Abstract

A large body of research shows that mobile money through its agent networks can potentially increase financial inclusion, especially in the unbanked rural regions of the developing world. This study intends to establish whether agent liquidity has a significant moderating effect in the relationship between mobile money services and financial inclusion of the unbanked poor population in rural sub-Saharan Africa. The data were collected from mobile money users through a cross-sectional approach using a semi-structured quantitative questionnaire and Analysis of Moment Structures was used to test for the moderating effect of agent liquidity between mobile money services and financial inclusion. The results revealed a significant moderating effect of agent liquidity in the relationship between mobile money services and financial inclusion of the unbanked poor population in rural sub-Saharan Africa with data collected from rural Uganda. Agent liquidity enhances access to and usage of mobile money services by 27 percentage points to spur financial inclusion among the unbanked rural poor population. Similarly, agent liquidity has a direct significant effect on access to and usage of mobile money services among the unbanked rural poor population. Overall, the results showed that agent liquidity plays a significant and positive moderating role between mobile money services and financial inclusion. The findings from this study can help mobile money providers to increase the amounts of float to boost agent liquidity to meet instant cash-in and cash-out demands of customers. Besides, regulations on mobile money agents should be loosen to allow more village “dukas” (small village shops) to offer mobile money financial services to crowd-in more unbanked rural poor population into the digital financial system.

Public Interest Statement

Globally, while mobile money has registered great strides in promoting financial inclusion by providing digital financial services, it’s success could be thwarted by insufficient stock of liquid cash to meet the daily transaction needs of potential unbanked customers. Thus, mobile money operators should ensure that mobile money agents have enough floats to meet instant cash-in and cash-out needs of customers. Indeed, maintaining sufficient float levels by mobile money agents to provide storage and withdrawals value can increase access to and use of digital financial services without the need for a bank account. This can significantly increase financial inclusion of the unbanked rural poor customers to enable them to move out of poverty.

1. Background

Currently, while evidence shows that a large number of adults, especially in sub-Saharan Africa do not have access to accounts and other basic financial services from the formal financial sector, the global financial system has been greatly revolutionized through the emergence of mobile money financial technology (World Bank, Citation2020).

The latest data from the Global System for Mobile Communications (GSMA, Citation2021) indicate that the global number of registered mobile money accounts grew by 12.7 percent down from 1.04 billion in the year 2019 to 1.21 billion at the end of the year 2020. The data further show that there were more than 300 million active accounts transacting over $USD 2 billion per day through 4.8 million active agent networks by the end of the same year. Predominantly, the data revealed that the total number of registered mobile money accounts grew by 12 percentage points (562 million) in sub-Saharan Africa with more than 161 million active accounts, which performed about 27.5 billion transactions amounting to over $USD 495 billion by the end of the same year. More specifically, the trends in the above registered performance were achieved due to the tremendous mobile money activities within the East African region, which had more than 293 million registered mobile money accounts with about 94 million that were active, which carried out more than 18.6 billion transactions amounting to over $USD 273 billion by the end of the same year. Contextually, more than 3.5 billion transactions were performed through 29,900,937 active accounts by 371,617 active mobile money agents amounting to over $USD 25.3 billion at the end of the same year (Bank of Uganda, Citation2021).

Okello Candiya Bongomin and Munene (Citation2021); Suri et al. (Citation2021); Ozili (Citation2021) suggest that the adoption and use of mobile money backed by massive phone penetration and ownership has the potential to effectively extend formal financial services to the unbanked poor population through reliable agent networks in rural sub-Saharan Africa.

Demirguc-Kunt et al. (Citation2018) contend that mobile money through its wider agent networks can deliver the required level of proximity to financial services at low transaction costs for most geographically dispersed rural poor population who lack access to formal banking services.

Additionally, Dikit et al. (Citation2012) show that mobile phones through a registered “subscriber identity module” (SIM) has the capability of connecting every town and village. This can facilitate the previously unbanked poor individuals to send and receive money, transfer funds between accounts, and pay bills using their cell phones to overcome distance and lack of bank branches in rural areas.

Furthermore, Donovan (Citation2012) also argues that mobile money can provide an accessible, convenient, and reliable medium for delivery of financial services, especially to the poor who live in remote areas as compared to the traditional banking system. Mobile money can allow the poor to get cash when and where they need it through the agents. This promotes timely access to and use of financial services among the unbanked rural poor population who have been financially excluded from the formal financial system.

Mobile money through its large agent networks can offer a better channel for financial inclusion since it’s cheaper and safer with privacy and autonomy of transactions than other alternative financial sources (Lehmann-Uschner & Menkhoff, Citation2020; Stuart & Cohen, Citation2011; Jack & Suri, Citation2011; Morawczynski, Citation2009).

Besides, Robinson et al. (Citation2022); Burlando et al. (Citation2021); Naito et al. (Citation2021) show that mobile money can help the poor to develop financial history through mobile money transactions trial. This gives them opportunity to access credit from alternative financial sources because the transaction history left behind by mobile money transactions trail can be analyzed and used to assign credit scores. Accordingly, this can allow them to gain access to additional financial services, which results into increased financial inclusion.

Mobile money is important because it allow individuals at the bottom of the pyramid to deposit cash and make withdrawals at retail agent point-of-sale without stringent documentation requirements common with the formal banking system (Okello Candiya Bongomin et al. Citation2021).

Whilst mobile money can provide a potential digital channel through which the unbanked rural poor population can be financially included, the availability of sufficient liquidity levels among agents to meet the daily cash-in and cash-out needs of customers within the mobile money ecosystem remains a great concern to ensure timely availability of financial services to the 1.7 billion unbanked adults (Kirton, Citation2020; GSAM, Citation2018).

According to the GSMA (Citation2019), when the amount in the retail agents’ mobile wallets are used up, they cannot perform additional services. Therefore, they need to refill their mobile money accounts with cash. However, if the agents do not have a bank account linked to their mobile wallets, they have to make a trip to the bank to transfer cash into electronic value. This creates a situation of liquidity problem that can result into long waiting time, costs, and ultimately financial exclusion.

Dermish et al. (Citation2012) suggest that availability of enough cash at the mobile money agents’ point-of-sales can promote timely and quick access to and use of financial services by the unbanked rural poor population, especially in remote regions of sub-Saharan Africa with limited banking structures. Indeed, the presence of sufficient electronic value at an agent point-of-sale to meet instant cash-in and cash-out demand of clients can attract more customers to built trust in the mobile money system and its continued use.

Nevertheless, although studies have linked mobile money to financial inclusion of the most formally excluded population in under developed regions of the world, there is no known study that establishes the moderating role of agent liquidity in the relationship between mobile money services and financial inclusion, especially in sub-Saharan Africa. Moreover, the Financial Inclusion Insights (FII) Survey covering Bangladesh, Ghana, India, Kenya, Nigeria, Pakistan, Rwanda, Tanzania, and Uganda found that lack of liquidity is the main top challenge faced by mobile money agents second to the problem of mobile network downtime. Similarly, a study conducted by Ssonko (Citation2020) within Kampala Capital City Authority jurisdiction further revealed that 62% of the respondents identified lack of cash (liquidity or float) at the agents’ point-of-sales as the number one challenge encountered when using mobile money.

Therefore, the main objective of this study is to establish whether agent liquidity has a significant moderating effect in the relationship between mobile money services and financial inclusion of the unbanked poor population in rural sub-Saharan Africa.

This study will contribute to literature and theory of mobile money by integrating the role of agent liquidity in boosting mobile money access and usage, especially among the unbanked rural poor population. Additionally, it will help regulators of mobile money in developing countries in sub-Saharan Africa to rethink on the importance of authorizing operations by more mobile money agents to increase financial inclusion through mobile money.

