?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

The study evaluates the impact of statutory audit and corporation tax charges on the profitability of Nigerian listed firms using data from 2016 to 2021. This study is highly inspired by corporate governance detects, which mandate corporations’ stewardship, civic, and transparency duties to stakeholders. However, there is a need to analyze the compliance rate and its implications for corporate performance. The research data for this study are derived from the yearly financial reports of the sampled businesses. The descriptive statistics, correlation matrix, Hausman test, fixed and random effects techniques are also used in the study to determine the suitability of the data collected for the study and to determine the relationship between the study variables as well as the influence of the predictor variables on the reliant factors. According to the findings, corporate tax costs and statutory audit have a considerable impact on business profitability but while the corporate tax impact positively on profitability, an immaterial negative effect on net asset base is established. The total assets employed as the control variable in this study does not have tangible effect on both the profit after tax and net asset base. In terms of the relationship, all variables have a large and very strong positive interconnection with one another except the total assets applied as the moderating variable. It is also established that the data used in this inquiry is entirely normally distributed and appropriate for analysis. According to the findings, organizations should maintain a consistent statutory audit and regularly comply with tax obligations to establish a stronger corporate image that would promote excellent financial performance.

1. Introduction

Accounting dates back to the 13th century, therefore, the importance of accounting cannot be exaggerated, especially in light of the global increase in investment in industrialization where there is no fusion between capital ownership and control of the firm. Without accountability, financial performance cannot be determined in corporate organizations. And accountability can be defined as the willingness and ability to take responsibility for one’s actions (T. Agwor, Citation2016). Industrialization is a critical component for the economic sustenance in any country, especially Nigeria, and industrial growth can be accomplished through enterprises’ successful operations in maximizing their value. The board of directors is charged with this responsibility, however, the need for a high-quality financial report has been highlighted due to corporate accounting standards involving high-profile companies around the world (Abba & Sadah, Citation2020).

One of the major roles of management is financial reporting because it allows them to account for their stewardship. Managers of corporate organizations are responsible for the preparation and presentation of the financial annual reports to the owners of the company (i.e. the shareholders) and other users of the financial statement such as creditors, financial analysts, the general public, tax authorities, and other government agencies, for them to make assessments and decisions (Amahalu & Obi, Citation2020). However, it is important to note that the public’s confidence in financial reporting has reduced due to the increased rate of fraud and illegal activities in these organizations (Jabbar, Citation2018), resulting in the emergence of auditing. Due to the public’s lack of confidence in financial reporting, fraud, errors, and other illegal activities discovered in financial reports. Financial misstatements are required to be checked, detected, and reported by external auditors (Ivungu et al., Citation2019). Stakeholders believe that the credibility of the financial statements is also enhanced through external auditing since it gives an opinion on whether the information contained in the financial reports is free from financial misstatements and it is done by an independent person who has a thorough understanding of the company’s operations and financial reporting standards. Therefore, external auditing protects the interests of stakeholders (Muchugia, Citation2018).

The external audit function is also important because it motivates management to make due corrections to any errors that have been identified, appropriately disclose any abnormalities, and make the proper financial statement revisions. As a result, the auditor’s opinion is vital in making economic decisions (T. C. Agwor & Amangala, Citation2020). The auditor’s ability to notice a misstatement or error is determined by his or her competence, whereas the auditor’s independence decides whether or not the auditor will disclose it. Therefore, because the opportunities for financial growth are high, external auditing improves the financial performance of businesses by recruiting new investors and maintaining existing ones. (Muchugia, Citation2018). Financial performance is a concept used to describe the overall financial health of a company in the long run and can be used to create comparisons among identical companies in the same industry (K. Ehiedu & I. Toria,). As a result, audit committees and external auditors are tasked with reducing fraud and improving financial performance at their companies (Chijoke-Mgbame et al., Citation2020). Many factors influence the financial performance of companies, including those linked to auditing, and some of these aspects are related to management (HAZAEA et al., Citation2020).

There is a substantial amount of literature on corporate tax as a key driver of business and how it affects organizations’ long-term performance. Furthermore, a lot of relevant studies look into corporate tax and its impact on the financial performance of companies, therefore, this has become a subject of interest to policymakers and business executives (Nwaorgu & Abiahu, Citation2020). The Nigerian tax system, like any other, involves tax legislation, policy, and enforcement. While tax policies define Nigeria’s tax laws, tax administration is the process of putting those laws into practice to avoid a conflict between taxpayers and the government. Due to the complex business environment and the likelihood of firms coming up with different tax avoidance strategies, the revenue authority, in recent times, has exhibited a lot of interest in quoted companies. The transfer pricing formulas used when dealing with the firms have also complicated things, Thereby, affecting the financial performance of these companies (Olarewaju & Olayiwola, Citation2019). This study aims to ascertain the impact of statutory audit and corporate taxation on the financial performance of companies listed on the stock exchange in Nigeria.

Due to globalization, rapid growth in technology, industry, and business, as well as the threats and complexities of information and data management, significant issues have been faced by businesses around the world in recent years. As a result of these developments, the risks in corporations have been increasing at a significant rate. As a result, the organizations have realized the essence of a proactive approach to fraud prevention and detection to reduce the risk of fraud (Kadhim Al-Fatlawi, Citation2019). Internal audits and internal control are critical to a company’s financial performance since they reveal how public funds were utilized. It also assesses if a company’s financial statements present a true and fair picture of its financial position. Public finances are not efficiently handled despite internal control and internal audit, necessitating the engagement of an independent entity to audit books of accounts. External auditors are known to handle the examination of the books of accounts better in public companies (UMURERWA, Citation2016). For example, in 1998, a waste management company in Houston declared $1.7 billion in fictitious earnings, despite Arthur Andersen serving as the firm’s auditors. The Enron crisis that occurred in 2001 where shareholders lost $74 billion and thousands of investors and employees lost their retirement savings, Arthur Andersen also served as the firm’s auditor (Osemene & Fakile, Citation2018).

Corporate taxation also affects the financial performance of companies. This is because effective charges that would boost commercial transactions and socioeconomic development are one of the main issues that the Nigerian government and organizations face. While tax evasion has posed a significant problem to the government, multiple tax payments have remained an issue that businesses have sought to address, particularly in Nigeria due to the inadequate tax system. The Federal Board of Inland Revenue Services Act of 2007, the National Tax Policy of 2017, the Voluntary Assets and Income Declaration Scheme (VAIDS) of 2017, etc. are examples of the policies that have been implemented recently in Nigeria to deal with the challenge of multiple taxations and poor tax collecting policies (Olurankinse et al., Citation2021). Despite the numerous advantages, there is a paucity of empirical research on how they both affect the financial performance of public companies. This is because the majority of empirical studies focus just on statutory audit (DeFond et al., Citation2000; K. Ehiedu & I. Toria,), leaving out taxation while some focus on taxation (Olurankinse et al., Citation2021; Oyeshile & Adegbie, Citation2020; Sunardi, Citation2022) and overlooking statutory audit. However, Steller and Pummerer (Citation2021) did not bother looking at the financial performance response to tax and statutory audit in their evaluation. This research attempts to close this empirical gap by examining the impact of external auditing and corporate taxation on the financial performance of selected quoted companies in Nigeria.

2. Literature review

2.1. Conceptual Review

The conceptual framework focuses on all aspects of corporate taxation, statutory audits, and profitability of firms.

