell, Citation1998; Harash et al., Citation2014). Finally, we extend the literature that examines innovative sources of finance and their impact on small businesses by introducing evidence for the case of Qatar (see, Cumming et al., Citation2021; Eldridge et al., Citation2019; Estrin et al., Citation2018; Paschen, Citation2017; Stanko & Henard, Citation2016).

3. Methodology

3.1. Conceptual Assumptions and Hypothesis Development

The purpose of this paper is to examine the impact of new and traditional types and sources of financing on SEBs in Qatar. Following the work of Elbanna (Citation2012), Jordi (Citation2010), and Eccles and Pyburn (Citation1992), we use (Kaplan & Norton, Citation1992) balanced scorecard measures to capture the firm (organizational) performance. We expressed our dependent variable, “Firm’s performance”, as a construct of three dimensions: financial, internal business and development (I&D, hereafter), and marketing performance. Growth rate of revenue, financial soundness and growth rate of sales were used to measure the financial dimension, while Internal business and development performance was measured by efficiency of operations, use of organizational assets, quality of products and services, employee satisfaction, product and service development, employee development, employee talent and quality of management. Finally, customer satisfaction and social responsibilities were used to measure the marketing perspective.

We built up our hypotheses according to the theories and empirical findings in the literature review. For example, most studies pointed to entrepreneurs’ preference for equity financing, even though accessing debt is still available (De Kort & Vermeulen, Citation2010). This is due to the lack of a strict regulatory system to control the interest rates imposed on SEBs’ loans, even if they are lent by government banks (Wellalage & Fernandez, Citation2019). Thus, it is reasonable that debts would have a negative impact on SEBs’ financial situation in comparison to equity. While debt would be expected to affect the financial outlook negatively, the impacts on marketing and internal business and development perspectives are still unclear, hence our first hypothesis focused only on the financial aspect:

H1: Debt financing sources are negatively related to SEBs’ financial performance in the context of Qatar.

Baker et al. (Citation2020) and De Kort and Vermeulen (Citation2010) argue that equity finance has a positive influence on the performance of SEBs, as internal equity would be a safer choice for businesses in their early stages instead of being liable. In this context, equity funding—especially the informal type—is preferable for SEBs in this phase, with sources including families, friends, venture capital and other unofficial types, as it mitigates some of the risks (De Kort & Vermeulen, Citation2010; Vasilescu, Citation2014). In a similar manner to debts, choice of equity also has an unclear impact on non-financial aspects of SEBs’ performance; therefore our second hypothesis focused on the impact of equity choice on the financial perspective.

H2: Equity financing sources are positively related to SEBs’ financial performance in the context of Qatar.

In another context, Harash et al. (Citation2014) state that the ease and accessibility of funds affects all aspects of performances. Henceforth, we would expect to find a positive relationship between the ease and accessibility of funds and other performance measures. Having diversity in gathering funds would always be the best choice for any business, because accessing a variety of sources would increase the opportunity to benefit from the best features of every source. For example, collecting funds from diversified sources would lower the risks to which businesses are exposed from each source. Because internal equity is sometime insufficient, entrepreneurs could choose to allow contributions from families, friends, investors, creditors and even innovations (Morse, Citation2015); this diversification of financial sources could lower financial costs and risk, ultimately leading to enhanced marketing and internal business and development performance. In this particular field, easy access to such sources improves development, ideas, employees, customer numbers and loyalty (Eldridge et al., Citation2019), as well as providing opportunities and equality for everyone to contribute, regardless of their demographics and geographic characteristics (Fleming & Sorenson, Citation2016), consequently having a noticeable effect on organizational and marketing perspectives.

