?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

Lack of investable capital has slowed down the development process in many developing nations, including Nigeria, and this has sparked empirical research on the factors affecting foreign capital flow. Therefore, the purpose of this study was to investigate the effects of interest rate differential, exchange rate changes, and political stability on the entrance of foreign capital into Nigeria between 1981 and 2021. To investigate the impact of the factors on foreign capital inflow in regimes with low and high interest rate differentials, the study used a discrete threshold regression model (DTRM). The study discovered an interest rate differential threshold value of 3.68 percent, indicating that an interest rate differential high and over the predefined threshold promotes a favorable and considerable inflow of foreign capital into the nation. Additionally, the country’s capital inflow is influenced by political stability and exchange rate fluctuations. The implication is that investors evaluate a country’s IRD in relation to other risk factors (political and macroeconomic) and will only invest if the IRD is higher than3.68 percent since it will balance out other opportunity costs at home and risk factors in the receiving country’s economy.

1. Introduction

Many economists and researchers have tried over the years to figure out what factors impact foreign capital flows in a country. This is due to the critical role capital inflows play in economies, not just in developing and emerging economies, but also in industrialized economies. Foreign capital flow can help a country close the savings–investment gap, attract innovative technologies, generate more foreign currency, and boost economic growth and development (UNCTAD, Citation2017). According to UNCTAD (Citation2018), the improved performance of most regions of the world in 2017 was related to an increase in foreign inflows, which enhanced GDP acceleration, stock market fundamentals, and global trade recovery, among other things. Foreign capital inflows are critical for growth and development in emerging countries, because sustained industrial development is impossible without foreign investment (UNCTAD, Citation2018).

There exist two popular theoretical accounts of cross-border capital flows. The two ideas are the Resource Gap Theory (RGT) and the Interest Rate Parity Theory (IRPT). The RGT contends that nations with open economies finance their differences in revenue and spending through external borrowing or loan, while the IRPT posits that interest rate differentials and forward premium spot exchange rates are not equal, which explains capital mobility (Adewuyi & Ogbode, Citation2019; Chenery & Stout, Citation1966; Karimo, Citation2020; Keynes, Citation1923; Thirlwall, Citation1976). Interest rate differentials encourage arbitrage, which encourages people to borrow money from a low-interest country and invest it in a high-interest country so as to make profit from the interest differential. Exchange rates enter the profitability equation of this type of arbitrage operation because several currencies are involved. What counts more specifically is the anticipated exchange rate change throughout the relevant investment horizon.

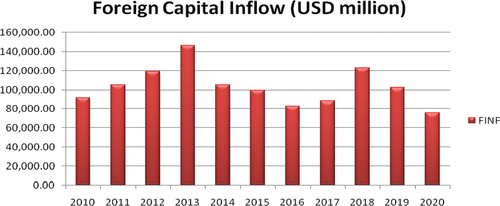

Consequent upon large disparity between the required capital and its availability to stimulate economic growth and development, most emerging countries suffer from insufficient investible capital. Consequently, foreign capital inflows become a valuable tool for closing the deficit (Sy & Rakotondrazaka, Citation2015; UNCTDA, Citation2015, Citation2018). Nigeria is not immune to this problem; as Olowookere et al. (Citation2020) pointed out, one of the major issues the country faces is inadequate investible capital, which has hampered the country’s development. According to data from the Central Bank of Nigeria’s statistical bulletin (Citation2020), the country’s foreign capital inflow has been declining since 2014, reaching an all-time low of 10 years in 2020 (see Figure ).

Figure 1. Trend analysis of foreign capital inflow between 2010 and 2020 in million of US Dollars.

Foreign inflows surged from USD91,132.6 million in 2012 to an all-time high of USD146,274.2 million in 2013, before dropping 28.2 percent to USD105,087.9 million in 2014. It continued to decline, falling to USD82,748.49 million in 2016, before rising to a 6-year high of USD122,964.3 million in 2018. In 2020, the country saw an all-time low in foreign inflows of USD75,593.5 million. This perspective needs an empirical investigation of how interest rate differentials, currency movement, and political stability affect a country’s fall in capital inflows. In principle, factors such as investment opportunities, high rates of return on investment, political and macroeconomic stability (Qadri et al., Citation2020; Bitar, Hamadeh and Khoueiri, Citation2019), and others are hypothesized to be key determinants of cross-border capital flows (Chenery & Stout, Citation1966; Keynes, Citation1923; Olowookere et al., Citation2020; Thirlwall, Citation1976). Hypothetically, political stability and capital movement are connected, as investors want to invest in countries with a relative stability in political system. Political instability creates fears of loss amongst investors (Shahzad & Qin, Citation2019; Qadri et al., Citation2020; Bitar, Hamadeh and Khoueiri, 2020). The Nigerian political system has been characterized by armed conflict, inter-ethnic crisis, political and civil strife, including assassinations and riots especially in the Northern and South Eastern parts of the country in recent years and more prominently during election time (ACLED, Citation2021). According to ACLED report, in 2021, the country recorded about 22 percent rise in political violence. These factors can reduce the investors’ confidence and hence affect capital inflow. This period of high incidence of political instability coincides with massive drop in capital inflow and economic recession in the country.