Figure highlights the study's variables and also serves as the diagramatical representation of the model applied in this study. Auditing can be defined as the process of gathering and reviewing evidence concerning the accounting information of an entity or institution to examine the adequacy of the information and reporting, according to the Generally Accepted Auditing Standards (GAAS) in that country (Oladejo et al., Citation2021). Regulation, in a firm, refers to the statute enacted by the management or the board of directors in that company (Yusof et al., Citation2019). A statutory audit is also referred to as an external audit, this is because it involves the engagement of an independent, professional individual (Olasupo et al., Citation2016). Statutory audits are no longer private since the auditing company (auditor) conducting an external audit in line with the legislation is actually performing a public duty. As a result, the relationships that arise during the statutory audit process are mostly public and legal in nature. Users of the financial information often request an independent examination of the accounts reported by the management as a result of these factors (T. Agwor, Citation2016). Nonetheless, in this literature, audit independence can be defined as impartiality, avoidance of biases, honesty, and the readiness to offer an honest view when making an audit opinion (Ogbodo & Ajuonu, Citation2021).

Figure 1. Diagrammatic representation of study objectives.

The tax is a fee levied by the government on individuals and businesses in order to generate revenue. Asides from the sale of crude oil in Nigeria, there are other sources of government revenue, one of these sources is tax. Proceeds gotten from taxation are used by the government to execute their functions, these functions include the provision of welfare goods, settling of disputes, protection of lives and properties, national defense, implementation of laws and policies, etc. (Chude & Chude, Citation2015). Many purposes are met through taxation, including providing funds to finance government spending, redistribution of wealth, macroeconomic stability, economic growth, etc. (Kabajulizi, Citation2019). Tax can be either direct or indirect. Examples include company income taxes and personal income taxes While tax is indirect if the charge is levied on one individual with the intention that the obligation would be passed on to third parties. Examples include custom charges and value-added taxes, this is because the government levy is calculated into the price of the goods on which they are imposed and transferred to the consumer (Gwangdi & Garba, Citation2015).

However, the government authorities should use tax collected to maintain law and order in that country (Oyedokun, 2020). Although the Nigerian economy is based on oil income, taxes have contributed considerably to the country’s Gross Domestic Product (GDP) throughout time (Adefolake & Omodero, Citation2022) ,). Thus, the most fundamental factor in controlling and creating an economy is taxation (Etim et al., Citation2020). The Federal Government authorized the range of taxes and levies that might be received by the three levels of government in Decree No.21 of 1998 Law of the Federation of Nigeria (LFN). The goal was to eliminate tax duplication and curb disputes among the three levels of government. The authorized list was then amended in 2015 using the Taxes and Levies (Approved List for Collection) (Act amendment) Order Adefolake and Omodero, (Citation2022).

From a conceptual perspective, the term corporate tax has several elements and has been defined distinctively by different authors (Nwaorgu & Abiahu, Citation2020). Corporate tax is defined as a legal transfer or payment paid to the government by people, entities or organizations (Abiahu & Amahalu, Citation2017). They are charged on the income made by businesses throughout the course of doing business within a certain tax period. Corporate taxes are mostly levied on businesses that generate profits after deducting expenditures from sales (Nwaorgu & Abiahu, Citation2020). The following charges are paid by Nigerian companies: Company Income Tax, Tertiary Education Tax, Capital Gains Tax, National Information Technology Development Levy, and Police Trust Fund levies, etc. (Ştefănescu et al., Citation2018).

Productivity explains the way a company makes productive and brilliant use of resources in order to achieve its intended result by increasing share price, revenue, the market value of shares, profitability, net present value, the demand of its product or service. etc. (Ibrahim et al., Citation2018). It can be measured in relation to profits or income (Olurankinse et al., Citation2021). Government taxes are based on a company’s profit, and profitability is defined as a company’s ability to generate more revenue while absorbing all costs associated with generating that revenue, including tax (Akadakpo & Akogo, 2021). After all tax expenditures have been subtracted, profit after tax is the net amount made by a firm (Omodero & Ogbonnaya, Citation2018). The greatest indication of a company’s economic performance in relation to the capital invested is profitability, the amount of the net profit indicates the financial performance (Adegboye, et al., Citation2020). The complexities that management faces in making important decisions, as well as the situational factors that accompany such judgments, necessitate an independent assessment. This is why an external auditor with financial expertise is required (T. Agwor, Citation2016). Net Asset Value is one way to assess the financial performance of a company. The NAV is calculated by deducting liabilities from the total value of the assets. The value of a company’s net assets is the sum of its assets less its liabilities. The formula for calculating net assets is (Total Non-Current Assets + Total Current Assets) – (Total Current liabilities + Total long term liabilities).

2.2. Theoretical framework

This aspect of the study provides appropriate theories associated with the research title. The goal is to provide the readers with a thorough understanding of the perspectives linked with this research. The theories are as follows:

2.2.1. Policeman theory

According to the policeman theory, the auditor is in charge of searching for, discovering, and preventing any fraudulent behavior. The role of an auditor is to focus on arithmetical accuracy as well as fraud prevention and detection (Ittonen, Citation2010). It may be argued that in modern societies, users of financial statements want auditors to be in charge of detecting fraud because they rely on audit reports to analyze and make judgments. Auditors, on the other hand, are not accountable for uncovering all fraud, but they should work to increase their detection rate in order to boost public confidence (Olagunju & Leyira, Citation2012). According to Jackson and Stent (Citation2010), there has been a paradigm change from searching for, detecting, and preventing fraud to providing adequate assurance as to whether an entity’s financial statement correctly depicts its financial situation, performance, and cash flows in all material elements.

2.2.2. The credibility theory

According to credibility theory, giving credibility to financial accounts is an essential aspect of auditing, making it a basic service provided by auditors to their customers. Users’ trust in an organization’s financial records and management’s stewardship increases as a result of audited financial statements, which improves the quality of their decisions, such as investments or new contracts, based on trustworthy data. This is due to the fact that financial statements must be trusted by all parties involved (Ittonen, Citation2010). Management uses audited financial statements to increase stakeholder confidence in the leadership of the company. According to the lending credibility theory, the audit’s principal purpose is to add credibility to the financial accounts. The service that auditors sell to their clients, in this view, is credibility (Owolabi & Olagunju, Citation2020).

2.2.3. Ability to pay theory

According to the ability to pay theory, persons should be requested to pay taxes based on their ability to pay, and their taxable capacity should be determined largely based on their income and property (Chauke et al., Citation2017). This theory is relevant to this study because it explains that companies or organizations should pay taxes based on their ability and capacity to pay. The ability of a company to pay taxes can be discovered by measuring the financial performance of such a company. Company income tax, for instance, is a tax levied on the profits of businesses unless the Act expressly exempts such businesses. As a result, only organizations with yearly revenue in a surplus of N100 million will be subject to 30 percent taxation (Timah & Chukwu, Citation2021). As a result, the profitability, liquidity, effectiveness, and share price of corporate entities and shareholders in Nigeria must not be significantly impacted to the point where organizations are trapped (Timah & Chukwu, Citation2021).

2.2.4. Sacrifice theory

This taxation theory explains that after exerting sufficient effort to sustain income, each individual’s surplus should be directed toward government spending. Taxation is a sacrifice made on the basis of corporate earnings in order to generate income for the government (Timah & Chukwu, Citation2021). Taxes are viewed as a sacrifice by taxpayers, which poses the question of what each taxpayer’s sacrifice should be and how such sacrifice should be measured (Chauke et al., Citation2017).

2.3. Empirical review

During the period 2003–2020, K. Ehiedu and I. Toria () studied the audit indicators and financial performance of Nigerian manufacturing enterprises (18 years). Findings showed that Audit committee financial expertise (AUCFE) and audit committee management expertise (AUCMT) had a substantial influence on Unilever Nigeria Plc’s profits per share, according to the research, which has a p-value t-statistics below 5% significance. Sunardi (Citation2022) investigated how gender roles affect tax compliance and how it is affected by both access to financial resources and financial statement audits. According to the conclusions of this research, the audit of financial statements improved tax compliance by facilitating the availability of financing. DeFond et al. (Citation2000) investigated the aspects that are seen as crucial for the statutory audit function in order to reestablish trust in financial statements, their value relevance, and their utility in making decisions. As a result of the paper’s findings, it has been determined that statutory audits may be improved by increasing the auditor’s responsibility, expanding the auditing curriculum and restricting the supply of non-audit services, as well as supporting the use of a joint audit process.