Likewise, the effective support of governments would be expected to have the same positive influence on SEBs’ overall performance, as a lack of supportive governmental loaning programmes can affect the quality and quantity of SEBs (Lee, Citation2018). This could be explained not only in terms of smoothing the path financially for such businesses, through factors like monitoring interest rates (Wellalage & Fernandez, Citation2019), but also in terms of improving their resources and creating an appropriate environment to boost their growth (Park et al., Citation2019; Ullah, Citation2020). In addition, the lack of collateral would logically be expected to have an undesirable consequence for SEBs in terms of their approachability towards being financed. Scherr et al. (Citation1993) and Hall and Lerner (Citation2010) note that when businesses are at their introductory stage, it is common not to be capable of offering worthy collateral, and thus financing agencies find their contributions riskier, restricting their involvement with SEBs. Based on this discussion, our third hypothesis was as follows:

H3: Ease and availability of financing sources are positively related to all performance perspectives of SEBs in the context of Qatar.

Lastly, funding through new, innovative sources has positive outcomes for SEBs in terms of having more diverse funds, enhancing financial performance (Morse, Citation2015) and thus marketing and organizational performance as well (Eldridge et al., Citation2019). Using innovative sources of finance such as online platforms, which include information and profiles for businesses, creates strong links for SEBs with ideas, professionals, other businesses and customers, which should improve non-monetary outcomes as well as the financial performance of SEBs.

H4: Innovative types and sources of financing are positively related to all performance perspectives of SEBs in the context of Qatar.

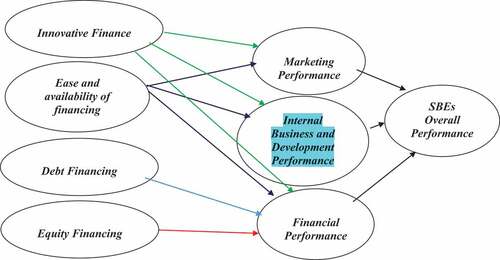

Figure displays a summary of the hypotheses and Table portrays the independent variable measurements and their expected signs.

Figure 1. Study Framework.

Table 1. Variables with Expected Sign of Influence on Businesses Performance

This graph shows the main framework of the study, including dependent and independent variables, based on the hypotheses.

3.2. Sample and Tool Description

To examine the impact of sources of financing on SEBs in Qatar, questionnaires and a quantitative approach were used. Questionnaires outperform other data-collection tools as they can avoid prejudice because the respondent completes such a questionnaire in private, devoid of any intrusion (Creswell, Citation2014). Moreover, it guarantees a consistent questioning style, which in turn enhances the compatibility of the responses. However, the initial phase employed in-depth interviews with the main stakeholders (finance providers and other entrepreneurship-supporting organizations in Qatar, e.g., Qatar Development Bank, Qatar Business Incubation Center, etc.) as an exploratory study. After the in-depth interviews with people from both positions—SEBs and the main finance providers in the country—four academics and five SBE owners examined the questions on the questionnaire. We utilized the outcomes of the in-depth interviews, in addition to the academics and experts’ feedback, to design and refine our questionnaire.

The research aimed to determine how financing decision influences the overall performance of SBEs from various business perspectives: financial, marketing and internal business and development. Therefore, the questionnaire was divided into two main sections in addition to the demographic data. In light of the literature (Elbanna, Citation2012; Kaplan & Norton,, Citation1992), we expressed our dependent variable, “Firm’s performance”, as a construct of three dimensions of performance: financial, internal business and development, and marketing performance. The growth rate of revenue, financial soundness and growth rate of sales were used to measure financial performance. Internal business and development performance was measured through efficiency of operations, use of organizational assets, quality of products/services, employee satisfaction, product and service development, employee development, employee talent and quality of management. Finally, customer satisfaction and social responsibilities were used to measure marketing performance. Every single dimension was allocated one question, leading to 13 other questions, the themes of which are illustrated in Table . A five-point Likert scale was applied as a data-collection instrument. A Likert scale is a rating scale that requires the subject to indicate his or her degree of agreement or disagreement with a statement. It attempts to quantify subjective information, and respondents indicate along a continuum where their particular attitude resides. The survey questions, adopted from the literature, has a five-point Likert scale ranging from 1—strongly disagree to 5—strongly agree. The reliability statistics were over 60%, which means that all the questions were reliable. Questions were then checked together to obtain an Alpha of 75.3%. This implies that the conclusions drawn from our sample are reliable.