Various explorations on the factors that drive international capital inflow in emerging and developed economies have been done; however, few studies investigated how interest rate differences and money instability mean for international capital inflow in Nigeria (Aisien, Citation2018; Enisan, Citation2017; Karimo, Citation2020; Nwokoye & Oniore, Citation2017; Wang et al., Citation2019). Except for Karimo (Citation2020), who investigated the effect of interest rate differentials and exchange rate movements on capital flow, Nwokoye and Oniore (Citation2017) focused on homegrown factors influencing foreign capital flow. While homegrown factors such as financial and political dependability have been displayed to impact capital streams, worldwide factors, for example, interest rate differences, changes in global market regulation, etc., additionally impact international capital flow (Hannan, Citation2018). This involves considering external factors such as foreign interest rate relative to local rate, as well as policy changes (structural break) on both the homegrown and worldwide business sectors.

Furthermore, interest rate plays dual purposes in a given economy as it serves as cost of borrowing to borrowers and, on the other hand, as yield from investment. A high local interest rate may deter domestic investment as cost of borrowed funds becomes high; on the other hand, it may attract foreign investors to move capital from a low interest rate economy to the country with high interest rate. This capital movement presumes that other political and macroeconomic factors are the same across countries. However, in reality, political and macroeconomic stability differ across countries, which serve as a risk factor towards capital inflow (Luangaram & Sethapramote, Citation2020; Bitar, et al 2020; Shahzad & Qin, Citation2019). Investors therefore juxtapose the least risk factors with maximum interest rate differentials in foreign land vis-à-vis the domestic economy in arriving at where to invest (Hannan, Citation2018). This requires knowledge of marginal interest rate differential enough to compensate for the risk factor in foreign land relative to domestic economy. This gives credence to the need for the estimation of threshold value of interest rate differential upon which a foreign investor is willing to accept and invest in an economy. Empirically, there is no known previous study on the threshold of interest rate differential upon which an investor will risk other factors so as to invest in another country.

This work, therefore, differs from past studies in Nigeria in three ways: first, it employs discrete threshold regression model (DTRM) to estimate a threshold value for interest rate differential and examine the effects on the explanatory variables across two regimes (low and high interest rate differential); second, it lays out the significance of political stability in capital flows; and third, it utilizes structural breaks in the unit root testing to represent changes in homegrown and global guidelines. Threshold regression model has been widely used in studies on exchange rate markets (Odionye & Chukwu, Citation2021) and energy and environmental (Khaskheli et al., Citation2021; Ullah et al., Citation2021) researches in recent years due to its numerous advantages. Some of the advantages of threshold regression model are as follows: (i) it estimates a threshold value that separates the explanatory variable(s) into different regimes, (ii) as a regime switching model, it enables the study of influence of variables at different regimes, (iii) it provides robust results in the presence of structural breaks, etc. (Hansen, Citation1999, Citation2011; Odionye & Chukwu, Citation2021 Ullah, Ahmed, Raza, Ali. Ullah et al., Citation2021).

Against this backdrop, this study investigates the impact of interest rate differentials, exchange rate changes, and political stability on Nigeria’s foreign capital inflows, using discrete threshold regression model (DTRM) in its analysis as well as testing the existence of structural break in the model series, cognizance upon economic and policy changes in Nigeria. This study is divided into five sections. Following the introduction is the review of related literature in Section 2. Section 3 discusses the method of analysis and data issues while Section 4 analytically presents the empirical results. Section 5 concludes and makes policy implications based on empirical findings.

2. Literature review

David Humes and David Richardo made the interest rate differential (IRP) idea, which was subsequently classified by John Maynard Keynes in Citation1923 as the hypothesis of interest rate. This hypothesis portrays the connection between the spot conversion scale and the normal spot swapping scale of two monetary forms when interest rate is evolving. As per the hypothesis, the anticipated swapping scale ought to rise to the spot money conversion standard duplicated by the local interest rate, and afterward isolated by the international interest rate. This thought expounded on the association in two ways: covered and unconvered interest rate parity.

2.1. Covered interest rate parity and uncovered interest rate parity

The financing cost equalities for uncovered and covered obligation are generally comparable. The qualification is that covered financing cost equality alludes to a state where no-exchange necessities are accomplished using a forward agreement. Financial backers would be freethinker in the covered IRP regarding whether to put resources into their nation of origin’s loan fee or the outside nation’s loan fee, as the forward conversion scale keeps up with money balance. This is an idea that is integrated into the forward swapping scale.

The revealed IRP indicates the state wherein no-exchange is fulfilled without a trace of a forward agreement. In the uncovered IRP, the anticipated conversion scale is changed so that the IRP stays stable. This thought is a part of deciding the anticipated spot conversion scale.

The Covered Interest Rate Parity (CIRP) is given as

where Ft and St are the forward rate and spot rate, respectively, at time t of naira vis-à-vis US dollar, rd is the domestic interest rate and rf is the foreign interest rate, t is the time to expiration date.