A study by Olurankinse et al. (Citation2021) looked at the impact of tax preparation on the financial performance of Nigerian development banks. From the results that emerged, effective tax rate, tax savings, capital intensity, and business size all had a significant impact on bank financial performance when analyzed using pooled regression analysis techniques. Return on equity was negatively and insignificantly affected by the effective tax rate, whereas tax savings were positively and insignificantly affected by the effective tax rate. Firm size and capital intensity, on the other hand, had a considerable impact on return on equity. The impact of the auditor’s personal income tax on the audit work was examined by Steller and Pummerer (Citation2021). Tax rates and loss recognition had a significant impact on how concerned an auditor should be about financial reporting. Using a complete enumeration sampling approach, Oyeshile and Adegbie (Citation2020) studied the influence of corporate tax planning on the financial performance of 15 listed food and drinks businesses on the Nigerian Stock Exchange (NSE) over ten years from 2008 to 2018. They found that all proxies of corporate tax planning had a substantial impact (Adjusted R 2 = 0.1095: F-statistic 37.76, p = 0.00005). For the period 2006 to 2016, Enekwe and Nwoha (Citation2020) studied the impact of audit quality on the financial performance of listed manufacturing companies in Nigeria. Auditor independence had a good and considerable impact on the financial performance of listed industrial companies, according to the research.

(- . To see whether a tax audit system is more efficient, Dada (Citation2017) analyzed whether it is possible for tax auditors to have access to the internal statutory audit report, which contains information on statutory audit modifications. The study showed that tax auditor incentives and business emphasis on book income had a significant impact on whether or not extra information improves efficiency. Incentives for highly-skilled tax auditors had little impact on our efficiency measures. From 2010 to 2019, Amahalu and Obi (Citation2020) examined the impact of audit quality on the financial performance of Nigeria’s publicly traded conglomerates. An audit committee’s return on assets was examined in relation to its size, independence, and financial skill, all of which were factors in this research. A substantial positive impact on return on assets (ROA) was found to be associated with audit committee size, independence, and financial knowledge (all at a 5% significance level).

For the period 2014 to 2016, Thanjunpong and Awirothananon (Citation2019) studied the relationship between tax planning (hereinafter referred to as TP) and financial performance (hence referred to as FP). There are 873 firm-years in the sample, which does not include the banking sector. According to the study, there were both positive and negative consequences of the TP. For ETR, the result was positive, however for TAX/ASSET, the result was negative. According to Olaoye (Citation2019), independent statutory auditors have an influence on the trustworthiness of Nigerian manufacturing businesses’ financial accounts. Independent statutory auditors were found to improve financial statements’ dependability (RFS) by a factor of 9.018, an adjusted R2 of 0.191, and a P value of 0.05 or below. Non-financial interest (NFI) also had a positive but negligible influence on RFS, AdjR2 = 0.195; F-Stat. = 9.255; P = 0.000, according to the findings. In addition, audit tenure (AT) had a favorable and substantial impact on RFS, AdjR2 = 0.078; F-Stat. = 3.877; and P value = 0.005; AdjR2 = 0.118; F-Stat. = 5.568; P-value = 0.000; NAS had a positive significant influence on RFS. An investigation on the link between corporate tax planning and the financial performance of non-financial enterprises was conducted by Olarewaju and Olayiwola (Citation2019). From 2007 to 2016, secondary annual statistics were obtained from 47 non-financial firms. Variance decomposition and the impulse response function were used in the panel vector autoregressive technique. Financial performance was shown to be directly linked to tax savings, whilst tax avoidance was found to be directly linked to financial performance. The financial performance responses to shocks in tax avoidance had an expansionary effect, which could hinder the performance of the companies, while the financial performance responses to shocks in tax savings had a contractionary effect, and as such, could improve the performance of the companies.

In Nigeria, Fagbemi (Citation2019) looked at systemically significant banks’ tax planning and financial performance. While Pooled OLS was employed for data analysis, ex-post facto was utilized as a research design. Research shows that the effective tax rate had a negative and considerable influence on financial results. Financial performance of Nigerian SIBs had been positively impacted by thin capitalization, although the capital intensity and the leasing option had little effect on SIBs’ financial performance. An investigation of investor responses to financial performance information and audit quality was conducted by Tarmidi and Zaman (Citation2019). Investors only responded negatively to strong financial performance but bad audit quality, indicating that they are worried about audit processes when evaluating the financial success of a firm, according to the findings. Due to a high firm’s performance, investors paid more attention to the company since the excellent value was regarded to be harmful to investors because of the uncertain quality. Audit committee efficacy as it relates to deposit money banks in Nigeria was evaluated empirically by Osemene and Fakile (Citation2018). Using ROE as a measure of financial success, financial independence, financial knowledge, and the frequency of meetings were found as possible influences on financial performance. According to the findings, audit committee meetings should be held more often so that members had more opportunity to discuss urgent and current concerns specific to their respective deposit money banks.

Nigerian banks’ financial performance was examined by Okenwa (Citation2017) to see how audit quality affected that performance. According to the study’s findings, Nigerian banks’ ROA, CAGR, and OPMR are all affected by audit quality in some way. However, audit quality had a considerable impact on the bank’s operational profit margin and return on assets, but had no impact on the bank’s cash generation ratio. Some chosen companies were studied by Eniola and Akinselure (Citation2016), who examined the impact of internal control on financial performance. Survey research is used as the study’s technique. The results demonstrated that internal control had a significant link with fraud committed in the firm. The study advised that management should adopt more effective techniques to guarantee that internal control was effective and efficient so that fraud perpetration in the organization is greatly decreased.

In light of recent events, such as the well-known accounting scandals, the enactment of the Sarbanes-Oxley Act, and regulatory measures by the SEC and PCAOB., According to Musa and Shehu (Citation2015), the financial performance of Nigerian quoted companies was impacted by the quality of their audits. Auditor independence has a greater impact on financial performance than auditor numbers. Shehu and Abubakar (Citation2015) evaluated the link between corporate governance and financial performance when the discretionary component of accruals is removed from the calculation. Research showed that corporate governance had a considerable influence on business performance.

3. Methodology

The research design is referred to as the framework of any research. It is the force that binds all of the components in research (Akhtar, Citation2016). It involves organizing the requirements relevant for data collection and analysis in a relevant approach to the research. This study makes use of the Ex-post facto research design. Essentially, Ex-post facto research design refers to how we might conduct impact analysis on available data. Ex-post facto means “from what is done after the fact” (Sharma, Citation2019). The study’s population consists of manufacturing enterprises registered on the Nigerian Stock Exchange (NSE). Although, the companies selected for use in this study are limited to just 3 sectors. They are the consumer goods, industrial goods, and service sectors. Thus, this research examines the financial statements of manufacturing companies listed on the Nigerian Stock Exchange (NSE). This research studies the annual reports for a period of 6 years (2016–2021) and this is because they have the most recent data available for these organizations. The study covers a population of 161 manufacturing companies.

This study involves a sample size of 10 listed manufacturing companies on the Nigerian Stock Exchange (NSE). The research focuses on these companies’ annual reports over a six-year period, beginning in 2016 and ending in 2021. This period was chosen based on the fact that this is the most recent period in which the necessary data exists, and this is important in deriving meaningful conclusions and comply with International and Financial Reporting Standards (IFRS). The criterion sampling method is adopted for this research. When financial information and reports for all organizations are irregular, the criteria sampling method is applied. Thus, only the organizations that meet the required criteria will be sampled. The conditions required for selection in this study were manufacturing companies listed on the Nigerian Stock exchange, which had their Audit fees, Net assets, Profit after tax, and other forms of corporate tax disclosed in their annual reports. The sampled organizations include: John Holt, Chellarams, SCOA, Guinness, Transcorp, International Breweries, Cadbury, Lafarge, Dangote Cement and Nestle Plc.