According to Qatar Development Bank (Citation2020), Qatar has around 24,500 SEBs. Data were collected from companies operating in the Qatari Small sector that listed and registered in the Ministry of Commerce and Industry (MOCI) in Qatar (2019–2020). The research sample was drawn from SEB owners and managers through a random selection of 300 Qatari SEBs invited to participate in the work represent. The sampling frame covers the entire country. We targeted the business owners or the mangers. We followed a delivery and collection technique following the work of Abou Aish et al. (Citation2003) and Elbanna (Citation2012). All 300 SEBs in the sampling frame were contacted at least once. Follow-up calls and visits were used to encourage respondents to reply. From the 300 questionnaires, which were dropped off in person, we ended up with 161 valid questionnaires (a final response rate of 53.6%). Every firm had a questionnaire answered by either the owner or entrepreneur (79%) or a director (21%). Seventy-one per cent of the respondents were male and 29% were female. Seventy-three per cent of them had a bachelor’s degree or above, reflecting a high level of education, which has been linked in the literature to the acceptance of innovation. Further, 75% of our sampled SEBs were private firms, 21% were joint ventures, 1% were from the public sector and 3% fitted into the “other” category. Forty per cent of the businesses from our sample had between ten and 50 employees, while 27% employed five to ten people, 27% had 50 or more employees and 6% had less than five employees. This may indicate that SBEs are labour-intensive. Thirty-eight per cent of our sample were new firms aged from one to three years, while 19% were less than one year old, 21% were between three and five years old and 22% were five years old or more. This means that our sample was dominated with young SEBs. Our sample contained SEBs from different sectors: 43% were from the service sector, 33% were from the consumer goods sector and only 6% and 5% were from the information technology and industrial sectors, respectively. The remaining 13% belonged to other industries.

3.3. Modelling

Based on the discussion above and the proposed hypotheses, we ran three different ordinary least squares (OLS) regression models to capture the impact of our independent variables on the three different dimensions of performance (Equationequations 1(1)

(1) to 3). In addition, we investigated the impact of our dependent variable on the overall performance of SEBs in Equationequation 4

(4)

(4) :

Note:

FPi is financial performance, which is a vector for growth rate of revenue, financial soundness and growth rate of sales. MPi represents the marketing performance, where it is a vector of customer satisfaction and social responsibilities. IDPi denotes the internal business and development performance vector, including efficiency of operations, use of organizational assets, quality and development of products and services, and employees’ satisfaction, talent and development, in addition to quality management. is the firm’s performance, which is an aggregate of the three dimensions (financial performance, internal business and development performance, and marketing performance). In all equations, (A) is equal and comprehensively exemplified with its expected impact sign on performance. All independent variables are defined in Table .

4. Empirical Analysis

4.1. Sources of Finance and the Three Aspects of Performance

Table presents the findings of regressing different performance aspects on our independent variables. Our models show that 20.3% of variations were found in financial performance, 15.5% of explained disparities were in marketing performance, and 22.6 per cent of internal business and development performance variations could be explained by the selected independent variables in the model (A1–A13). Our findings suggest a strong positive relationship between the accessibility of funds and the financial performance of SEBs. This result is consistent with a strand of the literature suggesting that the ease and availability of different opportunities to access sources of finance would affect SEBs’ overall performance positively and could push it to another level of success (Park et al., Citation2019; Ullah, Citation2020). Accessing finance easily allows business owners to benefit from each source’s features and diversify their capital structure (Morse, Citation2015). In addition, the results suggest insignificant positive relationships between accessibility of funds and both marketing and internal business and development performance. Eldridge et al. (Citation2019) insist on the positive influence of having easy access to funds, as this could allow for the international contribution of ideas, employees, customers and others aspects, yet the impact on organizational and marketing performance did not seem not to be sufficiently significant to prove this theory.

