?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

This study examines the nature of relationship between public debt and economic growth of Ethiopia. To this end, a time series data was collected over the period 1982–2018. Nonlinear ARDL and multiple thresholds nonlinear ARDL models were used to uncover whether the relationship between debt and economic growth of Ethiopia is asymmetric. Instrumental variable regression model with a quadratic specification was used to test threshold effect of debt. The results reveal there are evidences that support the existence of asymmetric relationship between the indicated variables. Accordingly, it was found that a major positive shock in debt is favorable to economic growth while the effect of a minor and negative shock to debt is unfavorable. The results further reveals that there is a threshold effect of debt such that it is beneficial to economic growth of Ethiopia when it is well below 66.75% of GDP or 36.27% of GNI. Above these threshold levels, debt incurred deteriorates economic growth of the country. The study recommends that government of Ethiopia should create conducive environment that helps to secure more debts from potential creditors and at the same time, keep the annual debt well below 66.75% of GDP and 36.27%.

1. Introduction

The impact of public debt on economic growth of nations is a controversial issue both at theoretical and empirical level. Keynesian macroeconomics prescribes government spending that could be financed by public borrowing to stimulate economy in times of economic recession in the short run (Elmendorf & Mankiw, Citation1999). On contrary to this, however, many others theorize the undesirable effect of such attempts on the economy: public debt crowd out investment by raising interest rate (Baldacci & Kumar, Citation2010; Modigliani, Citation1961), hampers fiscal balance (Adam & Bevan, Citation2005), and could result in financial crises (Burnside et al., Citation2001). Yet, classical economists like David Ricardo theorize that there is no relationship between public debt and economic growth at all, which is commonly known as Ricardian equivalence.

Ethiopia is one of the least developed countries on the planet earth: branded with poverty, drought, humanitarian crises, and war. Currently, there is a war going on in the country for more than a year and high cost of living, one of the usual and the most likely prediction of economy during war, is realized as inflation has skyrocketed to 34%. It is also known that government spending increases significantly during a time of war. In order to finance the increased spending, government is more likely to knock at doors of creditors. Most often, we see debtor countries unable to pay the debt back to the creditors and seek rescheduling or relief, which is an indication of their economy going nowhere forward. On top of that, rescheduling of debt to some future time will undeniably increase the debt burden, another headache. Ethiopia cannot be an exception as the country is now in the list of heavily indebted poor countries (HIPC). Therefore, the relationship between debt and economic growth of Ethiopia should be studied critically as the existing fact on ground in the country signals more demand for debt than ever.

To the best knowledge of the author, nonlinear relationship between debt and economic growth has never been studied for Ethiopian case and that the existing studies has utilized linear specification leading them obtain mixed result of negative (Atinafu, Citation2020; Getinet & Ersumo, Citation2020) and positive Mohanty (Citation2017). Even if the conflicting results by different studies for the same country might be an indication of something going wrong with anyone of the study, in part owing to the methodology chosen or data over short period, inter countries difference in results obtained is understandable since there are some peculiarities with all countries. For example, the threshold values of debt to GDP ratio varies for different countries. Therefore, country level studies (as far as debt-growth relationship is concerned) are deemed crucial and this is the motivation behind carrying out this paper.

Thus, the current study is aimed at investigating the relationship between debt and economic growth of Ethiopia. The study tests whether there exist asymmetric relationship between debt and economic growth and whether there exist debt threshold level. The novelty of this paper lies in: (1) test of nonlinearity of the relationship between debt and economic growth for Ethiopia based on test of asymmetry and threshold estimates for the first time. (2) Robustness check of results obtained by using different measurements of debt and alternative models to the main model. The rest of the paper is organized as follows. In the section that follows, review of the empirical examination of relationship between them is given. In section three, the methodology adopted to achieve the stated aim is given in detail. Results obtained based on the methodology adopted and its discussion is provided in section four. Finally, conclusion and recommendation are provided in section five.

2. Review of literature

2.1. On the link between public debt and economic growth: transmission mechanisms and the nature of relationship

Concerning the relationship between public debt and economic growth, the direction of the relationship (if any) is among the unsettled issue in the science of economics. Aggregate demand is an important economic variable that determine short-run level of output in the Keynesian economics: anything that increase aggregate demand boosts output level and vise versa. They (Keynesians) explains that public debt increases aggregate demand (as disposable income is induced following tax cut) and, thus, increases output level. Put simply, public debt stimulates economy via its positive effect on aggregate demand.

However, there exist theoretical blow ups to this assertion. David Ricardo, an influential classical economist of the 18th century, has earlier theorized that public debt is immaterial for economic growth, as consumption (aggregate demand) does not increase following tax cut, which is against the Keynesians anticipation. The original work of Ricardo was refined and expounded clearly by Barro (Citation1974). According to this theory, also known as Ricardian equivalence (Ricardo, Citation1817), a tax cut will not be followed by increased consumption due to the fact that the general public makes consumption decision in line with the prediction of life cycle hypothesis and rational expectation behavior. For example, if government decided to finance its expenditure by borrowing, there will be tax cut. Given expectation is rational and consumption decision is guided by the life cycle hypothesis, however, people will realize that it is them and no one else who pays the principal plus interest in the future. Cognizant of this, they will increase saving instead of consumption nullifying the Keynesians’ prediction.

Another line of theory concerning the relationship between debt and economic growth is the debt overhang theory. The theory was first developed by Myers (Citation1977). According to Myers (Citation1977), the eventual result of increased debt is reduction in incentive to invest. The reason is that the future benefit streams from investments will accrue to creditors in the form of repayment. The initial work of Myers (Citation1977) was microeconomic approach, as it was applied to behavior of companies with high debt. After the debt crises of 1982, some scholars attempted to model the same within the contexts of macroeconomics, notable of such works being that of Krugman (Citation1988). Krugman (Citation1988)’ concept of debt overhang theory pertains to the relationship between face value of debt and debtor’s ability to repay. In case the face value of debt incurred is too high to the extent of exceeding a debtor country’s ability to pay, the whole of resources generated by the debt will goes to creditor’s exchequer. Since the debtor country gets nothing, its incentive to undertake productive investments will dwindle.

