?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

This study examines the relationship between financial inclusion and women’s economic empowerment in the Ethiopian context. Scholars and development agents have long argued for the importance of access to financial products and services in achieving equitable economic growth and reducing poverty, particularly focusing on women. However, there is a limited understanding of how financial inclusion specifically impacts women’s economic empowerment in Ethiopia, and little evidence regarding the determinants of women’s financial inclusion within the country. This study attempts to address these research gaps. The empirical methods employed in this study include endogenous switching regression and instrumental variable methods. The data used in this study is from the Women’s module of the Ethiopian Demographic and Health Survey (DHS). The findings reveal a positive and statistically significant impact of financial inclusion on women’s economic empowerment in Ethiopia, indicating that greater access to financial services contributes to improved economic outcomes for women. These findings underscore the importance of collaboration between financial institutions, development agents, and policymakers to implement effective financial inclusion initiatives tailored to the Ethiopian context. Additionally, rigorous evaluation of these interventions is crucial to understand their specific effects and to ensure their successful implementation. By focusing on the Ethiopian case, this study contributes to our understanding of the relationship between financial inclusion and women’s economic empowerment in the country. The findings highlight the significance of prioritizing financial inclusion strategies in Ethiopia to advance gender equality, foster economic growth, and alleviate poverty.

1. Introduction

Women’s enhanced access to resources enhances not only their own well-being but also that of their entire family (Hashemi et al., Citation1996; Mayoux, Citation1998). This includes the reallocation of expenditures and prioritization of their children’s welfare, resulting in improved health and educational achievements (Doss, Citation2013; Duflo, Citation2003, Citation2012). Recent studies conducted in Ethiopia align with these findings, indicating that economically affluent mothers possess better means to protect their daughters from early marriage, ensuring improved future prospects (Muchomba, Citation2021). Additionally, a study focusing on Ethiopian women in Debre-Birhan town highlights the critical role played by women’s active engagement in economic activities in alleviating household poverty (Muchomba, Citation2021). Consequently, women’s empowerment extends its positive effects beyond the women themselves, benefiting a significant number of individuals within their families and communities.

However, pervasive gender inequality continues to persist globally and is intrinsically tied to underdevelopment (Jayachandran, Citation2015). Within most Global South countries, women often lack control over economic resources and face higher poverty rates compared to men (Munoz et al., Citation2018). For instance, in developing countries, a significant proportion of married women depend on their husbands for major financial decisions and lack autonomy over household finances (United Nations, Citation2015). Moreover, most women are not consulted on the utilization of their own household’s financial resources (United Nations, Citation2015). Furthermore, women encounter numerous obstacles in pursuing education, securing employment beyond domestic roles, owning property or land, and inheriting assets (Kabeer, Citation2001). Ethiopia is not an exception to these challenges. In 2021, Ethiopia obtained an overall gender gap index score of 0.69, positioning it 97th out of 156 countries globally (Statista, Citation2022). Notably, the country scored relatively low in terms of economic participation and opportunity, garnering a score of 0.56. This signifies the significant obstacles women face in accessing economic assets, thus impeding their agency in economic development. These realities underscore the importance of examining strategies aimed at empowering women, which serves as the central focus of this study.

The next question pertains to the methods of empowering women from developing countries, including Ethiopia. Bill and Melinda Gates Foundation has been at the forefront of advancing financial inclusion for a long time now (Hendriks, Citation2019)Footnote1 In her book, “The Moment of Lift,” Melinda Gates highlights the significance of empowering women through improved access to finance (Gates, Citation2019). The foundation’s efforts align with the understanding that financial inclusion plays a vital role in achieving equitable economic growth and poverty reduction (Cull et al., Citation2014). By promoting greater access to high-quality financial products and services, the foundation aims to enhance the lives of individuals, lower transaction costs, stimulate economic activity, and deliver social benefits (Cull et al., Citation2014; Gates, Citation2019). Recognizing the disproportionate impact of poverty on women, the foundation’s focus on increasing women’s financial participation is crucial for fostering inclusive growth and enabling women to become agents of change for themselves, their families, and society as a whole.

Notwithstanding this, the empirical question of whether financial inclusion empowers women remains unresolved. Existing research reveals significant gaps in literature. Firstly, there is limited study on the relationship between financial inclusion and women’s economic empowerment, necessitating further research to understand the importance of financial inclusion in empowering women economically. Similarly, there is a scarcity of research exploring the determinants of financial inclusion for women in developing countries like Ethiopia. Finally, it is important to highlight that the majority of existing research on financial inclusion for women in developing countries lacks comprehensive coverage and tends to be experimental in nature, often relying on methodologies such as randomized control trials. This narrow focus raises uncertainties regarding the generalizability of positive findings to different contexts beyond the specific settings where the experiments were conducted. For instance, the effectiveness of a savings tool that benefits women in Kenya may differ for a woman in Ethiopia (Dupas & Robinson, Citation2013). To address such questions, country-specific studies considering contextual factors are needed. In the context of Ethiopia, there is limited empirical work examining the potential of financial inclusion to empower a large sample of Ethiopian women, with the exception of a recent study by Nguse et al. (Citation2022) that reports a positive relationship between financial inclusion and women’s economic empowerment among registered women entrepreneurs in Addis Ababa. However, this study does not account for women in rural or other parts of Ethiopia and neglects empirical issues such as sample selection. Consequently, robust research on the link between financial inclusion and women’s economic empowerment in Ethiopia is still lacking. In light of these gaps, this study aims to investigate the impact of financial inclusion on women’s economic empowerment in Ethiopia. Additionally, the study seeks to identify the determinants of women’s financial inclusion in Ethiopia.

To investigate the link between financial inclusion and women’s economic empowerment for Ethiopia, the study utilizes data from the 2016 Ethiopian Demographic Household Survey. In order to establish causal inference, the study employs an endogenous switching regression methodology. The findings of the study reveal a positive and significant relationship between financial inclusion and women’s economic empowerment. Specifically, the results indicate that financially included women are approximately 7.7 percent more likely to be economicaly empowered compared to those who are not financially included. Furthermore, the study identifies several significant predictors of financial inclusion in Ethiopia. These predictors include owning a mobile phone, work history, education level, exposure to information, age, wealth, place of residence, sex of household head, and place of residence. Based on the results, it can be inferred that the the government of Ethiopia should develop and implement policies that promote financial inclusion. However, further research is required to gain a deeper understanding of the mechanisms through which financial inclusion enhances women’s economic empowerment. In practical terms, collaboration between financial institutions, development agencies, and other stakeholders is necessary to effectively implement financial inclusion initiatives targeted at women. Additionally, it is essential to evaluate the impacts of these interventions to ensure their effectiveness in promoting women’s empowerment.

The rest of this paper is organized as follows. Section 2 presents the existing research and the gaps thereof. The conceptual framework is presented in Section 3. Section 4 presents the empirical strategy. Data and variables are described in Section 5. The findings are presented in Section 6. Section 7 provides conclusions and policy recommendations.

2. Existing research

Women’s empowerment is an indicator of social change and a priority of the Sustainable Development Goals. There is a heated debate on what domains constitute women’s empowerment. Does financial inclusion empower women? If yes, how does financial inclusion affect certain outcomes for women? These questions are a subject of debate among scholars and development institutions. Financial inclusion may empower women by ensuring their financial stability, which better position women to accumulate money, make them adapt to economic shocks, and manage their finances more effectively even when their circumstances change (Mulili, Citation2020). Holvoet (Citation2005) compared the gender effects of two subsidized credit programs in Southern India and found that receiving credit transfers increases the decision-making power of the woman receiving the transfer. For Bangladesh, Pitt et al. (Citation2006) showed that women’s participation in micro credit programs helps to increase women’s economic empowerment. They have also documented a negative effect of male credit on women’s empowerment. Utilizing survey data encompassing 500 women in Bangladesh, Siddik (Citation2017) revealed that participation in financial inclusion programs leads to notable improvements in women's income, purchasing power, living standards, and familial roles. The study also brought to light that these initiatives empower rural women to effectively address emergencies, enhance their children's education, access improved medical facilities, and reduce dependence on local moneylenders.

