?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

This study aims to determine the impact of tax administration and corruption on firm self-financing in Africa. The paper also explores the level at which tax administration and corruption are firm financing obstacles and whether these effects on firms differ regarding their size. The article uses data from the World Bank Enterprise Survey, which covers 45,048 firms in 48 countries across Africa. Using the Tobit, IV Tobit, and Multinomial Probit models, the results are robust as we controlled for country, firm diversity, and survey year. The study reveals that corruption reduces a firm’s self-financing by negatively affecting its internal funds or retained earnings. In addition, weak tax administration reduces firm self-financing. The results also reveal that corruption and poor tax administration are severe obstacles to a firm’s self-financed. Furthermore, while weak tax administration generally harms firm financing, the negative impact on larger firms surpasses the adverse effects on smaller and medium firms. The corruption issue is more critical in the case of small and medium firms than big firms as they spend a large portion of their profit to government officials as gifts or informal payments to reduce the burden of regulations and circumvent taxes.

1. Introduction

Globally, firms are a major contributor to the economy in advanced, emerging, and developing economies (OECD, P. 2017). In Africa, SMEs contribute more than half of the GDP and employment (Africapractice, Citation2019). Well-functioning small and medium-sized enterprises (SMEs) are a significant part of the economic framework in developing countries. They contribute to GDP growth, reduce unemployment, and encourage innovation and growth. Governments, therefore, concentrate on improving the SME sector to stimulate economic development. These SMEs operate mainly in services, especially trade, and in manufacturing and agro-industries, thus reflecting the structure of these countries GDP. Although productive SMEs are in the minority ahead of those in the tertiary sector, they play a dominant role in these countries’ industrial sectors. For example, from Kauffmann (Citation2005), SMEs represent around 96% of manufacturing activity and 70% of industrial employment in Nigeria, the leading country in sub-Saharan Africa.

Despite their weight in local economies and their driving role in economic development, SMEs have limited access to financing, particularly in Africa. On the one hand, the bank penetration rate in Africa is meager, total bank assets amount to only 32% of GDP on average, and loans to the private sector constitute less than half of these assets (Kauffmann, Citation2005). On the other hand, it is mainly large companies, often foreign ones, which benefit from most financing, according to several studies (Aryeetey & Aryeetey, Citation1998). The problems of corruption, poor infrastructure, or abusive taxation aggravated these financing problems. Deprived of access to the financing market, SMEs often cover all their needs with personal resources (Africapractice, Citation2005).

African small and medium-sized enterprises have limited access to capital, hampering their development and emergence. Their primary capital sources are their earnings and informal investments, self-financing, and credit partnership such as tontines, which, due to their geographic or sectorial orientation, are volatile, not very stable, and lack risk-sharing.

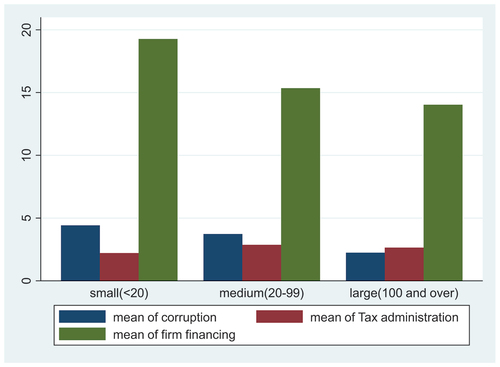

Figure indicates in the green color bar that, on average, 19% of small firms, 15% of medium-sized firms, and 14% of large firms have declared access to finance to be an obstacle. Figure confirms that SMEs are severely constrained in self-financing compared to large firms. Large-size firms do not have as many obstacles as depicted.

Figure 1. Percent of firms identifying access to finance, corruption, and financing as a constraint.

Firms that receive higher government help are more likely to get bank loans (Ruan et al., Citation2018). Therefore, enterprises strive to find efficient methods to get funds from financial institutions and mitigate financing constraints, such as getting government guarantees and corrupting officials. Because of certain government guarantees, even if firms with state ownership have lower control and achievement, they have higher political status. They are usually viewed as more protected than non-SOEs. State ownership can guarantee firms’ debt; hence, firms with state ownership have a lower possibility of bankruptcy than non-SOEs (Borisova et al., Citation2015). Government quality is necessary for reputation assets and financing support for firms. Banking institutions’ operations are ordinarily based on state policy in emerging countries. Therefore, firms with good government relations can share governments’ network resources to receive more bank assistance, such as low-cost loans. The government dramatically influences banks’ lending choices in government-led economies and extends a helping hand to relieve financial institutions’ matters concerning corporate moral hazards (Faccio et al., Citation2006). Government interference in capital allocation modifies the financial market’s allocative function and exacerbates the private sector’s financial climate (Guariglia & Poncet, Citation2008).

Besides government intervention as a helper, tax administration and corruption could be a constraint for firm performance that significantly impact firm self-financing. According to Auriol and Warlters (Citation2005), the ease with which collecting taxes from a relatively small number of large companies may lead the tax administration to concentrate more on SMEs by making their activity more difficult. High tax rates and administration complexity are significant constraints for SMEs and can steer them into the informal sector if the tax burden becomes excessive. However, a large informal economy can reduce government revenues and increase the tax burden on formal sector businesses, which increases the attraction of informal activities (OECD, Citation2008).

Besides that, ineffective tax administration raises compliance costs, which considerably raises companies’ fiscal burden (Dabla-Norris et al., Citation2017), and can harm their performance. Due to the significant compliance expenses caused by poor tax administration, some firms may decide to operate informally (Moore, Citation2023). Informality makes it difficult for enterprises to access financing, international exposure, assistance, and training programs. That limits their ability to increase performance (Capasso et al., Citation2022).

From the standpoint of generating public revenue, if tax administration is detrimental to enterprises’ activities, it is likewise detrimental to generating public revenue in three different ways. Firstly, a firm’s capacity to pay tax is based on its development, and if tax administration affects profit and development, government income will decline. Secondly, consumption tax (for example, VAT) will be reduced since firm performance has decreased due to bad tax administration. Lastly, employees’ income taxes will be lessened because of decreased wages/salaries from reduced firm output and earnings. Hence, understanding how tax administration affects firm performance will provide the basis for reforming the tax policy to minimize administrative costs.

The above Figure also shows in the maroon color that tax administration as a constraint impacts more firms depending on their size in Africa. The bigger the firm, the more it impacts the tax administration. About 3% of large-size firms are impacted compared to 3% and 2% for medium and small-size firms, respectively.

Corruption is an omnipresent and tenacious obstacle to various emerging economies (Martins et al., Citation2020). It is affirmed by the companies that corruption is one of the biggest barriers to business growth and performance (Gaviria, Citation2002). The rent-seeking concept of public policy notes that corruption is not helpful for development (Krueger, Citation1974). Because of information asymmetry in the credit rationing process, financial institutions usually have credit decision-making powers, like loan interest rates, loan length, and collateral forms (Barth et al., Citation2009). As a result, the rights of bank officers could cause companies to bribe them. Bribery gives corrupt administrators a higher impulse to formulate further complex loan terms, which drives firms to raise their gifts to evade these new terms (Guriev, Citation2004).

