?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

This research study examines the mediating role of cash holdings between the economic policy uncertainty (EPU) and corporate leverage relationship. Using stepwise regression analysis and annual firm-level data of 2,534 U.S. firms listed at NYSE over 1995–2018, we provide novel evidence that cash holdings significantly and partially mediate the EPU-leverage relationship, accounting for a 10.72% increase in the corporate leverage during EPU. We discover that the mediating role of cash holdings between EPU and leverage is sensitive to firm-level heterogeneity. Also, the mediating effect of cash holdings remains significant based on long- and short-term leverage. Finally, our findings are robust to outliers’ effect, alternate EPU measurement, endogeneity concerns and sample-selection bias. The findings of this study highlighted the role of firm cash holdings in a firm’s leverage decision during economic uncertainty and recommends increasing debt financing to incentivize value-increasing decisions and mitigate agency problems by reducing the cost of free cash flows. Policymakers should be aware of public and private firms’ challenges during high EPU. As we showed in this study, firms have to adjust their financial decisions during high economic uncertainty. Also, the study suggests that policymakers should maintain economic policies to avoid external shocks that may force firms to adjust their financial decision-making.

1. Introduction

The uncertainty about the monetary and fiscal policy of the economy leads to a detrimental effect on the various aggregate as well as firm-level outcomes (S. R. Baker et al., Citation2016). Firms align their financial and investment decision based on changes in economic policy to avoid adverse effects on firm efficiency in terms of investment loss and high cost of financing. Since the economic policy of a country plays a vital role in business activities and the firm’s operational and financial decisions are susceptible to economic policy uncertainty (Gulen & Ion, Citation2016; Phan et al., Citation2019; Zhang et al., Citation2015). In this regard, the research studies on the economic policy uncertainty (EPU) and leverage relationship, one of the fundamental financial decisions, show mixed results and still need to be investigated. On the one hand, based on the debt-market supply hypothesis, EPU negatively affects corporate leverage (X. M. Li & Qiu, Citation2021; Zhang et al., Citation2015). As EPU increases the information asymmetry between lender and borrower, hence increases the cost of debt financing (Zhang et al., Citation2015). On the contrary, based on the equity-market supply hypothesis, the relationship between EPU and corporate leverage is positively related (Bajaj et al., Citation2021; Schwarz & Dalmácio, Citation2020). The positive relationship between EPU and leverage is because equity financing becomes expensive as the equity investor demands a high-risk premium caused by increasing EPU (Pástor & Veronesi, Citation2013).

On the opposite verges of EPU-leverage relationship literature, limited studies discuss the relevant channels that impact this relationship. In the literature, Lee et al. (Citation2017) show that EPU impacts the financial institution’s debt financing decision through its risk-taking capacity and unstable lending behaviour channel. Further, Khan et al. (Citation2020) also document trade credit’s moderating role between EPU and leverage using the Chinese firm data. Also, Asimakopoulos et al. (Citation2023) examined the impact of EPU through the Environmental, Social and Governance (ESG) ratings channel on firm leverage. This study evaluates the mediating channel of cash holdings between EPU-leverage relationship based on U.S. non-financial firms listed at NYSE.Footnote1

Mainly, three main reasons motivate examining the impact of EPU on leverage through the mediating channel of firm cash holdings. Firstly, cash holdings play a crucial role in determining the financial decisions of firms. Since during high EPU, firms tend to save more cash as a precautionary measure (Demir & Ersan, Citation2017; Phan et al., Citation2019) to pay off debts and hedge against unexpected financial distress. Therefore, it is essential to understand the impact of economic policy uncertainty on cash holdings and how this affects leverage decisions. Secondly, when firms hold more cash, they may be more inclined to take on more debt because they have a cushion to fall back on in financial distress. In contrast, firms with less cash may be more cautious about taking on additional debt to avoid financial risk. As a result, cash holdings can mediate the relationship between EPU and leverage. Thirdly, understanding the relationship between EPU and leverage through the role of cash holdings can help firm managers to manage better risks associated with economic uncertainty. By examining the factors influencing the relationship between EPU and leverage, firms can make informed decisions about their financial and investment strategies. Policymakers can also use this information to design more effective policies to support firms during uncertain economic times.

Further, the theoretical underpinnings of agency theory suggest that managers do not use the cash holdings appropriately for shareholder wealth maximization and over-invest in the value-destroying investment (Harford et al., Citation2012). Also, when more cash is available due to precautionary motives, the manager may use it for personal benefits (Frésard Laurent & Salva, Citation2010; Pinkowitz et al., Citation2006). Thus, agency problems arise due to an increase in cash holdings. However, to deal with the agency problem, N. Jensen and Meckling (Citation1976) suggested increasing debt financing to curb the agency problem between shareholders and managers. In this way, managers may be unable to make value-decreasing decisions, which would decrease the cost of free cash flows (M. C. Jensen, Citation1986). Relying on these arguments, evaluating the role of cash holdings between EPU and corporate leverage is essential.

We conduct a stepwise regression analysis based on Preacher and Kelley (Citation2011) to check the impact of EPU on leverage through the mediating channel of cash holdings using a sample of U.S. non-financial firms listed at NYSE over 1995–2018, including Citation2534 unique firms with 32,329 firm-year observations. Recent studies use the same empirical design for mediation analysis (S. Chen et al., Citation2021; Zhou et al., Citation2021). Further, similar to earlier studies regarding EPU impact on leverage (Bajaj et al., Citation2021; X. M. Li & Qiu, Citation2021; Zhang et al., Citation2015), we employ the annual average monthly EPU index values for our empirical analysis developed by (S. R. Baker et al., Citation2016). We find that EPU positively and significantly impacts corporate leverage and cash holdings at a 1% significance level. Moreover, cash holdings significantly and partially mediate the relationship between EPU and corporate leverage, accounting for a 10.72% increase in the EPU effect on corporate leverage. Also, the mediating effect in the heterogeneous analysis is only significant in low-investment-intensive firms. Also, in additional analysis, we show evidence that the mediating effect of cash holdings between the EPU-leverage relationship remains equally significant using long- and short-term leverage. Finally, our results are robust to the outlier’s effect, alternate EPU measurement, endogeneity issues and sample selection bias.

Our study contributes to the literature in a manifold. First, unlike the previous studies that show formal analysis between EPU and leverage relationship (X. M. Li & Qiu, Citation2021; Pan et al., Citation2019; Zhang et al., Citation2015), we specify the novel evidence that there is a significant and partial mediating effect of cash holdings between the EPU-leverage relationship shows that cash holdings partially explain the impact of EPU on leverage decisions. Second, our study augments the empirical literature on the relationship between uncertainty and leverage and identifies cash holdings as a significant channel that mediate the relationship between EPU and leverage. Also, our analysis confronts the debt-market supply hypothesis over the equity-market supply hypothesis and shows that NYSE-listed firms prefer debt financing over equity financing during high EPU. These results provide policy insights from the agency problems perspective that arise due to increased cash holdings. Managers may only sometimes use cash holdings appropriately for shareholder wealth maximization and may engage in value-destroying investments or use the cash for personal benefits. By increasing debt financing, managers may be incentivized to make value-increasing decisions and decrease the cost of free cash flows to mitigate the agency problem. Hence, it is recommended to increase debt financing, while the increase in cash holdings due to high EPU. A better understanding of the relationship between EPU, firm cash holdings, and leverage can help managers make informed financial decisions and mitigate the potential risks associated with EPU. Also, these findings suggest that policymakers should manage risks associated with economic uncertainty to avoid any external shock to the business environment, forcing the firms to adjust their financial decision-making.

This study proceeds further as follows: in Section 2, we will discuss the literature; in Section 3, we will discuss the sample data, variables and empirical specification. Section 4 presents the empirical analysis, including heterogeneous analysis, robustness checks, and an additional test, and Section 5 will show the conclusion and policy implication of the study.