2. Literature review and hypotheses setting

2.1. Agent liquidity: moderator between mobile money services and financial inclusion

Recently, digital financial services delivered through mobile money has demonstrated immense potential towards extending formal financial services to the unbanked population, especially the poor who live in remote areas in sub-Saharan Africa. For example, Kim (Citation2022) examined the extent and the way by which mobile money has affected financial inclusion of women in Nairobi. The results revealed that mobile money significantly reduced the proportion of formally financially excluded women and made them to instantly benefit from remittances, payment services, and safe money storage. Okello Candiya Bongomin et al. (Citation2021) further discovered that mobile money had a significant positive effect on financial inclusion of rural poor individuals in Uganda. Batista and Vicente (Citation2021) using a randomized control trial to measure the economic impact of introducing mobile money for the first time in rural villages of Mozambique also found that financial inclusion through mobile money can accelerate African urbanization and structural change while improving welfare in rural areas.

Donovan (Citation2012) argues that mobile money can offer access to financial services such as payments, savings, withdrawals, and remittances to the unbanked population at a cheaper cost. Indeed, mobile money agents provide the channel through which financial services can be accessed by the unbanked individuals in a convenient manner with speed and transactional efficiency (Blumenstock et al. Citation2015; Jack & Suri, Citation2014). Mobile money agents help mobile money customers to easily move from cash to electronic deposits and vice versa (Omigie et al. Citation2017).

Conversely, although mobile money has demonstrated great potential towards delivering financial services to the unbanked rural poor population in most remote parts of the world, its success has been dwindled by inadequate liquidity among mobile money agents (Argent et al. Citation2013; Vutsengwa & Ngugi, Citation2013). Wright (Citation2015b) found that Digital Financial Service customers were primarily concerned about agent illiquidity in Bangladesh, the Philippines, and Uganda. Indeed, agent liquidity has remained a vexing problem, which has limited the reliability of the mobile money financial platform.

Accordingly, the GSMA (Citation2020); Hidayati (Citation2011) argue that providers of mobile money services should ensure that mobile money agents have enough liquidity to sufficiently meet instant customers’ cash-in and cash-out demand.

Mazambani et al. (Citation2018) suggest that mobile money agents should have adequate flow of cash to meet withdrawal demands of customers while retaining sufficient electronic balances to facilitate conversions. Sufficient amounts of cash allow transactions to take place as and when customers want to cash-in or cash-out at the mobile money agents’ point-of-sale without any delay. Moreover, having enough liquidity helps the agent to execute more transactions and provide the services in a much reliable way. This results into easy access to and use of financial services.

The GSMA (Citation2021) further contends that mobile money agents should have enough cash to achieve the main function of converting electronic money to cash. The mobile money transactions between a retail agent and a customer require that the retail agent has cash value in their mobile wallet to complete the mobile money transactions. As a result, more and more customers will cash-in and cash-out, which increases access to and use of financial services.

In addition, the availability of enough float also helps the mobile money agents to reduce the long hours spent on trips to rebalance points. This can enable them to provide timely cash-in and cash-out services to more customers. Consequently, more clients like the unbanked rural poor individuals can use mobile money services to make payments, withdrawals, borrowings, and savings (The Helix Institute of Digital Finance, Citation2017). This can offer convenient and increased access to financial services by customers located in different geographical locations at any time.

Thus, while past and current scholars have argued that mobile money can provide cheap and fast means by which individuals can access and use financial services, a gap exist in the literature on the importance of sufficient liquidity trances among mobile money agents to meet timely transactions by customers. Accordingly, we derive the hypothesis that:

H3:

Agent liquidity significantly moderates the relationship between mobile money services and financial inclusion of the unbanked poor population in rural sub-Saharan Africa.

2.2. Mobile money services and financial inclusion

According to Okello Candiya Bongomin and Ntayi (Citation2020), mobile money can offer easy access to financial services because of its wider coverage and presence of many agent networks operating in different geographical locations.

Tengeh and Gahapa (Citation2020) observe that since most agents work for extended hours to meet the mobile money demands of different customers, they make financial services available at any time and in any place to the customers. This increases access to and use of financial services by the unbanked rural poor individuals.

Similarly, Beck (Citation2020) asserts that while formal banks may require several documentations to open an account from the unbanked individuals, mobile money requires only the national identification card to open an account. This reduces barrier to access and ineligibility due to documentation requirements. Thus, this can attract more unbanked rural poor individuals with national identification document to acquire mobile money account to access and use financial services.

Besides, Batista and Vicente (Citation2021) argue that mobile money offer faster transactions as compared to the traditional banks that need more time to perform transactions. Storing, sending, and receiving money through mobile money is accomplished in a shorter time and at relatively low costs compared to costs and fees charged by banks. Therefore, this may attract more unbanked rural poor individuals to use mobile money, which results into increased access to and use of financial services (Suri & Jack, Citation2016, Suri , Citation2017).

In addition, Mararo and Ngahu (Citation2017) also show that mobile money transactions can be performed by the unbanked rural poor individuals at an agent point-of-sale without making a trip to the bank branches or ATMs. This saves time and costs that are incurred by the unbanked rural poor individuals to travel to the bank to access financial services. This makes it more convenient and cheaper to access and use financial services offered through mobile money than other alternative sources such as banks, thus, increased financial inclusion.

More so, Ndiwalana et al. (Citation2014) also state that the unbanked rural poor individuals do not need a bank account to access mobile money services. The mobile money system requires the customers to get a mobile SIM card from a mobile network operator, which is registered with a mobile money account that can be instantly used to perform transactions. This can speed up access to and use of financial services by the poor.

Indeed, mobile money can offer the unbanked rural poor population financial services with safety, convenience, privacy, and it allows them to quickly and cheaply perform transactions over a wider geographical coverage than banks. Here, we suggest the hypothesis that:

H1:

Mobile money services has a significant impact on financial inclusion of the unbanked poor population in rural sub-Saharan Africa.

2.3. Agent liquidity and financial inclusion

Kirton (Citation2020) observes that in predominately cash-based economies, consumers need a cheap and easy way to convert electronic money into cash, and vice versa. Therefore, agent networks exist to offer these services.

According to Rothe (Citation2020), mobile money agents are a key component of the financial systems in developing countries, especially for lower income households and informal businesses in rural communities. They provide the essential function of converting electronic money to cash that involve digitizing informal cash payments and enabling crucial financial transactions such as money transfers and bill payments.

Furthermore, the mobile money agents also provide last mile financial services to the unbanked rural communities and a viable digital alternative to the brick-and-mortar bank branches found mainly in urban areas (GSMA, Citation2018).

Thus, lack of sufficient funds can affect cash needs of customers, especially those at the bottom of the pyramid who live in rural areas with limited income levels. This puts a strain on the attractiveness of mobile money as a viable and potential channel for financial inclusion.

Accordingly, Rodriguez et al. (Citation2019) suggest that maintaining higher float amounts to respond to high customer demand for cash-in and cash-out can result into increased access to and use of basic financial services by all section of the unbanked population through mobile money.

Relatedly, Eijkman et al. (Citation2010) also observe that availability of enough liquidity at the agent outlet helps the poor who operate in a cash economy, and whose income comes in the form of small lumps of cash, to consistently participate in the mobile money ecosystem by cashing-in and cashing-out easily.

The UNCDF (Citation2020) further indicates that keeping enough float helps the mobile money agents to concentrate on improving their businesses, which makes them to grow and remain in operations. This may result into provision of better mobile money services to users, which can increase financial inclusion by bringing banking services closer to the unbanked rural poor population who live in rural communities.

Figure 1. Proposed conceptual model for the study.