Table 2. Sources of Finance and the Three Aspects of Performance

Surprisingly, the findings in Table demonstrate a significant negative association between governmental financial support and internal business and development performance. Although the result was expected to be the opposite, this may be explained by the fact that the expected results were based upon the ideal “gold-plated” scenario of governments smoothing the way for SEBs. In reality, depending on governmental support could negatively affect internal business and development performance, as the appropriate environment assumed by Park et al. (Citation2019) and Ullah (Citation2020) may not actually exist. In addition, Lee (Citation2018) suggests that the absence of suitable, structured lending programmes for government-supported SBEs might have a negative impact on the quality of the internal business and development performance of SEBs. Another explanation for the negative association between governmental support and internal business and development performance is the fact that most governmentally supported SEBs are new businesses that just have been launched, so logically they have less experience and their organizational structure is still in its development stage.

Our results also suggest that a lack of collateral marginally affects Qatari SEBs’ marketing and internal business and development performance. These results are aligned with the literature, as they reflect the difficulty of SEBs in obtaining funds through external equity providers, due to their lack of information and collateral (Hall & Lerner, Citation2010; Harvie et al., Citation2013; Scherr et al., Citation1993). Therefore, lacking worthy—or any—collateral limits the accessibility of funds and respectively affects all performance aspects of SEBs.

Furthermore, our findings imply that using more debt in financing expansion is associated with undesirable financial performance. This result contradicts the work of Astebro and Bernhardt (Åstebro & Bernhardt, Citation2003) and Fatoki (Citation2014), who argue that, according to the pecking order theory and since equity providers’ risk compensations are costly, SEBs would prefer debt over equity. This is not the case with Qatari SEBs, as our results show that Qatari SEBs opting for debt is associated with poor performance. Our reported negative association between debt and financial performance may be because entrepreneurs choose equity over debt even if access to debt is available, not preferring loans due to the weak regulatory system and uncontrolled interest rates that limit the loaning processes (De Kort & Vermeulen, Citation2010).

Interestingly, our findings suggest that non-traditional sources of finance—crowdfunding and business angels—can have negative impacts on different dimensions of performance. Specifically, we found a negative relationship between using business angels and SEBs’ financial performance. Furthermore, we found a significant negative impact of using crowdfunding on both marketing and internal business and development performance, while the impact on the financial perspective was negative yet non-significant. It is reasonable to assume that SEB owners believe that firms should turn to using innovative sources of finance when they are suffering from poor performance or when they lack sufficient traditional sources. Even though the results were inconsistent with what had been assumed in the hypothesis, the result was consistent with the research of Eldridge et al. (Citation2019), who suggest that using crowdfunding might have negative impacts on some non-monetary factors. Interestingly, non-traditional debt, like peer-to-peer finance, demonstrated a marginal positive impact on marketing performance. Our results align with those of Morse (Citation2015), who suggested that P2P benefits both investors and borrowers, as well as confirming the assumed hypothesis of the positive influence of innovative sources of finance on different SEBs’ multiple aspects of performance. Confusingly, the issue is unclear in the Qatari market in terms of small enterprises, as preferences did not align on a single method of obtaining funds, encouraging the argument of De Kort and Vermeulen (Citation2010), which suggests that entrepreneurs try to find distinct routes to finance their initiatives, whether weak or strong ties, debt or equity. Still, our findings cannot confirm a case of preferring debt over external equity, nor the effect of innovative sources of finance on SEBs’ performance, as each type of fund has its own impact and can act as either a benefit or a drawback for the business if it has not been chosen properly.

4.2. Sources of Finance and the Overall Aspects of Performance

In this section, we extend our analysis to examine the relationship between overall performance (as a construct of financial, marketing and internal business and development performance) and the correspondent affecting variables illustrated in Table . We began by running the model for Equationequation 4(4)

(4) , previously labelled M1. However, based on the regression results of M1 and the Wald test for redundant variables, we applied a restrictive model, M2:

Note:

is the firm performance which aggregates the three dimensions (financial, internal business and development, and marketing performance).

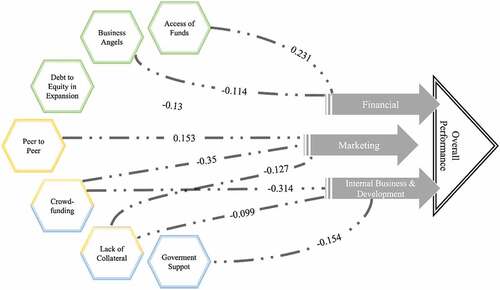

According to the regression results of M1, 14.6% of the variation in SEBs’ overall performance was explained by the independent variables A1 to A13. The regression results for M2 implied that 15.9% of the variation in aggregate performance was derived from four main factors, namely access to funds, governmental support, crowdfunding and lack of collateral.

