Abstract

The main impetus of the research is to inquire into the fintech adoption behaviour of India’s GenY population. The focus of this research paper is to enlarge the scope of the planned behaviour theory by including other exogenous variables, information quality (IQ), and readiness to pay for privileges. Responses from the 349 selected higher education students based on judgmental sampling were collected from various institutes of repute in India. The suggested framework was evaluated using the Smart PLS 4 software bootstrapping method. It was found that multiple hypotheses framed in the study exert notable impact besides the belief that there is a direct linkage between observed behavioural control (OBC) and actual intention (AI). The paper confirms the application of the theory of planned behaviour for the effective implementation of fintech in India. It was observed that information quality is one of the crucial elements which influences the fintech adoption behaviour. The research enriches past studies by expanding the blueprint of a theory of planned behaviour by identifying the information quality factor as the influencing intent and behaviour. The reliability and validity of the suggested framework were analyzed after keeping in mind the impact of a business environment’s constantly changing dynamic forces. The study identified the primary constructs affecting the fintech adoption behaviour with a particular focus on the GEN Y population of India. It will also help the financial technocrats to optimally utilize the immense underlying capabilities of the fintech users and strategically launch more user-friendly products and services.

1. Introduction

A nation’s overall development may be tied directly to the sophistication and progress of its technological infrastructure. It helps to design policies to control the competition and entrance of private actors in an economy. It is beneficial in formulating policies. The term “financial technology” refers to an innovative, revolutionary, and up-to-date system that helps an effective and seamless flow of economic transactions (Knewtson & Rosenbaum, Citation2020). Fintech is a syneresis of the word financial technology. It is a convergence of technological equipment, processes, and ecological communities, making commercial transactions much more accessible, approachable, optimized, and resourceful. The provision of monetary disbursement, financing, advancing, buying and selling of stocks, and exchange of currencies are all examples of the kinds of finance-related services that may be significantly influenced by the innovative medium of fintech

Over the most recent few years, the economy of India has been moving through the era of the most swiftly spiraling digital expansion. It is anticipated that by 2023, digital technology will have seen an enormous increase. The amount of time spent online will rise by forty percent. It is expected that there will be between 750 million and 800 million people using the internet. The number of people who use smart phones is expected to rise from 650 million to 700 million (McKinsey Global Institute, Citation2019). The Indian economy was estimated to be worth $85–90 billion in 2020. It is expected to skyrocket to $Business 800 billion by 2030 (Business Today, Citation2022). It is due to several positive factors, such as increased access to digital facilities, rising incomes, and a growing population of young people (The Economics Times, Citation2022). In addition, after the COVID-19 epidemic, India grew to become the world’s second-biggest emerging hotspot for fintech, behind only the United States (Bhasin & Gulati, Citation2021). Research analysts Boston Consulting Group (BCG) and Federation of Indian Chambers of Commerce and Industry (FICCI), in their joint project, forecasted that the value of the financial technology (fintech) industry in India would skyrocket to between $150–160 billion US dollars by the year 2025. Within the next several years, the fintech sector will be responsible for creating the most significant number of unicorns (India Briefing, Citation2022).

According to World Bank Findex Report 2021, 22% of adults in India are unbanked. Almost 540 million people in India who have an account make no use of technology in making payments. The report identified several reasons, namely, inadequate information quality, highly charged banking services, far away location of banking facilities, trim income level, requisite incomplete documents, low trust, insufficient banking needs, lack of mobile handset, taking help of others in financial transactions (Times of India, Citation2021b). Therefore, it is most appropriate to include information quality as a predictor and readiness to pay for privileges as the moderating variable in the existing theory of planned behaviour to measure the cause and effect of the actual adoption of fintech by the young Indian. This study has a one-of-a-kind place in the context of the Indian scenario, which was carried out for several different reasons. Firstly, The mechanization of the Indian financial sector results in the radical transformation and development of the economy (Sheokand & Gupta, Citation2017). Fintech leads to cost reduction, volume enhancement of financial transactions, increased employment opportunities, and increased financial literacy (Saba et al., Citation2019); Secondly, fintech enables financial institutions to adopt green technology such as green finance and green innovations. It allows the corporates to adopt environmentally sustainable policies by adopting a pro-environmental attitude, more dependence on renewable sources of energy, proper management of trash, and growth of the green industry. (Yan et al., Citation2022). Third, individuals were compelled to remain in their homes during the lockdown period. During the pandemic period, people were forced to face enormous kinds of economic and social volatility. They were compelled to use the internet and electronic devices to communicate with customers. They were given support and encouragement through digital technology, ultimately leading to changes in their consumption patterns (Yan et al., Citation2021). Fourth, the demonetization policy implemented in India in 2016 assumed that the country had ample cash reserves despite widespread tax evasion. That’s why the government of India decided to return to using the old currency instead of the new one. At that time, customers were coerced into using technology, which resulted in a significant behavioural shift on the part of consumers about financial technology (Bahl et al., Citation2022). Fifth, the main objective of the Digital India Mission is to expand people’s access to internet connection by cultivating an atmosphere that is hospitable, transparent, open, and responsive. The mission assists customers in more readily adopting modern information and communications technologies (Maiti et al., Citation2020). It is anticipated that the introduction of 5 G technology will give rise to a new ecological community of fintech companies in India. India’s banking and financial industry is set to undergo a massive transformation due to the advent of 5 G technology (Mohanasundaram et al., Citation2021).

In light of Ajzen’s theory of planned behaviour in 1991, the present research was intended to investigate multitudinous ways in which millennial generation members in India interact with financial technology. A person is considered a member of Generation Y if born between 1981 and 1996. This current generation relies heavily on many forms of digital media. They spend around 17 hours every week on the internet. They have a wealth of information and are resourceful. While making a buying choice, they do in-depth research on the internet (Jain et al., Citation2021). Gen Y comprises 23 percent of the planet’s total population. Thirty-four percent of people belong to Generation Y, the Indian population.

India has become the most critical market for millennials everywhere in the globe. This younger generation plays an important and transformative role in today’s society (The Times of India, Citation2021a). They are characterized by a unique driving force that sets them apart from people of other age groups. India has a median age of 28 years, while the United States, China, and Japan each have respective median ages of 38, 37, and 47. It indicates that most of India’s population is under 28. The young people of India make up the largest market for goods and services and the most significant labour force in the world. A demographic dividend is a potential financial gain that may be realized when there is a high proportion of employed persons relative to the overall population (United Nations Population Fund). The country’s young people are its most valuable resource because of their potential to bring about significant social upheaval and the critical part they play in the development of any nation. The generation Y population is India’s demographic advantage. They are masters of the internet because they were brought up alongside the application of technology (Nakagawa & Yellowlees, Citation2020). They can maintain their positive attitude thanks to digital technologies. (Sahni, Citation2021).

The inquisitions of researchers notably enrich the knowledge domain in various meaningful ways. The current analysis makes an effort to determine whether or not the theory of planned behaviour framework is legitimate by bearing in mind the many dynamic environment aspects that are significantly unlike those investigated in the previous studies. Second, the present research expands the scope of the theory of planned behaviour framework by considering two more variables, namely information quality (IQ) and readiness to pay for privileges (RPP). Third, researchers contemplated knowing the underlying linkage between the exogenous and endogenous components of consumer behaviour. Fourth, the researchers’ pioneer and test the new variable RPP as a moderator while keeping in mind the requirement of a link between PI and the conduct of fintech companies. In conclusion, the present study will enrich the knowledge domain by raising awareness about how the actions of India’s uneducated Gen Y population may also be influenced by financial technology. It will further assist fintech marketers in formulating highly individualized programs and policies to capitalize on the unrealized potential in this industry. Users fintech adoption intention is primarily based on environmental factors such as social, cultural, assurance, confidence, and faith. Although, most of the previous researches are mainly focused on technological aspects while neglected social implications. Therefore, the present study attempts to fill this research gap by including all the variable from theory of planned behaviour and information quality from information system success model which will add value to the fintech literature.

2. Theoretical framework and hypotheses development

Theory of planned behaviour notes that buying intention (BI) may be broken down into three categories: attitude, social norms, and observable behavioural control. In addition, it has been hypothesized that buying behaviour, abbreviated as BB, may be forecasted by combining all three of these factors. Depending on their respective contexts, the factors mentioned earlier have various consequences on consumers’ intentions to purchase and their actual shopping behaviours (Ajzen Citation1991). He argues that in some situations, just one of the three factors bears a substantial influence on the buyer’s behaviour and buying intent. Despite this, there are other contexts in which the interaction of two or all factors affects purchasing intentions and behaviour. Few studies support the theory of planned behaviour model in forecasting adoption intention and actual intention of fintech-enriched consumers (Aldammagh et al., Citation2021; Mazambani & Mutambara, Citation2020; Niswah et al., Citation2019), whereas some studies partially support the model. (Aldammagh et al., Citation2021; Chang et al., Citation2020; M.C. Lee, Citation2009; Mazambani & Mutambara, Citation2020; Niswah et al., Citation2019). The factors above are investigated in great depth in the following research. According to the theory of planned behaviour postulates, the influence of buying intent on buying behaviour may be broken down into three distinct categories.