In a nutshell, all agents of mobile money providers should have enough cash and electronic float to serve every customer transaction request at all times without being turned away. The long-term health of mobile money ecosystem depends on agents and availability of floats to satisfy customers’ demand. We develop the hypothesis that:

H2:

Agent liquidity has a significant impact on financial inclusion of the unbanked poor population in rural sub-Saharan Africa.

3. Methodology and research design

3.1. Design and data procedures

Cross-sectional research design was used to collect data to answer hypotheses developed under this study. This research design was used because it is superior over the longitudinal design since it can collect large amount of data over a shorter period of time. Therefore, a quantitative questionnaire was directly administered to obtain data from the selected respondents identified for this study.

3.2. Population and appropriate sample size

The population for this study was selected from individuals engaged in micro small and medium businesses who use mobile money to perform transactions. This particular group was selected because they are presumed knowledgeable about the operation of mobile money services as they frequently use it to conduct business. Thus, 379 micro small and medium owners/managers were probabilistically selected from a total population of 36,640 based on the Uganda Bureau of Statistical abstract on business categorization in Uganda (Uganda Bureau of Statistics, 2010/2011) to participate in this study using Krejcie and Morgan (Citation1970) table for sample size determination.

3.3. Variables for the study

Mobile money services was measured using 20 items based on the construct of intention to use, perceived ease of use, and user satisfaction as adopted from Okello Candiya Bongomin and Munene (Citation2021); Suri et al. (Citation2021); Batista and Vicente (Citation2021); Lehmann-Uschner and Menkhoff (Citation2020); Ozili (Citation2021); Aker et al. (Citation2016); Okello Candiya Bongomin et al. (Citation2018); and modified based on Venkatesh et al. (Citation2003).

Agent liquidity was measured using 12 questions developed and modified from Rodriguez et al. (Citation2019); Dermish et al. (Citation2012); GSMA (Citation2018); Omigie et al. (Citation2017); Mazambani et al. (Citation2018). The questions were derived based on the construct of availability of adequate floats.

Financial inclusion was measured using 19 questions developed and modified from the constructs of access, usage, quality, and welfare impact adopted from Okello Candiya Bongomin et al. (Citation2021); Demirguc-Kunt et al. (Citation2018).

3.4. Data collection, management, and analysis

The data for this study were collected using a quantitative questionnaire directly administered to the selected respondents to elicit responses. The data were collected from owners/managers of micro small and medium businesses by two research assistants over a period of two months from May to June, 2021.

The data for this study were analyzed at two stages: firstly, the data collected from the field were sorted, serially numbered, and captured into Statistical Packages for Social Sciences (SPSS). The data were tested for missing values, outliers, and normality to ensure that they were free of errors. Missing values were identified in the data using frequencies, and since the values were missing at completely random and less than 5%, they were replaced using linear interpolation as recommended by Field (Citation2009). The test for outliers using box plots was also performed on the raw data from the field. The results indicated that no outliers existed in the data. The test to establish assumption of parametric data was also conducted on the data through normality test. The results of the normality test based on the histogram, normal p-p plots, and scatter plots revealed that violation of the assumption of normality was not a problem in the data set and the data were good enough for further statistical test.

The cleaned data were used to construct measurement models through confirmatory factor analysis in Analysis of Moment Structures (AMOS) for each of the variables under this study. Finally, structural equation model through bootstrapping was constructed in AMOS to test for the moderating effect of agent liquidity in the relationship between mobile money services and financial inclusion.

3.5. Reliability and validity

The reliability of the instrument used in this study was tested to ensure internal consistency of the items. This was done to check whether the instrument can give the same answers and consistent results when used again in similar studies by different researchers at different time (Yin, Citation2003). Cronbach’s Alpha coefficient was used to test for the internal consistency of the items in the instrument based on the cut-off point of 0.7 (Nunnally & Bernstein, Citation1994).

Validity was tested to ensure that the instrument gives exact results of what it claims to measure (Babbie & Monton, Citation2002). Content validity was tested by giving the instrument to experts, academics, and professionals in the field of this study to rate the items based on the relevance and irrelevance of measurement items for each of the variables under this study. The content validity index was obtained by dividing the total number of valid items by total items in the instrument (Amin, Citation2005). Convergent validity and discriminant validity were determined using Eigen values and correlation coefficient generated through exploratory factor analysis (Creswell, Citation2014; Neuman, Citation2006; Sekaran, Citation2003). In addition, the average variance extracted (AVE) and composite reliability (CR) were also generated in AMOS through confirmatory factor analysis (Hair et al. Citation2018). The results of reliability and validity assessments are indicated in Tables .

Table 1. Reliability and validity

Table 2. Discriminant validity

3.6. Common method bias

The test for common method bias was performed in this study to ensure that type I and II errors (random and systematic), which inflate or deflate the mean and standard deviation of the constructs (Bagozzi & Yi, Citation1988; Podsakoff et al. Citation2000; Spector, Citation2006) is not a problem. Two approaches were used to test for common method bias in this study.

Statistically, Herman’s single factor test was used to examine whether any of the constructs used to measure the variables in this study emerged dominant (Podsakoff et al. Citation2003). This implies that when one factor emerges dominant as a manifest construct of a variable then common method bias is present in the study. The results of the confirmatory factor analysis revealed that all the manifest variables contributed to variation in the latent construct of mobile money services as the main exogenous variable (Hair et al. Citation2018; Schreiber et al. Citation2006). This indicated that common method bias was not a problem in this study and the results were good and tenable.

Procedurally, the questions in the instrument used to measure each of the variables under this study were checked to improve on the scale. Double barrel, vague, and ambiguous questions were deleted from the instrument and difficult questions were made simple, concise, and specific to suit the study (Tourangeau et al. Citation2000).

3.7. Moderating effect in AMOS

Baron and Kenny (Citation1986) suggest that while testing for interaction effect or moderation, the first step is to establish whether a relationship exist between the exogenous (independent) variable, endogenous (dependent) variable, and the moderator. Baron and Kenny argue that the exogenous variable and the endogenous variable should be associated; the moderator variable and endogenous variable should have some kind of association; the moderator variable and exogenous variable should have some kind of relationship; and finally, the exogenous variable, moderator, and exogenous variable should be related in order to fit in the structural model. The existence of the relationship warrants significance of the influence of the moderator in the relationship between the independent variable and dependent variable although the moderator does not depend on the exogenous variable.

Prior to testing the moderating effect, measurement models for the different variables under this study were constructed through confirmatory factor analysis in AMOS to test for convergent and discriminant validity. The measurement models were constructed for each of the variables under this study to confirm whether the manifest variables load well to their underlying latent constructs derived from exploratory factor analysis (Hair et al. Citation2016).

According to Hair et al. (Citation2014), the goodness-fit-indices (GOF) are used to confirm how well the manifest variables load well to the underlying latent constructs. The GOF is used to test how well the observed data fit to the model. The use of three to four GOF indices is recommended to test how well the observed data fit to the CFA measurement models for the different variables under this study because it provides adequate evidence for the model fit. Therefore, at least one incremental index and one absolute index combined with Chi-square (x2) value and degrees of freedom can be used to explain how well the data fit to the model although the use of three to four fit indices can provide adequate evidence for the model fit (Hair et al. Citation2014).

The use of Chi-square (x2) value with the degrees of freedom together with Comparative Fit index (CFI), Tucker Lewis index (TLI), Incremental Fit index, and Root Mean Square Error of Approximation (RMSEA) can provide sufficient evidence and information for evaluating the CFA measurement models and structural equation model to confirm how well the observed data fit to the models based on the recommended cut-off points (Hair et al. Citation2014; Schreiber et al. Citation2006). Thus, the Chi-square (x2) value with the associated degrees of freedom together with three incremental indices of Comparative Fit index (CFI), Tucker Lewis index (TLI), Incremental Fit index (IFI), and absolute index of Root Mean Square Error of Approximation (RMSEA) were used to test whether the observed data fitted to the model derived in this study guided by theory.