The Uncovered Interest Rate Parity (UIRP) is given as

where Et is the expected spot rate at time t in Nigerian currency vis-à-vis US dollar while others are as defined above.

Expressing equation 2.2 in terms of domestic rate as

Equation 2.3 shows the way that a Nigerian financial backer can procure (1 + r) in year t by putting a similar measure of cash in the nation or by putting a similar measure of cash in a far-off country (e.g. United States of America). The differential among neighborhood and unfamiliar loan fees demonstrates the heading of venture allure.

To put it plainly, IRP contends that the contrast between nations’ loan costs approaches the distinction between their forward and recognize trade rates. It further explains the connection between financing costs, spot rates, and forward rates, inferring that there will be no opportunities for loan fee exchange, as the distinction in return rates will be reflected as either forward premium or forward rebate.

2.2. Portfolio Theory (PT)

The Portfolio Theory as developed by Branson (Citation1986) decomposed types of capital flow into short-term flow and long-term flow. The theory posits short-term capital flow to be influenced by international trades (import and export), interest rate and exchange rate, whereas factors that determined long-term capital flow include national interest rate, international interest rate, risk and stock of wealth. That is: FCF = f (r—r*, E, W) where FCF is the foreign capital flow, f represents the functional form, r—r* = interest rate differentials, r is the national interest rate and r* is the international interest rate, E = the risk component and W is wealth.

In accordance with Aisien (Citation2018) and Karimo (Citation2020), this work utilizes Branson’s (Citation1986) Portfolio Theory (PT) and Keynes’ (Keynes, Citation1923) Interest Rate Parity Theory (IRPT) with minor changes as its hypothetical system for making sense of the effect of interest rate differentials, exchange rate changes, and political stability on foreign capital inflow in Nigeria.

3. Empirical literature

Numerous researches on the factors driving foreign capital flow exist in a variety of developing and emerging countries, but there are just handfuls in Nigeria. Except for Karimo (Citation2020) who considered interest rate differential and exchange rate changes in Nigeria, majority of the studies either focused on determinants of foreign direct investment or the influence of the exchange rate.

Jabbor and Awan (Citation2014) evaluated the factors of capital influx in a sample of developing nations, with a particular emphasis on Pakistan. The study’s focus variable was internal factors, which included the current account, foreign reserve, and domestic interest rate, and the study’s analytical technique was panel data. The study’s findings indicate, among other things, that foreign reserves and current account balances are significant determinants of capital inflows in the studied nations. In a related study, Liyanage (Citation2014) examined the factors that influence capital influx in Sri Lanka between 2001 and 2015. They used quarterly data from 2001 to 2015. The study examined both aggregated and disaggregated foreign capital flows and analysed the data using VECM. The model incorporated both internal and external factors, and its findings indicated that real national income, interest rates, and political stability are the primary determinants of capital flow in the country.

Bogdan (Citation2016) used regression analysis to examine the impact of push and pull factors in Ukraine from 2004:Q1 to 2014:Q4. He discovered that foreign bond spreads are driven by push factors and rises in commodity prices, and that increases in commodity prices draw money to Ukraine. This corroborates the findings of Culha (Citation2006), who examined post-crisis Turkey from 1992 to 2015 using a structural VAR approach within the Pull-Push factor framework and discovered that the relative importance of certain factors changed over time and that pull factors dominate the determinants of capital flows in Turkey.

Makhetha-Kosi et al. (Citation2016) explored how international capital flows respond to interest rate differentials in South Africa from 1990 to 2013. The study examined the impulse response of capital flow to interest rate differentials using VECM analysis. It concluded in its research that, while the country has a positive interest rate difference, it does not necessarily result in an increase in capital inflow. Additionally, the study discovered that various components of capital flow behave differently in response to interest rate differentials. Grzegorz et al. (Citation2017) concluded that equity investment is a more preferable type of foreign capital flow than loan inflows, which are more responsive to global conditions and hence more volatile. Grzegorz et al. (Citation2017) discovered that the impact of macroeconomic and portfolio-related variables on capital flows varies according to the type of capital inflow and the group of countries involved, which is in corroboration with Forster et al. (Citation2012)‘s findings that global and country-specific factors are significant for countries with more developed financial systems and that a fixed exchange rate regime has no effect on global capital flow dynamics.

While Su and Zhang (Citation2010), Ning and Zhang (Citation2018), and Wang et al. (Citation2019) found evidence that interest rates have an effect on foreign capital movement, Cheung et al. (Citation2016) suggest that the contrary is true. Su and Zhang (Citation2010), for example, employed the quadruplex arbitrage model to investigate the impact of China–US interest and tax differentials on China’s short-term capital flow from 2002 to 2009. According to them, interest rate arbitrage and taxation enhance short-term capital inflows. Ning and Zhang (Citation2018) used the Markov switching time varying transition probability (MS-TVTP) model with monthly data from 2000 to 2015 to examine the dynamics of China’s short-term debt. The procedures used in Ning and Zhang’s (Citation2018) investigation are comparable to those used in Karimo’s (Citation2020) study in Nigeria. Hannan conducted a survey-based investigation in 2018 to determine the reasons of capital flows in emerging economies. The study analyses both push and pull factors and concludes that, while both international and domestic factors influence foreign flows, the determinants vary over time and are dependent on the type of capital movement.