Field et al. (Citation2021) examines how providing women with greater control over their earned income can influence their labor supply and gender norms. The researchers collaborated with the Indian government to offer rural women individual bank accounts and randomly varied whether their wages from a public workfare program were directly deposited into these accounts or into the male household head’s account. Women who received direct deposit and training increased their labor supply in the public and private sectors, and their gender norms became more liberalized in the long run. These effects were more pronounced in households with lower levels of female work and stronger norms against it, resulting in increased empowerment for women. The results suggest that increased bargaining power from greater control over income can interact with and influence gender norms.

Using a Randomized Control Trail (RCT) , Dupas and Robinson (Citation2013) investigate whether limited access to formal savings services hinders business growth in Kenya. The researchers provided access to non-interest-bearing bank accounts to market vendors (mostly women) and bicycle-taxi drivers in rural Kenya through a randomized experiment. The results showed that despite large withdrawal fees, a significant proportion of market women used the accounts, saved more, and increased their productive investment and private expenditures. However, there was no impact on bicycle-taxi drivers. The study highlights the significant barriers to savings and investment for market women in the study context and suggests a need for further research to understand those barriers and test whether the results generalize to other types of businesses or individuals. Also using an RCT, Ashraf et al. (Citation2010) examine the impact of an individually held commitment savings product in Philippines. They find that this saving product positively impacted on the female decision-making power within the household.

In their study on South Africa, Van Biljon et al. (Citation2018) suggest that financial inclusion can assist women in overcoming intra-household gender norms and increase their bargaining power within the household. They argue that this increased bargaining power, as a result of financial inclusion, can further help women to be externally empowered to enter the labor market. The authors found that financially included women are more likely to enter the labor force, indicating that financial inclusion can play a crucial role in enhancing women’s economic empowerment.

Therefore, financial inclusion is now widely recognized as a critical driver of women’s empowerment. However, it is crucial to acknowledge that gender disparities continue to persist, resulting in women facing heightened vulnerability to financial exclusion. Cicchiello’s (Citation2021) study examines the effect of gender disparity on the financial inclusion of women in the Middle East and North Africa (MENA) region. The findings reveal significant gender gaps in accessing formal and informal financial services, including ownership of financial accounts, mobile money accounts, credit cards, and usage of savings and credit products. Addressing these disparities is crucial to promote financial inclusion and enhance women’s economic empowerment in the MENA region. Expanding the analysis to least developed countries in Asia and Africa, Cicchiello et al. (Citation2021) explore the relationship between financial inclusion and development. The study identifies economic growth, literacy rates, unemployment, and gender inequality as factors influencing financial inclusion. It emphasizes the need for policies that enhance literacy, eliminate gender inequality, and promote pay equality to improve financial inclusion rates and foster development in these countries.

In a similar vein, Girón et al. (Citation2021) investigate the determinants of financial inclusion in least developed countries in Asia and Africa. Their study highlights the exclusion of young people and women from financial inclusion and underscores the importance of education and income as key factors in increasing financial inclusion. Additionally, the study demonstrates a positive correlation between financial inclusion and official savings, indicating the role of financial inclusion in promoting development. Examining gender inequality in financial inclusion within the Middle East and North Africa, Kazemikhasragh et al. (Citation2022) find lower financial inclusion rates for women in the region. The study identifies gender, age, education, and income as significant determinants of financial inclusion. It emphasizes the need for policy interventions to address gender disparities and enhance financial inclusion, as this can contribute to higher levels of official savings and overall development.

While available studies contribute valuable insights into gender disparities in financial inclusion, there is a noticeable research gap concerning Ethiopia. If any, the existing literature on financial inclusion primarily consists of cross-country studies. Ethiopia, as a developing country, faces unique socio-economic challenges that require specific attention. Conducting further research in Ethiopia is crucial for several reasons. Firstly, Ethiopia’s distinct socio-cultural and economic landscape necessitates tailored approaches to effectively address financial inclusion and gender disparities. Secondly, understanding the specific barriers and challenges faced by Ethiopian women in accessing financial services can inform policymakers and stakeholders in designing targeted interventions. Lastly, evidence-based strategies that directly address financial inclusion and gender disparities within Ethiopia can better support the country’s development goals and aspirations.

That said, however, limited research has been conducted to examine the correlates of financial inclusion in Ethiopia. Bekele’s (Citation2023) comparative study of financial inclusion in Kenya and Ethiopia offers valuable insights into the determinants and barriers of financial inclusion at both macro and micro levels. The study reveals that Kenya exhibits a higher level of financial inclusion compared to Ethiopia, with differences in financial liberalization policy, gross domestic product, rural population percentage, and mobile money service expansion explaining some of the macro-level variations. At the micro-level, factors such as literacy rates, means of receiving payments, gender, age, employment status, and mobile phone ownership significantly impact financial inclusion. In the context of Ethiopia, Mossie’s (Citation2022) study focuses specifically on understanding financial inclusion within the country. Utilizing the World Bank’s 2017 Findex database, the study analyzes the drivers, barriers, and saving and credit behavior in Ethiopia. The findings indicate that education, wealth, gender, and age are associated with a higher level of financial inclusion, with income and education exerting a strong influence. Gender disparities in financial inclusion are attributed to women’s exclusion from the non-financial sector. Additionally, the study identifies variations in saving and credit behavior based on individual characteristics, such as younger and economically disadvantaged adults facing involuntary exclusion due to factors like proximity to financial access points and affordability, while older and wealthier individuals experience voluntary barriers like lack of funds and the presence of a family member’s existing account. The study emphasizes the need for targeted policies that address the specific needs of vulnerable population groups, including the poor, young, less educated, and women, to foster financial inclusion.

The existing literature on financial inclusion in Ethiopia, as elucidated by Bekele (Citation2023) and Mossie (Citation2022), offers significant insights into the determinants, barriers, and implications of financial inclusion in the country. However, further research is warranted, particularly with a focus on the gender dimension. The present study aims to address this research gap by examining the correlates of financial inclusion among a specific sample of women in Ethiopia. Unlike the aforementioned studies that provide a broader perspective on financial inclusion in Ethiopia, this study specifically concentrates on women, aiming to delve into the unique challenges and opportunities they encounter in accessing and benefiting from financial services. The outcomes of this study will contribute to a deeper understanding of the gendered aspects of financial inclusion and offer valuable insights to policymakers and stakeholders for the development of targeted strategies aimed at enhancing financial inclusion and promoting women’s empowerment in Ethiopia.

Likewise, the role of financial inclusion in women’s empowerment remains a relatively understudied in the context of Ethiopia, particularly among rural women and with a focus on a larger sample of women in different regions of the country. While existing research has primarily focused on the macro-level impacts of financial inclusion, there is a notable gap in understanding the specific effects on rural Ethiopian women as well as women in other parts of the country. The study conducted by Nguse et al. (Citation2022) provides valuable insights into the role of government policies and regulations on women’s economic empowerment through financial inclusion, focusing on small and medium-sized enterprises (SMEs) in Addis Ababa. However, to fully grasp the impact of financial inclusion on women’s empowerment, it is essential to expand the scope of research to include a larger sample of women from diverse regions of Ethiopia. By examining the correlates of financial inclusion among rural and urban women across different parts of Ethiopia, future research can provide a more comprehensive understanding of the factors influencing women’s economic empowerment and inform targeted policies and interventions that address their specific needs and circumstances. This broader perspective will contribute to promoting gender equality, inclusive development, and women’s empowerment on a national scale.