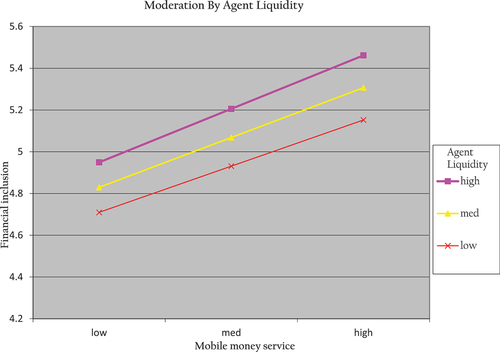

More so, the ModGraph was also used to show the interaction effect of agent liquidity in the relationship between mobile money services and financial inclusion. According to Jose (Citation2013), the results of the interaction effect of the moderator between the independent variable and dependent variable can be put on a graph to depict the strength of the effect based on the slopes or gradients. The indication that the effect of interaction is greater at one level of the variable than another shows that there is significant interaction between the independent, moderator, and dependent variables (Aiken & West, Citation1991). This is based on the fact that the lines on the ModGraph should not be parallel to each other and the slopes or gradients should be different to confirm existence of significant interaction effect. The results of the moderation effect using ModGraph are shown in Figure .

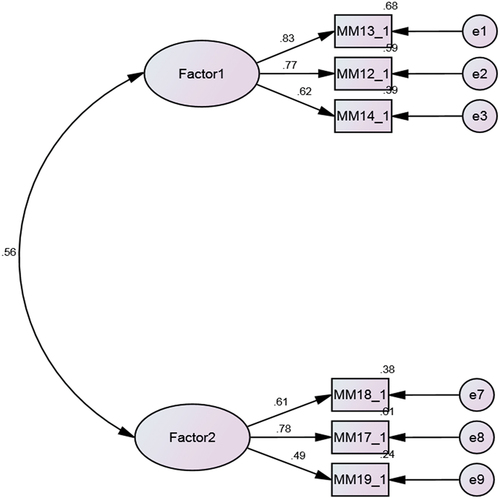

Figure 2. Measurement model for mobile money services.

4. Study findings

4.1. Sample response rate

The target sample selected for this study was 379 owners/managers of micro small and medium businesses located in northern Uganda. Thus, 100% response rate was achieved in this study since the questionnaires were directly administered by research assistants to the selected respondents. Additionally, in circumstances where the respondents did not have enough time to provide responses, the research assistants had to make appointments to ensure that all the data were collected from the samples identified for this study at an appropriate time. Similarly, the time allocated for data collection was enough to ensure that all the data were collected from the identified respondents.

4.2. Reliability and validity

The results of the reliability test revealed that all the variables under this study had Cronbach’s alpha coefficient above 0.7 (Nunnally & Bernstein, Citation1994). This means that all the items used for measuring the variables past the test of internal consistency and can yield similar results when used in related studies at different points in time. Mobile money services had 20 items that yielded Cronbach’s alpha coefficient of 0.825. Agent liquidity had 8 items, which achieved Cronbach’s alpha coefficient of 0.866. Finally, financial inclusion had 19 items that yielded Cronbach’s alpha coefficient of 0.742.

The validity test results also indicated that the average variance extracted and composite reliability were all significant and above the threshold cut-off points of 0.5 and 0.7, respectively (Hair et al., Citation2018). This implies that the instrument used in this study gave the exact results of what it claimed to measure as suggested by Babbie and Monton (Citation2002). The variables of mobile money services, agent liquidity, and financial inclusion had composite reliability figures of 0.806, 0.778, and 0.794, respectively. Besides, the average variance extracted values for mobile money services, agent liquidity, and financial inclusion were 0.751, 0.639, and 0.833, respectively. Furthermore, the results also revealed that the diagonal figures for the main variables were higher than the inter item correlation figures. The results for the reliability and validity tests are indicated in Tables .

4.3. Correlation analysis

The main purpose of this study is to establish the moderating effect of agent liquidity in the relationship between mobile money services and financial inclusion of the unbanked poor population in rural sub-Saharan Africa.

Baron and Kenny (Citation1986) argue that a relationship should exist between the independent, moderator, and dependent variables for test of interaction effect to proceed. Consequently, Pearson correlation analysis was conducted on the data to test for existence of relationships between the variables under this study. The results indicated that there is a significant and positive relationship between mobile money services and agent liquidity (r = 0.108; p < 0.05). In addition, the results also showed that mobile money services and financial inclusion are significantly and positively related (r = 0.312; p < 0.01). The results further confirmed that there is a significant and positive association between agent liquidity and financial inclusion (r = 0.100; p < 0.01). The correlation analysis validated existence of relationships between the independent, moderator, and dependent variables in this study, and the results were significant and tenable as indicated in Table .

Table 3. Correlation analysis

4.4. Confirmatory factor analysis

Confirmatory factor analysis was performed to test for convergent and discriminant validity between the items used as measures for the constructs and latent variables under this study. The measurement models were constructed using AMOS to confirm whether the manifest constructs loaded well to their underlying latent variables derived from exploratory factor analysis (Hair et al. Citation2016).

The results from the confirmatory factor analysis revealed that 14 items were dropped and the manifest constructs loaded well on to the latent variable of mobile money services with excellent model fit indices. The CFA measurement model indicated that 6 manifest constructs loaded well on to the latent variable of mobile money services with excellent model Fit indices and Chi-square (x2) of 6.918 with degrees of freedom of 8 and probability of 0.546; Incremental Fit index (IFI) of 1.002; Tucker Lewis index (TLI) of 1.004; Comparative fit index (CFI) of 1.000; and Root Mean Square Error of Approximation (RMSEA) of 0.000, all above the recommended cut-off points as suggested by Hair et al. (Citation2014).

Similarly, the results from the confirmatory factor analysis showed that 1 item was dropped and 7 manifest constructs loaded well on to the latent variable of agent liquidity with excellent model fit indices and Chi-square (x2) of 8.130 with degrees of freedom of 11 and probability of 0.702; Incremental Fit index (IFI) of 1.014; Tucker Lewis index (TLI) of 1.029; Comparative Fit index (CFI) of 1.000; and Root Mean Square Error of Approximation (RMSEA) of 0.000, all above the recommended cut-off points as suggested by Hair et al. (Citation2014).

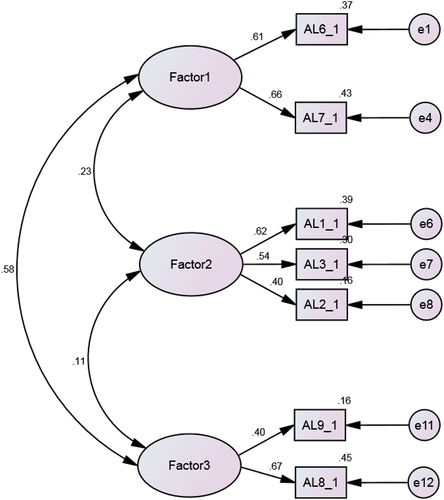

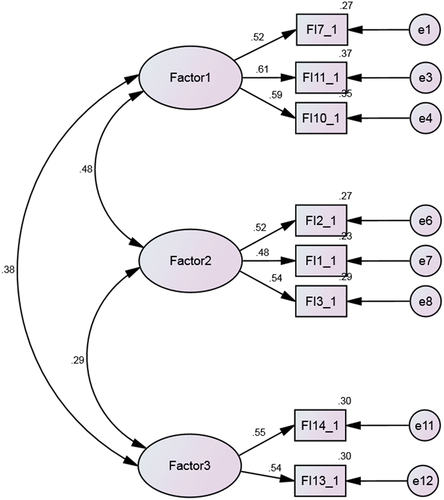

Finally, the results from the confirmatory factor analysis indicated that 11 items were dropped and 8 manifest constructs loaded well on the latent variable of financial inclusion with excellent model Fit indices and Chi-square (x2) of 11.408 with degrees of freedom of 17 and probability of 0.835; Incremental Fit index (IFI) of 1.023; Tucker Lewis index (TLI) of 1.039; Comparative fit index (CFI) of 1.000; and Root Mean Square Error of Approximation (RMSEA) of 0.000, all above the recommended cut-off points as suggested by Hair et al. (Citation2014). The results of the measurement models through confirmatory factor analysis are indicated in Figures .