In the study of political instability–capital flow connectivity, Qadri et al. (Citation2020) employed ARDL model for the case of Pakistan between 1976 and 2016. The study discovered empirically that political instability severely affects capital inflow inversely. In a related study, Bitar et al. (Citation2019) investigated how political instability affects FDI in Lebanon utilizing a static model in its data analysis. The study concluded that a strong nexus exists between political instability and capital inflow. Luangaram and Sethapramote (Citation2020) investigated the reaction of capital movement to political conflict in Thailand using quantile regression framework between 1997 and 2017. The study used a disaggregated foreign capital inflow and vector of political conflict. The study’s result indicates that political instability relates in opposite direction with the disaggregated foreign inflow in the investigated country.

In Nigeria, the few related researches are those by Nwosa and Adeleke (Citation2017), Aisien (Citation2018), and Karimo (Citation2020). Nwosa and Adeleke (Citation2017) used the EGARCH model to examine the factors that contribute to the volatility of foreign direct investment (FDI) and foreign portfolio investment (FPI) in Nigeria from 1986 to 2016. Their analysis concentrated on one aspect of foreign exchange flows: private investment. Their study examined local interest rates, stock values, trade openness, and global economic revenue. They discovered that the domestic interest rate, trade openness, and stock valuation are the primary drivers of private investment. The study made no mention of interest rate differentials between two trade countries.

Aisien (Citation2018) examined the influence of exchange rate fluctuations on private investment inflows into the country between 2007 and 2017. Using quarterly data, the study examined the private component of capital inflows and how it is influenced by exchange rate movements. The study used a VAR model to determine how a disaggregated private investment inflow responds to exchange rate changes. While the study emphasises on the relationship between interest rate differentials and private inflows, it used the domestic interest rate as a control variable due to a lack of foreign interest rate data. The study discovered that depreciation of the exchange rate is a negative function of private flow.

Karimo (Citation2020) conducted the most current study in Nigeria, examining how interest rate differentials and currency rate changes affect the country’s foreign private capital flow. The study’s paradigm was interest rate parity theory, and its estimating technique was the Markov switching time varying model. The study concentrated on the private foreign capital component, with interest rate difference and exchange rate as model variables. The analysis discovered that there is no statistically significant association between interest rate differentials and foreign currency direction. However, the analysis discovered evidence of a considerable effect of interest rate differentials on international portfolio investment. Although the Markov switching model is a structural break model, the study’s pre-estimation tests, such as the unit root test and cointegration test with structural break, did not account for structural break.

4. Data sources and method of data analysis

The data on domestic interest rate, exchange rate and foreign capital flow were sourced from statistical bulletin (Citation2021), while data on United State interest rate that was used as proxy for foreign interest rate was sourced from World Bank Development Indicator (Citation2021), and Polity IV data from World Bank was used as a proxy for political stability. The study adopted Discrete Threshold Regression (DTR) model in its analysis. In order to avoid the problem of structural break in unit root, the study utilized the Zivot-Andrews (Citation1992), unit root test with structural break to examine the time series features of the model variables. The choice of DTRM is predicated on its advantages (Hansen, Citation1999, Citation2011; Odionye & Chukwu, Citation2021; Ullah et al., Citation2021) over other models (e.g. ARDL and OLS) used in the previous studies as well as the fact that exchange rate regime, interest rate, and political system in Nigeria have passed through different policy changes and/or reforms since the 1980s (CBN, Citation2021) and hence different regimes.

4.1. The model

The theoretical framework upon which this work is based on is the Interest Rate Parity Theory (IRPT) and Portfolio Theory (PT) with minor modifications to account for the effect of interest rate differentials, exchange rate movements and political stability on foreign capital inflow in Nigeria (Branson, Citation1986; Keynes, Citation1923). In view of the above, the functional form is stated as

where LFCI = natural log of total foreign capital inflow was employed in the study, IRD = interest rate differential which is given as the difference between domestic interest rate and US interest rate as a proxy for foreign interest rate, LERA = natural log of exchange rate and LPOS = natural log of political stability, which we used polity 2 as a proxy for political stability. Note that interest rate differential (IRD) was used in its original form because most of the series contains negative values. Taking natural log of a negative value will generate missing number (zero); we considered the fact that interest rate differential is in percentage.

To estimate the above equation, we transformed the functional form into an estimated model as

Further, the work set out to present a Discrete Threshold Regression (DTR) model (Hansen (Citation1999)) to explain a non-linear regression of the impact of interest rate differential, exchange rate movement and political stability on foreign capital inflow in Nigeria. The DTR model in its general form is given as

where the Xs are the independent variables that do not vary across regimes where Zt represents the regime variable and Yt is the endogenous variable.

Following equation 3.3, we specify the DTR model as

where the last component of equation 3.4 is the non-linear component while the other components represent the linear part and the variables are as defined above; q is the identity threshold parameter, IRD is the threshold variable and γ is the threshold value.

