?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

The relationship between financial development and economic growth has been widely debated in the economics literature, but the results have been inconsistent and vary between the short and long run. In this study, we investigate the causal relationship between financial development and economic growth in Ethiopia using annual data from 1980 to 2021. We employ the Toda-Yamamoto causality test and the nonlinear autoregressive distributed lag (NARDL) modeling framework to analyze the data. Our results show that none of the variables are stationary at the level, but after applying first differences, all variables become stationary. Using the Toda-Yamamoto causality test, we find no causality running from financial development to economic growth, but there is evidence of reverse causality from economic growth to financial development. Furthermore, the NARDL model results suggest that economic growth drives financial development, and the relationship between financial development and economic growth in Ethiopia is nonlinear and asymmetric. Specifically, neither positive nor negative shocks to economic growth affect financial development in the short run, but both affect it in the long run and in joint short run and long run effects. We conclude from our study that financial development may not guarantee economic growth without building better institutions and following sound and stable fiscal policies. Consequently, constructing an effective economic growth strategy that maintains financial development is crucial. Our findings have significant implications for policymakers, academics, and investors and underscore the importance of informed decision-making based on a thorough understanding of the relationship between financial development and economic growth.

PUBLIC INTEREST STATEMENT

The present paper examines the causal relationship between financial development and economic growth in Ethiopia and challenges the conventional view that financial development is a prerequisite for economic growth. The paper finds that economic growth actually drives financial development, rather than the other way around. One possible explanation for this finding is that the Ethiopian financial system is relatively closed to foreign competition, has one of the lowest levels of financial inclusion in Africa and is not as well-developed as it could be. The findings have important implications for policymakers, as they suggest that focusing solely on financial sector reforms may not be sufficient for promoting sustainable economic growth. Instead, policies that promote broad-based economic growth may be more effective in stimulating financial sector growth. These findings will be of interest to anyone interested in understanding the complex relationship between financial development and economic growth in developing countries.

1. Introduction

Historically, debates about the link between economic growth and financial development have been ongoing since Bagehot (Citation1873), whose ideas were later popularized by Schumpeter (Citation1912), who argued that financial sectors drive innovation, leading to economic growth (Taivan & Nene, Citation2016). The field of endogenous growth theory has shown significant interest in the beneficial impact of financial development on the advancement of the economy. According to this theory, investing in financial development results in positive externalities and spill over effects within a knowledge- and technology-based economy, which ultimately leads to economic growth (Bencivenga & Smith, Citation1991; King & Levine, Citation1993).

As Bhole (Citation2004) (R. Levine, Citation1997), and (Luintel & Khan, Citation1999) assert that a robust financial system has the potential to greatly enhance economic growth by facilitating the mobilization of savings, directing resources towards the most profitable investments, minimizing transaction costs, spreading out risks, promoting innovation, and fostering technological advancements. Financial development leads to an increase in the range of financial services and transactions within a nation when money is being saved or transferred, which further leads to an enhancement in the country’s production and productivity (Omri et al., Citation2015). It is argued that financial development accelerates not only the economy but also creates job opportunities, reduces poverty and income disparity, by accumulating capital and introducing technological advancements, especially in developing nations (Abbas et al., Citation2022; Cetin et al., Citation2018; Honohan & Beck, Citation2007; M. R. Levine, Citation2021; Wen et al., Citation2021). At the same time, it is not rare to come across written works that state economic growth as the primary catalyst and powerhouse behind the progress of financial development. For example, Gurgul and Łukasz (Citation2011), and Song et al. (Citation2021) argue that as people’s incomes rise as a result of economic growth, so will their demand for financial services.

However, the causal relationship between financial development and the growth of a country’s national output has been a highly debated topic for many decades, but there is still little agreement on the issue (Bist & Read, Citation2018; Zhuang et al., Citation2009). Central to this debate is the question of whether solid economic growth is driven by financial development or the other way around. This question holds significant importance as identifying the causal relationship between financial progress and economic expansion can have crucial consequences for policymakers when devising suitable strategies and policies for growth and development

(R. Levine, Citation1997). The literature has well documented that previous empirical studies that employed various causality tests to examine the nature and direction of the causal relationship between financial development and national output growth produced mixed and inconsistent results (Akinci et al., Citation2014; Bist & Read, Citation2018; Durusu-Ciftci et al., Citation2017; Guru & Yadav, Citation2019; Haque et al., Citation2022; Jung, Citation1986; Khan & Senhadji, Citation2003; R. Levine, Citation1997; H. M. Nguyen et al., Citation2022; Nyasha et al., Citation2016; Odhiambo & Nyasha, Citation2022; Okuyan, Citation2022; Omoke, Citation2009; Opoku et al., Citation2019; Swamy & Dharani, Citation2019; Taivan & Nene, Citation2016; Wolde Rufael, Citation2009; Zhuang et al., Citation2009).

One or more reasons can explain why there are significant differences in the empirical results. One possible explanation is that the tests for causality can be affected by the omission of relevant variables, leading to omitted variable bias (Almassri et al., Citation2020). Using a bivariate model, one might conclude that financial development is not related to economic growth, but a multivariate model that includes other relevant variables may not necessarily confirm this. Furthermore, numerous previous studies failed to incorporate financial development into their estimates of production functions, though financial development is partly endogenous within an output equation. However, omitting the financial development variable can result in spurious conclusions regarding the financial development—economic growth nexus. Therefore, this leads to a strong bias towards favouring a connection between the two variables, regardless of their actual cause-and-effect association (P. T. Nguyen & Pham, Citation2021).

It was also evident during the literature review that significant financial investments, particularly in developing countries, are necessary to attain the Sustainable Development Goals (Tinta, Citation2022). However, the need to guide the existing financial system toward this goal requires further investigation of the relationship between financial development and economic growth (Odhiambo & Nyasha, Citation2022). There are also clear indications that the financial sector is still in its infancy in the East African region (of which Ethiopia is a part) and is dominated by government-owned banks (Worku, Citation2016), despite the fact that the banking sector has experienced growth in recent years as a result of branch expansion, total banking industry capital, deposit mobilization, and credit facilities (NBE, Citation2022).

Furthermore, to our knowledge, there are only a limited number of studies that investigate the relationship between financial development and economic growth in Ethiopia, and these studies have produced different results depending on the research methods and the financial development indicators used. Previous analyses have mainly used a narrow indicator of financial development, which is the credit available to domestic firms as a percentage to GDP, to proxy for financial development (See Table ). However, in accordance with the IMF’s 2016 working paper titled “Introducing a New Broad-based Index of Financial Development”, it is explicitly stated that the credit available to domestic firms as a percentage of GDP only accounts a quarter of the overall depth component within the realm of financial institutions (FI). Moreover, this depth component itself accounts for less than half of the subcomponent associated with financial institutions (FI) (Svirydzenka, Citation2016, p. 5). It would, therefore, be intriguing to see the effect of the broad-based financial development index on the economic growth, or vice versa.

Against this backdrop, the study’s overarching objective was to investigate the causal relationship between financial development and economic growth in Ethiopia using annual time series data between 1980 and 2021. In order to achieve this objective, the researchers have employed advanced and rigorous econometric techniques, including the Toda-Yamamoto causality test, which is commonly used for evaluating causal relationships in time series data, and the NARDL model, which enables the estimation of non-linear relationships among variables in time series data. This latter method is particularly valuable for examining the asymmetric effects of variables during different phases, such as expansion and contraction. By applying these advanced econometric techniques, the study enhances the methodological rigor of the analysis and contributes to the existing literature on the subject.