This study collected data using secondary sources which consists of audited annual reports of the sample companies within the period of 6 years (2016–2021) from the companies’ official websites. Their financial statements will be examined to obtain the data required for the study. This source of data collection was adopted because the data required for this study are embodied in that single document. It was also selected because the necessary data for this study can only be found in financial reports, primary sources of data collection don’t provide these facts. The data to be collected includes the companies’ audit fees, tax expenses, net assets, and profit after tax. After collecting all the relevant data, an analysis of the data is required to be done. This study makes use of the panel regression method of data analysis. This method was adopted because it measures the relationship between the independent and dependent variables and it is an efficient means to evaluate variables over a given period. This paper assesses the impact of statutory audit and corporate taxation on the financial performance of companies.

The independent variables in this study are statutory audits and corporate taxation. The control variable is the Total assets (TAS). Statutory audit is measured using audit fees, while corporate taxation is measured using tax expenses charged against the statement of profit or loss. Financial performance is the dependent variable in this study. Profit after tax and Net Assets are the measures of financial performance adopted. Profitability is measured by the Profit-after-tax (PAT) of the companies being analyzed. All data necessary for the measurement of the independent and dependent variables are contained in the annual reports of the selected listed organizations.

3.1. Model specification

From the title of this research, the dependent variable is “financial performance” operationalized into “profit after tax” and “net assets” while the independent variables are “statutory audit” and “corporate taxation”. The “statutory audit” variable will be tested on “audit fees” while “corporate taxation” will be tested on “tax expenses”. The dependent variable (financial performance) will be tested on “profit after tax” and “net assets”.

The functional relationship is:

Where:

Y= Financial Performance

X1= Statutory Audits; X2 = Corporate taxation; X3 = Total assets (control variable)

Equation 1 can be further explained as:

Equation 2 can be used to understand the relationship between the constructs by breaking it further into the several proxies of the dependent, independent and control variables. The equation becomes:

Where:

FPF= Financial Performance (proxied by PAT and NTA)

PAT= Profit After Tax

NTA= Net Assets

While the explanatory and control variables include:

AUDF= Audit Fees (independent variable)

TEX= Tax Expenses (independent variable)

TAS = Total assets (used as a control variable)

β0 = Intercept of the regression

β1 = Coefficient of Audit Fees; β2 = Coefficient of Tax Expenses; β3 = Coefficient of Total assets.

μ = Error term

it = Time Coefficient (Mauris & Rizal, 2021).

4. Data presentation and analysis

This chapter is about presenting and evaluating the data obtained for this report. It reveals the statistical approach of descriptive analysis, correlation analysis, and the analysis of regression methodology used to interpret the data for the study with the objective of achieving the objectives of the research stated earlier. This chapter focuses on the presentation of data obtained from the annual reports of selected listed companies in Nigeria. The empirical study covers a sample of 10 listed manufacturing companies over a period of 6 years (2016–2021). This chapter allows the data gathered to undergo descriptive, correlation, regression, and panel data analysis. The impact of statutory audits and corporate taxation on a firm’s financial performance is examined through the analyses carried out, and the results of the Hypotheses tested are shown. The instrument for the data analysis is Eviews.

4.1. Descriptive statistics

The table below gives us the statistics used for the description of the dependent variables and independent variables ranging from the average, mid-value, maximum, minimum, and deviation to the spread and normality of all the variables used on the aggregate study. The table below represents the descriptive statistics of the model in Table .

Table 1. Variable types and measurement

From the table presented above, the descriptive analysis result showed the attributes and nature of the variable used in the study. It showed each variable’s median, mean, minimum and maximum values, standard deviations, kurtosis, skewness, probability, Jarque-Berra, and the sum of square deviations. The described variables were the log of Audit Fees (LNAUDF) and log of Tax Expenses (LNTEX) which were the independent variables, the other two were the log of Net Assets (LNNTA) and log of Profit After Tax (LNPAT) which were the dependent variables and measures of companies’ financial performance. The mean and median both represented the measures of central tendency. The mean score of log of Audit fees (LNAUDF) was 17.16, the mean value of log of Net Assets (LNNTA) was 23.82, the log of Profit After tax (LNPAT) mean value was 22.08, the log of Tax Expenses (LNTEX) mean value of was 20.78 and LNTAS used as a control variable is 24.44.

The standard deviation describes the deviation of each series from its mean value. The log of Profit After Tax (LNPAT) had the highest value of 2.288250. The standard deviation of the log of Audit Fees (LNAUDF) was 1.221624, 2.405785 for the log of Net Assets (LNNTA), while the log of Tax Expenses (LNTEX) had a standard deviation of 2.2877888. The minimum and maximum numbers were 14.50866 and 19.70439 respectively for the log of Audit Fees (LNAUDF), 18.00517 and 2,801,047 for the log of Net Assets (LNNTA), 17.81662 and 26.90008 for the log of Profit After Tax (LNPAT), 15.20180 and 29.45412 for the log of Tax Expenses (LNTEX). Skewness is a distortion or asymmetry in a data set that differs from the normal distribution or the symmetrical bell curve. Data that is skewed left indicates that the skewness values are negative, whereas data that is skewed right indicates that the skewness values are positive. The left tail is long in comparison to the right tail if it is skewed to the left. Skewed right, on the other hand, merely signifies that the right tail is long in comparison to the left tail. If skewness is = 0, the data is perfectly symmetrical. Therefore, it is shown in Table that all the variables (LNAUDF, LNNTA, LNPAT and LNTEX) were skewed as their values fell between 0 and 1 with values of −0.013548, −0.214708, 0.373170, and 0.241459 respectively. Although, LNAUDF and LNNTA were negatively skewed while LNPAT and LNTEX were positively skewed.

Table 2. Descriptive Statistics results

The kurtosis value in the descriptive statistics shows how peak or flat the distribution of the series included in the study. The decision criteria is placed at 3 and values greater than three are regarded as leptokurtic, values less than 3 are regarded as platykurtic while values equal to 3 are regarded as mesokurtic. From Table above, the kurtosis of log of Audit Fees (LNAUDF) is 2.461597, therefore it is platykurtic. The kurtosis of the log of Net Assets (LNNTA) is 2.579839, therefore it is platykurtic. The kurtosis of the log of Profit after Tax is platykurtic, with a value of 2.429978 while the kurtosis of the log of Tax Expenses is leptokurtic, having a value of 3.129553. Jarque-Bera test is done to evaluate the normality of the series and its probability is used to determine this. To demonstrate that the variables are normally distributed, the probability values must be significant at either 1, 5, or 10% level of significance. From Table , all the variables (LNAUDF, LNNTA, LNPAT, and LNTEX) were normally distributed as the probability values were significant at 10 percent level of significance with probability values of 0.695402, 0.636884, and 0.332061, and 0.731622 respectively.

4.2. Correlation analysis

The researcher made use of the correlation matrix to study the link between the independent and dependent variables. The degree and direction of a linear relationship between variables are shown by correlations. Correlation coefficients range between −1 and+1. A negative correlation is represented by −1, a positive correlation by+1, and no connection at all by 0. A positive coefficient (+) means that when one variable’s value rises, so does the other, and they result in an upward slope on a scatterplot. Negative coefficients (-) indicate that when one variable’s value rises, the value of the other variable fall.

Table shows the correlation coefficients of the dependent, and independent examined in the study. It shows that the coefficient correlation of a variable with respect to itself is 1.000. This indicates that there exists a perfect Correlation between a variable with respect to itself. The correlation coefficient depicts the association between the dependent variables (PAT and NTA) and the independent variables (AUDF and TEX) while the control variable is (TEX). The result above shows the correlation values coupled with the appropriate probabilities. According to Table , AUDF has a positively significant relationship with NTA, AUDF has a positively significant relationship with PAT, TEX has a positively significant relationship with NTA and TEX has a positively significant relationship with PAT. The control variable (TAS) does not correlate positively with any of the variables used in this study.

