?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

Access to agricultural credit is still a challenge in developing countries. The weakness of agricultural financing prevents producers from acquiring the modern technologies that are essential for the development of their activity. This paper aims to determine the impact of access to credit on agricultural productivity in Benin using alternative measures of productivity. To do this, we use the endogenous switching regression model to control for potential selection and unobserved heterogeneity issues associated with this impact analysis. The data used comes from the statistical databases of the National Agricultural Research Institute of Benin. The results show that the adoption of improved seeds, the geographic location, the area sown and member of peasant organization determine producers’ access to credit are factors that determine producers’ access to credit. Farmers’ access to credit generates an estimated gain of 40.07% and 31.97% respectively for production per hectare and production per FCFA invested. These results require a comprehensive and coherent public action.

PUBLIC INTEREST STATEMENT

The demand for agri-food products is growing and diversifying in Benin, as it is in other developing countries (DCs). The quantitative and qualitative improvement of the supply of these products appears to be urgent in order to reduce dependence on the countries of the North. The recent experiences related to the war in Ukraine have shown that such dependence is harmful to developing countries in terms of the supply difficulties it has caused. This paper assesses the impact of agricultural credit in improving agricultural productivity, particularly that of maize in Benin. The results suggest that access to credit allows producers to increase their productivity by about 40.07%. Productivity gains are also observed at the level of capital but in a lesser proportion, i.e. 31.97%. These results call for a strengthening of measures that facilitate access to credit for maize producers.

1. Introduction

Agriculture is a key sector of the Beninese economy. This sector is the main source of food, employment, and income. The agricultural sector contributes nearly 27.8% to the gross domestic product and generates more than 71.5% of export earnings on average over the period 2015–2020 (MAEP, Citation2022). Because of its importance, public authorities have chosen to develop agricultural sectors more, in particular the food sectors that were hitherto neglected in favour of cash products such as cotton. In this perspective, the maize sector is ranked in second position out of the six (06) flagship agricultural sectors behind cotton (WFP, Citation2017). While the level of production of this cereal, widely consumed in Benin, makes it possible to cover household food needs,Footnote1 the marketable surpluses generated are still not sufficient enough to meet the country’s foreign exchange needs (MAEP, Citation2017). Insufficient surplus may be associated with low yield. For example, according to FAO (Zedillo, Citation2015), maize yield in Benin declined between 2011 and 2020, from 1422 kg/ha to 1272 kg/ha, with an average yield of 1347 kg/ha over the same period compared to West Africa and World averages of 1642 kg/ha and 5530 kg/ha respectively (see Figure in the appendices). Lower yields could lead to lower income levels. Available statistics show a drop in real terms of the annual income per capita between 2011 and 2015, going from 154,070 FCFAFootnote2 to 148,424 FCFA, i.e. a decrease of about 3.7% (INSAE/EMICoV, Citation2015). As a result, the standard of living in rural areas decreased. The literature also shows that farmers in low-income countries are mostly poor (Cervantes-Godoy & Dewbre, Citation2010; Salami et al., Citation2010). The studies point out that low productivity is one of the underlying factors for the low standard of living among farmers.

However, productivity in the agricultural sector is still very low in many African countries (Nakano & Magezi, Citation2020). Large areas of arable land have remained untapped. Zedillo (Citation2015) estimates the total unused arable land on the continent at almost 60%. Progress in improving agricultural productivity over the past three decades has been disappointing for majority of African countries according to the Africa Progress Panel (2010). In sub-Saharan Africa, agricultural productivity levels, although increasing, are still far behind those of other developing regions (Magrini et al., Citation2017). However, projections indicate that the next decade will be marked by rapid population growth, rising incomes, and urbanization which will exert pressure on the demand for food products. Recent production paths clearly show that this growing demand will not be able to be satisfied (OECD and FAO, Citation2016). These stylized facts pose the challenge of improving agricultural productivity in Africa in general and in Benin in particular.

The empirical literature identifies several factors which may explain low productivity. Exogenous factors such as climatic changes, invasions of insect pests, floods, etc., which are out of the control of farmers. In addition to these constraints, there are other factors described as endogenous which are linked to the decisions of farmers. These include the low rate of adoption of modern technologies, such as fertilizers, modern varieties and poor agronomic practices (Nakano et al., Citation2016;Otsuka & Larson, Citation2016). In this same vein, other works emphasize the lack of access to credit as an obstacle to the adoption of better technologies and agricultural practices (Guirkinger & Et Boucher, Citation2008; Moser and Barrett, Citation2006). Credit has been found to be key to improving agricultural productivity since Carter’s (Citation1988).

The low productivity of smallholders farmers is seen as the result of the effect of credit constraints. Theoretically, credit constraints have a negative impact on agricultural productivity. The poor, without sufficient collateral, are generally excluded from formal financial services because of high transaction costs and information asymmetries that increase formal banks’ reluctance to offer them these financial services (Akerlof, Citation1970;Stiglitz & Weiss, Citation1981). As a result, most poor smallholders are often unable to invest in new technologies or in the acquisition of inputs such as fertilizer, improved seeds, etc. (Conning & Udry, Citation2007; Markelova et al., Citation2009;). For Feder et al. (Citation1990), credit allows producers to have the necessary resources they need to cover the financing needs induced by the production cycle. This agricultural production cycle is particularly long because of the period between sowing and harvesting. The availability of credit allows for greater consumption and greater use of purchased inputs, which increases farmers’ production and subsequently their income.

It is therefore not surprising that a large part of the literature shows the positive effects of producers’ access to credit on agricultural productivity (Akudugu, Citation2016; Guirkinger & Et Boucher, Citation2008;Khandker & Et Koolwal, Citation2014) even though some studies have shown that these effects are sometimes limited (Carter, Citation1989). Nevertheless, a number of recent studies perceive as challenging the many virtues of agricultural credit showing that the effects are not as predictable as one might think (Agbodji & Johnson, Citation2019;Nakano & Magezi, Citation2020;Njeru et al., Citation2016). For example, Agbodji and Johnson (Citation2019) find contrasting results, highlighting a negative impact of cash credit on productivity. Nakano and Magezi (Citation2020) draw attention to the insufficiency of a credit improvement policy in guaranteeing increased productivity. Such results highlight variations in the effects of access to credit and therefore call for specific reflections within countries.

The contribution of this article to the literature is twofold. First, in Benin, most of the work available on the subject generally focuses on the determinants of access to credit or the mechanisms for financing agricultural sectors (Adégbola et al., Citation2009;Assogba et al., Citation2017;Sossou, Citation2015). Exceptions are the work of Acclassato Houensou et al. (Citation2021) and that of Mahoukede et al. (Citation2015). The former examines the impact of financing on the productivity of small family farms while the latter focused on rice farming. Acclassato Houensou et al. (Citation2021) do not distinguish between producers according to the crop grown. Indeed, the data used in their analysis covers a range of crops, namely cotton, maize, rice and market gardening. Not separating producers can lead to at least two biases. On the one hand, the yield measured in kilograms per hectare of a vegetable farmer is not comparable to that of a cotton farmer, let alone a maize farmer. Thus, the difference in productivity between these two groups of farmers is meaningless. On the other hand, producers do not have the same needs in terms of financing. The rice farmer may express a need for financing both for the establishment of an irrigation mechanism and the purchase of crop-specific inputs, whereas the maize farmer may not need to establish irrigated crops. Complementing Mahoukede et al. (Citation2015), we address this issue with respect to maize producers because, as mentioned earlier, maize remains the main crop produced by the majority of farmers in Benin. Secondly, this study, in addition to the yield per hectare generally used in the literature, relies on an alternative indicator for measuring productivity, namely capital per hectare. The use of production yield is insufficient because an increase in production is a necessary but not sufficient condition to guarantee an increase in the producer’s income if the latter faces important transaction costs.