The examination of the causal relationship between financial development and economic growth in Ethiopia is of paramount importance for policymaking, investment decision-making, and academic research, as well as for advancing the overall economic growth of the country. The findings of this study can be used by policymakers to assess the causal link between financial development and economic growth, particularly in unstable economic environments. A comprehensive understanding of this relationship can also aid policymakers in formulating policies that encourage economic growth, which, in turn, can foster financial development. For investors, the study’s insights can be used to make informed decisions on resource allocation, identify opportunities for growth, and maximize returns. Additionally, this study can provide valuable insights to the existing body of academic research in the field of economics focusing on developing countries.

The remaining portion of the paper is structured in the subsequent manner: the next part concentrates on examining pertinent literature, succeeded by the methodology section. The penultimate section comprises the results section. The paper ends with a section discussing the conclusions and limitations.

2. Financial development and economic growth nexus: Theoretical framework

The relationship between financial development and economic growth has been studied long ago in economics (Akinci et al., Citation2014; Bist & Read, Citation2018; R. Levine, Citation1997) and has been well recognized and emphasized in economic development (Acemoglu, Citation2012; Gurley & Shaw, Citation1955). It’s important to be skeptical of the claim that financial development will always result in economic growth because it’s a highly intricate matter that is influenced by various factors. These factors include country-specific circumstances, the specific empirical model employed, the proxy that’s utilized to measure the level of financial development, and the method of data analysis employed (Nyasha & Odhiambo, Citation2018). Existing studies in the field have produced inconsistent results when examining the connection between financial development and economic growth (Bist & Read, Citation2018; Guru & Yadav, Citation2019; R. Levine, Citation1997; Odhiambo & Nyasha, Citation2022).

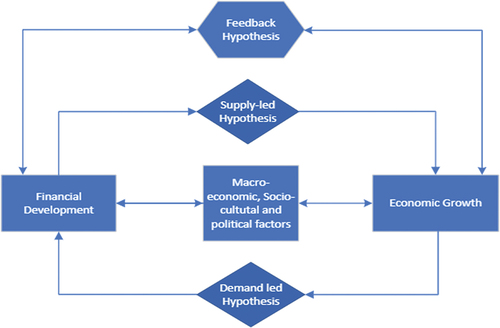

Based on the direction of the causality relationship, the approaches are categorized into four types namely, supply-leading, demand-following, feedback, and neutrality hypotheses. The supply-leading growth hypothesis is the first possibility, which states that an improved financial development policy can result in increased access to credit, investment opportunities, and financial services. These factors are considered to be the drivers of economic growth. This hypothesis proposes that modern financial systems can be the catalyst for economic growth, and the financial sector can become the main engine of growth. As a result of the expansion of the banking and financial services sector and the corresponding increase in capital inflows, the economic growth rate increased significantly. Durusu-Ciftci et al. (Citation2017), Bist and Read (Citation2018), Guru and Yadav (Citation2019) and Taddese Bekele and Abebaw Degu (Citation2021) found results that support the supply-leading hypothesis that financial development leads to economic growth, not the other way around.

However, there is also a clear argument for opposite causality, also known as the demand-following hypothesis, which stresses that financial development is a consequence, not a cause, of economic growth. According to this proposition, it is the economic growth that drives the need for financial institutions, assets, and services, which in turn promotes the development of the financial sector, instead of the reverse. For instance, Rajan and Zingales (Citation1998) suggested that economic growth creates investment opportunities, stimulates credit demand, and thus has a positive impact on financial development. Omoke (Citation2009) conducted an empirical analysis using Granger causality tests to investigate the relationship between financial development and economic growth in the case of Nigeria. Based on the Granger causality analysis, he found that there was no evidence to support the notion that financial development (measured by domestic credit, private credit, and broad money) causes economic growth. Instead, the results suggest that economic growth Granger-causes financial development, implying that growth-led financial development is the more likely scenario. Adeyeye et al. (Citation2015), Akinci et al. (Citation2014) and Haque et al. (Citation2022) supported the demand-following hypothesis. In general, this causal relationship between growth and the level of financial development could reflect that countries with higher income consume more financial services.

The third possibility is the feedback hypothesis, which proposes that there is a two-way causal relationship between financial development and economic growth. Almassri et al. (Citation2020), H. M. Nguyen et al. (Citation2022), Abbas et al. (Citation2022), Pradhan et al. (Citation2017), Swamy and Dharani (Citation2019) (Saqib, Citation2022; Vo et al., Citation2022), P. T. Nguyen and Pham (Citation2021) (Manta et al., Citation2020), Jung (Citation1986), (1999) and (Wolde Rufael, Citation2009) backed the idea that financial development and economic growth have a mutual cause-effect relationship. Proponents of this hypothesis emphasize the significance of a reliable and effective financial system in facilitating economic development. Simultaneously, economic growth can also drive the progress of finance by increasing the need for financial services and enhancing the profitability of financial intermediaries. The supporters of this approach also suggest that an efficient financial system can aid the economy in utilizing its trade openness effectively, leading to a rise in the country’s economic growth. Consequently, an improvement in the economic growth of the country can enhance the financial development, leading to an upsurge in the demand for financial services. Furthermore, the public will benefit from financial services due to their increasing demand, resulting in a positive effect on financial development (Faisal et al., Citation2019; Shahbaz et al., Citation2018).

The fourth possibility is the neutrality hypothesis, which stresses that no causal relationship exists in either of the flips (financial development-economic growth). Menyah et al. (Citation2014), Nyasha et al. (Citation2016), Opoku et al. (Citation2019), Odhiambo and Nyasha (Citation2022) and Okuyan (Citation2022) support this hypothesis.

Based on different theoretical frameworks, Figure illustrates the four possible hypotheses through which economic growth and financial development relate.

Figure 1. The possible causal relationship between Financial Development and Economic Growth.

To sum up, it is clear from the available literature that the relationship between financial development and economic growth has been a topic of extensive research, yet the literature lacks a consensus on their causal link. Current studies suggest that this relationship is multifaceted and context-dependent, with the influence of various internal and external dynamics of a nation shaping its outcome. Moreover, the particular model and dataset used may also impact the results (Samargandi et al., Citation2015). Research on this topic in Ethiopia is limited, and the existing literature uses a narrow measure of financial development, which may not provide a comprehensive understanding of the phenomenon or lead to specific policy implications. As a result, there is a research gap that needs to be filled by rigorous empirical methods to establish the causality between financial development and economic growth in Ethiopia. This study aims to address this gap by examining the validity of the four hypotheses in the Ethiopian context, providing a more comprehensive understanding of the relationship and potentially informing policies to promote financial development and economic growth in the country.

3. Data sources, model specifications and estimation methods

3.1. Data sources

The availability of reliable and long-term macroeconomic data sets is one of the most pressing issues in Ethiopia, and most of the data sets are not long enough to allow reliable and long-term analysis. For data consistency, therefore, attempts have been made to rely on international sources. The study uses annual secondary data covering a period of 42 years (1980–2021) and was obtained from the World Bank open database (data.worldbank.org), the IMF’s financial development index database (data.imf.org), the FRED economic data (fred.stlouisfed.org), the Bruegel dataset (www.bruegel.org) and the Penn World Table (Feenstra et al., Citation2015). This study used six variables to examine the relationship between financial development and annualized average growth rate of GDP per capita in Ethiopia. The variables are GDP per capita (Y), financial development (FD), capital (K), human capital (HC), trade openness (To) and real effective exchange rate (REER). A detailed description of the dependent variable, the independent variables, the measurement units, and the data sources is provided in Table .

Table 1. The variables used in the data analysis and their corresponding data source

3.2. Model specifications

Building upon the research referenced in the conceptual framework, the relationship between economic growth and financial development can be examined through the use of endogenous growth models (Bist & Read, Citation2018; Guru & Yadav, Citation2019; Haque et al., Citation2022; P. T. Nguyen & Pham, Citation2021). Several previous research works have shown that financial development, along with other economic, social, and political factors, affect economic growth. To examine the connection between financial development and economic growth in Ethiopia, this study established a simple empirical research model, represented by EquationEquation 1(1)

(1) .