2. Literature review

Prior literature shows evidence that EPU affects different macro and firm-level outcomes. Like on aggregate-level outcomes, Prüser & Schlösser (Citation2020) reported the negative impact of EPU on the financial market and real economy in European monetary union economies. Hu and Gong (Citation2019) studied EPU with bank lending and prudential regulations. They reported that EPU impacts bank lending growth rate in the case of large and riskier banks but has a weaker effect on liquid and diversified banks. Kido (Citation2016) checked the spillover effect of US EPU on the global financial market, including exchange rates, equity prices, and commodity prices. L. Liu and Zhang (Citation2015) also checked the impact of EPU on stock market volatility and claimed that with an increase in EPU, stock market volatility increases. The evidence of EPU’s effect on long-term industry beta is presented by Yu et al. (Citation2017). Demir et al. (Citation2018) provided evidence that suggests that EPU predicts a negative impact on Bitcoin returns. Apart from aggregate-level outcomes, on the firm level, EPU impacts corporate financial decisions extensively, including firms’ cash holdings (Demir & Ersan, Citation2017; Phan et al., Citation2019) and leverage (Bajaj et al., Citation2021; Istiak & Serletis, Citation2020; X. M. Li & Qiu, Citation2021, Makololo & Seetharam, Citation2020; Schwarz & Dalmácio, Citation2020; Tabash et al., Citation2022; Zhang et al., Citation2015). However, these studies show only the direct impact of EPU on firm leverage and present mixed results. At the same time, this relationship is multifaceted and needs to be addressed. So, this study undertakes cash holdings as an essential mediating channel in the relationship between EPU and firm leverage. We also discuss the theoretical reason for this relationship in Section 2.3.

2.1. Economic policy uncertainty and corporate leverage

The literature regarding the impact of EPU on the firm leverage shows results in different dimensions. Zhang et al. (Citation2015) report that Chinese firms decrease their leverage ratio when EPU increases. However, firms from the less marketized region, having prior bank relationships and state ownership, can moderate the negative effect of EPU on debt financing in China. Also, this study shows that EPU negatively impacts both short-term and long-term leverage, though the significance is more promising to the short-term leverage. Another study by Liu and Zhang (Citation2020) on Chinese firms claimed that EPU impedes real investment and debt issuance for private firms, while the state-owned firm has no such effects. Lv and Bai (Citation2019) state that political uncertainty rises during political turnover, and Chinese firms decrease debt financing. In the Chinese market, the negative impact of EPU on firm leverage may be due to the limited access to credit and financial markets. Further, Schwarz and Dalmácio (Citation2020) show that EPU positively impacts the corporate leverage of Brazilian firms. Bajaj et al. (Citation2021) analysed the impact of EPU on leverage using Indian firms listed on the National Stock Exchange and found a positive relationship channel through the available growth options. Athari and Bahreini (Citation2022) conducted a study based on samples of travel and leisure firms from Western European economies and revealed that EPU negatively impacts the debt level.

Based on U.S. firm sample data, Pan et al. (Citation2019) show that policy uncertainty decreases corporate leverage, and negative impact on debt maturity and corporate leverage is more pronounced in firms with lower credit ratings and high investment reversibility. Also, another study based on panel data from U.S. manufacturing firms shows that high-uncertainty firms have lower book and market mean targeted capital structures than low-uncertainty firms (Im et al., Citation2020). The study of X. M. Li and Qiu (Citation2021) evaluated the combined effect of EPU and firm-based characteristics on the capital structure using the firm-level data of U.S. firms listed on the NASDAQ and NYSE. Their study proves that the impact of EPU on the leverage ratio is not identical between the cross-sections. Due to the diverse characteristics of firms, this effect can be damaging for some corporates while positive for others.

Conclusively, the relationship between EPU and corporate leverage is complex and multifaceted. On the one hand, EPU may decrease corporate leverage by increasing the demand for liquidity and precautionary savings. The reason is that EPU may increase the uncertainty and volatility of future cash flows, investment opportunities, and financing conditions, making firms more reluctant to take on debt and more inclined to hold cash. On the other hand, EPU may increase corporate leverage by reducing the cost of debt relative to equity. The rationale for a positive relationship is that EPU may lower the risk-free interest rate, increase the equity risk premium, or reduce the debt tax shield due to lower expected profits. On these opposite results on the relationship between EPU and leverage in the literature, this study assumes that EPU impacts corporate leverage; however, this relationship is multifaceted, and changes in cash holdings during high EPU mediate the relationship between EPU and leverage.

2.2. Economic policy uncertainty and cash holdings

The recent literature shows results about the impact of EPU on cash holdings through various channels. N. Xu et al. (Citation2016) empirically proved that Chinese firms hold less cash during high political uncertainty due to political extraction and agency conflict. In the same notion, the study of Feng et al. (Citation2019) states that state-owned firms have fewer cash holdings during high uncertainty, whereas, for private firms, the result is opposite to this notion due to precautionary motives. However, through the same channel of precautionary motives, the study of Su et al. (Citation2020) shows a U-shaped relationship between economic policy uncertainty and corporate cash holdings for precautionary motives. This relationship indicates that there is a negative relationship between them and then an increased relationship. Further, this relationship is significant for both state-owned and private firms, but the relationship is more robust for state-owned firms.

The study of Y. Liu et al. (Citation2021) suggested that the assets reversibility channel decreases the firm’s cash holdings even during high economic policy uncertainty. The study by Cheng et al. (Citation2018) suggests that policy uncertainty increases the volatility of the financial market. In contrast, political uncertainty increases cash holdings during the normal financial condition and decreases under the complex financial condition in U.S. firms. In the same context of U.S. firms, the study of Phan et al. (Citation2019) empirically proved that economic policy uncertainty increases the firm cash holdings due to investment irreversibility and precautionary intentions, and a firm dependent on government spending has a greater propensity for this phenomenon. Further, Benkraiem et al. (Citation2020) highlighted the role of corporate diversification using French firm data. They showed that firms with multinational existence tend to hold less cash from their cash flow because of diversification and access to external financing. However, during the economic crisis, the influence on diversified firms is more significant than on non-diversified firms; hence, cash holdings increase in an economic slump.

Apart from the above studies, which are solely based on single-country data, some studies are based on cross-country data to test the relationship between economic policy uncertainty and cash holdings. The study of Demir and Ersan (Citation2017) suggests that firm cash holdings increase in BRIC countries during high economic policy uncertainty. Further, in a cross-country setting, X. Li (Citation2019) suggests that firms tend to hold more cash during the high EPU due to precautionary motives. In summary, two main channels from the literature are precautionary motives and investment irreversibility during high EPU, which increases cash holdings. This study also assumes that EPU increases cash holdings, mediating the EPU and corporate leverage relationship.

2.3. Theoretical linkage and hypothesis

Agency theory explains why EPU may affect firm leverage decisions through cash holdings. During the high EPU, precautionary motives increase cash holdings (Demir & Ersan, Citation2017; Phan et al., Citation2019). At the same time, managers do not use the cash holdings appropriately for the wealth maximization of shareholders and over-invest in the value-destroying investment (Harford et al., Citation2012). Further, when more cash is available, it will also lead the manager to use it for personal benefit (Frésard Laurent & Salva, Citation2010; Pinkowitz et al., Citation2006). So, increased cash holdings lead to agency problems between shareholders and managers. Primarily, agency theory captivates attention to mitigate the disagreement between the managers and shareholders due to their conflict of interest (Menéndez-Alonso, Citation2003). Literature suggested increasing debt financing to mitigate the agency problem between managers and shareholders (N. Jensen & Meckling, Citation1976). In this context, managers may hesitate to take value-decreasing decisions because they do not want to risk the firm’s financial health or creditworthiness. Instead, they may focus on preserving cash and paying down debt, even if it means forgoing potential investment opportunities that could increase the firm’s value. Based on these theoretical arguments and previous literature concludes that cash holdings are expected to increase during high EPU due to the precautionary motive of managers (Demir & Ersan, Citation2017; Phan et al., Citation2019) and fewer investments opportunities (Bates et al., Citation2009), this study assumes that increase in cash holdings during high EPU, expected to mediate the EPU corporate leverage relationship.

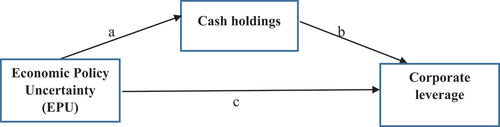

In essence, the above discussion suggests that EPU is expected to increase its cash holdings, which, in turn, will affect EPU and corporate leverage relationships. The line of reasoning is shown in Figure : the effect of economic policy uncertainty (EPU) on corporate leverage (path “c”) through a mediating role of cash holdings (path “a” * “b”). Hence, we hypothesize that;

Figure 1. The relationship between EPU, corporate leverage and cash holdings.

Hypothesis:

Other things equal, cash holdings mediate the effect of EPU on corporate leverage.

Path ‘c ‘shows the direct effect of economic policy uncertainty (EPU) on corporate leverage, adding all relevant control variables as per EquationEq.1(1)

(1) in empirical specifications.

Path “a” and “b” shows the indirect effect of EPU on corporate leverage through cash holdings following EquationEquations 2(2)

(2) and Equation3

(3)

(3) in empirical specifications.

3. Data, variables, and empirical specification

This section explains the data sample, data sources, variable measurement, descriptive statistics, and empirical specification of the study.