3. Conceptual framework

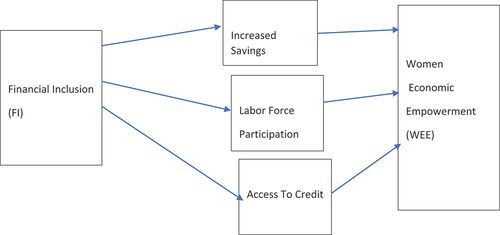

Figure presents theoretical mechanisms drawn from bargaining household models (Manser & Brown, Citation1980). Household bargaining theories posit that women’s earnings enhance their bargaining power within households. Building upon this framework, financial inclusion can contribute to women’s economic empowerment through at least three theoretical mechanisms. First, women included in the financial system are likely to save more and increase their productive investments and private expenditures. Dupas and Robinson (Citation2013) conducted a study in Bumala Town, Kenya, utilizing a randomized controlled trial (RCT) with a sample size of 250. Their research provided empirical support for the mechanisms through which financial inclusion enhances women’s economic empowerment. One of the key findings from their study was that women included in the financial system were more likely to save money. By gaining access to formal financial services such as savings accounts, women could securely deposit their earnings and build up savings over time. This ability to save not only provides a safety net for women during emergencies but also enables them to accumulate capital for investment purposes. Moreover, the study revealed that financial inclusion increased women’s engagement in productive investments. With access to credit and other financial resources, women could invest in income-generating activities such as starting or expanding a business. This increased economic activity not only benefits women individually but also contribute to the overall economic development of their communities. In addition to productive investments, financial inclusion also had a positive impact on women’s private expenditures. By having access to formal financial services, women could manage their finances more effectively and make informed decisions regarding household expenses. This, in turn, empowers women to have greater control over their financial resources and improve the well-being of themselves and their families (Agarwal, Citation1997; Dupas & Robinson, Citation2013; Karlan et al., Citation2016). Financial autonomy enhances women’s bargaining power and influence in decision-making processes (Benería & Sen, Citation1982; Johnson & Rogaly, Citation1997).

Figure 1. Conceptual framework.

Second, financial inclusion provides women with the opportunity to establish a financial identity by accessing formal financial services and building a credit history (World Bank, Citation2018). This enables them to demonstrate their creditworthiness and access loans and credit facilities (Demirgüç-Kunt et al., Citation2018). By having access to credit, women can invest in their businesses, expand economic activities, and generate income (Kabeer, Citation1999). This increased access to credit not only enhances women’s financial resources but also strengthens their entrepreneurial capabilities and economic independence. Furthermore, financial inclusion fosters women’s financial literacy and capacity to manage credit effectively. Through financial literacy programs and tailored financial education, women gain the knowledge and skills necessary to understand credit terms, make informed borrowing decisions, and manage their finances responsibly (Cole et al., Citation2011). This improved financial literacy empowers women to use credit strategically, invest wisely, and repay loans punctually, thereby enhancing their creditworthiness and building trust with financial institutions (Field et al., Citation2013). As women gain access to credit and develop a positive credit history, their economic empowerment is elevated. Access to credit provides them with the necessary financial resources to seize business opportunities, expand their enterprises, and invest in assets (Kabeer, Citation1999). This, in turn, increases their income generation, economic security, and overall financial well-being. Moreover, the ability to access credit empowers women to make autonomous financial decisions, exert control over their economic activities, and challenge traditional gender norms that restrict their economic participation (World Bank, Citation2018).

Third, financial inclusion plays a pivotal role in promoting labor force participation among women (Van Biljon et al., Citation2018). By providing access to credit, savings, and other financial services, financial inclusion empowers women to invest in their businesses, expand economic activities, and generate income (Kabeer, Citation1999). This increased labor force participation not only contributes to economic growth but also enhances women’s economic empowerment. As women become more actively engaged in the workforce, they gain greater control over their financial resources, decision-making power, and overall economic independence. Therefore, financial inclusion serves as a catalyst for labor force participation, which in turn increases women’s economic empowerment (Van Biljon et al., Citation2018).

4. Empirical method

The main aim here is to test the hypothesis that financial inclusion empowers an Ethiopian woman. To that end, one may estimate a specification of the form:

Where,

the measure of empowerment for the ith woman;

is an indicator of financial inclusion;

is the vector of controlvariables ; and

are normally distributed error terms.

In specification 1, the objective is to identify λ. However, identifying λ solely through observational data is challenging, if not impossible. Estimating λ is susceptible to both observed and unobserved sources of endogeneity. The process of self-selection into financial inclusion is likely to be highly systematic. These selection parameters, whether observed or unobserved, could also influence the dependent variable (WEE), making it difficult to isolate the impact of financial inclusion (FI).

To address this empirical issue, this study employs endogenous switching regression (ESR). ESR allows for controlling the biases that may arise from both observed and unobserved sources (Lokshin & Sajaia, Citation2004). The endogenous switching regression approach to estimating the impact of FI on WEE involves a two-step procedure (Wooldridge, Citation2015). Following Lokshin and Sajaia (Citation2004), we consider two regimes into which women are non-randomly sorted: those who are financially included and those who are not.

In the first step, we estimate the likelihood of a given woman being financially included using a probit regression of the form:

Where is a latent variable which depends on factors that affect the likelihood of being included financially;

is a vector of characteristics that influence the sorting of women into FI;

stands for unknown coefficient parameters; and

is a stochastic term.

In the second step, one derives separate WEE regressions financially included vs non included women. These regression functions can be given as follows.

and

stands for WEE status financially included and non- included groups respectively. The vectors

and

represent various socio-economic controls;

and

are unknown coefficient parameters;

and

are inverse mills ratios generated from the first stage estimation; and

and

are stochastic terms.

To identify the impact of FI on WEE, the Average Treatment effect on the treated (ATT) and/or the Average Treatment effect on the Untreated (ATU) should be estimated after the second-stage endogenous switching regression (Lokshin & Sajaia, Citation2004). To this effect, the expected values of the outcome variables for both affected and non-affected women will be estimated in both actual and counterfactual cases. The actual expected value of WEE outcomes for affected women is estimated as follows:

Similarly, the actual expected value of WEE outcomes for non-affected women is estimated as

Finally, to estimate ATT and ATU, the expected values of WEE outcomes in counterfactual cases should be estimated. Counterfactual indicates the expected values of WEE outcomes of affected women if they were not affected and the expected values of WEE outcomes of non-affected women if they were affected. Following Lokshin and Sajaia (Citation2004), the counterfactual of WEE outcomes for financially included woman had she not been included is estimated as

Using the same logic, the counterfactual of WEE outcomes for financially non-included woman had she been included is:

Following Imbens and Wooldridge (Citation2009), it is possible to calculate the average treatment effect on treated women (ATT). The impact of FI on those women that receive the treatment may be assessed as the difference between the expected outcomes in both regimes for the treated women. This can be done by combining EquationEquations (6)6

6 and (Equation8

8

8 ). That is, the average treatment effect on the treated (ATT) is obtained as:

And the average treatment effect on the untreated (ATU) is estimated as:

The endogenous switching model (also known as the Roy model or the type 5 Tobit model) is often applied in evaluation studies. The original implementation of this model relies on the strong assumption of joint normality of the error terms (Aakvik et al., Citation2005). In particular, the model depends on the assumption of trivariate joint normality of the stochastic terms,

, and

which can be stated as:

Where is the variance of the disturbance term of the selection equation in the first stage of the estimation;

and

are the variance of the disturbance terms of the two outcome equations in the second step of the estimation;

are the covariance between the disturbance terms of the two outcome equations. Since the two outcomes—being affected and non-affected—cannot occur simultaneously for a particular woman, these variances cannot be defined.

and

measure the covariance between the selection equation and the outcome equations in each of the two regimes. If this covariance is statistically different from zero, there is a problem of endogeneity.