Furthermore, a significant level of corruption leads to opportunistic behaviors in ineffective systems. It raises the non-performing loans created by bank institutions due to loan defaults. Corruption practices bring up the uncertainty of banks’ avoidance of default and raise the risk of borrowers’ default. That reduces banks’ readiness to lend to firms and increases the obstacles to firm financing (Qi & Ongena, Citation2019; Wellalage & Fernandez, Citation2019). Firms and individuals with low incomes are more likely to join corrupt activities (Haque & Sahay, Citation1996). Unfair income distribution in countries (Swamy et al., Citation2001) and changes in regulations such as tax systems, tariffs, and state policies (Gupta et al., Citation2005) are additional determinants influencing corruption. This problem is more critical in small firms as they spend a considerable portion of their income on the government as a gift or informal payment.

For this reason, big businesses are habitually more protected in emerging countries. Further, they are constrained to heavier controls and taxation such as labor rules, company implantation, tax office, and tax rates. Corruption encourages firms to gather resources (Tollison, Citation2012), but it reduces the financial intermediaries’ performance and entrepreneurship (Djankov et al., Citation2007). Therefore, corruption due to government interference constrains financial development.

Besides, corruption can be a springboard to access to finance. Financial institutions give funds in a challenging and restraining system, which guides the exclusion of firms that do not satisfy financial institutions’ requirements to issue loans. Accordingly, keeping a great connection with banks has become tricky for enterprises to get bank loans. Gift exchange creates significant social capital, allowing firms to keep relationships with administrators (Cai et al., Citation2011). The lubricant hypothesis implies that bribery reduces the system’s rigidity, which can cause corrupt actions advantageous to economic development (Dreher & Gassebner, Citation2013). Bribery can relax the rigid credit system, simplify cumbersome loan procedures, decrease loan approval waiting time, and improve investment efficiency (Levin & Satarov, Citation2000). The bribery of administrators by enterprises decreases the unfavorable influences of red tape and encourages them to get bank loans, although this results in a rise in the short-term bank debt ratio (Chen et al., Citation2013; Fungáčová et al., Citation2015). Hence, corruption actions improve the connection among banks and firms and are powerful strategic behaviors for enterprises to get bank credits. From the above figure, the navy color bar shows that 4% of small and 4% of medium-sized firms are experiencing corruption. The figure also indicates that, on average, large firms have to pay 2% as a bribe payment for a contract.

This paper will enrich the current literature in several ways. We exclusively focus on the African World Bank Enterprise Survey database. The database gives new insights to apprehend the financing behavior of the firm in Africa. It will help to find creative and innovative ways to achieve strong firm growth that is crucial in alleviating poverty. We diverge from many current studies by designing objective and subjective indicators for firm access to finance and corruption that explain how tax administration and corruption affect corporate self-financing and what drives firms to finance obstacles. Although there is a significant number of previous studies on corruption or poor tax administration, limited studies have been conducted on the effect of poor tax administration and corruption on firm financing, mainly on firm self-financing. To the best of our knowledge, our study is among the first ones to empirically examine the impact of tax administration and corruption on firm self-finance, mainly in Africa. This paper is different from other research on corruption or tax administration in that it studies the combined effect of both corruption and tax administration on firm self-financing using both Tobit and multinomial probit model models.

The main finding is that corruption reduces a firm’s self-financing by negatively affecting its internal funds or retained earnings. In addition, we find that weak tax administration reduces firm self-financing too. Furthermore, we investigate the level at which corruption and tax administration are obstacles to firm financing by employing the Multinomial Probit model. We categorized financing obstacles as minor, moderate, major, and severe. We find that corruption and poor tax administration best predict firm self-finance obstacles. The results reveal that tax administration and corruption increase firm self-finance obstacles (minor, moderate, major, and severe). The findings are also robust after using alternative corruption and tax administration measures. We also find that while weak tax administration harms firm financing in general, the negative impact on larger firms surpasses that on smaller and medium firms. Corruption issue is more critical in the case of small and medium firms than big firms are as they spend a large portion of their profit to the government official as a gift or informal payments to reduce the burden of regulations and circumvent taxes. The results are robust after controlling for firm characteristics, endogeneity issues, year of survey, and country specifications.

The continuation of this study is organized as follows. Section 2 examines how the paper compares to the literature. Section 3 sets out the data, hypothesis, and econometric model. Section 4 explains the findings and checks for the robustness of the findings, Section 5 does the extended analysis, and Section 6 concludes.

2. Empirical literature review

For many decades, the debate on the impact of corruption and taxation on firm growth and financing constraints has been heavily contested. The impact of corruption is also perceived to be more like a tax, primarily because the payment will not end up as government revenue (Johnson et al., Citation1998). Corruption can be more counterproductive to firm performance than taxes, depriving the government of the revenues needed to provide efficient public goods. More recently, Murphy et al. (Citation1993) claimed that bribes might be much more harmful than taxes due to various higher transaction costs, given the complexity and privacy that inevitably follow bribery payments and the fact that fraudulent contracts are not lawful.

Firms that do not satisfy the requirements for financial institutions to grant loans are excluded because financial institutions operate under strict and binding regulation that restricts their ability to give funding. Thus, keeping a positive connection with banks has become a strategic decision for businesses seeking bank loans. Giving and receiving gifts create significant social capital that helps businesses keep their relationships with government officials (Cai et al., Citation2011). According to the lubricant theory, corruption might be advantageous for economic growth since it reduces the rigor of the system (Dreher & Gassebner, Citation2013). In particular, corruption can ease the strict loan process, simplify complicated loan processes, shorten the delay for loan approval, and boost investment effectiveness (Loayza et al., Citation2000). Bribery and other corrupt practices are, in our opinion, the second most successful way to increase a company’s bank loan approval speed.

According to the rent-seeking approach of public choice theory, corruption harms growth (Krueger, Citation1974). Bank executives typically have decision-making authority over credit conditions, including interest rates on loans, loan maturities, and the forms of collateral, due to the knowledge asymmetry in the credit rationing mechanism (Barth et al., Citation2009). As a result, firms could bribe bank personnel because of their privileges. Bribery encourages dishonest authorities to create more complex loan terms, prompting businesses to pay additional bribes to circumvent the new conditions (Guriev, Citation2004). Additionally, a high level of corruption encourages opportunistic behavior in poor systems, raising the amount of non-performing loans that banking institutions create due to credit default.

Consequently, the question of whether bribery is more detrimental than taxes or harmful is mainly an empirical question. The macro literature has intensively investigated the connection between firm growth and bribery, starting with Mauro (Citation1995). These papers have found a negative link between bribery and growth. Nevertheless, this research body is wholly focused on cross-country analyses, which often pose significant worries about non-observed heterogeneity through datasets. Also, bribery information is based on perception corruption indices, usually expert perceptions of aggregate corruption in a region, which pose queries about perception biases. Finally, a cross-country analysis of the relationship between bribery and development shows us nothing about the impact of corruption on individual firms.

