Abstract

Financial socialisation techniques are known to influence students’ financial behaviour in the Eastern Cape. Still, the role of family structure on financial socialisation techniques and financial behaviour is unknown in the Eastern Cape. This study investigates the role of family structure on financial socialisation techniques and students’ financial behaviour in the Eastern Cape. A quantitative study was adopted, and closed-ended questionnaires were used in this study to collect primary data from 360 students in one university in the Eastern Cape. It was found that 66.11% of the students were raised in intact families, while 33.89% were raised in non-intact families. In terms of regression results, it was found that family structure significantly influences and shows differences in financial socialisation techniques and students’ financial behaviour. Also, financial socialisation techniques mediate the influence of family structure on students’ financial behaviour. It was recommended that financial educators should take into account the family variables such as family structure when planning for financial education programmes. Ideally, financial educators should develop a financial education programme that separately targets intact and non-intact families. Also, financial educators should encourage students to invite their parents to attend and participate in financial education workshops. This is to ensure that parents are educated on parental financial teaching and modelling as a way to improve students’ financial behaviour. This study demonstrates that family structures should be considered when targeting students’ financial behaviour. Also, financial socialisation techniques are important in improving students’ financial behaviour in the Eastern Cape. This study contributes to personal finance literature by providing empirical data on the role of family structure in financial socialisation and the behaviour of students.

Public Interest Statement

A description of your paper of NO MORE THAN 150 words suitable for a non-specialist reader, highlighting/explaining anything which will be of interest to the general public. Students who are raised in a single parented household have less opportunity to learn about personal finances from their parents than students raised in a two-parented household. They have less opportunity to learn about personal finance concept from their parents and few chances to observe their parents’ responsible financial behaviour. As result children raised in a single parented household report lower exposure to financial socialisation that leads to positive financial behaviour than students raised in a two parented. Therefore, financial educators need to be aware of this gap and deliver unique content to students raised in single and two parented households.

1. Introduction

Financial socialisation refers to the process by which students acquire and develop their financial outcomes (Danes, Citation1994:128). Parents are the primary socialisation agents (LeBaron & Kelley, Citation2021; Shim et al., Citation2009) and influence students’ financial outcomes the most (Ndou & Ngwenya, Citation2022:129). Parents may use techniques such as parental financial teaching and modelling of financial behaviour to influence individuals’ financial behaviour (Shim et al., Citation2015:36–37). Parental financial teaching and modelling of financial behaviour have the most influence on students’ financial behaviour (Antoni et al., Citation2019:82LeBaron & Kelley, Citation2021). Even though parents have the most influence on students’ financial outcomes, many studies do not differentiate between the role of the father and mother as financial socialisation agents (Henegar et al., Citation2013: 46). However, Clarke et al. (Citation2005:321) has shown that a father and a mother have different roles in modelling financial tasks. Also, Agnew et al. (Citation2018) show that mother and father have different roles in forming the children’s financial attitude and behaviour. In addition, women have lower levels of financial literacy (Fan et al., Citation2022; Lusardi et al., Citation2010: 367) and tend to own more credit cards than men (Henegar et al., Citation2013:45) and thus influence children differently. Therefore, the presence or absence of both mother and father in the family must be considered when studying the financial socialisation of students due to the dissolution of two-parent families (Rindfleisch et al., Citation1997:312). Also, students who grow up without their biological mother or father until their 18 birthdays tend to spend more time with socialisation agents such as television and social media (Benmoyal- Benmoyal-Bouzaglo & Moschis, Citation2010undefined65Nomlala, Citation2021).

In contrast, children from divorced families report owing more credit card debt than those from other family structures. Family structure is an essential consideration for students’ socialisation and financial outcomes. As motivated by Moschis (Citation2007:297), major life events such as death or separation of parents mark the transition into important life roles and a child’s earlier-life experiences that influence their behaviours. This study will use the family structure model to differentiate between children who are socialised financially by intact family (two-parented) versus non-intact family structures (for example, single-parented) (Roberts et al., Citation2003:301). This is possible since the family structure model acknowledges that children’s behaviour is rooted in their early experiences, such as parental divorce, separation or death. Also, early experiences of the child are shown to influence the way children are financially socialised. Thus, it is expected that family structures have a role in the financial socialisation of students and, thus, in their financial behaviour. This study uses the family structure model to investigate the role of family structure on students’ financial socialisation techniques and behaviour in the Eastern Cape. Eastern Cape is relevant since financial socialisation techniques influence students’ financial behaviour (Antoni et al., Citation2019:82). Also, the role of family structure on financial socialisation and behaviour is unknown.