Firstly, our results show that access to funds positively affected the overall performance for SEBs in Qatar. However, we cannot confirm the expected relationship discussed in the literature, that the flexibility of accessing sources of finance enhances the performance of entrepreneurs. Secondly, our results suggest that government support for small businesses might be marginally harmful for aggregate performance. Therefore, this relationship conflicts with the prediction in the literature, although it is not significant due to the restricted model (M2). Thirdly, crowdfunding in M1 had a positive impact on Qatari businesses performance, although this impact was converted to negative after omitting the unrelated variables as shown in the M2 regression results, due to removing the multicollinearity problem of other variables. Moreover, this finding could be considered reasonable, as the cost of hiring an intermediate platform to obtain funds from the “crowd” is high, which in fact aligns with the literature (Qin et al., Citation2016). Finally, a lack of collateral was found to negatively impact SEBs. Logically, this can be explained because creditors probably do not have the courage to risk their money by lending to start-ups or new businesses that do not provide worthy collateral. Figure below summarizes the significant results reported in Tables .

Figure 2. Results Summary.

Table 3. Sources of Finance and the Overall Aspects of Performance

This graph displays the main results reported in Table and Table .

5. Implications, Contributions and Limitations

Our findings suggest that the availability of access to distinct sources of funds enhances the financial performance of SEBs. Moreover, there was found to be a negative impact of governmental support on internal business and development performance specifically. Governmental influence is usually accompanied by intervention on one hand and support on the other, which could lead SEBs to become more dependent and thus ignore opportunities to enhance their internal business efficiency. Unexpectedly, crowdfunding finance was found to have a negative impact on the non-financial performance aspects of SEBs. Again, this may suggest that less-efficient SEBs, in terms of their internal business and development and marketing performance, are more active in obtaining both governmental support and crowdfunding, as they may be not eligible for other sources of finance. Furthermore, results showed that Qatari SEBs prefer equity financing instead of debt, in all its forms—traditional and new—and in all situations, both introduction and expansion. Consistent with the findings of Schmalz et al. (Citation2017) requiring collateral from businesses that are newly launched could logically affect their performance negatively, especially the internal business and development, and marketing aspects, as well as constrain their growth.

The findings and implications of this research could fill some gaps, as no work has been carried out to investigate the impact of financing decisions on the performance of SEBs in Qatar. Thus, this research explains the preference of Qatari businesses towards certain sources of finance over others. In addition, no previous research has investigated innovative finance methods and applicability in the Qatari context, while this study aimed to compare the new, innovative methods with conventional lending models and consider their impact on different performance perspectives. This was investigated because there is a lack of research exploring the effects of alternative funding sources on the performance of SEBs (Block et al., Citation2018). Moreover, it seems that previous studies have only focused on the availability of venture capital and crowdfunding as innovative sources specifically, while ignoring other alternative finance vehicles like business angels, while entrepreneurs usually utilize several financing sources and seek to diversify among them, even the traditional sources.

However, we also need to report two limitations of our research. First, the small number of observations does not allow us to consider the market sector’s impact on the relationship between sources of finance and performance. The second limitation is that our measures were based on the perceptions of SBE owners and managers of their firms’ performance. These two limitations could be avenues for future study.

6. Conclusion

The purpose of this research was to test different and alternative sources of finance and their impact on performance perspectives in the context of SEBs in Qatar. By using a sample of 161 businesses, we concluded that each type and source of finance has its own benefits and drawbacks, as accessing different types of funds could boost the business on one hand but could also harm it on the other. Examining the impact of alternative sources and types of finance on the performance dimensions uncovered some different and unexpected results in comparison to the findings in the literature. For example, we found that the governmental impact could boost financial but not internal business and development or marketing performance. Another unexpected result was the preference of Qatari SEBs towards equity instead of debt, even though this is considered a more expensive source. This may be because of the lack of access to debit; Blackmon (Citation2019) suggests raising debt limits for SEBs who lack access to equity sources.