3. Attitude (ATT)

An individual’s favourable or unfavourable conduct, which emerges from the individual’s belief of the behaviour and its aftermaths, is the basis of a person’s attitude formation. When it comes to the prediction of purchase behaviour, this is the most crucial proximal variable. It has been shown that a person’s perspective on the practicality and straightforwardness of fintech is correlated to the generation of good psychological intent (Chuang et al., Citation2016). Krivkovich et al. (Citation2020) discovered that during the coronavirus pandemic phase, the southern part of the United States showed substantial support for implementing fintech. According to the research findings, the way people lived throughout this historical period significantly altered how people across the globe live their lives now.

Additionally, it demonstrated a significant effect on technology adoption in money matters. According to Meyliana et al. (Citation2019), the use of technology in financial transactions is unaffected by the risk element involved. The authors stated that the end users in Indonesia had a favourable attitude toward financial technology services. Mehta and Kumari (Citation2021) highlighted the primary reasons for encouraging consumers to adopt fintech in India. Their research was conducted from an Indian viewpoint. The user experience may be enhanced, along with other aspects such as ease, economy, and availability. The optimistic outlook tremendously influences the process of incorporating new technologies. In contrast, Ryu (Citation2018) observed that exposure to legal risk significantly deterrents a buyer’s propensity regarding financial technology usage. Hussein (Citation2021) marked those factors such as gender, amount of wealth, and danger all have a significant negative influence on an individual’s attitude toward and desire to utilize fintech services offered by banks in Yemen.

4. Social Norms (SN)

The concept of social norms focuses on the stresses and strains placed on society about its attachment or detachment from purchasing behaviour. According to the findings of Mohammad and Nawayseh (Citation2020), social networks carry a substantial effect on desires regarding the usage of financial apps. According to Belanche et al. (Citation2019), SN is considerably relevant to users with less understanding of fintech. These consumers are more likely to be found in Anglo-Saxon nations. The social distancing norms practiced during COVID-19 discouraged the usage of analog technology in favour of the increased use of digital devices. As a result, it fosters the development of a new standard set of behaviours among users of fintech (Minh, Citation2021).SN’s influence on purchase intent regarding cryptocurrency adoption is insignificantly negative (Ramchandran & Stella, Citation2022). However, Shubhangi et al. (Citation2020) concluded that there is a considerable detrimental influence of SN on behavioural intention to avail oneself of the services of fintech.

5. Observed Behavioural Control (OBC)

The observed behavioural control of a person is a predicted capacity and strength of that individual, which in turn is another proximal characteristic for forecasting the purchase behaviour of that individual. An individual’s sense of either uninhibitedness or inhibitedness while carrying out certain behaviours is observed behavioural control. It is a person’s emotional state when engaging in such behaviour (Ajzen, Citation1991). It is beneficial in anticipating a person’s purchase purpose and behaviour when it is beyond the capability of self-imposed limitations. It does this by analyzing the individual’s spending history. OBC helps to motivate postgraduate university students in India regarding using cryptocurrencies (Ramchandran & Stella, Citation2022). OBC influences the buyer’s intent to use fintech (Mohammad & Nawayseh, Citation2020). According to Warshaw and Davis’s (Citation1985) definition, it is a buyer’s impression of whether as easy as a pie or hard to endure concerning the performance of specific behaviour. In its most basic form, one’s competency means a person’s trust or confidence in their capabilities to carry out particular behaviour in a given setting. Akhtar and Das (Citation2019) decided to use the term “financial self-efficacy” rather than “OBC” while discussing the situation from an Indian viewpoint. They concluded that a buyer’s financial self-efficacy not only has a significant influence on their personality attributes but also carries a big impact on the buyer’s desire to make a purchase. According to Daniel Antonius (Citation2022), the government of Indonesia devised regulations governing digital money. However, he concluded that the perceived behavioural control of fintech users does not substantially influence such users’ behaviour in terms of adhering to the legislation governing fintech.

6. Adoption intention and actual intention

The possibility that a customer will purchase a particular marketed brand in the following year may be used as a proxy for estimating the consumer’s intention (Myers et al., Citation2000). It refers to the client’s state when they are prepared to purchase products or services. According to Afandi (Citation2021), there is a considerable effect of ATT, SN as well as OBC on buyers’ intent for fintech usage. The researchers Pascual-Miguel et al. (Citation2015) discovered a tangible link between purchasing behaviour and purchasing intent. According to the findings of Nayanajith and Damunupola (Citation2019), there is a considerable influence of OBC on using fintech when using banking services. According to Agrebi and Jallais (Citation2015), the intent to buy a product is a significant factor in adopting and utilizing smartphones.

Furthermore, Talwar et al. (Citation2020) found that the most considerable constraint of technological improvements is consumers’ difficulty adapting to new developments. Further research has shown a low desire to utilize fintech in India. It may be attributed to a lack of readiness concerning the payment of bills online as well as a concern about having an increased tax burden. Researchers Razak et al. (Citation2013) and Escobar-Rodríguez and Carvajal-Trujillo (Citation2014) concluded that intention is not a primary predictor of purchase behaviour.

7. The following hypotheses are stated based on the arguments that were given before in this sentence

H1:

Attitude holds a substantial and favourable influence on the fintech adoption intention.

H2:

Social Norms strongly and favourably influence the fintech adoption intention.

H3:

Observed Behavioural Control holds a substantial and favourable influence on the buyer’s intent to adopt fintech.

H4:

Adoption intention holds a powerful and favourable influence on the buyer’s actual intent to adopt fintech.

8. Information Quality (IQ.)

The quality of the information gets differs for every individual, and this valuation is further influenced by the consumption patterns of those individuals (Peters et al., Citation2007). As per Priyadarshini et al. (Citation2017), the accessibility of high-quality content on various websites favours the users’ mentality about such websites. According to Bizer and Cyganiak (Citation2009), technology users struggle with selecting high-quality information from the plethora of information accessible in cyberspace. Gao et al. (Citation2012) observed that when people are confronted with an abundance of high-quality data that exceeds their cognitive capabilities, it might leave them feeling overwhelmed and confused. Chung, Inuk (Citation2007) found evidence that a substantial increase in the amount and quality of information led to a revolutionary shift in social norms. Erwin et al. (Citation2020) established that observable behavioural control is connected to customers’ intentions—albeit unfavourable. The quality of the information and the user’s attitude are two factors that exert tremendous influence on the buyer’s intent to acquire and operate (Erwin et al., Citation2020; H. Kim & Niehm, Citation2009; Jeong & Lambert, Citation2001). According to research by A. J. Kim and Johnson (Citation2016), information attributes substantially influence buyers’ adoption intent. Nagaraju (Citation2015) found that information quality is essential for customer satisfaction while using fintech. Almajali et al. (Citation2023) conducted their study during the coronavirus pandemic period. They found a positive relationship between information quality and intention to adopt and use the latest technology.

H5:

IQ holds a strong and favourable influence on ATT

H6:

IQ holds a strong and favourable influence on SN

H7:

IQ holds a powerful and favourable influence on OBC

9. Readiness to Pay for the Privileges (RPP)

Zhang et al. (Citation2020) indicated that the most significant risk to the world at this time is using a considerable quantity of energy. There is widespread adoption of energy-efficient financial technology devices all around the globe to make a low-carbon economy. It was determined that a significant positive association exists between the buyer’s purpose to use these devices and their willingness to pay for the rights. According to Nomura and Akai (Citation2004), using non-depletable resources in energy generation contributes to reducing greenhouse gas emissions, which benefits the environment. Compared to the cost of producing power using exhaustible resources, the cost of producing electricity using limitless resources is much higher. It was discovered that Japanese people are willing to pay extra if it means the environment is protected. According to Yalcıntekin and Saygili (Citation2020), the increased willingness of customers to spend a higher price for the purchase of tech-savvy products is correlated with an accelerated utility derived from technology usage. There is a significantly favourable relationship between the attractiveness of technical devices and the willingness to pay for the advantages (E.J. Lee, Citation2022). The research conducted by Stephanie and her colleagues in Citation2022 concluded that the social, psychological, and environmental elements that influence the acceptance and use of fintech impact the willingness to pay for the advantages. It is primarily seen that fintech is deeply penetrated in the countries where it is provided at a high cost. Philippon (Citation2016) observed in the United States that despite the high price of fintech services, customers are ready to adopt fintech services as it increases productivity and efficiency (See Figure ).

Figure 1. Conceptual Model.