2. Research Aim and Objectives of the Study

This study aims to investigate the role of family structure on financial socialisation techniques and students’ financial behaviour in the Eastern Cape. In achieving the research aim, the study’s objectives were to investigate the concepts of the family structure model, financial socialisation and financial behaviour. Then empirically tested the role of family structure on financial socialisation techniques and students’ financial behaviour. To provide recommendations to financial educators on how to improve students’ financial behaviour using financial socialisation.

3. Literature Review

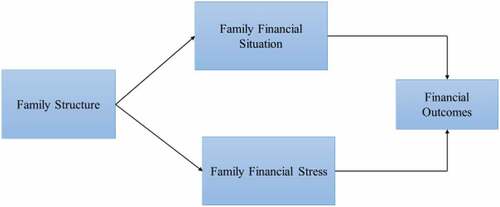

This study adopted the family structure model; see Figure for the family structure model.

Figure shows the family structure model developed by Rindfleisch et al. (Citation1997:313). The family structure model explains the role of family structures in consumer behaviour. In terms of the model, the financial outcomes of children differ by family structure. This means that children who are raised in a non-intact family due to divorce or separation exhibit higher levels of financial outcomes such as materialism, compulsive behaviour and even financial behaviour (Rindfleisch et al., Citation1997:313) than children raised in intact families. Furthermore, financial situations and stress partially mediate the relationship between family structures and children’s financial outcomes. (Rindfleisch et al., Citation1997:320). This study will adopt a similar model to explain the influence of family structure on financial socialisation techniques and financial behaviour.

3.1. Family structures

There are two types of family structure, namely, intact family and non-intact family. An intact family structure refers to two parents nurturing and developing a child (Sanni et al., Citation2010:23). Rindfleisch et al. (Citation1997:312) support that an intact family structure refers to a traditional family with two parents and a child. Intact family structure also refers to children raised by married parents (Regnerus, Citation2012 757; Shek et al., Citation2014). In contrast, a non-intact or disrupted family structure refers to the dissolution of two-parent families due to divorce or separation (Rindfleisch et al., Citation1997:312). This is also supported by Francesconi et al. (Citation2010: 1213) that a non-intact family refers to a child living with one biological parent or an adoptive parent (who is not married) because of death, divorce or separation in the family.

Additionally, a non-intact family can result from a child being born outside marriage (Francesconi et al., Citation2010:1213). Therefore, in this study, intact family structure refers to two parents who are married and raising a child. In comparison, a non-intact family structure refers to a single parent or two parents who are not married but raising a child together. The non-intact family may include extended, single-parent, reconstituted, three-generation, skip-generation and child-headed, cohabitation, same-sex and polygamous families (Hill et al., Citation2001:277–278).

3.2. Financial socialisation

As previously indicated, financial socialisation refers to the process by which individuals acquire and develop their financial outcomes (Danes, Citation1994:128). Many authors (Fan et al., Citation2022; Serido, Curran, Willmarth, Ahn, Shim, & Ballard, 2015) use the family financial socialisation model by Gudmunson and Danes (Citation2011:647) to explain financial socialisation in the household or family. The family financial socialisation model is divided into two main parts: the financial socialisation process and financial socialisation outcomes. The financial socialisation process consists of family factors such as family characteristics, indirect financial techniques such as family relationships, and direct financial socialisation techniques such as parental financial modelling. The indirect financial socialisation technique refers to individuals acquiring financial behaviour through everyday interactions with family members and the nature of the relationship between individuals and family members (Danes & Yang, Citation2014:62–65; Gudmunson & Danes, Citation2011: 647–649LeBaron & Kelley, Citation2021).

In contrast, direct financial socialisation refers to an explicit process where family members intentionally teach their children about personal finances to develop their financial outcomes. In terms of the model, financial outcomes may be influenced by indirect financial socialisation techniques, such as family interactions, and direct financial socialisation techniques, such as parental financial teaching, may influence financial outcomes. Therefore, direct and indirect financial socialisation techniques influence the financial outcomes of individuals’ financial knowledge, attitudes, self-efficacy, behaviour and well-being (Gudmunson & Danes, Citation2011:646–647). As implied above, family members may use different financial socialisation techniques to socialise individuals about personal finance (Xiao, Citation2016:66). However, the most influential financial socialisation techniques are parental financial teaching and modelling of financial behaviour (Antoni et al., Citation2019:82). Therefore, this study will discuss and measure parental financial teaching and financial modelling.