In addition, innovative sources of finance can boost SEBs’ financials, but they could also harm internal business and development, and marketing performance. This may be because most firms that are looking for innovative, alternative sources of finance are firms that have poor internal business, and marketing performance and suffer difficulties in attracting traditional finance.

Other significant variables, however, were consistent with previous literature. For instance, having a diversity and ease of accessing various sources of finance would definitely improve any business and contribute to its growth on all sides. In addition, certain new sources of funds can be expected to influence positively if they are available and efficiently used. Therefore, the hypotheses that direct relationships can occur between types and sources of finance and firms’ financial, marketing and internal business and development dimensions can be confirmed, in which the relationships and influences can be both positive and negative, according to the source of finance decision and the impacted perspective. Finally, it can be concluded that if they consider diverse sources of funds, taking into account the new, innovative techniques and various affecting factors, the performance of small, start up and entrepreneurship businesses in Qatar can improve greatly and thus contribute to the economy.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

Notes on contributors

Mohammed M. Elgammal

Mohammed Elgammal is associate professor of Finance in Qatar University, before that worked at University of Westminster, University of Aberdeen, East London University, and Menoufia University. Elgammal is an active researcher in the area of expected return modelling with particular focus on macroeconomic variable and he has published more than 30 papers in international journals. He has been awarded many grants from prestigious institutions, including the Egyptian government, the European Economic Research Council, NPRP, UREP funded from QNRF and Qatar University.

Anas A. Al Bakri

Anas A. Al-Bakri is working with Qatar University as Assistant Professor of Management - Department of Management and Marketing, College of Business and Economics. He received his PhD of Business (Management) 2011, University of Southern Queensland (USQ), Australia. Research Area: Entrepreneurship performance and evaluation, E-business, E-commerce, Business innovation and CSR. Published and submitted on these research topics at the international conferences proceeding and peer-reviewed journals.

AlDana Y. AlJanahi

AlDana AlJanahi is a BSc honor degree holder in Finance and Economics from Qatar University. Her research interests focus on small businesses, financial innovations, as well as behavioral finance and economics. Currently, she is acting for the role of Budgeting Analyst in Qatar Gas Operating Company.

References

- Abdeldayem, M. M., & Aldulaimi, S. H. (2022). Predicting crowdfunding economic success in the gulf cooperation council. International Journal of Engineering Business Management, 14, 18479790221074477. https://doi.org/10.1177/18479790221074477

- Abou Aish, E. M., Ennew, C. T., & McKechnie, S. A. (2003). A cross-cultural perspective on the role of branding in financial services: The Small Business Market. Journal of Marketing Management, 19(9–10), 1021–23. https://doi.org/10.1080/0267257X.2003.9728249

- Abraham, F., Schmukler, S., & Abraham, F., Addressing the SME Finance Problem (October 1, 2017). World Bank Research and Policy Briefs No. 120333, Available at SSRN: https://ssrn.com/abstract=3249560

- Ahlers, G. K., Cumming, D., Günther, C., & Schweizer, D. (2015). Signaling in equity crowdfunding. Entrepreneurship Theory and Practice, 39(4), 955–980. https://doi.org/10.1111/etap.12157

- Ahmed, S., & Cozzarin, B. P. (2009). Start-up funding sources and biotechnology firm growth. Applied Economics Letters, 16(13), 1341–1345. https://doi.org/10.1080/13504850701367338

- Aiello, F., Bonanno, G., & Rossi, S. P. (2020). How firms finance innovation. Further empirics from European SMEs. Metroeconomica, 71(4), 689–714. https://doi.org/10.1111/meca.12298

- Ashta, A., & Assadi, D. (2009). Do social cause and social technology meet? Impact of web 2.0 technologies on peer-to-peer lending transactions. Cahiers du CEREN, 29, 177–192. https://papers.ssrn.com/sol3/papers.cfm?abstract_id=1518637