3.1. Sample specification

We obtained firm-level financial data of all U.S. non-financial firms listed at NYSE over 1995–2018 from the THOMSON REUTERS EIKON database.Footnote2 To measure the economic policy uncertainty, we opt for the news-based EPU index developed by (S. R. Baker et al., Citation2016).Footnote3 The EPU index has been widely used in earlier studies to proxy economic policy uncertainty (Demir & Ersan, Citation2017; Ilyas et al., Citation2021; X. M. Li & Qiu, Citation2021; Phan et al., Citation2019; Zhang et al., Citation2015). We exclude all the financial firms (SIC codes 6000–6999) from the dataset following (Z. Xu, Citation2019; Zhou et al., Citation2021).Footnote4 We also remove firms with significant missing values on total debt and total assets. Further, we winsorize all the financial variables by (the 1st and 95th percentile) to reduce the effect of the possible outliers. Our final sample comprises 2,534 unique firms and 32,329 firm-year official observations. However, the sample observations may fluctuate during analysis due to missing values of various explanatory variables in several regression models. Also, the number of firms in each sector is shown in Appendix A.

3.2. Variable specification

The following section explains the dependent, independent, mediator, and control variables.

3.2.1. Dependent variable: Corporate leverage

Former studies relevant to economic policy uncertainty use the ratio of total debt to book value of total assets as a measure of corporate leverage (Lee et al., Citation2017; X. M. Li & Qiu, Citation2021; Pan et al., Citation2019; Zhang et al., Citation2015). We follow the exact definition to estimate corporate leverage to maintain consistency with earlier studies. In an additional analysis following Zhang et al. (Citation2015), we extend the analysis based on long- and short-term corporate leverage. We measure the long-term and short-term corporate leverage as the ratio of long-term debt to the book value of total assets and the short-term debt to the total book value of assets, respectively.

3.2.2. Explanatory variable: Economic Policy Uncertainty (EPU)

We employ the one-year lagged news-based EPU index developed by (S. R. Baker et al., Citation2016) to measure economic policy uncertainty. This index covers discussions on policy-related uncertainty published in the top ten newspapers in the US. The reason for taking this index is that it covers the general economic conditions, changes in economic policies, and the sentiment of general people based on the overall macroeconomy (Istiak & Serletis, Citation2018; F. Li et al., Citation2021). The higher value of the EPU index shows greater economic policy uncertainty and vice-versa. Further, this index is widely used in many recent studies to gauge uncertainty related to economic policy, including (Demir & Ersan, Citation2017; Ilyas et al., Citation2021; X. M. Li & Qiu, Citation2021; Phan et al., Citation2019; Zhang et al., Citation2015). Further, to balance the frequency with firm-level yearly data, we derive the annual average of monthly EPU index values and transform it with natural logarithm (L.N. news-based EPU) following (Akron et al., Citation2020). This study deals with the EPU index data as follows.

where t denotes the year, and m denotes the monthly value of the U.S. EPU index.

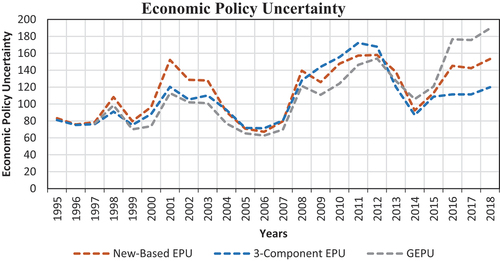

Further, for the robustness test, we use a three-component based U.S. EPU index, including the coverage of news related to economic policy uncertainty, the uncertainty about the modifications in tax code based on Congressional Budget Office (CBO) report, last, the disagreement on fiscal and monetary policy based on Federal Reserve Bank of Philadelphia’s Survey of Professional Forecasters. Next, we use the global economic policy uncertainty index (GEPU hereafter) as the U.S. EPU index is the significant subset of the GEPU index.Footnote5 The derivation for these two variables is the same as the above formula. Further, Figure shows the graphical representation of all three measures of EPU. The figure shows significant variation in all three measurements over the sample period. Moreover, there is also a high positive correlation among them, and all three measures of EPU increased over time.Footnote6

Figure 2. The plot of News-based EPU, 3-component-based EPU and GEPU indexes over the sample period (1995–2018) .

3.2.3. Mediating variable: Cash holdings

This study is based on mediation analysis using cash holdings as a mediating channel on the relationship between EPU and corporate leverage. We compute the cash holdings using the ratio of cash and cash equivalent to the total asset. The same proxy is used by (Demir & Ersan, Citation2017; Loncan, Citation2020; Phan et al., Citation2019) to quantify the firm cash holdings.

3.2.4. Control variables

Additionally, we add various one-year lagged control variables to set apart the mediating role of cash holdings between the EPU-leverage relationship and the direct effect of EPU on leverage. The inclusion of the control variables enables us to compare the results with previous studies and overcome the omitted variable issue. Following the model specification of Lemmon et al. (Citation2008) and Zhang et al. (Citation2015), we control for tangible assets ratio (Tangibility), initial leverage (initial leverage), firm size (Size), firm profitability (Profitability), growth opportunity (ΔSales), and sales revenue (Sales revenue). Further, we also include firm-fixed effects to address the undetected heterogeneity concern and industry effects (Dittmar & Mahrt-Smith, Citation2007).Footnote7 Appendix B provides detailed information about the dependent, independent, mediating and control variables employed in the primary and additional tests.

3.3. Descriptive statistics

Table shows the descriptive statistics for all variables, including observations, mean, median, standard deviation, and minimum-maximum values. The sample period is from 1995 to 2018. A duration of 24 years is significant to show the complete picture of the U.S. EPU index, corporate leverage, and cash holdings of U.S. non-financial firms listed at NYSE. Our sample data shows that the average corporate leverage and cash holdings ratios are 30.4% and 9.9%, respectively. The mean value of the EPU index (natural logarithm of news-based EPU index) is 4.706. The mean value for the three-component EPU index and GEPU index is 4.635 and 4.648, respectively. The maximum, minimum, and standard deviation of dependent, independent, and mediating variables show enough variation within the sample period, displaying the study’s practical inference and viability. We also reflect the long-term debt to the total-debt ratio for the viability of additional analysis to show how much U.S. firms listed at NYSE rely on long-term debt financing.Footnote8 The value of the long-term debt to total debt ratio is 83.11%, which shows that firms listed at NYSE heavily rely on long-term debt financing.

Table 1. Descriptive statistics

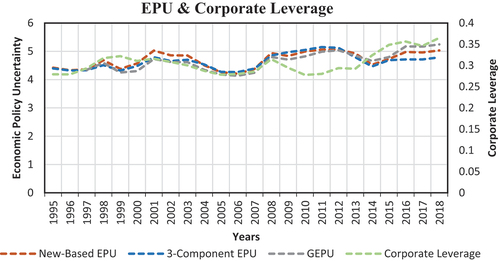

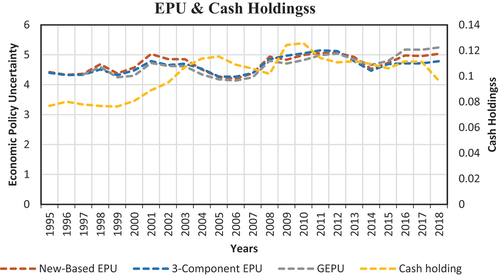

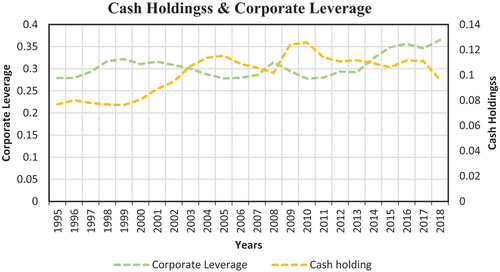

Next, a first approach to showing the association between EPU and corporate leverage through cash holdings is shown in Figures and 5. In Figures , the graphical representation of EPU with corporate leverage and cash holdings shows a positive relationship, respectively. Figure shows the negative relationship between yearly average cash holdings and corporate leverage ratio. Hence, we can posit a mediating effect of cash holdings between the EPU-leverage relationship. We also report the Pearson correlation among all the variables in Appendix C. Based on correlation results, all three measures of EPU show a positive correlation with corporate leverage and cash holdings. Also, cash holdings and corporate leverage are negatively correlated. Hence, the results shown in the graphical representation are also consistent with correlation results estimation.

Figure 3. Economic policy uncertainty and average corporate leverage behaviour over 1995–2018.

Figure 4. Economic policy uncertainty and average cash holdings behaviour over 1995–2018.

Figure 5. Average corporate leverage and average cash holdings behaviour over 1995–2018.