One of the financial socialisation techniques that may be used is parental financial teaching (Danes, Citation1994:129). Parental financial teaching refers to parents sharing their financial knowledge about certain financial concepts while interacting with their children (Gudmunson & Danes, Citation2011:649, 662). Parental financial teaching may include financial discussions about family matters, informing children about the importance of saving, teaching them how to be smart shoppers, and using a credit card appropriately (Shim et al., Citation2009). According to Grinstein-Weiss et al. (Citation2012:257), parental financial teaching is a way of transferring financial knowledge to children but also protects children against demonstrating irresponsible financial behaviour later in life. Many authors (Angulo-Ruiz & Pergelova, Citation2015:566; Ndou & Ngwenya, Citation2022:129) also show that parental financial teaching influenced financial behaviour directly. However, Angulo-Ruiz and Pergelova (Citation2015:566) indicate when financial knowledge is introduced in the study, it completely moderated the effect of financial teaching on financial behaviour. This result means that parental financial teaching increases financial knowledge and as a result improves financial behaviour.

Parents may also use modelling of financial behaviour to influence children’s financial behaviour. Modelling of financial behaviour refers to children observing the parents performing a behaviour and then imitating such behaviours from parents (Moschis & Churchill, Citation1978:200). Solheim et al. (Citation2011:101) indicate that most students learn most about saving money by observing their parents’ financial behaviour. For example, students observe how their parents save money (positive modelling) and how their parents do not save money (negative modelling). Students indicated that they learned about money management by observing how their parents prioritised needs over wants, budgeted, tracked expenses and reconciled bank accounts (Solheim et al., Citation2011:101 &104). Financial lessons learned through observation may positively or negatively influence children’s financial behaviour. However, Ndou and Ngwenya (Citation2022:129) found financial modelling does not influence the financial behaviour of young black adults.

3.3. Financial behaviour

Financial behaviour refers to any human behaviour that involves money management (Ndou & Ngwenya, Citation2022:122; Angulo-Ruiz & Pergelova, Citation2015:560×iao Xiao, Citation2016:73;). Financial behaviours consist of money management practices such as cash, credit, savings, investments and insurance (Dew & Xiao, Citation2011:53). Angulo-Ruiz and Pergelova (Citation2015:560) confirm that financial behaviour relates to behaviour where individuals keep their spending within their budget, save money and control their cash or money.

Additionally, financial behaviours that individuals demonstrate can also be positive or negative; for example, responsible (positive) and risky (negative) financial behaviour can occur (Asaad, Citation2015:108; Xiao, Ahn, Serido, Shim Citation2014:421). Responsible financial behaviours refer to money management practices with positive financial outcomes, while risky financial behaviours refer to those with negative financial outcomes (Asaad, Citation2015:108). Additionally, responsible financial behaviour includes checking credit ratings or savings money regularly in a savings account or using a financial plan to manage expenses and avoid overspending (Asaad, Citation2015:108; M. Gutter & Copur, Citation2011:705). In contrast, risky financial behaviours may include spending too much money, overusing credit and running out of money (Garman et al., Citation1996:158). Risky financial behaviour also refers to overspending, having an overdrawn cheque account, taking out large amounts of loans, keeping a balanced amount in a credit card account, using a credit card over its limit and being late on mortgage payments (Xiao et al. Citation2014:421).

3.4. Family structure, financial socialisation techniques and behaviour

From a family structure perspective, students born or raised in disrupted or non-intact family structures exhibit lower financial outcomes such as financial behaviour than children born or raised in intact family structures. This means that children who are born or raised in different family structures will exhibit different levels of financial behaviour. As a result, children who are born or raised in intact or non-intact family structures will exhibit different levels of financial behaviour (Agnew et al., Citation2018; Rindfleisch et al., Citation1997). In addition, the financial socialisation perspective shows that family variables such as family structure influence financial socialisation techniques (Gudmunson & Danes, Citation2011:648). Family structure was also found to moderate the relationship between parental involvement and how children are taught money management by their parents (Flouri, Citation2000:79). This means that children who are raised in a two-parented families are more likely to report that their parents were involved in their lives and also taught them adequately about money management than children raised from non-intact families (Flouri, Citation2000:79–80).

Additionally, Mauldin et al. (Citation2011:9) found the discrepancy in communication about money between children and parents was higher in the non-intact family than in intact family structures. This means that family structure influences the perception of children and parents on communication about money in the household. Therefore, family structure is expected to influence students’ financial socialisation techniques and financial behaviour. However, financial socialisation theory dictates that financial socialisation mediates the relationship between family variables and students’ financial outcomes (Gudmunson & Danes, Citation2011:648). As a result, financial socialisation techniques are expected to mediate the influence of family structures on financial behaviour.