A closely related concept to the debt overhang theory is debt Laffer curve. Debt Laffer curve shows the amount of debt beyond which debt overhang starts to operate. At lower debt level, there will be repayment of debt in full and everything will be fine. With an increase in amount of debt, however, probability of defaulting will also increase taking the suit. Ultimately, a point will be reached beyond which the debtor cannot manage, giving a way to debt Laffer curve. Because the current study takes a nonlinear approach to the relationship between public debt and economic growth, the debt Laffer curve theory provides rigor theoretical foundation.

2.2. Empirical review of literature

Motivated by the controversial theoretical arguments about the relationship between the variables, there exist extant accounts of varied empirical findings at both country level and cross-country. According to some empirical findings, the effect of public debt on economic growth varies not only with the amount of public debt incurred but also over time. In the paragraphs that follow, the review of such diverse empirical findings is given.

In their investigation of the effect of external debt on economic growth for the case of Nigeria, Sulaiman and Azeez (Citation2012) found that external debt promotes economic growth over the period covering 1970–2010 as evidenced by error correction model. In the same country, the study by Erhieyovwe and Onovwoakpoma (Citation2013) has also found positive effect of debt on economic growth. Gövdeli (Citation2019) studied the relationship between external debt and economic growth for the case of Turkey during the period 1970–2016. The author utilized ARDL based bounds testing approach for analysis. The study result shows that external debt exerts favorable impact on economic growth of Turkey. Another evidence of positive effect of debt stock on economic growth is contributed by the study by Ndubuisi (Citation2017). The study was conducted in Nigeria over the period covering 1985–2015.

Mohanty (Citation2017) has studied the impact of external debt on economic growth for the case of Ethiopia for the period 1981–2014. Results obtained from the study shows that external debt has positive long-run impact on economic growth of Ethiopia. Using quarterly data from 2000Q1 to 2017Q3 (Ganiev et al., Citation2020), studied the relationship between external debt and economic growth in transition countries, the case of Kyrgyzstan. The result from ARDL based error correction shows there is positive relationship between external debt and economic growth. By disaggregating total public debt in to domestic debt and external debt (Didia & Ayokunle, Citation2020), studied the impact of public debt on economic growth for the case of Nigeria. In their study, they found that domestic debt has positive effect on economic growth while the effect of external debt is negative.

In stark contrast to empirical findings given in the preceding paragraphs, however, considerable empirical literatures found the negative relationship between public debt and economic growth. Bidzo (Citation2018) studied whether public debt has a scissor impact on economic growth of developing countries by taking Gabon as a case study. The author used generalized method of moment for estimation purpose and found a scissor impact between public debt and economic growth indeed. The negative long-run effect of public external debt on economic growth was also established by the study conducted by Gizaw and Ferede (Citation2020) on Ethiopia from 1981 to 2014. According to the study by Getinet and Ersumo (Citation2020), both the stock of external debt and external debt service had affected economic growth of Ethiopia from 1983 to 2015 negatively. Using ARDL modeling, Atinafu (Citation2020) found that the stock of public debt has adverse effect on economic growth of Ethiopia from 1970 to 2017. Faizulayev et al. (Citation2020) studied the dynamic effect of external debt on economic growth of Nigeria over the period covering 1981–2017. The authors found that the long-run effect of both debt stock and debt service is adverse and that the debt forgiveness initiative does not influence economic growth positively.

On the other hand, some empirical findings obtained so far appears to confirm the theoretical prediction of Ricardian equivalence. In these empirical findings, no statistically significant relationship between public debt and economic growth is obtained. Considering a large panel data set comprising 82 countries across the globe over the period covering 1980–2009, Kourtellos et al. (Citation2013) investigated the relationship between public debt and economic growth. The result from structural threshold regression shows that the impact of public debt on economic growth of nations is statistically insignificant, if the institutional environment in the countries is sufficiently high.

The empirical findings indicated above are those with liniar specification of the relationship between public debt and economic growth. In addition to these liniar specifications, there is also significant number of nonliniar specification. Based on the data collected from 93 developing countries over the period 1969–1998, Pattillo et al. (Citation2002) assessed the nonliniar effect on economic growth. Their findings support the nonliner inverted U-shaped relationship between public debt and economic growth, where the effect of public debt on economic growth turns significantly negative at debt to GDP ratio of 35–40. Ehikioya et al. (Citation2020) studied the relationship between public debt and economic growth of 43 African countries over the period 2001–2018 using system generalized method of moment method. The study result shows that there is inverted U-shape nonliniar relationship between public debt and economic growth. With an aim of analyzing the effect of debt on economic growth, Munir and Mehmood (Citation2018) conducted research on panel of four south Asian countries from the period covering 1990–2013. Again, the study confirms the inverted U-shape relationship between the variables.

In spite of the observed inverted U-shaped relationship established by some studies as stated above, however, studies of some authors failed to establish the nonliniar relationship between public debt and economic growth. For instance, the nonliniar relationship between the variables was not supported by the study carried out by Asafo (Citation2019). Their study was based on a panel of 48 sub Saharan countries from 19,090–2017 using generalized method of moment. Based on instrumental variable methodology, Panizza and Presbitero (Citation2013) studied the effect of public on economic growth of OECD countries. In their study, the evidence of nonliniar relationship between the variables is not established. Similar result was also obtained by a country level study undertaken by (Benli, Citation2020) for the case of Turkey.

3. Material and methods

3.1. Methods

3.1.1. Econometric model specification

Assuming Cobb–Douglas production function with constant returns to scale, the popular neoclassical growth model, also known as exogenous growth model, developed by Solow (Citation1956) predicts that the key drivers of growth are physical capital, labor, and technological advancement. Until the wave of endogenous growth theories in the late 1980s, roughly for three decades, the exogenous growth model has widely been used in empirical growth studies. The empirical work of Mankiw et al. (Citation1992) improved explanatory power of exogenous growth model of Solow (Citation1956) by incorporating human capital in to the model as given in Equationequation 1(1)

(1) .

where, Y is output, K is capital, L is labor (proxied by population growth), H is human capital, and

are measures of elasticity of output with respect to the indicated inputs, and t indexes time.

