?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

This paper analyzes the contribution of foreign direct investment (FDI) to economic growth in Côte d’Ivoire, for the period 1980–2019. We use the World Development Indicators (World Bank) database. The Autoregressive Distributed Lag (ARDL) cointegration approach results show that, in the short and long-run, FDI negatively impacts economic growth in Côte d’Ivoire. We conjecture that these results are due to the predominance of extractive FDI in Côte d’Ivoire. Indeed, the extractive sector is weakly linked to the national economy and is subject to practices of fraud and corruption. Our results also show the importance of education (human capital) in the country’s economic growth. All of these findings suggest the need for selective FDI attraction policies, the integration of the enclave extractive sector into the national economy and the strengthening of the education system for a more efficient human capital capable of absorbing and using new knowledge and high technologies transferred by FDI.

PUBLIC INTEREST STATEMENT

Foreign direct investment (FDI) has always been considered a source of economic growth. However, the main results of this study covering the period 1980–2019 show that in Côte d’Ivoire, FDI has a negative effect on growth in the short and long term. We speculate that these results are explained by the predominance of extractive FDI. Indeed, the extractive sector remains fundamentally enclave, weakly linked to the economies of developing countries and often exposed to many corrupt practices. We have proposed policies to attract appropriate FDI and to strengthen the Ivorian education system.

1. Introduction

The issue of the contribution of the FDI to economic growth, especially in developing countries (DCs), is a much-discussed topic in the economic literature. The theory considers that FDI stimulates economic growth through new practices and technology transfer, increased knowledge and capital stock, total factor productivity and consumption (Dunning, Citation1973; Fischer et al., Citation1998; King & Levine, Citation1993). These assumptions, sometimes controversial by empirical results (see, for example, Artus & Cartapanis, Citation2008; Ekodo et al., Citation2020; Rogoff, Citation2003), have served as a basis for economic policies of attraction of FDI (Bosworth & Collins, Citation1999; Mainguy, Citation2004; Mughal & Vechiu, Citation2015). Empirical controversies have prompted some DCs to express their concerns about the economic, social and political consequences of foreign investments. They fear to cede important sectors of their economy to foreign interests, which seek only the maximization of their profits. Then, they impose restrictions on the entry of private capital including the tightening of laws governing conditions for the establishment and operation of foreign-owned enterprises, the screening and supervision of investors, restrictions on foreign ownership and control in certain sectors, requirements related to investments such as the minimum volume of R&D (Esso, Citation2005; Globerman & Shapiro, Citation2002; Golub, Citation2003). But all these restrictions did not curb the massive inflow of foreign capital. On the contrary, the net resources received by DCs have increased from 52 billion up to 95 billion US dollars constant between 1970 and 1982 to reach 1,223 billion US dollars in 2007 (BCEAO, Citation2013). In 2019, they amounted to US$ 1,540 billion before falling below US$ 1,000 billion in 2020 due to the coronavirus (COVID−19) crisis (CNUCED, Citation2020).

In Côte d’Ivoire, especially with the promotion instruments and attraction of foreign capital, there has been a substantial increase in the level of investments and the creation and restructuring of businesses (Ahouré, Citation2009). The country attracts almost half of FDI in the area of West African Economic and Monetary Union (WAEMU). It is followed by Senegal and Mali which, respectively, benefit from 19% and 17% (Kinda, Citation2008). However, the attraction of FDI by Côte d’Ivoire has not always been linear. It was at times hampered by changes in the economic environment of the 1980s and the various politico-military crises. The evolution in FDI has suffered the same shocks of economic and political instability as the country’s economic growth movement (FMI, Citation2000). Indeed, the growth rate which was around 4% after independence until the end of the 1970s experienced successive periods of slowdown and recovery from the 1980s until the 2000s. Since 2012, growth has resumed due to the regained stability. The country adopted new investment codes and numerous structural reforms. One of the major reforms is the reduction to 15,000 Franc CFAFootnote1 of the cost of setting up a limited liability company (LLC) with a capital less than or equal to 10 million Franc CFA. These reforms have helped attract even more foreign capital. In 2018, Côte d’Ivoire recorded US$ 913 million in foreign investment (CNUCED, Citation2019b) and about US$ 1 billion in 2019 (CNUCED, Citation2020).

According to FMI (Citation2016), the significant growth recorded by Côte d’Ivoire since 2012 can be explained by the volume of public and private investment. However, to our knowledge, no recent rigorous empirical study confirms the positive effects of FDI on economic growth in Côte d’Ivoire. The work of Esso (Citation2005, Citation2010) using econometric tools (cointegration tests, OLS and Toda-Yamamoto causality tests) shows that FDI causes economic growth without demonstrating a direct relationship between the two variables for the periods 1970–2001 and 1970–2007. As for Pokou (Citation2005), he uses Jo-Hansen cointegration and Granger causality tests and results in an absence of causality between FDI and growth over the period 1975–2002. Finally, Johnston and Ramirez (Citation2015) use an error correction model and show a negative effect of FDI on Ivorian economic growth for the period 1975–2011. These authors explain this unexpected effect by the large repatriation of profits and dividends generated by FDI. Therefore, the empirical literature remains controversial about the real effect of foreign capital on economic growth, especially when the host country is an African DC.

The objective of this paper is to investigate empirically the nature of the relationship between economic growth and FDI in Côte d’Ivoire. Do FDI inflows directly contribute to the economic growth of Côte d’Ivoire? To address this concern, we use an ARDL cointegrating econometric approach and time series of FDI inflows and national income growth rates for the period 1980–2019. We also include other variables such as trade openness, savings, education, inflation and infrastructure. Our results show that in the short- and long-run, FDI negatively impacts economic growth in Côte d’Ivoire. This result can be explained in large part by the nature of inward FDI flows, which are mainly dominated by extractive FDI, the effects of which are poorly connected to the national economy. The results also highlight the importance of education (human capital) in the country’s economic growth. All of these results suggest the need for selective FDI attraction policies, the integration of the enclave extractive sector into the national economy and finally the strengthening of human capital training policies.

The contributions of this study can be summarized in two points. The first is at the methodological level. In fact, in addition to the classic Dickey and Fuller (Citation1981) and Phillips and Perron (Citation1988) unit root tests, we use the Zivot and Andrews (Citation1992) unit root test which considers the presence of an endogenous structural break in the series to refine our analyses. In addition, to verify the long-run relationship between the study series, we use a more robust technique of cointegration analysis, the ARDL bound test approach developed by Pesaran et al. (Citation2001) and adapted to small samples. Finally, we estimate from a dynamic unrestricted error correction model. The second contribution is at the level of the analysis of the results. Indeed, the negative impact of FDI on the economic growth in Côte d’Ivoire is consistent with the results already obtained by Johnston and Ramirez (Citation2015) over the period 1975–2011. However, our analyses of this result have the merit of initiating a more global reflection on the real contribution of the extractive sector to the economy of Côte d’Ivoire in particular and West African countries in general.

The remainder of this paper is organized as follows: Section 1 presents a review of the theoretical and empirical literature on the relationship between FDI and economic growth. Section 2 describes the evolution of FDI in Côte d’Ivoire. Section 3 discusses the methodological framework. Section 4 presents the empirical results and interpretations. We conclude the paper in Section 5.