4.1.1. Unit root test

The legitimacy of time series is dependent upon the order of integration of the model variables. Given the successive changes in macroeconomic strategy and governmental issues at the public and worldwide levels, the Zivot-Andrews unit root test with strategy change is utilized.

Unit Root Test Zivot-Andrews:

where = 1, if t > T

, 0 otherwise;

= t—T

, 0 otherwise. Z is the variable. The null hypothesis of the Z-A unit root test is that the variable has a unit root with a structural break in either the intercept or the trend, or both. If the estimated t statistics are greater than the crucial value, the null hypothesis is rejected.

5. Empirical result and discussion of findings

5.1. Descriptive statistics

Typically, every empirical exposition begins with some preliminary descriptive statistics that largely pave the way for more robust estimates. This test enables the examination of the series’ behavioural pattern as well as the shape of the distributions. The descriptive statistics was conducted on the original form of the series to ensure their true values. In specific terms, the descriptive statistics avails information that underscores whether the series is normally distributed and this is summarized in Table .

Table 1. Descriptive outcomes

The outcomes from Table demonstrate that the series deviates from normal distribution on the basis that the Jarque-Bera statistics is significant. Notably, these outcomes justify the choice and applications of nonlinear model (Ullah et al., Citation2021, Citation2022). The Kurtosis indicates normal peak for exchange rate (ERA) while the other variables indicate abnormal peak. It further indicates that foreign capital inflow (FCI), interest rate differential (IRD) and political stability (POS) skewed to the left while exchange rate positively skewed. Within the period of study, the minimum values for exchange rate, foreign inflow, interest rate differentials and political stability are 0.61, −5701752, −74.45 and −7.0, respectively, while their corresponding maximum values are 387.65, 1932253, 15.71 and 7.0, respectively.

5.2. Unit root test

The stationarity features of the series were examined to ascertain the series of order of integration. The study adopted the conventional ADF test of stationarity and Zivot-Andrews (Z-A) unit root test with structural break in order to address the presence of a breakpoint in the series. Both the ADF and the Z-A unit root tests estimate that the series has a unit root (non-stationary) rather than the other option, which is that the variable does not have a unit root (stationary). The best lag length was selected using Akaike and Schwartz-Bayesian information criteria. The choice rule is to reject the null hypothesis of unit root if both the ADF and Z-A tests statistics exceed its critical value in absolute term at 5% significant level. Table sums up these discoveries.

Table 2. Unit roots test result

The ADF statistics that the series ERA and FCI were not stationary in level form, however, became stationary after first difference, whereas POS was not stationary in level and at first difference but only became stationary after second difference, implying that it is integrated of order two (I (2)). In the case of IRD, it was stationary in the level form. The Z-A unit root test indicates varying order of order zero (IRD and POS) and order one (ERA and FCI). The choice was based on the fact that ADF and Z-A statistics were significant at 5% level. This result upholds the view that unit root results are sensitive to structural break, as failure to account for structural break can lead to misleading inference (Perron, Citation1989; Odionye & Chukwu, Citation2021). Given that the variables are integrated of different order (of order 2), the cointegration test cannot be carried out. The condition for testing cointegration (ARDL bound, dyn-ARDL bound, NARDL bound) is not satisfied (Li & Guo, Citation2022; Pesaran et al., Citation2001; Sarkodie & Owusu, Citation2020; Shin et al., Citation2014). However, other results are carried out based on their order of integration.

5.3. Thresholds specification

In order to determine the number of thresholds in the model, threshold specification was carried out in line with Hansen (Citation1999, Citation2011) and the summary of the threshold behaviour test result is presented Table .

The outcome of threshold specification test in Table demonstrates that, out of maximum thresholds of 5, one threshold coefficient was selected based on the least sum of square residual. According to Hansen (Citation1999; Citation2011), m-threshold value produces m + 1 regimes. The empirical outcome indicates one threshold with two regimes corresponding to high and low interest rate differentials (IRD regimes. The threshold value is 3.68297 while the adjacent value is 3.2118, which means that threshold values of IRD between 3.21 and 3.68 have similar influence on capital flow in the investigated country (Hansen, Citation1999).

Table 3. Discrete threshold specification test

5.4. Bai-Perron multiple threshold test

In confirmation with the appropriate number of thresholds, Bai-Perron multiple thresholds test was carried out to ascertain the threshold behaviour of the model series. The null hypothesis of the test is that there is L number of threshold as against L + 1 number of thresholds (Hansen, Citation1999). The result is summarized in Table .

Table 4. Bai-Perron Multiple Thresholds Test

5.5. Bai-Perron multiple thresholds test

Table indicates the confirmation of one threshold as the null hypothesis of zero threshold versus one threshold was rejected. Thus, single threshold exists in the model and hence both the sequential and the repartition threshold values are the same.

5.6. Discrete Threshold Regression (DTR) result

The summary of DTR result of the impact of interest rate differentials, exchange rate and political stability on foreign capital inflow in Nigeria is presented in Table .