Where Y, FD and X, respectively, represent the national production measured by the Gross Domestic Product per capita of the country at time t, financial development (FD) and the set of macro-control variables, including physical capital, human capital, trade openness and real effective exchange rate, while ε is the error term.

In order to ensure accurate and reliable results, the variables utilized in the research were transformed into their logarithmic form using the natural log. This was done to simplify estimations, reduce issues of heteroskedasticity, and yield more accurate results compared to a basic linear approach. Based on the definitions mentioned above, the time series model was transformed into its log-log format as:

indicates the intercept of the model,

is the coefficient of financial development (FD), and the coefficients

,

,

, and

represent Capital (K), Human Capital (HC), Trade Openness (To), and real effective Exchange Rate (REER), respectively. In the model,

is the error term.

In this model, the dependent variable is economic growth, which is measured by the logarithmic value of the gross domestic product per capita of the country at time t. The most crucial economic gauge for measuring a country’s level of development is Per Capita Income, which is computed by dividing a nation’s gross domestic product by its population (Beylik et al., Citation2022). The degree of economic progress and advancement in any given nation is contingent upon a multitude of variables (Aye et al., Citation2017), however, we have exclusively considered variables for which empirical data is accessible. The main factor that is being investigated as a cause of economic growth is the level of financial development (FD). Since the variable could not be measured directly, we used a proxy variable. Unlike other studies conducted in Ethiopia that used only domestic credit to the private sector as percentage of GDP as a proxy for financial development, the one we conducted uses a comprehensive measure of financial development developed by Svirydzenka (Citation2016). This broad-based index alternatively known as the IMF financial development index, which captures financial depth, access, and efficiency. Several empirical studies have shown that it is a better measure of financial development (Chen et al., Citation2020; T. A. N. Nguyen, Citation2022; Raifu & Afolabi, Citation2022).

The level of a country’s trade openness, which reflects how much it relies on foreign trade and is calculated by taking the ratio of the total value of trade to its gross domestic product, could also boost the technology index and consequently, lead to economic growth (Jalil & Rauf, Citation2021). This could be because trade spurs the diffusion of technology and the transfer of skills and knowledge, resulting in a more efficient allocation of resources and higher factor productivity, ultimately contributing to a country’s economic growth (Islam et al., Citation2022; Mtar & Belazreg, Citation2023). Furthermore, human capital accumulation improves a country’s innovation capability and ultimately economic growth (Romer, Citation1990). There is evidence from various empirical studies indicating that human capital plays a significant role in raising the level of technology adoption, which, in turn, leads to an increase in production and overall productivity (Mtar & Belazreg, Citation2023; Papalia et al., Citation2011).

Finally, a number of studies have empirically confirmed that real effective exchange rates drive a country’s economic growth trajectory and that its fluctuation or stability is the key factor that shapes the significance and behaviour of macroeconomic variables. Also, empirical research indicates that Real Effective Exchange Rates (REERs) can have a significant impact on the actual economic growth of low-income countries (Giordano, Citation2023). However, the relationship between real effective exchange rates (REERs) and economic growth is a complex and varies across countries and time periods. While some studies show that REER depreciation has a positive impact on economic growth, others suggest no significant relationship or even an intended effect. Eliminating the institutional and market failures that cause the economic distortions would be the optimal solution. However, it goes without saying that proposing this strategy to developing nations would be equivalent to advising them to “get rich to become rich.”. In light of these challenges, the impact of REER on economic growth remains indeterminate (Dani, Citation2009).

3.3. Estimation methods

In order to analyze time series data, different econometric techniques are used, including unit root tests, cointegration, estimation of long-run and short-run coefficients using the NARDL method, as well as the Toda-Yamamoto causality test (TY). We applied all these techniques in our analysis.

There is a tendency for time series data to be non-stationary or to change over time in terms of means, variances, and covariances. Therefore, it is essential to use unit root tests specifically designed to analyze and account for such non-stationarity (Hamilton, Citation1989). Based on the levels of integration of variables, unit root tests are an effective way to determine which co-integration method will be most appropriate for the specific data set. The concept of cointegration denotes that two or more time series variables are each non-stationary, yet their linear combination is stationary (Engle & Granger, Citation1987; Watson, Citation1994). There are several unit-root tests in the literature that can be used to check if a time series is stationary. In this study, the Augmented Dickey-Fuller (Dickey & Fuller, Citation1981), the Phillips-Perron (Peter & Perron, Citation1988), and the Dickey-Fuller Generalized Least Squares (Elliott et al., Citation1992) unit root tests were used to determine data stationarity. The Akaike information criterion (AIC) was used to examine the optimal lags for both the independent and dependent variables.

To examine the causal relationship between economic growth and financial development, we employ Toda and Yamamoto (Citation1995) Granger causality technique. This technique is notable because it doesn’t need to assess the cointegrating properties of the system beforehand, which helps to prevent any bias that might occur with unit root and cointegration tests. By doing so, the approach overcomes the problem of the traditional Granger causality analysis and is robust in accounting for the unit root and cointegration characteristics of the VAR system.

The test assumes that financial development (FD) and economic growth (EG) are two separate variables that may be related to each other. The method relies on the estimation of a VAR model with lag length p and maximum integration order d. This means that the VAR model, denoted as VAR (p + d), can be expressed in the following manner:

Where the vector consists of K endogenous variables, the intercept terms represented by the vector

, coefficient matrices are denoted by

and white noise residuals are represented by

. To test for Granger non-causality, the null hypothesis is that the first p parameters of the

element of

are zero, indicated by the notation:

:

.

Toda and Yamamoto (Citation1995) presented a Wald test statistic that has the property of asymptotically following the chi-square distribution with p degrees of freedom. This holds true regardless of the variables’ order of integration or cointegration properties. Wald statistics can therefore be used to test the null hypothesis of Granger non-causality in EquationEquation 3(3)

(3) .

Using the Toda-Yamamoto approach, one can formulate the following causality analysis equation for economic growth.

It is possible to construct equations for other series in a similar manner.

The relationship between financial development and economic growth in Ethiopia can also be investigated using the standard ARDL specification without asymmetry in short- and long-run dynamics, as described by Pesaran et al. (Citation2001) as follows.

where denotes the first difference operator and

represents the white noise term.

However, in several recent studies it has been shown that most economic fundamentals have nonlinear (asymmetric) dynamics (Kassi et al., Citation2023), and that the relationship between financial development and economic growth is not different (H. M. Nguyen et al., Citation2022; Odhiambo & Nyasha, Citation2022; Tinta, Citation2022). For instance, a negative shock might have a greater short run effect, while a positive shock might have a larger long run effect (or vice versa) (Udeagha & Breitenbach, Citation2023). Thus, the ARDL method may produce inaccurate results and unreliable conclusions. In order to address this issue, the research has adopted the nonlinear autoregressive distributed lags (NARDL) modeling technique proposed by Shin et al. (Citation2014) to capture the nonlinearity, asymmetries, as well as long- and short-term dynamics (Faisal et al., Citation2019), making it well suited for the investigation of the financial development-economic growth nexus in Ethiopia. The NARDL model computation is applied by many empirical researchers (Chen et al., Citation2020; Raifu & Afolabi, Citation2022; Uche & Effiom, Citation2021; Udeagha & Breitenbach, Citation2023).

The NARDL model is a generalization of the ARDL model that can accommodate departures from linearity in a way that is relevant to many integrated economic time series. It can also nest the linear ARDL model as a special case, which provides a means to test the hypothesis of linearity. The NARDL model uses partial sum decompositions of the explanatory variables to accommodate asymmetry (Cho et al., Citation2021).