H8: RPP holds a powerful and favourable influence on the buyer’s actual intent

H9: RPP moderates the relation between adoption intention and actual intention of fintech

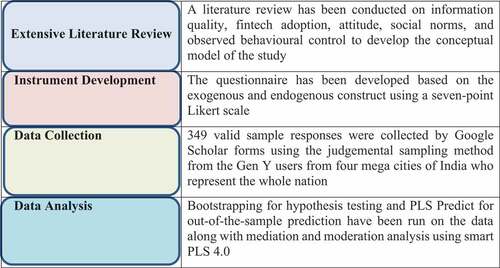

10. Research methodology

The needed number of samples for the PLS-SEM 4 analysis is ten times the most significant number of arrowheads pointing in the direction of the variables. It is done so that the research may be carried out (Hair et al., Citation2014). The current investigation used a standardized questionnaire that had a total of 31 different questions. Finally, this research requires essentially 40 respondents, which is calculated by multiplying 4 and 10.

When picking students obtaining their higher education from various institutions in India, the authors opted to use a judgemental sample strategy. The students chosen to participate are typical members of Generation Y, who are heavy users of various forms of financial technology in their day-to-day activities. While gathering the students’ participation information, it was ensured that every student had an equal opportunity to do so. An electronic questionnaire was sent to them in September 2022 through email IDs and WhatsApp groups established by their respective institutions. After three weeks, a friendly reminder of the online questionnaire was sent again over the same email -id and WhatsApp groups. The online questionnaire, in its entirety, was sent out, and a total of 405 completed questionnaires were obtained. Because there was inadequate information and an excessive amount of deviation, only 349 of the responses to the questionnaire that were filled out were chosen for the in-depth study. The actual response rate that was achieved as a consequence is denoted by 86%. The demographic distribution of the respondent’s profile is as under:

The demographics of the respondents include a male representation of 52.14% and a female representation of 47.86%. Additionally, 37.24% of respondents were between the ages of 18 and 22, 37.53% were between the ages of 22 and 26, and 25.23% were between the ages of 26 and 30. Regarding educational levels, 21.48% had completed their bachelor’s degrees, 25.80% had completed their postgraduate degrees, 52.72% were professionals. Regarding the respondents’ monthly income, 20.91% made less than 2,000,00, while 28.65% earned between 2,000,00 and 500,000. 26.64% of people brought home between 500,000 and 1,000,000, while 23.8% earned more than 1,000,000 monthly. Those respondents already utilizing fintech or considering switching to fintech were counted as respondents.

The results of an electronic survey consisting of 25 questions are depicted in the forthcoming table. The e-questionnaire used in the study comprised four questions exhibiting information quality, three questions showing attitude, four questions demonstrating observed behavioural control, four questions indicating social norms, four questions showing adoption intention, three questions exhibiting privilege to pay, and three questions displaying actual intent (See Figure ).

Figure 2. Flowchart of research methods.

11. Empirical findings

The authors made different hypotheses based on the conceptualization of their measurement methodology. Measurement and structural models were used to analyze the collected data. Relationships between components and their underlying variables may be identified in the measurement model, while the structural model explains the effect of exogenous factors on endogenous factors.

12. Assessment of measurement model

Factor analysis helps solve the bias caused by the conventional research approach. The EFA analysis was performed on the statements chosen with the assistance of the Harman single factor. According to the Harman single factor technique, the tolerable limit is the value should be less than 50%. The proportion of the variation from a single factor was 25%. Each cross-sectional study of human behaviour has some degree of common method bias (CMB) (Podsakoff et al., Citation2003). CMB may exist if researchers have gathered data on all relevant endogenous and exogenous factors using previously recognized scale items. So, our research used qualitative and quantitative tests to ensure no CMB-related problems in the dataset (T. S. Hew & Kadir, Citation2016). It was clear to respondents in advance that there was no “right” response to any of the questions. The confidentiality of their data was also assured (Leong et al., Citation2019). In this research, we used a variety of scales to measure a wide range of factors. The study’s primary scale variables were all tested using a seven-point Likert scale. Secondary scale factors such as gender and education were measured using two- and four-level nominal scales. The age scale had three levels, whereas the income scale had four (refer to Table ).

Table 1. Demographic profile

Harman’s single factor test retrieved 36.78 percent of the variance, which is less than the cut-off value of 50 percent when dealing with this issue statistically. Therefore, it shows that the CMB is very little in the available data (Podsakoff et al., Citation2003). Due to the limitations of Harman’s single-factor methodology, further, more robust techniques were used to verify CMB. In the first place, CMB was analyzed using VIF (Variation Inflation Factor) values produced from the block and full collinearity test (Kock et al., Citation2012), which shows that the VIF value for each construct is less than the threshold of 3.3 (N. Kock, Citation2015) in an independent block and complete collinearity test. Second, VIF was calculated for every scale and instrument combination. When looking at the current data set as a whole, it is clear that all VIF values for each scale item are lower than the cut-off value of 5 (RM, Citation2007). Because of the above, it is reasonable to conclude that CMB will have no problems using this data set.

With the assistance of reliability and validity, the efficiency of the reflective measurement model may be evaluated (J. F. Hair et al., Citation2011). The values of outer loading and CR need to be more than 0.7, and the importance of AVE has to be greater than 0.5. (Chin, Citation2010; J. F. Hair et al., Citation2011).

The calculations made for outer loading, convergent reliability (CR), and the average variance extracted (AVE) are depicted in Table . The research outcomes for outer loading and CR are shown in the table ; all values are more than 0.70. Additionally, the values of AVE are greater than 0.5.

Table 2. Variables and factors

Table 3. Convergent validity for the reflective measurement model

According to Henseler et al. (Citation2015), the HTMT ratio is used to determine whether or not discriminant validity has been met. Values of the HTMT ratio that are lower than 1.00 are taken into consideration to be acceptable. The findings of the HTMT ratio are given in Table , and it was discovered that every estimated ratio for every pair of constructs had a value lower than the needed value of 1.00. Consequently, the findings provided evidence that the reflective measurement scale has both discriminant and concurrent validity.

Table 4. Discriminant validity- HTMT ratio

The assistance of yet another criterion, namely the FL Criterion, might be used to check the discriminant validity of the model. The values for the diagonals ought to be higher than those for the non-diagonals and are regarded as ideal (Chin Citation2010; Hair et al. 2017). Table demonstrates that all diagonal values are greater than those found outside the diagonal. Since this is the case, the table again satisfies the discriminatory validity requirement.

Table 5. Fornell Larcker (FL) criteria

A bootstrapping approach determines whether or not the structural model is significant. The goodness of fit (GOF) for the inner model can be checked with the help of the Coefficient of determination (R2), path coefficient (β value), and T-statistic value. Other criteria include effect size (F2), model’s predictive relevance (Q2), and GOF index. The relevance of route coefficients may be inferred from the value of the T-statistics (Ringle et al., Citation2015).

One can use the beta coefficient to assess the influence of exogenous variables on endogenous variables. If there is a larger β value, we may anticipate that the impact of the independent variable will be much more pronounced on the value of the dependent variable. Influence of an external latent construct onto an internal latent construct, the values of the VIF may be used to consider the multicollinearity in the variables. The value of the VIF provides evidence that there is no multicollinearity in the data. The value of the VIF should be less than 5 to meet the criteria for acceptability. These are the primary criteria that will be used to assess the internal model. F2 value may be used to estimate the magnitude of the effect caused by the independent variables. It refers to the variation in the value of R2 that takes place by removing a separate variable from the statistical model. The following criteria are used to determine the effect size. It is considered less when the value of F2 is less than or equal to 0.02; the effect size is considered to be medium when the value of F2 is between 0.15 and 0.35, and the effect size is considered to be significant when F2 is 0.35 or more. (Cohen, Citation1988).

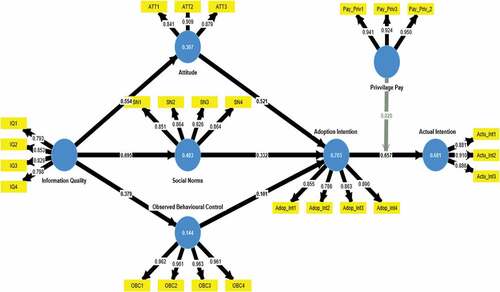

The outcomes of the path coefficient are depicted in Table and Figure . The findings in Table show a significant and favourable association exists between all the variables except for observed control behaviour. Figure depicts a graphical representation of the model’s complete set of route coefficients.

Figure 3. Path coefficient model.