In the empirical review using a firm-level dataset, several authors have argued about the effect of corruption on firms’ access to external financing, including banks and credit institutions. Liu et al. (Citation2020) used Chinese enterprises’ business environment survey by the World Bank and saw an inverted U-shaped association linking corrupt acts and firms’ access to bank credit. They found that a low degree of corruption can encourage firms to have bank funds, but a high level of corruption makes it impossible for companies to secure bank loans. Besides, corruption affects firms’ access to external financing by enabling them to obtain government guarantees, which are positively associated with firm financing. In the same vein, Li et al. (Citation2008), using a nationwide survey of private enterprises in China, find that party membership of private entrepreneurs not only enhances their firm’s performance but also helps them obtain loans from banks.

Oppositely, Qi et al. (Citation2018) used a sample of European firms from transition countries from 2008–09 and 2012–14. Their findings reveal that access to bank loans is difficult when a firm is involved too much in corruption practices and that corruption generates this loss of access. The bribery-driven increase in financing obstacles significantly impedes future firm growth. Following the findings, Wellalage and Fernandez (Citation2019) used data on 130,000 firms in 135 countries. He finds that high corruption increases difficulties for financial institutions to control borrower risk and recover loans from a supply side. Unlike large firms, SMEs give bribes to grease the wheel to the informal sector to avoid the attention of tax administration agents. The demand-side considers bribes like tax, increasing credit costs to SMEs. The degree to which private companies obtain bank credit in China is determined by bribery rather than company performance. Bribery encourages financial results by awarding more extensive credits to companies with more significant economic results, and they pay more for bribery (Chen et al., Citation2013).

Many researchers have linked tax administration and firm productivity, and some related tax administration and government intervention in firm financing. However, there is no direct review linking tax administration and firm financing to the extent of our knowledge.

In government-led economies, the government considerably influences bank lending choices, extending a helping hand to assuage financial institutions’ worries about firm moral hazards. A comprehensive follow-up research has linked the relationship between tax administration and firm external finance. Fu (Citation2020), using Investment Climate Survey on China’s firms, shows the dilemma of government intervention in a firm’s financing. He argues that government intervention supports a firm’s financial access but impedes the firm’s micro-financial development. So far, Faccio et al. (Citation2006) analyzed the probability of government bailouts of 450 politically related firms in 35 countries from 1997 to 2002. Politically connected firms are significantly more likely to be bailed out than similar non-connected firms. Also, in some countries, political connections determine capital allocation through financial assistance when affiliated companies face economic distress.

Government guarantees affect enterprises’ ability to borrow from banks in two directions. Firstly, government guarantees are valuable reputation assets and funding opportunities for firms. Government policy concerns often predicate financial institutions’ behavior in developing countries. Thus, firms with government guarantees can share state network resources to gain additional help from banks, such as low-interest lending. Because of implicit government assurances, firms with state ownership have stronger political prestige and are considered safer than non-SOEs. Secondly, state ownership offers an implicit guarantee for enterprises’ debt, resulting in a decreased likelihood of bankruptcy compared to non-SOEs (Borisova et al., Citation2015). Private firms that get greater government help are more likely to get bank loans. Thus, firms aim to discover efficient ways to receive cash from banking institutions and reduce financing limitations, such as securing government guarantees and bribing authorities. Government intervention in capital allocation weakens the financial system and affects the financing climate for the private sector (Guariglia & Poncet, Citation2008).

3. Data, hypothesis, and econometric model

This section presents the data and the economic model used to study the relationship between firm self-financing, corruption, and tax administration quality.

3.1. Enterprise surveys dataset

This research uses data from the Enterprise surveys, a firm-level data set recently accessible from the World Bank and its collaborators worldwide. The survey was conducted from 2006 to 2020 and represents more than 160,000 firms in 140 countries. Enterprise Surveys concentrate on many aspects that shape the industrial climate and can accommodate or minimize business operations and play a significant role in a country’s success or failure (World Bank, Citation2020). The survey is done in the non-agricultural economy to a representative group of firms, and a key questionnaire that keeps surveys comparative between various countries and survey years.

The essential questionnaire comprising a survey answered by company owners and top managers worldwide offers subjective and objective details regarding firms’ market environment. Subjective analyses demonstrate the severity of the challenges that firms face. The survey asks businesses to rank 16 elements on a range of 1 to 5 (1 is no obstacle, and 5 is a major obstacle). This detail facilitates recognizing the highest obstacles and analyzing the obstacles that businesses deem to be the most relevant. Enterprise Surveys are very useful because they have a range of objective measures, such as how much a firm pays as bribes, total firm sales, and internal funds, or if there are often power outages. These quantitative measures become very useful as we try to overcome the possible limitations of subjective measures. Subjective indicators include the assumption that companies’ business climate impressions represent characteristic variations in the degree of optimism or pessimism of the people’s opinion of the survey. Subjective tests are often deficient when reactions are likely to be heavily affected by the firm’s experience and outcomes (Aterido et al., Citation2011).

This paper investigates the impact of corruption and tax administration quality on firm self-financing in Africa. We will use subjective and objective indicators of firm financing from the World Bank Enterprise Surveys to reach this aim.

We use a sample of 45,048 firms from 47 African nations for our study. Table of Appendix A shows the distribution of firms in the study, and the average sample size is 958 firms, although estimates vary by nation. Some nations are more highly represented than others. Egypt, Kenya, and Nigeria represent more than 5% of each firm sample, with Egypt having the highest total firms in the sample, 17.28% for 7786 firms. The lowest representation goes to Benin, Chad, Togo, Liberia, and Nigeria, representing less than 0.67% of the firm sample. After data cleaning, we remained at 6,798 observations.

3.2. Dependent variable: firm self-financing

The self-financing capacity consists of the future capital that is open to the company for self-financing after the activity. A mixture of financial and non-financial measures will be our appropriate indicator of firm self-financing. The firm’s benefit and profit can express financial measures (Santos & Brito, Citation2012). They have the bonus that they are objective and easily understandable. They have the limitation that they are not readily accessible and historical, so they just provide lagging information. They may also be vulnerable to manipulation and incompleteness. The downside to non-financial measures is that they are arbitrary (Santos & Brito, Citation2012). Due to the drawbacks of financial and non-financial measures, using a hybrid solution, including financial and non-financial measures, has become the widely accepted norm.

Thus, firm self-financing is the dependent variable. Our measure of firm self-financing is an objective indicator that emanated from the question asked in the survey to a firm to know the part of this firm’s working capital financed by Internal funds/Retained earnings. Our subjective is derived from the respondent’s answers in the survey from rating 16 firms’ environmental constraints. In fact, on a range between zero and five (zero for no obstacle, one for minor, two moderate, three major, and four very severe obstacles), respondents rate “access to finance.” Therefore, if access to financing restricts business efficiency, corruption and tax administration will have an increased impact and decrease the effect on its objective measure. The subjective measure is a categorical variable comprising financing as a minor, moderate, major, and severe obstacle.

3.3. Independent variables

The first key independent variable is the quality of tax administration. It is based on the question asked to know on a scale of 0–4 to what degree the tax administration poses an obstacle to their operations, with responses as no obstacle (0), minor obstacle (1), moderate obstacle (2), major barrier (3), and severe obstacle (4). The quality of tax administration will be a dummy variable, one if there is a major and severe obstacle and zero otherwise.

The second key explanatory variable is corruption. Corruption is defined in the survey as a percentage of the contract value on average paid as informal gifts following the survey question, “what is the percent value of the contract that will be typically paid in informal payments or gifts to secure the contract?”