The NARDL model differs from other nonlinear frameworks, like the smooth transition regression and the Markov-switching model, by utilizing partial sum decompositions to incorporate both nonlinear long-run relationship and nonlinear error correction (Udeagha & Breitenbach, Citation2023). So, following Shin et al. (Citation2014), to incorporate both short-run and long-run dynamics, the ARDL approach in EquationEquation 5(5)

(5) can be extended by replacing the variable

with

and

as follows:

where are the optimal lags derived from the Akaike information criterion (AIC).

represent the long-run coefficient and the positive and negative partial sums of financial development respectively. The intercept and coefficients of the control variables are represented by

respectively. Each variable has its own short-run coefficients represented by

,

,

,

.

We examine the potential long-run asymmetric relationship (cointegration) between the series using the test of Banerjee et al. (Citation1998) for testing

, against

and the

test of Pesaran et al. (Citation2001) for testing the joint null hypothesis

against the alternative hypothesis

as suggested by Shin et al. (Citation2014). The Wald test is used to determine whether there is asymmetry by testing the null hypothesis that

, where

, and

. If the null hypothesis is accepted (i.e., there is a symmetry between financial development and economic growth), EquationEquation 6

(6)

(6) will be transformed into EquationEquation 5

(5)

(5) ; if the null hypothesis is rejected, EquationEquation 6

(6)

(6) will become a co-integration NARDL with short- and long-run asymmetry.

The asymmetric dynamic multipliers can be used to quantify the asymmetric adjustment processes (responses) of economic growth to changes in financial development, as shown in EquationEq. (7)(7)

(7) below:

Note that as ,

and

, where

and

are the asymmetric long-run coefficients. On the basis of the estimated multipliers, we are able to see the direction of change from the old to the new equilibrium following a negative or positive shock, as well as the short-term disequilibria.

Finally, the present study also performs sensitivity analysis to check consistency and validity of long run dynamics using fully modified ordinary least squares (FMOLS) developed by Phillips and Hansen (Citation1990), canonical cointegrating regression (CCR) developed by Park (Citation1992) and dynamic ordinary least squares (DOLS) developed by Stock and Watson (Citation1993) econometric techniques to confirm the outcome from NARDL cointegration approach. We use the FMOLS and DOLS methods to correct for small-sample bias and take into account the possibility of serial correlation and endogeneity (Djeunankan et al., Citation2023).

4. Empirical results

4.1. Descriptive analysis of national output and financial development trends

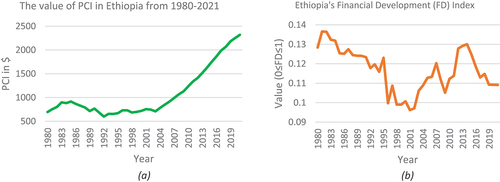

Figure shows a graphical representation of the main research variables, GDP and financial development. Despite the positive role of financial development in promoting economic growth, the level and growth rate of financial development remained very low in Ethiopia, as is clear from Figure . The country’s average financial development index is 0.116, making it one of the lowest in the world. As Figure clearly shows, economic growth has gone through upward and downward movements over time and has been strongly affected by political instability and civil war from 1980 to 1991 (Collier, Citation1999) and the Ethiopia-Eritrea war between 1998 and 2000 (Lata, Citation2003). In addition, Figure presents GDP trends that consistently increased from 2003 to 2021, albeit not at the same rate. This shows a country’s resilience in absorbing the shocks of global and domestic crises, as the economy’s performance is not severely affected.

Figure 2. Trend Analysis of GDP per capita and Financial Development Index in Ethiopia (1980–2021).

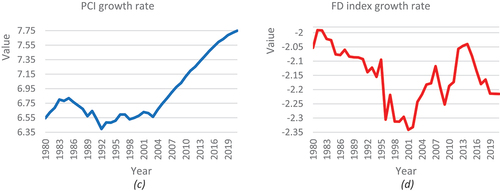

Figure 3. Trend Analysis of Financial Development Growth and Economic Growth in Ethiopia (1980–2021).

Moreover, a stable negative rate of financial development (varying around −2.2%) was observed in Ethiopia during the study period as clearly shown in Figure , indicating that the global economic situation did not significantly affect the sector. The reason for this might be that the financial system in Ethiopia is dominated by state-owned banks and relatively less integrated into the global economy, which might make it somewhat immune to some of the shocks and volatility experienced in other parts of the global financial system (Beck et al., Citation2014).

It can be seen from the graph that the trends in the growth of the financial development index and the economic growth curves do not show a positive correlation. However, correlation does not necessarily imply causation (Brooks, Citation2019), and we hypothesize that economic growth is influenced by financial development or vice versa.

4.2. Econometric analysis

4.2.1. Unit test results

In order to fully investigate the stationarity property of each variable and to identify the integration order, we first apply three conventional unit root tests. In this regard, the Augmented Dickey-Fuller test (Dickey & Fuller, Citation1981), the Philips-Perron test (Peter & Perron, Citation1988) and the Dickey-Fuller Generalized Least Squares (Elliott et al., Citation1992) were applied to all the variables of the study. As displayed in Tables , all the ADF, PP and ADF-GLS tests fail to reject the null hypothesis that all variables are nonstationary at level, with the exception of GDP growth, which is stationary at level. However, once the first difference is taken, all variables become stationary, indicating that the integration order of the variables is unique, and this excludes any time series spurious relationships of unit root property.

Table 2. Augmented Dickey-Fuller (ADF) unit root tests

Table 3. Philips-Perron (PP) unit root test

Table 4. ADF—GLS unit root tests

We next use stationary variables to construct the Toda Yamamoto model to test causality and the NARDL model to examine asymmetric cointegration, non-linear relationships, and long- and short-run dynamics (Faisal et al., Citation2019).

4.2.2. The Toda-Yamamoto approach for causality analysis result

Once the cointegration relationship among the variables has been identified, the next step is to estimate the Toda and Yamamoto (Citation1995) Granger noncausality test using the Wald test statistic, and the results are shown in Table . Based on the findings, the growth of financial development does not appear to be a Granger cause of economic growth, but the growth of human capital and trade openness are. Ethiopia has experienced significant economic growth in recent years, and human capital and trade openness are some of the factors that have contributed to this growth. The results also showed that the growth of GDP per capita, human capital and real effective exchange rate Granger cause of the growth of financial development in Ethiopia. Therefore, we conclude from the Toda-Yamamoto non-causality test results that economic growth is unidirectionally causal to financial development in Ethiopia in the sample period.

Table 5. Wald test statistic result

Overall, considering the findings of the study as shown in ), unidirectional causality was observed from economic growth to physical capital, economic growth to real effective exchange rate, trade openness to economic growth, financial development to capital, financial development to trade openness, real effective exchange rate to financial development, human capital to economic growth and human capital to capital. On the other hand, capital and financial development, human capital and real effective exchange rate, capital and trade openness, real effective exchange rate and capital, and real effective exchange rate and trade openness showed bidirectional causality. Finally, no causality was observed between human capital and trade openness in Ethiopia during the sample period considered.

4.2.3. NARDL cointegration analysis test results

To estimate how changes in economic growth and other independent variables asymmetrically affect the growth of financial development in both the short and long run, the NARDL framework was used. The results of the NARDL model have been reported only for financial development as a dependent variable. This is because, as shown previously in the Toda Yamamoto model, unidirectional causality runs from economic growth to financial development and also to preserve space. The values of other variables can be obtained from the authors upon request. The NARDL model findings indicate that the variables have a long-run relationship in the presence of asymmetry, which reinforces the reliability of our estimations.