Specifically, this research provides answers to a number of questions, namely What is the impact of access to credit on agricultural productivity in Benin? What are the expected productivity gains from agricultural credit in Benin? The objective of this research is to determine the impact of access to credit on agricultural productivity. It therefore intends to provide additional empirical evidence on the role of credit in increasing agricultural productivity in Benin. The results will therefore be very useful to public authorities by allowing them to better refine strategies to improve access to finance for producers. To achieve this, we estimate the productivity of farmers according to two identified regimes, namely those who have access to formal credit and those who do not. We rely on the results of the endogenous switching regression model using survey data to estimate the yield of factors of production when farmers are endogenously sorted between the two regimes.

The results show that the adoption of improved seeds, the geographic location, the area sown and member of peasant organization are factors that determine farmers’ access to credit. Our results also suggest that the productivity of farmers without access to credit is determined by education, farm size, use of fertilizer and total labour. Among producers with access to credit, farm size, use of improved seed and being located in the central region of the country positively influence productivity. With regard to the impact of agricultural credit, the estimates revealed a productivity gain of 40.07% and 31.97% for producers with access to credit compared to their counterparts without access, respectively for production per hectare and production per CFA invested.

The rest of the paper is structured as follows. Section 2 contextualizes the study by identifying productivity issues that constraint the majority of rural households in Benin. Section 3 reviews the existing literature on the agricultural performance with financing constraints. Section 4 presents the data used as well as the methodological approach. Section 5 displays the descriptive statistics by highlighting the possible interrelationships between the main variables of the study and presents the mains econometric results. Section 6 summarizes the major findings and draws the policy implications.

2. Financing and productivity challenges of agriculture in Benin

Agricultural production in Benin, like in other developing countries (DCs), is mainly practiced by farmers. The average land area is estimated at 1.7 ha with about 34% of farms covering less than one (01) hectare. Smallholders, estimated at about 550,000, account for nearly 95% of the output of the agricultural sector (MDAEP and UNDP, Citation2015). This sector has a preponderant share in GDP, averaging nearly 36% (WFP, Citation2017). Despite the importance of agriculture in Benin’s economy, the sector faces many financing challenges.

Agricultural financing in Benin, like in most sub-Saharan African countries, has long been provided by the public authorities. These direct State interventions in rural financial markets ended up in failure in the 1960s and 1970s, leading to the questioning of the state’s mandate in financing agriculture in favour of the Structural Adjustment Programs (SAP) in 1980s. The return of the Government to the agricultural sector was observed gradually towards the end of the 2000s, notably from 2006 following the change of regime which occurred in the country’s top leadership. The authorities then expressed the desire to make agriculture the backbone of the economy. The 2007–2008 food crisis further reinforced this and lead to the establishment of an emergency plan to support food security (PUASA). In addition to this plan, subsidies were established in order to support increased food production.

The various agricultural financing instruments planned in Benin are supposed to combine public actions with private initiatives (MAEP, Citation2016). The intent to develop the agricultural sector, as displayed by the public authorities, will result in the development of the strategic plan to revive the agricultural sector and the national plan of agricultural investment (PSRSA/PNIA). Despite the political will, the development of the agricultural sector is slowed down by the low level of funding. In fact, the resources allocated from the national budget and external funds established with the support of technical and financial partners to finance the implementation of the PSRSA, indicate a low level of funding for the sector. For illustration purposes, with an estimated agricultural investment of 1531.05 billion FCFA between 2011 and 2015, only 742.31 billion FCFA were invested by both the State and the private sector, i.e. a financial execution rate of 48.48% (See Table ).

Table 1. Financing of the agricultural sector strategic recovery plan (PSRSA)

The gaps in funding results in ineffective public administration including “the National Fund for Agricultural Development (FNDA)” created in 2014 and confirmed in 2017.Footnote3 The FNDA is indeed the main instrument expected to finance agricultural activities. The counters dedicated to implement this fund have not been operational since their establishment. The activities of this fund were only launched in 2018. In the absence of operationalization of the main financing instruments, actors in agricultural value chains continue to turn to decentralized financial services (DFS) to obtain funding despite the difficult conditions they face accessing finance and the inappropriate services they receive in respect to agricultural activities. Farming households continue to struggle in their attempts to develop their farms because of the lack of an adequate financing mechanism.

Producers, especially cotton farmers, have for a long time relied on FECECAMFootnote4 whose activities have been able to prosper thanks to a credit repayment mechanism favoured by the public monopoly in the sector (Wampfler & Et Mercoiret, Citation2002). These important initiatives, however, struggle to be effective. Most of the products provided by microfinance institutions (MFIs) in the agricultural sector are often either poorly designed or poorly adapted to the needs of the sector. This lack of access to credit is exacerbated by the virtual absence of an appropriate agricultural insurance mechanism. The nature and frequency of risks in agriculture demotivate insurance structures to provide insurance products to this sector. The experiences in this field are very recent in Benin and relate to the actions of private operators who include AMAB.Footnote5

The association of farmers applying for group credit has not always been accompanied by a sustained increase in access to credit because of the high arrears resulting from the rejection of the solidarity guarantee by some members (MDAEP and UNDP, Citation2015). The situation in central Benin illustrates this difficulty. Agricultural cooperatives in this region are still not very familiar with the behaviour and history of their members, particularly in terms of loan repayments. This uncertainty about the credit repayment capacity associated with the hazards affecting agriculture justifies, among other things, the pronounced shortfall of financing in this sector. Due to the lack of adequate means to enlarge cultivated areas, many farmers in Benin, like in developing countries, work on a small scale.

These production constraints hinder public policies that are mainly aimed at the diversifying agriculture. Indeed, the potential of agriculture in Benin, particularly with regard to food crops, is still poorly exploited despite the increase in production. However, the public authorities have opted to develop the food sectors hitherto left behind in favour of cash crops such as cotton. In this perspective, the corn sector is ranked second out of the six (06) flagship agricultural sectors after cotton (WFP, Citation2017). If the level of production of this cereal makes it possible to cover the food needs of households, the fact remains that the generated marketable surpluses are not sufficient enough to meet the country’s real needs (MAEP, Citation2017). Meeting farmers’ specific financing needs would significantly increase production and put maize in the range of cash crops that generate significant foreign exchange for the country and reduce poverty among farmers.

The above development clearly indicates the challenges of financing in the agricultural sector and call for attention from public authorities. However, the effectiveness of public policies requires clarification of the relationship between financing and the performance issues.