When employing endogenous switching regression (ESR), two issues require attention. The first pertains to the assumption of normality in ESR. As indicated, ESR relies on the joint normality assumption, and violating this assumption can lead to inconsistent estimates (Radicic et al., Citation2016). To address this, Smith (Citation2003) introduced the copula switching regression (CSR) approach, which allows for different joint distributions in the error terms between the outcome and selection equations (Hasebe, Citation2013). Copulas represent joint distribution functions that bind the marginal distributions of the error terms in the selection and outcome equations, independent of the specific marginal distributions themselves (Smith, Citation2003, Citation2005). There are several types of copulas available, including Gaussian, Frank, Plackett, Clayton, AMH, FGM, Joe, and Gumbel. These copulas offer various ways to model the dependence between the error terms, allowing for more flexibility in capturing different dependence patterns (Hasebe, Citation2022; Smith, Citation2003; Trivedi & Zimmer, Citation2007). Another advantage of the copula method is its ability to estimate the model using the maximum likelihood method. This means that the estimates derived from the copula approach are efficient, making the most use of the available data (Hasebe, Citation2022). In summary, the copula switching regression approach addresses the violation of the joint normality assumption by utilizing copulas, which provide flexibility in modeling the dependence structure between the error terms. This method allows for more accurate estimation while ensuring efficiency through maximum likelihood estimation.

The second issue in endogenous switching regression (ESR) pertains to the necessity of having at least one excluded instrument for the estimation process. In order to achieve identification in the outcome equation of ESR, the inclusion of selection instruments is essential (Aakvik et al., Citation2005). According to the requirement, at least one significant variable from the selection equation should be excluded during the second stage of estimation when constructing the outcome equation. In line with this principle, this study utilized place of residence as a selection instrument. The rationale behind using place of residence as an instrument is that it is expected to be correlated with the selection into financial inclusion but should not have a direct impact on women’s economic empowerment. By including place of residence as a significant variable in the selection equation but excluding it from the outcome equation in the second stage of estimation, we meet the requirement for identification. Place of residence is often considered a proxy for various unobservable factors that may influence both the selection into financial inclusion and women’s economic empowerment. For example, it could capture regional differences in access to financial services or socioeconomic characteristics associated with specific areas. By using place of residence as an instrument, the study aims to address potential biases arising from these unobservable factors, improving the internal validity of the estimated impacts of financial inclusion on women’s economic empowerment.

5. Data

The main source of data is the Ethiopian Demographic Household Survey (EDHS).Footnote2 Of the data, we consulted the data pertaining to women. In the women’s questionnaire, DHS interviewed women about their literacy, employment history, decision-making capacity, fertility and fertility preferences, pregnancy prevention tools and other related topics (Croft & Allen et al., Citation2018). The women’s module of the DHS is the source of the data used for the analysis.

5.1. Measuring women economic empowerment

There is no readily available measure of Women Economic Empowerment (WEE). If anything, measuring women’s empowerment poses a challenge, as it is a complex multidimensional concept that can be measured in many different ways (Kabeer, Citation1999; Miedema et al., Citation2018). A growing body of research is attempting to overcome this challenge. This line of research uses and recommends Demographic and Health Surveys (DHS) as source of data on women’s empowerment (e.g., see Ewerling et al., Citation2017; Miedema et al., Citation2018; Williams et al., Citation2022). Following this line of research, this study constructs a DHS survey-based women’s empowerment index. This index is constructed from several questions from the DHS. The list of variables/questions used for constructing the index are reported in Table .

Table 1. DHS items for constructing the empowerment index

The DHS asks currently married women aged 15–49 on who decides over different domains: own health, daily household needs, large household purchases, and visits to family and relatives. Relevant answers include “I mostly decide”, “We consult each other and decide together”, and “My husband mostly decides”. The first two answers are coded as one and the rest as zero. Similarly, DHS asked currently married women aged 15–49 whether they agree a husband is justified in beating his wife. These questions are presented in Table . The relevant answers are 1 for “yes” and 0 for “no”. This variable is recoded such that higher values show disagreement to beating a wife.

To create the empowerment index, explanatory factor Analysis (EFA) analysis is applied. The first step in EFA is to determine if the data has the required characteristics. Data with limited or no correlation between the variables are not appropriate for factor analysis. Two criteria are used to test if the data are suitable for factor analysis.

These are the Kaiser-Meyer-Olkin (KMO) and Bartlett’s test approaches. The KMO and Bartlett test evaluate all available data together. A KMO value over 0.5 and a significance level for the Bartlett’s test below 0.05 suggest there is substantial correlation in the data. In our case, Bartlett test of sphericity rejects the null hypothesis of variables are not intercorrelated at the 1 percent. The KMO measure of sampling adequacy is 0.85. Thus, EFA is appropriate for constructing the index. Kaiser criterion suggests retaining those factors with eigenvalues equal or higher than 1. In our case, only the first two factors have eigenvalue of over 1. Factor 1 has eigenvalue of 3.19517 and Factor 2 has eigenvalue of 1.92100. Following these results, the measure of empowerment index is the first factor. Hereafter, we refer to this index as “WEE index”. As shown in Table , this measure ranges between −2.005 and 1.023. Higher positive values on this index corresponds to higher involvement of women in household decision-making as well as higher disagreement on attitudes towards beating wife.

Table 2. Summary statistics

5.2. Measuring financial inclusion

The key explanatory variable in this study is a measure of financial inclusion. Financial inclusion can be measured using various indicators, with the most common one being account ownership at financial institutions (e.g., see Asuming et al., Citation2019; Irankunda & Van Bergeijk, Citation2020). Consistent with the existing literature, this study measures financial inclusion using a basic indicator, namely, account ownership at financial institutions.

The question on account ownership is sourced from the 2016 Ethiopian DHS, as no similar data is available in the recent DHS for Ethiopia. The specific question asks women whether they have an account in a bank or other financial institution. The responses to this question are coded as 1 for “Yes” and 0 for “No”. In this study, this variable serves as a measure of financial inclusion. More specifically, the primary regressor in the analysis is a dummy variable representing financial inclusion, taking a value of 1 if a woman has an account in a bank or other financial institution, and 0 otherwise.

5.2.1. Controls variables

Control variables were extracted from the EDHS dataset for analysis. These variables encompass the respondent’s education, work history, age, wealth status, places of residence, and access to information. Table presents the summary statistics for these variables. As shown in Table , out of the total sample of 15,683 married women, 2,953 have a bank account or are affiliated with another financial institution, and 10,335 reside in rural areas. Additionally, 7,162 women own a house, 5,325 own land, and 5,842 possess a mobile phone. The wealth index ranges from −2 to 1.

6. Results and discussion

6.1. Determinants of women financial inclusion in Ethiopia

Table reports the estimation results from copula switching regression (CSR). The estimates for the selection equation and for the two outcomes (regime 0 and regime 1) equations are presented. In all columns, the unit of observation is the ith woman. In column 2, the dependent variable is the measure of financial inclusion. In column 3 and 4, the dependent variable is the empowerment index.

Table 3. Results of copula switching regression

Column 2 of Table presents the findings of the selection equation, which examines the determinants of women’s financial inclusion. The variables included in the selection equation are consistent with the existing literature on financial inclusion. For instance, Mossie’s (Citation2022) study conducted in Ethiopia identifies education, wealth, and age as factors associated with a higher level of financial inclusion among women. Similarly, Bekele’s (Citation2023) comparative study on financial inclusion in Kenya and Ethiopia reveals that literacy rates, age, employment status, and mobile phone ownership significantly impact women’s financial inclusion. In the present study, these factors were also considered in the selection equation, and their effects on women’s financial inclusion were analyzed.