3.4. Empirical specification

The current study hypothesizes that cash holdings mediate the relationship between EPU and corporate leverage. We employ stepwise regression analysis based on Preacher and Kelley (Citation2011) to explore the mediating impact of the cash holdings between EPU and corporate leverage. Recent studies used a similar empirical design for mediation analysis (S. Chen et al., Citation2021; Zhou et al., Citation2021). First, we investigate the effect of EPU on corporate leverage using model (1) without adding a mediating variable. Second, we find the impact of EPU on a mediator, that is, cash holdings, where EPU is set as an explanatory variable and mediator as an explained variable, as shown in model (2). Last, we identify the mediating role of cash holdings between EPU and corporate leverage by adding the mediator in a model (1), shown as a model (3). The purpose of using the stepwise regression analysis is twofold. Along with investigating the mediating role of cash holdings between the EPU-leverage relationship, this analysis also examines the direct impact of EPU on corporate leverage (direct effect path “c” as shown in Figure ) based on model (1), which is unclear in the literature. The empirical model specification to address the core proposition of this study is as follows:

where i denotes the firm, t represents the year, EPU, leverage, mediator, and control variables defined above. To establish the mediating effect using stepwise regression, the coefficients

and

must be significant (Preacher & Kelley, Citation2011; Zhao et al., Citation2010). If any of the coefficients from

and

are insignificant, then there is no mediation. Further, if the coefficients

,

, and

are significant, this shows a full mediation effect. However, if the coefficients

,

and

are all significant, this proposes that the mediation effect is partial. Moreover, following Dittmar & Mahrt-Smith (Citation2007), we also include firm-fixed effects to address the unobserved heterogeneity concern and industry effects. However, to further constraint the firm-level heterogeneity, we divided the total sample into two groups based on investment intensiveness, that is, high- and low-investment-intensive firms, and performed the heterogeneous analysis. This analysis also serves the purpose of a robustness check for our baseline regression.

3.4.1. Robustness check

We perform different robustness checks for the baseline results. First, following the study of (M. Baker & Wurgler, Citation2002; Kayhan & Titman, Citation2007; Zhang et al., Citation2015), we exclude the firm-yearly observation where the value of the total leverage ratio is larger than one. Secondly, to rule out the measurement concern about the EPU and cash holdings, we use two different proxies for it. For EPU, we use a three-component-based EPU index and GEPU index, as explained in section 2.2.2 based on the prior studies (Fang et al., Citation2017; Gulen & Ion, Citation2016; Suh & Yang, Citation2021). We use the cash and cash ratio equivalent to the total sales for cash holding. Third, our baseline empirical specification is based on the hypothesis that EPU is an exogenous variable. However, a possible reverse causal relationship in all three equations of stepwise regression analysis leads to endogeneity concerns. To deal with this issue, we conduct a two-stage least-squares estimation using the Canadian EPU index as an instrumental variable. Finally, we utilize the propensity score matching (PSM) technique developed by (Rosenbaum & Rubin, Citation1983) to deal with sample selection bias.

3.4.2. Additional analysis

The study of Zhang et al. (Citation2015) shows that EPU negatively impacts long-term and short-term leverage, though the significance is more promising for short-term leverage in Chinese firms. The reason for the more significant results of short-term leverage shown by (Ding et al., Citation2020) is that, on average, short-term leverage is 69% of the total debt in Chinese firms. Contrary to this, our study shows that, on average, total debt is 83% comprised of long-term leverage based on U.S. firms listed at NYSE.Footnote9 Therefore, we conduct additional analysis by substituting the total corporate leverage with long-term and short-term leverage to identify whether the cash holdings as the mediating channel is significant using both types of corporate leverage. Also, we examine whether the effect of EPU is equally pronounced on long-term and short-term leverage. We use baseline empirical specification to verify the additional analysis except for replacing total corporate leverage with long-term and short-term leverage.

4. Empirical findings

4.1. Baseline analysis

Table shows the parameter estimates based on the stepwise regression models for mediation analysis in Section 3.4. Based on EquationEq. (1)(1)

(1) –(Equation3

(3)

(3) ), the coefficients

,

and

are significant at a 1% level, as shown in Column (1) – (3), implying the mediating effect (path “a” * “b” as shown in Figure ). Further, the mediating impact of the cash holdings between EPU and leverage is partial, as the coefficients

= 0.014,

= 0.012,

= 0.015 and

= −0.127, all significant at 1% level (Preacher & Kelley, Citation2011). In Column (1), EPU shows a significant positive impact on corporate leverage at a 1% significance level (direct effect path “c” as shown in Figure ). Hence, confronting the debt market supply hypothesis entails that NYSE listed firms prefer debt financing over equity financing during high EPU aligned with the prior studies (Bajaj et al., Citation2021; Schwarz & Dalmácio, Citation2020). The reason could be the high equity premium, which forces NYSE-listed firms to resort to debt financing. In Column (2), EPU also shows a significant positive impact on cash holdings at a 1% significance level. The increase in cash holdings during high EPU attributed to precautionary motives and investment irreversibility aligned with earlier studies (Demir & Ersan, Citation2017; Phan et al., Citation2019). Further, in Column (3), the effect of EPU on corporate leverage is 0.015, which suggests that the mediating effect of the cash holdings is measured as (0.015095) – (0.013633) = 0.00146, accounting for a 10.72% increase in the effect of EPU on corporate leverage.Footnote10,Footnote11 The Sobel (Citation1982) test validates the statistical significance of mediating channel (z-statistics=4.121, p-value=0.000). The increase of cash holdings during high EPU can realize the leveraging effect during a period of high uncertainty.

Table 2. Baseline results

Next, we explain the effect of each control variable based on Columns (1) and (3); the initial leverage shows a positive association with leverage and is significant at a 1% level, validating the role of the firm initial leverage in shaping its capital structure (Lemmon et al., Citation2008). The tangibility ratio and firm size increase lead to a significantly lower leverage ratio. In general, mature firms tend to rely less on debt financing (Kieschnick & Moussawi, Citation2018). Further, profitability and ΔSales (growth opportunities) are significant at 10% and tend to increase the leverage ratio based on Column (3); however, in Column (1), only profitability is significant at the 5% level. It could be because firms may resort to debt financing to finance their potential growth prospects (Zhang et al., Citation2015). Finally, the impact of sales revenue on leverage is insignificant in both columns.

4.2. Heterogeneous analysis

We next investigate whether the mediating role of cash holdings between EPU and corporate leverage is sensitive to firm-level heterogeneity. Specifically, we perform the heterogeneous analysis based on investment intensiveness following (Akron et al., Citation2020; An et al., Citation2016).

The existing literature shows that EPU negatively affects corporate investment (Akron et al., Citation2020; P. F. Chen et al., Citation2019; Gulen & Ion, Citation2016; Wang et al., Citation2014). However, the effect of EPU on corporate investment is different at different quantiles (Akron et al., Citation2020). Also, the irreversibility of capital investment is one of the reasons for an increase in cash holdings through delaying investment (Phan et al., Citation2019). Given the role of investment delays in increased cash holdings, we investigate whether the mediating role of cash holdings between EPU and corporate leverage relationship would be the same for high- and low-investment-intensive firms.

We split the total sample into two samples concerning investment intensity. First, the high-investment-intensive firms with a capital expenditure ratio greater than the total sample’s median capital expenditure ratio. Second, low-investment-intensive firms with capital expenditure ratios below the total sample median capital expenditure ratio.Footnote12 We run the stepwise regression analysis (Preacher & Kelley, Citation2011), following the exact empirical specification in Section 3.4 for both samples.

Table reports the results of heterogeneous analysis based on firm investment intensive. In Columns (1)–(3), the result for high-investment-intensive firms shows that there is no mediating effect of cash holdings between EPU and corporate leverage because EPU has an insignificant impact on cash holdings in Column (2). Whereas, in Column (4)–(6), based on low-investment intensive firms, there is a partial mediating effect of cash holdings between the EPU-leverage relationship as the coefficients = 0.010,

= 0.019,

= 0.012 and

= −0.110, all significant at 1% level (Preacher & Kelley, Citation2011).Footnote13 In Column (4), EPU positively impacts corporate leverage at a 1% significance level, computed as 0.010. In Column (5), EPU also positively impacts cash holdings at the 1% significance level. Further, in Column (6), the effect of EPU on corporate leverage is 0.012, which suggests that the mediating effect of the cash holdings is, measured as (0.012432) – (0.010341) = 0.00209, accounting for a 20.20% increase in the EPU effect on corporate leverage.Footnote14 The Sobel (Citation1982) test validates the statistical significance of mediating channel effect (z-statistics = 3.907, p-value = 0.000).