2. Literature review

2.1. Theoretical arguments

The theoretical economic literature identifies three ways that FDI can promote economic growth (Ajayi, Citation2006). The first is the release of national savings constraints, especially in DCs where local savings are insufficient. Indeed, private external capital flows and accumulation help to fill the existing financial gap and to develop the financial market of the host country (Ajayi, Citation2004; King & Levine, Citation1993). The second is that FDI is the main access instrument for technology transfer from the developed world to the host country (Mensah & Mensah, Citation2021). FDI contributes to added value through productivity gains generated by technology transfers to local businesses. The transmission of innovative best practices and induced spillovers are at the heart of endogenous growth theory (Borensztein et al., Citation1998; De Mello, Citation1997; Grossman & Helpman, Citation1991; Romer, Citation1990). The third way is that FDI induces an increase in exports resulting from increased capacities and greater competition in domestic production (Alaya et al., Citation2009; Dunning, Citation1973; Miah & Majumder, Citation2022).

In addition, according to economic theory, FDI is generally motivated by two types of factors, push factors and pull factors (Ajayi, Citation2004). The push factors are related to growth and financial market conditions in the industrial country. The pull factors are rather linked to macroeconomic policies and to characteristics of the recipient country (such as market size, costs and quality of workforce, tax incentives, quality of public infrastructure, transaction costs, technological level) (Alaya et al., Citation2009; Dembelé & Machrafi, Citation2021). The pull factors determine the distribution of FDI among countries and characterize the absorptive capacity of the recipient country.

Finally, we note that FDI present some negative effects. According to the literature, negative effects are often inevitable and result from distortions and inadequacies of the national economy (Akinlo, Citation2004; Sun, Citation2002). Three negative effects of FDI are identified. First, the crowding-out effect, which can arise when foreign investors take advantage of opportunities instead of local investors. Secondly, FDI can create an imbalance of payments balance due to the repatriation of profits outward. Third, FDI can lead to enclave economies or sectors, which have poor connection and effect with and on the national economy. This is especially true in the mining and extractive industry, which requires heavy capital investment but a small local workforce. This is also true for African’s Export Processing Zones (EPZs) (which receive special concessions and privileges from the host country), although recent studies such as Majumder et al. (Citation2022) show that FDI accelerates EPZs exports and promotes job creation.

2.2. Empirical background

In the empirical literature, the positive impact of FDI on domestic investment and economic growth is controversial. While some authors confirm this positive link, others, on the contrary, maintain that FDI inflows have negative or counterproductive effects on the performance of productive units and growth.

Among supports of the positive effects of FDI on growth, we have Williams and Williams (Citation1999), Brana (Citation1999), Bosworth and Collins (Citation1999), Mainguy (Citation2004), Bouoiyour and Toufik (Citation2007), Diaw and Lessoua (Citation2013), Bouyacoub and Bouyacoub (Citation2017), Nkoa (Citation2016, Citation2018), Eka and Bouoiyour (Citation2020), Miah and Majumder (Citation2020) and Miah and Majumder (Citation2022). For example, Williams and Williams (Citation1999) analyze the relationship between FDI, investment and economic growth in the unified currency area of the Eastern Caribbean Central Banks. They show that FDI attracts gross investment and improves economic growth. Diaw and Lessoua (Citation2013) and Eka and Bouoiyour (Citation2020) analyze FDI from China and show the positive effect of foreign capital on the economic growth of sub-Saharan African countries, respectively, for the period from 1995 to 2009 and 2003 to 2017. Particularly, Eka and Bouoiyour (Citation2020) use a dynamic panel Generalized Method of Moments (GMM) and show that FDI has favored the creation of joint ventures between Chinese companies and local companies. Majumder and Rahman (Citation2020)’s results on China for the period 1982 to 2019 are in the same direction. The authors explain their results by the effects of local market size, cheap labor, good infrastructures and more open policies in favor of FDI. Nkoa (Citation2016) uses the GMM model and shows that FDI contribute to the industrialization and growth of Africa through the improvement of manufacturing added value and industrial sector employment in 53 countries for the period 1975–2014. The author suggests that African countries strengthen private investment and select FDI geared towards building infrastructure. Nkoa (Citation2018) also suggests the need for African countries to improve the quality of financial infrastructure, which is a source of significant improvement of FDI impacts on economic growth. The positive effect of FDI on growth is also demonstrated for countryrs in North Africa (see, for example, Bouyacoub & Bouyacoub, Citation2017). Finally, we note that many empirical works in favor of positive impacts of FDI insist on the channels of transmission of these impacts, in particular, positive externalities, technology diffusions, skills, capacities and marketing networks (see Bosworth & Collins, Citation1999; Bouoiyour & Toufik, Citation2007; Brana, Citation1999; Mainguy, Citation2004). For example, Miah and Majumder (Citation2022) analyze the impact of FDI on exports and employment in Bangladesh for the period 1972–2017 and 1991–2017, respectively. Their results show that, by pro- moting job creation and increasing the volume of exports, FDI has a positive impact on the country’s economic growth.

The studies showing no effect or negative effects of FDI on growth are also numerous (see Akinlo, Citation2004; Alvarado et al., Citation2017; Artus & Cartapanis, Citation2008; Bouoiyour et al., Citation2009; Busse et al., Citation2016; Caceres, Citation1995; Carbonell & Werner, Citation2018; Ekodo et al., Citation2020; Haddad & Harrison, Citation1993; Jackman, Citation1982; Kokko, Citation1994; Mapalad, Citation1998; Rogoff, Citation2003; Rothgeb, Citation1984; Van Huffez, Citation2001). For example, Mapalad (Citation1998) uses the double least-squares method and shows, in a study in the Philippines for the period 1952–1993, that foreign capital inflows have no direct effect on domestic savings and growth. According to the author, the most effective way to increase domestic savings in the Philippines is through rapid and sustained economic growth. Van Huffez (Citation2001) show that FDI generate budgetary difficulties, oblige local firms to strong competition and lead to a difficult technology adaptation. Caceres (Citation1995) carried out a study in four Central American countries (Costa Rica, Guatemala, Honduras and El Salvador) for the period from 1971 to 1985 and showed that external resources generate financial instabilities with no effect on economic growth. In a study on Nigeria, Akinlo (Citation2004), using an Error Correction Model, showed that extractive and manufacturing FDI did not improve economic growth from 1970 to 2001. The analysis by Artus and Cartapanis (Citation2008) using a dynamic model shows that the high international mobility of capital deprives the economy of any possibility of stabilizing production or inflation. The authors also point out that external savings transfers can exacerbate macroeconomic dilemmas and induce dynamic instability that can induce adjustment and slow growth. Bouoiyour et al. (Citation2009) use panel data from 63 countries in the Middle East and North Africa (MENA) for the period from 1960 to 2004. Their results show that FDI has no impact on the productivity and growth of countries. Busse et al. (Citation2016) use a Solow (Citation1956) growth model and panel data for the period 1991–2010 and show that FDI and aid from China do not affect growth in Africa. Alvarado et al. (Citation2017) examined the effect of FDI on economic growth in 19 Latin American countries. Using panel data econometrics, their results suggest that the effect of FDI on economic growth is not statistically significant in aggregate form. Indeed, the result varies according to the levels of development achieved by the countries. FDI has a positive and significant effect on growth in high-income countries, while in upper-middle-income countries the effect is insignificant. The effect in lower-middle-income countries is negative and statistically significant. The authors conclude that FDI is not an adequate mechanism to accelerate economic growth in Latin America, except in high-income countries. Carbonell and Werner (Citation2018) analyze the effect of FDI on growth in Spain, which is among the countries that receive the most FDI. Over the observation period 1984–2010, FDI flows increased significantly and Spain offered ideal conditions. However, these favorable Spanish conditions did not allow FDI to stimulate the country’s economic growth. Finally, in their recent study, Ekodo et al. (Citation2020) used the dynamic panel GMM method and showed that FDI, even combined with the control of corruption, have no significant effect on the economic growth of the Central African Economic and Monetary Community zone from 1996 to 2018.