4. Theoretical Framework and Hypotheses

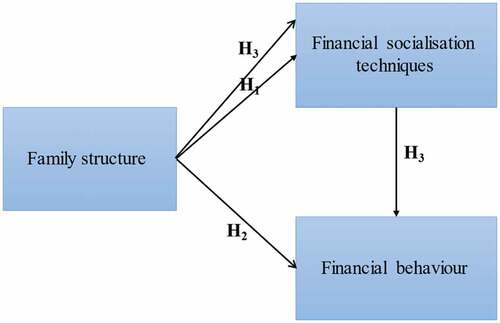

Figure demonstrates the model used in the study based on the theoretical framework (family structure model) and the literature review. The model illustrates the relationships between the independent (family structure) and the dependent variables (financial socialisation techniques and financial behaviour). The hypotheses of the study are provided below.

Figure 2. Framework of the study.

H1:

Family structure has a significant influence and difference on financial socialisation techniques.

H2:

Family structure has a significant influence and difference on financial behaviour.

H3:

Financial socialisation techniques mediate the influence of family structure and behaviour.

5. Research Methodology

This study adopted a positivist research paradigm and implemented a quantitative research design using cross-sectional data. This section will describe the research design employed in the study, the sampling technique, the questionnaire design and the data analysis.

5.1. Sampling

This study’s target is 533 registered undergraduate students at a selected Eastern Cape, South African university. A non-probability criterion sampling was used to select the students as it was difficult, costly and time-consuming to access the list of students’ names. The students completed 451 usable questionnaires, and 360 questionnaires were found to be suitable for quantitative statistical analysis.

5.2. Questionnaire Design

The questionnaire consisted of a cover letter and two sections, A and B. The cover letter provided respondents with information about their rights to participate in the study and explained how respondents’ confidentiality would be maintained. Section A collected respondents’ demographic information such as age, gender, ethnicity, highest qualification and family structure. This section used a nominal scale where we were coded with the number one and women with the number two. The family structure is coded using dummy coding, intact family structure = 1 and non-intact family structure = 0.

Section B used a five-point Likert-type scale. The respondents were asked to rate the statements between 1 and 5, where 1 represented “strongly disagree” and 5 represented “strongly agree”. The five-point Likert-type scale was used for the following constructs: financial socialisation techniques and financial behaviour. Financial socialisation techniques were measured as parental financial teaching (8 statements) and modelling financial behaviour (5 statements). The statements used to measure parental financial teaching was adopted from Shim et al. (Citation2009:1462) and modelling of financial behaviour using the scale of Serido et al. (2015:704). Financial behaviour (7 statements) is measured using the statements adopted from Akben-Seluk (2015: 90).

5.3. Data Analysis

Each completed questionnaire was scrutinised for missing data, and those that were incomplete or completed incorrectly were disregarded. The completed questionnaires were captured in Microsoft Excel and were subsequently transferred to Statistica version 14. Thereafter, the data was subjected to extensive statistical analysis, such as descriptive statistics (mean scores and standard deviation) and frequency distributions. Furthermore, exploratory factor analysis (EFA) was performed to assess validity and reliability, and Cronbach’s alpha was calculated. According to Hardy and Bryman (Citation2011:28), factor analysis is a statistical procedure that summarises the relationships between the items/statements and the factors. In this study, items/statements with a factor loading of 0.5 were considered significant (Wiid & Diggines, Citation2013:242).

Furthermore, Cronbach’s alpha was used to assess reliability, and a value greater than 0.7 was considered acceptable (Collis & Hussey, Citation2021:256; Wiid & Diggines, Citation2013:238). This study’s constructs were regarded as reliable if they had a Cronbach’s alpha of 0.7 or above. Cronbach’s alpha is used in this study to measure internal reliability (Collis & Hussey, Citation2021:256; Tavakol & Dennick, Citation2011:53). Simple and multiple regression analyses are used to assess the influence of independent variables on the dependent variable (Collis & Hussey, Citation2021:262; Hair et al., Citation2014:158). Part of the results produced by a simple regression analysis is the p-value, regression coefficient (b) and r-squared. The p-value, which is usually less than 0.05, indicates a statistical relationship between the independent and dependent variables, while the regression coefficient (b) shows the direction and the magnitude of the relationship between the dependent and independent relationship. The r-squared indicates that the total variance in the dependent variable is explained by the independent variable (Hair et al., Citation2014:189Wiid & Diggines, Citation2013:286;). Before the independent test was calculated, Levene’s test was calculated to assess the quality of variance of factors (parental teaching, modelling of financial behaviour and financial behaviour) across different groups (intact versus non-intact). After that, the independent test was used to examine the differences between the mean scores of two groups, namely intact and non-tact family structures concerning their parental financial teaching, modelling of financial behaviour and financial behaviour (Tredoux & Durrheim, Citation2002:148). Cohen’s d was used to calculate the effect size of the mean difference between parental financial teaching, modelling of financial behaviour, and financial behaviour. Effect size is intended to provide the magnitude of the differences between the mean scores (Gravetter & Wallnau, Citation2011:231). Cohen’s d = 0.2 is considered a small effect, while Cohen’s d = 0.5 is a medium effect, and Cohen’s d = 0.8 is considered a large effect (Gravetter & Wallnau Citation2011: 232). Lastly, the mediation was tested using the Kenny approach. For perfect mediation, the statistically significant relationship between the independent and dependent variables will disappear when the mediating variable is added to the regression equation. Alternatively, in the case of partial mediation, the statistically significant relationship between the independent and dependent variable will still exist, but the relationship will be weaker when the mediating variable is added to the equation (Baron & Kenny 1986:1177).