Table shows how economic growth affects financial development in non-linear ways. Specifically, using the NARDL framework, we have identified both positive and negative long-term effects of economic growth on financial development. It can be seen from the table that economic growth has a significant effect on financial development in the long-run positive and negative effects, which is 1.113 and −1.386 respectively. The long run positive and negative effects of a 1% rise in the economy or a 1% drop will be 1.113% and rise or 1.386% drop in financial development, respectively. These effects have also been observed when both positive and negative shocks affect the variable simultaneously. In long-run asymmetric impacts, we read that both the one period lagged positive partial sum () and the one period lagged negative partial sum (

) changes in economic growth asymmetrically affect financial development. Therefore, the significant long-run coefficient by positive shock of economic growth (

) which is 0.808 demonstrates that increasing economic growth by 1% increases financial development by 0.804%. In the same fashion, in the long run, negative partial shocks of economic growth are seen to decrease financial development by 1.241%. Exploring short-run results, an increase or a decrease in economic growth doesn’t significantly influence financial development. In the short run, therefore, we observe no trade-off between economic growth and financial development.

Table 6. Full information estimates of the asymmetric effects of economic growth on financial development in Ethiopia with the NARDL approach

Turning to specific insights in Table , we reject the null hypothesis of long-run symmetry for GDP per capita growth rate at 5% significance levels, and we also reject the joint symmetry test for GDP per capita growth rate at all reasonable significance levels, but we fail to reject the null hypothesis of short-run symmetry for GDP per capita growth rate at all reasonable significance levels.

Table 7. Coefficient-Symmetry Tests

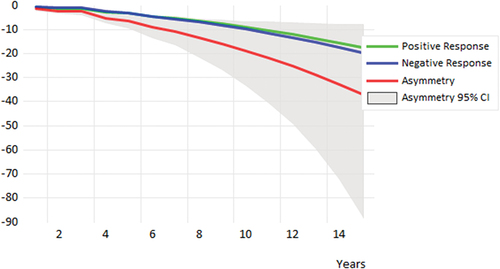

The results of the Conditional Error Correction model summarized in Table and the dynamic multiplier graph in Figure confirm the existence of a co-integrating relationship between the growth of GDP per capita and financial development growth. In fact, this co-integrating relationship is itself significant as the coefficient in the error-correction regression is highly significant.

Figure 4. Cumulative Dynamic Multiplier Graph: The effect of GDP per capita growth on the growth of financial development index shock evolution.

Table 8. Conditional Error Correction Results

Cumulative dynamic multipliers allow us to study the evolution of adjustment patterns following negative and positive shocks to asymmetric regressors and quantify the path of asymmetry as they evolve towards their respective (cointegrating) equilibrium states. As shown by the asymmetry curve and its associated 95% confidence interval, as the zero line is not located between the lower and upper bands in Figure , the asymmetric effects of GDP per capita growth is significant. The graph validates the significant asymmetric response of the financial development to shocks in GDP per capita. These findings reveal that there is an overall positive relationship between financial development and GDP per capita in Ethiopia since the cumulative effects of a positive change in GDP dominate the cumulative effects of a negative change in GDP per capita.

In order to ensure the validity and robustness of the results produced through NARDL testing approach, three different techniques were used: FMOLS, DOLS, and CCR. As seen in Table , the results of FMOLS indicate that GDP growth has a positive and significant impact on financial development growth. The results of DOLS and CCR are not significantly different from those of FMOLS, supporting each other. Consequently, the results of three alternative approaches support the results obtained from the Toda Yamamoto and NARDL testing approaches.

Table 9. FMOLS, DOLS, and CCR analysis

Thus, regardless of estimation methods, economic growth leads to financial development, not the other way around. This could be attributed to a variety of factors, including the fact that the financial sector is still not fully integrated into the Ethiopian economy to the point where it can influence economic growth.

5. Discussion

For many years, the financial development—economic growth hypothesis has been a topic of sustained interest and controversy in the economic development literature. This study improves upon previous studies by proposing a theoretically reasonable multivariate time series approach to investigate the financial development—economic growth causal relationship in the Ethiopian context using annual time-series data from 1980 to 2021.

The research utilizes Toda-Yamamoto and Nonlinear Autoregressive Distributed Lag (NARDL) models to explore the cause-and-effect connections between financial development and economic growth in Ethiopia. According to the Toda-Yamamoto causality tests, there is noteworthy one-way causation from economic growth to financial development. To put it differently, the findings of the present study reinforce the proposition that economic growth drives financial development (demand-following hypothesis).

The findings of this study are in line with some previous studies while contradicting others. Our results are largely consistent with previous research, which has generally found a causal relationship that runs from economic growth to financial development not the other way around. For instance, our findings are consistent with the observation of Adeyeye et al. (Citation2015), Akinci et al. (Citation2014) and Haque et al. (Citation2022) which predicted unidirectional causality running from economic growth to financial development. Additionally, our results are similar to Omoke (Citation2009) who used data from Nigeria to demonstrate that economic growth precedes the development of the financial system.

However, the findings of this study contradict the findings of some other studies such Teklu and Jemal (Citation2019), Durusu-Ciftci et al. (Citation2017), Taddese Bekele and Abebaw Degu (Citation2021), Bist and Read (Citation2018), and Guru and Yadav (Citation2019) which predict unidirectional causality running from financial development to economic growth. The results of this study also contradict the findings of Nyasha et al. (Citation2016), Almassri et al. (Citation2020), H. M. Nguyen et al. (Citation2022), Abbas et al. (Citation2022), Pradhan et al. (Citation2017), Swamy and Dharani (Citation2019), Vo et al. (Citation2022), Saqib (Citation2022), P. T. Nguyen and Pham (Citation2021) and Manta et al. (Citation2020) who found bidirectional causality between economic growth and financial sector development. The study also differed from Menyah et al. (Citation2014), Nyasha et al. (Citation2016), Opoku et al. (Citation2019), Odhiambo and Nyasha (Citation2022) and Okuyan (Citation2022), who reported no causal relationship between financial development and economic growth.

Our study results are also in contrast with the research conducted by Moyo et al. (Citation2018) in Brazil. They employed the Nonlinear Autoregressive Distributed Lag (NARDL) model to investigate the association between financial development and economic growth and reported that financial development had a significant and positive effect on economic growth, but the linkage between the two was nonlinear, which is similar to our findings. However, our findings do not support their claim of a significant positive impact of financial development on economic growth. The results of this study also somehow contradict those of Nyasha et al. (Citation2016) who found that both financial development and economic growth Granger cause each other in the short run and that a one-way causal relationship from financial development to economic growth in the long run in Ethiopia from 1980 to 2014.

The findings from the nonlinear autoregressive distributive lag (NARDL) model reinforce the proposition that economic growth drives financial development. However, our findings also offer some unique insights into this relationship. Specifically, we find that the relationship between financial development and economic growth is not linear (asymmetrical) in the context of Ethiopia. The results of the model further indicate that economic growth had non-linear (asymmetrical) impacts on financial development in Ethiopia. The model suggests that positive changes in economic growth had more favourable effects on financial development, especially in the long run, as opposed to their negative effects in Ethiopia.

Joint positive shocks to economic growth also had a positive impact on financial development. Our findings partially support the idea put forth by the NARDL model that a negative shock will probably have a greater short run impact, while a positive shock is more likely to have a greater long-run effect (Udeagha & Breitenbach, Citation2023). These asymmetrical effects might be caused by the macroeconomic environment and inefficient financial management.

The study findings differ from those of Teklu and Jemal (Citation2019), who used annual data from 1975 to 2016 to assess the nexus between financial development and economic growth in Ethiopia using multiple econometric regression protocols. According to their study, financial development leads to economic growth unidirectionally in both the short and long runs, leaving the issue unresolved. Various factors may have contributed to the variation in the results, such as the inclusion of additional macroeconomic variables; the use of a relatively recent sample period; and a different methodology.

Overall, our study adds to the ongoing debate on the relationship between financial development and economic growth in developing countries. Our findings confirm some previous research but contradict others, indicating that the relationship between economic growth and financial development may not be universal and may depend on various contextual factors. Although economic growth can have a positive impact on financial development, policymakers in developing countries should consider the specific context of their country when formulating policies to promote economic growth as a means of stimulating financial development.