As depicted in column 2 of Table , one strong determinant of financial inclusion is education. In particular, the result reveal that in Ethiopia, educated women have a higher likelihood of being financially included. This finding is consistent with the research conducted by Hoernig and Maugeri (Citation2017) in Mozambique. The results are consistent with the findings of Kazemikhasragh et al. (Citation2022), who concluded that higher education is a significant and positive predictor of financial inclusion in the Middle East and North Africa region. It is worth noting that although a high proportion of girls in the Ethiopia enroll in primary school, only a small percentage continue their studies to the secondary level, and even fewer have the opportunity to attend university. This limited access to higher education directly affects the average levels of financial literacy among women and their overall familiarity with financial instruments. Based on these findings, one key recommendation is to prioritize access to education and training for Ethiopian women. Women with lower levels of education are less likely to start their own businesses, which contributes to limited entrepreneurial activity among women in the country. Furthermore, lower levels of education may decrease survival rates among women-owned businesses, emphasizing the importance of addressing the educational gap to promote the growth and sustainability of women-owned micro, small, and medium enterprises in Ethiopia. Additionally, women in Ethiopia may have lower financial literacy rates, posing challenges in navigating the loan market effectively. Factors such as limited or no credit history, incomplete financial statements, limited savings, and unreliable profit records compound the difficulties faced by women entrepreneurs in accessing credit and financial services, making women-owned enterprises less appealing to credit providers in Ethiopia.

Hence, in Ethiopia, it is crucial to concentrate on improving access to education and training for women. By addressing educational disparities and enhancing financial literacy, women entrepreneurs can overcome the challenges related to credit access and financial inclusion. This can be achieved through targeted educational programs that offer relevant technical and business training, empowering Ethiopian women to navigate the loan market more effectively and increasing their chances of business success. The recommendations for developing targeted financial literacy programs for rural Ethiopian women align with and follow the findings of a study conducted in South Africa by Steinert et al. (Citation2018). In their study, Steinert et al. implemented an RCT of a financial literacy program and observed evidence that such a program resulted in increased savings and improved financial self-efficacy. This implies that providing financial education and literacy programs specifically tailored to the needs of rural women in Ethiopia has the potential to positively impact their financial inclusion, similar to the outcomes observed in the South African study.

The study also reveals that rural Ethiopian women experience lower levels of financial inclusion, which aligns with similar findings in Mozambique and Tanzania as documented in FAO’s report (Citation2020). Interestingly, exposure to information through mediums like radio or television has a positive association with the likelihood of financial inclusion. This highlights a significant policy recommendation for rural Ethiopia. In particular, the present study indicates a positive correlation between access to information, such as watching television or listening to the radio, and financial inclusion. Additionally, owning a mobile phone serves as a positive predictor of financial inclusion. Building upon these findings, a crucial strategy emerges: the development and implementation of targeted financial literacy programs specifically tailored to meet the needs of rural Ethiopian women. These programs should prioritize empowering women by equipping them with the necessary knowledge and skills to effectively engage with financial services, make informed financial decisions, and manage their finances. By enhancing the financial literacy of rural Ethiopian women, they can overcome the challenges they face in accessing financial services and improve their likelihood of achieving financial inclusion.

These findings align with existing research. The Global Findex Database 2017 study by Demirgüç-Kunt et al. (Citation2018) highlights the role of information and communications technology (ICT) in promoting financial inclusion, which is consistent with the finding that access to information, such as watching television or listening to the radio, correlates positively with financial inclusion in Ethiopia. Ahmad et al. (Citation2023) and Asongu (Citation2013) emphasize the significance of information and communication technology (ICT) and mobile phones for promoting financial inclusion. The findings of these studies align with the finding that owning a mobile phone positively predicts financial inclusion in Ethiopia. Moreover, Andrianaivo and Kpodar (Citation2012) demonstrate the positive impact of mobile phones on financial inclusion and gender equality in Sub-Saharan Africa, providing further support for the finding that owning a mobile phone is a positive predictor of financial inclusion in Ethiopia.

Another significant finding is the enduring financial exclusion experienced by rural Ethiopian women, emphasizing the need for targeted interventions. Research by Dupas et al. (Citation2018) underscores the transformative impact of banking services on previously unbanked individuals, highlighting the far-reaching implications of enhancing financial inclusion. To address the financial exclusion of rural Ethiopian women, strengthening the rural financial infrastructure is crucial. This can involve expanding the presence of formal financial institutions, such as banks, and establishing mobile banking units in rural communities. Emphasizing the use of technology and digital financial services can also play a pivotal role in improving accessibility for rural women facing geographical barriers (Roy & Patro, Citation2022). By leveraging these strategies, it is possible to enhance the availability and accessibility of financial services for rural Ethiopian women, promoting their financial inclusion and empowerment within the formal financial system.

Promoting women’s entrepreneurship and savings is another important policy recommendation. By providing targeted training programs, mentorship opportunities, and improved access to credit and savings mechanisms, rural Ethiopian women can be empowered to engage in entrepreneurial activities, generate income, and build assets. This, in turn, will contribute to their financial resilience and overall economic well-being. Lastly, fostering collaboration and partnerships among government agencies, financial institutions, civil society organizations, and international development partners is crucial. By pooling resources, knowledge, and expertise, stakeholders can work together to design and implement comprehensive and sustainable interventions that effectively address the financial inclusion gap for rural Ethiopian women.

Implementing these policy recommendations will contribute to reducing the disparities in financial inclusion faced by rural Ethiopian women. It will empower them to actively participate in the economy, improve their livelihoods, and contribute to overall economic development and poverty reduction efforts in rural communities.

6.2. Financial inclusion and women empowerment

6.2.1. Results from copula switching regression

The paper argues that selection into financial inclusion is likely. The results in Table confirm that this is indeed the case. The likelihood-ratio test for joint independence of the three equations is reported in the last row of Table . As reported, LR test statistic is 71 with p-value of zero. As such the null hypothesis stating the independence between the selection equation error term, and the different outcome equations is rejected. The last rows of the table show the strength of the dependence between the errors term of the selection equation and those of regime 0 and regime 1 outcome equations. The parameter atheta0 is significant at 1% and is less than one. This indicates that the errors terms are negatively dependent. Thus, the use of ESR is justified.

There are interesting results from the estimates of the two outcome equations. The results are given in Table . The first outcome equation is labeled as Regime 0. This gives the predicted values of WEE for the non-included women. In regime 0, only a few variables are statistically different from zero. In this regime, family size and owning a house are negatively correlated with WEE. Wealthy and educated women have higher WEE.

The second outcome equation is labeled as Regime 1. This gives the predicted values of WEE for the included women. When compared to regime 0, several variables statistically. In regime 1, family size and owning a house are negatively correlated with WEE. Wealthy and educated women have higher with WEE. These include owning a mobile phone, owning a house, education, exposure to news, age, wealth index, and age of the household head. This indicates that different factors matter for WEE across the two groups of women. In this case, it is less likely that the conditional independent assumption (CIA) holds.Footnote3 The implication is that it is not possible to estimate the impact of FI by accounting only observable factors. This is justifying the use of ESR.

6.2.1.1. Average treatment on the treated (ATT)

Table reports the average treatment effect estimates after copula switching regression. As shown, the average treatment effect on the treated is positive and is statistically significant at a 1% level of significance. This shows that financial inclusion has a significant effect on women economic empowerment. The average treatment effect on the untreated is negative and is also statistically significant at the 1% level of significance. This indicates that financially unincluded women’s economic empowerment is significantly lower since they are not financially included. The counterfactual for the financially non-included women is positive (1.05). This is an interesting finding with the implication that financial inclusion is an effective tool for WEE.

Table 4. Average treatment effect estimates after copula switching regression

6.2.1.2. Sensitivity analysis: estimates from instrumental variable (IV)

There can still be several concerns. The use of ESR requires that the decision to be financially included is internal to the woman. The fact that a woman has a bank account does not necessary mean that she made the decision to open it. The decision to open the bank account might be subject to a third omitted variable. If such omitted variable simultaneously affects FI and WEE, this introduces a reverse causality problem. It is also possible that the causation runs from WEE to FI rather than from FI to WEE. Similarly, having a bank account or not might not be a perfect measure of financial inclusion. Among other things, having a bank account does not show the intensity of treatment. Thus, the estimate from ESR is only indicative of the extensive margin.