6. Empirical Results

A total of 360 questionnaires were used for data analysis. This means a response rate of 79.82% was achieved. All questionnaire data were captured on a Microsoft Excel spreadsheet and were then analysed using Statistica version 14.

6.1. Family structure

Section A of the questionnaire asked respondents about their family structures. Table shows the responses of the respondents.

Table 1. Results of Family Structure

Table shows that most respondents indicated that they belong to an intact family structure (66.11%), while 33.89% indicated that they belong to a non-intact family structure.

6.2. Validity and reliability results

Table shows the EFA and Cronbach’s Alpha results for financial socialisation techniques.

Table 2. Validity and reliability results of financial socialisation techniques

Table shows that factor 1 had five items loaded onto it. The five items (B12, B6, B20, B13 and B1) were intended to measure parental financial teaching. From the five items, B12 had the highest loading, and B1 had the lowest loading score. Factor 1 is named parental financial teaching and had a Cronbach’s alpha of 0.838572. This result means that factor 1 is valid and reliable. Table also shows that factor 2 had five items loaded onto it. The five items (B23, B22, B18, B19 & B10) were intended to measure modelling of financial behaviour. From the five items, B23 had the highest loading, and B10 had the lowest loading score. Factor 2 is named modelling of financial behaviour and had a Cronbach’s alpha of 0.771336. This result means that factor 2 is valid and reliable. Table shows the EFA and Cronbach’s Alpha results for financial behaviour

Table 3. Validity and reliability results of financial behaviour

Table shows that factor 3 had seven items loaded onto it. The six items (D6, D7, D17, D1, D13 & D9) measured financial behaviour. Of the six items, D6 had the highest loading, and D14 had the lowest loading score. Factor 3 is named financial behaviour and had a Cronbach’s alpha of 0.875. This result means that factor 3 is valid and reliable.

6.3. Regression analysis results

Table shows the regression analysis results for the study’s independent and dependent variables.

Table 4. Regression results

Table shows a significant positive relationship (b × 0.271; p = 0.000) between family structure and parental financial teaching. This result means that students raised in intact family structures are more likely to report a higher level of parental financial teaching than those raised in a non-intact family structure. It also shows a significant positive relationship (b × 0.287; p = 0.000) between intact family structure and the modelling of financial behaviour. This result meant that students raised in intact family structures are more likely to report a higher level of modelling of financial behaviour than those raised in a non-intact family structure. Lastly, there is a significant positive relationship (b × 0.287; p = 0.000) between intact family structure and the modelling of financial behaviour for children raised in a non-intact family structure than those raised in a non-intact family structure.

6.4. Group comparisons

An Independent t-test was calculated to determine the mean differences of family structure on financial socialisation techniques and financial behaviour. Table provides the results for group comparison between intact and non-intact family structure regarding financial socialisation techniques and financial behaviour.

Table 5. Group comparisons

Table shows a significant difference (p = 0.000) between intact (X = 3.758) and non-intact (X = 3.257) family structure regarding parental financial teaching. This result means that those students raised in an intact family structure were more likely to agree with parental financial teaching. In contrast, those students raised in a non-tact family were more neutral on parental financial teaching. Also, Cohen’s d (d = 0.593) shows the significant difference in parental financial teaching between intact and non-intact family structures is of a medium difference. There was a significantly different (p = 0.000) between intact (X = 3.690) and non-intact (X = 3.177) regarding the modelling of financial behaviour. This result means that those students raised in the intact family structure were more likely to agree with the modelling of financial behaviour than those raised in non-intact family structures. Also, Cohen’s d (d = 0.632) shows the significant difference in modelling financial behaviour between intact and non-intact family structures is of a medium difference. Lastly, there was a significant difference (p = 0.002) between intact (X = 3.173) and non-intact (X = 2.875) family structure regarding financial behaviour. This result meant that those students raised intact families are more likely to be neutral on financial behaviour, while those raised in non-intact families tend to disagree with financial behaviour. Cohen’s d (d = 0.340) shows the significant difference in financial behaviour between intact and non-intact family structures is a small difference.