6. Conclusions and policy implications

Based on the results of our study, one may conclude that financial development does not matter for economic growth. However, it may be more reasonable to conclude that financial development will not guarantee economic growth without building better institutions and following sound and stable fiscal policies (R. Levine, Citation1997). The implications of these findings for government policymakers in Ethiopia revolve around the necessity of constructing an effective economic growth strategy that maintains financial development. Besides, contrary to the primary drivers of financial development in developed countries, which are often technological innovation and market competition, the situation in developing countries like Ethiopia requires a different approach. Researchers suggest that policymakers in Ethiopia should initiate specific projects that have a direct impact on and facilitate the advancement of the economy, thus expediting the progress of financial development (Song et al., Citation2021).

Therefore, the study’s results emphasize the need for policymakers in Ethiopia to prioritize policies aimed at promoting economic growth. By prioritizing economic growth, policymakers can stimulate financial development, indicating the importance of creating an environment that fosters economic growth as a means of promoting financial development.

7. Limitations and future research directions

Although this study is the first study to use asymmetric cointegration to examine the nexus between broad-based financial development and economic growth in Ethiopia, it has some limitations that need to be considered. First, the study focuses solely on investigating the causal link between economic growth and financial development in Ethiopia, which makes it difficult to generalize the results to other developing countries. As such, future studies should extend the analysis to other developing countries to provide insights into whether the findings in Ethiopia are generalizable to other countries and to highlight any differences or similarities in the relationship between economic growth and financial development across diverse contexts. Second, the study has a small sample size of around 40 data points in total, which may not be adequate for conducting rigorous time series econometric analyses. In addition, the short period data used in the study may not allow for a thorough investigation of the potential long lags in financial development that may have a significant impact on PCI growth. While the small sample size is an understandable limitation given the specific context of the research, future researchers in similar situations may consider using cross-country time series panel datasets or large cross-sectional datasets to enhance the reliability and robustness of their findings.

Third, the association between economic growth and financial development is intricate and influenced by a range of factors (Nyasha & Odhiambo, Citation2018). However, the study does not consider additional drivers of PCI growth such as innovation intensity, product and labor market regulations, and institutions due to the unavailability of reliable data in Ethiopia. Future research on this topic could consider examining these and related issues thoroughly to gain a deeper understanding of the relationship between economic growth and financial development in developing countries and to enhance the reliability and robustness of the findings. Future research should also focus on investigating the specific channels through which economic growth affects financial development in Ethiopia, to provide a more comprehensive understanding of the relationship between the two variables and identify areas for further policy intervention.

Ethical Considerations

The ethical responsibility for the data lies with the institutions that conducted the surveys in Ethiopia, and we did not need ethics approval for our study.

Correction

This article has been corrected with minor changes. These changes do not impact the academic content of the article.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Data availability statement

The data sets used in this study can be found in the World Bank open database (data.worldbank.org), the IMF’s financial development index database (data.imf.org), the FRED economic data (fred.stlouisfed.org), the Bruegel dataset (www.bruegel.org), and the Penn World Table (Feenstra et al., Citation2015).

Additional information

Funding

References

- Abbas, Z., Afshan, G., & Mustifa, G. (2022). The effect of financial development on economic growth and income distribution: An empirical evidence from lower-middle and upper-middle-income countries. Development Studies Research, 9(1), 117–26. https://doi.org/10.1080/21665095.2022.2065325

- Acemoglu, D. (2012). Introduction to economic growth. Journal of Economic Theory, 147(2), 545–550. https://doi.org/10.1016/j.jet.2012.01.023

- Adeyeye, P. O., Fapetu, O., Aluko, O. A., & Migiro, S. O. (2015). Does Supply-leading Hypothesis Hold in a Developing Economy? A Nigerian Focus. Procedia Economics and Finance, 30, 30–37. https://doi.org/10.1016/S2212-5671(15)01252-6

- Akinci, G. Y., Akinci, M., & Yilmaz, Ö. (2014). Financial development-economic growth nexus: A panel data analysis upon oecd countries. Hitotsubashi Journal of Economics, 55(1), 33–50. http://www.jstor.org/stable/43296269

- Almassri, H., Ozdeser, H., & Saliminezhad, A. (2020). Does financial development promote growth in Kuwait? time- and frequency- domain causality testing. The Journal of International Trade & Economic Development, 29(8), 952–972. https://doi.org/10.1080/09638199.2020.1769711

- Aye, G. C., Edoja, P. E., & Charfeddine, L. (2017). Effect of economic growth on CO2 emission in developing countries: Evidence from a dynamic panel threshold model. Cogent Economics & Finance, 5(1), 1379239. https://doi.org/10.1080/23322039.2017.1379239

- Bagehot, W. (1873). Lombard Street: A Description of the Money Market. Henry S. King.

- Banerjee, A., Dolado, J., & Mestre, R. (1998). Error-correction mechanism tests for cointegration in a single-equation framework. Journal of Time Series Analysis, 19(3), 267–283. https://doi.org/10.1111/1467-9892.00091

- Beck, T., Fuchs, M., Singer, D., & Witte, M. (2014). Making cross-border banking work for Africa. Deutsche Gesellschaft für Internationale Zusammenarbeit.

- Bencivenga, V. R., & Smith, B. D. (1991). Financial Intermediation and Endogenous Growth. The Review of Economic Studies, 58(2), 195–209. https://doi.org/10.2307/2297964

- Beylik, U., Cirakli, U., Cetin, M., Ecevit, E., & Senol, O. (2022). The relationship between health expenditure indicators and economic growth in OECD countries: A Driscoll-Kraay approach. Frontiers in Public Health, 10. Article 1050550. https://doi.org/10.3389/fpubh.2022.1050550

- Bhole, L. (2004). Financial institutions and markets: Structure, growth and innovations, 4e. Tata McGraw-Hill Education.

- Bist, J. P., & Read, R. (2018). Financial development and economic growth: Evidence from a panel of 16 African and non-African low-income countries. Cogent Economics & Finance, 6(1), 1449780. https://doi.org/10.1080/23322039.2018.1449780

- Brooks, C. (2019). Introductory econometrics for finance. Cambridge university press.

- Cetin, M., Ecevit, E., & Yucel, A. G. (2018). The impact of economic growth, energy consumption, trade openness, and financial development on carbon emissions: Empirical evidence from Turkey. Environmental Science and Pollution Research, 25(36), 36589–36603. https://doi.org/10.1007/s11356-018-3526-5

- Chen, H., Hongo, D. O., Ssali, M. W., Nyaranga, M. S., & Nderitu, C. W. (2020). The Asymmetric Influence of Financial Development on Economic Growth in Kenya: Evidence from NARDL. SAGE Open, 10(1), 215824401989407. https://doi.org/10.1177/2158244019894071

- Cho, J. S., Greenwood‐Nimmo, M., & Shin, Y. (2021). Recent developments of the autoregressive distributed lag modelling framework. Journal of Economic Surveys, 37(1), 7–32. https://doi.org/10.1111/joes.12450

- Collier, P. (1999). On the economic consequences of civil war. Oxford Economic Papers, 51(1), 168–183. https://doi.org/10.1093/oep/51.1.168

- Dani, R. (2009). The Real Exchange Rate and Economic Growth. Brookings Papers on Economic Activity, 2008(2), 365–412. https://doi.org/10.1353/eca.0.0020

- Darvas, Z. (2012). Real effective exchange rates for 178 countries: A new database. https://www.bruegel.org/publications/datasets/

- Dickey, D. A., & Fuller, W. A. (1981). Likelihood ratio statistics for autoregressive time series with a unit root. Econometrica: Journal of the Econometric Society, 49(4), 1057–1072. https://doi.org/10.2307/1912517

- Djeunankan, R., Njangang, H., Tadadjeu, S., & Kamguia, B. (2023). Remittances and energy poverty: Fresh evidence from developing countries. Utilities Policy, 81, 101516. https://doi.org/10.1016/j.jup.2023.101516

- Durusu-Ciftci, D., Ispir, M. S., & Yetkiner, H. (2017). Financial development and economic growth: Some theory and more evidence. Journal of Policy Modeling, 39(2), 290–306. https://doi.org/10.1016/j.jpolmod.2016.08.001

- Elliott, G., Rothenberg, T. J., & Stock, J. H. (1992). Efficient tests for an autoregressive unit root. In: National Bureau of Economic Research Cambridge.