Similar to the exogenous growth model, however, Mankiw et al. (Citation1992) model also assume the technology parameter (total factor productivity) as given. Rather than taking for granted, endogenous growth theories (see Grossman & Helpman, Citation1991; Lucas, Citation2000; Romer, Citation1990) explains factors up on which total factor productivity depends (Rao, Citation2006). Public debt is one of the different factors that determine total factor productivity (Kaas, Citation2016). Therefore, by incorporating public debt and trade openness, another variable that affects economic growth via total factor productivity (Rumanzi et al., Citation2021), and taking natural logarithm to both side of Equationequation 1(1)

(1) , the following econometric model is specified for estimation purpose for Ethiopia over the sampled period.

where, is per capita output,

is gross capital formation,

is number of people engaged,

is expenditure on education,

is public debt as percent of GDP,

is trade openness,

,

, … ,

are parameters to be estimated, and

is the error term.

3.1.2. ARDL model

Based on Pesaran et al. (Citation2001), the following general form of linear ARDL model is presented.

where, in addition to definitions given in Equationequation 2(2)

(2) ,

,

, … ,

are short-run coefficients,

,

, … ,

are long-run coefficients, and

,

, … ,

are lag length. Whether the variables considered in these variables have long-run relationship can be tested by bounds test of co-integration where the null hypothesis of the test states that none of the long-run coefficients are different from zero.

3.1.3. NARDL model

The linear ARDL cannot capture asymmetric impact of covariate (s) on the dependent variables. In this study, the relationship between public debt and economic growth is expected to be asymmetric such that a negative shock and positive shock to public debt affect economic growth differently (Mosikari & Eita, Citation2021; Sharaf, Citation2021). As an extension to the linear ARDL, Shin et al. (Citation2014) proposed the nonlinear version where in the variable of interest (in this study debt) is decomposed in to negative and positive partial sums. Accordingly, the public debt series is decomposed as in Equationequation 4(4)

(4) .

In Equationequation 4(4)

(4) ,

, and

, respectively, captures partial sum of increase and decrease of change in public debt expressed as follows.

where, is the first difference of public debt defined as

. By incorporating the partial sum of public debt in to the ARDL framework, the nonlinear ARDL (NARDL) is given as:

where, definition of variables and notations is as provided in the preceding equations. In the NARDL model represented by Equationequation 6(6)

(6) , the null hypothesis of long-run symmetry (

) and short-run symmetry (

will be tested against the alternative hypothesis of asymmetry. On the other hand, the long-run association ship between the variables selected is tested with the use of bounds test approach where the null hypothesis of no co-integration (all of the long-run coefficients are equal to zero) is tested against the alternative.

3.1.4. MTNARDAL model

The NARDL model is surely helpful to make more rigorous analysis than the linear ARDL model as it enables one to find out whether the relationship between variables of interest is asymmetric. The NARDL approach decomposes a variable in to negative (less than zero) and positive (greater than zero) changes in the variable, and thus, zero can be considered as a threshold value. Limitation of the NARDL approach is, however, it does not help to examine whether the asymmetric impact of the threshold variable on the outcome varies with major and minor change in the threshold variable. For example, the NARDL model can help examine whether reduction and building up of public debt have different effect on economic growth of Ethiopia, but not whether change in public debt above 75% of GDP is beneficial or detrimental to the economy. Since it is expected in this study that the effect of public debt may differ from significant to minimal changes, we employ multiple threshold nonlinear autoregressive distributive lag (MTNARDL) model developed by (Pal & Mitra, Citation2015, Citation2016) The model is currently becoming popular in nonlinear time series analysis (Chang, Citation2020; Keho, Citation2021; Li & Guo, Citation2021; Uche & Effiom, Citation2021). Accordingly, the current study decomposes public debt in to three partial sums taking the 25th and 75th quintiles as threshold level, which is given below.

where, and

are the two partial sums of debt at 25th and 75th quartiles, respectively. For each of the series, the thresholds are represented by

and

are calculated as follows.

In Equationequation 7a(7)

(7) , Equation7b

(7)

(7) , and Equation7c

(7)

(7) , I

indicate the indicator function taking a value of 1 if the condition is satisfied and 0 if not.

3.1.5. The threshold model

As far as the relationship between debt and economic growth is concerned, nonlinear models are becoming popular in contemporary researches on the subject. Following the classic work of Reinhart and Rogoff (Citation2010), many nonlinear empirical researches have been conducted so far regarding the relationship between the variables (Baum et al., Citation2013; Checherita-Westphal & Rother, Citation2012; Chikalipah, Citation2021; Chudik et al., Citation2015; Eberhardt & Presbitero, Citation2015; Lee et al., Citation2017; Ndoricimpa, Citation2020; Yang & Su, Citation2018; Égert, Citation2015). The current study follows the works of (Checherita-Westphal & Rother, Citation2012; Chikalipah, Citation2021; Eberhardt & Presbitero, Citation2015) and employ quadratic specification to explore threshold effect of debt on economic growth by adding square of debt (Lndebts) to Equationequation 2(2)

(2) .

Before diving in to running regression, however, the nature of possible interaction between debt and economic growth deserves emphasis. Rather than high debt incurred to slowdown economic growth rate, it is possible that low rate of economic growth to cause high debt, which create endogeneity problem (Baum et al., Citation2013; Checherita-Westphal & Rother, Citation2012, Chudik et al., Citation2015;; Panizza & Presbitero, Citation2013). The current study uses instrumental variable approach to deal with the possible reverse causality. Though instrumental variable approach is relatively simpler to implement, it is cumbersome when it comes to identification of relevant instrumental variables: the instrumental variable(s) should affect the endogenous variable in some ways (debt accumulation in this study), but not correlated with the residuals and, thus, does not directly influence the dependent variable. Accordingly, two external instrumental variables, namely exchange rate and interest rate on external debt were used in this study. A fall in US dollar makes debt costly to Ethiopia because the value of Ethiopian export denominated in us dollar declines, whereas the value of debt denominated in other currencies rises. The effect of interest rate on the amount of debt incurred is straightforward. The lower the interest, the cheaper will the debt incurred is. Moreover, according to (Nagou et al., Citation2021), the two variables significantly influence debt.