Figure 3. Measurement model for agent liquidity.

Figure 4. Measurement model for financial inclusion.

4.5. Moderating effect hypothesis

The main purpose of this study is to establish the moderating effect of agent liquidity in the relationship between mobile money services and financial inclusion of the unbanked poor population in rural sub-Saharan Africa.

The moderating effect of agent liquidity in the relationship between mobile money services and financial inclusion was tested by constructing a structural equation model in AMOS. The variables of mobile money services, agent liquidity, interaction effect, and financial inclusion were entered into the structural equation model by requesting 5000 samples in bootstrap AMOS sub-menu.

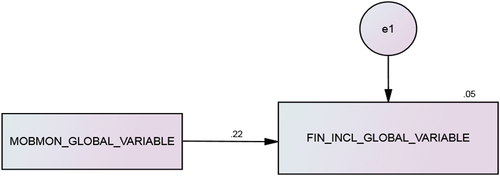

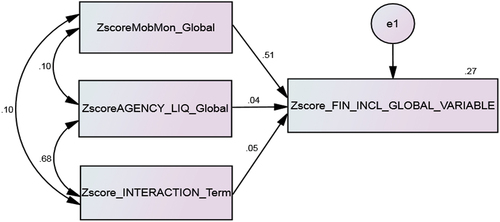

The results revealed that agent liquidity has a significant and positive interacting effect in the relationship between mobile money services and financial inclusion (β = 0.472, t = 2.755; p < 0.001). This supports hypothesis (H3) of this study, which states that agent liquidity significantly moderates the relationship between mobile money services and financial inclusion of the unbanked poor population in rural sub-Saharan Africa. Initially, mobile money services explained only 5% variation in financial inclusion before entering the interaction terms and agent liquidity into the structural equation model as shown in Figure . This implies that when the interaction term obtained as a product of mobile money services and agent liquidity is included into the structural equation model (mobile money services X agent liquidity), the impact of mobile money services on financial inclusion increases by 27 percentage points as indicated in Figure .

Figure 5. Non-moderated structural equation model without interaction term.

Figure 6. Moderated structural equation model with interaction term.

The moderated structural equation model also produced excellent model fit indices with Chi-square x2 of 3.112 and degrees of freedom of 6 with probability of 0.950; Incremental Fit index (IFI) of 1.000; Tucker Lewis index (TLI) of 1.056; Comparative Fit index (CFI) of 1.000; and Root Mean Square Error of Approximation (RMSEA) of 0.000, all above the recommended cut-off points as suggested by Hair et al. (Citation2014). The results for the test of moderation effect of agent liquidity in the relationship between mobile money services and financial inclusion are indicated in Table and Figure .

Table 4. Results of testing indirect and direct hypotheses

Furthermore, the interaction effect of agent liquidity in the relationship between mobile money services and financial inclusion was also plotted on a ModGraph based on the recommendation of Jose (Citation2013). The results indicated that the interaction effect of mobile money services was different at all level with low, medium, and high impact on financial inclusion through agent liquidity as a moderator. The gradients/slopes were different at all points in the interaction process as shown in Figure .

Figure 7. ModGraph for the interaction effect of agent liquidity.

4.6. Direct hypotheses

While the main purpose of this study is to test for the moderating effect of agent liquidity between mobile money services and financial inclusion, two other direct hypotheses derived under this study were also tested.

The results of the direct hypothesis test revealed that mobile money services has a significant impact on financial inclusion of the unbanked poor population in rural sub-Saharan Africa (β = 0.508, t = 3.181; p < 0.001). This implies that mobile money services increase access to and use of financial services through mobile phones. This result supports hypothesis (H1) derived under this study, which states that mobile money services has a significant impact on financial inclusion of the unbanked poor population in rural sub-Saharan Africa.

More so, the results also showed that agent liquidity has a significant impact on financial inclusion of the unbanked poor population in rural sub-Saharan Africa (β = 0.340, t = 2.689; p < 0.005). This means that availability of enough float at the mobile money agent point-of-sales can increase access to and use of financial services through mobile phones. This result supports hypothesis (H2) generated under this study, which states that agent liquidity has a significant impact on financial inclusion of the unbanked poor population in rural sub-Saharan Africa. The results of the direct hypotheses test are indicated in Table .

5. Discussion of findings

The main purpose of this study is to establish the moderating effect of agent liquidity in the relationship between mobile money services and financial inclusion of the unbanked poor population in rural sub-Saharan Africa.

5.1. Agent liquidity: moderator between mobile money services and financial inclusion

The results from this study showed that agent liquidity has a significant and positive interacting effect in the relationship between mobile money services and financial inclusion. This finding corroborates with the argument that availability of enough float helps mobile money agents to provide timely cash-in and cash-out services to more customers.

Mazambani et al. (Citation2018) observe that mobile money agents should have adequate flow of cash to meet withdrawal demands of customers while retaining sufficient electronic balances to facilitate conversions. Sufficient amounts of cash allow transactions to take place as and when customers want to cash-in or cash-out at the mobile money agents’ point-of-sale without any delay. Moreover, having enough liquidity helps the agent to execute more transactions and provide the services in a much reliable way. This results into easy access to and use of financial services.

Additionally, the GSMA (Citation2021) indicates that mobile money agents should have enough cash to achieve the main function of converting electronic money to cash. The mobile money transactions between a retail agent and a customer require that the retail agent has cash value in their mobile wallet to complete the mobile money transactions. As a result, more and more customers will cash-in and cash-out, which increases access to and use of financial services. This result supports hypothesis (H3) of this study.

5.2. Mobile money services and financial inclusion

The results from this study also indicated that mobile money services has a significant impact on financial inclusion of the unbanked poor population in rural sub-Saharan Africa. Indeed, Tengeh and Gahapa (Citation2020) observe that since most agents work for extended hours to meet the mobile money demands of different customers, they make financial services available at any time and in any place to the customers. This increases access to and use of financial services by the unbanked rural poor individuals.

Beck (Citation2020) also argues that while formal banks may require several documentations to open an account from the unbanked individuals, mobile money requires only the national identification card to open an account. This reduces barrier to access and ineligibility due to documentation requirements. Therefore, this can attract more unbanked rural poor individuals with national identification document to acquire mobile money account to access and use financial services.

Furthermore, Must and Ludewig (Citation2010) also state that mobile money can allow users to transact with safety and privacy because customers can only transact by entering a unique Personal Identification Number (PIN) to authenticate transactions over the mobile money platform. Thus, assurance of safety give customers confidence to continue using mobile money financial services, which results into increased use of digital financial services.

Similarly, Ndiwalana et al. (Citation2014) show that the unbanked rural poor individuals do not need a bank account to access mobile money services. The mobile money system requires the customers to get a mobile SIM card from a mobile network operator, which is registered with a mobile money account that can be instantly used to perform transactions. This can speed up access to and use of financial services by the poor.