3. Literature review

The issue of access to credit and agricultural productivity is well discussed in the literature. But there is no consensus on the nature of the impact. This lack of consensus in the literature on the effect of access to credit could be explained by the socio-economic realities and the initial agricultural endowments that characterize producers from one country compared to another (Seck, Citation2019). Moreover, this lack of consensus could be justified by the across country variations in the strategies employed by the public authorities to finance the agricultural sector. Indeed, it is well documented that the banking and non-banking financial systems are reluctant to finance agricultural activities given the risks inherent to the sector and the problem of information asymmetry raised by Akerlof (Citation1970). Thus, financial institutions generally make their decisions by considering the uncertainties in the credit market due to imperfection of information (Stiglitz & Weiss, Citation1983).

Overall, the empirical literature identifies three trends in terms of the impact of credit on agricultural productivity. Firstly, there are those who point out the positive effects of credit in terms of improving agricultural productivity, then those who conclude that credit has a limited or even neutral effect, and finally, those who even see a negative effect. In what follows, we present the various empirical works by considering these three trends.

In Senegal, Diallo et al. (Citation2020) provide empirical evidence on the need to promote agricultural credit in production. Using stochastic frontier analysis (SFA) from a sample of 216 producers surveyed in 2019, Diallo et al. (Citation2020) show that farmers accessing credit have a higher output than their counterparts by 37.32%. Diamoutene and Jatoe (Citation2020) also report a positive effect of credit on maize yield in Mali using endogenous switching regression model. In the same vein, D. A. Ali et al. (Citation2014), on a larger sample of 3600 farm households in Rwanda in 2011, use regime-switching models and find that lifting credit constraints leads to an improvement in agricultural productivity of at least 17%. In Ghana, Akudugu (Citation2016) finds a significant relationship between credit from formal and informal sources and agricultural production. For Akudugu (Citation2016), the interactions of informal credit with farm size; formal and informal credit with farm size have a positive and significant effect on production. More recently, Martey et al. (Citation2019), using the propensity score matching (PSM) method, report a positive effect of credit on the productivity of maize producing households in Northern Ghana. They argue that credit allows producers to access agricultural inputs in a timely manner and to allocate production factors more efficiently. In their study of credit constraints and productivity in Peru, Guirkinger and Et Boucher (Citation2008) conclude that the output of constrained households is determined by their productive asset endowments. In addition, they find that formal credit constraints negatively impact the efficiency in resource allocation. These main results suggest the importance of credit in the performance of farmers. However, limited or neutral effects of credit on agricultural productivity have also been highlighted in the literature.

Some of the literature shows that credit does not contribute to increased agricultural productivity (Nwaru and Onuoha, Citation2010). Njeru et al. (Citation2016), using a sample of 259 farmers in Kenya, find that there is no significant difference in fertiliser use and yield among farmers who have access to credit and those who do not. Nwaru and Onuoha (Citation2010) even find a better performance by farmers who do not benefit from credit compared to beneficiaries. Seck (Citation2019) interprets this result as a sign of an inappropriate lending system. The poor performance of the farmers who benefited is also highlighted by Khan et al. (Citation2013). The latter explain this as resulting from application of high interest rate, the delays generally noted in setting up loans, and the cumbersome administrative procedures.

Regarding the negative effects of credit on productivity, Nakano and Magezi (Citation2020) are categorical. Their results suggest that improved access to credit is not sufficient to increase technology adoption by farmers and lead to increased agricultural productivity and welfare among Kenyan farmers. Agbodji and Johnson (Citation2019) distinguish in their analysis the effects according to the type of credit on a sample of 2,226 households in Togo. Using endogenous switching regression model (ESR) and propensity score matching (PSM) methods, they specifically show a negative effect of cash credit on maize productivity versus a positive effect of in-kind credit. The precariousness and low purchasing power of small farmers explain these results. Due to a lack of sufficient savings and due to extreme poverty, small farmers sell their harvest even if it means resorting to borrowing at a future date to meet basic needs such as housing, health and education. As a result, loans obtained by these farmers are not used to acquire other factors of production such as improved seeds.

Clearly, most studies that examine the relationship between access to credit and agricultural productivity come up with mixed results, thus necessitating country-specific case studies. In Benin, existing studies generally fail to empirically address the link between access to credit and farmer productivity. Interest is more focused on the mechanisms of financing agricultural sectors or on the determinants of access to credit (see Adégbola et al., Citation2009;Assogba et al., Citation2017;Sossou, Citation2015). Acclassato Houensou et al. (Citation2021) recently made an attempt to estimate the impact of credit among family farmers in Benin. But as mentioned earlier in the introduction, this study lumps together farmers producing different crops to determine productivity. Such an approach is likely to lead to biased policy implications as it may result in under- or overestimation of gains for some producers. The present study therefore corrects for this problem, focusing on maize farmers in Benin while considering possible selection bias and unobserved heterogeneity issues. This study contributes to the available literature on the impact of access to credit on agricultural productivity in Benin.

4. Methodology and data

This section presents the data that will be used in this study and describes the methodological approach that will be followed.

4.1. Data

The data used in this study come mainly from the statistical databases of the National Institute of Agricultural Research of Benin (INRAB) attached to the Ministry in charge of agriculture. The data were collected as part of a survey conducted in 2016 for the Agricultural Policy Analysis Program (PAPA). The survey aimed to determine the optimal conditions for increased production of maize and cotton in Benin. Thus, this survey was conducted among a representative sample of 490 maize producers in 49 communes of Benin. The representativeness of the producers is ensured because the producers selected for the survey are control producers identified by INRAB and therefore likely to reflect the characteristics of all maize producers in each village. The communes were selected with respect to their appropriate agroecological conditions for maize production. This choice is guided by the existence in the communes of maize seed multipliers and the extension system. Supporting producers in setting up seed companies and extension services to facilitate their access to financial services is one of the components assessed by the PAPA programme through the survey. Of the 490 respondents, 356 respondents produced maize for household consumption while 134 produced improved maize seed.

The collected data provides detailed information on the socio-economic characteristics of producers. The administered questionnaire also addresses issues such as credit constraints, use of improved maize varieties, use of inputs, costs and quantity of production, and yield. This study focuses on the relationship between access to credit and productivity. To do this, only data on maize producers for household consumption were considered. Indeed, as previously specified, the two groups of producers do not face the same technical constraints of production. For instance, the risk faced by the producer of maize for consumption differs from the risk pertaining to the use of credit for the purpose of seed production. Thus, the sample from which the empirical analyses are made comprises a total of 356 producers. For reasons related to the errors contained in nine (09) observations, they have been deleted. The remaining 347 observations will be used in this study.

The main dependent variable in this study is agricultural productivity. It is measured using yield per hectare. Access to credit used in the selection equation refers to farmers who access formal sector institutions for agricultural credit. The variable measuring access to credit is then considered as an explanatory variable in determining farmers’ productivity. As for the independent variables, we have identified a set of variables suggested by the empirical literature on the subject, the main ones of which are described in Table in the Appendix.