3.2. Data

The current study analyzes the relationship between public debt and economic growth for the Ethiopian case over the period 1982–2018. For this purpose, real GDP was used as dependent variable. Following various empirical model specification of economic growth and theories of economic growth determination, control variables such as trade openness, gross capital formation, human capital, population growth, employment, government consumption, investment, and inflation are considered in this study. Exchange rate and interest rate were selected by the study to be used as external instrumental variables. Concerning public debt, our variable of interest, public debt as percentage of GDP is used. The data on the mentioned variables are sourced from different international databases. Accordingly, the data on real GDP, employment, government consumption, gross capital formation, and trade openness were obtained from pen world table. Debt as percent of GDP was obtained historical database of the IMF while the data on debt as percent of GNI, investment and interest rate on external debt were sourced from international debt statistics of the World Bank. Regarding the human capital variable, expenditure on education was used and it was sourced from world development indicators along with inflation and population growth. The data on investment was accessed from world economic outlook and exchange rate data was collected from national bank of Ethiopia.

4. Result and discussion

Table depicts the result of descriptive statistics. For each variable, total number of observations is 37. The result shows that the data on all of the variables is characterized by low variability, as the value of standard deviation for respective variables is low. Over the study period, real GDP was averaged 13.14 (508,896 birr in level) while amount of public debt incurred on average was 4.29 (72.96 percent of annual GDP). On the average, therefore, more than the optimal threshold level of 66.75% of GDP, as documented by this study. Close examination of the result obtained shows that nearly three-fourth of annual national output is incurred as debt each year, which indicates high level of indebtedness of the country.

Table 1. Summary statistics

4.1. Unit root test

According to Menegaki (Citation2019), unit root test precedes all procedures in ARDL estimation. Among the alternative test methods, augmented Dicky Fuller (ADF), and Philips and Perron (PP) test are the most common. The two tests were preferred owing to advantages with them as they take care of serial correlation of the residuals. In both of these techniques, the null hypothesis of non-stationarity is tested against the alternative hypothesis of stationarity. The result of unit root test is given in Table . The result reveals that none of the variables is stationary at level except population growth, investment, inflation, and interest rate in case of all of the test techniques.

Table 2. Unit root test

However, the variables become stationary after first difference. In all cases, the test was conducted with constant and trend for each variable. Since no variables is integrated of order two (I(2)), we can proceed with ARDL estimation.

4.2. BDS test of nonlinearity of the variables

Following the works of Li and Guo (Citation2021); Mosikari and Eita (Citation2021), the variables under study were tested whether they exhibit nonlinearity characteristics or are chaotic. The test method is helpful as an initial inspection of the nature of possible relationship that exists between variables. Developed by Broock et al. (Citation1996), the test method tests the null hypothesis of independence and identical distribution of a series. As shown in Table , however, the null hypothesis cannot be accepted (except for inflation for some dimensions). Therefore, we conclude that all of the variables are nonlinearly distributed. This justifies inadequacy of liniar specifications and appropriateness of nonlinear specifications to study the relationship between variables considered by the current study.

Table 3. BDS test

4.3. Co-integration test

The current study employs ARDL based bounds test approach developed by Pesaran et al. (Citation2001) due to its superiority over the traditional co-integration tests like Engle and Granger (Citation1987) and Johansen (Citation1991). The latter, for instance, is too restrictive, as it requires all of the variables to be stationary only after the first difference, which is rare as far as macroeconomic variables are concerned. Moreover, the ARDL methodology provides reliable results even in the face of shorter sample size (Nadeem et al., Citation2020). Lastly, but by no means least, the ARDL methodology handles the problem of endogeneity in case endogenous predictors exist in the model (Rodríguez & Halicioglu, Citation2011). The result of cointegration test is given in Table . The test was performed for the linear, nonlinear, and threshold specifications and, as it can be observed from the table, there is strong evidence of long-run relationship between the variables. This conclusion is achieved because the computed F-statistics is greater than the upper bound critical value even at 1% level of significance in the three models. Because cointegration among the variables is detected consistently throughout the three models, it can be said that the result obtained is robust to different model specification.

Table 4. Cointegration test

4.4. The relationship between public debt and economic growth

The regression output indicating the long-run impact of public debt and the other predictors on economic growth of Ethiopia is reported in Table . Since long-run relationship between the variables is confirmed by cointegration test, it is possible to run a long-run model to examine the nature of relationship between public debt and economic growth. As indicated in Tables , the result from linear ARDL model reveals that public debt is detrimental to economic growth of Ethiopia both in the short run and in the long run, although its long-run effect is statistically negligible. Specifically, the study finding shows that a 10% increase in public debt is associated with slowdown in economic growth by 1.93% in the short run (Table ). This result is consistent with studies by Getinet and Ersumo (Citation2020); Atinafu (Citation2020); Gizaw and Ferede (Citation2020).

Table 5. The long-run model

Table 6. The short-run model

The result from NARDL model shows that negative shock (debt reduction) and positive shock (debt accumulation) in public debt are significant in explaining economic growth of Ethiopia only in the long run. As indicated in Table , debt accumulation fuels economic growth of Ethiopia because the coefficient of lnDebt_P is positive and statistically significant at 10%. On the other hand, since the coefficient of lnDebt_N is negative and significant at 1%, debt reduction results in slowdown of economic growth of Ethiopia in the long run. Specifically, it was found in this study that a 10% increase (decrease) in public debt causes economic growth to increase (decrease) by 4.29% and 4.23% in Ethiopia.

As reported in Table , the result from Wald test of asymmetry also shows that the relationship between public debt and economic growth is asymmetric in the long run and symmetric in the short run. The NARDL model result concerning the relationship between the variables appeared in extreme contradiction with what was recorded by the linear ARDL model. Therefore, it implies that linear models are misleading to isolate the relationship between debt and economic growth. Similar result regarding the negative and significant effect of debt reduction on economic growth was obtained by (Mosikari & Eita, Citation2021; Sharaf, Citation2021).

Table 7. Diagnostic tests, asymmetric tests, and the error correction term (ECT)

As an extension of the standard NARDL model, the multiple threshold nonlinear autoregressive distributive lag (MTNARDL) model was used in this study to make analysis of the relationship between public debt and economic growth more rigorous. Accordingly, two threshold levels were constructed at 25th and 75th. It would be better to introduce more thresholds in to the analysis, but due to small sample size considered by the study, doing so might produce unreliable results. The partial sum of debt less than the 25th quintile (rigeme1) captures the impact of minor change in debt, partial sum of debt between the 25th and 75th quintile (regime2) captures the effect of moderate change in debt and the partial sum above 75th quintile captures the effect of major change in debt. As presented in Table , moderate change in public debt is not significant in statistical terms in the long run. However, the minor change (regime1) is statistically significant with negative coefficient, which implies that extremely lower change in public debt adversely affect economic growth. On the other hand, the upper quintile (regime3) is significant with positive sign meaning that a major change in debt accelerates economic growth in the long run. Similar to its effect in the long run, a minor change in debt affect economic growth negatively in the short run. The result also reveals that extremely high changes in public debt negatively affect economic growth in the short run with some time lags. The result from Wald test further shows that asymmetric relationship between debt and economic growth presents in both the short run and long run.