Table 3. Heterogeneous analysis

4.3. Discussion of the results

Our baseline results are consistent on empirical as well as on theoretical grounds. On empirical grounds, the cost of financing is a primary determining factor for corporates to choose between equity or debt financing. During high uncertainty, equity investors seek excessive risk premiums; thus, the cost of equity increases (Pástor & Veronesi, Citation2013). Hence, firms resort to debt financing instead of equity financing during high uncertainty. Though the debt financing cost also increases during high EPU but is less than the cost of equity financing (Bajaj et al., Citation2021). Another possible empirical explanation for our results is that the volatility of a firm’s earnings increases; consequently, firms are inclined toward debt financing during high uncertainty (Lee et al., Citation2017; Schwarz & Dalmácio, Citation2020). Last, our study is solely based on U.S. firms listed at NYSE, where firms get easier access to external funding due to better reputation and liquidity (Yang et al., Citation2009). Thus, there is a significant positive association between EPU and corporate leverage. Theoretically, our results align with the agency theory that increasing debt financing due to rising cash holdings resolves agency problems between shareholders and managers (N. Jensen & Meckling, Citation1976). Due to high EPU corporate cash holdings, increases lead to agency problems as managers use that for their benefit (Dittmar et al., Citation2003; Kim et al., Citation1998). However, increasing debt financing forces managers to use firms’ resources better to maintain strong creditworthiness and avoid default risk, decreasing the agency cost of free cash flows (M. C. Jensen, Citation1986). Further, our results align with Myers (Citation1984) suggestions that the optimal financing order under information asymmetry is internal financing and debt financing. Whereas in the end, firms should resort to equity financing.

Further, regarding heterogeneous analysis results, our results show that the mediating channel of cash holdings on the relationship between EPU and corporate leverage is significant in low-investment intensiveness firms only. Since high-investment-intensive firms are usually large and face fewer financial constraints than low-investment-intensive firms (An et al., Citation2016), it can be one of the reasons that high-investment-intensive firms hold fewer cash holdings as a precautionary saving. Conversely, due to financial constraints and insufficient collateral for debt contracts, low-investment-intensive firms tend to have high cash holdings as precautionary savings. That might be the fundamental reason that in our analysis, the mediating channel of cash holdings between EPU and corporate leverage is significant in low-investment intensive firms only. Further, the results of control variables are maximum in line with the baseline results and prior literature.

4.4. Robustness test

This section reports various robustness tests to ensure our baseline findings are robust to outliers’ effect, variable measurement concerns, endogeneity concerns and sample-selection bias.

4.4.1. Excluding corporate leverage observations greater than one

Firstly, in our sample, the highest value of corporate leverage is 7.188, which is extraordinarily high. Following the prior literature, we exclude the firm-yearly observation where the corporate leverage value is more significant than one (M. Baker & Wurgler, Citation2002; Kayhan & Titman, Citation2007; Zhang et al., Citation2015). Following the same baseline empirical specification in Section 3.4 for stepwise regression analysis, the results are shown in Table . These results remain significant and align with baseline results—hence alleviating the effect of the outliers.

Table 4. Robustness checks 1 & 2: Excluding corporate leverage observations greater than one and alternate measure of cash holdings

4.4.2. Alternative cash holdings measure

To rule out the measurement concern about cash holding, we re-estimate our baseline results using alternate measures of cash holding. We calculate cash holdings with the ratio of cash and cash equivalent to the total sales. Following the same baseline empirical specification in Section 3.4, the result for stepwise regression analysis is shown in Table , Columns (4)–(6). Based on the alternate proxy of cash holdings, the results remain significant and consistent with our main results. Hence, mitigating the cash holdings measurement concern.

4.4.3. Alternative EPU measures

To rule out the measurement concern about the EPU, we re-estimate our baseline results using alternate proxies for EPU following prior literature. We use a three-component-based EPU index and GEPU index as alternate measurements of the U.S. news-based EPU index following (Fang et al., Citation2017; Gulen & Ion, Citation2016; Suh & Yang, Citation2021).Footnote15 We follow the exact baseline empirical specification in Section 3.4 for stepwise regression analysis. Table reports the results with alternative U.S. news-based EPU index measurements. The results for the three-component-based EPU index (3-ComponentEPU) and GEPU index are provided in Columns (1)–(3) and (4)–(6), respectively. The results using both alternative measures of EPU are significant and in line with baseline results, thus controlling for EPU measurement concerns.

Table 5. Robustness check 2: Alternative EPU measures

4.4.4. Robustness check for endogeneity concern

The U.S. EPU index might not be a strictly exogenous variable. There are possibly some common factors that affect U.S. firms’ corporate leverage, cash holdings, and the U.S. EPU index simultaneously. So, a possible reverse causal relationship of variables in all three equations of stepwise regression analysis leads to endogeneity concerns. To mitigate this issue, following Jumah, Younas and Al-Faryan (Citation2022), we use the Canadian EPU index as the instrumental variable for the U.S. EPU index and follow the two-stage least square (2SLS) estimation procedure.Footnote16 The first-stage regression results in Appendix D indicate the positive impact of the Canadian-EPU index on the U.S. news-based EPU index. Whereas in the second stage, predicted EPU from the first stage is employed in baseline stepwise regression specification, as shown in Section 3.4. The results for the second stage, shown in Table , Columns (1)–(3), are significant and in line with baseline results, mitigating the endogeneity concern.

Table 6. Robustness checks 3 and 4: Mitigating endogeneity concern and sample selection bias

4.4.5. Robustness check for sample selection bias

Next, another concern is that sample selection bias may influence the significant mediating channel of cash holdings between EPU and corporate leverage. Following the study, we conduct the propensity score matching (PSM) analysis to deal with this issue (R. Chen et al., Citation2017). PSM analysis aims to randomize the sample selection process by tallying firms with a cash holdings ratio above and below the sample’s median regarding observable firm characteristics. In the first stage, we use the probit model. To identify the matching probabilities, we regress a dummy variable set to value one if the firm cash holdings ratio exceeds the sample median and 0 otherwise, on profitability and ΔSales (growth opportunities). After that, we match firms with a cash holdings ratio above the sample’s median with firms with a cash holdings ratio below the sample’s median based on the closest propensity score drawn after the first stage. However, after this procedure, the overall sample size is decreased to 6,356 firm-year observations; but PSM analysis enables us to mitigate the selection bias. In the second stage, we re-estimate our baseline stepwise regression specification, as shown in Section 3.4, using the matched sample from the first stage of PSM analysis. The estimation of PSM analysis is shown in Table , Columns (4)–(6). These results are significant and consistent with our baseline results, therefore-alleviating sample selection bias concerns.

4.5. Additional test

Zhang et al. (Citation2015) provided evidence that EPU negatively impacts short-term and long-term leverage based on Chinese firms’ data. However, the significance is higher for the short-term leverage. The reason for more pronouncing results to short-term leverage shown by (Ding et al., Citation2020) is that, on average, short-term leverage is 69% of the total leverage in Chinese firms. However, based on our sample data descriptive results, in the U.S. firms listed at NYSE, about 83% of the total corporate leverage ratio consists of long-term leverage. Suppose we replace long-term and short-term leverage with total corporate leverage; in that case, it will be interesting to see whether the mediating effect of cash holdings between the EPU-leverage (Short and long term, respectively) relationship remains significant and equally promising. Also, is the effect of EPU equally impacting short-term and long-term leverage?

Using the baseline empirical specification in Section 3.4, we analyse by replacing the corporate leverage with short-term and long-term leverage to identify whether the role of the mediator remains significant using both measures of corporate leverage. In Table , the results for long-term and short-term leverage are provided in Columns (1)–(3) and (4)–(6), respectively. Overall, cash holdings have a significant partial mediating effect between EPU and leverage (both long- and short-term leverage). Further, in Column (3), the effect of EPU on long-term leverage is 0.010, which proposes that the mediating effect of the cash holdings is measured as (0.009821) – (0.008826) = 0.00099, accounting for an 11.21% increase in the EPU effect on long-term leverage. Whereas in Column (6), the effect of EPU on short-term leverage is 0.004, which suggests that the mediating effect of the cash holdings is measured as (0.004343) – (0.003912) = 0.00043, accounting for a 10.99% increase in the EPU effect on short-term leverage.Footnote17 Conclusively, the mediating effect of cash holdings on the relationship between EPU and corporate leverage (based on short term and long term) is approximately equally pronounced in relative magnitude.