3.4. Control variables

After choosing the key independent variables, controlling for general firm environments, country controls, and firm characteristics is important. Fixed effects at the firm level attenuate the impacts of industrial heterogeneity, whereas city fixed effects are employed to address the issue of unobservable factors missing from regional characteristics.

Using indicators from the Enterprise Surveys dataset, we track general business conditions. Firms should say in percentage of the time spent by their senior management in collaborating with government regulations. We obtained the variable regulation from that question. The tax rate is a dummy equal to 1 if the tax rate is an obstacle and 0 otherwise. We consider variable training, which is the formal training done by employees. Training is a dummy that equals one if there is formal training and 0 otherwise. We also include employment with the number of employees at the end of three fiscal years ago. The control is also for technology equal to one if the firm has its website for transactions and 0 otherwise. So far, we control for loss due to theft and crime, the difficulties of the firm to access land, firm international quality recognition, firm external audition, and firm legal status.

The survey gives information on the firm’s size, sector, and female manager ownership characteristics. It is an important aspect of the data that allows the exploration of why and how the dynamics of the economic world vary across various categories of businesses and affect them separately (Aterido et al., Citation2011). Integrating these firm features helps control the variations in objective circumstances encountered by firms with different characteristics. The firm’s size is represented in three categories: small, medium, and large. SMALL comprises firms with less than 20 employees, MEDIUM comprises firms with 20–99 employees, while LARGE comprises firms with over 99 employees. The firm sector is a manufacturing firm or a services firm. Firm ownership is whether the firm leader is female or not. Infrastructure represents the number of power outages experienced in a typical month. The experience here is the number of years top managers’ have experience in the firm sector. Production is the percent of total annual national sales. The summary of all variables included in the study is detailed in Table .

Table 1. Variable, definition, and measurement of variables

3.5. Summary statistics

This part presents the descriptive statistic of all the variables included in the data. Table shows that about 51% % of the firm’s internal funds have been used for self-financing. Whereas 8% of the firms reported minor internal financing constraints, 8% reported moderate constraints, 79% major constraints, and 6% severe constraints on average. One percent of the firm has signaled that some informal payments are required for treating officials. Tax administration is a major and severe obstacle to 74% of firm respondents. Eight percent of firm managers are female, 95% of the firm experience tax rate obstacle, 92% of firm managers have responded to have power outage issues, and 26% of firm losses is due to crime, theft, and vandalism. Twenty-four percent of the firm have not had access to the land problem, and 9% of the firm uses website technology for transactions on average. Five percent of firms are internationally recognized on average. Eighty-two percent on average of firms undergo internal audition. On average, 97% of firm production is national, 86% of the firm are small, and 10% are medium enterprises. The rest of the variables are also listed.

Table 2. Summary statistics

3.6. Econometric model and discussion

The following firm panel model estimates the effects of corruption and tax administration on firm self-financing.

Where Financei represents firm i self-financing status, Taxadmqi is the quality of tax administration for firm i, Corri refers to corruption level between firms and tax administration, Zi denotes a control variable. ui and wi are firm and city fixed effects, respectively, and ϵi is the error term.

As obvious from the model above, because our data come from a survey performed at a given time, our data do not have a time dimension.Footnote1 This paper will adopt cross-sectional regressions following other researchers (Dethier et al., Citation2011). The Tobit model is used for a baseline regression when the dependent is an objective variable. The multinomial probit model is used as a subjective dependent variable.

The Tobit model is a censored regression model developed to measure linear relationships among variables when either a left or a right censor is present in the outcome variable (Often recognized as censorship from below and above) (Tobin, Citation1958). In our case study, our dependent variable Internal fund/retained earnings, is a proportional variable derived from the question posed to the firms to give the proportion of their working capital used from an internal fund or retained earnings. The response is censored to 0% from below (lower limit = 0%) and a hundred percent from above (upper limit = 100%).

In the multinomial probit model, we analyze the degree to which a firm chooses between access to financing as minor, moderate, major, and severe obstacles. Thus, we have four (4) categorical variables. The choice of multinomial probit instead of multinomial logit modelFootnote2 comes from the IIA assumption. The IIA assumption says that Ceteris Paribus, the inclusion or exclusion of a categorical variable, will not affect the existing choice variable. Our categorical variables fail to meet the Hsiao and Hausman tests (see Table ) of the IIA assumption, hence the choice of multinomial probit, which does not need to meet the assumption.

3.7. Hypothesis

Tax administration and corruption may hinder a firm’s performance, affecting firm self-financing considerably. According to Auriol and Warlters (Citation2005), the speed with which a relatively limited number of large enterprises may collect taxes may force the tax administration to focus more on SMEs by making their activities more difficult. High tax rates and administrative complexity are important restrictions for SMEs, driving them into the informal sector if the tax burden gets too high. Conversely, a big informal economy can lower government income and raise the tax burden on regular sector enterprises, making the informal activity more appealing (OECD, T. O.-O, Citation2008).

Hypothesis 1:

Corruption and tax administration worsen a firm’s internal funds/retained earnings

Hypothesis 2:

Corruption and tax administration increase firm’s obstacles to self-finance

4. Empirical results

This section presents the baseline results of corruption and the quality of tax administration on firm self-financing in Africa. The first regression will compute the Tobit model based on a proportional dependent variable, internal funds. The second regression will compute the Multinomial Probit Model for a categorical dependent variable: financing as an obstacle (minor, moderate, major, and severe). For better interpretation, we use marginal effect. Detecting the causal effects of bribery on firm self-financing is a significant issue of this paper due to reverse causal relationships and omitted variables. Firm self-finance is most probably endogenous regarding the firm and business characteristics and the market environment. This study employs an instrumental variable to estimate the main Tobit model to overcome the endogeneity and reverse causality issues.

We use the instrumental variables (IVTobit) approach to discuss the possible endogeneity. The approach to determining instrumental variables needs an instrument that does not influence the dependent variable directly but influences it through the instrument (Silwal, Citation2016). We suspect corruption to be endogenous.

The World Bank Enterprise survey gives a variety of instrumental variables, including dummies for firms applying for electrical, water, and telephone connections and obtaining their license. Following Liu et al. (Citation2020), who use a dummy for electrical application as an instrumental variable for corruption, in our study, we employ not only a firm application for electrical connection (Electricity) but also the application for water connection (Water). Dummy equals 1 if the firm applies to electrical or water connection and 0 otherwise.

We claim that the company’s application to the officials is necessary for resolving the power and water issue and that the company will continue normal operations once the issue is fixed. The power supply and water sector are a natural monopoly with no efficient regulatory system, and government officials can give companies access to it. Monopoly is the main source of firm corruption with government authorities (Yang, Citation2005). As a result, submitting to government authorities to use energy and water facilities means that companies have to negotiate with government officials. Thus, the application follows by negotiations intensifies rent-seeking actions.

Furthermore, there is no clear evidence of a link between companies filing applications for electrical and water connections and firm self-financing. Therefore, these variables’ electric and water connection applications are good IV. We use the IVTobit technique by instrumenting the corruption by application for electrical and water connection in the baseline regression.