To overcome, the endogeneity that might arise from measurement error and a reverse causation, instrumental variable (IV) is employed. The IV is a place of residence. It is a dummy that takes a value of 1 if a woman lives in rural area or 0 otherwise. In the sample and as can be seen from Table , 65.9% of women in the data live in rural areas.

The results from the IV method are presented in Table . Column 1 displays the IV estimates without any additional controls. Column 2 includes all the controls that were used in the CSR (Copula Switching Regression) analysis. In Column 3, Region Fixed effects are added, which capture the variations across all administrative regions of Ethiopia as reported in the 2016 DHS (Demographic and Health Survey) for Ethiopia. Lastly, Column 4 presents the results from the first stage, where the indicator of financial inclusion is regressed on the urban residence dummy variable.

Table 5. Results from using place of residence as instrumental variable (IV)

The results from column 4 of Table reveal a significant association between the instrumental variable (rural residence) and the likelihood of financial inclusion. Specifically, rural resident women are found to be less likely to be financially included compared to their urban counterparts. This suggests the presence of disparities in financial access and highlights the importance of targeting rural areas to improve financial inclusion for women. Moreover, the IV estimates, which consider the instrumental variable, are larger than the CSR (Copula Switching Regression) estimates. This indicates that the IV approach provides a more substantial estimate of the relationship between financial inclusion and women’s empowerment. The most conservative IV estimate, reported in column 3, is approximately 28 times larger than the CSR estimate. This suggests that the positive impact of financial inclusion on women’s empowerment is more pronounced when considering the instrumental variable. According to the IV estimates, financially included women are about twice as likely to be empowered compared to financially non-included women. This finding highlights the significant role that financial inclusion plays in promoting women’s economic empowerment. By providing access to financial services and resources, financial inclusion empowers women to enhance their economic status, pursue entrepreneurial activities, and improve their overall well-being.

6.2.1.3. IIV estimates (relaxing the exclusion restriction assumption)

The 2SLS estimate obtained here is valid only if the IV satisfies the instrument relevance and exclusion restriction conditions. The instrument relevance assumption requires that the IV and the endogenous regressors are strongly related. This assumption is said to be satisfied when the first stage F statistic is greater than 10. In this study, the first stage F statistic reported in Table demonstrates the relevance of the instrumental variable, namely the rural residence dummy. The F statistic, which exceeds 10, indicates a strong relationship between the instrument and the endogenous regressors. Therefore, the rural residence dummy serves as a relevant instrumental variable in this analysis.

The exclusion restriction assumption, which relates to the behavior of the unobservable error term, is challenging to directly test. As an alternative approach, the study relaxes this assumption and employs the “Imperfect Instrumental Variable” (IIV) framework proposed by Nevo and Rosen (Citation2012). The IIV method allows for the estimation of lower and upper bounds of the instrumental variable (IV) estimate. To utilize the IIV approach, three key assumptions must be satisfied.

Firstly, the instrument should have a (weak) correlation in the same direction as the omitted error term, replacing the exogeneity assumption of the typical IV method with an assumption regarding the sign of the correlation between the instrument and the unobservable error term. Secondly, the correlation between the instrument and the error term should be weaker than the correlation between the original endogenous variable and the error term. This implies that the IIV is less endogenous than the endogenous variable of interest (x). Lastly, the instrument (z) should be negatively correlated with the endogenous variable (x). These assumptions together form the foundation of the Imperfect Instrumental Variable (IIV) approach proposed by Nevo and Rosen (Citation2012). In essence, the IIV is an instrumental variable that shares the same direction of correlation with the unobserved error term as x but is less endogenous.

Table presents the IIV estimates based on the approach by Nevo and Rosen (Citation2012). As shown in Table , the estimated coefficient of financial inclusion falls between 2.179 and 0.162, with a confidence interval of 0.679 and 0.245. The ESR estimate from Table falls outside the confidence interval, while the IV estimates lie within the boundary of the confidence interval. Thus, the IIV estimates indicate that the findings remain consistent and robust, even when relaxing the exclusion restriction assumption. This offers valuable additional support for the relationship between financial inclusion and women’s empowerment. The results from the IIV method provide more confidence and strengthen the causal interpretation of the relationship between financial inclusion and women’s empowerment found using the IV or CSR methods.

Table 6. Nevo and Rosen (Citation2012)‘s imperfectIV bounds

These findings align with and contribute to the existing literature on financial inclusion and women’s empowerment. Similar to previous studies, this research emphasizes the crucial role of financial inclusion in empowering women and promoting gender equality. The results are consistent with the findings of Mossie (Citation2022) and Bekele (Citation2023), which highlight the positive associations between education, wealth, age, and financial inclusion. The study also expands on the existing literature by specifically focusing on a sample of women in Ethiopia, providing valuable insights into the unique challenges and opportunities they face in accessing and benefiting from financial services. Furthermore, this study adds to the literature by employing Copula Switching Regression (CSR) and instrumental variable (IV) analysis, which address endogeneity and reverse causation concerns. The robustness of the results is demonstrated through sensitivity analysis using the Imperfect Instrumental Variable (IIV) approach, which provides lower and upper bounds of the estimates. These methodological advancements enhance the validity and reliability of the findings, contributing to the methodological literature on financial inclusion and women’s empowerment.

7. Concluding remark

Women’s empowerment is widely recognized as a crucial element for driving social change, and it holds significant priority within the United Nations’ Sustainable Development Goals. However, there exists a contentious debate regarding the specific dimensions that encompass women’s empowerment. One policy recommendation put forth by scholars and institutions, including the Bill and Melinda Gates Foundation, is financial inclusion. Despite this recommendation, the factors that facilitate the advancement of such a policy and the actual impact of financial inclusion remain poorly understood, particularly in countries like Ethiopia. It is this research gap that serves as the motivation for conducting this study. Against this backdrop, the study aims to assess the determinants of financial inclusion and examine its impact on women’s empowerment in Ethiopia, utilizing data for a larger sample of Ethiopian women.

This paper examines the hypothesis that financial inclusion contributes to women’s economic empowerment using a larger sample of women in Ethiopia. The study utilizes data from the 2016 Ethiopian DHS and employs endogenous switching regression and instrumental variables to establish causal inferences. As hypothesized, the findings provide evidence that financial inclusion has a positive and significant impact on women’s economic empowerment. Additionally, the study documents that owning a mobile phone, having a working history, level of education, exposure to information, age, wealth, place of residence, sex of household head, and residence place are significant predictors of financial inclusion.

The paper contributes to the existing research on financial inclusion and its potential to empower women. It highlights that access to formal savings services can help women accumulate money, manage their finances effectively, and increase their decision-making power within the household. The control over earned income can also influence labor supply and gender norms, ultimately leading to increased empowerment for women. However, it is important to acknowledge that barriers to savings and investment exist for market women in certain contexts, necessitating further research to understand these barriers and their applicability to different business types and individuals. Overall, financial inclusion plays a crucial role in assisting women in overcoming gender norms and enhancing their bargaining power, thereby promoting empowerment and facilitating their entry into the labor market.

Based on the study’s results, it is recommended that Ethiopia prioritizes financial inclusion as a key strategy for promoting women’s economic empowerment. This entails expanding access to affordable financial products and services tailored to the needs of women, implementing financial literacy and education programs specifically designed for women, and promoting gender-sensitive policies and regulations within the financial sector. Additionally, efforts should be made to address structural barriers that hinder women’s economic empowerment, including gender-based discrimination, limited access to education and training, and constrained market opportunities. By emphasizing financial inclusion and addressing these structural barriers, Ethiopia can unlock the full economic potential of women, foster equitable and sustainable economic growth, and reduce the gender gap in financial inclusion.