Table 7. Additional test: Substituting long-term and short-term leverage with total leverage

Moreover, the direct impact of EPU on short-term and long-term leverage is significant and positive in Columns (1) and (4), respectively. However, the magnitude of the EPU effect is more promising for long-term leverage. These results are precisely the opposite of the study of Zhang et al. (Citation2015). Chinese firms face financial constraints during high EPU (Zhang et al., Citation2015); on average, short-term leverage in Chinese firms is 69% of their total leverage (Ding et al., Citation2020). Contrary to this, based on our sample data descriptive results, about 83% of the total corporate leverage ratio consists of long-term leverage. Also, firms listed at NYSE are less vulnerable to financial constraints (Yang et al., Citation2009). Hence, our results are opposite to the study (Zhang et al., Citation2015).

5. Conclusion

Economic policy uncertainty impacts corporate financial decisions due to rapid fluctuation in economic policies, and firms need to adjust their financing and investment decision. This study shows that during high EPU, the corporate leverage of U.S. non-financial firms listed at NYSE increases. Which means that firms resort to debt financing during uncertainty as the equity investors seek excessive risk premiums during high uncertainty; thus, the equity financing becomes more expensive (Pástor & Veronesi, Citation2013). However, the relationship between EPU and leverage is multifaceted. During high EPU, cash holdings also increase, which mediates the EPU and leverage relationship, accounting for a 10.72% increase in firm leverage. These results show that changes in cash holdings partially explain the impact of EPU on a firm’s leverage decision. The mediating effect of cash holdings between EPU and leverage remains significant even after dealing with the endogeneity and sample selection bias. Hence, our study’s hypothesis accepted that cash holdings mediate the EPU and leverage relationship. We also find that the mediating effect is only significant in low-investment-intensive firms. Since high-investment-intensive firms are usually large and face lesser financial constraints than low-investment-intensive firms (An et al., Citation2016). In an additional analysis, we provide evidence that the mediating effect of cash holdings remains significant based on long- and short-term leverage.

On theoretical grounds, our results align with the agency theory that increasing corporate leverage due to rising cash holdings is related to agency problem mitigation. Due to high EPU corporate cash holdings increases, which leads to the agency problem as managers use that cash for their own benefits. However, an increase in debt financing forces managers to utilize firm’s resources cautiously to avoid the default risk and to maintain firm creditworthiness. Further, on empirical grounds, we specify the novel evidence that cash holdings have a significant and partial mediating effect on the EPU-leverage relationship. Also, our study augments the empirical literature on the relationship between uncertainty and leverage and shows that this relationship is multifaceted and complex. Last, our analysis shows that during high EPU NYSE listed firms prefer debt financing over equity financing, confronting the debt market supply hypothesis and accepting the equity-market supply hypothesis aligned with previous literature (Bajaj et al., Citation2021; Schwarz & Dalmácio, Citation2020).

The policy implication based on our empirical analysis is as follows. Policymakers should be aware of public and private firms’ challenges during high EPU. As we showed in the current study, firms have to adjust their financial decisions during high economic uncertainty. Our analysis recommends increasing debt financing to incentivize value-increasing decisions and mitigate agency problems by reducing the cost of free cash flows during high uncertainty. Understanding the relationship between EPU, firm cash holdings, and leverage can help managers make better financial decisions and mitigate risks associated with EPU. Also, policymakers should manage economic uncertainty to avoid external shocks that may force firms to adjust their financial decision-making.

The results of this study are based on non-financial firms listed at NYSE, which may limit the generalization of the results to other types of firms or stock exchanges. Also, we only examine the role of cash holdings that impact the corporate leverage decision during high EPU and does not consider other factors that may impact corporate financial decisions. Future research studies may analyse similar studies on financial firms to examine the impact of EPU on their financial decisions. Also, conducting a cross-country analysis to examine the impact of EPU on financial decisions in different economic and cultural contexts can be a valuable extension of the literature.

Disclosure statement

No potential conflict of interest was reported by the authors.

Data availability statement

The data used in this study was obtained from Thomson EIKON Datastream (URL https://eikon.thomsonreuters.com), a paid data provider and (URL: http://www.policyuncertainty.com/index.html) am open source data.

Additional information

Notes on contributors

Zahid Jumah

Zahid Jumah is a Data Management Professional and a PhD candidate at the NUST Business School, National University of Sciences and Technology (NUST), Islamabad, Pakistan. He obtained his M. Com in Finance from the Federal Urdu University of Arts Science and Technology, Islamabad, Pakistan and MS Finance with distinction from Bahria University Islamabad, Pakistan. His area of interest is economic uncertainty, corporate finance and corporate diversification.

Zahid Irshad Younas

Dr. Zahid Irshad Younas is an expert academic with experience of more than ten years in teaching and research. Previously, he has served as an Assistant Professor at the Department of Finance Investment (NUST Business School, Islamabad) from 2017 to 2022. He has also served as a lecturer in Accounting and Finance at the Department of Economics GC University, Lahore from 2008 to 2014. He obtained his PhD in Finance from Kassel Universität, Germany. He has published several research papers in well-reputed and indexed journals. He is also a member of the reviewers’ board at the Journal of Global Responsibility launched by Leeds Business School, UK.

Nabeel Safdar

Dr. Nabeel Safdar is an accomplished assistant professor specializing in Business Management and Finance. He obtained his Ph.D. from the University of International Business and Economics, where he was awarded the prestigious Chinese Scholarship Council (CSC) scholarship. With a strong academic background, Dr. Safdar received several accolades during his studies, including the Campus Gold Medal and the Institute Gold Medal for his outstanding performance in the Master of Business Administration program at COMSATS Institute of Information Technology. Renowned for his research contributions, he has published numerous articles in esteemed journals, focusing on topics such as corporate governance, corporate social responsibility, and international migration.

Mamdouh Abdulaziz Saleh Al-Faryan

Mamdouh Abdulaziz Saleh Al-Faryan, a visiting Researcher at the University of Portsmouth, school of accounting, economics and finance, faculty of business and law. Mamdouh is a member of forty national and international professional associations. He has worked tirelessly to expand his experience and financial acumen, which would guide him down the path into leadership and higher level of responsibility. So far, he has several publications in the field of economics, finance, corporate governance, and accounting, which have been published in top international journals. Mamdouh also serves as a reviewer for a number of international journals and holds academic and research distinction.

Notes

1. NYSE is an abbreviation of “New York Stock Exchange”.

2. The reason for taking data since 1995 is the maximum availability of firm-level data at the THOMSON REUTERS EIKON database.

3. Data for the news-based EPU index collected from the following web source; https://www.policyuncertainty.com/index.html.

4. The four-digit Standard Industrial Classification Codes are used for industrial categorization according to business activity.

5. News-based EPU and three-component EPU indexes were developed by (S. R. Baker et al., Citation2016), whereas the GEPU index developed by (Davis, Citation2016). Detail construction and data for these indexes are available at the same link provided in footnote 3.

6. Following Akron et al. (Citation2020), in Figure , we have shown the graphical representation of policy uncertainty indexes without taking the natural logarithm. However, in Figures , we use the natural logarithm of EPU measures to show its graphical representation with corporate leverage and cash holdings.

7. Since the EPU index has only time variation, results would be biased if we add year fixed-effects. Thus, adding firm-fixed effects only. See, for example (Bermpei et al., Citation2021).

8. In descriptive statistics, the mean value of short-term leverage is far below long-term leverage, which shows that long-term leverage has a significant portion of total firm leverage on average.

9. The mean value of the total long-term debt to total debt ratio is 83.11%, based on descriptive statistics.

10. The results tables show the results with three digits after the decimal point. However, we use six digits after the decimal points for main variables, including dependent, independent, and mediating variable estimates to calculate the mediation effect in footnote 11.

11. The mediating effect can be calculated by -

. Also, to calculate the mediating effect in percentage, we follow this method ((

-

)/

)), i.e., ((0.015095–0.013633)/(0.013633)) = 10.72%. See, for example (S. Chen et al., Citation2021; Zhou et al., Citation2021), for using the same method for mediation effect calculation.

12. We measure the capital expenditure ratio by dividing the total capital expenditure of a firm by its total asset following (Gulen & Ion, Citation2016).

13. In Columns (1) and (4), EPU positively and significantly impacts the corporate leverage in low and high-investment-intensive firms. However, the impact is more pronounced for high-investment-intensive firms, as large firms tend to have higher leverage.

14. The mediating effect of cash holdings on the relationship between EPU & corporate leverage is calculated as follows; ((0.012432–0.010341)/(0.010341)) = 20.20%

15. Both indexes are briefly explained in Section 3.2.2.

16. We utilize the Canadian EPU index as an instrumental variable because the long-ranging economic ties between the two countries instituted a resilient economic relationship. Thus, the economic shock affecting the US EPU may also impact the Canadian EPU index.