Concerning the effect of the control variables, the impact of physical capital accumulation on economic growth is positive and statistically significant consistently throughout the models in both the short run and long run. The impact of population growth is significant only in the long run across the three models with positive coefficient. Trade openness seems not favorable for Ethiopian case, as the variable’s coefficient is negative and significant in the long run (linear ARDL) and in the short run (NARDL and MTNARDL). The human capital variable has positive sign throughout the specification, which means that it promotes economic growth of Ethiopia. However, its contribution is statistically significant only in linear ARDL in both short run and long run.

In general, the implication of the results obtained in this study is that reliance on linear models to examine the relationship between debt and economic growth in Ethiopia, though consistent with some theoretical predictions, hides crucial insights. These crucial insights are unraveled by the nonlinear models adopted in this study. As obtained in this study, debt reduction hampers economic growth while debt accumulation stimulates it. Most social welfare projects and various development projects are financed in the country with borrowed funds from external partner creditors and Ethiopian development bank and commercial bank of Ethiopia. No matter source of the borrowing, reduction in debt incurred retards these development investment activities and adversely affect economic growth eventually. And, if possible, a substantial increase (but not more than 66.75%) in debt produces favorable results.

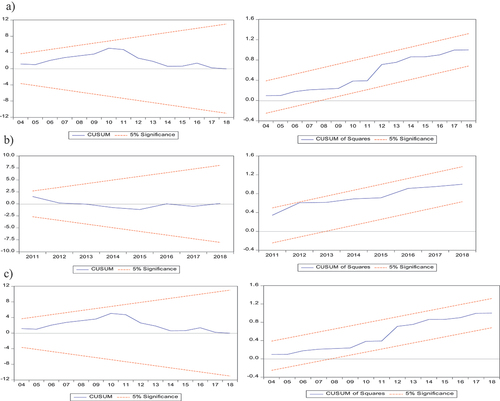

Diagnostic tests were performed and reported in Table to check acceptability of results obtained in each model. As the result reveals, the employed growth model is well specified, there is no problem of serial correlation of residuals, no heteroskedasticity problem, the residuals are normally distributed, the model is dynamically stable (see Figure ) and better fits to the data. The lagged error correction term (ECT) is statistically significant at 1% with negative sign in all models. The coefficient of ECT shows speed of adjustment toward long-run equilibrium. In case the ECT is between 0 and −1, the process of adjustment toward the long-run equilibrium is monotonic. On the other hand, the adjustment process is done in dampening and oscillatory way if the magnitude of the ECT is less than −1 (Narayan & Smyth, Citation2006). Accordingly, the result shows that it takes roughly two years to monotonically return to long-run equilibrium once shock is occurred in case of the linear ARDL model. As regards to the nonlinear models, the speed of adjustment is 128.2% and 139.6% for NARDL and MTNARDL model, respectively.

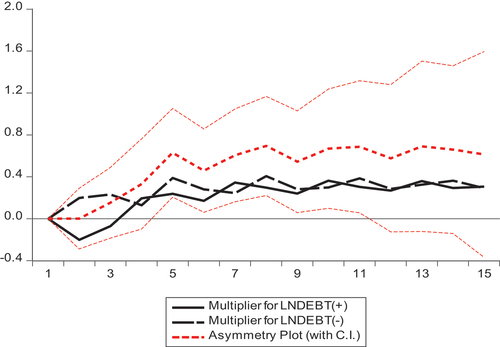

The dynamic multiplier effect of negative and positive shocks in debt on variations in GDP is shown in Figure . Dynamic multiplier graph shows asymmetric adjustment toward a new equilibrium position following a one period negative and positive recorded in the predictor variable of interest (Ullah et al., Citation2020). The dark smooth line represents asymmetric adjustment of positive shock while the dark broken line represents the asymmetric adjustment of the negative shock. The broken line in red color reveals the difference between the two shocks. Both of the shocks exhibit fluctuation in both long run and short run, but the fluctuation is greater in the short run. Since the broken red line is consistently never below the zero line, the liniar combination of positive and negative shock to debt if favorable to economic growth of Ethiopia. The adjustment process of the shocks also confirms the oscillatory speed of adjustment that was established by the lagged error term (ECT) with coefficient less than −1.

Figure 1. Dynamic multiplier graph.

4.5. Threshold regression

The threshold regression result is given in . As reported in the table, the threshold estimates of each variable varies across the two specifications (OLS versus TSLS), though the threshold effect of debt is maintained in both, which rationalize the use of instrumental variable regression.

Table 8. Threshold regression

The result further reveals that the threshold level of debt is equal to 4.201, which is equivalent to 66.75% of GDP. Below this threshold level, debt is beneficial to the economic growth of Ethiopia. Above the threshold level, however, debt is detrimental to economic growth of Ethiopia because its coefficient is negative and statistically significant at 1%. Specifically, a 1% increase in debt stimulates and cost the economy by 1.605% and 0.191%, respectively. Over the study period, the Ethiopian public debt amounts to log of 4.29 (72.966% of GDP) on average. Therefore, it can be said that Ethiopia is incurring too much public debt and, thus, putting the economy at stake. All of the control variables significantly and positively affect economic growth except trade openness, which has a negative effect. The sign of variable coefficients are in line with what was established by ARDL model. However, the coefficients are a bit higher in the two stage least square (TSLS) estimator. The result from model diagnostic tests shows that the results obtained are acceptable, as the instruments chosen were not under identified, strong, and over identification restriction is valid.

4.6. Robustness check

As a robustness check strategy, six different models were specified as can be seen from Table .