Table 3. Correlation analysis

4.3. Regression analysis

In order to capture the impact of statutory audits and corporate taxation on the financial performance of companies, Panel regression technique was used. In Panel Data methodology, either the Fixed Effect or Random Effects are used. Therefore, the Hausman Test would be used to help us determine which of the two methods to choose. The results from the regression analysis for the firms are presented below.

According to Table , the probability value (0.02) of the correlated random-effect Hausman test is less than 5% (0.05). We, therefore, accept the fixed effect model as the basis for discussing the findings.

Table 4. Hausman Test showing fixed effect outcome

Table shows the relationship between the independent variables and net assets using panel square regression method. The R-squared value of 0.928 shows that about 93% systematic cross-sectional variations in Net Assets are explained by the independent variables of the log of Audit Fees and the log of Tax Expenses leaving 7% unaccounted for. The robust F-statistic of 50.87 and the associated probability value of 0.000 indicates a significant linear relationship between the dependent variable and the independent variables. Based on the individual significance level of the variables as shown by the t-statistics and the direction of their relationships with the dependent variable (LNNTA), the result shows that Audit Fee (LNAUDF) has a significant positive impact on Net Assets (NTA). This is because the probability value of 0.072 is less than 0.10. In this case, the null hypothesis which states that audit fee does not impact significantly on net assets is hereby rejected or nullified. This suggests that an increase in net assets can be caused by an increase in audit fees. Also, Tax Expense (LNTEX) and total asset (LNTAS) have an insignificant positive effect on Net Assets (NTA). Thus, we accept the null hypotheses because LNTEX and LNTAS do not have significant effect on LNNTA.

Table 5. NTA Regression Analysis (Fixed Effect)

According to Table , the probability value (0.562) of the correlated random-effect Hausman test is more than 5% (0.05). We, therefore, accept the random effect model as the basis for discussing the findings.

Table 6. Hausman Test indicating random effect

Table shows the relationship between the independent variables and Profit after Tax using panel square regression method. The R-squared value of 0.535 shows that about 53% systematic cross-sectional variations in Profit after Tax are explained by the independent variables of the log of Audit Fees and the log of Tax Expenses leaving 47% unaccounted for. The robust F-statistic of 21.45 and the associated probability value of 0.000 indicates a significant linear relationship between the dependent variable, independent and control variables. Based on the individual significance level of the variables as shown by the t-statistics and the direction of their relationships with the dependent variable (LNPAT), the result shows that Audit fee has a positively significant effect on the profit after tax. This is because the t-statistics value of 5.93 is greater than 1.96 and the probability value of 0.000 is less than 0.1 at 10% level of significance. Therefore, the null hypothesis which infers that audit fee does not have direct positive influence on profit after tax is hereby invalidated. In the same vein, tax expense (LNTEX) has a significant positive effect on profit after tax (PAT). This is because the t-statistics value of 2.693 is greater than 1.96 and the probability value of 0.009 is less than 0.10 at 10% level of significance. We have also rejected the null hypothesis that LNTEX does not impact significantly on LNPAT. The result further shows that LNTAS which is the control variable has an insignificant negative outcome. Thus, the null hypothesis is accepted, implying that LNTAS does not impact significantly on LNPAT.

Table 7. PAT Regression Analysis (Random Effect)Dependent variable: LNPAT

4.4. Test of hypotheses

The hypotheses stated at the commencement of this research work will be tested, discussed, and reviewed in this section of the study. The P-value and t-statistic of the regression analysis will determine whether to accept or reject the null hypotheses. The 10 percent level of significance and t-statistic value of 1.96 are the decision rules considered in accepting or rejecting the null hypotheses. As a result, if the p-value of a particular variable is less than 0.1 and the t-statistic is greater than 1.96, the null hypothesis will be rejected.

Hypothesis 1

Statutory audits have no significant impact on the profit after tax of selected listed companies in Nigeria.

The panel regression results above show that the impact of statutory audits on profit after tax has a P-value of 0.0000 and a t-value of 5.934. As a result, we reject the hypothesis which states that statutory audits have no significant impact on the profit after tax of selected listed companies in Nigeria. We reject the null hypothesis because its P-value is lower than 0.1 and the t-value is higher than 1.96.

Hypothesis 2

Statutory audits do not significantly affect the net assets of selected listed companies in Nigeria.

The panel regression results above show that the impact of statutory audits on net assets has a P-value of 0.072 and a t-value of 1.839. As a result, we reject the hypothesis which states that statutory audits have no significant impact on the net assets of selected listed companies in Nigeria. We reject the null hypothesis because its P-value is lower than 0.1 and the t-value is higher than 1.96.

Hypothesis 3

Corporate taxation has no significant influence on the profit after tax of selected listed companies in Nigeria.

The panel regression results above show that the impact of corporate taxation on profit after tax has a P-value of 0.009 and a t-value of 2.693. As a result, we reject the hypothesis which states that corporate taxation has no significant influence on the profit after tax of selected listed companies in Nigeria. We reject the null hypothesis because its P-value is lower than 0.1 and the t-value is higher than 1.96.

Hypothesis 4

Corporate taxation has no significant impact on the net assets of selected listed companies in Nigeria

The panel regression results above show that the impact of corporate taxation on net assets has a P-value of 0.118 and a t-value of 1.594. As a result, we do not reject the hypothesis which states that corporate taxation has no significant impact on the net assets of selected listed companies in Nigeria. We accept the null hypothesis because its P-value is higher than 0.1. Table shows the details of the outcome of the study and the hypothses we reject or do not reject.

Table 8. Test for Hypothesis

Hypothesis 1:Statutory audits have no significant impact on the profit after tax of selected listed companies in Nigeria.

The panel regression results above show that the impact of statutory audits on profit after tax has a P-value of 0.0000 and a t-value of 5.934. As a result, we reject the hypothesis which states that statutory audits have no significant impact on the profit after tax of selected listed companies in Nigeria. We reject the null hypothesis because its P-value is lower than 0.1 and the t-value is higher than 1.96.

Hypothesis 2: Statutory audits do not significantly affect the net assets of selected listed companies in Nigeria.

The panel regression results above show that the impact of statutory audits on net assets has a P-value of 0.072 and a t-value of 1.839. As a result, we reject the hypothesis which states that statutory audits have no significant impact on the net assets of selected listed companies in Nigeria. We reject the null hypothesis because its P-value is lower than 0.1 and the t-value is higher than 1.96.

Hypothesis 3: Corporate taxation has no significant influence on the profit after tax of selected listed companies in Nigeria.

The panel regression results above show that the impact of corporate taxation on profit after tax has a P-value of 0.009 and a t-value of 2.693. As a result, we reject the hypothesis which states that corporate taxation has no significant influence on the profit after tax of selected listed companies in Nigeria. We reject the null hypothesis because its P-value is lower than 0.1 and the t-value is higher than 1.96.

Hypothesis 4: Corporate taxation has no significant impact on the net assets of selected listed companies in Nigeria

The panel regression results above show that the impact of corporate taxation on net assets has a P-value of 0.118 and a t-value of 1.594. As a result, we do not reject the hypothesis which states that corporate taxation has no significant impact on the net assets of selected listed companies in Nigeria. We accept the null hypothesis because its P-value is higher than 0.1.