3. Evolution of FDI in Côte d’Ivoire

Since its independence, Côte d’Ivoire has been adopting several institutional and structural reforms to attract foreign capital including the first private investment code in 1959, followed by several other investment codes, sectoral or not, in 1984, 1995, 2012 and 2018. The objective of these reforms was to adapt the regime of private investment to the economy, to promote local and foreign private investment. In particular, the 2012 investment code led to the creation of an investment promotion center (called CEPICI) and the establishment of an ’one-stop-shop’ for business creation, investment code, land industrial and administrative formalities. The 2018 revised version included the promotion of green and socially responsible investments, technology, research and innovation.

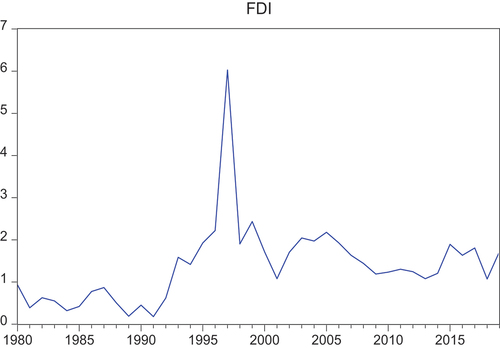

FDI inflows, whether in the form of loans, equity investments or joint ventures, have contributed to the wealth creation in Côte d’Ivoire. Figure shows the evolution of FDI as a percentage of GDP for the last 40 years (1980–2019) based on the data from the World Development Iindicators (WDI) (Citation2021).

Figure 1. Evolution of inward FDI flows in Côte d’Ivoire as % of GDP.

We note that FDI inflows contributed less than 1% of the GDP between 1980 and 1990. The share of FDI reached a peak of 6.02% of GDP in 1997. On the one hand, this is due to the devaluation of the Franc CFA in 1994, and, on the other hand, to the adoption of the private investment code of 1995 which sharply contributed to increasing inward FDI flows from US$ 211.48 million in 1995 to US$ 415.30 million in 1997. The downward trend that began in the early 2000s was caused by the military coup of 1999 and the multiple tensions and crises of the 2000s. Since the end of the crises in 2011, the economic recovery has vigorously started thanks to the strong mobilization of the government in favor of reconstruction. Since then, improving the business climate and promoting public–private partnerships has attracted foreign capital. The period from 2015 to 2019 thus saw a clear recovery in inward FDI flows with an annual average of US$ 675.07 million. The distribution of inward FDI by country of origin shows that in 2016, the first investors were African countries with 53.8%, followed by European countries with 22.9% of investment and Asia with 21% (CEPICI, Citation2016; Dembelé, 2021). However, France remains the leading foreign investor. It has around 39% of foreign assets in the country.

Finally, the sectoral breakdown of inward FDI in Cote d’Ivoire shows that FDI is mainly directed towards the extractive sector. Indeed, in his recent study, Keho (Citation2020) reports the distribution of FDI by sector as a percentage of total FDI inflows and indicates that the share of FDI in the manufacturing sector is decreasing in favor of the extractive sector (mining, hydrocarbons, distribution of petroleum products and energy). For the period from 2014 to 2017, the average share FDI in the extractive sector was 37.70%, while it represented 18.4% in the manufacturing sector (see Table ). CNUCED (Citation2019a), in a report on the review of investment policy in Côte d’Ivoire, confirms this trend for the year 2019 with 39.2% of the total FDI flow directed to the extractive sector. According to the report of ITIE (Citation2018), the stretch of West African coast that sprawls over more than a dozen countries in the Gulf of Guinea is a growing source of oil on world markets. The Ivorian oil fields are located in this gulf between Liberian and Ghanaian borders. The offshore zone, stretching from the coast up to 150 km, includes deposits with high potential. Côte d’Ivoire’s proven oil and gas reserves are estimated at 250 million barrels and 28.32 million cubic meters, respectively. The country also has significant mineral resources consisting of gold, iron, manganese, bauxite, nickel, cobalt, diamonds, and copper. These hitherto poorly exploited resources are now attracting a lot of foreign investment. Foreign companies, such as Ampella Mining Ivory Coast, Bondoukou Manganèse S.A, CNR international LDC, Foxtrot international LDC, Persus Mining Ivory Coast, and Semafo, are involved in the Ivorian extractive sector.

Table 1. Foreign direct investment by sectors (as share of total FDI inflows)

4. Research design

4.1. Data and variables

The series used in this study are macroeconomic data from World Development Indicators (World Bank) and cover the period from 1980 to 2019 (see the database in Appendix). The data processing, cointegration and causality test procedures as well as econometric estimations are implemented with the software EViews 9.0.

4.1.1. Dependant variable

The gross domestic product per capita, denoted GDPPC, is the dependent variable. We consider its natural logarithm form. Côte d’Ivoire is experiencing very contrasting phases of economic growth. The growth rate is linked to the economic crisis of the 1980s and to the various politico-military troubles.

4.1.2. Explanatory variables

We use two kinds of explanatory variables. The explanatory variable of interest is the flow of foreign direct investment (FDI), net inflows as a percentage of GDP. The other explanatory or control variables are the trade openness (TO), domestic savings (SAVE), education (EDUC), inflation (INFL) and infrastructure (INFR). The choice of these variables stems from the economic literature on the determinants of economic growth.

The trade openness rate is calculated as the sum of exports and imports of goods and services divided by GDP. It measures the country’s foreign trade. According to economic theory, trade openness by allowing increased imports of goods and services drive economic growth through investment (Levine & Renelt, Citation1992). Several empirical studies also confirm the causal link between trade openness and economic growth (see Frankel & Romer, Citation1999; Wacziarg & Welch, Citation2008). The gross domestic savings are calculated as a percentage of GDP. According to economic theory, the financing of healthy and sustainable economic growth depends on the mobilization of significant domestic savings (Aglietta, Citation1991). The education variable measures the access to secondary education as a percentage. It is the proxy of the level and quality of human capital in the country’s growth process. Indeed, a higher and better level of human capital increases the absorptive capacity of new technologies and decreases the cost of imitating ideas discovered elsewhere (Nelson and Phelps, Citation1966). The inflation variable is measured by the consumer price index as an annual percentage. Inflation or the general increase in prices deteriorates economic activity because it expresses the loss of the purchasing power of money. According to economic theory, the volatility of inflation negatively influences the rate of economic growth (Bruno & Musso, Citation2000). Finally, the proxy for the infrastructure variable is the number of telephone lines connected to a public network per 100 inhabitants. It represents telecommunication infrastructures that facilitate emission and transmission of information. The theoretical and empirical literature agree that adequate infrastructure attracts foreign capital and promotes economic growth (Barro, Citation1990; Kinda, Citation2008).