4.1. Baseline results: effect of corruption and tax administration on firm self-financing

The baseline estimates of the marginal Tobit model and Instrumental variable are reported in Table . Column 1 and 2 present the result of Tobit model with no controlling for firm characteristic and controlling for firm sector, country, and year dummies, respectively. In column 3, we present IVTobit result with Electricity et Water variables as instrumentals variables. The signs of the results are consistent from column 1 to 3. Table indicates that our key independent variables corruption and tax administration are a negative and statistically significant link to self-financing or internal fund/retailed earnings at 1% significance level. The negative relationship means that corruption and poor tax administration are detrimental to firm internal financing. The result means that an increase in corruption and a poor tax administration decrease the likelihood of firms to self-finance. Increased corruption raises the operating expenses of firms thus reduce firm profit. The failure of officials to meet their initial promises in order to obtain bribes will lead to a higher degree of corruption, and these authorities can seek additional bribes from firms. The results of negative impact of corruption are in line with the study of Beck et al. (Citation2006) and Wellalage and Fernandez (Citation2019) who found that high level on corruption is associated with low capacity of firm bank loan. When the efficiency of fiscal administration is low, firm productivity decreases thus reduces firm profit, which lowers the internal fund. This result supports the hypothesis that a high tax burden is related to bribery, tax avoidance, lower company entry, and lower profits (Braunerhjelm & Eklund, Citation2014; Sequeira & Djankov, Citation2010). That is, weak tax administration raises compliance costs, raising the tax burden (both administrative side and financial side of view) on companies (Dabla-Norris et al., Citation2017) and reducing profits. Administrative burden redirects resources (time and employees) away from profitable activities to those relevant to tax compliance. As a result, firm productivity suffers as production costs rise without extra output.

Table 3. Effect of the effect of corruption and tax administration on firm self-financing: Tobit marginal model

Most control variables are significant and the signs are consistent in the four columns. About control variables, only regulation is not significant linked to firm self-financing. This shows that our control variables gather important information to clarify the outcome variable. Tax rate is significantly positive, which demonstrate that more tax rate is an obstacle, less the likelihood of firms to self-finance. The financial burdens make it tough for firms to use more factors of production to grow due to increased corporate taxes. Tax Foundation (2018) states that Africa’s average corporate tax is 28.81%. That rate is far higher than the rate in other region like Asia 20.65%, Europe region 18.38%, North America region 23.01%, and the average rate in the world that is 23.03%. In columns 1 and 2, being female top manager decrease the likelihood of firm to self-finance. This negative impact of female management on firm performance is in line with the works of scholars such as Van der Zwan et al. (Citation2012), Coleman (Citation2007), Coleman and Robb (Citation2009) who state that female-owned businesses have lower levels of firm size, ability to survive, and productivity than male-owned businesses. After controlling for endogeneity, in column 3 the impact of female being manager becomes insignificant (Campbell & Mínguez-Vera, Citation2008). Training which represents the full time employee formal training is found to be positive and statically significant at 1 percent level. Increasing in trainings improve the likelihood of employees to perform well thus increase profit. Employee training will lead to reduced staff turnover, lower operating costs by reducing equipment breakdowns, and less consumer complaints. Employee training increases worker outcome, saving time and reduces the need for more supervision (Elnaga & Imran, Citation2013).

Since experience is a desirable quality that has been proven to maximize overall productivity, consumer confidence, the economic profit of the firm, as well as managerial salaries, human capital theory argues that an experienced management team should be far more profitable than a less talented manager should. Managers with more experience will also make better strategic decisions. Surprisingly, we found manager experience to decrease the likelihood to firm self-financing. This finding suggests that managers from traditional corporate environments could be more conservative or risk averse when it comes to implementing new business strategies, which will certainly low firm productivity, thus reduce the profit (Flota & Mora, Citation2001; Hundley, Citation2001; Shrader & Siegel, Citation2007). Employment, which is the number, is full-time employees reduce the likelihood for firm to self-finance. This happens when the workforce is not qualified for the needs of the firm. In this, it increases the cost of production. Therefore, it reduces the performance of the firm and the profit (Opeyemi, Citation2019). An increase in the production not surprisingly increases the likelihood to firm self-finance as many sales mean much production thus more profit in line with reviews. Technology in column 1 is positive meaning a company’s website is used to advertise sales and merchandise thus increase the likelihood for firm to increase their performance and profit. Infrastructure is negative in column 1 and 3. Electricity outage decreases firm performance (Opeyemi, Citation2019). Regulation in column 3, loss due crime or thief reduces the likelihood to firm internal finance through reducing firm growth or performance. Also, more firms have access to land more they expand their productivity (Fowowe, Citation2017).

Quality, which is the international firm recognize quality, increases the likelihood of firm accessing to self-finance. More firms are externally recognized by other organizations, more it will be for the firm to expand their activity. Thus, more opportunities and more revenue. Also, external audit decreases the likelihood to firm self-financing. The external audition and expectation reduce firm self-financing in the sense that the auditors impose firm many regulations and no tax evasion (Liu et al., Citation2020). Firm legal status decreases the likelihood of firm self-financing. Small and medium firms are negatively associated with self-financing which mean they have more difficulties to self-finance (Dabla-Norris et al., Citation2019; Fowowe, Citation2017; Fu, Citation2020).

Wald test suggests that corruption is endogenous and rejects the null hypothesis. AR test rejects the null hypothesis that the instrumental are weak, which shows that there is no issue of weak instrumental variables. The first stage results confirming the strong and significance of our instrument variables are shown in Table of Appendix A.

The second baseline results of the marginal effects of Multinomial Probit model estimates are shown in Table . The results show that tax administration, that is a proxy for the quality of tax administration, is positive and statistically significant in financing as minor, moderate, major, and severe obstacles. The meaning is that, for poor tax administration, the likelihood of firm all level of obstacles increase. The same results are seen in the second row with corruption. An increase in corruption increases the likelihood of firms at all levels of obstacles from minor to severe obstacles.

Table 4. Effect of tax administration and corruption on firm self-financing constraints: multinomial probit model marginal effects

For the control variables, Table reports the tax rate to be major and severe financing obstacles. This can be explained by the fact that corporate tax is too excessive in Africa. The average corporate tax in Africa is 28.81% compare to Asia 20.65%, Europe region 18.38%, North America region 23.01% and world average that is 23.03% (Tax Foundation, Citation2018). Being a female manager is reported to be minor and moderate financing obstacle. Financial obstacles increase with number of employees, infrastructure proxies by number of power outage, loss due crime/thief increase the likelihood of financing obstacle at all level. Reported finance obstacle reduces the training and access to land in all level. Production which is total nation sales is reported to reduce the likelihood of financing obstacles at minor level. Quality of firm to be internationally recognized firm legal status are reported to be minor and severe obstacle to financing. External audit is major obstacle to financing. Small and medium firms are seen to have major and severe levels of financing obstacles (Beck et al., Citation2006). The results from manager experience and regulation are not significant.

4.2. Robustness check

To confirm, the results mentioned above of the Tobit model and Multinomial Probit Model, we carry out robustness checks by using different proxies of corruption and the quality of tax administration. In this stage, I use corruption as a dummy variable from the question posed to the firm managers to know whether a gift is requested for an electrical connection. The value of a corruption dummy is 1 if a gift is requested and 0 otherwise. The new proxy of the quality of tax administration that was coded in baseline results as a dummy equal to 1 for major and severe obstacles and 0 otherwise is proxy now as 1 for a response of moderate, major, and severe obstacles and “0” (if otherwise).