4.5. Trend analysis

4.5.1. Profit after tax (PAT)

4.5.2. Net assets (NTA)

4.6. Discussion of findings

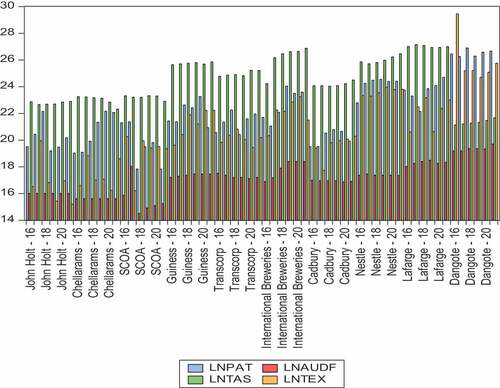

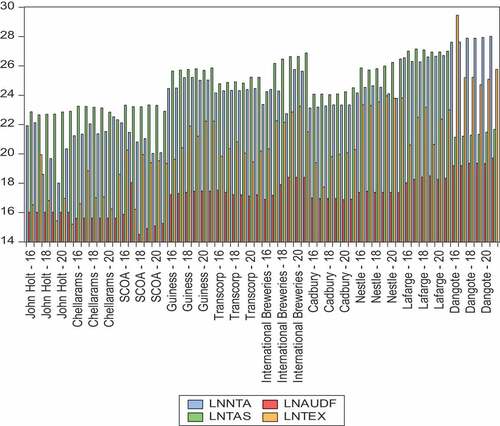

The findings of this study can now be likened and distinguished from past studies based on the empirical analysis of the study on the impact of statutory audits and corporate taxation on the financial performance of companies. Figure provides the trend of data set used in this investigation. This would give room for a better understanding of the investigation’s results. This will begin systematically, giving precedence to the objectives of the study. The first objective of this study was to ascertain the effect of statutory audits on the profit after tax of selected listed companies in Nigeria. According to the results from our analysis, Audit fee has a positively significant relationship with profit after tax. This is because the t-statistics value of 5.934 is greater than 1.96 and the probability value of 0.0000 is less than 0.1 at 10% level of significance. This suggests that an increase in net assets can be caused by an increase in audit fees. The null hypothesis is therefore rejected while the alternative hypothesis is accepted (P < 0.1). The null hypothesis states that statutory audits have no significant effect on profit after tax. The findings of this study are consistent with the works of Enekwe and Nwoha (Citation2020) where financial performance is influenced by the quality of audits.

Figure 2. Trend of data from 2016–2021.

Figure 3. Trend of data from 2016–2021.

The second objective of this study was to investigate the impact of corporate taxation on the profit after tax of selected listed companies in Nigeria. According to the results from our analysis, tax expense (LNTEX) had a significant positive relationship with profit after tax (PAT). This was because the t-statistics value of 2.693 was greater than 1.96 and the probability value of 0.009 was less than 0.1 at 10% level of significance. The null hypothesis is therefore rejected while the alternative hypothesis is accepted (P < 0.1). The null hypothesis states that corporate taxation has no significant effect on profit after tax. The findings of this study are consistent with the works by Olurankinse et al. (Citation2021) which showed a positive significant relationship.

The third objective of this study was to examine the effect of statutory audits on the net assets of selected listed companies in Nigeria. According to the findings, the result shows that Audit Fee (LNAUDF) has a significant positive relationship with Net Assets (NTA). This is because the t-statistics value of 1.839 was greater than 1.96 and the probability value of 0.072 was less than 0.1. Hence, the null hypothesis is rejected (P < 0.1). The null hypothesis states that statutory audits have no significant effect on net assets. The findings of this study are consistent with the work of Amahalu and Obi (Citation2020) which showed a substantial positive impact of ROA as a measure of financial performance.

The last objective of this study was to determine the influence of corporate taxation on the net assets of selected listed companies in Nigeria. Findings reveal that tax expense (LNTEX) has no significant positive effect on Net Assets (NTA). This is because the probability value of 0.118 is greater than 0.1 at 10% level of significance. Hence, the null hypothesis is accepted (P < 0.1). The null hypothesis states that tax expenses have no significant effect on net assets. The findings of this study are inconsistent with the work of Oyeshile and Adegbie (Citation2020) where financial performance is not significantly influenced by corporate tax.

5. Conclusion

The purpose of this research work is to study the impact of statutory audits and corporate taxation on the financial performance of selected listed companies in Nigeria by assessing the current status. The study was done by conducting an investigation on 10 manufacturing companies listed on the Nigerian Stock Exchange. The results showed significant effects of the independent variables on the dependent variables. This section discusses in detail the findings discovered in the research conducted. Based on the findings from the research, conclusions would be drawn. After drawing conclusions, further recommendations would be made towards solving the research problems. These recommendations are then given for subsequent research of the topic and other related studies. The main objective of the study has been to determine the impact of statutory audit and corporate taxation of the financial performance of selected listed companies in Nigeria. The first section served as basic introduction to the work, the background to the study, the statement of the research problem, the objectives of the study, research questions, research hypotheses, significance of the study, scope and limitation of the study and definition of key terms. Section contains the conceptual framework, theoretical framework, empirical framework and the gap in literature. The conceptual framework include various views on the subject of auditing, statutory audits, characteristics of statutory audits, importance of statutory audits, auditor’s independence, taxation, taxation in Nigeria, corporate taxation, types of corporate taxes, financial performance, profitability, and net assets. The theoretical framework embraced about four theories to back up the research while the literature gap stated ways in which the research was done differently.

The section three of this study explains in details, the research design used, the population of the study, the sample size derived from the population, sampling techniques, data gathering method and sources, the method of data presentation and analysis and its instruments. In the fourth phase, correlation and the panel regression analytical tool were employed in the analysis of data collected on the variables. This chapter was focused on testing the hypotheses stated earlier in chapter one. This was done using the Eviews package. The data gathered and used for the correlation and regression analysis were obtained from the Annual Financial Statements of 10 selected manufacturing companies listed on the Nigerian Stock Exchange (NSE) for a period of six years (2016 – 2021). The null hypotheses for hypothesis 1,2,3 and 4 were all rejected. The coefficient values were also positive showing that an increase in the independent variable will lead to an increase in the dependent variables. Finally, the fifth phase entails the summary of work done, the summary of findings, theoretical and empirical findings, recommendations, conclusion, and suggestions for further study and contribution to knowledge. This explains all the data gathered during the investigation. There is the theoretical findings and the empirical finding.

5.1. Empirical findings

The empirical findings associated with this study include:

In hypothesis one, the researcher revealed that statutory audits have a significant impact on the profit after tax of selected listed companies in Nigeria. The null hypothesis is rejected

In hypothesis two, the researcher revealed that statutory audits have a significant impact on the net assets of selected listed companies in Nigeria. The null hypothesis is rejected

In hypothesis three, researcher revealed that corporate taxation has a significant influence on the profit after tax of selected listed companies in Nigeria. The null hypothesis is rejected

In hypothesis four, the researcher revealed that corporate taxation has no significant impact on the net assets of selected listed companies in Nigeria. The null hypothesis is accepted

5.2. Recommendation (s)

Based on the results generated from the analysis, the research suggests that audit firms should continue to be independent, as auditor’s independence has a positive impact on financial performance. Manufacturing companies should be mandated to pay corporate taxes since it has a positive impact on financial performance of the companies. This study leveraged on previous works that have centered on the concept of statutory audits and corporate taxation. However, as stated earlier in the gaps in literature, there is a substantial amount of literature on the impact of statutory audits on the financial performance of companies and, the effects of corporate taxation on the financial performance of companies distinctively, but no researcher has examined the impact of both on the financial performance of companies; thus, this study filled a gap in the literature by providing results on both variables. This study also assisted in reducing the level of inconsistency, as well as a gap in time due to the period covered by the research.