The variables description and summary statistics are, respectively, recorded in Tables . Education is the most volatile variable with regard to its standard deviation. It is followed by the trade openness, while the infrastructure variable is the least dispersed.

Table 2. Description of variables

Table 3. Summary statistics

4.2. Econometric model

The study aims to assess the contribution of FDI to economic growth in Côte d’Ivoire. The general model to be estimated is as follows:

with = 1980, 1981, 1982, … , 2019 ; a period of 40 years; et is the error term, .

4.2.1. Stationarity

The analysis of the stationarity of variables is important when one works with time series. Stationarity refers to the temporal constancy of time-series properties. For the analysis of the stationarity of our series, we use the Augmented Dickey and Fuller (Citation1981) test (or ADF test) and the Phillips and Perron (Citation1988) test (or PP test) as well as the Zivot and Andrews (Citation1992) test (or ZA test) which takes into account structural breaks of series. The ADF test is a parametric test based on the estimation of an autoregressive model. It is marked by an essential limit because the null hypothesis of the unit root assumes that the trend of the series does not change over the entire period. However, we know that a few one-off shocks can influence, even appreciably, the trend of the series. Thus, the ADF test is biased in favor of the null hypothesis (Perron, Citation1992; Perron, Citation1989; Rappoport & Reichlin, Citation1989). The PP test builds a nonparametric correction of the Dickey–Fuller statistic to take into account heteroscedastic errors. It is therefore reduced to the simple Dickey–Fuller test for homoscedastic errors. The implementation of the PP test is identical to that of the ADF test. However, the ADF and PP tests do not take ruptures into account. We use the unit root test of Zivot and Andrews (Citation1992) to capture structural breaks in the series. The ZA test offers a unit root test with endogenous rupture. It is based on the initial hypothesis of the presence of a unit root against the alternative hypothesis of stationarity with a single structural break with an unknown date.

4.2.2. The ARDL bound test to cointegration

The cointegration tests are used to estimate the long-run effects among variables of a model. There are many statistical methods for testing a cointegrating relationship between variables. The most common techniques for time series are the Engle and Granger (Citation1987) test and the Johansen (Citation1988) test which only apply to integrated variables at the same order. The inability of these traditional tests to be applied to series integrated into different orders prompted Pesaran and Shin (Citation1995) and Pesaran et al. (Citation2001) to propose a cointegration test procedure called ARDL bound test for cointegration. The ARDL cointegration approach is applicable irrespective of whether the variables are I(0), purely I(1) or mixed cointegrated as in the present study (see results of unit root tests in Tables ). This technique of cointegration is unbiased and efficient and performs well in small samples (Narayan, Citation2004). It is applied on the basis of an ARDL cointegration specification. The bounds testing procedure assumes the existence of long-run equilibrium relationships. These relations can be combined with the short-run dynamics of series in a dynamics unrestricted error correction model (UECM) which takes the following form:

Table 4. Pearson’s correlation matrix

Table 5. Results of Toda-Yamamoto causality test

Table 6. Results of ADF and PP unit root test (with intercept and trend)

Table 7. Results of ZA unit root test (with intercept and trend)

with is the first difference operator, Yt the dependant variable whose dynamics are explained,

the intercept;

is the coefficient associated with the lagged of

. X is a k x 1 vector of regressors and A is a k x 1 vector of associated parameters.

is the parameter associated with

;

is the parameters associated with

;

∼ iid(0,

) is the error term. Once formulation (2) is applied to EquationEquation 1

(1)

(1) to be estimated, we obtain the dynamic ARDL (m, n, p, q, r, s, t) model with unrestricted intercept and no trend as shown in EquationEquation 3

(3)

(3) :

where a0 is the drift a1, a2, a3, a4, a5, a6 and a7 are the long-term coefficients. b1, b2, b3, b4, b5, b6 and b7 represent the error correction dynamics of the model convergence to equilibrium. There are two steps involved in applying the cointegration test of Pesaran et al. (Citation2001). First, we determine the optimal lag. To do, we select the optimal ARDL model. It is the model which offers statistically significant results with the fewest parameters and which presents the smallest value of the Schwartz Information Criterium (SIC). Secondly, the cointegration relationship between the series is examined under the following hypothesis: H0: a1 = a2 = a3 = a4 = a5 = a6 = a7 = 0 and H1 : a1a2

a3

a4

a5

a6

a7

0. There is cointegration if the null hypothesis is rejected. The Fisher test is used to verify the cointegration. The OLS calculated F-statistics value is compared ,with the critical values, which form the upper bound (UB) and the lower bound (LB) provided by Pesaran et al. (Citation2001) for k regressors and n observations. However, as our sample size is small (<80 observations), then we compare with critical values provided by Narayan (Citation2005, page 1988, table case III: unrestricted intercept and no trend). Indeed, Narayan (Citation2005) argue that the critical bounds provided by Pesaran and Shin (Citation1995) and Pesaran et al. (Citation2001) are downwards and produce misleading resumes. If the F-statistics is more than the UB, cointegration exists. There is no cointegration if the F-statistics is less than the LB. If the F-statistic falls within the two bounds, the test is inconclusive.

4.2.3. Error correction term

Once long-run cointegration relationship is verified, the empirical methodology involves the examination of the error correction term as specified in EquationEquation 4(4)

(4) below:

with is the error correction term represented by the OLS residual series from the long-run cointegration relationships ;

describes the adjustment coefficient and measures the speed at which variables return to this long-run equilibrium relationship. It must be negative and statistically significant for the correction mechanism to take place.

4.2.4. Diagnostic and stability tests

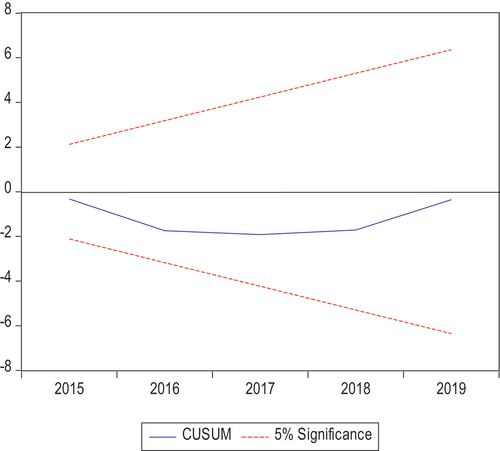

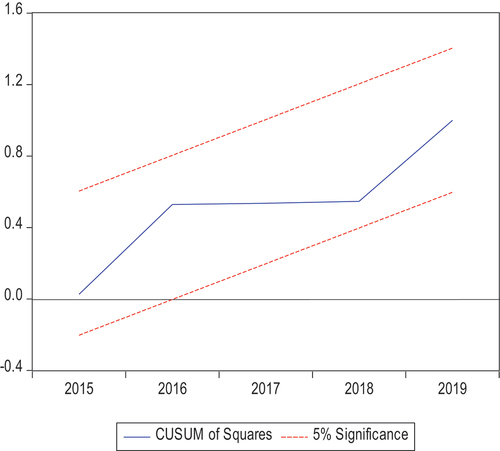

The validation of the ARDL model is based on a set of tests, the most important are Jarque–Bera normality test, the Breusch-Godfrey autocorrelation test, the White and ARCH heteroskedasticity tests and the Ramsey error specification test. Finally, we test the stability or constancy of the coefficients using the cumulative sum (CUSUM) and the cumulative sum of squares (CUSUMSQ) proposed by Brown et al. (Citation1975). Diagnostic and stability tests will reveal the soundness of the model.