Mararo and Ngahu (Citation2017) also observe that mobile money transactions can be performed by the unbanked rural poor individuals at an agent point-of-sale without making a trip to the bank branches or ATMs. This saves time and costs that is incurred by the unbanked rural poor individuals to travel to the bank to access financial services. This makes it more convenient and cheaper to access and use financial services through mobile money than other alternative sources such as banks, hence, increased financial inclusion.

Batista and Vicente (Citation2021) further suggest that mobile money offer faster transactions compared to the traditional banks that need more time to perform transactions. Storing, sending, and receiving money through mobile money is accomplished in a shorter time and at relatively low costs compared to costs and fees charged by banks. Consequently, this may attract more unbanked rural poor individuals to use mobile money, which results into increased access to and use of financial services. This result is in agreement with hypothesis (H1) of this study.

5.3. Agent liquidity and financial inclusion

The results from this study further revealed that there is a significant impact of agent liquidity on financial inclusion of the unbanked poor population in rural sub-Saharan Africa. According to Rothe (Citation2020), mobile money agents are a key component of the financial systems in developing countries, especially for lower income households and informal businesses in rural communities. They provide the essential function of converting electronic money to cash that involve digitizing informal cash payments and enabling crucial financial transactions such as money transfers and bill payments.

Rodriguez et al. (Citation2019) argue that maintaining higher float amounts to respond to high customer demand for cash-in and cash-out can result into increased access to and use of basic financial services over the mobile money platform that can increase financial inclusion.

Eijkman et al. (Citation2010) contend that availability of enough liquidity at the agent outlet helps the poor who operate in a cash economy, and whose income comes in the form of small lumps of cash, to consistently participate in the mobile money ecosystem by cashing-in and cashing-out easily.

Overall, the UNCDF (Citation2020) states that keeping enough float helps the mobile money agents to concentrate on improving their businesses, which makes them to grow and remain in operations. This may results into provision of better mobile money services to users, which can increase financial inclusion by bringing banking services closer to the unbanked rural poor population who live in rural communities. This result lends support to hypothesis (H2) of this study.

6. Conclusion

The conclusion from this study is centred on the study findings, research limitations and future studies, and implications.

6.1. Study findings

The main purpose of this study is to establish the moderating effect of agent liquidity in the relationship between mobile money services and financial inclusion of the unbanked poor population in rural sub-Saharan Africa.

The results from this study showed that agent liquidity has a significant and positive interacting effect in the relationship between mobile money services and financial inclusion. The availability of enough float helps to reduce the long hours spent on trips by agents to rebalance points. This can lead to timely provision of cash-in and cash-out services to more customers. As a result, more customers can access and use the payment, withdrawal, borrowing, and saving services offered through mobile money.

Besides, the results from this study indicated that mobile money services has a significant impact on financial inclusion of the unbanked poor population in rural sub-Saharan Africa. Mobile money through its wider agent networks can deliver the required level of proximity at low transaction costs, especially to geographically dispersed poor households who do not have access to formal financial services offered by banks. Mobile money can allow individuals at the bottom of the pyramid to deposit cash and make withdrawals at the retail agent point-of-sale. This allows them to quickly and cheaply perform transactions over a wider geographical coverage than banks.

Finally, the results from this study showed that there is a significant impact of agent liquidity on financial inclusion of the unbanked poor population in rural sub-Saharan Africa. This means that all agents of mobile money providers ought to have enough cash and electronic float to serve every customer transaction request at all times without being turned away. Indeed, the long-term health of mobile money ecosystem depends on agents and availability of floats to satisfy customers’ demand, especially in rural areas where there are no banking services.

6.2. Research limitations and future studies

Whereas the findings from this study revealed significant interaction effect of agent liquidity between mobile money services and digital financial inclusion, the data were collected from only the unbanked poor population in rural sub-Saharan Africa. Therefore, studies involving other users of mobile money could add more evidence on the role of mobile money agents in promoting financial inclusion.

The current study also collected data from only one rural region in Uganda as a country within sub-Saharan Africa. Future studies may collect data from more than one country in order to perform comparative analysis for generalization purpose.

Similarly, the current study investigated the liquidity of mobile money agents over a shorter period of time. Future studies may help to analyze whether liquidity of agents can remain a persistent challenge over a longer period of time.

Lastly, this study considered only mobile money financial services as an innovative digital channel for delivering financial services. Future studies may be conducted to investigate liquidity needs across other spectrum of FinTech.

6.3. Implications

The findings from this study can help mobile money regulators in low-and-middle income countries in sub-Saharan Africa to revisit and loosen requirements for registration and operation of mobile money agents. The initial capital and minimum float requirements should be revised downwards to enable many local “dukas” (small shops) to operate as agents to offer mobile money financial services, especially in rural villages not served by formal banks. This can increase the scope of financial inclusion in rural areas.

The findings from this study can also offer opportunity for bank linkages between the formal financial services’ providers and agent banks in the villages. The formal banks can operate through agent banks to deliver financial services to remote areas at reduced cost of operation. Extending financial services through retail agent banks and ATMs can help to solve the problem of high cost seen as a major bottle neck associated with delivering banking services to rural areas. As a result, this can increase access to and use of financial services by the unbanked rural poor population.

In addition, the findings from this study can also help mobile money agents to revise daily float levels and maintain sufficient liquidity. This can help them to consistently meet cash-in and cash-out needs of customers, thereby, increasing access to and use of financial services. Similarly, the findings from this study can be used by the mobile network operators (MNOs) to revise the minimum credit extended to mobile money agents. This can be achieved by determining daily float needs of customers within the mobile money ecosystem. Timely provision of enough floats to mobile money agents can help to meet cash withdrawal and deposit needs of customers, which can result into increased financial inclusion.

The findings from this study can also be used as a tool for controlling inflation within the economy by financial sector regulators in sub-Saharan Africa. The central bank can use mobile money agents to monitor liquidity within the mobile money ecosystem to prevent inflation. Consequently, the balance between money supply and demand can result into availability of enough money to increase financial inclusion.

Furthermore, the findings from this study can also help MNOs to invent the quickest means through which they can replenish agents’ cash needs. Since most agents complain about lack of cash due to MNOs delay in crediting their accounts, the use of zonal master agents to meet timely cash request can help to solve the problem of agents’ illiquidity, especially in remote villages. This can help them to meet timely cash needs of mobile money clients, hence, increased financial inclusion.

Additionally, the findings from this study can help mobile network operators to plan to extend float advances or credit and overdraft facilities to agents to maintain sufficient liquidity. The mobile money providers may partner with financial service aggregators to provide digital credit for float to agents at a lower rate of interest than they charge customers.

More so, the findings from this study can also help mobile network operators to reconsider the use of artificial intelligence (AI) through predictive data analytics that may improve liquidity management by providing efficient estimates of float inventory. The MNOs may use customer volume and value transaction data around agent locations to predict future demand for float. This can enable them to manage and control liquidity (electronic float and cash) at peak and off-peak times of the day, week, or month, which results into increased access to and use of financial services.

Further to the above, the findings from this study may help the mobile money stakeholders to create diversity within the mobile money services. The increase in mobile money service diversity will create more opportunities for retail agents to balance their cash holdings through disbursements and withdrawals. This will help them to manage liquidity in order to meet timely financial transaction needs of clients.

Besides, the findings from this study can be used by governments in sub-Saharan Africa for public remittances. The mobile money agents can be used by government to remit national payments such as pension and salaries. The agents can also adopt staggered payment strategy to manage government transfers, especially for payouts that tend to occur at almost the same time. This can promote financial inclusion of the needy population such as retirees who live in rural areas with limited banking facilities.

Finally, the findings from this study can help to promote cashless monetary system in sub-Saharan Africa. The presence of mobile money agents in every village in sub-Saharan Africa can promote use of electronic payments for essentials among the rural communities. This can reduce the risks associated with use of physical cash for transactions. This can ultimately promote digital financial inclusion.