4.2. Methodology

This section describes the empirical approach used to analyse the impact of access to credit on agricultural productivity and the extent of the productivity lost due to the lack of access to financial services by farmers in Benin. Several techniques are used in the literature including the Heckman Selection Model (Pham and Talavera, Citation2018; Aristei and Gallo, Citation2016), the Propensity Score Matching Method (PSM) (Liu et al., Citation2021; Duta and Banedji Citation2018; Alemu and Adesina, Citation2017), the Regime Switching Model (ESR) (see Liu et al., 2019). The advantage of the ESR technique is that it takes into account selection issues. Specifically, it is a matter of assessing the differences in productivity between producers who have access to credit and those who do not. Estimating the effects of access to credit poses two methodological problems: unobserved heterogeneity and sample selection bias.

To control for these potential problems of selection and unobserved heterogeneity, we apply the Endogenous switching regression model to estimate the yield of farmers that have access to credit and those who do not (Agbodji & Johnson, Citation2019; Ali and Deininger, Citation2012,Diamoutene & Jatoe, Citation2020;Guirkinger & Et Boucher, Citation2008;Lokshin & Et Sajaia, Citation2004). In a first step, a probit model is used to estimate the determinants of farmers’ access to credit from a number of socio-economic and credit variables identified as theoretically likely to influence the availability of access to or non-access to credit. Second, regressions of productivity models are applied separately depending on whether or not the producer has access to credit.

Let us consider , a latent variable that defines the status of the producer with or without access to credit and

his level of productivity.

The regression model with change of regime is specified as follows:

Where and

are the exponents of credit access and non-access, respectively. In Equationequation 3

(3)

(3) , the binary variable

takes the value 1 if the latent variable

in Equationequation 2

(2)

(2) is strictly positive; which corresponds to the situation where the producer has access to credit. Otherwise, the binary variable

takes the value 0; which implies instead that the farmer does not have access to the credit market.

In Equationequations 1(1)

(1) and Equation2

(2)

(2) ,

denotes a vector of variables that can influence both the state of access to credit and the productivity

such as the characteristics of the producer such as age, gender, the level of education.

designates the set of variables that affect only the productivity of the farmer without having any influence on the possibility of having access to credit or not, such as access to extension services.

is a vector of instrumental variables that do not directly influence the productivity of the farmer, but that do influence access to credit. We use in this study as an instrument the ownership of non-agricultural assets because these assets can be used as collateral for obtaining credit from microfinance institutions (MFIs). This variable does not have a direct impact on productivity. D. A. Ali et al. (Citation2014) used the sale value of household assets in their case. In the absence of such a variable, we believe that using the ownership of non-agricultural assets as an instrument is appropriate given the practices in MFIs in Benin.

,

,

and

are parameters to be estimated. The error terms in the two regimes (

,

,

) are assumed to follow a trivariate normal distribution with a zero mean and a covariance matrix equal to

.

Unobserved factors affecting the selection regime may also affect the productivity of the farmer. Lee (Citation1978) and Maddala (Citation1983) note that the terms and

can be correlated and make estimators from ordinary least squares (OLS) inconsistent. To address this problem with the endogenous switching regression model, the estimation of the selection and productivity equations is performed simultaneously using the full information likelihood method. This method has the advantage of obtaining estimates of robust standard errors, in contrast to methods that proceed step by step by estimating the equations separately (Guirkinger & Et Boucher, Citation2008;Lee, Citation1978;Petrick, Citation2004).

Under the assumptions made on the distributions of the error terms of EquationEquations 1(1)

(1) and Equation2

(2)

(2) , and according to Lokshin and Et Sajaia (Citation2004), the log likelihood function of the switching regression model is given by:

Where a cumulative normal distribution function,

is a normal density distribution function and:

With the correlation coefficient between

and

;

the correlation coefficient between

and

, with

and

respectively the covariance of

and

,

and

.

,

and

represent the respective standard deviations of

,

and

.

The results of estimating EquationEquation 4(4)

(4) using the full information likelihood method will be used to determine the potential productivity gains or losses resulting from the removal of access to agricultural credit or the level of productivity that could be reached by farmers without access to credit if they saw the removal of barriers to access to credit. The procedure will therefore consist of estimating of

for farmers who do not have access to credit. Using EquationEquations 1

(1)

(1) and Equation2

(2)

(2) , and according to Guirkinger and Et Boucher (Citation2008), the expected value of the productivity differential

conditionally in the state of no access to credit (

) is given by:

Where and

are parameters to be estimated from the regression model with change of regime.

The higher the value of the differential forecast, the greater the loss of the productivity due to the lack of access to credit. If this is the case, then it would be urgent to put in place a mechanism to correct the problems of imperfections in the credit market to improve access to financial services for small farmers.

Prior to the estimation of the different models that have just been described, we will present the descriptive analysis showing the possible links between the main variables of the study. This descriptive analysis is discussed in Section 5.

5. Results and discussions

5.1. Descriptive analysis

As part of this work, a descriptive analysis is done before the actual econometric estimates. Thus, a descriptive analysis was performed on the main variables included in the study. Table below presents the main results. From the results in Table , it appears that the surveyed maize producers recorded an average yield of 1283.38 Kg per ha with a maximum yield of 5650 Kg/ha against a minimum of 183.33 Kg/ha.

Table 2. Descriptive statistics of the main variables

The variability around this average is of the order of 761.25 Kg/ha. Producers achieved this average yield while averaging an area of 2.39 ha. The largest area planted by the producers in the sample is 4 ha compared to a minimum of 0.1 ha. In order to plant this area, a number of factors of production have been used. In fact, the producers surveyed used on average 198.83 kg of inputs per hectare, 94.74 kg of seed on a plot. In addition, the surveyed producers have an average age of 52.05 years with the oldest aged 95 versus 30 for the youngest producer.

Trying to fill the resource gap, some producers resort to financial institutions. Out of the 356 producers in the sample, 19,94% have access to credit against 80,06% who do not. A cross-analysis was performed between yield and access to credit as shown in Table . Approximately 19.94% with access to credit produce an average of 1672.268 Kg per ha against 1186.499 Kg per ha for producers without access to credit (80.06%). Farmers who have access to credit therefore realize an average yield slightly above the average of their counterparts who do not have access to itFootnote6 . The Chi2 test of equality between the means reveals that this difference observed between these two groups is significant. This result predicts a positive effect of access to credit on yield. In contrast, producers with access to credit have an average of 2.29 ha, which is below the average for all producers (2.38 ha) and that of producers who do not have access to credit. In fact, those who do not have access to credit exploit an area of 2.41 ha, which is therefore above the average for all producers. However, the equality test carried out shows that the difference in the farmed area observed between the two groups of producers is not significant.

Table 3. Socioeconomic characteristics of producers according to access to credit

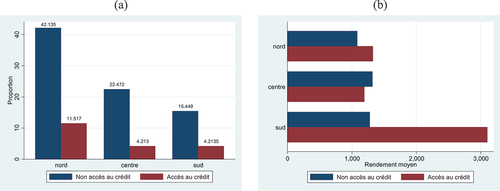

In addition, access to credit differs sensitively across regions of the country. Overall, the trend shows that problems of access to credit are common in all regions of Benin. Farmers who have access to credit are largely in Northern region, where more than half of the producers in the sample (53%) are concentrated. However, the North is also the region of the country where the problem of inaccessibility to credit is more pronounced (Figure ). North Benin is also the region where population density is lowest thus allowing for access to large areas of agricultural land. Unfortunately, most farmers in this region do not have access to credit. However, as described in Figure , we find that access to credit could lead to an increase in the yield per hectare for these producers in the North.