4.2.5. Causality analysis

The classical causality test of Granger (Citation1980, Citation1988) concerns stationary series integrated at the same order. It does not apply to series integrated at different orders as in the case in our study. We, therefore, use the Granger causality test in the sense of Toda and Yamamoto (Citation1995). Indeed, Toda and Yamamoto propose a non-sequential causality test procedure adapted to series integrated at different orders, which consists in estimating a VAR (over-parameterized) which will serve as a basis for the causality test. The test procedure takes place in three stages: (i) determine the maximum order of integration (dmax) of the series under study by using unit root tests, (ii) determine the optimal lag (k) of the VAR or autoregressive (AR) polynomial using the information criteria of Akaike (AIC), Schwarz (SIC) and Hannan-Quinn (HQ) and (iii) estimate an augmented in level VAR of order p = k+ dmax, such that dmax < k. The Toda-Yamamoto causality test is based on Wald’s W-statistic distributed following χ2. The null hypothesis states that there is no causality between the series (probability χ2 >5%).

5. Empirical results and discussions

5.1. Correlation and causality between variables

Tables respectively present the Pearson’s correlation matrix and the Toda-Yamamoto causality test results. Pearson’s correlation coefficient is used to analyze linear relationships. Indeed, the problem of multi-collinearity can appear when some variables of the prediction model are correlated with others. But Table does not provide any strong link between the explanatory variables, the degrees of association not exceeding 0.80.

We identify unidirectional casualties. FDI flows cause economic growth and level of education. The infrastructure causes level of education, FDI flows and economic growth. The trade openness rate has an effect on infrastructures. This shows the importance of foreign trade in the development of infrastructure in Côte d’Ivoire. The results also show that household savings rate variable directly influences inflation. Indeed, inflation can be created by an excess of money in an economy, especially if the large part of the domestic savings injected into economic activity does not correspond to the quantity of goods and services offered (see Friedman, Citation1968).

5.2. Stationarity and cointegration tests

The results of ADF, PP and ZA unit root tests, taking into account the constant and the trend, are given in Tables , respectively. With the ADF and PP tests, FDI and INFL are stationary at level, I(0), and the other variables lnGDPPC, TO, SAVE, EDUC and INFR are stationary at first difference, I(1). But with ZA structural break unit root test, variables SAV E and IN F L are stationary at level, I(0), while the others are I(1). Let us note that I(0) variables generally provide long-run essential information in explaining the dynamics of the series, while the I(1) variables provide short-run information. As our variables are not stationary of the same order, we will study cointegration relationships among them. The ARDL methodology is well suited for estimating these cointegration relationships.

The results of the optimal lag-order analysis are given in Table . The lag structure (1, 1, 4, 0, 2, 1, 2) of the optimal ARDL model to be estimate is selected from the Schwartz Bayesian Criterium. Table gives the results of the Pesaran et al. (Citation2001) cointegration-bound test on EquationEquation 3.(3)

(3) The results confirm the existence of a cointegration relationship between the series because the calculated F-statistics value of 4.017 is greater than the upper critical bound 3.599 at the significance level of 10% (using Narayan (Citation2005) table: case III, with k = 6 regressors and sample size = 40 observations). We then reject the Ho hypothesis. In other words, we can estimate the long-run effects between the model variables.

Table 8. Results of lag order selection criteria

Table 9. ARDL bounds test results for cointegration

5.3. Short- and long-run estimates

The results of the short-run estimates are reported in Table . The coefficient associated with the adjustment term is negative (−0.2408) and significant at the 1% level. There is, therefore, an error correction mechanism. In other words, in the long-run, the imbalances between the variation in economic growth and explanatory variables are compensated so that the series have similar evolutions. It emerges from Table that FDI negatively affects economic growth at 1% level of significance. One percent increase in inward FDI flows leads to a 0.08% drop in growth. Indeed, from the early 1990s until the end of the 2000s, the country was weakened by numerous military-political crises. These periods of instability, mixed with the structural corruption that the country is experiencing, have made it impossible for the country to benefit from foreign investment in the short-run. Two other variables, trade openness and education showed a negative effect on economic growth. In the short-run, the country has there- fore not taken advantage of the know-how of other nations and the increase in the level of human capital.

Table 10. Short-run estimates

The long-run estimates are reported in Table . Only the FDI and EDUC variables show significant effects on economic growth. FDI has a negative impact at 5% level of significance. 1% increase in inward FDI flows results in a less than proportional drop in growth of 0.46%. Several reasons can explain this result. We suspect that the nature of the inward FDI in Côte d’Ivoire in recent years, dominated by extractive FDI as shown in Table . Foreign investment in the extractive sector is growing in proportion to the detriment of the manufacturing sector. However, the extractive sector is an enclave sector in which external capital has little or no effect on the national economy of DCs. It has a poor link with the national economy and employs a weak local workforce. In addition, in general, the inputs are imported, the production is exported, the funds and profits are repatriated and the decision-making centers are abroad. Investments in the extractive sector often go through a specific ministry, outside the usual circuit of economic development agencies. Consequently, the redistribution of benefits has less impact on populations directly affected. The results of Akinlo (Citation2004) confirm this analysis and show that FDI in the extractive sector has no effect on growth. Daouda (Citation2014) approaches in the same direction, pointing out that sub-Saharan Africa countries are unable to convert the mining rent generated by extraction activities for purposes of economic and social development. On the contrary, the mining rent accentuates corruption, social inequalities and administrative and fiscal laxity. The results of the GIABAFootnote2 Experts group corroborate our analysis. In a survey carried out on money laundering and terrorist financing linked to the extractive and mining industry in West Africa, they show that, in Côte d’Ivoire, the regulation and supervision of subcontracting processes in the sector extractive lacks credibility. The subcontractor companies, often aided by corrupt government officials, hide their profits through overcharging (GIABA, Citation2018). According to the Experts, it is for all these reasons that FDI does not have a strong economic impact on the hydrocarbon sector and other extractive resources in Côte d’Ivoire.

Table 11. Long-run estimates

Regarding the Education variable, unlike the short-run results, the long-run results show a positive and significant effect on economic growth. A 1% increase in the secondary education rate results in a 0.03% growth in per capita income. This result confirms the importance of the quality of human capital in the economic growth pro- cess. Indeed, a high and quality level of human capital increases the absorption capacity of new technologies and decreases the cost of imitating new ideas.

5.4. Diagnostic and stability tests statistics

We summarize the diagnostic tests of the estimated ARDL model in Table . The null hypothesis is accepted for all tests. Thus, the model is statistically validated. The estimated ARDL model (1, 1, 4, 0, 2, 1, 2) is good and well explains the dynamics of economic growth in Côte d’Ivoire from 1980 to 2019 (see and

). The F-statistics shows that the model is globally significant (see Table ). In addition, Figures show that the statistics for the CUSUM and CUSUM Squares tests, after having introduced a dummy variable to take into account the structural break, are within the confidence interval at the 5% level. We conclude in favor of the stability of parameters. Therefore, the model is stable.