Table 5. Summary of discrete threshold regression result

The result from the discrete threshold regression (DTR) model, as summarized in Table , is divided into three parts. The first part shows the low interest rate differential (IRD) regime with a threshold value of 3.68, which shows that interest rate differential high and above 3.68% will impact foreign capital inflow into the country positively and significantly. The outcome indicates 22 observations in the low IRD regime and 19 observations in the high IRD regime. What this means is that out of the 41 observations, more than half of the study period (54%) falls withing the low regime (IRD <3.68) while about 46% observations are within the high IRD regime (IRD >3.68). In the low IRD regime, interest rate differential has positive but insignificant impact on foreign inflow, which suggests that a low interest rate differential era will attract infinitesimal flow of capital and hence the insignificant impact. This is because investors compare the IRD with other drivers (political and macroeconomic variables) of foreign inflow in the recipient country vis-à-vis opportunity cost in the local economy. The coefficient of exchange rate (LERA) in the low IRD period is negative and significant, implying the country’s exchange rate depreciation reduces capital inflow into the country. In specific terms, a percentage depreciation in exchange rate in the low IRD regime significantly reduces capital inflow by 1.8 percent. This result supports the findings of Aisien (Citation2018), but contradicts the theoretical postulation that depreciation of exchange rate attracts foreign inflow. However, this can be explained on the ground that low IRD will lead to outflow of capital to country where return on investment is high relatively, which will lead to an adverse effect on capital account of the domestic economy. This outflow of capital may lead to foreign exchange shortage, which would further degenerate the capital inflow of the country. In the case of the constant value, the outcome demonstrates that at a low IRD regime, when the explanatory variables (IRD and LERA) are zero, the foreign capital inflow into Nigeria is N4.5 billion.

The second segment of the DTR result demonstrates the high IRD regimes. Expectedly, both interest rate differential (IRD) and exchange rate (LERA) are positively and significantly influencing foreign capital inflow in Nigeria. The positive coefficient of IRD corroborates the findings of Karimo (Citation2020) and Makhetha-Kosi et al. (Citation2016) and validates both the portfolio theory and interest rate parity theory that increase in domestic interest rate relative to foreign rate will attract foreign capital inflow into a country. Specifically, one percent increase in interest rate differential above 3.68% will attract significantly about N0.26 billion worth of foreign investment into the country.

Similarly, exchange rate depreciation will lead to increase in the inflow of foreign capital in the country. What this means is that, a high IRD above 3.68% will attract huge inflow of capital into Nigeria and this inflow will mount pressure on demand for local currency (increased supply of foreign currency) and hence bring stability in foreign exchange rate market which, in turn, will lead to a further increase in foreign capital inflow. The constant value in the high IRD regime, interestingly, indicates a higher value relative to the low IRD regime. The implication of this outcome is that there is a monumental positive response of foreign inflow to variables other than the IRD and LERA in high IRD regime than in its low IRD regime.

The last part of the DTR result shows political stability variable as the non-threshold variable. As anticipated, political stability (LPOS) has a favourable and substantial effect on the flow of foreign capital into Nigeria. The positive coefficient of LPOS indicates that high stability in the country’s political environment will result in an increase in international capital flows into the country and this outcome corroborates the findings of Qadri et al. (Citation2020) for Pakistan and Bitar et al. (Citation2019) for Luangaram and Sethapramote (Citation2020) for Thailand. This is consistent with a priori expectations, as investors seek relative stability in both political and economic terms in order to ensure their profits.

The coefficient determination and its adjusted value are 0.821 and 0.782, respectively. This indicates that the model is reasonably well fitted and that approximately 82.1 percent of the variation in foreign capital inflow is explained by changes in the model’s explanatory variables (interest rate differential, exchange rate, and political stability), with the remaining 17.9 percent explained by the error term. The overall regression measured by the F-statistics shows that the combined exogenous variables significantly influence international capital inflow in Nigeria.

The robustness of our estimated outcome within DTR result were examined through diverse test of validity. The Ramsey RESET test of model misspecification shows that the model was well specified as its p-value is greater 0.05. The Breusch-Pagan-Godfrey Heteroskedasticity test shows that the residual has constant variance. The Breusch-Godfrey serial LM test shows no evidence of autocorrelation in model as the p-value is greater than 0.05 while the J-B statistics indicates a normal distribution in the residual. The Wald tests demonstrate the rejection of null hypothesis of symmetric of the coefficients of IRD and ERA, implying that the variables are asymmetric and thus validates the nonlinearity estimation within the discrete threshold model.

6. Conclusion and policy implication

This study examined the influence of interest rate differentials, exchange rate fluctuations, and political stability in Nigeria using discrete threshold regression model (DTRM). In light of the fact that Nigeria has achieved some levels of stability and economic reforms after the country’s return to democracy in 1999, following many years of volatility in its political space, the study explored regime switching estimation technique. The study found out a single threshold value of interest rate differential of 3.69%, implying that interest rate differential high and above the threshold value attracts a positive and significant inflow of foreign capital into the country. Thus, monetary authority should fix a situation-varying, inflation-adjusted and investment-friendly interest rate, taking cognizance of international interest rate in order to attract foreign capital flow into the country. Furthermore, political stability and exchange rate movement also affect inflow of capital in the country. The implication is that investors compare the IRD in a country with other risk factors (political and macroeconomic) and will only invest if the IRD is greater than 3.68% as this will compensate for other opportunity cost at home as well as risk factors in the recipient’s economy. The direct response of capital inflow to stable political system in the country indicates that political-related crisis enervates business climate and creates fear of losses among investors and hence affects capital flow inversely (Qadri et al., Citation2020; Bitar et al., Citation2019 for Luangaram & Sethapramote, Citation2020). This result is in tandem with the report from CBN (Citation2021) that total foreign capital inflow into the country declined by 15% in 2021 following 22% rise in political-related violence in Nigeria especially in the Northern and South Eastern parts of the country (ACLED, Citation2021). Therefore, government reforms must target policies that enhance political stability, removal of structural distortions and creation of business-friendly environment to attract foreign capital inflow into the country.