Figure 1. Access to credit by region and average regional yield by access to credit.

Despite these statistics, we note that the best performances in terms of average yield were obtained overall in the South and the Centre (see Figure ). However, it is not easy to show the likely effect of access to credit on the producers’ performance in terms of yield based only on these descriptive statistics. We therefore conducted further analysis using econometric techniques and present the estimates in the next section.

5.2. Determinants and impacts of access to credit

This section presents the main econometric results regarding the effects of access to credit on the productivity of farmers. The estimated coefficients of the variables by the full information maximum likelihood method using endogenous switching regression model are reported in Table . The estimated correlation coefficient between the credit access equation and the productivity equations () is significantly different from zero. The results confirm that there are both observable and unobservable factors that determine farmers’ access to credit and their productivity depending on whether or not they have access to credit. The significance of the correlation coefficient between the access to credit equation and the productivity equation of farmers who have access to credit suggests that there was self-selection in accessing credit. Likewise, the differences in the coefficients of the productivity equation of farmers with access to credit and those without access illustrate the presence of heterogeneity in the sample.

Table 4. Estimation of the endogenous switching regression model

More concretely, the estimates lead to two main results. They make it possible to identify the main determinants of farmers’ access to credit. The main explanatory factors of agricultural productivity depending on access or not to credit are also highlighted.

From the results reported in column (3) of Table , it appears that the adoption of improved seeds, the geographic location, the area sown and member of peasant organization determine producers’ access to credit. Thus, farmers who have at least the primary level, are likely to have access to credit.

Access to credit is also positively associated with the use of fertilizers by farmers. The use of agricultural inputs such as fertilizer requires producers to incur expenses and leads them to seek loans from financial institutions. A similar case can be made for the adoption of improved seed varieties by farmers. The adoption of best practices that would lead to increased production indeed represents intangible guarantees that further reassures loan officers in financial institutions. Houeninvo et al. (Citation2020) have also shown that the adoption of improved seed varieties is associated with an increase in productivity allowing farmers to increase their income. The supply of quality inputs and seeds is one of the criteria that condition the disbursement of loans by MFIs in Benin. (AgriProFocus, Citation2016). The guarantee of high productivity is indeed associated with the use of improved seeds and reduces the uncertainties associated with agricultural activity. Reducing these uncertainties to facilitate producers’ access to credit is one of the components of the PAPA programme as mentioned in the previous section.

Regarding the explanatory factors of farmers’ productivity, there are differences depending on their access to credit or not. The estimated parameters of the productivity model for farmers without access to credit and those who do have access to it are reported in columns (1) and (2) respectively. The use of fertilizers is crucial in explaining productivity especially for the farmers with access to credit. The determining role of fertilizers in the growth of agricultural productivity as we have demonstrated is also widely demonstrated in the literature (Rehman et al., Citation2019; Chandio et al., 2019;Asante et al., Citation2019). The farm size appears to be negatively associated with productivity for both categories of farmers. An increase in the area sown results in a decrease in yield, reflecting the extensive nature of Beninese agriculture. This result is in contrast to the results of Chandio et al. (2019), Abdallah (Citation2016) and Tijani (Citation2006). The latter indeed found a positive and significant relationship between farm size and rice yield. Their result can be justified by the investment in equipment and seeds required for rice production.

In addition, the results suggest that the productivity of farmers without access to credit is also determined by education, fertilizer use, and total labour. Among producers with access to credit, being located in the central region of the country negatively influences productivity. The policy of distributing agricultural inputs, particularly fertilisers, which favours cotton growers in Benin, could explain this result. Producers in the central and northern parts of the country benefit more from fertilisers because they grow most of their cotton. Maize, which is a back-season crop in these two regions, benefits from the after-effects of the fertiliser initially applied to the land. Unsurprisingly, the use of improved seeds provided to producers by deconcentrated services has had positive effects in terms of improving production. The government’s decision to deploy technical agents throughout the country has undoubtedly enabled producers to adopt improved seeds.

From the results thus obtained, we determined whether or not access to credit generates a gain in productivity. The findings suggest that farmers with access to credit obtain a productivity gain compared to those without access to credit (see Table and Figure ). Indeed, there has been an improvement in the productivity of farmers with access to credit. Access to credit leads to an increase in yield per hectare estimated at 1602.625 kg/ha against 1144.151 kg/ha for the counterfactual, i.e. an estimated increase of 40.07%. Several reasons can justify this good performance recorded among farmers with access to credit. Otsuka and Larson (Citation2016) argue that access to credit enables farmers to adopt the best production technologies and acquire quality inputs. Access to credit offers the possibility for farmers to hire quality labour on their farms, which ensures they set up production under the most optimal conditions.

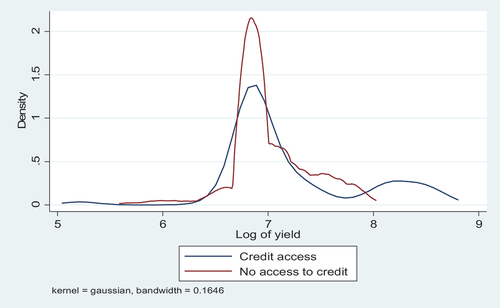

Figure 2. Kernel density of the logarithm of yield according to access to credit. (Source: Author based on estimating results).

Table 5. Productivity difference according to access to credit or not

The results regarding productivity gains are consistent with previous empirical work. Indeed, Diamoutene and Jatoe (Citation2020) also found that credit is positively related to maize yield in Mali. Specifically, they find an average increase of productivity due to credit that is estimated at 477 kg per acre. The positive gains highlighted in this paper also confirm the findings reached by Agbodji and Johnson (Citation2019) for Togo. Maize farmers, beneficiaries of agricultural credit, improve their productivity by about 10.7%. The effect found by E. Ali and Awade (Citation2019) for Soybeans is smaller and estimated at 1.35%. Nakano and Magezi (Citation2020) find that improved access to credit for rice farmers in Tanzania is insufficient to lead to productivity gains. However, the authors emphasise that their results should be analysed with caution, as the negative impact of weather conditions could have outweighed the potential benefits of access to credit for rice farmers.

6. Robustness analysis

In order to test the robustness of our results, we use another productivity indicator, capital productivity, measured as the ratio of output to capital. The results obtained are consistent with the estimates made with the variable yield per hectare. More concretely, the preliminary verifications lead us to validate the model thus estimated (see Table in the Appendix). Indeed, we obtain a significant correlation coefficient between the productivity equations and the credit access equation (). The coefficient is indeed significantly different from zero, suggesting that access to credit affects producers in the two groups differently.

The results broadly confirm those obtained previously. On the one hand, the use of improved seed varieties and membership of a farmer organisation positively determine farmers’ access to credit. On the other hand, the quantity of fertiliser used and the cost of fertiliser have positive and negative effects respectively on the farmer’s productivity. Another more interesting result is that, according to the productivity gain estimate, access to credit improves capital productivity by 31.97% (see Table ).