Table 6. Testing of Hypothesis

As per the findings of PLS-SEM analysis, hypothesis 1 predicts that attitude bears a powerful and positive effect on buyers’ usage intention of fintech. The data in Table and Figure confirmed that attitude exerts a notable influence on the usage intention of the fintech value (β value =.521, T = 8.511, p < 0.01). As a result, H1 may be trusted. It is further hypothesized that the influence of SN regarding the selection and adoption of fintech would be considerable and beneficial. Table and Figure showed that social norms substantially impacted the desire to embrace fintech (β value = 0.332, T = 4.695, p < 0.01). As a result, H2 may be trusted. It is hypothesized that the observable control of behaviour would significantly impact the decision to adopt, particularly a favourable one. The data are shown in Table , and Figure confirmed what was hypothesized to be the case, namely that observable behavioural control had a substantial impact on the adoption intention of fintech (β value =.101, T = 2.131, p > 0.01). Because there is insufficient evidence to support H3, we cannot proceed. It was revealed that there was a significant association between actual intention (β value = 0.657, T value = 12.823, and p < 0.01). It was discovered that the fintech adoption intention exerts a significant and favourable impact on actual intention. Therefore, the H4 hypothesis is accepted.

Table and Figure demonstrate that information quality has the highest β value. It can be treated as the leading factor of the model. Information quality has favourable and substantial impacts on attitude (β value = 0.554, T = 11.18, p < 0.01) as well as on social norms (β value = 0.695, T = 17.816, p < 0.01) and on observed behavioural control (β value = 0.379, T = 7.02, p < 0.01). It has been determined that Hypotheses 5, 6, and 7 may be accepted. In addition, the results show that there exists a significant and positive linkage between actual intention and one’s readiness to pay for the privilege (β value = 0.251, T = 4.252, p < 0.01). As a result, Hypothesis 8 has been validated. In addition, this research investigated the moderating effect of a participant’s willingness to pay for the privilege of adopting a child on the connection between their adoption intention and actual intention. It was proposed by Muller et al. (Citation2005) that to consider a construct to be a mediator, it needs to satisfy certain conditions, which are as follows: Firstly, the association among endogenous as well as exogenous variables must be notable without considering the effect of the proposed mediator. Secondly, the proposed mediator should not affect the relationship between the endogenous and exogenous variables. Second, the suggested mediator must be affected by the variable doing the explaining. The data indicate that there is a positive influence. However, it is not significant, of ready to pay for the privilege as a moderator (with a β value equal to 0.02, T equal to 0.681, and a p-value greater than 0.01).

Since each indicator’s VIF value was lower than 5, it is demonstrated in Table that there is no evidence of multicollinearity. The vast majority of considerations are located within the band proposed by Cohen (Citation1988). As a result, the research successfully met the requirements for multicollinearity and effect size.

The current study model can account for 68.10 of the variance in predicting the outcome variable. The values of SRMR, dULS, and dG discrepancies of estimated models were 0.052, 0.721, and 0.412, respectively. The goodness of fit of the bootstrapping estimated model was determined. Notably, the values at 0.067, 0.857, and 0.730 were below their respective 95%-quartile bootstrap confidence intervals. Additionally, NFI’s score of 0.913 was higher than its threshold value of 0.90. (Bentler & Bonetl, Citation1980). The findings above show that the model has a higher goodness of fit index and is trustworthy for additional research.

13. Mediation analysis

The research is predicated on mediation and indirect effect sizes (Hayes, Citation2015; Nitzl et al., Citation2016). The bootstrapping method (Jose, Citation2013) was used in this study so that researchers could evaluate the moderating effects of factors such as attitude, social norms, and observable behavioural controls. The mediating effects were demonstrated via a two-step technique (Baron and Kenny, Citation1986). During the first step of the evaluation process, the conceptual model was examined without the assistance of mediators. In the subsequent step, the mediators were factored in, and an estimate of the indirect influence was derived. The bootstrapping method was used, and 5000 samples were employed. This technique can both explain and make predictions. R2 is a valuable tool for determining how accurate the model’s predictions will be. J. F. Hair et al. (Citation2013) recommended the values of R2 for dependent variables. The acceptable range is as follows: 0.75 (considerable), 0.50 (moderate), and 0.25 (weak). The predictive importance of the dependent variables is evaluated using the Q-square statistic. If the value of Q2>0, the model carries high predictive power (Table ).

Table 7. Specific indirect effect

shows that the R2 value for attitude was 0.307, that the value for social norms was 0.483, that the value for observed behavioural control was 0.144, that the value for adoption intention was 0.703, and that the value for the actual intent was 0.681. It demonstrates that the model has a significant capacity for explaining the data.

Table 8. Goodness of Fit and Predictive Relevance

shows that the values of Q2 for all the factors are more than zero. It shows the model has high predictive power.

By comparing the values of the root mean squared error (RMSE) for the dependent variables of the PLS-SEM with those of the linear regression model (LM), PLS predicts the predictive ability of the model (Hair, 2019).

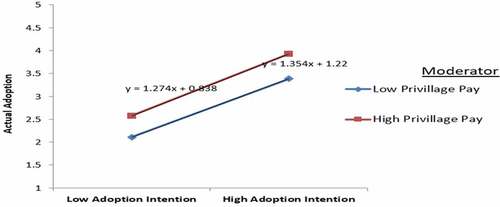

Table reveals that there is only one number from Act 2 that was greater in PLS-SEM than it was in LM (See Table ). It can be concluded that the model has a level of predictive ability between medium and high. As shown in Figure below, a consumer’s readiness to pay for a privilege contributes positively to the link between their buy intention and actual purchase intention.

Figure 4. Consumer’s readiness to pay for a privilege as moderating variable.

Table 9. Predictive capacity of the model

Table 10. The PLS predict

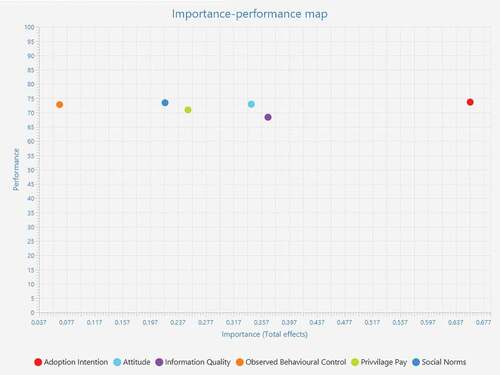

14. Importance performance map analysis

According to the findings of the significant performance map study, the adoption intention of Millennials is the most critical element in the adoption of financial technology. It was then followed by the quality of the information, an attitude, a willingness to pay for privileges, social standards, and observable behavioural control. In addition, it was discovered that the performance of adopting intentions and social norms was the greatest, followed by observable behavioural control, attitude, willingness to pay for privileges, and information quality (See Figure ).

Figure 5. Importance performance map.

15. Discussion

The present study investigates theory of planned behaviour’s relevance in forecasting adoption intention and actual intention of the Gen Y population in developing countries. The research accepts and broadens the outcomes of insufficient past research (Ramchandran & Stella, Citation2022; Sujood et al., Citation2022)) carried out an investigation of adoption intention and actual intention of fintech among Indian users by applying theory of planned behaviour. The paper widely accedes for the theory of planned behaviour apart from the direct linkage between OBC and the user’s intent. It indicates that the user’s emotional state to carry out specific behaviour proves straightly ineffective on the fintech adoption intention of the users. The study authenticates the findings of past studies whereby OBC carried no impact on user intent (Purwantini et al., Citation2020, Majid, Citation2021).

Meanwhile, the research disagrees with the findings where OBC affirmed a remarkable impact on user’s intention of Indian users (Darmansyah et al., Citation2020; Mazambani & Mutambara, Citation2020; Putranto and Sobrari, Citation2021). At the same time, OBC indirectly impacted users’ adoption and actual intention. Furthermore, the research asserts that fintech adoption intention influences actual intention. Over and above, the mediation effects discussed in this paper highlight the dynamics of the behavioural psychology of fintech users wherein IQ, attitudes, social norms, and OBC impact the actual intention through adoption intention. Subsequently, the research unveils intrinsic tendencies of in-depth association among the various antecedents of Gen Y’s fintech actual intention. Hence, the research outcomes primarily witness the sustainability of theory of planned behaviour in illustrating the fintech adoption behaviour of the Gen Y population in India.

In addition, the research supports the broadening of theory of planned behaviour by building the effectiveness of further adding two extra variables in determining user’s adoption and actual intention. It was observed in the study that IQ had a remarkable impact on all the exogenous variables, namely attitude, social norms, and observed control behaviour. This result is corroborated by (Fanoberova and Kuczkowska, Citation2016; Khwaja et al., Citation2020). The study’s results confirmed the work of Lee et al. (Citation2016), where the quality of information significantly affects the purchase intention of youngsters. Indirect effects in this study highlight the subconscious mechanism that exists in the Gen Y population between information quality and purchase intention.

Additionally, readiness to pay for the privileges remarkably influenced the intention to use fintech. The study highlights the price sensitivity of India’s young consumers. The researchers tried to broaden the scope of planned behaviour theory by introducing additional constructs. It provides critical knowledge to marketers regarding the strong relationship between adoption intention and actual intention. The users are ready to pay an extra price if they adopt fintech.