Table indicates the results of the effect of tax administration and corruption on firm self-financing using different proxies of corruption and tax administration discussed above. The results related to our key independent variables are similar to those in the baseline results. The formal training and female manager are not statistically significant. The rest of the control variables such as tax rate, manager experience, employment, production, technology, infrastructure, regulation, loss due crime and thief, access to land, firm international quality, external audit and firm status keep the consistent, and the signs of the baseline results. Except for minor differences in the variables coefficient, Table shows the estimates are not statistically different from the baseline findings. Furthermore, the effects of the controlled variables did not significantly differ statistically from those of the baseline. This suggests that the baseline finding is reliable.

Table 5. Effect of tax administration and corruption on firm self-financing. Tobit marginal model. Alternative corruption and tax administration measures

Table shows with the alternative measures of tax administration and corruption, the effect of tax administration and corruption on firm self-financing constraints does not vary. The results show that tax administration is positive and statistically significant in financing as minor, moderate, major, and severe obstacles. The meaning is that, for poor tax administration, the likelihood of firm all level of obstacles increase. The same results are seen in the second row with corruption. An increase in corruption increases the likelihood of firms at all levels of obstacles from minor to severe obstacles. The result is similar to our baseline results more precisely for our key independent variables. Except for minor differences in the variable coefficients, table 4.6 shows the estimates are not statistically different from the baseline findings by exception regulation that was not significant in became significant as indicates that regulation that is time wasted dealing with official in an obstacle to firm self-finance. Furthermore, the effects of the controlled variables did not significantly differ statistically from those of the baseline. This suggests that the baseline finding is robust.

Table 6. Effect of tax administration and corruption on firm self-financing constraints: multinomial probit model marginal effects. Alternative corruption and tax administration measures

5. Extended analysis: effect of tax administration and corruption on firm self-financing by firm size and the interactions with firm size

For testing the impact of weak tax administration on firm self-financing according to firm size, we divide our sample into three parts SMALL, MEDIUM, and LARGE size.

Table indicates that the effect of poor quality of tax administration and corruption on small firms in column 1 for medium firms in column 2, large firms, and large firms in column 3, respectively. The results show that large firms suffer a lot more than smaller and medium firms do. For example, Column 1 indicates a 0.05 decrease in small firm self-financing for the poor perception of tax administration. However, for medium and larger firms as indicated in Columns 2 and 3, a perception of poor tax administration quality lessens their self-financing by 0.03 and 0.10, respectively. This finding illustrates that, while weak tax administration harms firm financing in general, the negative impact on larger firms surpasses the negative impact on smaller and medium firms. That is, in the face of weak tax administration, small and medium businesses tend to benefit in a way than larger firms in Africa. Small firms can effectively stay informal, and thus escape tax commitments (which can compensate for some of the effects) compared with bigger firms that cannot escape poor taxation administrations, as most of them are they are on display for everyone’s attention. This indicates that firms are not encouraged to work on a large scale.

Table 7. Effect of tax administration and corruption on firm self-financing by firm size

This can account for the presence of several smaller informal firms in Africa and the obstacle posed by officials in the effort to formalize informal firms in Africa. On the other hand, large firms struggle more in the sense that they have to gain social capital and reputation, which might, in turn, contribute to more constraints, causing their incapability to use some means to address any unfavorable pressure put upon them by the poor quality of the fiscal administration (i.e. evading taxes by being informal) (Kamasa et al., Citation2019).

Table also shows that SMEs suffer more from corruption than large enterprises. An increase in corruption decreases the likelihood of small and medium firms to self-finance by, respectively, 0.13 and 0.24, whereas the reduction in large firm is not even significant. Thus, corruption issue is more critical in the case of small and medium firms as they spend a large portion of their profit to the government official as a gift or informal payments to reduce the burden of regulations and circumvent taxes. For this reason, big firms are habitually more protected from corruption but further, they are constrained to heavier controls and taxation such as the judiciary, labor regulations, company authorizing, tax administration, and tax charges (Ezebilo et al., Citation2019).

In Table , two interaction terms for tax administration and corruption are included to determine whether the impact of inadequate tax administration on firm self-financing differs for smaller to large enterprises. Table indicates that smaller firms and poor quality tax administration interact negatively (0.0161), and this interaction is significant at 1%. Hence, the overall impact of low tax administration quality on firm self-financing is −0.0659–0.0161(1) = −0.082. For the large firm, the total effect will be −0.0659–0.0288(1) = −0.0947. In line with the results found in Table , this finding demonstrates that although inefficient tax administration reduces self-financing generally, it has a more negative impact on larger firms than on smaller ones. For corruption side, the interaction term for small firm is negative (0.0289) and significant. The overall effect for small firm is −0.0659–0.0289(1) = −0.0948. For large firm, the interation term is −0.0116 but insignificant. The results confirm our findings in Table where we argued that small firms suffer more from corruption than large enterprises.

Table 8. Interaction between firm size, tax administration, and corruption

6. Conclusion

This study looks into the influence of corruption and tax administration on firm self-financing in Africa. By employing the World Bank Enterprise survey (WBES) data for over 45,048 firms across 48 African countries, the findings using the Tobit model reveal that corruption makes it difficult for a firm to self-finance by securing their internal funds or retained earnings. In addition, we discover that weak tax administration decreases firm self-financing. The results are consistent after taking into account firm characteristics, year and country specifications, and endogeneity issues. The finds are robust by using alternation corruption and tax administration proxies. Furthermore, we investigate the level at which corruption and tax administration are obstacles for firm financing by employing the Multinomial Probit model. We categorized financing obstacles into minor, moderate, major, and severe obstacles. We find that firm self-finance obstacles are best predicted by corruption and poor tax administration. The results show that tax administration and corruption are positive and statistically significant in financing as minor, moderate, major, and severe obstacles. The findings are also robust after using alternative corruption and tax administration measures.

In addition, the finding also illustrates that, while weak tax administration harms firm financing in general, the negative impact on larger firms surpasses the smaller and medium firm’s ones. That means for a poor tax administration, small and medium businesses tend to benefit in a way than larger firms in Africa. Small firms can effectively stay informal and thus escape tax commitments compared to

A total of 102 large firms that cannot escape from poor taxation administrations, as most of them are on display for all attention. SMEs suffer more from corruption than large enterprises. Also, the corruption issue is more critical in the case of small and medium companies as they spend a large portion of their profit on the government official as a gift to down the burden of impositions and circumvent taxes. For this reason, big firms are habitually more protected from corruption but further, they are constrained to heavier controls and taxation such as the judiciary, labor regulations, company authorizing, tax administration, and tax charges.

Authors’ contribution

Toure Moumbark (corresponding author) wrote the main manuscript text including the introduction, the literature review, data collection, and the conclusion.

Yawovi M. A. Koudalo wrote formal analysis, software and prepared figures and tables. Toure Moumbark and Yawovi M. A. Koudalo did reviewing/editing.

Disclosure statement

No potential conflict of interest was reported by the authors.