Figure 2. Graph of CUSUM.

Figure 3. Graph of CUSUMSQ.

Table 12. ARDL model long-run diagnostic tests

6. Concluding remarks

The paper analyzed the contribution of FDI to the economic growth in Côte d’Ivoire by using an ARDL cointegration approach. We find that FDI did not contribute positively to economic growth for the period 1980–2019. On the contrary, they had a negative impact on growth in the short-run as well as in the long-run. Taking into account the breakdown of FDI flows in Côte d’Ivoire in the recent years, these results can be explained in large part by the predominance of extractive FDI. Indeed, extractive FDI does not tend to contribute positively to the growth of host countries because the extractive sector is an enclave sector, disconnected from the national economy and subject to fraud and structural corruption practices. These negative effects of FDI on the growth of Côte d’Ivoire are consistent with those obtained by Johnston and Ramirez (Citation2015) over the period 1975–2011. Our interpretation of this result raises the question of the need for a more comprehensive reflection on the real effects of the extractive sector on the economy of Côte d’Ivoire in particular and Africa in general. This first result suggests a rigorous FDI selection policy that can generate positive effects on growth and economic development. The country must attract FDI targeting activity sectors that have a considerable effect on growth and which are based on the win–win principle. It should also promote better integration of the extractive sector into the national economy. To do this, we must, on the one hand, more strictly control institutional governance, and, on the other hand, liberalize the sector by increasingly favoring the concession of operating rights involving national champions, local subcontracting and employment of the local workforce. Note, however, that this study could have been more exhaustive if we had available data on extractive FDI over the entire period of analysis. A more complete modelling taking into account the flows of extractive FDI and non-extractive FDI would have enabled us to estimate more concretely the effects of extractive FDI.

Another important result of this paper is that education contributes positively to the economic growth of the country. We therefore suggest that particular emphasis be placed on strengthening the education system and human capital training to further take advantage of new knowledge and technologies transferred by FDI.

Acknowledgements

The authors would like to thank the anonymous reviewers and the Editor of the journal for their valuable comments and suggestions that greatly contributed to improving the quality of this paper. They are also grateful to Maxime Tano, Jean-Eudes Koffi, and researchers of the Laboratory for Law, Economics and Management (LADEG) for very useful comments on earlier versions of this paper. However, any remaining errors or omissions are indebted to the authors.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Notes on contributors

B. G. Jean Jacques Iritié

B. G. Jean Jacques Iritié is an Assistant Professor in Economics. He is the Director of the Department of Business Management and Applied Economics at INP-HB. He received his PhD in Economics since 2012 from the University of Grenoble (France) with a major in Industrial Economics of Innovation. He previously completed a Master in Economics from the Toulouse School of Economics. Dr. Iritié mainly teaches economic theory and applied econometrics. His research interest includes industrial economics, the economics of innovation and intellectual property, development economics, and the economics of agriculture and natural resources.

Jean Baptiste Tiémélé

Jean Baptiste Tiémélé is an Assistant in Economics at the Department of Business Management and Applied Economics of INP-HB. He obtained his PhD in Economics since 2019 from the University Alassane Ouattara of Bouaké (Côte d’Ivoire) with a specialization in development economics. He mainly teaches microeconomics and international economics. His research focuses on development economics and the economics of agriculture and natural resources.

Notes

1. 1 US $ ≃ 566.5 Francs CFA at the time of the study.

2. The GIABA is the Intergovernmental action group against money laundering in West Africa. It is an ECOWAS institution responsible for capacities building of member states in preventing and combating money laundering and terrorist financing in the region.

References

- Aglietta, M. (1991). Épargne, innovations financières et croissance. Revue d’économie financière, (17), 3–21. https://doi.org/10.3406/ecofi.1991.1714

- Ahouré, A. A. E. & Tano A. P., (2009). Bilan diagnostic de l’industrie ivoirienne. Cellule d’Analyse de Politiques Économiques du CIRES.

- Ajayi, S. I. (2004). The determinants of foreign direct investment in Africa: a survey of the evidences contenteditable. Paper presented at the IMF/AERC Special Workshop on the determinants of Foreign Direct Investment in Africa. December 2-3, Nairobi, Kenya.

- Ajayi, S. I. (2006). L’IDE et le développement économique en Afrique. Document à présenter lors du Congrès International ADB/AERC sur l’Accélération du Développement de l’Afrique les cinq premières années du 21ème siècle ( du 22 au 24 novembre). Tunisie.

- Akinlo, A. E. (2004). Foreign direct investment and growth in Nigeria: An empirical investigation. Journal of Policy Modeling, 26(5), 627–639. https://doi.org/10.1016/j.jpolmod.2004.04.011

- Alaya, M., Nicet-Chenaf, D., & Rougier, E. (2009). À quelles conditions les IDE stimulent-ils la croissance ? Mondes en Développement, 4(148), 119–138. https://doi.org/10.3917/med.148.0119

- Alvarado, R., Iñiguez, M., & Ponce, P. (2017). Foreign direct investment and economic growth in latin america. Economic Analysis and Policy, 56, 176–187. https://doi.org/10.1016/j.eap.2017.09.006

- Artus, P., & Cartapanis, A. (2008). Globalisation financière et croissance dans les économies émergentes: la sous-estimation des contraintes macroéconomiques induites. Revue économique, 59(6), 1145–1158. https://doi.org/10.3917/reco.596.1145

- Barro, R. J. (1990). Economic growth in a cross section of countries. Quarterly Journal of Economics, 106(2), 407–443. https://doi.org/10.2307/2937943

- BCEAO. (2013). Évolution des investissements directs étrangers dans les pays de l’uemoa au cours de la période 2000-201. BCEAO.

- Borensztein, E., De Gregorio, J., & Lee, J. W. (1998). How does foreign direct investment affect economic growth? Journal of International Economics, 45(1), 115–135. https://doi.org/10.1016/S002219969700033-0

- Bosworth, B., & Collins, S. (1999). Capital flows to developing economies: Implications for savings and investment. Brookings Papers on Economic Activity, (1)143–180.

- Bouoiyour, J., El Mouhoub, M., & Hicham, H. (2009). Investissements Directs Étrangers et productivité: quelles interactions dans le cas des pays du moyen orient et l’Afrique du nord? Revue économique, 60(1), 109–131. https://doi.org/10.3917/reco.601.0109

- Bouoiyour, J., & Toufik, S. (2007). L’impact des Investissements Directs Étrangers et du capital humain sur la productivité des industries manufacturières Marocaines. Revue Région et Développement, (25), 116–136. https://EconPapers.repec.org/RePEc:tou:journl:v:25:y:2007:p:115-136

- Bouyacoub, A., & Bouyacoub, B. (2017). Impact de l’investissement direct étranger sur la croissance économique en Algérie : « une étude empirique en utilisant l’approche ARCH and GARCH » (Revue Économie). Gestion et Société.