- Engle, R. F., & Granger, C. W. J. (1987). Co-Integration and Error Correction: Representation, Estimation, and Testing. Econometrica, 55(2), 251–276. https://doi.org/10.2307/1913236

- Faisal, F., Sulaiman, Y., & Tursoy, T. (2019). Does an asymmetric nexus exist between financial deepening and natural resources for emerging economy? Evidence from multiple break cointegration test. Resources Policy, 64, 101512. https://doi.org/10.1016/j.resourpol.2019.101512

- Feenstra, R. C., Inklaar, R., & Timmer, M. P. (2015). The Next Generation of the Penn World Table. American Economic Review, 105(10), 3150–3182. https://doi.org/10.1257/aer.20130954

- Giordano, C. (2023). Revisiting the real exchange rate misalignment‐economic growth nexus via the across‐sector misallocation channel. Review of International Economics. https://doi.org/10.1111/roie.12669

- Gurgul, H., & Łukasz, L. (2011). Financial development and economic growth in Poland in transition: Causality analysis.

- Gurley, J. G., & Shaw, E. S. (1955). Financial Aspects of Economic Development. The American Economic Review, 45(4), 515–538. http://www.jstor.org/stable/1811632

- Guru, B. K., & Yadav, I. S. (2019). Financial development and economic growth: Panel evidence from BRICS. Journal of Economics, Finance and Administrative Science, 24(47), 113–126. https://doi.org/10.1108/jefas-12-2017-0125

- Hamilton, J. D. (1989). A new approach to the economic analysis of nonstationary time series and the business cycle. Econometrica: Journal of the Econometric Society, 57(2), 357–384. https://doi.org/10.2307/1912559

- Haque, M. I., Faruk, B. U., & Tausif, M. R. (2022). Growth-finance nexus in oil abundant GCC countries of MENA region. Cogent Economics & Finance, 10(1). https://doi.org/10.1080/23322039.2022.2087646

- Honohan, P., & Beck, T. (2007). Making finance work for Africa. World Bank Publications. https://doi.org/10.1596/978-0-8213-6909-8

- Islam, M. S., Alsaif, S. S., & Alsaif, T. (2022). Trade Openness, Government Consumption, and Economic Growth Nexus in Saudi Arabia: ARDL Cointegration Approach. SAGE Open, 12(2), 21582440221096661. https://doi.org/10.1177/21582440221096661

- Jalil, A., & Rauf, A. (2021). Revisiting the link between trade openness and economic growth using panel methods. The Journal of International Trade & Economic Development, 30(8), 1168–1187. https://doi.org/10.1080/09638199.2021.1938638

- Jung, W. S. (1986). Financial Development and Economic Growth: International Evidence. Economic Development and Cultural Change, 34(2), 333–346. https://doi.org/10.1086/451531

- Kassi, D. F., Li, Y., Gnangoin, Y. T., N’Drin, M. G.-R., Gnahe, F. E., & Edjoukou, A. J. R. (2023). Investigating the Finance-Energy-Growth Trilogy in Sub-Saharan Africa: Evidence from the NARDL Framework. SAGE Open, 13(1), 21582440221149714. https://doi.org/10.1177/21582440221149714

- Khan, M. S., & Senhadji, A. S. (2003). Financial development and economic growth: A review and new evidence. Journal of African Economies, 12(suppl_2), ii89–ii110. https://doi.org/10.1093/jae/12.suppl_2.ii89

- King, R. G., & Levine, R. (1993). Finance and Growth: Schumpeter Might Be Right*. The Quarterly Journal of Economics, 108(3), 717–737. https://doi.org/10.2307/2118406

- Lata, L. (2003). The Ethiopia-Eritrea War. Review of African Political Economy, 30(97), 369–388. http://www.jstor.org/stable/4006982

- Levine, M. R. (2021). Finance, growth, and inequality. International Monetary Fund.

- Levine, R. (1997). Financial development and economic growth: Views and agenda. Journal of Economic Literature, 35(2), 688–726.

- Luintel, K. B., & Khan, M. (1999). A quantitative reassessment of the finance–growth nexus: Evidence from a multivariate VAR. Journal of Development Economics, 60(2), 381–405. https://doi.org/10.1016/S0304-3878(99)00045-0

- Manta, A. G., Florea, N. M., Bădîrcea, R. M., Popescu, J., Cîrciumaru, D., & Doran, M. D. (2020). The Nexus between Carbon Emissions, Energy Use, Economic Growth and Financial Development: Evidence from Central and Eastern European Countries. Sustainability, 12(18), 7747. https://doi.org/10.3390/su12187747

- Menyah, K., Nazlioglu, S., & Wolde Rufael, Y. (2014). Financial development, trade openness and economic growth in African countries: New insights from a panel causality approach. Economic Modelling, 37, 386–394. https://doi.org/10.1016/j.econmod.2013.11.044

- Moyo, C., Khobai, H., Kolisi, N., & Mbeki, Z. (2018). Financial development and economic growth in Brazil: A Non-linear ARDL approach.

- Mtar, K., & Belazreg, W. (2023). On the nexus of innovation, trade openness, financial development and economic growth in European countries: New perspective from a GMM panel VAR approach. International Journal of Finance & Economics, 28(1), 766–791. https://doi.org/10.1002/ijfe.2449

- NBE. (2022). National Bank of Ethiopia 2021-22 Annual Report. https://nbe.gov.et/annual-report/

- Nguyen, T. A. N. (2022). Financial Development, Human Resources, and Economic Growth in Transition Countries. Economies, 10(6), 138. https://doi.org/10.3390/economies10060138

- Nguyen, P. T., & Pham, T. T. T. (2021). The impact of financial development on economic growth: Empirical evidence from transitional economies. The Journal of Asian Finance, Economics & Business, 8(11), 191–201. https://doi.org/10.13106/jafeb.2021.vol8.no11.0191

- Nguyen, H. M., Thai-Thuong Le, Q., Ho, C. M., Nguyen, T. C., & Vo, D. H. (2022). Does financial development matter for economic growth in the emerging markets? Borsa Istanbul Review, 22(4), 688–698. https://doi.org/10.1016/j.bir.2021.10.004

- Nyasha, S., Gwenhure, Y., & Odhiambo, N. M. (2016). Financial development and economic growth in Ethiopia: A dynamic causal linkage. https://ideas.repec.org/p/uza/wpaper/20160.html

- Nyasha, S., & Odhiambo, N. M. (2018). Financial Development and Economic Growth Nexus: A Revisionist Approach. Economic Notes, 47(1), 223–229. https://doi.org/10.1111/ecno.12101

- Odhiambo, N. M., & Nyasha, S. (2022). Financial Development and Economic Growth in Uganda: A Multivariate Causal Linkage. Journal of African Business, 23(2), 361–379. https://doi.org/10.1080/15228916.2020.1838834

- Okuyan, H. A. (2022). The Nexus of Financial Development and Economic Growth Across Developing Economies. South East European Journal of Economics and Business, 17(1), 125–140. https://doi.org/10.2478/jeb-2022-0009

- Omoke, P. C. (2009). The causal relationship among financial development, trade openness and economic growth in Nigeria. Trade Openness and Economic Growth in Nigeria. December 30, 2009. https://doi.org/10.2139/ssrn.1529644

- Omri, A., Daly, S., Rault, C., & Chaibi, A. (2015). Financial Development, Environmental Quality, Trade and Economic Growth: What Causes What in MENA Countries? SSRN Electronic Journal. https://doi.org/10.2139/ssrn.2575048

- Opoku, E. E. O., Ibrahim, M., & Sare, Y. A. (2019). The causal relationship between financial development and economic growth in Africa. International Review of Applied Economics, 33(6), 789–812. https://doi.org/10.1080/02692171.2019.1607264

- Papalia, R. B., Bertarelli, S., & Filippucci, C. (2011). Human capital, technological spillovers and development across OECD countries.