Disclosure statement

No potential conflict of interest was reported by the authors.

Additional information

Notes on contributors

George Okello Candiya Bongomin

George Okello Candiya Bongomin holds a PhD in Finance, MSc (Accounting & Finance) and Bachelor’s degree in Commerce Accounting from Makerere University, Kampala, Uganda. He is a Research Fellow at the Faculty of Graduate Studies and Research, Makerere University Business School, Kampala, Uganda, and an international financial inclusion scholar. Currently, he is a Visiting Professor and Scholar at Laboratory for Financial Engineering at Laval University, State University of New York, and a member of Centre for Global Finance at SOAS University of London. He is a Principal Investigator on MUBS and Bank of Uganda Joint Research Collaboration on Digital Financial Services and Financial Inclusion in Uganda. His research interests are in financial inclusion, artificial intelligence/machine learning and financial services, digital financial services, microfinance, behavioural finance, banking and finance practice, institutional economics, financial consumer protection, and business psychology. George Okello Candiya Bongomin is the corresponding author and can be contacted at [email protected].

References

- Aiken, L. S., & West, S. G. (1991). Multiple Regression: Testing and Interpreting Interactions. Sage.

- Aker, J. C., Boumnijel, R., McClelland, A., & Tierney, N. (2016). Payment mechanisms and antipoverty programs: Evidence from a mobile money cash transfer experiment in Niger. Economic Development and Cultural Change, 65(1), 1–22. https://doi.org/10.1086/687578

- Amin, M. (2005). Social sciences research, Conception, methodology and analysis. Makerere University Printery.

- Argent, J., Hanson, J. A., & Gomez, M. P. (2013). The regulation of mobile money in Rwanda. International Growth Centre.

- Babbie, E., & Monton, J. (2002). The practice of social research. Oxford University Press.

- Bagozzi, R., & Yi, Y. (1988). On the evaluation of structural equation models. Journal of the Academy of Marketing Science, 16(1), 74–94. https://doi.org/10.1007/BF02723327

- Baron, R. M., & Kenny, D. A. (1986). The moderator-mediator variable distinction in social psychological research: Conceptual, strategic, and statistical considerations. Journal of Personality and Social Psychology, 51(6), 1173–1182. https://doi.org/10.1037/0022-3514.51.6.1173

- Batista, C., & Vicente, P. C. (2021). Improving Access to Savings through Mobile Money: Experimental Evidence from African Smallholder Farmers. Forthcoming at World Development.

- Beck, T. (2020). Fintech and Financial Inclusion: Opportunities and Pitfalls. Asian Development Bank Institute. https://www.adb.org/sites/default/files/publication/623276/adbi-wp1165.pdf (accessed 6 March).

- Bank of Uganda, (2021), Mobile Money Statistics: Data and Statistics - Department of Statistics, Bank of Uganda, Kampala, Uganda.

- Blumenstock, J. E., Callen, M., Ghani, T., & Koepke, L. (2015). Promises and Pitfalls of Mobile Money in Afghanistan: Evidence from a Randomized Control Trial. Proceedings of the Seventh International Conference on Information and Communication Technologies and Development. ACM. https://doi.org/10.1145/2737856.2738031.

- Burlando, A., Kuhn, M., & Prina, S. (2021). Too Fast, Too Furious? Digital Credit Delivery Speed and Repayment Rates. UC Berkeley CEGA Working Papers, University of California Berkeley.

- Creswell, J. W. (2014). Research Design: Qualitative, Quantitative, and Mixed Methods Approaches (4th ed.). SAGE Publications, Inc.

- Demirguc-Kunt, A., Klapper, L., Singer, D., & Ansar, S. (2018). The Global Findex Database 2017. Measuring Financial Inclusion and the Fintech Revolution. World Bank Group.

- Dermish, A., Kneiding, C., Leishman, P., & Mas, I. (2012). Branchless and Mobile Banking Solutions for the Poor: A Survey of the Literature. Innovations: Technology, Governance, Globalization, 6(4), 81–98. https://doi.org/10.1162/INOV_a_00103

- Dikit, S. V., Shringarpure, A. A., & Pathan, F. N. (2012). Strategies to Make Mobile Banking Popular in India. Advances in Management, 5(13), 6.

- Donovan, K. (2012). Mobile Money for Financial Inclusion. Information and Communications for Development, 61(1), 61–73.

- Eijkman, F., Kendall, J., & Mas, I. (2010). Bridges to Cash: The Retail End of M-Pesa. Savings and Development, 34(2), 219–252. 2010 2010.

- Field, A.P. (2009). Discovering Statistics using SPSS, 3rd Ed, Sage, London.

- GSAM. (2018). The future of mobile money agent distribution network. GSMA Publications.

- GSMA. (2019). The Mobile Economy: Sub-Saharan Africa. GSMA Publications.

- GSMA, (2020). The State of the Industry Report on Mobile Money 2020. GSMA Mobile Money programme, GSMA publication, Available at: http://www.gsma.com

- GSMA. (2021). State of the Industry Report on Mobile Money 2021. GSMA Publications.

- Hair, J. F. J., Hult, G. T. M., Ringle, C. M., & Sarstedt, M. (2014). A Primer on Partial Least Squares Structural Equation Modeling (PLS-SEM). Sage, London.

- Hair, J. F., Hult, G. T. M., Ringle, C. M., & Sarstedt, M. (2016). A Primer on Partial. Least Squares Structural Equation Modeling (PLS-SEM) (2nd Ed.). Sage, London.

- Hair, J. F., Sarstedt, M., Ringle, C. M., & Gudergan, S. P. (2018). Advanced issues in partial least squares structural equation modeling (PLS-SEM). Sage.

- Helix Institute of Digital Finance. (2017) “Fitting the Pieces of the Liquidity Management Puzzle”. Available at: https://goo.gl/o6q3xL

- Hidayati, S. (2011). Cash-in and Cash-out Agents for Mobile Money in Indonesia. Innovations: Technology, Governance, Globalization, 6(4), 117–123. https://doi.org/10.1162/INOV_a_00106

- Jack, W., & Suri, T. (2011). Mobile money: The economics of M-PESA. National Bureau of Economic Research.

- Jack, W., & Suri, T. (2014). Risk sharing and transaction costs: Evidence from Kenya’s mobile money revolution. The American Economic Review, 104(1), 183–223. https://doi.org/10.1257/aer.104.1.183

- Jose, E. P. (2013). Welcome to the Moderation/Mediation Help Centre. School of Psychology Victoria University of Wellington. On-line Version: 3.0.

- Kim, K. (2022). Assessing the impact of mobile money on improving the financial inclusion of Nairobi women. Journal of Gender Studies, 31(3), 306–322.

- Kirton, J. (2020). Addressing Agent Liquidity Needs with Hapa Cash by Kuunda Digital. FINCA Forward Case Study. USAID.GOV and FINCA.

- Kirton, J. (2020). From Response to Recovery: How the COVID-19 Crisis Will Accelerate Digitization in Microfinance. FINCA Ventures. https://fincaventures.com/from-response-to-recovery-how-the-covid-19-crisis-will-accelerate-digitization-in-microfinance/ (accessed 3 March).

- Krejcie, R. V., & Morgan, D. W. (1970). Determining Sample Size for Research Activities. Educational and Psychological Measurement, Sage Publications.

- Lehmann-Uschner, K., & Menkhoff, L. (2020). Mobile money is driving financial development in Africa, DIW Weekly Report, ISSN 2568-7697, Deutsches Institut für Wirtschaftsforschung (DIW). (Vol. 10). Iss. 21/22. https://doi.org/10.18723/diw_dwr:2020-21-1

- Mararo, M. W., & Ngahu, S. (2017). Influence of Mobile money services on the growth of SME in Nakuru town, Kenya. IOSR Journal of Humanities Social Science, 22(10), 64–72.