- Brana, S. (1999). Systèmes financiers et croissance en méditerranée : une analyse Comparative. Revue d’économie financière, (52), 207–233. https://doi.org/10.3406/ecofi.1999.3539

- Brown, R. L., Durbin, J., & Evans, J. M. (1975). Techniques for testing the constancy of regression relationships over time. Journal of the Royal Statistical Society Series B (Methodological), 37(2), 149–192. https://doi.org/10.1111/j.2517-6161.1975.tb01532.x

- Bruno, M., & Musso, P. (2000). Volatilité de l’inflation et croissance économique. Revue économique, 51(3), 693–701. https://doi.org/10.3406/reco.2000.410547

- Busse, M., Erdogan, C., & Mühlen, H. (2016). China’s impact on Africa: The role of Trade, FDI and AID. KYKLOS, 69(2), 228–262. https://doi.org/10.1111/kykl.12110

- Caceres, L. R. (1995). Capitaux étrangers, épargne intérieure et croissance économique : le cas de l’Amérique centrale. Savings and Development, 19(4), 393–404.

- Carbonell, J. B., & Werner, R. A. (2018). Does foreign direct investment generate economic growth? a new empirical approach applied to spain. Economic Geography, 94(4), 425–456. https://doi.org/10.1080/00130095.2017.1393312

- CEPICI. (2016). World investment report: Reforming international investment governance,

- CNUCED. (2019a) . EPI : Examen de la Politique d’Investissement, Côte d’Ivoire. Nations Unies, Genève.

- CNUCED. (2019b) . IDE : à contre-courant de la tendance mondiale, les flux à destination de l’Afrique en hausse. Par Aboubacar Yacouba Barma. UNCTAD Genève.

- CNUCED. (2020) . Rapport sur l’investissement dans le monde. Repères et vue d’ensemble. 30e. édition Nations Unies.

- Daouda, Y. H. (2014). Responsabilité sociétale des multinationales en Afrique Subsaharienne : enjeux et controverses (cas du groupe AREVA au Niger). VertigO- Revue électronique en sciences de l’environnement, 14(1). https://doi.org/10.4000/vertigo.14712

- Dembelé, B. S., & Machrafi, M. (2021). Les investissements directs en Côte d’Ivoire : une analyse de 2003 à 2016. Finance et Finance Internationale, 1(21), 1–28. https://doi.org/10.34874/IMIST.PRSM/ffi-v1i21.24456

- De Mello, L. R. (1997). Foreign direct investment in developing countries and growth: A selective survey. Journal of Developing Studies, 34(1), 1–34. https://doi.org/10.1080/00220389708422501

- Diaw, D., & Lessoua, A. (2013). Natural resources exports, diversification and economic growth of CEMAC countries: On the impact of trade with china. African Development Review, 25(2), 189–202. https://doi.org/10.1111/j.1467-8268.2013.12023.x

- Dickey, D. A., & Fuller, W. A. (1981). Likelihood ratio statistics for autoregressive time series with a unit root. Econometrica, 49(4), 1057–1072. https://doi.org/10.2307/1912517

- Dunning, J. H. (1973). The determinants of international production. Oxford Economic Papers, (3), 289–336.

- Eka, F., & Bouoiyour, J. (2020). IDE Chinois et croissance économique des pays d’Afrique Sub-saharienne : Approche par la MMGEN données de panel. Revue Économie, Gestion et Société, 1(25), 1–31. https://doi.org/10.48382/IMIST.PRSM/regs-v1i25.22422

- Ekodo, R., Ndam, M., & Ousmanou, K. (2020). Investissement direct étranger et croissance économique en zone CEMAC : Le rôle du contrôle de la corruption. Revue Repères et Perspectives Economiques, 4(2), 1–22. https://doi.org/10.34874/IMIST.PRSM/RPE/21529

- Engle, R. F., & Granger C. W. J. (1987). Cointegration and error correction: Representation, estimation and testing. Econometrica, 55(2), 251–276. https://doi.org/10.2307/1913236

- Esso, L. J. (2005). Investissements directs étrangers: déterminants et influence sur la croissance économique. Politique Économique et Développement, E. No 117, CAPEC.

- Esso, L. J. (2010). Long-run relationship and causality between foreign direct investment and growth: Evidence from Ten Africa countries. International Journal of Economics and Finance, 2(2), 168–176. https://doi.org/10.5539/ijef.v2n2p168

- Fischer, S., Cooper, R. N., Dornbusch, R., Garber, P. M., Massad, C., Polak, J. J., Rodrik, D., & Tarapore, S. S. (1998). Should the IMF pursue capital-account convertibility? In Essays in International Finance (No. 207, pp. 20–27). 0071-142X. International Finance Section, Princeton University.

- FMI. (2000). Côte d’Ivoire: Selected Issues and statistical. IMF Staff Country Report, (107), 106. 978145.

- FMI. (2016). Côte d’Ivoire, Documents de Développement Économique-Plan National, Développement, 2016-2020. Rapport du FMI 16388. IMF.

- Frankel, J. A., & Romer, D. H. (1999). Does Trade cause growth. American Economic Review, 89(3), 379–399. https://doi.org/10.1257/aer.89.3.379

- Friedman, M. (1968). The role of monetary policy. The American Economic Review, LVIII(1), 1–17.

- GIABA. (2018). Rapport de recherche et de documentation, Blanchiment de capitaux et financement du terrorisme liés à l’industrie extractive/au secteur minier en Afrique de l’Ouest, Rapport de typologie.

- Globerman, S., & Shapiro, D. (2002). Global foreign direct investment flows: The role of governance infrastructure. World Development, 30(11), 1899–1919. https://doi.org/10.1016/S0305-750X0200110-9

- Golub, S. (2003). Mesures des restrictions visant les investissements directs étrangers dans les pays de l’OCDE. Revue économique de l’OCDE, 1(36), 96–128. https://doi.org/10.1787/eco_studies-v2003-art3-fr

- Granger, C. W. J. (1980). Testing for causality: A personal viewpoint. Journal of Economic Dynamics and Control, 2, 329–352. https://doi.org/10.1016/0165-18898090069-X

- Granger, C. W. J. (1988). Causality, cointegration and control. Journal of Economic Dynamics and Control, 12(2–3), 551–559. https://doi.org/10.1016/0165-1889(88)90055-3

- Grossman, G. M., & Helpman, E. (1991). Quality ladders in the theory of growth. The Review of Economic Studies, 58(1), 43–61. https://doi.org/10.2307/2298044

- Haddad, M., & Harrison, A. (1993). Are there positive spillovers from direct foreign investment? Evidence from panel data for morocco. Journal of Development Economics, 42(1), 51–74. https://doi.org/10.1016/0304-3878(93)90072-U

- ITIE. (2018). Initiative pour la transparence dans les industries extractives de la Côte d’Ivoire. Rapport du conseil national Côte d’Ivoire.