To implement these recommendations, several options are available. Firstly, improving access to financial services is paramount. This can be achieved by expanding the availability of banking services, mobile banking, and digital financial platforms in rural and underserved areas. By increasing the reach of these services, women will have greater convenience and opportunity to open and manage financial accounts. Secondly, prioritizing financial literacy and education is crucial. Targeted financial literacy programs should be developed to equip women with knowledge and skills related to financial products, services, and effective financial management. Collaboration with educational institutions, NGOs, and community-based organizations can play a vital role in integrating financial education into existing programs for women.

Additionally, empowering women through entrepreneurship is a key strategy. This involves providing support and resources for women to start and grow their businesses. Initiatives such as business development services, mentorship programs, access to markets, and networking opportunities can enable women to become successful entrepreneurs and contributors to the economy. Moreover, promoting gender-responsive regulations and policies is essential. Advocacy efforts should focus on implementing policies that promote gender equality within financial institutions. This includes addressing discriminatory practices, ensuring fair access to financial services, and encouraging the representation of women in leadership and decision-making roles.

Lastly, fostering partnerships and collaboration is critical. It is important for government agencies, financial institutions, NGOs, and women’s organizations to work together to create an enabling environment for women’s financial inclusion. By pooling resources, sharing best practices, and coordinating efforts, stakeholders can maximize their impact and accelerate progress towards gender equality in financial access and empowerment.

Acknowledgments

The author acknowledges the support of the Ethiopian Economics Association (EEA) and the Bill & Melinda Gates Foundation for funding this research work through the Gender Profitability Project (GPG) summer school program. The author would like to express gratitude to the participants of the Validation Workshop on Women Empowerment in Ethiopia held by EEA on April 25, 2023, for their valuable insights and feedback. Lastly, We also thank Dr. GOODNESS AYE and anonymous reviewers of Cogent Economics & Finance for their valuable feedback, which has tremendously improved the quality of this paper.”

Disclosure statement

No potential conflict of interest was reported by the author(s).

Data availability statement

The data used in this study is the publicly available 2016 Demographic Household Survey (DHS) for Ethiopia.

Additional information

Funding

Notes

1. Watch Bill & Melinda Gates Foundation’s Financial Inclusion Portion of Gender Equality Strategy at https://www.youtube.com/watch?v=I9V_hud1wqU.

2. The data is accessed from the DHS website at https://www.dhsprogram.com.

3. The CIA assumption states that, after controlling for a set of observed covariates, treatment assignment is independent of potential outcomes. In several applications, CIA is referred to as unconfoundedness, exogenous selection, or selection on observables.

References

- Aakvik, A., Heckman, J. J., & Vytlacil, E. J. (2005). Estimating treatment effects for discrete outcomes when responses to treatment vary: an application to Norwegian vocational rehabilitation programs. Journal of econometrics, 125(1–2), 15–21.

- Agarwal, B. (1997). “Bargaining” and gender relations: Within and beyond the household. Feminist Economics, 3(1), 1–51. https://doi.org/10.1080/135457097338799

- Ahmad, A. H., Green, C. J., Jiang, F., & Murinde, V. (2023). Mobile money, ICT, financial inclusion and growth: How different is Africa? Economic Modelling, 121, 106220. https://doi.org/10.1016/j.econmod.2023.106220

- Andrianaivo, M., & Kpodar, K. (2012). Mobile phones, financial inclusion, and growth. Review of Economics and Institutions, 3(2), 30. https://doi.org/10.5202/rei.v3i2.75

- Ashraf, N., Karlan, D., & Yin, W. (2010). Female empowerment: Impact of a commitment savings product in the Philippines. World Development, 38(3), 333–344. https://doi.org/10.1016/j.worlddev.2009.05.010

- Asongu, S. A. (2013). How has mobile phone penetration stimulated financial development in Africa? Journal of African Business, 14(1), 7–18. https://doi.org/10.1080/15228916.2013.765309

- Asuming, P. O., Osei-Agyei, L. G., & Mohammed, J. I. (2019). Financial inclusion in sub-Saharan Africa: Recent trends and determinants. Journal of African Business, 20(1), 112–134. https://doi.org/10.1080/15228916.2018.1484209

- Bekele, W. D. (2023). Determinants of financial inclusion: A comparative study of Kenya and Ethiopia. Journal of African Business, 24(2), 301–319. https://doi.org/10.1080/15228916.2022.2078938

- Benería, L., & Sen, G. (1982). Accumulation, reproduction, and women’s role in economic development: Boserup revisited. Signs: Journal of Women in Culture & Society, 7(2), 279–298. https://doi.org/10.1086/493882

- Cicchiello, A. F. (2021). Gender disparity effect among financially included (and excluded) women in Middle East and North Africa. Economics and Business Letters.

- Cicchiello, A. F., Kazemikhasragh, A., Monferrá, S., & Girón, A. (2021). Financial inclusion and development in the least developed countries in Asia and Africa. Journal of Innovation and Entrepreneurship, 10(1), 1–13. https://doi.org/10.1186/s13731-021-00190-4

- Cole, S., Sampson, T., & Zia, B. (2011). Prices or knowledge? What drives demand for financial services in emerging markets? The Journal of Finance, 74(2), 831–863.

- Croft, T. N., Marshall, A. M., Allen, C. K., Arnold, F., Assaf, S., & Balian, S. (2018). Guide to DHS statistics. Rockville: ICF.

- Cull, R., Demirgüç-Kunt, A., & Morduch, J. (2014). Financial inclusion and development: Recent impact evidence. World Bank Policy Research Working Paper No. 7255.

- Demirgüç-Kunt, A., Klapper, L., Singer, D., Ansar, S., & Hess, J. (2018). The global findex database 2017: Measuring financial inclusion and the Fintech revolution. World Bank Policy Research Working Paper No. 8443.

- Doss, C. (2013). Intrahousehold bargaining and resource allocation in developing countries. The World Bank Research Observer, 28(1), 52–78. https://doi.org/10.1093/wbro/lkt001

- Duflo, E. (2003). Grandmothers and granddaughters: Old-age pensions and intrahousehold allocation in South Africa. The World Bank Economic Review, 17(>1), 1–25. https://doi.org/10.1093/wber/lhg013

- Duflo, E. (2012). Women empowerment and economic development. Journal of Economic Literature, 50(4), 1051–1079. https://doi.org/10.1257/jel.50.4.1051

- Dupas, P., Karlan, D., Robinson, J., & Ubfal, D. (2018). Banking the unbanked? Evidence from three countries. American Economic Journal: Applied Economics, 10(2), 257–297. https://doi.org/10.1257/app.20160597

- Dupas, P., & Robinson, J. (2013). Savings constraints and microenterprise development: Evidence from a field experiment in Kenya. American Economic Journal: Applied Economics, 5(1), 163–192.

- Ewerling, F., Lynch, J. W., Victora, C. G., van Eerdewijk, A., Tyszler, M., & Barros, A. J. (2017). The SWPER index for women’s empowerment in Africa: Development and validation of an index based on survey data. The Lancet Global Health, 5(9), e916–e923. https://doi.org/10.1016/S2214-109X(17)30292-9

- FAO. (2020). Deconstructing the gender gap in rural financial inclusion – the cases of Mozambique and Tanzania. https://doi.org/10.4060/cb0569en

- Field, E., Pande, R., & Rigol, N. (2013). Does the classic microfinance model discourage entrepreneurship among the poor? Experimental evidence from India. The American Economic Review, 104(5), 219–223.

- Field, E., Pande, R., Rigol, N., Schaner, S., & Troyer Moore, C. (2021). On her own account: How strengthening women’s financial control impacts labor supply and gender norms. The American Economic Review, 111(7), 2342–2375. https://doi.org/10.1257/aer.20200705

- Gates, M. (2019). The moment of lift: How empowering women changes the world. Flatiron Books.