- Åstebro, T., & Bernhardt, I. (2003). Start-up financing, owner characteristics, and survival. Journal of Economics and Business, 55(4), 303–319. https://doi.org/10.1016/S0148-6195(03)00029-8

- Baker, H. K., Kumar, S., & Rao, P. (2020). Financing preferences and practices of Indian SMEs. Global Finance Journal, 43, 100388. https://doi.org/10.1016/j.gfj.2017.10.003

- Basha, S. A., Elgammal, M. M., & Abuzayed, B. M. (2021). Online peer-to-peer lending: A review of the literature. Electronic Commerce Research and Applications, 48, 101069. https://doi.org/10.1016/j.elerap.2021.101069

- Beck, T., Demirgüç-Kunt, A., & Maksimovic, V. (2008). Financing patterns around the world: Are small firms different? Journal of Financial Economics, 89(3), 467–487. https://doi.org/10.1016/j.jfineco.2007.10.005

- Berger, A. N., & Udell, G. F. (1998). The economics of small business finance: The roles of private equity and debt markets in the financial growth cycle. J. Bank. Finance, 22(6–8), 613–673. https://doi.org/10.1016/S0378-4266(98)00038-7

- Blackmon, M. C. (2019). Revising the Debt Limit for” Small Business Debtors”: The Legislative Half-Measure of the Small Business Reorganization Act. Brook. J. Corp. Fin. & Com. L, 14, 339. https://heinonline.org/HOL/Page?handle=hein.journals/broojcfc14&div=21&g_sent=1&casa_token=aoRRCLu5jaUAAAAA:ICHKu7YfHl3Pyh2V4gsvOjEmBZ1MohwhTz4nldIZ-1_lhDxFkKxc_Kw4-LSqw72nK2p5VXnXFQ&collection=journals

- Block, J. H., Colombo, M. G., Cumming, D. J., & Vismara, S. (2018). New players in entrepreneurial finance and why they are there. Small Business Economics, 50(2), 239–250. https://doi.org/10.1007/s11187-016-9826-6

- Block, J. H., Fisch, C. O., & Van Praag, M. (2017). The Schumpeterian entrepreneur: A review of the empirical evidence on the antecedents, behaviour and consequences of innovative entrepreneurship. Industry and Innovation, 24(1), 61–95. https://doi.org/10.1080/13662716.2016.1216397

- Block, J. H., Groh, A., Hornuf, L. (2021). The entrepreneurial finance markets of the future: A comparison of crowdfunding and initial coin offerings. Small Bus. Econ., 57, 865–882. https://doi.org/10.1007/s11187-020-00330-2

- Bodlaj, M., Kadic-Maglajlic, S., & Vida, I. (2020). Disentangling the impact of different innovation types, financial constraints and geographic diversification on SMEs’ export growth. Journal of Business Research, 108, 466–475. https://doi.org/10.1016/j.jbusres.2018.10.043

- Boucly, Q., Sraer, D., & Thesmar, D. (2011). Growth LBOs. Journal of Financial Economics, 102(2), 432–453. https://doi.org/10.1016/j.jfineco.2011.05.014

- Brown, J. R., & Haynes, G. W. (2009). How strong is the link between internal finance and small firm growth? Evidence from the survey of small business finances. Proceedings of the United States Association for Small Business and Entrepreneurship (p. 96). United States Association for Small Business and Entrepreneurship.

- Bruton, G., Khavul, S., Siegel, D., & Wright, M. (2015). New financial alternatives in seeding entrepreneurship: Microfinance, crowdfunding, and peer‐to‐peer innovations. Entrepreneurship Theory and Practice, 39(1), 9–26. https://doi.org/10.1111/etap.12143

- Carpenter, R. E., & Petersen, B. C. (2002). Is the growth of small firms constrained by internal finance? Review of Economics and Statistics, 84(2), 298–309. https://doi.org/10.1162/003465302317411541

- Chemmanur, T. J., Krishnan, K., & Nandy, D. K. (2011). How does venture capital financing improve efficiency in private firms? A look beneath the surface. Review of Financial Studies, 24(12), 4037–4090. https://doi.org/10.1093/rfs/hhr096