7. Limitations

This study is a country-specific study in a country prone to political crisis. Similar study can be conducted in other sub-Saharan African and Asian countries to juxtapose the empirical results. These regions have experienced surged capital flow in recent years as reported by IMF, and thus study on the roles of interest rate differentials and political risk in influencing capital surge is recommended.

Disclosure statement

No potential conflict of interest was reported by the authors.

References

- ACLED. (2021). Armed Conflict Location and Event Data Project (ACLED). Codebook. 2021 .

- Adewuyi, A. O., & Ogbode, J. O. (2019). The validity of uncovered interest parity: Evidence from African members and non-member of the Organization of Petrileum Exporting Countries (OPEC). Economic Modelling, 82, 229–14. https://doi.org/10.1016/j.econmod.2019.01.008

- Aisien, L. N. (2018). The impact of exchange rate of foreign private investment in Nigeria. Asian Finance and Banking, 2(2), 19–32. https://doi.org/10.46281/asfbr.v2i2.208

- Bitar, A., Hamadeh, M., & Khoueiri, R. (2019). Impact of political instability on foreign direct investment in Lebanon. Asian Social Science, 16(1), 41–48. https://doi.org/10.5539/ass.v16n1p41

- Bogdan, T. (2016). Determinants of capital flows to emerging market economy: A case of Ukraine. Transformations in Business and Economics, 15(37), 127–146.

- Branson, W. H. (1986). Stabilization, stagflation, and investment incentives: The case of Kenya 1979-1980. In S. Edwards & L. Armed (Eds.), Economic adjustment and exchange rates in developing countries (pp. 267–293).

- CBN. (2020). Central bank of Nigeria statistical bulletin.

- CBN. (2021). Centralbank of Nigeria statistical bulletin.

- Chenery, H. B., & Stout, A. (1966). Foreign assistance and economic development. The American Economic Review, 55, 679–733.

- Cheung, Y. W., Sven, S., & Frank, W. (2016). China’s capital flight: Pre and post crisis experience. Journal of International Money and Finance, 6(6), 88–112. https://doi.org/10.1016/j.jimonfin.2015.12.009

- Culha, A. A. (2006). A structural VAR analysis of the determinants of capital flows into Turkey. Central Bank Review, 2, 11–35.

- Enisan, A. A. (2017). Determinants of foreign direct investment in Nigeria. Review of Innovation and Competitiveness, 3(1), 21–48. https://doi.org/10.32728/ric.2017.31/2

- Forster, M., Jerra, M., & Tillmenu, P. (2012). The dynamics of international capital flows: Result from a dynamic heirarchial factor model. MAGKS Joint Discussion Paper Series in Economics. No. 21- 2012. Philipps-University Marbung.

- Grzegorz, T., Brzozowski, M., & Shiwinski, P. (2017). Determinants of capital flows to emerging and advanced economies between 1990 and 2011. Port Economics Journal. https://doi.org/10.1007/s10258-016-0126-5

- Hannan, S. A. (2018). Revisiting the determinants of capital flows to emerging market – A survey of the evolving literatures. IMF Working Paper No.WP/18/214.

- Hansen, B. (1999). Testing for linearity. Journal of Economic Surveys, 13(5), 551–576. https://doi.org/10.1111/1467-6419.00098

- Hansen, B. (2011). Threshold autoregression in economics. Statistics and Its Inference, 4(2), 123–127. https://doi.org/10.4310/SII.2011.v4.n2.a4

- Jabbor, A., & Awan, A. G. (2014). The determinants of capital inflow in developing countries with special reference to Pakistan. Developing Countries Studies, 4(12), 159–182.

- Karimo, T. M. (2020). Impact of interest rate differential and exchange rate movement on the dynamics of Nigeria’s international private capital flows. Central Bank of Nigeria Journal of Applied Statistics, 11(2), 29–63. https://doi.org/10.33429/Cjas.11220.2/8

- Keynes, J. M. (1923). A tract on monetary reform. Macmillian and Co Ltd.