Table 9. Robustness check

In all of the models, two additional control variables (government consumption and inflation) were introduced. Models 1 through 4 were estimated with TSLS estimator while model 5 and 6 were estimated with fully modified ordinary least square (FMOLS) and dynamic ordinary least square (DOLS), respectively. The two additional regression models were considered to check whether the threshold effect is sensitive to choice of econometric models. In order to check whether the results obtained are sensitive to the variables selected, two additional control variables were introduced, investment and employment were, respectively, used instead of capital and population growth in model 2 and 4, and debt as percent of GNI and its square replaced debt as percent of GDP in model 3 and 4. The result reveals that, notwithstanding slight differences across the models, there is a threshold effect of debt on economic growth of Ethiopia, which underscores the nonlinear nature of relationship between debt and economic growth in the country. The result further shows that, the threshold estimate in model 1, 2, and 3 is, respectively, 4.122 (61.68%), 3.984 (53.73%), and 3.591 (36.27%), while it is 3.450 (31.50), 4.151 (63.49%), and 4.353 (77.71%) in model 4, 5, and 6, respectively. In model 3 and 4, the threshold estimate was so small because debt is measured as percent of GNI in those models.

Figure 2. (a) CUSUM and CUSUMQ for the linear ARDL model. (b) CUSUM and CUSUMQ for the NARDL model. (c)CUSUM and CUSUMQ for the MTARDL model.

5. Conclusion and policy implication

The relationship between debt and economic growth is among the controversial issues in public sector economics. The controversy arises from theoretical explanations and empirical findings. Prominent theoretical literatures predict positive (negative) relationship in the short run (long run). As regard to empirical literatures, not only is the sign of impact of debt on economic growth inconsistent, but also there is considerable variations in the nature of the relationship (linear versus nonlinear) documented by prior studies. As far as threshold effect is concerned, the estimated threshold values vary even in panel data studies depending on the time period considered, methodology adopted, and countries sampled, let alone to be magically unique for each country on the face of the earth. It is within this context that the current study was conceived. For this purpose, a time series data covering economic variables relevant for the study from 1982–2018 was collected from credible sources on annual basis. Various appropriate statistical and econometric tests were applied to insure acceptability of results obtained. Various robustness analyses were also performed to check whether results are sensitive to different specifications.

The result from linear ARDL model reveals that debt harms economic growth both in the long run and short run, though its long-run impact is statistically does not make a sense. Using NARDL model, It is also found that the relationship between debt and economic growth is asymmetric in the long run such that the impact of positive shock is positive and slightly higher the impact of negative shock, which is negative. The implication is that debt accumulation stimulates economic growth while its reduction is harmful. The impact of minor shock, moderate shock, and major shock in debt was also examined in this study. The results obtained from MTNARDL model shows that a minor shock slowdown the economy both in the long run and short run and the moderate shock is growth neutral. In the long run, the effect of a major shock to debt stimulates the economy whereas its effect in the short run is just the reverse. The asymmetric test of the model shows that the three scales of shocks exert asymmetric impact on economic growth in both the short run and long run.

An important lesson that can be drawn from NARDL and MTNARDL model the results is that the economy will be severely hit if government failed to secure borrowings due to some reasons (negative shock). The result obtained is also in line with the big push theory whereby a huge pool of resources should be mobilized to stimulate long-run economic growth. This conclusion is achieved because a major shock to debt is positive and statistically significant in the long run. Even though the threshold values are sensitive to different specifications, the threshold effect of debt on economic growth is established consistently. Accordingly, the estimated threshold level is 66.75% of GDP below (above) which it is favorable (detrimental) to the economy. Drawing on the results obtained, the study recommends that government of Ethiopia should create conducive environment that helps to secure more debts from potential creditors and at the same time, keep the annual debt well below 66.75% of GDP. Focusing on aggregate public debt data, the current study explored the nature of relationship between debt and economic growth. However, it would be better to look at disaggregated data (e.g. multilateral versus bilateral debt) to isolate the impact of debt on economic growth. Future studies also can build on the current study by analyzing the role of political and economic institutions in shaping the relationship between debt and economic growth.

Disclosure statement

No potential conflict of interest was reported by the author(s).

References

- Adam, C. S., & Bevan, D. L. (2005). Fiscal deficits and growth in developing countries. Journal of Public Economics, 4(4), 571–20. https://doi.org/10.1016/j.jpubeco.2004.02.006

- Asafo, S. S. (2019). External debt and economic growth: Two-step system GMM evidence for Sub-Saharan Africa Countries. International Journal of Business, Economics & Management, 6(1), 39–48. https://doi.org/10.18488/journal.62.2019.61.39.48

- Atinafu, W. (2020). External debt-growth nexus: Empirical evidence from Ethiopian economy. Economics, Management and Sustainability, 5(2), 6–27. https://doi.org/10.14254/jems.2020.5-2.1

- Baldacci, E., & Kumar, M. (2010). Fiscal deficits, public debt and Sovereign bond yields. IMF Working Paper WP/10/184. International Monetary Fund

- Barro, R. J. (1974). Are government bonds net wealth? Journal of Political Economy, 82(6), 1095–1117. https://doi.org/10.1086/260266

- Baum, A., Checherita-Westphal, C., & Rother, P. (2013). Debt and growth: New evidence for the euro area. Journal of International Money and Finance, 32, 809–821. https://doi.org/10.1016/j.jimonfin.2012.07.004

- Benli, M. (2020). The effect of external debt on long run economic growth in developing economies: Evidence from heterogeneous panel data models with cross sectional dependency. Theoretical and Applied Economics, 27(3), 127–138.

- Bidzo, M. M. (2018). Public debt and economic growth: A scissor effect in developing countries? The case of Gabon. Modern Economy, 9(10), 1672–1686. https://doi.org/10.4236/me.2018.910106

- Broock, W. A., Scheinkman, J. A., Dechert, W. D., & Lebaron, B. (1996). A test for independence based on the correlation dimension. Econometric Reviews, 15(3), 197–235. https://doi.org/10.1080/07474939608800353

- Burnside, C., Eichenbaum, M., & Rebelo, S. (2001). Prospective deficits and the Asian currency crisis. Journal of Political Economy, 10(6), 1155–1197. https://doi.org/10.1086/323271

- Chang, B. H. (2020). Oil prices and E7 stock prices: An asymmetric evidence using multiple threshold nonlinear ARDL model. Environmental Science and Pollution Research, 27(35), 44183–44194. https://doi.org/10.1007/s11356-020-10277-2

- Checherita-Westphal, C., & Rother, P. (2012). The impact of high government debt on economic growth and its channels: An empirical investigation for the euro area. European Economic Review, 56(7), 1392–1405. https://doi.org/10.1016/j.euroecorev.2012.06.007

- Chikalipah, S. (2021). Social sciences & humanities open Sovereign debt and growth in Zambia: Determining the tipping point. Social Sciences & Humanities Open, 4(1), 100188. https://doi.org/10.1016/j.ssaho.2021.100188

- Chudik, A., Mohaddes, K., Pesaran, M. H., & Raissi, M. (2015). Is there a debt-threshold effect on output growth? federal reserve bank of Dallas, globalization and monetary policy institute working papers, 2015(245). https://doi.org/10.24149/gwp245

- Chudik, A., & Pesaran, M. H. (2015). Common correlated effects estimation of heterogeneous dynamic panel data models with weakly exogenous regressors. Journal of Econometrics, 188(2), 393–420.