6.5. Mediation results

Table shows the mediation results of financial socialisation techniques on family structure and financial behaviour.

Table 6. Regression results

Table shows that financial socialisation techniques, such as parental financial teaching (b × 0.269; p = 0.000) and modelling of financial behaviour (b × 0.194; p = 0.001), significantly influence financial behaviour. Also, when financial socialisation techniques is added as independent variables in the regression analysis, family structure (b × 0.03; p = 0.544) stops having a significant relationship with financial behaviour. This result means that financial socialisation techniques (parental financial teaching and modelling of financial behaviour) fully mediate the influence of family structure on financial behaviour. Table provides a summary of the statistical results of the study.

Table 7. Addressing the research hypotheses

Table shows that all the hypotheses (H1, H2 and H3) were accepted.

7. Discussion of Results

The results of the study show that financial socialisation techniques and behaviour differ based on the student’s family structure in the Eastern Cape. Students raised in intact family structures tend to have higher financial socialisation techniques and financial behaviour levels than students raised in non-intact families. This result means that students, because of different family structures, are exposed to different levels of financial socialisation and therefore have different financial outcomes. A study by Flouri (Citation2000) agrees that family structure moderates the relationship between parental involvement and financial behaviour. This means parental involvement and financial behaviour are weaker for children raised in non-intact families than for intact families (Flouri, Citation2000). In addition, the study’s results support the family structure model that family structure influences the students’ financial outcomes, such as financial behaviour (Rindfleisch et al., Citation1997). However, the family structure model and financial socialisation indicate that relevant factors mediate the outcomes of students. From the perspective of financial socialisation, family variables (family structures) and financial outcomes are mediated by financial socialisation techniques (Gudmunson & Danes, Citation2011:648). The study’s results provide empirical support that the financial socialisation techniques mediated the influence of family structure on financial behaviour. Financial socialisation techniques fully mediate the influence of family structure on financial behaviour.

8. Recommendations

Financial educators should not ignore the students’ family variables, such as family structure, when attempting to improve students’ financial behaviour. The results show that students from non-intact families versus intact families need more financial education to improve their financial behaviour. Thus, the one fits all financial education does not work for all students (Van Campenhout, Citation2015:202). However, developing a separate financial education programme that targets intact and non-intact families is ideal. Also, to improve students’ financial behaviour, financial educators should encourage the participation of parents in financial education workshops (Van Campenhout, Citation2015:208). This is because financial socialisation techniques used by parents play an important role in improving students’ financial behaviour (Antoni et al., Citation2019:82). Parents play a crucial part in improving students’ financial behaviour (Shim et al., Citation2015:36–37).

Parental financial teaching is one way of improving students’ financial behaviour. This is important because parental financial teaching has been found to improve students’ financial behaviour. Therefore, parents need to transfer high levels of financial knowledge to their children. However, for parents to be able to transfer high levels of financial knowledge, parents need to be educated on financial concepts by financial experts. Therefore, financial educators must target and arrange financial education workshops for intact and non-intact families.

Another way of improving students’ financial behaviour is modelling financial behaviour. To improve the modelling of financial behaviour, a financial educator should teach parents about financial practices such as saving money and paying bills on time. These financial practices need to be demonstrated by parents in a way that students can observe and learn financial from them. Students and parents need to be encouraged to learn from each other.

It is important to note that these results and recommendations are limited to students in the Eastern Cape. However, since the study’s sample is a representation of one university, more universities will have to be included in the sample to be able to generalise the results of this study to the population in the Eastern Cape. More financial socialisation techniques need to be included in future studies to see whether all financial socialisation techniques mediate the influence of family structure on financial behaviour.

Notwithstanding the study’s limitations, this study contributes to the literature by providing empirical data on the role of family structure on financial socialisation and behaviour. This study shows the importance of including family variables as predictor variables of financial outcomes of students but also the role of financial socialisation techniques on financial outcomes. In conclusion, this study shows the important role of family structure and financial socialisation in personal finance research.

Acknowledgments

I want to acknowledge my supervisors who help me complete my PhD qualification.

Disclosure statement

No potential conflict of interest was reported by the author.

Additional information

Notes on contributors

Xolile Antoni

Xolile Antoni is employed by Rhodes University as a Senior Lecturer in the Department of Management. He lectures Financial Management to third year and Personal Financial Management to honours students. He is a CERTIFIED FINANCIAL PLANNER and an expert of Personal Finance. He is a member of the Financial Planning Institute (FPI), a professional certification body for the financial planning industry in South Africa. His research interests are financial socialisation, financial literacy, money attitude and personal finance. He publishes mostly in the area of financial socialisation and financial literacy. He uses the theory of financial socialisation as a way to improve financial literacy and financial behaviour in the Eastern Cape, South Africa.