- Khaskheli, A., Jiang, Y., Raza, S. A., Khan, K. A., & Qureshi, M. A. (2021). Financial development, international trade and environmental degradation: A nonlinear threshold model based on panel smooth transition regression. Environmental Science and Pollution Research, 28(21), 26449–26460. https://doi.org/10.1007/511356-020-11912-8

- Li, Y., & Guo, J. (2022). The asymmetric impacts of oil price and shocks on inflation in BRICS: A multiple threshold nonlinear ARDL model. Applied Economics, 54(12), 1377–1395. https://doi.org/10.1080/00036846.2021.1976386

- Liyanage, E. (2014). Determinant of capital inflows: Evidence from Sri Lanka. Staff Studies Central Bank of Sri Lanka, 44(1&2), 1–32.

- Luangaram, P., & Sethapramote, Y. (2020). Capital flows and political conflicts: Evidence from Thailand. The Economics of Peace and Security Journal, 15(2), 83–99. https://doi.org/10.15355/epsj.15.2.83

- Makhetha-Kosi, P., Mishi, S., & Ngonyama, N. (2016). The response of capital flows to interest rate differentials: The case of South Africa. Journal of Economics, 7(23), 119–129. https://doi.org/10.1080/09765239.2016.11907827

- Ning, Y., & Zhang, L. (2018). Modelling dynamics of short term international capital flows in China: A Markov regime switching approach. North America Journal of Economics and Finance, 44, 193–203. https://doi.org/10.1016/j.najef.2018.01.002

- Nwokoye, E. S., & Oniore, J. O. (2017). Impact of monetary policy on capital inflows in Nigeria. Business, Management and Economic Review, 3(10), 192–200. https://doi.org/10.4314/afrrev.v10i3.13

- Nwosa, P. I., & Adeleke, O. (2017). Determinants of FID and FPI volatility: an EGARCH approach. CBN Journal of Applied Statistics, 8(2), 47–67.

- Odionye, J. C., & Chukwu, J. O. (2021). The asymmetric effects of currency devaluation in selected sub-Saharan Africa. Economic Annals, 66(230), 135–155. https://doi.org/10.2298/EKA2130135O

- Olowookere, J. K., Olowo, S. O., Mabinuori, O. T., & Aderemi, T. A. (2020). Foreign capital inflow and poverty reduction on Nigeria: implication for sustainable development. EuroEconomica, 3(39), 33–41.

- Perron, P. (1989). The great crash, the oil price shock, and the unit root hypothesis. Econometrica, 57, 1361–1401.

- Pesaran, M. H., Shin, Y., & Smith, R. J. (2001). Bounds testing approaches to the analysis of level relationships. Journal of Applied Econometrics, 16(3), 289–326. https://doi.org/10.1002/jae.616

- Qadri, N., Shah, N., & Qureshi, M. N. (2020). Impact of political instability on international investment and trade in Pakistan. European Online Journal of Natural and Social Sciences, 9(2), 283–305.

- Sarkodie, S. A., & Owusu, P. A. (2020). How to apply the novel dynamic ARDL simulation (dynardl) and Kernel-based regularized least square (krls). MethodsX, 7(2020), 101160. https://doi.org/10.1016/j.mex.2020.101160

- Shahzad, U., & Qin, F. (2019). New terrorism and capital flight: Pre and post nine eleven analysis for Asia. Annals of Economics and Finance, 20(1), 465–487.

- Shin, Y., Yu, B., & Greenwood-Nimmo, M. (2014). Modelling asymmetric cointegration and dynamic multipliers in a nonlinear autoregressive distributed lag framework. In R. Sickles, & W. C. Horrace (Eds.), Festschrift in honour of peter schmidt (pp. 281–314). Springer.

- Su, D. S., & Zhang, Z. G. (2010). Quadruplex arbitrage model and short-term international capital flow. Finance & Economics, 269, 17–24.

- Sy, A., & Rakotondrazaka, R. M. (2015). Private capital flows, official development assistance and remittances to Africa: who gets whar?. Brookings Institution, Washington DC.

- Thirlwall, P. A. (1976). Financing economic development. The Macmillian Press, Ltd.

- Ullah, A., Mansoora, A., Raza, S. A., & Ali, S. (2021). A threshold approach to sustainable development: Nonlinear relationship between renewable energy consumption, natural resource rent and ecological footprint. Journal of Environmental Management, 295, 1–10.

- Ullah, A., Zhao, X., Amin, A. A., Syed, A. A., & Riaz, A. (2022). Impact of COVID-19 and economic policy uncertainty on China’s stock market returns: Evidence from quantile-on-quantile and causality-in quantile approaches. Environmental Sciences and Pollution Research. https://doi.org/10.1007/s11356-022-22680-y

- UNCTAD. (2015). World investment report (2015); reforming international investment governance. United Nations Publication.

- UNCTAD. (2017). World investment report (2017); investment and digital economy. United Nations Publication.

- UNCTAD. (2018). World investment report (2018); investment and new industrial policies. United Nations Publication.

- Wang, K. H., Su, C. W., & Tao, R. (2019). Time-varying character for short-term capital flow from the interest rate aspect in China. Economic Research-Ekonomska Istrazivanja, 32(1), 2761–2779.

- World Development Indicator. (2021). The World Bank Group. https://data.worldbank.org/indictor.

- Zivot, E., & Andrews, K. (1992). Further evidence on the great crash, the oil price shock, and the unit root hypothesis. Journal of Business and Economic Statistics, 10(10), 251–270.