- Didia, D., & Ayokunle, P. (2020). External debt, domestic debt and economic growth: The case of Nigeria. Advances in Economics and Business, 8(2), 85–94. https://doi.org/10.13189/aeb.2020.080202

- Eberhardt, M., & Presbitero, A. F. (2015). Public debt and growth: Heterogeneity and non-linearity. Journal of International Economics, 97(1), 45–58. https://doi.org/10.1016/j.jinteco.2015.04.005

- Égert, B. (2015). Public debt, economic growth and nonlinear effects: Myth or reality? Journal of Macroeconomics, 43, 226–238. https://doi.org/10.1016/j.jmacro.2014.11.006

- Ehikioya, B. I., Omankhanlen, A. E., Osuma, G. O., & Inua, O. I. Dynamic relations between public external debt and economic growth in African countries: A curse or blessing?. (2020). Journal of Open Innovation: Technology, Market, and Complexity, 6(3), 88. https://doi.org/10.3390/JOITMC6030088

- Elmendorf, D. W., & Mankiw, N. G. (1999). Government debt. NBER Working Paper No. 6470. https://doi.org/10.3386/w6470

- Engle, R. F., & Granger, C. W. J. (1987). Co-integration and error correction: Representation, estimation, and testing. Econometrica, 55(2), 251–276. https://doi.org/10.2307/1913236

- Erhieyovwe, E. K., & Onovwoakpoma, O. D. (2013). External debt burden and its impact on growth: An assessment of major macro- economic variables in Nigeria. Academic Journal of Interdisciplinary Studies, 2(2), 143–154. https://doi.org/10.5901/ajis.2013.v2n2p143

- Faizulayev, A., Bakitjanovna, K. R., & Wada, I. (2020). Revisiting the dynamic impact of external debt on economic growth in Nigeria: Cointegration and conditional causality analysis. Journal of Public Affairs, 22(3). https://doi.org/10.1002/pa.2538

- Ganiev, J., Baigonushova, D., Madmarov, N., & Abdieva, R. (2020). External debt and economic growth in transition countries: Case of Kyrgyzstan. MANAS Sosyal Araştırmalar Dergisi, 9(1), 60–75. https://doi.org/10.33206/mjss.581860

- Getinet, B., & Ersumo, F. (2020). The impact of public external debt on economic growth in Ethiopia: The ARDL approach to co-integration. Journal of Economics & Sustainable Development, 11(11), 25–39. https://doi.org/10.7176/JESD/11-11-03

- Gizaw, G. E., & Ferede, T. (2020). Effect of public external debt on economic growth in Ethiopia. Journal of Economics & Sustainable Development, 10(13), 33–42. https://doi.org/10.7176/jesd/10-13-04

- Gövdeli, T. (2019). External Debt and Economic Growth in Turkey: An Empirical Analysis. Sosyoekonomi, 27(40), 119–130. https://doi.org/10.17233/sosyoekonomi.2019.02.07

- Grossman, G. M., & Helpman, E. (1991). Trade, knowledge spillovers, and growth. European Economic Review, 35(2–3), 517–526. https://doi.org/10.1016/0014-2921(91)90153-A

- Johansen, S. (1991). Estimation and hypothesis testing of cointegration vectors in Gaussian vector autoregressive models. Econometrica, 59(6), 1551–1580. https://doi.org/10.2307/2938278

- Kaas, L. (2016). Public debt and total factor productivity. Economic Theory, 61(2), 309–333. https://doi.org/10.1007/s00199-015-0900-0

- Keho, Y. (2021). Effects of real exchange rate on trade balance in Cote d’Ivoire: Evidence from threshold nonlinear ARDL model. Theoretical Economics Letters, 11(3), 507–521. https://doi.org/10.4236/tel.2021.113034

- Kourtellos, A., Stengos, T., & Ming, C. (2013). The effect of public debt on growth in multiple regimes. Journal of Macroeconomics, 38, 35–43. https://doi.org/10.1016/j.jmacro.2013.08.023

- Krugman, P. (1988). Financing vs. forgiving a debt overhang. National Bureau of Economic Research (NBER), Working Paper 2486.

- Lee, S., Park, H., Seo, M. H., & Shin, Y. (2017). Testing for a debt-threshold effect on output Growth. Fiscal Studies, 38(4), 701–717. https://doi.org/10.1111/1475-5890.12134

- Li, Y., & Guo, J. (2021). The asymmetric impacts of oil price and shocks on inflation in BRICS: A multiple threshold nonlinear ARDL model. Applied Economics, 1–19. https://doi.org/10.1080/00036846.2021.1976386

- Lucas, R. E., Jr. (2000). Some macroeconomics for the 21st century. Journal of Economic Perspectives, 14(1), 159–168. https://doi.org/10.1257/jep.14.1.159

- Mankiw, N., Romer, D., & Weil, D. (1992). A contribution to the empirics of economic growth. The Quarterly Journal of Economics, 107(2), 407–437. https://doi.org/10.2307/2118477

- Menegaki, A. N. (2019). The ARDL method in the energy-growth nexus field ; Best implementation strategies. Economies, 7(4), 105–116. https://doi.org/10.3390/economies7040105

- Modigliani, F. (1961). Long-run implications of alternative fiscal policies and the burden of the national debt. The Economic Journal, 71(284), 730–755. https://doi.org/10.2307/2228247

- Mohanty, A. K. (2017). External debt and economic growth in Ethiopia: A time series econometrics approach. International Journal of Researches in Social Science, 7(10), 574–602.