16. Theoretical contribution

The present research focuses on identifying diversified research gaps, and thus it will make an extensive addition to the body of knowledge. Firstly, Ajzen’s theory of planned behaviour (1991) is used here to confirm whether the theory can be applied or not in the effective implementation of fintech in India. ATT, SN, and OBC are the three components that makeup theory of planned behaviour. The study broadens the scope of theory of planned behaviour by applying it to Gen Y’s intention to adopt and use fintech. This research paper is among the first to consider the notable impact of information quality on the adoption intention of the millennial population of India. Secondly, the study examined the mediation role of three factors of theory of planned behaviour, namely attitude, social norms, and observed control behavior between information quality and adoption intention. Thus, it tries to define how information quality can affect the buying intent of consumers. Thirdly, it is found on exploring the peer-referred databases and the best of the authors’ comprehension, no earlier study exists to identify the impact of information quality on the buying intent of fintech consumers. Although, many research works show the impact of attitude, social norms, and observed behavior control on the adoption intent of fintech, excluding information quality (Mazambani & Mutambara, Citation2020; Setiawan, Citation2020; Shaikh et al., Citation2020).

Nonetheless, the impact of information quality on fintech usage is still an unexplored area in research. (Cai & Zhu, Citation2015). Fourthly, the latest past studies showed a lack of attention to the influence of quality of information on the adoption and usage of fintech in the Gen Y population. Fifthly, the adoption of fintech is said to have enormous potential in addressing the under-banked and unbanked people along with those with a poor level of financial literacy (B. Setiawan et al., Citation2021). This study will motivate the use of financial technology among young people in India. Sixthly, this study also addresses the problem of the dearth of studies focusing on the variables that affect the adoption intent of financial technology in India (Gupta & Agrawal, Citation2021). The findings of this research cover a knowledge gap in adoption intention and actual intention of fintech among the millennial generation in India. Finally, as mentioned above, the model primarily focuses on India’s Gen Y population. Hence the researchers endeavor to enrich the knowledge by widening the area of research to the Asian subcontinent.

17. Practical implications

The current study focuses on the elements driving Gen Y’s adoption of financial technology in India and looks specifically at India. As a result, gaining knowledge about the consumers’ adoption of fintech in India would benefit marketers. They can get information about the acceptance and true purpose of users of fintech in India. It will help to promote new start-up enterprises to advertise the latest fintech advancements among existing customers and future consumers. It will lead to great assistance for fintech marketers. In addition to this, fintech marketers in India have the opportunity to explore a new market sector. It would be beneficial to fintech marketers to understand how people in India react and behave in response to changes by fintech. The strategies may be developed to take advantage of the enormous potential that lies inside India’s digital economy. It will assist the marketers of fintech services, allowing them to improve their products and make them more user-friendly. It will also help fintech marketers to erase uncertainties and fear among consumers of fintech by delivering user-friendly, innovative fintech services. It would be of great assistance to fintech marketers. It will help consumers feel more confident and trustworthy in their interactions with the platform. The present study is hoped to be a stepping-stone in forecasting user behaviour in the Indian economy. The Indian government is consistently penetrating internet services even in remote areas and transforming the Indian economy into a digital economy. In addition, it is the goal of the Indian government to change the Indian economy into a digital economy. Despite the widespread availability of fintech services, there is a need to gain knowledge about the users’ intentions and behaviour towards adopting fintech. The expanding use of financial technology helps broaden the current investigation’s horizon.

18. Conclusion

In recent years, India has emerged as one of the top digital economies, with a wide range of everyday duties and commercial transactions conducted online. (Bhatt et al. (Citation2020). Everyday online financial transactions have increased significantly in a developing nation like India. There was a scarcity of relevant literature accessible to the general public that specifically addressed how diverse behavioural aspects impact practical adoption of technology for financial transactions, especially among Gen Y. The examination of this data, with a special emphasis on Gen Y adoption of fintech, adds to the previously existing notion of planned behaviour.

The findings of our study provide evidence for the substantial effect that the quality of information has on social norms and attitude. In addition, mediating variables attitudes and social conventions have a direct and considerable influence on the desire to use technology for financial transactions. The intention to use financial technology is the factor that has the most significant impact on Generation Y’s behaviour. The findings of this investigation lend credence to the hypothesis that direct effects are caused by privilege pay as moderating variable. How members of Generation Y conduct their online financial transactions is directly influenced by the myriad of promos, discounts, and coupons that are available.

According to the findings of the present research, cultural norms and mindset play an important mediating role in the adoption of fintech by Generation Y in emerging countries like India. In general, many different determinants of the theory of planned behaviour, with the exception of perceived behaviour control, have a substantial effect on the adoption of fintech, particularly Gen-y. Our research expands the theoretical bounds by presenting strong evidence in favour of the relevance of the dual process of theory of planned behaviour in gaining an understanding of the adoption intention of financial technology.

The future researchers can use more mediators and moderators such as green technology, financial innovations, perceived trust, green finance, rational consumer behavior in order to conduct in-depth study of underlying relationships. Besides it, an experimental study can be undertaken to know about the before and after impact of fintech adoption by millennials. Now a days, experimental research is undertaken in order to know the underlying causal relationships among the variables. Further, effective reservoir experimental research based on data partitioning can be conducted. Experimental research based on neural science can be further explored. The present study is based on theory of planned behavior and it can be explored further on the basis of several circumstantial justifications. It will be gainful to carry out meta-analysis study to know antecedents and consequences of adoption intention and actual intention for adoption of fintech among Gen Z. It would further provide much more vision and develop embryonic areas of research.

19. Limitations and future research direction

The population of India’s Generation Y is all that will be covered in this research. Future studies may involve members of India’s Gen Z. Another disadvantage of the study is that the user’s real and adoption intention towards fintech is exclusively based on theory of planned behaviour. It is a significant restriction, given the nature of the research. On the other hand, the scope of the study may be expanded further by including additional dependent and independent variables. As potential moderators, demographic parameters such as sex, age group, level of education, as well as an economic level might be considered (Ferdaous & Rahman, Citation2021). Based on Global Findex Report 2022, there is 22% of Indians lack an account in any financial institution due to distance to financial institutions, lack of trust, and lack of need were the most commonly cited reasons for account inactivity. Therefore, trust, lack of need, perceived security and risk can be considered as exogeneous variable in the existing model for future research.

Disclosure statement

No potential conflict of interest was reported by the authors.

References

- Afandi, M. Y. (2021). Antecedents of digitizing ZIS payments: A TAM and THEORY of PLANNED BEHAVIOUR Approaches. Journal of Finance and Islamic Banking, 41, 55–25

- Agrebi, S., & Jallais, J. (2015). Explain the intention to use smartphones for mobile shopping. Journal of Retailing and Consumer Services, 22, 16–23. https://doi.org/10.1016/j.jretconser.2014.09.003

- Ahmed Alshari, H., & Lokhande, M. A. (2022). The impact of demographic factors of clients’ attitudes and their intentions to use FinTech services on the banking sector in the least developed countries. Cogent Business & Management, 9(1), 2114305. https://doi.org/10.1080/23311975.2022.2114305

- Ajzen, I. (1991). The theory of planned behavior. Organizational Behavior and Human Decision Processes, 50(2), 179–211. https://doi.org/10.1016/0749-5978(91)90020-T

- Akhtar, F., & Das, N. (2019). Predictors of investment intention in Indian stock markets: Extending the theory of planned behavior. International Journal of Bank Marketing, 37(1), 97–119. https://doi.org/10.1108/IJBM-08-2017-0167

- Aldammagh, Z., Abdeljawad, R., & Obaid, T. (2021). Predicting mobile banking adoption: An integration of TAM and THEORY of PLANNED BEHAVIOUR with trust and perceived risk. Financial Internet Quarterly ‘E-Finance, 17(3), 35–46. https://doi.org/10.2478/fiqf-2021-0017

- Almajali, D., Al-Radaideh, A., Nussir, N., Eid, A., Al-Fakeh, F., & Masad, F. (2023). Antecedents of mobile banking app adoption during COVID19: A perspective of Jordanian consumer. International Journal of Data and Network Science”, 7(1), 477–488. https://doi.org/10.5267/j.ijdns.2022.8.011

- Antonius, D. (2022). The Effect of Regulatory Sandbox on the Behaviour of FinTech Actors in Indonesia Using Theory of Planned Behaviour Approach ICEBE. EAI. https://doi.org/10.4108/eai.7-10-2021.2316146

- Bahl, K., Kiran, R., & Sharma, A. (2022). Impact of Drivers of Change (Digitalisation, Demonetisation, and Consolidation of Banks) with Mediating Role of Nature of Training and Job Enrichment on the Banking Performance. SAGE Open, 12(2), No.2. https://doi.org/10.1177/21582440221097393

- Baron, R. M., & Kenny, D. A. (1986). The moderator–mediator variable distinction in social psychological research: Conceptual, strategic, and statistical considerations. Journal of Personality and Social Psychology, 51(6), 1173–1182. https://doi.org/10.1037/0022-3514.51.6.1173

- Belanche, D., Casaló, L. V., & Flavián, C. (2019). Artificial Intelligence in fintech: Understanding robo-advisors adoption among customers. Industrial Management and Data Systems, 119(7), 1411–1430. https://doi.org/10.1108/IMDS-08-2018-0368

- Bentler, P. M., & Bonetl, D. G. (1980). Significance tests and goodness of fit in the analysis of covariance structure. Psychological Bulletin, 88(3), 588. https://doi.org/10.1037/0033-2909.88.3.588

- Bhasin, N. K., & Gulati, K. (2021). Challenges of COVID-19 During 2020 and Opportunities for fintech in 2021 for Digital Transformation of Business and Financial Institutions in India. In Zhao, J., & Richards, J. (Eds.), E-Collaboration Technologies and Strategies for Competitive Advantage Amid Challenging Times (pp. 282–299). IGI Global publisher.