References

- Agnew, S., Maras, P., & Moon, A. (2018). Gender differences in financial socialisation in the home—an exploratory study. International Journal of Consumer Studies, 42(3), 275–14. https://doi.org/10.1111/ijcs.12415

- Angulo-Ruiz, F., & Pergelova, A. (2015). An empowerment model of youth financial behaviour. The Journal of Consumer Affairs, 49(3), 550–575. https://doi.org/10.1111/joca.12086

- Antoni, X. L., Rootman, C., & Struwig, F. W. (2019). The influence of parental financial socialisation techniques on student financial behaviour. International Journal of Economics and Finance Studies, 11(2), 72–88. https://doi.org/10.34109/ijefs.201911205

- Asaad, C. T. (2015). Financial literacy and financial behavior: Assessing knowledge and confidence. Financial Services Review, 24(2), 101–117.

- Benmoyal-Bouzaglo, S., & Moschis, G. P. (2010). Effects of family structure and socialisation on materialism: A life course study in France. Journal of Marketing Theory and Practice, 18(1), 55–71. https://doi.org/10.2753/MTP1069-6679180104

- Clarke, M. C., Heaton, M. B., Isrealsen, C. L., & Eggett, D. L. (2005). The acquisition of family financial roles and responsibilities. Family and Consumer Sciences Research Journal, 33(4), 321. https://doi.org/10.1177/1077727X04274117

- Collis, J., & Hussey, R. (2021). Business research: A practical guide for students (5th ed.). Red Globe.

- Danes, S. M. (1994). Parental perceptions of children’s financial socialisation. The Journal of Financial Counselling and Planning, 5, 127–149.

- Danes, S. M., & Yang, Y. (2014). Assessment of use of theories within the journal of financial counselling and planning and contribution to family financial socialisation conceptual model. Journal of Financial Counselling and Planning, 25(1), 53–68.

- Dew, J., & Xiao, J. J. (2011). The Financial management behaviour scale: Development and validation. Association for Financial Counseling and Planning Education, 22(1), 43–59.

- Fan, L., Lim, H., & Lee, J. M. (2022). Young adults’ financial advice‐seeking behavior: The roles of parental financial socialisation. Family Relations, 71(3), 1226–1246. https://doi.org/10.1111/fare.12625

- Flouri, E. (2000). The role of parental involvement on adolescents’ money management. Children’s Social and Economics Education, 4(2), 75–82. https://doi.org/10.2304/csee.2000.4.2.75

- Francesconi, M., Jenkins, S. P., & Siedler, T. (2010). Childhood family structure and schooling outcomes: Evidence for Germany. Journal of Population Economics, 23(3), 1073–1103. https://doi.org/10.1007/s00148-009-0242-y

- Garman, E. T., Leech, I. E., & Grable, J. E. (1996). The negative impact of employee poor personal financial behaviors on employers. Association for Financial Counseling and Planning Education, 7(1), 157–167.

- Gravetter, F. J., & Wallnau, L. B. (2011). Essentials of statistics for the behavioural sciences (8th ed.). United states of America: Cengage.

- Grinstein-Weiss, M., Spader, J. S., Yeo, Y. H., Key, C. C., & Freeze, E. B. (2012). Loan performance among low-income households: Does prior parental teaching of money management matter? Social Work Research, 36(4), 256–270. https://doi.org/10.1093/swr/svs016

- Gudmunson, C. G., & Danes, S. M. (2011). Family financial socialisation: Theory and critical review. Journal of Family and Economic Issues, 32(4), 644–667. https://doi.org/10.1007/s10834-011-9275-y

- Gutter, M., & Copur, Z. (2011). Financial behaviours and financial well-being of college students: Evidence from a national survey. Journal of Family and Economic Issues, 32(4), 699–714. https://doi.org/10.1007/s10834-011-9255-2

- Hair, J. F., Black, W. C., Babin, B. J., & Anderson, R. E. (2014). Multivariate data analysis (7th ed.). Pearson.

- Hardy, M., & Bryman, A. (2011). The handbook of data analysis. Cengage.

- Henegar, J. M., Archuleta, K., Grable, J., Britt, S., Anderson, N., & Dale, A. (2013). Credit card behavior as a function of impulsivity and mother’s socialisation. Association for Financial Counseling and Planning Education, 24(2), 37–49.