- Mosikari, T. J., & Eita, J. H. (2021). Asymmetric effect of government debt on GDP growth: Evidence from Namibia. Public Sector Economics, 45(4), 545–558. https://doi.org/10.3326/pse.45.4.7

- Munir, K., & Mehmood, N. R. (2018). Exploring the channels and impact of debt on economic growth: Evidence from South Asia. South Asia Economic Journal, 19(2), 171–191. https://doi.org/10.1177/1391561418794692

- Myers, S. (1977). Determinants of corporate borrowing. Journal of Financial Economics, 5(2), 147–175. https://doi.org/10.1016/0304-405X7790015-0

- Nadeem, M. A., Liu, Z., Ali, H. S., Younis, A., Bilal, M., & Xu, Y. (2020). Innovation and sustainable development: Does aid and political instability impede innovation? SAGE Open, 10(4), 215824402097302. https://doi.org/10.1177/2158244020973021

- Nagou, M., Bayale, N., Kouassi, B. K., & Camarero, M. (2021). On the robust drivers of public debt in Africa: Fresh evidence from Bayesian model averaging approach on the robust drivers of public debt in Africa. Cogent Economics & Finance, 9(1). https://doi.org/10.1080/23322039.2020.1860282

- Narayan, P. K., & Smyth, R. (2006). Higher education, real income and real investment in China: Evidence from granger causality tests. Education Economics, 14(1), 107–125. https://doi.org/10.1080/09645290500481931

- Ndoricimpa, A. (2020). Threshold effects of public debt on economic growth in Africa: A new evidence. Journal of Economics and Development, 22(2), 187–207. https://doi.org/10.1108/JED-01-2020-0001

- Ndubuisi, P. (2017). Analysis of the impact of external debt on economic growth in an emerging economy: Evidence from Nigeria. African Research Review, 11(4), 156–173. https://doi.org/10.4314/afrrev.v11i4.13

- Pal, D., & Mitra, S. K. (2015). Asymmetric impact of crude price on oil product pricing in the United States: An application of multiple threshold nonlinear autoregressive distributed lag model. Economic Modelling, 51, 436–443. https://doi.org/10.1016/j.econmod.2015.08.026

- Pal, D., & Mitra, S. K. (2016). Asymmetric oil product pricing in India: Evidence from a multiple threshold nonlinear ARDL model. Economic Modelling, 59, 314–328. https://doi.org/10.1016/j.econmod.2016.08.003

- Panizza, U., & Presbitero, A. F. (2013). Public debt and economic growth in advanced economies: A survey. Swiss Journal of Economics and Statistics, 149(2), 175–204. https://doi.org/10.1007/BF03399388

- Pattillo, C., Poirson, H., & Ricci, L. (2002). External debt and growth. Finance and Development, 39(2), 32–35. https://doi.org/10.2139/ssrn.879569

- Pesaran, M. H., Shin, Y., & Smith, R. J. (2001). Bounds testing approaches to the analysis of long-run relationship. Journal of Applied Econometrics, 16(3), 289–326. https://doi.org/10.1002/jae.616

- Rao, B. (2006). Time series econometrics of growth models: A guide for applied economists. MPRA Working Paper No. 3372, University of South Pacific

- Reinhart, C. M., & Rogoff, K. S. (2010). Growth in a time of debt. The American Economic Review, 100(2), 573–578. https://doi.org/10.1257/aer.100.2.573

- Ricardo, D. (1817). On the Principles of Political Economy and Taxation (John Murray, London). In P. Sraffa (Ed.), The Works and Correspondence of David Ricardo (Vol. 1). Cambridge: Cambridge University Press.

- Rodríguez, A., & Halicioglu, F. (2011). Testing the hypothesis of the natural suicide rates: Further evidence from OECD data. Economic Modelling, 28(1–2), 22–26. https://doi.org/10.1016/j.econmod.2010.10.004

- Romer, P. M. Endogenous Technological change. (1990). Journal of Political Economy, 98(5), S71–S102. https://doi.org/10.1086/261725

- Rumanzi, P. I., Turyareeba, D., Kaberuka, W., Mbabazize, R. N., & Ainomugisha, P. (2021). Uganda’s growth determinants : A Test of the Relevance of the Neoclassical Growth Theory. https://doi.org/10.4236/me.2021.121006

- Sharaf, M. F. (2021). The asymmetric and threshold impact of external debt on economic growth: New evidence from Egypt. Journal of Business and Socio-Economic Development, 2(1), 1–18. https://doi.org/10.1108/JBSED-06-2021-0084

- Shin, Y., Yu, B., & Greenwood-Nimmo, M. (2014). Modelling asymmetric cointegration and dynamic multipliers in a nonlinear ARDL framework. In R. Sickles & W. Horrace (Eds.), Festschrift in honor of Peter Schmidt (pp. 281–314). Springer New York. https://doi.org/10.1007/978-1-4899-8008-3_9

- Solow, R. M. (1956). A contribution to the theory of economic growth. The Quarterly Journal of Economics, 70(1), 65–94. https://doi.org/10.2307/1884513

- Solow, R. M. (1956). A Contribution to the Theory of Economic Growth.Quarterly. Journal of Economics, 70, 65–94. https://doi.org/10.2307/1884513

- Sulaiman, L. A., & Azeez, B. A. (2012). Effect of external on economic growth of Nigeria. Journal of Economics & Sustainable Development, 3(8), 71–79.

- Uche, E., & Effiom, L. (2021). Financial development and environmental sustainability in Nigeria: Fresh insights from multiple threshold nonlinear ARDL model. Environmental Science and Pollution Research, 28(29), 39524–39539. https://doi.org/10.1007/s11356-021-12843-8

- Ullah, A., Zhao, X., Abdul, M., & Zheng, J. (2020). Modeling the relationship between military spending and stock market development (a) symmetrically in China: An empirical analysis via the NARDL approach. Physica A: Statistical Mechanics & Its Applications, 554, 124106. https://doi.org/10.1016/j.physa.2019.124106

- Yang, L., & Su, J. (2018). Debt and growth: Is there a constant tipping point? Journal of International Money and Finance, 87, 133–143. https://doi.org/10.1016/j.jimonfin.2018.06.002