- Bhatt, V., Ajmera, H., & Nayak, K. (2020). An Empricial Study on Analyzing A User‘s Intention Towards Using Mobile Wallets; Measuring The Mediating Effect of Perceived Attitude and Perceived Trust. Turkish Journal of Computer and Mathematics Education, 12(10), 5332–5353. https://doi.org/10.17762/turcomat.v12i10.5336

- Bizer, C., & Cyganiak, R. (2009). Quality-driven information filtering using the WIQA policy framework. Web Semantics: Science, Services, and Agents on the World Wide Web, 7(1), 10. https://doi.org/10.1016/j.websem.2008.02.005

- Business Today. (2022), “Digital economy to see exponential growth to $800 billion by 2030: FM Sitharaman,” Business Today, March 12, available at https://www.businesstoday.in/latest/economy/story/digital-economy-to-see-exponential-growth-to-800-billion-by-2030-fm-sitharaman-325726-2022-03-12 (accessed on March 23,2023).

- Cai, L., & Zhu, Y. (2015). The challenges of data quality and data quality assessment in the big data era. Data Science Journal, 14(0), 2. https://doi.org/10.5334/dsj-2015-002

- Chang, V., Baudier, P., Zhang, H., Qianwen, X., Zhang, J., & Arami, M. (2020). How Blockchain can impact financial services – the overview, challenges and recommendations from expert interviewees. Technological Forecasting and Social Change, 158, 158. https://doi.org/10.1016/j.techfore.2020.120166

- Chin, W. W. (2010). How to Write Up and Report PLS Analyses. In V. Esposito Vinzi, W. W. Chin, J. Henseler, & H. Wang (Eds.), Handbook of Partial Least Squares: Concepts, Methods and Applications (pp. 655–690). Heidelberg, Dordrecht, London, New York: Springer. https://doi.org/10.1007/978-3-540-32827-8_29

- Chuang, L.M., Liu, C.C., & Kao, H.K. (2016). The adoption of fintech service: TAM perspective. International Journal of Management and Administrative Sciences, 3(07), 01–15.

- Chung, Inuk. (2007), “Roles and Impacts of IT on new Social Norms, Ethical Values, and Legal Frameworks in Shaping a Future Digital Society”, Social and economic factors shaping the future of the internet speakers’ position papers, NSF/OECD Washington, https://www.oecd.org/sti/ieconomy/37985728.pdf (Retrieved on October 10, 2022).

- Cohen, J. (1988). Statistical power analysis for the behavioural sciences (2nd ed.). Routledge.

- Dai, M., & Van Hove, L. (2017). The impact of customer images on online purchase decisions: Evidence from a Chinese C2C Web site. First Monday, 22(10).

- Darmansyah, F., A., B., Hendratmi, A., & Aziz, P. F. (2020). Factors determining behavioral intentions to use Islamic financial technology: Three competing models. Journal of Islamic Marketing, 12(4), 794–812.

- The Economics Times. (2022), “Digital economy to see exponential growth bn by 2030: FM”, The Economic Times, March 31, available at: https://economictimes.indiatimes.com/news/economy/finance/digital-economy-to-see-exponential-growth-to-usd-800-bn-by-2030-fm/articleshow/90156544.cms?from=mdr (Retrieved on September 19, 2022).

- Erwin, A. H., RA Aryanti, W. P., Antonius, R., & Marylise, H., (2020), “The Impact of Marketing Influencer and Information Quality to Purchase Intention of Instagram Users”, International Conference on Information Management and Technology (ICIMTech), Bandung, Indonesia (pp.794–799).

- Escobar-Rodríguez, T., & Carvajal-Trujillo, E. (2014). Online purchasing tickets for low-cost carriers: An application of the unified theory of acceptance and use of technology (UTAUT) model. Tourism Management, 43, 70–88. https://doi.org/10.1016/j.tourman.2014.01.017

- Fanoberova, & Kuczkowska, H. (2016). Effects of source credibility and information quality on attitudes and purchase intentions of apparel products : A quantitative study of online shopping among consumers in Sweden.

- Ferdaous, J., & Rahman, M. N. (2021). Banking Goes Digital: Unearthing the Adoption of fintech by Bangladeshi Households. Journal of Innovation in Business Studies, 1(1), 7–42.

- Gao, J., Zhang, C., Wang, K., & Sulin, B. (2012),“Understanding Online Purchase Decision Making: The Effects of Unconscious Thought, Information Quality, and Information Quantity”, available at: https://www.semanticscholar.org/paper/Understanding-Online-Zhang/59d87c76cdd2e92a9ac251681e4d6d959e405a99 (Retrieved on October 21, 2022).

- Gholami, Z., Abdekhoda, M., & Zarea Gavgani, V. Determinant Factors in Adopting Mobile Technology-based Services by Academic Librarians. (2018). Journal of Library & Information Technology, 38(4), 271–277. July 2018. https://doi.org/10.14429/djlit.38.4.12676

- Gupta, S., & Agrawal, A. (2021). Analytical Study of fintech in India: Pre & Post Pandemic Covid-19. Indian Journal of Economics and Business, 20(3), 33–71.

- Hair, J. F., Hult, G. T. M., Ringle, C. M., & Sarstedt, M. (2014). A Primer on Partial Least Squares Structural Equation Modeling (PLS-SEM). USA: SAGE.

- Hair, J. F., Ringle, C. M., & Sarstedt, M. (2011). PLS-SEM: Indeed, a silver bullet. Journal of Marketing Theory and Practice, 19(2), 139–152. https://doi.org/10.2753/MTP1069-6679190202

- Hair, J. F., Ringle, C. M., & Sarstedt, M. (2013). Partial least squares structural equation modeling: Rigorous applications, better results, and higher acceptance. Long-Range Planning, 46(1–2), 1–12. https://doi.org/10.1016/j.lrp.2013.01.001

- Hayes. (2015). An index and test of linear moderated mediation. Multivariate Behavioral Research, 50, 1–22. https://doi.org/10.1080/00273171.2014.962683

- Henseler, J., Ringle, C. M., & Sarstedt, M. (2015). A new criterion for assessing discriminant validity in variance-based structural equation modelling. Journal of the Academy of Marketing Science, 43(1), 115–135. https://doi.org/10.1007/s11747-014-0403-8

- Hew, T. S., & Kadir, S. L. S. A. (2016). Understanding cloud base VLE from the SPT and CET perspectives: Development and validation of measurement Instrument Computer education. Computer & Education, 101(101), 132–149. https://doi.org/10.1016/j.compedu.2016.06.004

- Hew, J. -J., Lee, V. -H., Ooi, K. -B., & Lin, B. (2016). Mobile social commerce: The booster for brand loyalty? Computers in Human Behavior, 59, 142–145. https://doi.org/10.1016/j.chb.2016.01.027

- Huang, H., Stvilia, B., Jörgensen, C., & Bass, H. W. (2012). Prioritisation of Data Quality Dimensions and Skills Requirements in Genome Annotation Work. Journal of the American Society for Information Science and Technology, 63(1), 195–207. https://doi.org/10.1002/asi.21652

- Hu, Z., Ding, S., Li, S., Chen, L., & Yang, S. (2019). Adoption Intention of fintech Services for Bank Users: An Empirical Examination with an Extended Technology Acceptance Model. Symmetry, 11(3), 340. https://doi.org/10.3390/sym11030340

- Hui-Wen Chuah, S., Cheng-Xi Aw, E., & Cheng, C.F. (2022). A silver lining in the COVID-19 cloud: Examining customers’ value perceptions, willingness to use and pay more for robotic restaurants. Journal of Hospitality and Marketing Management, 31(1), 49–76. https://doi.org/10.1080/19368623.2021.1926038

- India Briefing. (2022), “What trends are driving the fintech revolution in India?”, June 9, India-briefing.com/news/what-trends-are-driving-the-fintech-revolution-in-India-23809.html/ (Retrieved October 10, 2022).