- Hill, M. S., Yeung, W. J. J., & Duncan, G. J. (2001). Childhood family structure and young adult behaviors. Journal of Population Economics, 14(2), 271–299. https://doi.org/10.1007/s001480000039

- LeBaron, A. B., & Kelley, H. H. (2021). Financial socialisation: A decade in review. Journal of Family and Economic Issues, 42(Suppl S1), 195–206. https://doi.org/10.1007/s10834-020-09736-2

- Lusardi, A., Mitchell, O. S., & Curto, V. (2010). Financial literacy among the young. The Journal of Consumer Affairs, 44(2), 358–380. https://doi.org/10.1111/j.1745-6606.2010.01173.x

- Mauldin, T. A., Mimura, Y., Kabaci, M. J., Koonce, J. C., Rupured, M., & Jordan, J. W. (2011). Does marital status of the parent relate to family communication regarding finances. Journal of Youth Development, 6(11), 1–14. https://doi.org/10.5195/jyd.2011.196

- Moschis, G. P. (2007). Life course perspectives on consumer behavior. Journal of the Academy of Marketing Science, 35(2), 295–307. https://doi.org/10.1007/s11747-007-0027-3

- Moschis, G. P., & Churchill, G. A. (1978). Consumer socialisation: A theoretical and empirical analysis. Journal of Marketing Research, 15(4), 599–609. https://doi.org/10.1177/002224377801500409

- Ndou, A., & Ngwenya, S. (2022). THE influence of parental financial socialization on young black African adults’ financial behavior. Eurasian Journal of Economics and Finance, 10(4), 120–134. https://doi.org/10.15604/ejef.2022.10.04.001

- Nomlala, B. (2021). Financial socialisation of accounting students in South Africa. International Journal of Finance & Banking Studie, 10(2), 01–15. https://doi.org/10.20525/ijfbs.v10i2.1128

- Regnerus, M. (2012). How different are the adult children of parents who have same-sex relationships? Findings from the new family structure study. Social Science Research, 41(4), 752–770. https://doi.org/10.1016/j.ssresearch.2012.03.009

- Rindfleisch, A., Burroughs, J. E., & Denton, F. (1997). Family structure, materialism, and compulsive consumption. The Journal of Consumer Research, 23(4), 312–325. https://doi.org/10.1086/209486

- Roberts, J. A., Manolis, C., & Tanner, J. F. (2003). Family structure, materialism and compulsive buying: A reinquiry and extention. Journal of the Academy of Marketing Sciences, 31(3), 301–310. https://doi.org/10.1177/0092070303031003007

- Sanni, K. B., Udoh, N. A., Okediji, A. A., Modo, F. N., & Ezeh, L. N. (2010). Family types and juvenile delinquency issues among secondary school students in akwa ibom state, Nigeria: Counseling implications. Journal of Social Science, 23(1), 21–28. https://doi.org/10.1080/09718923.2010.11892807

- Shek, D. T. L., Xie, Q., & Lin, L. (2014). The impact of family intactness on family functioning, parental control, and parent–child relational qualities in a Chinese context. Front Pediatrics, 2, 149. https://doi.org/10.3389/fped.2014.00149

- Shim, S., Barber, B. L., Card, N. A., Xiao, J. J., & Serido, J. (2009). Financial socialisation of first-year college students: The roles of parents, work, and education. Journal of Youth and Adolescence, 39(12), 1457–1470. https://doi.org/10.1007/s10964-009-9432-x

- Shim, S., Serido, J., Card, N., & Tang, C. (2015). Socialisation processes and pathways to healthy financial development for emerging young professionals. Journal of Applied Developmental Psychology, 38:29–38.

- Solheim, C. A., Zuiker, V. S., & Levchenko, P. (2011). Financial socialisation family pathways: Reflections from college students’ narratives. Family Science Review, 16(2), 97–112.

- Tavakol, M., & Dennick, R. (2011). Making sense of Cronbach’s alpha. International Journal of Medical Education, 2(1), 52–53. https://doi.org/10.5116/ijme.4dfb.8dfd

- Tredoux, C., & Durrheim, K. (2002). Numbers, hypotheses and conclusions: A course in statistics for the social sciences. UCT Press.

- Van Campenhout, G. (2015). Revaluing the role of parents as financial socialisation agents in youth financial literacy programs. The Journal of Consumer Affairs, 49(1), 186–222. https://doi.org/10.1111/joca.12064

- Wiid, J., & Diggines, C. (2013). Marketing research (2nd ed.). Juta.

- Xiao, J. J. (2016). Handbook of consumer finance research (2nd ed.). Springer.

- Xiao, J. J., Ahn, S. Y., Serido, J., & Shim, S. (2014). Earlier financial literacy and later financial behaviour of college students. International Journal of Consumer Studies, 38(6), 593–601.