Table 6. Capital productivity difference according to access to credit or not

In other words, a franc invested in maize production would yield more for the farmer who has access to credit than for his counterpart without access to credit. However, the effect is slightly below the 40.07% obtained with yield measured in Kg per hectare. This suggests that access to credit leads to an improvement in production per CFA, but less than proportionally to the resulting increase in Kg per hectare. The difference may be attributable to the magnitude of the transaction costs faced by farmers. An illustration is the effect of the cost of fertiliser used, which in absolute terms reduces the productivity of farmers with access to credit more than those without (see Table in the Appendix).

7. Conclusion and policy implications

Agricultural productivity in developing countries (DCs) remains low and below the attainable levels. Insufficient productivity is a threat to food security in these countries where poverty levels are worrying. The poor access of producers to financial services such as agricultural credit is one of the factors that explain this low productivity. This article aimed to determine whether or not access to credit improves agricultural productivity in Benin. The analysis is based on the estimation of the Endogenous Switching Regression (ESR) model. The results identified the main factors that determine farmers “access to credit on the one hand and farmers” productivity on the other. Indeed, this study shows that the adoption of improved seeds, the geographic location, the area sown and member of peasant organization determine producers’ access to credit Also, the results of the ESR model suggest that farmers with access to credit present a higher productivity level compared to farmers who do not.

Two specific questions have been examined in this paper. The first is to identify the determinants of access to credit and farmer productivity and the second is to assess the productivity effect of access to credit. In view of the results of the impact assessment of access to credit, some measures could be taken to refine the public intervention strategies that aim to support the agricultural sector, in particular the food sectors. The policy implications we formulate are therefore aimed at improving access to credit for farmers, in particular maize producers.

The positive effect highlighted in this study suggests that it is advantageous for decision-makers to facilitate access to finance for maize producers. The Beninese authorities, having included the maize sector among their priority sectors, must further strengthen the financing mechanisms for producers. In fact, the National Agriculture Development Fund (FNDA), which is the relay of the Regional Agricultural Development Fund, will have to redefine the instruments and/or means of promoting agricultural financing The results of this research suggest that actions should be taken both at the upstream level to facilitate access to finance and the downstream level to ensure the efficiency of credit in terms of productivity. It is therefore appropriate, in the operationalisation of the support intended for microfinance institutions (MFIs), to make more flexible the refinancing mechanism set up with the FNDA. Periodic evaluation of such a device is necessary to ensure its effectiveness. It will also be necessary to make the conditions of access to agricultural credit for farmers more flexible. The financing mechanism intended for this purpose should be integrated into the objectives of proximity financing pursued by the FNDA’s partner microfinance institutions.

With regard to the constraints identified in this study, there is a need to intensify literacy programmes for farmers to facilitate their access to credit. These adult education programmes need to focus not only on language learning but also, and more importantly, on the concepts of designing a financing project. Likewise, it is necessary to initiate extension actions in order to support most of the farmers to adopt improved seeds since the adoption of improved varieties of seeds is likely to reassure the financial operators who see in it a sure way to increase productivity. A better subsidy policy that supports access to improved seeds should also be considered in order to make them more accessible to producers. However, this policy should be coupled with a good exit strategy from these subsidies, so that the sector remains viable even after the short-term subsidy mechanisms.

Moreover, it is also necessary to take measures to enable farmers in the southern part of the country to access credit. While it is true that the farmers in the south of the country work on small areas, it is also obvious that financial support granted to these farmers would lead to improved productivity and strengthen food security since maize is mainly consumed in this part of the country. It is also important that the public authorities strengthen technical supervision mechanisms of farmers through extension sessions. To this end, the territorial agricultural development agencies (ATDA) could conveniently be called upon to support the training of farmers. Finally, due to the existence of a large proportion of farmers who do not have access to finance, the state actors involved in the promotion of agricultural financing in Benin can make the financial support granted to the agricultural sector more effective.

This study, which is a first in Benin, analysing the effects of farmers’ access to credit, deserves to be examined in greater depth on one particular aspect. Indeed, the positive impact of capital per hectare in the category of farmers who do not have access to credit probably reflects the absence of credit constraints among some of the farmers concerned. The analyses should therefore be further refined by distinguishing between farmers who do or do not have access to credit and those who are constrained. To do this, a survey specifically designed to address this issue is needed.

Acknowledgments

This work was carried out with scientific support from the African Economic Research Consortium (AERC). The authors are grateful to Alessandra Guariglia, Victor Murinde, and Issouf Soumare, for technical support and guidance and to the anonymous referees for their feedback on an earlier draft of this paper.

Disclosure statement

No potential conflict of interest was reported by the authors.

Additional information

Funding

Notes on contributors

Achille Barnabé Assouto

Achille Barnabé Assouto is a researcher affiliated with the Laboratoire d’Economie d’Orléans (LEO) of the University of Orléans and the “Laboratoire de Recherche en Finances et Financement du Développement (LARFFID)” of the University of Abomey-Calavi (UAC). He holds a PhD in economics from the University of Orleans. Since 2018, he has been a lecturer at the Faculty of Economics and Management (FASEG) of the University of Abomey-Calavi (UAC). His research interests include issues on Economic Development, Agricultural policy and Poverty. Author of several publications, his research focuses on agricultural finance, agricultural public policies, development finance and issues related to poverty and vulnerability.

Dewanou Jean-Luc Houngbeme

Dewanou Jean-Luc HOUNGBEME holds a PhD in Economics from the University of Abomey-Calavi (UAC) in Benin and a Professional Master’s Degree in Economics and Management of Intellectual Property from the University of Yaoundé II in Cameroon. Researcher affiliated with the “Laboratoire de Recherche en Finance et Financement du Développement (LARFFID)” and the “Centre de Recherche, d’Analyse et de Politique Economique (CRAPE)” of the University of Abomey-Calavi (UAC), his research interests primarily focus on the relationship between economic growth, welfare, renewable energy consumption and tourism development in natural areas, and beach tourism in particular.

Notes

1. Maize is the first cereal crop in terms of production and is widely consumed in South Benin (seeMAEP, 2016).

2. The FCFA is the local currency of Benin used by the countries of the West African Economic and Monetary Union (UEMOA) 1FCFA = 0.0015Euro.

3. The FNDA was created in 2014 by decree n ° 2014–100 of January 31, 2014 but was not really operational. A more recent decree n ° 2017–304 dated June 21, 2017 with the same purpose was taken by the new political regime.

4. Federation of Local Agricultural Mutual Credit Banks.

5. Benin Mutual Agricultural Insurances.

6. This result has confirmed by the kernel density (see).

References

- Abdallah A. (2016). Agricultural credit and technical efficiency in Ghana: is there a nexus?. Agricultural Finance Review, 76(2), 309–22. https://doi.org/10.1108/AFR-01-2016-0002

- Acclassato Houensou, D., Goudjo, G. G., & Senou, M. M. (2021). Access to finance and difference in family farm productivity in Benin: Evidence from small farms. Scientific African, 13, e00940. https://doi.org/10.1016/j.sciaf.2021.e00940

- Adégbola, P. Y., Adékambi, S. A., & Et Tidjani Serpos, A. A. (2009, Novembre). Microfinance et production agricole : cas de l’anacarde au Bénin. Institut National des Recherches Agricoles du Bénin (INRAB), Rapport d’étude.