17. The mediating effect of cash holdings between EPU & corporate leverage (both long- & short-term leverage) relationship is calculated as follows; for long-term leverage ((0.009821–0.008826)/(0.008826)) = 11.21% and for short-term leverage; ((0.004343–0.003912)/(0.003912)) = 10.99%

References

- Akron, S., Demir, E., Díez-Esteban, J. M., & García-Gómez, C. D. (2020). Economic policy uncertainty and corporate investment: Evidence from the U.S. hospitality industry. Tourism Management, 77(October 2019), 104019. https://doi.org/10.1016/j.tourman.2019.104019

- An, H., Chen, Y., Luo, D., & Zhang, T. (2016). Political uncertainty and corporate investment: Evidence from China. Journal of Corporate Finance, 36(2014), 174–28. https://doi.org/10.1016/j.jcorpfin.2015.11.003

- Asimakopoulos, P., Asimakopoulos, S., & Li, X. (2023). The combined effects of economic policy uncertainty and environmental, social, and governance ratings on leverage. European Journal of Finance, 1–23. https://doi.org/10.1080/1351847X.2022.2150559

- Athari, S. A., & Bahreini, M. (2022). Does economic policy uncertainty impact firms’ capital structure policy? Evidence from Western European economies. Environmental Science and Pollution Research, 30(13), 37157–37173. https://doi.org/10.1007/s11356-022-24846-0

- Bajaj, Y., Kashiramka, S., & Singh, S. (2021). Economic policy uncertainty and leverage dynamics: Evidence from an emerging economy. International Review of Financial Analysis, 77(May), 101836. https://doi.org/10.1016/j.irfa.2021.101836

- Baker, S. R., Bloom, N., & Davis, S. J. (2016). Measuring economic policy uncertainty. The Quarterly Journal of Economics, 131(4), 1593–1636. https://doi.org/10.1093/qje/qjw024

- Baker, M., & Wurgler, J. (2002). Market timing and capital structure. The Journal of Finance, 57(1), 1–32. https://doi.org/10.1111/1540-6261.00414

- Bates, T. W., Kahle, K. M., & Stulz, R. M. (2009). Why do U.S. firms hold so much more cash than they used to? The Journal of Finance, 64(5), 1985–2021. https://doi.org/10.1111/j.1540-6261.2009.01492.x

- Benkraiem, R., Lakhal, F., & Zopounidis, C. (2020). International diversification and corporate cash holdings behavior: What happens during economic downturns? Journal of Economic Behavior and Organization, 170(xxxx), 362–371. https://doi.org/10.1016/j.jebo.2019.12.016

- Bermpei, T., Kalyvas, A. N., Neri, L., & Russo, A. (2021). Does economic policy uncertainty matter for financial reporting quality? Evidence from the United States. Review of Quantitative Finance & Accounting, 58(2), 795–845. https://doi.org/10.1007/s11156-021-01010-2

- Chen, R., El Ghoul, S., Guedhami, O., & Wang, H. (2017). Do state and foreign ownership affect investment efficiency? Evidence from privatizations. Journal of Corporate Finance, 42, 408–421. https://doi.org/10.1016/j.jcorpfin.2014.09.001

- Cheng, C. H. J., Chiu, C. W.Hankins, W. B., & Stone, A. L. (2018). Partisan conflict, policy uncertainty and aggregate corporate cash holdings. Journal of Macroeconomics, 58(August), 78–90. https://doi.org/10.1016/j.jmacro.2018.08.010

- Chen, P. F., Lee, C. C., & Zeng, J. H. (2019). Economic policy uncertainty and firm investment: Evidence from the U.S. market. Applied Economics, 51(31), 3423–3435. https://doi.org/10.1080/00036846.2019.1581909

- Chen, S., Wang, Y., Albitar, K., & Huang, Z. (2021). Does ownership concentration affect corporate environmental responsibility engagement? The mediating role of corporate leverage. Borsa Istanbul Review, 21, S13–S24. https://doi.org/10.1016/j.bir.2021.02.001

- Davis, S. (2016). An index of global economic policy uncertainty. National Bureau of Economic Research. (22740). https://doi.org/10.3386/w22740

- Demir, E., & Ersan, O. (2017). Economic policy uncertainty and cash holdings: Evidence from BRIC countries. Emerging Markets Review, 33, 189–200. https://doi.org/10.1016/j.ememar.2017.08.001

- Demir, E., Gozgor, G., Lau, C. K. M., & Vigne, S. A. (2018). Does economic policy uncertainty predict the Bitcoin returns? An empirical investigation. Finance Research Letters, 26(January), 145–149. https://doi.org/10.1016/j.frl.2018.01.005

- Ding, N., Bhat, K., & Jebran, K. (2020). Debt choice, growth opportunities and corporate investment: Evidence from China. Financial Innovation, 6(1), 1–22. https://doi.org/10.1186/s40854-020-00194-1

- Dittmar, A., & Mahrt-Smith, J. (2007). Corporate governance and the value of cash holdings. Journal of Financial Economics, 83(3), 599–634. https://doi.org/10.1016/j.jfineco.2005.12.006

- Dittmar, A., Mahrt-Smith, J., & Servaes, H. (2003). International corporate governance and corporate cash holdings. The Journal of Financial and Quantitative Analysis, 38(1), 111. https://doi.org/10.2307/4126766

- Fang, L., Yu, H., & Li, L. (2017). The effect of economic policy uncertainty on the long-term correlation between U.S. stock and bond markets. Economic Modelling, 66(June), 139–145. https://doi.org/10.1016/j.econmod.2017.06.007

- Feng, X., Lo, Y. L., & Chan, K. C. (2019). Impact of economic policy uncertainty on cash holdings: Firm-level evidence from an emerging market. Asia-Pacific Journal of Accounting and Economics, 1–23. https://doi.org/10.1080/16081625.2019.1694954

- Frésard Laurent, L., & Salva, C. (2010). The value of excess cash and corporate governance: Evidence from U.S. cross-listings. Journal of Financial Economics, 98(2), 359–384. https://doi.org/10.1016/j.jfineco.2010.04.004

- Gulen, H., & Ion, M. (2016). Policy uncertainty and corporate investment. Review of Financial Studies, 29(3), 523–564. https://doi.org/10.1093/rfs/hhv050

- Harford, J., Mansi, S. A., & Maxwell, W. F. (2012). Corporate governance and firm cash holdings in the U.S. Corporate Governance: Recent Developments and New Trends, 9783642315, 107–138. https://doi.org/10.1007/978-3-642-31579-4_5

- Hu, S., & Gong, D. (2019). Economic policy uncertainty, prudential regulation and bank lending. Finance Research Letters, 29(August), 373–378. https://doi.org/10.1016/j.frl.2018.09.004

- Ilyas, M., Khan, A., Nadeem, M., & Suleman, M. T. (2021). Economic policy uncertainty, oil price shocks and corporate investment: Evidence from the oil industry. Energy Economics, 97, 105193. https://doi.org/10.1016/j.eneco.2021.105193

- Im, H. J., Kang, Y., & Shon, J. (2020). How does uncertainty influence target capital structure? Journal of Corporate Finance, 64(December 2018), 101642. https://doi.org/10.1016/j.jcorpfin.2020.101642

- Istiak, K., & Serletis, A. (2018). Economic policy uncertainty and real output: Evidence from the G7 countries. Applied Economics, 50(39), 4222–4233. https://doi.org/10.1080/00036846.2018.1441520

- Istiak, K., & Serletis, A. (2020). Risk, uncertainty, and leverage. Economic Modelling, 91(May), 257–273. https://doi.org/10.1016/j.econmod.2020.06.010

- Jensen, M. C. (1986). Agency costs of free cash flow, corporate finance. American Economic Review, 76(2), 323–329.