- Mazambani, L., Rushwaya, T. J., & Mutambara, E. (2018). Financial inclusion: Disrupted liquidity and redundancy of mobile money agents in Zimbabwe. Investment Management and Financial Innovations, 15(3), 131–142. https://doi.org/10.21511/imfi.15(3).2018.11

- Morawczynski, O. (2009). Exploring the Usage and Impact of “Transformational” Mo- bile Financial Services: The Case of M-PESA in Kenya. Journal of Eastern African Studies, 3(3), 509–525.

- Must, B., & Ludewig, K. (2010). Mobile Money: cell phone banking in developing countries. Policy Matter of Journal, 7(2), 27–33.

- Naito, H., Ismailov, A., & Kimaro, A. B. (2021). The effect of mobile money on borrowing and saving: Evidence from Tanzania. World Development Perspectives, 23, 100342. https://doi.org/10.1016/j.wdp.2021.100342

- Ndiwalana, A., Morawczynski, O., & Popov, O. (2014). Mobile money use in Uganda: A preliminary study.Paper Presented at the 15th International Conference on Human Computer Interaction: Users and Contexts of Use - Volume Part III, Las Vegas, NV, July 21-26.

- Neuman, L. (2006). Social Research Methods: Qualitative and quantitative approaches (6th ed.). Pearson International.

- Nunnally, J. C., & Bernstein, I. H. (1994). Psychometric Theory (3rd edn ed.). Mcgraw-Hill.

- Okello Candiya Bongomin, G., & Ntayi, J. M. (2020). Mobile money adoption and usage and financial inclusion: Mediating effect of digital consumer protection. Digital Policy, Regulation and Governance, 22(3), 157– 176. https://doi.org/10.1108/DPRG-01-2019-0005.

- Okello Candiya Bongomin, G., Ntayi, J.M., Munene, J.C. & Akol, M.C. (2018). “Mobile money and financial inclusion in Sub-Saharan Africa: the moderating role of social networks”, Journal of African Business, 19(3),361–384. Doi: 10.1080/15228916.2017.1416214.

- Okello Candiya Bongomin, G., Yourougou, G., Yosa, P., Amani, F., & Ntayi, J. M. (2021). Psychoanalysis of the mobile money ecosystem in the digital age: Generational cohort and technology generation theoretical approach. Development in Practice. https://doi.org/10.1080/09614524.2021.1937539.

- Okello Candiya Bongomin, G., & Munene, J. C. (2021). Analyzing the Relationship between Mobile Money Adoption and Usage and Financial Inclusion of MSMEs in Developing Countries: Mediating Role of Cultural Norms in Uganda. Journal of African Business, 22(1), 1–20. https://Econpapers.Repec.org/Article/Tafwjabxx/

- Omigie, N. O., Zo, H., Rho, J. J., & Ciganek, A. P. (2017). Customer Preadoption Choice Behavior for M-PESAMobile Financial Services: Extending the Theory of Consumption Values. Industrial Management and Data Systems, 117(5), 910–926. https://doi.org/10.1108/IMDS-06-2016-0228

- Ozili, P. K. (2021). Financial inclusion research around the world: A review. Forum for Social Economics, 50(4), 457–479. https://doi.org/10.1080/07360932.2020.1715238

- Podsakoff, P. M., MacKenzie, S. B., Lee, J. Y., & Podsakoff, N. P. (2003). Common method biases in behavioral research: A critical review of the literature and recommended remedies. The Journal of Applied Psychology, 88(5), 879–903. https://doi.org/10.1037/0021-9010.88.5.879

- Podsakoff, P. M., MacKenzie, S. B., Paine, J. B., & Bachrach, D. G. (2000). Organizational citizenship behavior: A critical review of the theoretical and empirical literature and suggestions for future research. Journal of Management, 26(3), 513–563. https://doi.org/10.1177/014920630002600307

- Robinson, J., Park, D. S., & Blumenstock, J. E. (2022). The impact of digital credit in developing economies: A review of recent evidence.

- Rodriguez, C., Conrad, J., Davico, G., Lonie, S., & Denyes, L. (2019). A New Banking Model for Africa: Lessons on digitization from four years of operations. International Finance Corporation and the World Bank.

- Rothe, M. (2020). Instant Liquidity Support for Mobile Money Agents. Flow Uganda, FinDev Blog. CGAP.

- Schreiber, J. B., Nora, A., Stage, F. K., Barlow, E. A., & King, J. (2006). Reporting structural equation modeling and confirmatory factor analysis results: A review. The Journal of Educational Research, 99(6), 323–337. https://doi.org/10.3200/JOER.99.6.323-338

- Sekaran, U. (2003). Research methods for business: A skill building approach. John Wiley & Sons, Inc.

- Spector, P. E. (2006). Method Variance in Organizational Research: Truth or Urban Legend? Organizational Research Methods, 9(2), 221–232. https://doi.org/10.1177/1094428105284955

- Ssonko, G. W. (2020). Mobile Money Architecture and the Safety of Digital Financial Services in Uganda: A Practitioner’s Reflection. Working Paper No. 30/202, Bank of Uganda Working Paper Series, September 2020.

- Stuart, G., & Cohen, M. (2011). Cash-In, Cash-Out: The Role of M-PESA in the Lives of Low-Income People. Financial Services Assessment.

- Suri, T. (2017). Mobile money. Annual Review of Economics, 9(1), 497–520. https://doi.org/10.1146/annurev-economics-063016-103638

- Suri, T., Aker, J., Batista, C., Callen, M., Ghani, T., Jack, W., Klapper, L., Riley, E., Schaner, S., & Sukhtankar, S. (2021). Mobile Money. VoxDevlit. 2(1), pp 1–28. February 2021.

- Suri, T., & Jack, W. (2016). The long-run poverty and gender impacts of mobile money. Science, 354(6317), 1288–1292. https://doi.org/10.1126/science.aah5309

- Tengeh, R. K., & Gahapa, F. S. T. (2020). Mobile Money as a Sustainable Alternative for SMEs in Less Developed Financial Markets. Journal of Open Innovation, Technology, Market, and Complexity, 6, 163. https://doi.org/10.3390/joitmc6040163

- Tourangeau, R., Rips, L. J., & Rasinski, K. (2000). The psychology of survey response.Cambridge. Cambridge University Press.

- United Nations Capital Development Fund-UNCDF. (2020). ‘Agent Cash’ addresses agent liquidity to expand financial inclusion in Zambia. Policy Brief, UNCDF.

- Venkatesh, V., Morris, M. G., Davis, G. B., & Davis, F. D. (2003). User Acceptance of Information Technology: Towards a Unified View. MIS Quarterly, 27(3), 425–478. 2003. https://doi.org/10.2307/30036540

- Vutsengwa, R. M., & Ngugi, K. (2013). An assessment of the challenges facing commercial banks in sustainability of agency banking in Kenya: A case of commercial banks. International Journal of Economics and Finance, 1(2), 1–8.

- World Bank, (2020). Fintech Market Reports Rapid Growth During COVID-19 Pandemic. https://www.worldbank.org/en/news/press-release/2020/12/03/fintech-market-reports-rapid-growth-during-covid-19-pandemic (accessed 2 March).

- Wright, G. (2015b). Solving Customer Service Issues in Digital Finance – Can Do, Must Do. MicroSave Blog Series. Available at: https://www.microsave.net/2015/06/26/solving-customer-service-issues-in-digital-finance-can-do-must-do

- Yin, R. K. (2003). Case study research: Design and methods (3rd ed.). W.G. (2003). Business Research methods. 7th Edition. Ohio: South western. Sage.Zikmund.