- Cho, H., Park, J. Y., & Sung, C. S. (2019). The study on the difference in corporate performance and employment outcomes according to the results of equity-based crowdfunding investment. Journal of Open Innovation: Technology, Market, and Complexity, 5(4), 83. https://doi.org/10.3390/joitmc5040083

- Conlin, M. (1999). Peer group micro-lending programs in Canada and the United States. Journal of Development Economics, 60(1), 249–269. https://doi.org/10.1016/S0304-3878(99)00043-7

- Cowling, M., Liu, W., Ledger, A., & Zhang, N. (2015). What really happens to small and medium-sized enterprises in a global economic recession? UK evidence on sales and job dynamics. International Small Business Journal, 33(5), 488–513. https://doi.org/10.1177/0266242613512513

- Creswell, J. W. (2014). A concise introduction to mixed methods research. Sage Publications.

- Cumming, D. J., Martinez-Salgueiro, A., & Reardon, R. S. (2022). COVID-19 bust, policy response, and rebound: Equity crowdfunding and P2P versus banks. The Journal of Technology Transfer, 47, 1825–1846. https://doi.org/10.1007/s10961-021-09899-6

- Cumming, D. J., Vanacker, T., & Zahra, S. A. (2021). Equity crowdfunding and governance: Toward an integrative model and research agenda. Academy of Management Perspectives, 35(1), 69–95. https://doi.org/10.5465/amp.2017.0208

- De Kort, M. J., & Vermeulen, P. A. (2010). Entrepreneurial decision-makers and the use of biases and heuristics. In V. Patrick & P. L. Curseu (Eds.), Entrepreneurial Strategic Decision-Making A Cognitive Perspective (pp. 123–134). Edward Elgar Limited.

- Donald, D. C. (2020). Smart precision finance for small businesses funding. In European Business Organization Law Review (pp. 1–19). https://doi.org/10.1007/s40804-020-00180-1.

- Eccles, R. G., & Pyburn, P. J. (1992). Creating a comprehensive system to measure performance. Strategic Finance, 74(4), 41. https://www.proquest.com/docview/229747276?pq-origsite=gscholar&fromopenview=true

- Effiom, L., & Edet, S. E. (2020). Financial innovation and the performance of small and medium scale enterprises in Nigeria. Journal of Small Business & Entrepreneurship, 1–34. https://doi.org/10.1080/08276331.2020.1779559

- Elbanna, S. (2012). Slack, planning and organizational performance: Evidence from the Arab Middle East. European Management Review, 9(2), 99–115. https://doi.org/10.1111/j.1740-4762.2012.01028.x

- Eldridge, D., Nisar, T. M., & Torchia, M. (2019). What impact does equity crowdfunding have on SME innovation and growth? An empirical study. In Small Business Economics (pp. 1–16). Springer.

- Emine, D. (2012). Financial challenges that impede increasing the productivity of SMEs in Arab region. Journal of Contemporary Management, 1, 17–32. https://web.archive.org/web/20180422063946id_/http://www.bapress.ca/jcm/jcm2012-2/Financial%20Challenges%20That%20Impede%20Increasing%20the%20Productivity%20of%20SMEs%20in%20Arab%20Region.pdf

- Eniola, A. A., & Entebang, H. (2015). SME firm performance-financial innovation and challenges. Procedia-Social and Behavioral Sciences, 195, 334–342. https://doi.org/10.1016/j.sbspro.2015.06.361

- Erdogan, A. I. (2018). Factors affecting SME access to bank financing: An interview study with Turkish bankers. Small Enterprise Research, 25(1), 23–35. https://doi.org/10.1080/13215906.2018.1428911

- Estrin, S., Gozman, D., & Khavul, S. (2018). The evolution and adoption of equity crowdfunding: Entrepreneur and investor entry into a new market. Small Business Economics, 51(2), 425–439. https://doi.org/10.1007/s11187-018-0009-5

- Fatoki, O. (2014). The financing options for new small and medium enterprises in South Africa. Mediterranean Journal of Social Sciences, 5(20), 748. https://doi.org/10.5901/mjss.2014.v5n20p748