- Jensen, N., & Meckling, W. (1976). Theory of the firm: Managerial behavior, agency costs, and capital structure. Journal of Financial Economics, 3(4), 305–360. https://doi.org/10.1016/0304-405X(76)90026-X

- Jumah, Z., Younas, Z. I., & Al-Faryan, M. A. S. (2022). Economic policy uncertainty, corporate diversification, and corporate investment. Applied Economics Letters, 1–11. https://doi.org/10.1080/13504851.2022.2106028

- Kayhan, A., & Titman, S. (2007). Firms’ histories and their capital structures. Journal of Financial Economics, 83(1), 1–32. https://doi.org/10.1016/j.jfineco.2005.10.007

- Khan, M. A., Qin, X., & Jebran, K. (2020). Uncertainty and leverage nexus: Does trade credit matter? Eurasian Business Review, 10(3), 355–389. https://doi.org/10.1007/s40821-020-00159-5

- Kido, Y. (2016). On the link between the U.S. economic policy uncertainty and exchange rates. Economics Letters, 144, 49–52. https://doi.org/10.1016/j.econlet.2016.04.022

- Kieschnick, R., & Moussawi, R. (2018). Firm age, corporate governance, and capital structure choices. Journal of Corporate Finance, 48, 597–614. https://doi.org/10.1016/j.jcorpfin.2017.12.011

- Kim, C.-S., Mauer, D. C., & Sherman, A. E. (1998). The determinants of corporate liquidity: Theory and evidence. The Journal of Financial and Quantitative Analysis, 33(3), 335. https://doi.org/10.2307/2331099

- Lee, C. C., Lee, C. C., Zeng, J. H., & Hsu, Y. L. (2017). Peer bank behavior, economic policy uncertainty, and leverage decision of financial institutions. Journal of Financial Stability, 30, 79–91. https://doi.org/10.1016/j.jfs.2017.04.004

- Lemmon, M. L., Roberts, M. R., & Zender, J. F. (2008). Back to the beginning: Persistence and the cross-section of corporate capital structure. The Journal of Finance, 63(4), 1575–1608. https://doi.org/10.1111/j.1540-6261.2008.01369.x

- Li, X. (2019). Economic policy uncertainty and corporate cash policy: International evidence. Journal of Accounting and Public Policy, 38(6), 106694. https://doi.org/10.1016/j.jaccpubpol.2019.106694

- Li, F., Liang, T., & Zhang, H. (2021). Does economic policy uncertainty affect cross-border M&As? —— a data analysis based on Chinese multinational enterprises. International Review of Financial Analysis, 73, 101631. https://doi.org/10.1016/j.irfa.2020.101631

- Li, X. M., & Qiu, M. (2021). The joint effects of economic policy uncertainty and firm characteristics on capital structure: Evidence from U.S. firms. Journal of International Money and Finance, 110, 102279. https://doi.org/10.1016/j.jimonfin.2020.102279

- Liu, Y., Li, J., Liu, G., & Lee, C.-C. (2021). Economic policy uncertainty and firm’s cash holdings in China: The key role of asset reversibility. Journal of Asian Economics, 74, 101318. https://doi.org/10.1016/j.asieco.2021.101318

- Liu, G., & Zhang, C. (2020). Economic policy uncertainty and firms’ investment and financing decisions in China. China Economic Review. https://doi.org/10.1016/j.chieco.2019.02.007

- Liu, L., & Zhang, T. (2015). Economic policy uncertainty and stock market volatility. Finance Research Letters, 15, 99–105. https://doi.org/10.1016/j.frl.2015.08.009

- Loncan, T. (2020). Foreign institutional ownership and corporate cash holdings: Evidence from emerging economies. International Review of Financial Analysis, 71(December), 101295. https://doi.org/10.1016/j.irfa.2018.12.003

- Lv, M., & Bai, M. (2019). Political uncertainty and corporate debt financing: Empirical evidence from China. Applied Economics, 51(13), 1433–1449. https://doi.org/10.1080/00036846.2018.1527455

- Makololo, P., & Seetharam, Y. (2020). The effect of economic policy uncertainty and herding on leverage: An examination of the BRICS countries. Cogent Economics & Finance, 8(1), 1821482. https://doi.org/10.1080/23322039.2020.1821482

- Menéndez-Alonso, E. J. (2003). Does diversification strategy matter in explaining capital structure? Some evidence from Spain. Applied Financial Economics, 13(6), 427–430. https://doi.org/10.1080/09603100210150930

- Myers, S. C. (1984). The capital structure puzzle. The Journal of Finance, 39(3), 575. https://doi.org/10.2307/2327916

- Pan, W. F., Wang, X., & Yang, S. (2019). Debt maturity, leverage, and political uncertainty. The North American Journal of Economics & Finance, 50(November 2018), 100981. https://doi.org/10.1016/j.najef.2019.04.024

- Pástor, Ľ., & Veronesi, P. (2013). Political uncertainty and risk premia. Journal of Financial Economics, 110(3), 520–545. https://doi.org/10.1016/j.jfineco.2013.08.007

- Phan, H. V., Nguyen, N. H., Nguyen, H. T., & Hegde, S. (2019). Policy uncertainty and firm cash holdings. Journal of Business Research, 95(March 2018), 71–82. https://doi.org/10.1016/j.jbusres.2018.10.001

- Pinkowitz, L., Stulz, R., & Williamson, R. (2006). Does the contribution of corporate cash holdings and dividends to firm value depend on governance? A cross-country analysis. The Journal of Finance, 61(6), 2725–2751. https://doi.org/10.1111/j.1540-6261.2006.01003.x

- Preacher, K. J., & Kelley, K. (2011). Effect size measures for mediation models: Quantitative strategies for communicating indirect effects. Psychological Methods, 16(2), 93–115. https://doi.org/10.1037/a0022658

- Prüser, J., & Schlösser, A. (2020). The effects of economic policy uncertainty on European economies: Evidence from a TVP-FAVAR. Empirical Economics, 58(6), 2889–2910. https://doi.org/10.1007/s00181-018-01619-8

- Rosenbaum, P. R., & Rubin, D. B. (1983). The central role of the propensity score in observational studies for causal effects. Biometrika, 70(1), 41–55. https://doi.org/10.1093/biomet/70.1.41

- Schwarz, L. A. D., & Dalmácio, F. Z. (2020, June). The relationship between economic policy uncertainty and corporate leverage: Evidence from Brazil. Finance Research Letters, 40, 101676. https://doi.org/10.1016/j.frl.2020.101676

- Sobel, M. E. (1982). Asymptotic confidence intervals for indirect effects in structural equation models. Sociological Methodology, 13, 290. https://doi.org/10.2307/270723

- Suh, H., & Yang, J. Y. (2021). Global uncertainty and global economic policy uncertainty: Different implications for firm investment. Economics Letters, 200, 109767. https://doi.org/10.1016/j.econlet.2021.109767

- Su, X., Zhou, S., Xue, R., & Tian, J. (2020). Does economic policy uncertainty raise corporate precautionary cash holdings? Evidence from China. Accounting and Finance, 60(5), 4567–4592. https://doi.org/10.1111/acfi.12674

- Tabash, M. I., Farooq, U., Ashfaq, K., & Tiwari, A. K. (2022). Economic policy uncertainty and financing structure: A new panel data evidence from selected Asian economies. Research in International Business and Finance, 60(October 2021), 101574. https://doi.org/10.1016/j.ribaf.2021.101574

- Wang, Y., Chen, C. R., & Huang, Y. S. (2014). Economic policy uncertainty and corporate investment: Evidence from China. Pacific Basin Finance Journal, 26, 227–243. https://doi.org/10.1016/j.pacfin.2013.12.008

- Xu, Z. (2019). Economic policy uncertainty, cost of capital, and corporate innovation. Journal of Banking & Finance, 105698. https://doi.org/10.1016/j.jbankfin.2019.105698

- Xu, N., Chen, Q., Xu, Y., & Chan, K. C. (2016). Political uncertainty and cash holdings: Evidence from China. Journal of Corporate Finance, 40, 276–295. https://doi.org/10.1016/j.jcorpfin.2016.08.007

- Yang, C. C., Baker, H. K., Chou, L. C., & Lu, B. W. (2009). Does switching from NASDAQ to the NYSE affect investment-cash flow sensitivity? Journal of Business Research, 62(10), 1007–1012. https://doi.org/10.1016/j.jbusres.2008.05.006

- Yu, H., Fang, L., Du, D., & Yan, P. (2017). How EPU drives long-term industry beta. Finance Research Letters, 22, 249–258. https://doi.org/10.1016/j.frl.2017.05.012

- Zhang, G., Han, J., Pan, Z., & Huang, H. (2015). Economic policy uncertainty and capital structure choice: Evidence from China. Economic Systems, 39(3), 439–457. https://doi.org/10.1016/j.ecosys.2015.06.003

- Zhao, X., Lynch, J. G., & Chen, Q. (2010). Reconsidering Baron and Kenny: Myths and truths about mediation analysis. Journal of Consumer Research, 37(2), 197–206. https://doi.org/10.1086/651257

- Zhou, M., Li, K., & Chen, Z. (2021). Corporate governance quality and financial leverage: Evidence from China. International Review of Financial Analysis, 73(October 2020), 101652. https://doi.org/10.1016/j.irfa.2020.101652

Appendix A.

The number of firms from each sector in our data sample

Number of firms from each sector (summary of sample composition)

Appendix B.

Variable definitions

Variable definitions

Appendix C.

Pairwise correlation matrix among dependent, independent, mediator and control variables

Pairwise correlation matrix

Appendix D.

Estimation of First Stage 2SLS

First-Stage 2SLS (two-stage least square)