Additional information

Funding

Notes

1. The surveys were conducted in 2006 in 8 countries: Angola, Botswana, Burundi, Democratic Republic of Congo, Eswatini, Gambia, Guinea, Guinea-Bissau, Mauritania, Namibia, Rwanda, and Uganda. 2007 for 8 countries: Ghana, Kenya, Nigeria, Mali, Mozambique, Senegal, South Africa, Zambia; 2009 for 17 countries: Benin, Burkina Faso, Cape Verde, Chad, Congo, Cote d’Ivoire, Eritrea, Gabon, Lesotho, Liberia, Madagascar, Malawi, Mauritius, Niger, Sierra Leone, Togo, Cameroon; 2010 for 3 countries: Angola, Botswana, Democratic Republic of Congo; 2011 for 4 countries: CAR, Ethiopia, Rwanda, Zimbabwe. 8 countries for 2014: Burundi, Malawi, Mauritania, Namibia, Nigeria, Senegal, South Sudan, Sudan. 8 countries for 2016: Cameroon, Egypt, Eswatini, Guinea, Lesotho, Mali, Togo, Zimbabwe. 3 countries for 2017: Liberia, Niger, Sierra Leone. 3 countries for 2018: Chad, Kenya, Mozambique. 3 countries for 2019: Morocco, Rwanda, Zambia. 2 countries for 2020: Egypt, Tunisia.

2. Following Dow and Endersby (Citation2004) who argue that multinomial Logit gives better results even failed to pass IIA assumption, we present the result of multinomial Logit in Table of Appendix A for robustness. The results are similar.

References

- Africapractice. (2005, January). The African Year in 2005.

- Africapractice. (2019, January). The African Year in 2019. Africa practice.

- Aryeetey, E., & Aryeetey, E. (1998). Informal finance for private sector development in Africa. African Development Bank Group.

- Aterido, R., Beck, T., & Iacovone, L. (2011). Gender and finance in sub-Saharan Africa: Are women disadvantaged? World Bank Policy Research Working Paper, (5571).

- Auriol, E., & Warlters, M. (2005). Taxation base in developing countries. Journal of Public Economics, 89(4), 625–28. https://doi.org/10.1016/j.jpubeco.2004.04.008

- Barth, J. R., Lin, C., Lin, P., & Song, F. M. (2009). Corruption in bank lending to firms: Cross-country micro evidence on the beneficial role of competition and information sharing. Journal of Financial Economics, 91(3), 361–388. https://doi.org/10.1016/j.jfineco.2008.04.003

- Beck, T., Demirgüç-Kunt, A., Laeven, L., & Maksimovic, V. (2006). The determinants of financing obstacles. Journal of International Money and Finance, 25(6), 932–952. https://doi.org/10.1016/j.jimonfin.2006.07.005

- Borisova, G., Fotak, V., Holland, K., & Megginson, W. L. (2015). Government ownership and the cost of debt: Evidence from government investments in publicly traded firms. Journal of Financial Economics, 118(1), 168–191. https://doi.org/10.1016/j.jfineco.2015.06.011

- Braunerhjelm, P., & Eklund, J. E. (2014). Taxes, tax administrative burdens and new firm formation. Kyklos, 67(1), 1–11. https://doi.org/10.1111/kykl.12040

- Cai, H., Fang, H., & Xu, L. C. (2011). Eat, drink, firms, government: An investigation of corruption from the entertainment and travel costs of Chinese firms. The Journal of Law and Economics, 54(1), 55–78. https://doi.org/10.1086/651201

- Campbell, K., & Mínguez-Vera, A. (2008). Gender diversity in the boardroom and firm financial performance. Journal of Business Ethics, 83(3), 435–451. https://doi.org/10.1007/s10551-007-9630-y

- Capasso, S., Ohnsorge, F., & Yu, S. (2022). Informality and financial development: A literature review. The Manchester School, 90(5), 587–608.

- Chen, Y., Liu, M., & Su, J. (2013). Greasing the wheels of bank lending: Evidence from private firms in China. Journal of Banking & Finance, 37(7), 2533–2545. https://doi.org/10.1016/j.jbankfin.2013.02.002

- Coleman, S. (2007). Women-owned firms and growth. Journal of Business and Entrepreneurship, 19(2), 31.

- Coleman, S., & Robb, A. (2009). A comparison of new firm financing by gender: Evidence from the Kauffman firm survey data. Small Business Economics, 33(4), 397–411. https://doi.org/10.1007/s11187-009-9205-7

- Dabla-Norris, E., Misch, F., Cleary, D., & Khwaja, M. (2019). The quality of tax administration and firm performance: Evidence from developing countries. International Tax and Public Finance, 27(3), 1–38. https://doi.org/10.1007/s10797-019-09551-y

- Dabla-Norris, M. E., Misch, F., Cleary, M. D., & Khwaja, M. (2017). Tax administration and firm performance: New data and evidence for emerging market and developing economies. International Monetary Fund.

- Dethier, J. J., Hirn, M., & Straub, S. (2011). Explaining enterprise performance in developing countries with business climate survey data. The World Bank Research Observer, 26(2), 258–309. https://doi.org/10.1093/wbro/lkq007

- Djankov, S., Qian, Y., Roland, G., & Zhuravskaya, E. (2007). What makes a successful entrepreneur? Evidence from Brazil (pp. 1–20). Working Paper w0104. Center for Economic and Financial Research:

- Dow, J. K., & Endersby, J. W. (2004). Multinomial probit and multinomial logit: A comparison of choice models for voting research. Electoral Studies, 23(1), 107–122. https://doi.org/10.1016/S0261-3794(03)00040-4

- Dreher, A., & Gassebner, M. (2013). Greasing the wheels? The impact of regulations and corruption on firm entry. Public Choice, 155(3), 413–432. https://doi.org/10.1007/s11127-011-9871-2

- Elnaga, A., & Imran, A. (2013). The effect of training on employee performance. European Journal of Business and Management, 5(4), 137–147.

- Ezebilo, E. E., Odhuno, F., & Kavan, P. (2019). The perceived impact of public sector corruption on economic performance of micro, small, and medium enterprises in a developing country. Economies, 7(3), 89. https://doi.org/10.3390/economies7030089

- Faccio, M., Masulis, R. W., & McConnell, J. J. (2006). Political connections and corporate bailouts. The Journal of Finance, 61(6), 2597–2635. https://doi.org/10.1111/j.1540-6261.2006.01000.x

- Flota, C., & Mora, M. T. (2001). The earnings of self-employed Mexican Americans along the US-Mexico border. The Annals of Regional Science, 35(3), 483–499. https://doi.org/10.1007/s001680100051

- Fowowe, B. (2017). Access to finance and firm performance: Evidence from African countries. Review of Development Finance, 7(1), 6–17. https://doi.org/10.1016/j.rdf.2017.01.006

- Fu, T. (2020). The dilemma of government intervention in a firm’s financing: Evidence from China. International Review of Financial Analysis, 71, 101525. https://doi.org/10.1016/j.irfa.2020.101525

- Fungáčová, Z., Kochanova, A., & Weill, L. (2015). Does money buy credit? firm-level evidence on bribery and bank debt. World Development, 68, 308–322. https://doi.org/10.1016/j.worlddev.2014.12.009