- Jain, A., Joshi, N., & Mayee, A. J. (2021). Millennial’s Tide Over the COVID-19 Crises: Buying Behaviour of Indian Millennial’s Post-COVID-19 Crises. Jindal Journal of Business Research, 10(2), 214–221. https://doi.org/10.1177/22786821211045196

- Jeong, M., & Lambert, C. U. (2001). Adaptation of an information quality framework to measure customers’ behavioral intentions to use lodging Web sites. International Journal of Hospitality Management, 20(2), 129–146. https://doi.org/10.1016/S0278-4319(00)00041-4

- Jose, P. E. (2013). Doing Statistical Mediation and Moderation. The Guilford Press.

- Khwaja, M. G., Jusoh, A., & Nor, K. M. (2019). Does online social presence lead to purchase intentions?. Int. J. Econ. Policy Emerg. Econ, 12, 198–206.

- Kim, A. J., & Johnson, K. K. P. (2016). Power of consumers using social media: Examining the influences of brand-related user-generated content on Facebook. Computers in Human Behavior, 58, 98–108. https://doi.org/10.1016/j.chb.2015.12.047

- Kim, H., & Niehm, L. S. (2009). The impact of website quality on information quality, value, and loyalty intentions in apparel retailing. Journal of Interactive Marketing, 23(3), 221–233. https://doi.org/10.1016/j.intmar.2009.04.009

- Knewtson, H. S., & Rosenbaum, Z. A. (2020). Toward understanding fintech and its industry. Managerial Finance, 46(8), 1043–1060. https://doi.org/10.1108/MF-01-2020-0024

- Kock, N. (2015). Common method bias in PLS-SEM: A full collinearity assessment approach. International Journal of E-Collaboration, 11(4), 1–10. https://doi.org/10.4018/ijec.2015100101

- Kock, Lynn, Kock, N., & Lynn, G. (2012). Lateral Collinearity and Misleading Results in Variance-Based SEM: An Illustration and Recommendations. Journal of the Association for Information Systems, 13(7), 546–580. https://doi.org/10.17705/1jais.00302

- Krivkovich, A., White, O., Townsend, Z., & Euart, J. (2020). How US customers’ attitudes to fintech are shifting during the pandemic. McKinsey & Company, December, 17.

- Lee, M.C. (2009). Factors influencing the adoption of internet banking: An integration of TAM and THEORY of PLANNED BEHAVIOUR with perceived risk and perceived benefit. Electronic Commerce Research and Applications, 8(3), 130–141. https://doi.org/10.1016/j.elerap.2008.11.006

- Lee, E.J. Do tech products have a beauty premium? The effect of visual aesthetics of wearables on willingness-to-pay premium and the role of product category involvement. (2022). Journal of Retailing and Consumer Services, 65(102872), 102872. article no. https://doi.org/10.1016/j.jretconser.2021.102872

- Lee, T. S., Ariff, M. S. M., Zakuan, N., Sulaiman, Z., & Saman, M. Z. M. (2016). Online sellers’ website quality influencing online buyers’ purchase intention. [Paper presentation] IOP Conference Series: Materials Science and Engineering, Bali, Indonesia

- Leong, L. Y., Hew, T. S., Ooi, K. B., & Lin, B. (2019). Do electronic word-of-mouth and elaboration likelihood model influence hotel booking? Journal of Computer Information Systems, 59(2), 146–160. https://doi.org/10.1080/08874417.2017.1320953

- Lestari, M. R., & Nita, A. (2021). The Influence of Sustainable Product’s Attributes Toward the Willingness to Pay for Sustainable Products. Malaysian Journal of Social Sciences and Humanities (MJSSH), 6(8), 542–551. https://doi.org/10.47405/mjssh.v6i8.981

- Maiti, D., Castellaci, F., & Melchior, A. (2020), “Digitalisation and development: Issues for India and beyond”, January, available at https://www.researchgate.net/publication/338320003_Digitalisation_and_Development_Issues_for_India_andBeyondIssues_ (Retrieved September 25, 2022).

- Majid, R. (2021). The role of religiosity in explaining the intention to use Islamic fintech among MSME actors. International Journal of Islamic Economics and Finance (IJIEF), 4(2), 207–232.

- Mazambani, L., & Mutambara, E. (2020). Predicting fintech innovation adoption in South Africa: The case of cryptocurrency. African Journal of Economic and Management Studies, 11(1), 30–35. https://doi.org/10.1108/AJEMS-04-2019-0152

- McKinsey Global Institute. (2019), “Digital India- Technology to transform a connected nation,” available at McKinsey Global Institute, March, available at: https://www.mckinsey.com/~/media/mckinsey/business%20functions/mckinsey%20digital/our%20insights/digital%20india%20technology%20to%20transform%20a%20connected%20nation/digital-india-technology-to-transform-a-connected-nation-full-report.pdf (Retrieved September 21, 2022).

- Mehta, D., & Kumari, S. (2021). Drivers fintech in India – a study of customers’ attitude and adoption. Zenith International Journal of Multidisciplinary, 11(1), 29–41.

- Meyliana, M., Fernando, E., & Surjandy, S. (2019). The Influence of Perceived Risk and Trust in Adoption of fintech Services in Indonesia. Commit Journal, 13(1), 31–37. https://doi.org/10.21512/commit.v13i1.5708

- Mikalef, P., Giannakos, M., & Pateli, A. (2013). Shopping and Word-of-Mouth Intentions on Social Media. Journal of Theoretical and Applied Electronic Commerce Research, 8(1), 17–34. https://doi.org/10.4067/S0718-18762013000100003

- Minh, T. H. L. (2021). Examining factors that boost intention and loyalty to use fintech post COVID-19 lockdown as a new normal behavior. Cell Press Heliyon, 7(8), 1–9. https://doi.org/10.1016/j.heliyon.2021.e07821

- Mohammad, K., & Nawayseh, A. (2020). Fintech in COVID-19 and beyond: What factors are affecting customers’ choice of fintech applications? Journal of Open Innovation, Technology, Market, and Complexity, 6(4), 1–15. https://doi.org/10.3390/joitmc6040153

- Mohanasundaram, T., Sathyanarayana, S., & Rizwana, M.(2021), “Disruption on India’s fintech landscape: The 5G wave”, International Conference on Innovative Technology for Sustainable Development,Vol.37,https://www.itmconferences.org/articles/itmconf/abs/2021/02/itmconf_icitsd2021_01008/itmconf_icitsd2021_01008.html (Retrieved October 10, 2022).

- Muller, D., Judd, C. M., & Yzerbyt, V. Y. (2005). When moderation is mediated, and mediation is moderated. Journal of Personality and Social Psychology, 89(6), 852. https://doi.org/10.1037/0022-3514.89.6.852

- Myers, M. B., Calantone, R. J., Page, T. J., Jr., & Taylor, C. R. (2000). Academic insights: An application of multiple-group causal models in assessing cross-cultural measurement equivalence. Journal of International Marketing, 8(4), 108–121. https://doi.org/10.1509/jimk.8.4.108.19790

- Nagaraju, S. (2015). Mobile Banking- Perception of Customers and Bankers. International Journal of Business Administration Research Review, 3(9), 236.

- Nakagawa, K., & Yellowlees, P. (2020). Inter-generational Effects of Technology: Why Millennial Physicians May Be Less at Risk for Burnout Than Baby Boomers. Current Psychiatry Report, 22(9), No.9, pp. 45. https://doi.org/10.1007/s11920-020-01171-2

- Nayanajith, G., & Damunupola, K. A. (2019). Relationship of perceived behavioral control and adoption of internet banking in the presence of a moderator. Asian Journal of Multidisciplinary Studies, 2(2), 30–41.

- Niswah, F., Mutmainah, L., & Legowati, D. (2019). Muslim millennial’s intention of donating to charity using fintech platform. Journal of Islamic Monetary Economics and Finance, 5(3), 623–644. https://doi.org/10.21098/jimf.v5i3.1080

- Nitzl, C., Roldan, J. L., & Cepeda-Carrion, G. (2016). Mediation Analysis in Partial Least Squares Path Modeling: Helping Researchers Discuss More Sophisticated Models. Industrial Management & Data Systems.