- Jackman, R. W. (1982). Dependence on foreign investment and economic growth in the third world. World Politics, 34(2), 175–196. https://doi.org/10.2307/2010262

- Johansen, S. (1988). Statistical analysis of cointegrating vectors. Journal of Economic Dynamic and Control, 12(2–3), 231–254. https://doi.org/10.1016/0165-1889(88)90041-3

- Johnston, K. A., & Ramirez, M. D. (2015). Foreign direct investment and economic growth in cote D’Ivoire: A time series analysis. Business and Economic Research, 5(2). https://doi.org/10.5296/ber.v5i2.7638

- Keho, Y. (2020). Foreign direct investment and import demand in Côte d’Ivoire. International Journal of Trade, Economics and Finance, 11(2), 24–31. https://doi.org/10.18178/ijtef.2020.11.2.661

- Kinda, T. (2008). Infrastructures et flux de capitaux privés vers les pays en développement. Revue économique, 59(3), 537–549. https://doi.org/10.3917/reco.593.0537

- King, R. V., & Levine, R. (1993). Finance, and growth: Schumpeter might be right. The Quarterly Journal of Economics, 108(3), 717–737. https://doi.org/10.2307/2118406

- Kokko, A. (1994). Technology, market characteristics, and spillovers. Journal of Development Economics, 43(2), 279–293. https://doi.org/10.1016/0304-38789490008-6

- Levine, R., & Renelt, D. (1992). A sensibility analysis of cross-country growth regressions. The American Economic Review, 82(4), 942–963.

- Mainguy, C. (2004). Impact des investissements directs étrangers sur les économies en Développement. Revue Région et Développement, (20), 66–89. https://ideas.repec.org/a/tou/journl/v20y2004p65-89.html

- Majumder, S. C., & Rahman, M. H. (2020). Impact of Foreign Direct Investment on economic growth of China after economic reform. Journal of Entrepreneurship, Business and Economics, 8(2), 120–153.

- Majumder, S. C., Rahman, M. H., & Martial, A. A. A. (2022). The effects of foreign direct investment on export processing zones in Bangladesh using Generalized method of moments approach. Social Sciences & Humanities Open, 6(1), 1–10. https://doi.org/10.1016/j.ssaho.2022.100277

- Mapalad, M. C. M. (1998). Foreign capital inflows and domestic savings in the philippines. Savings and Development, 22(1), 5–25.

- Mensah, I., & Mensah, E. K. (2021). The impact of inward FDI on output growth volatility: A country-sector analysis. Research in Globalization, 3, 1–15. https://doi.org/10.1016/j.resglo.2021.100063

- Miah, M. M., & Majumder, S. C. (2020). An empirical investigation of the impact of FDI, export and gross domestic savings on the economic growth in Bangladesh. The Economics and Finance Letters, 7(2), 255–267. https://doi.org/10.18488/journal.29.2020.72.255.267

- Miah, M. M., & Majumder, S. C. (2022). Impact of FDI on exports and employment in bangladesh. Bangladesh Journal of Political Economy, 38(1), 83–102.

- Mughal, M., et Vechiu, N. (2015). Investissements directs étrangers et éducation dans les pays en voie de développement. Revue économique, 66(2), 369–400. https://doi.org/10.3917/reco.pr2.0038

- Narayan, P. K. (2004). Reformulating critical values for the bounds f -statistics approach to cointegration: An application to the tourism demand model for fiji. Technical report, Department of Economics Discussion Papers No. 02/04, Monash University,

- Narayan, P. K. (2005). The saving and investment nexus for china: Evidence from cointegration tests. Applied Economics, 37(17), 1979–1990. https://doi.org/10.1080/00036840500278103

- Nelson, R. R., & Phelps, E. S. (1966). Investment in Humans, Technological Diffusion, and Economic Growth. The American Economic Review, 56(1/2), 69–75. http://www.jstor.org/stable/1821269

- Nkoa, B. E. O. (2016). Investissements directs étrangers et industrialisation de l’Afrique : un nouveau regard. Revue Innovations, 3(51), 173–196. https://doi.org/10.3917/inno.051.0173

- Nkoa, B. E. O. (2018). Effets différenciés des IDE sur la croissance économique africaine : le rôle de la finance. Revue d’économie du développement, 26, 33–63. https://doi.org/10.3917/edd.323.0033

- Perron, P. (1989). The great crash, the oil price shock and the unit root hypothesis. Econometrica, 57(6), 1361–1401. https://doi.org/10.2307/1913712

- Perron, P. (1992). Racines unitaires en macroéconomie: le cas d’une variable. L’Actualité économique, 68(1–2), 325–356. https://doi.org/10.7202/602070ar

- Pesaran, M. H., & Shin, Y. (1995). An autoregressive distributed-lag modelling approach to cointegration analysis. Proceedings of the Econometrics and Economic Theory in the 20th Century: The Ragnar Frisch Centennial Symposium, United Kingdom (UK), 31, 371–413.

- Pesaran, M. H., Shin, Y., & Smith, R. J. (2001). Bounds testing approaches to the analysis of level relationships. Journal of Applied Econometrics, 16(3), 289–326. https://doi.org/10.1002/jae.616

- Phillips, P. C. B., & Perron, P. (1988). Testing for a unit root in a time series regression. Biometrika, 75(2), 335–346. https://doi.org/10.1093/biomet/75.2.335

- Pokou, K. (2005). Investissements directs étrangers et croissance économique en Côte d’Ivoire. Politique Économique et Développement, E, (130c).

- Rappoport, P., & Reichlin, L. (1989). Segmented Trends and Nonstationary Time Series. Economic Journal, 99(395), 168–177. https://doi.org/10.2307/2234078

- Rogoff, S. K. (2003). Contrôle des flux de capitaux faut-il garder l’esprit ouvert à cet égard? Revue d’économie financière, (70), 123–127. https://doi.org/10.3406/ecofi.2003.4826

- Romer, P. M. (1990). Endogenous technological change. Journal of Political Economy, 98(5), 71–102. https://doi.org/10.1086/261725

- Rothgeb, J. (1984). The effects of foreign investment on overall and sectoral growth in third world States. Journal of Peace Research, 21(1), 5–14. https://doi.org/10.1177/002234338402100102

- Solow, R. M. (1956). A contribution to the theory of economic growth. Quarterly Journal of Economics, 70(1), 65–94. https://doi.org/10.2307/1884513

- Sun, X., (2002). Foreign direct investment and economic development what do states need to do? Paper prepared for the Capacity Development Workshops and Global Forum on Reinventing Government on Globalization, Role of the State and Enabling Environment, Marrakech, Morocco, 10-13 décembre. 2002.

- Toda, H. Y., & Yamamoto, T. (1995). Statistical inference in vector autoregressions with possibly integrated processes. Journal of Econometrics, 66, 225–250. https://doi.org/10.1016/0304-4076(94)01616-8

- Van Huffez, C. (2001). Investissements directs étrangers : problèmes et enjeux pour les pays du sud et de l’est de la méditerranée. Revue Région et Développement, (13), 196–216.

- Wacziarg, R., & Welch, K. H. (2008). Trade liberalization and growth: New evidence. The World Bank Economic Review, 22(2), 187–231. https://doi.org/10.1093/wber/lhn007

- Williams, O., & Williams, S. (1999). The impact of foreign direct investment flows to the eastern Caribbean central bank unified currency area. Savings and Development, 23(2), 131–146.

- World Development Iindicators (WDI). (2021). Last Updated 24/05/2021. Indicateurs du développement dans le monde. Banque mondiale Washington.

- Zivot, E., & Andrews, D. W. K. (1992). Further evidence on the great crash, the oil price shock and the unit root hypothesis. Journal of Business and Economic Statistics, 10(3), 251–270. https://doi.org/10.1080/07350015.1992.10509904