- Gaviria, A. (2002). Assessing the effects of corruption and crime on firm performance: Evidence from Latin America. Emerging Markets Review, 3(3), 245–268. https://doi.org/10.1016/S1566-0141(02)00024-9

- Guariglia, A., & Poncet, S. (2008). Could financial distortions be no impediment to economic growth after all? Evidence from China. Journal of Comparative Economics, 36(4), 633–657. https://doi.org/10.1016/j.jce.2007.12.003

- Gupta, S., Clements, B., Baldacci, E., & Mulas-Granados, C. (2005). Fiscal policy, expenditure composition, and growth in low-income countries. Journal of International Money and Finance, 24(3), 441–463. https://doi.org/10.1016/j.jimonfin.2005.01.004

- Guriev, S. (2004). Red tape and corruption. Journal of Development Economics, 73(2), 489–504. https://doi.org/10.1016/j.jdeveco.2003.06.001

- Haque, N. U., & Sahay, R. (1996). Do government wage cuts close budget deficits? Costs of corruption. Staff Papers - International Monetary Fund, 43(4), 754–778. https://doi.org/10.2307/3867368

- Hundley, G. (2001). Why and when are the self‐employed more satisfied with their work? Industrial Relations: A Journal of Economy & Society, 40(2), 293–316. https://doi.org/10.1111/0019-8676.00209

- Johnson, S., Kaufmann, D., & Zoido-Lobaton, P. (1998). Regulatory discretion and the unofficial economy. The American Economic Review, 88(2), 387–392.

- Kamasa, K., Adu, G., & Oteng-Abayie, E. F. (2019). Tax compliance in sub-Saharan Africa: How important are non-pecuniary factors? African Journal of Economic Review, 7(1), 154–175.

- Kauffmann, C. (2005). Financing SMEs in Africa, policy insights no. 7. African Economic Outlook 2004/2005, African Development Bank and the OECD Development Centre, 9. https://wwwoecd-org.proxy.library.uu.nl/dev/34908457.pdf

- Krueger, A. O. (1974). The political economy of the rent-seeking society. The American Economic Review, 64(3), 291–303.

- Levin, M., & Satarov, G. (2000). Corruption and institutions in Russia. European Journal of Political Economy, 16(1), 113–132. https://doi.org/10.1016/S0176-2680(99)00050-6

- Li, H., Meng, L., Wang, Q., & Zhou, L. A. (2008). Political connections, financing and firm performance: Evidence from Chinese private firms. Journal of Development Economics, 87(2), 283–299. https://doi.org/10.1016/j.jdeveco.2007.03.001

- Liu, P., Li, H., & Guo, H. (2020). The impact of corruption on firms’ access to bank loans: Evidence from China. Economic Research-Ekonomska Istraživanja, 33(1), 1963–1984. https://doi.org/10.1080/1331677X.2020.1768427

- Loayza, N., Schmidt-Hebbel, K., & Servén, L. (2000). Saving in developing countries: An overview. The World Bank Economic Review, 14(3), 393–414.

- Martins, L., Cerdeira, J., & AC Teixeira, A. (2020). Does corruption boost or harm firms’ performance in developing and emerging economies? A firm‐level study. The World Economy, 43(8), 2119–2152. https://doi.org/10.1111/twec.12966

- Mauro, P. (1995). Corruption and growth. The Quarterly Journal of Economics, 110(3), 681–712. https://doi.org/10.2307/2946696

- Moore, M. (2023). Tax obsessions: Taxpayer registration and the “informal sector” in sub‐Saharan Africa. Development Policy Review, 41(1), e12649.

- Murphy, K. M., Shleifer, A., & Vishny, R. W. (1993). Why is rent-seeking so costly to growth? The American Economic Review, 83(2), 409–414.

- (OECD), T. O.-O. (2008). OECD annual report 2008. The Organisation for Economic Co-operation and Development (OECD).

- Opeyemi, A. (2019). The impact of firm size on firms performance in Nigeria: A comparative study of selected firms in the building industry in Nigeria. Asian Development Policy Review, 7(1), 1–11. https://doi.org/10.18488/journal.107.2019.71.1.11

- Qi, S., & Ongena, S. (2019). Will money talk? Firm bribery and credit access. Financial Management, 48(1), 117–157. https://doi.org/10.1111/fima.12218

- Qi, S., Ongena, S., & Cheng, H. (2018). When they work with women, do men Get all the credit? Swiss Finance Institute Research Paper, (18–01).

- Ruan, W., Xiang, E., & Ma, S. (2018). Lending to private firms: Evidence from China on the role of firm openness and bribery. The Chinese Economy, 51(1), 1–19. https://doi.org/10.1080/10971475.2017.1368905

- Santos, J. B., & Brito, L. A. L. (2012). Toward a subjective measurement model for firm performance. BAR-Brazilian Administration Review, 9(SPE), 95–117. https://doi.org/10.1590/S1807-76922012000500007

- Sequeira, S., & Djankov, S. (2010). An empirical study of corruption in ports, MPRA Paper, University Library of Munich,

- Shrader, R., & Siegel, D. S. (2007). Assessing the relationship between human capital and firm performance: Evidence from technology–based new ventures. Entrepreneurship Theory and Practice, 31(6), 893–908. https://doi.org/10.1111/j.1540-6520.2007.00206.x

- Silwal, A. R. (2016). Three essays on agriculture and economic development in Tanzania (Doctoral dissertation, University of Sussex).

- Swamy, A., Knack, S., Lee, Y., & Azfar, O. (2001). Gender and corruption. Journal of Development Economics, 64(1), 25–55. https://doi.org/10.1016/S0304-3878(00)00123-1

- Tax Foundation. (2018). Corporate tax rates around the world, 2018. https://taxfoundation.org/corporate-tax-rates-around-world-2018

- Tobin, J. (1958). Estimation of relationships for limited dependent variables. Econometrica: Journal of the Econometric Society, 26(1), 24–36. https://doi.org/10.2307/1907382

- Tollison, R. D. (2012). The economic theory of rent seeking. Public Choice, 152(1), 73–82. https://doi.org/10.1007/s11127-011-9852-5

- Van der Zwan, P., Verheul, I., & Thurik, A. R. (2012). The entrepreneurial ladder, gender, and regional development. Small Business Economics, 39(3), 627–643. https://doi.org/10.1007/s11187-011-9334-7

- Wellalage, N. H., & Fernandez, V. (2019). Innovation and SME finance: Evidence ftrom developing countries. International Review of Financial Analysis, 66, 101370. https://doi.org/10.1016/j.irfa.2019.06.009

- World Bank. (2020). Global economic prospects, June 2020. The World Bank.

- Yang, D. D. H. (2005). Corruption by monopoly: Bribery in Chinese enterprise licensing as a repeated bargaining game. China Economic Review, 16(2), 171–188. https://doi.org/10.1016/j.chieco.2004.11.003

Appendix A

Table A1. Number of firms in the sample per country

Table A2. Hausman and small-Hsiao tests of IIA assumption

Table A3. Effect of tax administration and corruption on firm self-financing constraints: multinomial Logit model marginal effects

Table A4. First stage of IV Tobit marginal effect model: instrumental variable estimation results