This study came across a few limitations regarding the lack or unavailability of data required from the annual reports of the selected companies that made up the sample size of the study. A reasonable amount of companies was omitted from the population of financial companies as a result of lacking data in the financial statements of those companies. Thus, access to more available data would have constituted a more robust search. Also, in the process of conducting the analysis, not all data extracted were suitable for the study. This led to the exclusion of some already extracted variables. Further research can be made to broaden the concept of statutory audits, corporate taxation and financial performance using other variables asides profit after tax and net assets. In addition, research done at a later date can be conducted using a primary data approach through the use of questionnaires or surveys to analyze this course of study in a different light from the perspective of auditors, tax experts and stakeholders that have direct contact with the financial statements. This study serves as one of the pioneer studies to have considered the effects of statutory audit and corporate taxation on firms’ financial performance. Thus, we suggest inclusion of more control variables in further studies covering this research area.

Acknowledgments

This paper is a piece from Grace Awotayo-Ayeni Oyinkansola’s finished BSc Project from the Department of Accounting Covenant University Ota, Ogun State, Nigeria. Grace Awotayo-Ayeni Oyinkansola appreciates Covenant University’s administration for the opportunity to complete the full research project. She expresses her deepest appreciation to her Supervisor (Dr. Cordelia Onyinyechi Omodero) for her sacrifice, time, patience, counselling, and professional direction during the study period. She also thanks all her course mates for their numerous contributions and help in completing this project.

Disclosure statement

The authors claim absence of conflicts of interest in this research.

Additional information

Funding

Notes on contributors

Grace Awotayo-Ayeni Oyinkansola

Grace Awotayo-Ayeni Oyinkansola is a 2021/2022 graduating set from the Department of Accounting at Covenant University Ota in Ogun State, Nigeria. Her research area emphases the need for statutory audits and corporates taxes to have beneficial impact on financial performance of firms to guarantee their sustainability and fulfill the going concern concept.

Cordelia Onyinyechi Omodero

Cordelia Onyinyechi Omodero is a researcher, an Associate member of the Institute of Chartered Accountants Nigeria and a full-time Lecturer in the Department of Accounting, College of Management and Social Sciences, Covenant University Ota, Ogun State, Nigeria. Her research interests include public finance, fiscal decentralization, taxation, and capital market analysis.

References

- Abba, H. I., & Sadah, A. A. (2020). Audit quality and firm value of listed deposit money banks in Nigeria. International Journal of Economics and Financial Issues, 1(4), 269–22. https://arfjournals.com/image/52477_5_hirhyel_ibrahim.pdf

- Abiahu, M. C., & Amahalu, N. N. (2017). Effect of taxation on dividend policy of quoted deposit money banks in Nigeria (2006-2015). International Journal of Academic Research in Accounting, Finance and Management Sciences, 7(2), 30–46. https://doi.org/10.6007/IJARAFMS/v7-i2/2787

- Adefolake, A. O., & Omodero, C. O. (2022). Tax revenue and economic growth in Nigeria. Cogent Business & Management, 9(1), 1–19. https://doi.org/10.1080/23311975.2022.2115282

- Adegboye, A., Ojeka, S., & Kofo, A. (2020). Corporate governance structure, Bank externalities and sensitivity of non-performing loans in Nigeria. Cogent Economics & Finance, 8(1), 1–21. https://doi.org/10.1080/23322039.2020.1816611

- Agwor, T. (2016). Quality external auditing and profitability of selected manufacturing firms in port harcourt, Nigeria. Journal of Accounting Research, 2(1&2). https://moam.info/quality-external-auditing-and-profitability-ofselected-5b7086e8097c47831c8b456b.html

- Agwor, T. C., & Amangala, P. D. (2020). Audit evidence and financial statement quality in government owned companies in rivers state, Nigeria. European Journal of Business and Management Research, 5(6), 1–6. https://doi.org/10.24018/ejbmr.2020.5.6.606

- Akhtar, D. M. I. (2016). Research design. Research Design (February 1, 2016). Electronic copy available at: https://ssrn.com/abstract=2862445. https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2862445

- Ali Kadhim, H. -F. (2019). The Role of Internal Auditing and Internal Control System on the Financial Performance Quality in Banking Sector. Option, 34(86), 3045–3056. https://produccioncientificaluz.org/index.php/opcion/article/view/27373

- Amahalu, N. N., & Obi, J. C. (2020). Effect of audit quality on financial performance of quoted conglomerates in Nigeria. International Journal of Management Studies and Social Science Research, 2(4), 87–98. https://www.ijmsssr.org/paper/IJMSSSR00194.pdf

- Chauke, K. R., Sebola, M. P., & Mathebula, N. E. (2017). Reflection on the ability to pay theory of taxation in the context of South African Municipalities. International Conference on Public Administration and Development Alternatives. http://ulspace.ul.ac.za/bitstream/handle/10386/1848/chauke_reflection_2017.pdf?sequence=1&isAllowed=y.

- Chijoke-Mgbame, A. M., Boateng, A., & Mgbame, C. O. (2020, July). Board gender diversity, audit committee and financial performance: Evidence from Nigeria. Accounting Forum, 44(3), 262–286. https://doi.org/10.1080/01559982.2020.1766280

- Chude, D. I., & Chude, N. P. (2015). Impact of company income taxation on the profitability of companies in Nigeria: A study of Nigerian Breweries. European Journal of Accounting Auditing and Finance Research, 3(8), 1–11. http://www.eajournals.org/wp-content/uploads/Impact-of-Company-IncomeTaxation-On-The-Profitability-Of-Companies-In-Nigeria-A-Study-of-Nigerian-Breweries.pdf

- Dada, S. O. (2017). Tax planning and firms’ performance in Nigeria. International Journal of Advance Research, 5(5), 1950–1956. https://doi.org/10.21474/IJAR01/4600

- DeFond, M. L., Wong, T. J., & Li, S. (2000). The impact of improved auditor independence on audit a market concentration in China. Journal of Accounting and Economics, 28(1), 269–305. https://doi.org/10.1016/S0165-4101(00)00005-7

- Ehiedu, V. C., & Toria, G. (2022). Audit indicators and financial performance of manufacturing firms in Nigeria. Linguistics and Culture Review, 6(1), 14–41. https://doi.org/10.21744/lingcure.v6nS1.1887

- Enekwe, M., & Nwoha, L. (2020). Impact of audit quality and financial performance of quoted cement firms in Nigeria. International Journal, 2(2), 1–22. https://citeseerx.ist.psu.edu/viewdoc/download?doi=10.1.1.1063.7263&rep=rep1&type=pdf

- Eniola, E., & Akinselure, V. (2016). Auditor Size and Audit Quality. Journal of Accounting and Economics, 3(3), 183–199. https://doi.org/10.1016/0165-4101(81)90002-1

- Etim, E. O., Nweze, A. U., Umoffon, N., & Elias, A. (2020). Empirical analysis of the relationship between tax revenue components and economic growth in Nigeria: 1980-2018. International Institute of Academic Research and Development, 6(3), 61–82. https://www.iiardjournals.org/get/JAFM/VOL.%206%20NO.%203%202020/EMPIRICAL%20ANALYSIS%20OF%20THE%20RELATIONSHIP.pdf

- Fagbemi, I. (2019). Earnings management in response to the introduction of the Australian Gold Tax. Contemporary Accounting Research, 20(4), 747–774. https://doi.org/10.1506/KC7W-C1VN-Y5D4-NAV4

- Gwangdi, M. I., & Garba, A. (2015). Administration of companies income tax in Nigeria: Issues of compliance and enforcement. European Journal of Business and Management, 7(2), 2222–2839. https://core.ac.uk/download/pdf/234626363.pdf

- HAZAEA, S. A., TABASH, M. I., KHATIB, S. F., ZHU, J., & AL-KUHALI, A. A. (2020). The impact of internal audit quality on financial performance of Yemeni commercial banks: An empirical investigation. The Journal of Asian Finance, Economics and Business, 7(11), 867–875. https://doi.org/10.13106/jafeb.2020.vol7.no11.867

- Ibrahim, M., Lawal, S., & Ahmed, A. D. (2018). The Impact of Corporate Taxation on Financing Decisions of Listed Conglomerates in Nigeria. International Journal of Service Science, Management and Engineering, 5(2), 32–39. https://www.eldis.org/document/A102993

- Ittonen, K. (2010). A theoretical examination of the role of auditing and the relevance of audit reports. Accessible at: https://www.uwasa.fi/materiaali/pdf/isbn_978-952-476-298-4.pdf.