- Agbodji, A. E., & Johnson, A. A. (2019). Agricultural credit and its impact on the productivity of certain cereals in togo. Emerging Markets Finance and Trade, 57(12), 1–17. https://doi.org/10.1080/1540496X.2019.1602038

- AgriProFocus. (2016). « Répertoire cartographique des institutions de financement de l’agri business au Bénin. ». Report. 52p. AgriProFocus with DEDRAS and Eminence international. https://images.agri-profocus.nl/upload/post/Répertoire_des_institutions_de_financement_de_l’AgroBusiness_version_finale1508944775.pdf

- Akerlof, G. (1970). The market for ‘Lemons’: Quality uncertainty and the market mechanism. The Quarterly Journal of Economics, 84(3), 488–500. https://doi.org/10.2307/1879431

- Akudugu, M. A. (2016). Agricultural productivity, credit and farm size nexus in Africa: A case study of Ghana. Agricultural Finance Review, 76(2), 288–308. https://doi.org/10.1108/AFR-12-2015-0058

- Ali, E., & Awade, N. E. (2019). Credit constraints and soybean farmers’ welfare in subsistence agriculture in Togo. Heliyon, 5(4), e01550. https://doi.org/10.1016/j.heliyon.2019.e01550

- Ali, D. A., & Deininger, K. (2012). Causes and implications of credit rationing in rural Ethiopia: The importance of spatial variation. World Bank Policy Research Working Paper, 6096.

- Ali, D. A., Deininger, K., & Duponchel, M. (2014). Credit constraints and agricultural productivity: Evidence from rural Rwanda. The Journal of Development Studies, 50(5), 649–665. https://doi.org/10.1080/00220388.2014.887687

- Aristei, D., & Gallo, M. (2016). Does gender matter for firms' access to credit? Evidence from international data. Finance Research Letters, 18, 67–75. https://doi.org/10.1016/j.frl.2016.04.002

- Asante, B. O., Temoso, O., Addai, K. N., & Villano, R. A. (2019). Evaluating productivity gaps in maize production across different agroecological zones in Ghana. Agricultural Systems, 176, 102650. https://doi.org/10.1016/j.agsy.2019.102650

- Assogba, P. N., Haroll Kokoye, S. E., Yegbemey, R. N., Djenontin, J. A., Tassou, Z., Pardoe, J., & Et Yabi, J. A. (2017). Determinants of credit access by smallholder farmers in North-East Benin. Journal of Development and Agricultural Economics, 9(8), 210216.

- Carter, M. R. (1988). Equilibrium credit rationing of small farm agriculture. Journal of Development Economics, 28(1), 83–103. https://doi.org/10.1016/0304-3878(88)90015-6

- Carter, M. R. (1989). The impact of credit on peasant productivity and differentiation in Nicaragua. Journal of Development Economics, 31(1), 13–36. https://doi.org/10.1016/0304-3878(89)90029-1

- Cervantes-Godoy, D., & Dewbre, E. (2010). “Economic Importance of Agriculture for Poverty Reduction”, OECD Food, Agriculture and Fisheries Working Papers, No. 23, OECD Publishing. https://doi.org/10.1787/5kmmv9s20944-en

- Conning, J., & Udry, C. (2007). Rural financial markets in developing countries. Handbook of Agricultural Economics, 3, 2857–2908. https://doi.org/10.1016/S1574-0072(06)03056-8

- Diallo, M. F., Zhou, J., Elham, H., & Zhou, D. (2020). Effect of agricultural credit access on rice productivity: Evidence from the irrigated area of Anambe Basin, Senegal. The Journal of Agricultural Science, 12(3), 78. https://doi.org/10.5539/jas.v12n3p78

- Diamoutene, A. K., & Jatoe, J. B. D. (2020). Access to credit and maize productivity in Mali. Agricultural Finance Review. 81(3). 458–477. https://doi.org/10.1108/AFR-05-2020-0066.

- Dutta, A., & Banerjee, S. (2018). Does microfinance impede sustainable entrepreneurial initiatives among women borrowers? Evidence from rural Bangladesh. Journal of Rural Studies, 60, 70–81. https://doi.org/10.1016/j.jrurstud.2018.03.007

- Ejigu, A. A., & Adesina, J. O. (2017). In Search of Rural Entrepreneurship: Non-farm Household Enterprises (NFEs) as Instruments of Rural Transformation in Ethiopia. African Development Review, 29(2), 259–271. https://doi.org/10.1111/1467-8268.12255

- Feder, G., Lau, L. J., Lin, J. Y., & Et Luo, X. (1990). Credit Relationship Agriculture: Productivity the Disequilibrium. American Journal of Agricultural Economics, 72(5), 11511157. https://doi.org/10.2307/1242524

- Guirkinger, C., & Et Boucher, S. R. (2008). « Credit constraints and productivity in Peruvian agriculture ». Agricultural Economics, 39(3), 295308. https://doi.org/10.1111/j.1574-0862.2008.00334.x

- Houeninvo, G. H., Célestin Quenum, C. V. & Nonvide, G. M. (2020). Impact of improved maize variety adoption on smallholder farmers’ welfare in Benin. Economics of Innovation and New Technology, 29(8), 831–846. https://doi.org/10.1080/10438599.2019.1669331

- INSAE/EMICoV. (2015, octobre). Enquête Modulaire Intégrée sur les Conditions de Vie des Ménages (EMICOV). Note sur la pauvreté au Bénin en 2015. INSAE.

- Khandker, S. R., & Et Koolwal, G. B. (2014). How has microcredit supported agriculture? Evidence using panel data from Bangladesh. Agricultural Economics, 46(2015), 1–12.

- Khan, M. N., Khan, M., Abassi, S. S., Ali, A. M., & Noshed, S. (2013). The effect of Zarai Taraqiati bank in enhancing farm productivity through agricultural credit - a case study of district Lakki Marwat, KPK-Pakistan. Research Journal of Agriculture and Forestry Sciences, 1(8), 1–4.

- Lee, L. (1978). Unionism and wage rates: A simultaneous equations model with qualitative and limited dependent variables. International Economic Review, 19(2), 415–433. https://doi.org/10.2307/2526310

- Liu, T., He, G., and Turvey, C. G. (2021). Inclusive Finance, Farm Households Entrepreneurship, and Inclusive Rural Transformation in Rural Poverty-stricken Areas in China. Emerging Markets Finance and Trade, 57(7), 1929–1958. https://doi.org/10.1080/1540496X.2019.1694506

- Lokshin, M., & Et Sajaia, Z. (2004). Maximum likelihood estimation of endogenous switching regression models. The Stata Journal, 4(3), 282–289. https://doi.org/10.1177/1536867X0400400306

- Maddala, G. (1983). Limited-dependant and qualitative variables in econometrics. Cambridge University Press.