- Park, J. Y. (1992). Canonical Cointegrating Regressions. Econometrica, 60(1), 119–143. https://doi.org/10.2307/2951679

- Pesaran, M. H., Shin, Y., & Smith, R. J. (2001). Bounds testing approaches to the analysis of level relationships. Journal of Applied Econometrics, 16(3), 289–326. https://doi.org/10.1002/jae.616

- Peter, C. B. P., & Perron, P. (1988). Testing for a Unit Root in Time Series Regression. Biometrika, 75(2), 335–346. https://doi.org/10.1093/biomet/75.2.335

- Phillips, P. C. B., & Hansen, B. E. (1990). Statistical Inference in Instrumental Variables Regression with I(1) Processes. The Review of Economic Studies, 57(1), 99–125. https://doi.org/10.2307/2297545

- Pradhan, R. P., Arvin, M., Nair, M., Bennett, S., & Bahmani, S. (2017). ICT-finance-growth nexus: Empirical evidence from the Next-11 countries. Cuadernos de Economía, 40(113), 115–134. https://doi.org/10.1016/j.cesjef.2016.02.003

- Raifu, I. A., & Afolabi, J. A. (2022). The Effect of Financial Development on Unemployment in Emerging Market Countries. Global Journal of Emerging Market Economies, 09749101221116715. https://doi.org/10.1177/09749101221116715

- Rajan, R., & Zingales, L. (1998). Financial development and growth. American Economic Review, 88(3), 559–586.

- Romer, P. M. (1990). Endogenous technological change. Journal of Political Economy, 98(5, Part 2), S71–S102. https://doi.org/10.1086/261725

- Samargandi, N., Fidrmuc, J., & Ghosh, S. (2015). Is the Relationship Between Financial Development and Economic Growth Monotonic? Evidence from a Sample of Middle-Income Countries. World Development, 68, 66–81. https://doi.org/10.1016/j.worlddev.2014.11.010

- Saqib, N. (2022). Green energy, non-renewable energy, financial development and economic growth with carbon footprint: Heterogeneous panel evidence from cross-country. Economic Research-Ekonomska Istraživanja, 35(1), 6945–6964. https://doi.org/10.1080/1331677X.2022.2054454

- Schumpeter, J. A. (1912). 1934. The theory of economic development.

- Shahbaz, M., Naeem, M., Ahad, M., & Tahir, I. (2018). Is natural resource abundance a stimulus for financial development in the USA? Resources Policy, 55, 223–232. https://doi.org/10.1016/j.resourpol.2017.12.006

- Shin, Y., Yu, B., & Greenwood-Nimmo, M. (2014). Modelling Asymmetric Cointegration and Dynamic Multipliers in a Nonlinear ARDL Framework. In R. C. Sickles & W. C. Horrace (Eds.), Festschrift in Honor of Peter Schmidt: Econometric Methods and Applications (pp. 281–314). Springer New York. https://doi.org/10.1007/978-1-4899-8008-3_9

- Song, C.-Q., Chang, C.-P., & Gong, Q. (2021). Economic growth, corruption, and financial development: Global evidence. Economic Modelling, 94, 822–830. https://doi.org/10.1016/j.econmod.2020.02.022

- Stock, J. H., & Watson, M. W. (1993). A Simple Estimator of Cointegrating Vectors in Higher Order Integrated Systems. Econometrica, 61(4), 783–820. https://doi.org/10.2307/2951763

- Svirydzenka, K. (2016). Introducing a new broad-based index of financial development. International Monetary Fund.

- Swamy, V., & Dharani, M. (2019). The dynamics of finance-growth nexus in advanced economies. International Review of Economics & Finance, 64, 122–146. https://doi.org/10.1016/j.iref.2019.06.001

- Taddese Bekele, D., & Abebaw Degu, A. (2021). The effect of financial sector development on economic growth of selected sub-Saharan Africa countries. International Journal of Finance & Economics, 28(3), 2834–2842. https://doi.org/10.1002/ijfe.2566

- Taivan, A., & Nene, G. (2016). Financial development and economic growth: Evidence from southern African development community countries. The Journal of Developing Areas, 50(4), 81–95. https://doi.org/10.1353/jda.2016.0154

- Teklu, T., & Jemal, A. (2019). The causality between Financial Development and Economic Growth in Ethiopia: Supply Leading vs Demand Following Hypothesis. Journal of Economics and Financial Analysis, 87–115. https://doi.org/10.1991/jefa.v3i1.a25

- Tinta, A. A. (2022). Financial development, ecological transition, and economic growth in Sub-Saharan African countries: The performing role of the quality of institutions and human capital. Environmental Science and Pollution Research, 29(25), 37617–37632. https://doi.org/10.1007/s11356-021-18104-y

- Toda, H. Y., & Yamamoto, T. (1995). Statistical inference in vector autoregressions with possibly integrated processes. Journal of Econometrics, 66(1), 225–250. https://doi.org/10.1016/0304-4076(94)01616-8

- Uche, E., & Effiom, L. (2021). Financial development and environmental sustainability in Nigeria: Fresh insights from multiple threshold nonlinear ARDL model. Environmental Science and Pollution Research, 28(29), 39524–39539. https://doi.org/10.1007/s11356-021-12843-8

- Udeagha, M. C., & Breitenbach, M. C. (2023). On the asymmetric effects of trade openness on CO2 emissions in SADC with a nonlinear ARDL approach. Discover Sustainability, 4(1). https://doi.org/10.1007/s43621-022-00117-3

- Vo, D. H., Tran, Q., Tran, T., & Vasa, L. (2022). Economic growth, renewable energy and financial development in the CPTPP countries. PLOS ONE, 17(6), e0268631. https://doi.org/10.1371/journal.pone.0268631

- Watson, M. W. (1994). Chapter 47 Vector autoregressions and cointegration. In Handbook of Econometrics (Vol. 4, pp. 2843–2915). Elsevier. https://doi.org/10.1016/S1573-4412(05)80016-9

- Wen, J., Mahmood, H., Khalid, S., & Zakaria, M. (2021). The impact of financial development on economic indicators: A dynamic panel data analysis. Economic Research-Ekonomska Istraživanja, 35(1), 1–13. https://doi.org/10.1080/1331677X.2021.1985570

- Wolde Rufael, Y. (2009). Re-examining the financial development and economic growth nexus in Kenya. Economic Modelling, 26(6), 1140–1146. https://doi.org/10.1016/j.econmod.2009.05.002

- Worku, U. R. (2016). The Contribution of Financial Sector Development for Economic Growth in East Africa. Applied Economics and Finance, 3(2). https://doi.org/10.11114/aef.v3i2.1251

- Zhuang, J., Gunatilake, H. M., Niimi, Y., Khan, M. E., Jiang, Y., Hasan, R., Khor, N., Martin, A. L., Bracey, P., & Huang, B. (2009). Financial Sector Development, Economic Growth, and Poverty Reduction: A Literature Review. SSRN Electronic Journal. https://doi.org/10.2139/ssrn.1617022

Appendix

Table A1. The expanded versions of the acronyms used in the paper