- Girón, A., Kazemikhasragh, A., Cicchiello, A. F., & Panetti, E. (2021). Financial inclusion measurement in the least developed countries in Asia and Africa. Journal of the Knowledge Economy, 13(2), 1–14. https://doi.org/10.1007/s13132-021-00773-2

- Hasebe, T. (2013). Copula-based maximum-likelihood estimation of sample-selection models. The Stata journal, 13(3), 547–573.

- Hasebe, T. (2022). Endogenous models of binary choice outcomes: Copula-based maximum-likelihood estimation and treatment effects. The Stata Journal, 22(4), 734–771. https://doi.org/10.1177/1536867X221140943

- Hashemi, S. M., Schuler, S. R., & Riley, A. P. (1996). Rural credit programs and women’s empowerment in Bangladesh. World Development, 24, 635–653. https://doi.org/10.1016/0305-750X(95)00159-A

- Hendriks, S. (2019). The role of financial inclusion in driving women’s economic empowerment. Development in Practice, 29(8), 1029–1038. https://doi.org/10.1080/09614524.2019.1660308

- Hoernig, S., & Maugeri, N. (2017). Achieving greater financial inclusion in Mozambique: Challenges and the way forward. International Growth Centre.

- Holvoet, N. (2005). The impact of microfinance on decision‐making agency: evidence from South India. Development & Change, 36, 75–102. https://doi.org/10.1111/j.0012-155X.2005.00403.x

- Imbens, G. W., & Wooldridge, J. M. (2009). Recent developments in the econometrics of program evaluation. Journal of Economic Literature, 47(1), 5–86. https://doi.org/10.1257/jel.47.1.5

- Irankunda, D., & Van Bergeijk, P. A. (2020). Financial inclusion of urban street vendors in Kigali. Journal of African Business, 21(4), 529–543. https://doi.org/10.1080/15228916.2019.1695182

- Jayachandran, S. (2015). The roots of gender inequality in developing countries. Annual Review of Economics, 7(1), 63–88. https://doi.org/10.1146/annurev-economics-080614-115404

- Johnson, S., & Rogaly, B. (1997). Microfinance and poverty reduction. Oxfam Publishing. https://doi.org/10.3362/9780855988005

- Kabeer, N. (1999). Resources, agency, achievements: Reflections on the measurement of women’s empowerment. Development & Change, 30(3), 435–464. https://doi.org/10.1111/1467-7660.00125

- Kabeer, N. (2001). Conflicts over credit: Re-evaluating the empowerment potential of loans to women in rural Bangladesh. World Development, 29(1), 63–84. https://doi.org/10.1016/S0305-750X(00)00081-4

- Karlan, D., Kendall, J., Mann, R., Pande, R., Suri, T., & Zinman, J. (2016). Research and impacts of digital financial services (no. w22633). National Bureau of Economic Research.

- Kazemikhasragh, A., Cicchiello, A. F., Monferrá, S., & Girón, A. (2022). Gender inequality in financial inclusion: An exploratory analysis of the Middle East and North Africa. Journal of Economic Issues, 56(3), 770–781. https://doi.org/10.1080/00213624.2022.2079936

- Lokshin, M., & Sajaia, Z. (2004). Maximum likelihood estimation of endogenous switching regression models. The Stata Journal, 4(3), 282–289. https://doi.org/10.1177/1536867X0400400306

- Manser, M., & Brown, M. (1980). Marriage and household decision-making: A bargaining analysis. International Economic Review, 21(1), 31–44. https://doi.org/10.2307/2526238

- Mayoux, L. (1998). Participatory Learning for Women's Empowerment in Micro-Finance Programmes: Negotiating Complexity, Conflict and Change. IDS Bulletin, 29, 39–50. https://doi.org/10.1111/j.1759-5436.1998.mp29004005.x

- Miedema, S. S., Haardörfer, R., Girard, A. W., & Yount, K. M. (2018). Women’s empowerment in East Africa: Development of a cross-country comparable measure. World Development, 110, 453–464. https://doi.org/10.1016/j.worlddev.2018.05.031

- Mossie, W. A. (2022). Understanding financial inclusion in Ethiopia. Cogent Economics & Finance, 10(1), 2071385. https://doi.org/10.1080/23322039.2022.2071385

- Muchomba, F. M. (2021). Parents’ assets and child marriage: Are mother’s assets more protective than father’s assets? World Development, 138, 105226. https://doi.org/10.1016/j.worlddev.2020.105226

- Mulili, B. M. (2020). Financial inclusion as a tool for women’s economic empowerment in Africa: Achieving UN’s 2030 SDG. In O. Adeola (Ed.), Empowering African Women for sustainable development (pp. 133–143). Palgrave Macmillan. https://doi.org/10.1007/978-3-030-59102-1_12

- Munoz, A. M., Buitrago, P., Leroy De La Briere, B., Newhouse, D. L., Rubiano Matulevich, E. C., Scott, K., & Suarez-Becerra, P. (2018). Gender differences in poverty and household composition through the life-cycle: A global perspective. World Bank Policy Research Working Paper, (8360).

- Nevo, A., & Rosen, A. M. (2012). Identification with imperfect instruments. The Review of Economics and Statistics, 94(3), 659–671. https://doi.org/10.1162/REST_a_00171

- Nguse, T., Desalegn, G., Oshora, B., Tangl, A., Nathan, R. J., & Fekete-Farkasne, M. (2022). Enhancing women economic empowerment through financial inclusion: Evidence from SMES in Ethiopia. Polish Journal of Management Studies, 25(1), 270–291. https://doi.org/10.17512/pjms.2022.25.1.17

- Pitt, M. M., Khandker, S. R., & Cartwright, J. (2006). Empowering women with micro finance: Evidence from Bangladesh. Economic Development & Cultural Change, 54(4), 791–831. https://doi.org/10.1086/503580

- Radicic, D., Pugh, G., Hollanders, H., Wintjes, R., & Fairburn, J. (2016). The impact of innovation support programs on small and medium enterprises innovation in traditional manufacturing industries: An evaluation for seven European Union regions. Environment & Planning C: Government & Policy, 34(8), 1425–1452. https://doi.org/10.1177/0263774X15621759

- Roy, P., & Patro, B. (2022). Financial inclusion of women and gender gap in access to finance: A systematic literature review. Vision: The Journal of Business Perspective, 26(3), 282–299. https://doi.org/10.1177/09722629221104205

- Siddik, M. N. A. (2017). The does financial inclusion promote women empowerment? Evidence from Bangladesh. Applied Economics and Finance, 4(4), 169–177. https://doi.org/10.11114/aef.v4i4.2514

- Smith, M. D. (2003). Modelling sample selection using Archimedean copulas. The Econometrics Journal, 6(1), 99–123. https://doi.org/10.1111/1368-423X.00101

- Smith, M. D. (2005). Using copulas to model switching regimes with an application to child labour. The Economic Record, 81(s1), S47–S57. https://doi.org/10.1111/j.1475-4932.2005.00246.x

- Statista. (2022). Global gender gap index 2021. https://www.statista.com/statistics/1204236/global-gender-gap-index-score-by-country/.

- Steinert, J. I., Cluver, L. D., Meinck, F., Doubt, J., & Vollmer, S. (2018). Household economic strengthening through financial and psychosocial programming: Evidence from a field experiment in South Africa. Journal of Development Economics, 134, 443–466. https://doi.org/10.1016/j.jdeveco.2018.06.016

- Trivedi, P. K., & Zimmer, D. M. (2007). Copula modeling: An introduction for practitioners. Foundations and Trends® in Econometrics, 1(1), 1–111. https://doi.org/10.1561/0800000005

- United Nations. (2015). Integrating a Gender Perspective into Statistics. New York: UN Department of Economic and Social Affairs, Statistics Division. https://unstats.un.org/unsd/demographic-social/Standards-and-Methods/files/Handbooks/gender/Integrating-a-Gender-Perspective-into-Statistics-E.pdf