- Njanja, L., Ogutu, M., & Ogutu, R. O. (2014), “The Moderating Effect of Subjective Norms, Perceived Behavioural Control and Gender on the Relationship Between Attitude Towards Internet Advertising and Purchase Intention of University Students in Kenya,” available at: https://www.semanticscholar.org/paper/the-moderating-effect-of-subjective-norms%2c-control-njanja-ogutu/21d1bfec355e9d5bd5d65aa81717e2877788102e, Retrieved on October 23, 2022)

- Nomura, N., & Akai, M. (2004). Willingness to pay for green electricity in Japan as estimated through contingent valuation method. Applied Energy, 78(4), 453–463. https://doi.org/10.1016/j.apenergy.2003.10.001

- Pascual-Miguel, F. J., Agudo-Peregrina, Á. F., & Chaparro-Pelaez, J. (2015). Influences of gender and product type on online purchasing. Journal of Business Research, 68(7), 1550–1556. https://doi.org/10.1016/j.jbusres.2015.01.050

- Peters, E., Dieckmann, N., Dixon, A., Hibbard, J. H., & Mertz, C. K. (2007). Less is more in presenting quality information to consumers. Medical Care Research and Review, 64(2), No2, pp. 169–190. https://doi.org/10.1177/10775587070640020301

- Philippon, T., (2016). The fintech Opportunity. NBER Working Paper No. 22476, August.

- Podsakoff, P. M., MacKenzie, S. B., Lee, J. Y., & Podsakoff, N. P. (2003). Common method biases in behavioral research: A critical review of the literature and recommended remedies. The Journal of Applied Psychology, 88(5), pp.No.5, pp.879–903. https://doi.org/10.1037/0021-9010.88.5.879

- Priyadarshini, C., Sreejesh, S., & Anusree, M. R. (2017). Effect of information quality of employment website on attitude toward the website: A moderated mediation study. International Journal of Manpower, 38(5), No.5, pp. 729–745. https://doi.org/10.1108/IJM-12-2015-0235

- Purwantini, A. H., Athief, F. H. N., & Waharini, F. M. (2020). Indonesian consumers’ intention of adopting islamic financial technology services. Shirkah, 5(2), 171–196.

- Putranto, B. D., & Sobari, N. (2021). Predicting Intention of Using Fintech Lending to Bank Users in Indonesia. In 18th International Symposium on Management (INSYMA 2021) (pp. 206–211). Atlantis Press.

- Ramchandran, T., & Stella, M. (2022). Behavioural intention towards cryptocurrency adoption among students: A fintech innovation. Journal of Positive School Psychology, 5(6), 5046–5053.

- Razak, M. M., Aminudin, N., Amir, A. F., & Ismail, M. A. (2013). Assessing consumer behavior from a main website of tourism product. Hospitality and Tourism: Synergizing Creativity and Innovation in Research, 452–459.

- Ringle, C., Da Silva, D., & Bido, D. (2015). Modelagem de Equações Estruturais com Utilização do Smartpls. Brazilian Journal of Marketing, 13(2), 56–73. https://doi.org/10.5585/remark.v13i2.2717

- RM, O. (2007). A Caution Regarding Rules of Thumb for Variance Inflation Factors. Quality & Quantity, 41(5), 673–690. https://doi.org/10.1007/s11135-006-9018-6

- Ryu, H. -S. (2018). What makes users willing or hesitant to use fintech? the moderating effect of user type. Industrial Management & Data Systems, 118(3), 541–569. https://doi.org/10.1108/IMDS-07-2017-0325

- Saba, I., Kouser, R., & Sharif Chaudhry, I. (2019). Fintech and Islamic Finance-Challenges and Opportunities. Review of Economics and Development Studies (READS), 5(4), 581–590. https://doi.org/10.26710/reads.v5i4.887

- Sahni, J. (2021). Employee Engagement Among Millennial Workforce: Empirical Study on Selected Antecedents and Consequences. SAGE Open, 11(1), No.1. https://doi.org/10.1177/21582440211002208

- School of Health Management and Medical Informatics. Tabriz University of Medical Sciences.

- Setiawan. (2020). Digital financial literacy, current behavior of saving and spending and its future foresight, Econ (pp. 1–19). Innovation and Technology.

- Setiawan, B., Pandu Nugraha, D., & Irawan, A.; Zoltan, Z. (2021). Robert Jeyakumar Nathan. Journal Open Innovation Technology, Market and Complexity, 7(3), 188. https://doi.org/10.3390/joitmc7030188

- Shaikh, I. M., Qureshi, M. A., Noordin, K., Shaikh, J. M., Khan, A., & Shahbaz, M. S. (2020). Acceptance of Islamic financial technology (fintech) banking services by Malaysian users: An extension of technology acceptance model. Foresight, 22(3), 367–383. https://doi.org/10.1108/FS-12-2019-0105

- Sheokand, K., & Gupta, N. (2017). Digital India programme and impact of digitalization on the Indian economy. Indian Journal of Economics and Development, 5(5).

- Shubhangi, S., Sahni, M. M., & Kovid, R. K. (2020). What drives fintech adoption? A multi-method evaluation using an adapted technology acceptance model. Management Decision, 58(8), 1675–1697. https://doi.org/10.1108/MD-09-2019-1318

- Sujood, B. N., Siddiqui, S., & Siddiqui, S. (2022). Consumers intention towards the use of smart technologies in tourism and hospitality (T&H) industry: A deeper insight into the integration of TAM, THEORY of PLANNED BEHAVIOUR and trust. Journal of Hospitality and Tourism Insights, ahead-of-print). https://doi.org/10.1108/JHTI-06-2022-0267

- Talwar, S., Talwar, M., Kaur, P., & Dhir, A. (2020). Consumers’ resistance to digital innovations: A systematic review and framework. Australian Marketing Journal, 28(4), 289–299. https://doi.org/10.1016/j.ausmj.2020.06.014

- Teo, A.C., Wei-Han Tan, G., Cheah, C.M., Ooi, K.B., & Yew, K.T. (2012). Can the Demographic and Subjective Norms Influence the Adoption of Mobile Banking? International Journal of Mobile Communications, 10(6), 578–597. https://doi.org/10.1504/IJMC.2012.049757

- Thoradeniya, P., Lee, J., Tan, R., & Ferreira, A. (2015). Sustainability reporting and the theory of planned behavior. Accounting, Auditing & Accountability Journal, 28(7), 1099–1137. https://doi.org/10.1108/AAAJ-08-2013-1449

- The Times of India. (2021a), “How India is outpacing the world in digital payment,” The Times of India, December 30, available at: https://timesofindia.indiatimes.com/business/india-business/explained-how-india-is-outpacing-the-world-in-digital-payments/articleshow/ (Retrieved on September 24, 2022).

- The Times of India. (2021b), “The rise of the Indian millennial”, September 6, available at:https://timesofindia.indiatimes.com/blogs/voices/the-rise-of-the-indian-millennial/ (Retrieved September 30, 2022).

- Tsai, M. T., Cheng, N. C., & Chen, K. S. (2011). Understanding online group buying intention: The roles of sense of virtual community and technology acceptance factors. Total Quality Management & Business Excellence, 22(10), 1091–1104. https://doi.org/10.1080/14783363.2011.614870

- Tun-Pin, Keng-Soon, C., Choo Yen-San, W., Pui-Yee, Y., Hong Leong, C., & Teh Shwu-Shing, J. (2019). An Adoption of fintech Service in Malaysia, South East Asia journal of contemporary business. Economics and Law, 18, N0 5, pp.134–147.

- Vicente Sales Melo, F., de Farias, S. A., & Trajano Barbosa, O. (2019). Dressing in white, a true Brazilian tradition: Social influence, values, and symbolic consumption. Revista de Administração da Universidade Federal de Santa Maria, 12(2), 215–232. https://doi.org/10.5902/1983465917984

- Warshaw, P. R., & Davis, F. D. (1985). Disentangling behavioral intention and behavioral expectation. Journal of Experimental Social Psychology, 21(3), 213–228. https://doi.org/10.1016/0022-1031(85)90017-4

- Yalcıntekin, T., & Saygili, M. (2020). Brand Loyalty at Smartphones Market: Linking Between Brand Passion, Hedonic and Utilitarian Values. Marketing and Management of Innovations, 1(1), 274–284. https://doi.org/10.21272/mmi.2020.1-23

- Yan, C., Siddik, A. B., Akter, N., & Dong, Q. (2021). Factors influencing the adoption intention of using mobile financial service during the COVID-19 pandemic: The role of Fintech. Environmental Science and Pollution Research, 1–19. https://doi.org/10.1007/s11356-021-17437-y

- Yan, C., Siddik, A. B., Yong, L., Dong, Q., Zheng, G. W., & Rahman, M. N. (2022). A Two-staged SEM-artificial neural network approach to analyze the impact of fintech adoption on the sustainability performance of banking firms: The mediating effect of green finance and innovation. Systems, 10(5), No.5, pp.148. https://doi.org/10.3390/systems10050148

- Zhang, Y., Xiao, C., & Zhou, G. Willingness to pay a price premium for energy-saving appliances: Role of perceived value and energy efficiency labeling. (2020). Journal of Cleaner Production, 242(118555), 118555. article no. https://doi.org/10.1016/j.jclepro.2019.118555