- Ivungu, J. A., Anande, K. G., & Ogirah, A. U. (2019). Effect of Audit Quality on Firm Performance: A Review of Literature. International Journal of Advance Acadamic Research, 5(6), 1–13.

- Jabbar, N. S. (2018). The Implications of internal and external auditing integration on the auditing performance and its impact on the expectation Gap: An Exploratory Study in the Iraqi Environment. Academy of Accounting and Financial Studies Journal, 22(3), 1–15.

- Jackson, R. D. C., & Stent, W. J. (2010). Auditing notes for South African students. Audit Education. Accessible at https://pdfprodocs.vip/download/4330427-lexisnexis-auditing-notes-for-south-african-students

- Kabajulizi, C. (2019). The effect of taxation policies on the financial performance of small and medium enterprises in Hoima District: A case of Hoima Municipality. Mparo Division.

- Maydew, C. (2015b). Investigating the relationship between auditor’s opinion and stock return in the companies listed at Tehran stock exchange market. Management Science Letters, 4(1), 81–90. https://doi.org/10.5267/j.msl.2012.11.015

- Muchugia, G. G. (2018). The Effects of External Audit Quality on the Financial Performance of Commercial Banks in Kenya (Doctoral dissertation, university of nairobi).

- Musa, F., & Shehu, U. (2015). An Assessment of Audit Expectation Gap in Ghana. International Journal of Academic Research in Accounting, Finance and Management Sciences, 3(4), 112–118.

- Nafisah, H., & Supriyono, S. (2020). Analysis of the effect of macroeconomics on net assets value (nav) of sharia mutual funds in Indonesia. International Journal of Islamic Business and Economics, 4(1), 11–20. https://doi.org/10.28918/ijibec.v4i1.1527

- Nwaorgu, I. A., & Abiahu, M. F. C. (2020). Effect of corporate tax on sustainable financial performance of listed firms in Nigeria. Journal of Taxation and Economic Development, 19(1), 50–63.

- Ogbodo, O. C., & Ajuonu, A. (2021). Effect of non-audit services on auditor’s independence: Evidence from accounting practitioners in Abia State. Research Journal of Management Practice| ISSN, 2782, 7674. https://doi.org/10.46654/RJMP.1432

- Okenwa, T. (2017). Audit quality, corporate governance and firm characteristics in Nigeria. International Journal of Business and Management, 5(5), 169–179.

- Oladejo, M., Yinus, S. O., Shittu, S., & Rutaro, A. (2021). Internal audit practice and financial reporting quality: Perspective from Nigerian quoted foods and beverages firms. KIU Interdisciplinary Journal of Humanities and Social Sciences, 2(1), 410–428. https://kijhus.kiu.ac.ug/assets/articles/1618054789_internal-audit-practice-and-financial-reporting-quality-perspective-from-nigerian-quoted-foods-and-beverages-firms.pdf

- Olagunju, A., & Leyira, M. C. (2012). Audit expectation gap: Perspectives of auditors and audited account users. International Journal of Development and Management Review, 7(1), 197–215. https://www.ajol.info/index.php/ijdmr/article/view/79309

- Olaoye, E. (2019). The impact of the presence of audit committees on the financial performance of Tunisian companies. International Journal of Management & Business Studies, 2(4 436–449).

- Olarewaju, O. M., & Olayiwola, J. A. (2019). Corporate tax planning and financial performance in Nigerian non‐financial quoted companies. African Development Review, 31(2), 202–215. https://doi.org/10.1111/1467-8268.12378

- Olasupo, S. F., Sorunke, O. A., & Olawuyi, L. (2016). Statutory auditing and performance of small and medium scale enterprises in lagos state, South West Nigeria. The International Journal of Academic Research in Business and Social Sciences, 6(9), 58–67. https://doi.org/10.6007/IJARBSS/v6-i9/2282

- Olurankinse, H., Mamidu, K., & Zhou, N. (2021). Audit committee quality, auditor independence, and internal control weaknesses. Journal of Accounting and Public Policy, 26(3), 300–327. https://doi.org/10.1016/j.jaccpubpol.2007.03.001

- Omodero, C. O., & Ogbonnaya, A. K. (2018). Corporate tax and profitability of deposit money banks in Nigeria. Journal of Accounting, Business and Finance Research, 3(2), 47–55. https://doi.org/10.20448/2002.32.47.55

- Osemene, O. F., & Fakile, O. G. (2018). Effectiveness of audit committee and financial performance of deposit money banks in Nigeria. Fpuntain University Osoghbo Journal of Management, 3(3), 23–34.

- Owolabi, S. A., & Olagunju, A. O. (2020). Historical Evolution of Audit Theory and Practice. International Journal of Management Excellence, 16(1), 2252–2259. https://doi.org/10.17722/ijme.v16i1.1197

- Oyeshile, K., & Adegbie, O. (2020). Internal Control vs. External Manipulation: A model of corporate income tax evasion. The Rand Journal of Economics, 36(4), 151–164.

- Sharma, R. R. (2019). Evolving a model of sustainable leadership: An ex-post facto Research. Vision, 23(2), 152–169. https://doi.org/10.1177/0972262919840216

- Shehu, Q., & Abubakar, N. (2015). Determinants of the Variability in Corporate Effective Tax Rate. Journal of Accounting and Public Policy, 16, 1–34.

- Ştefănescu, A., Pitulice, I. C., & Mînzu, V. G. (2018). The impact of income tax over financial performance of companies listed on the Bucharest Stock Exchange. Journal of Accounting and Management Information Systems, 17(4), 626–640. https://doi.org/10.24818/jamis.2018.04006

- Steller, E., & Pummerer, N. (2021). The Impact of tax cuts on economic growth: evidence from the Canadian Provinces. National Tax Journal, 65(1), 563–594. https://doi.org/10.17310/ntj.2012.3.03

- Sunardi, O. (2022). The effect of auditors opinions on shares prices and returns in Tehran stock exchange. Research Journal of Management Sciences, 1(1), 23–27.

- Tarmidi, C., & Zaman, M. (2019). The corporate governance effects of audit committees. Journal of Management & Governance, 8(3), 305–332. https://doi.org/10.1007/s10997-004-1110-5

- Thanjunpong, L., & Awirothananon, R. (2019). Financial Performance of Firms: Evidence from Pakistan Cement Industry. Journal of Teaching and Education, 7(5), 81–94.

- Timah, B. P., & Chukwu, G. J. (2021). Corporate Taxation and Stakeholders’ Welfare of Selected Manufacturing Companies in Nigeria. Social Sciences, 11(2), 13–26. https://doi.org/10.6007/IJARAFMS/v11-i2/9894

- Ugwuanyi, G. O. (2014b). Taxation and tertiary education enhancement in Nigeria: An evaluation of the education tax fund (ETF) between 1999-2010. Journal of Economics and Sustainable Development, 5(6), 131–141. https://www.iiste.org/Journals/index.php/JEDS/article/viewFile/11945/12288

- UMURERWA, D. (2016). The impact of external audit on the financial management in public organizations: A case study of Rwanda development board (Doctoral dissertation, University of Rwanda). http://dr.ur.ac.rw/bitstream/handle/123456789/868/UMURERWA%20Denyse%20thesis.pdf?sequence=1&isAllowed=y.

- Yusof, N. A. Z. M., Haron, H., Ismail, I., & Chye, O. H. (2019). Independence of internal audit unit influence the internal audit capability of Malaysian public sector organizations. KnE Social Sciences, 1230–1253. https://doi.org/10.18502/kss.v3i22.5122.