- MAEP. (2016). Rapport de Performance du Secteur Agricole, Gestion 2016. https://api.sitetest.agriculture.gouv.bj//media/63ce96fa517c5_7_Rapport%20de%20performance%202016%20sect%20%20agricole.pdf

- MAEP. (2017). Plan Stratégique de Développement du Secteur Agricole (PSDSA) 2025 et Plan National d’Investissements Agricoles et de Sécurité Alimentaire et Nutritionnelle PNIASAN 2017 – 2021. Ministère de l’Agriculture de l’Elevage et de la Pêche (MAEP), Mai, 139.

- MAEP. (2022). Rapport de Performances du Secteur Agricole, Gestion 2021. MAEP. https://api.sitetest.agriculture.gouv.bj//media/63ce982dee910_12_Rapport%20de%20performance%20du%20secteur%20agricole_gestion%202021.pdf

- Magrini, E., Balié, J., & Et Morales-Opazo, C. (2017). Price signals and supply responses for staple food crops in Sub-Saharan Africa. Applied Economic Perspectives and Policy, 0(0), 1–21. https://doi.org/10.1093/aepp/ppx037

- Mahoukede, K. M., Aliou, D., & Gauthier, B. (2015). Impact of Use of Credit in rice farming on rice Productivity and Income in Benin. Communication in International Conference of agricultural Economists, Milan, pp. 1–29.

- Markelova, H., Meinzen-Dick, R., Hellin, J. & Dohrn, S. (2009). Collective action for smallholder market access. Food Policy, 34(1), 1–7. https://doi.org/10.1016/j.foodpol.2008.10.001

- Martey, E., Wiredu, A. N., Etwire, P. M. & Kuwornu, J. K. M. (2019). The impact of credit on the technical efficiency of maize-producing households in Northern Ghana. AFR, 79(3), 304–322. https://doi.org/10.1108/AFR-05-2018-0041

- MDAEP, PNUD. (2015). Rapport National sur le Développement Humain (RNDH) 2015. Agriculture, Sécurité alimentaire et développement humain au Bénin. Ministère du Développement, de l’Analyse Economique et de la Prospective (MDAEP) et Programme des Nations Unies pour le développement (PNUD). https://planipolis.iiep.unesco.org/sites/default/files/ressources/rndh_2015_benin.pdf

- Moser, C. M., & Barrett, C. B. (2006). The complex dynamics of smallholder technology adoption: The case of SRI in Madagascar. Agricultural Economics, 35(3), 373–388. https://doi.org/10.1111/j.1574-0862.2006.00169.x

- Nakano, Y., Kajisa, K., & Otsuka, K. (2016). On the possibility of a rice green revolution in irrigated and rainfed areas in Tanzania: An assessment of management training and credit programs. In K. Otsuka & D. L. Larson (Eds.), Pursuit of an African green revolution: Views from rice and maize farmers’ fields (pp. 39–64). Springer.

- Nakano, Y., & Magezi, E. F. (2020). The impact of microcredit on agricultural technology adoption and productivity: Evidence from randomized control trial in Tanzania. World Development, 133, 104997. https://doi.org/10.1016/j.worlddev.2020.104997

- Njeru, T. N., Mano, Y., & Otsuka, K. (2016). Role of access to credit in rice production in Sub-Saharan Africa: The case of Mwea irrigation scheme in Kenya. Journal of African Economies, 25(2), 300–321. https://doi.org/10.1093/jae/ejv024

- Nwaru, J. C., & Onuoha, R. E. (2010). Credit use and technical change in smallholder food crop production in Imo state of Nigeria. New York Science Journal, 3(11), 144–151.

- OCDE, FAO. (2016). OECD-FAO Agricultural Outlook 2016-2025, 136. https://www.oecd-ilibrary.org/content/publication/agr_outlook-2016-en

- Otsuka, K., & Larson, D. F. (2016). In pursuit of an African green revolution. Springer.

- Petrick, M. (2004). A microeconometric analysis of credit rationing in the Polish farm sector. European Review of Agricultural Economics, 31(1), 23–47. https://doi.org/10.1093/erae/31.1.77

- Pham, T., & Talavera, O. (2018). Discrimination, Social Capital, and Financial Constraints: The Case of Viet Nam. World Development, 102, 228–242. https://doi.org/10.1016/j.worlddev.2017.10.005

- Rehman, A., Chandio, A., Ali Hussain, I., & Jingdong, L. (2019). Fertilizer consumption, water availability and credit distribution: Major factors affecting agricultural productivity in Pakistan. Journal of the Saudi Society of Agricultural Sciences, 18(3), 269–274. https://doi.org/10.1016/j.jssas.2017.08.002

- Salami, A., Kamara, A. B., & Brixiova, Z. (2010). Smallholder agriculture in East Africa: Trends, constraints and opportunities (pp. 52). Tunis, Tunisia: African Development Bank.

- Saqib, S. E., Kuwornu, J. K., Panezia, S., & Ali, U. (2018). Factors determining subsistence farmers' access to agricultural credit in flood-prone areas of Pakistan. Kasetsart Journal of Social Sciences, 39(2), 262–268. https://doi.org/10.1016/j.kjss.2017.06.001

- Seck, A. (2019). Heterogeneous credit constraints and smallholder farming productivity in the Senegal River Valley. Emerging Markets Finance and Trade, 57(12), 1–19. https://doi.org/10.1080/1540496X.2019.1601080

- Sossou, C. H. (2015). Le financement de l’agriculture au Bénin : stratégies de gestion et d’adaptation des exploitations. Université de Liège.

- Stiglitz, J. E., & Weiss, A. (1981). Credit rationing in markets with imperfect information. The American Economic Review, 71(3), 393–410.

- Stiglitz, J. E., & Weiss, A. (1983). Incentive effects of terminations: Applications to the credit and labor markets. The American Economic Review, 73(5), 912–927.

- Tijani, A. A. (2006). Analysis of the technical efficiency of rice farms in Ijesha Land of Osun State, Nigeria. Agrekon, 45(2), 126–135.

- Wampfler, B., & Et Mercoiret, M. -R. 2002. Microfinance, organisations paysannes : quel partage des rôles, quels partenariats dans un contexte de libéralisation?Le financement de l’agriculture familiale dans le contexte de libéralisation : quelle contribution de la microfinance. B. Wampfler, C. Lapenu, & M. Roesch. Eds., Actes du Séminaire internationalCirad/Cerise: 21-24. janvier 2002.

- WFP (2017). Analyse Globale de la Vulnérabilité et de la Sécurité Alimentaire (AGVSA 2017), World Food Programme Service de l’Analyse de la Sécurité Alimentaire (VAM), 170 https://instad.bj/images/docs/insae-statistiques/enquetes-recensements/Autres-Enquetes/AGVSA/Rapport_AGVSA_VF_2017.pdf

- Zedillo, E. (2015). Overview (O. Cattaneo & H. O. Wheeler, Eds.), Yale Centre for the Study of Globalization.

Appendix

Table A1. Definitions and measures of study variables

Table A2. Estimation of the endogenous switching regression model

Figure A1. Maize yield from 2011 to 2020 (Kg/ha).

Source: Authors from FAOSTAT data (2022)