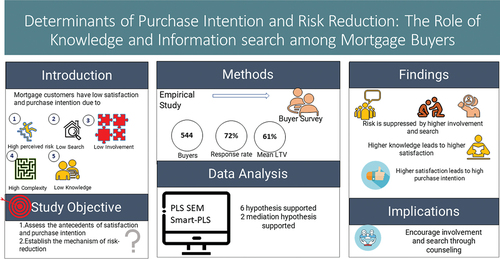

Abstract

As housing demand rose post-COVID-19, new mortgage buyers with distinct preferences are entering the market. Nevertheless, the mortgage purchasing process can prove intricate and precarious for individuals lacking familiarity. Customers leverage various online platforms and supplementary sources to augment their knowledge and mitigate perceived risks, enabling them to make well-informed decisions during the mortgage buying process. Despite exerting these efforts, customers continue to harbor unfavorable purchase intentions due to their subpar purchasing experience, leaving mortgage lenders grappling with retention issues. Research has highlighted that only 15% of mortgage transfer customers would buy a mortgage from the original provider. The present study examines mortgage purchase intention and risk reduction by integrating customer empowerment and uncertainty reduction theories to contribute to the existing literature on mortgage decision-making. A survey was conducted among 554 mortgage buyers, and PLS-SEM was used to test the hypotheses. Knowledge positively influenced satisfaction (β = 0.15, p= = 0.01), and satisfaction positively affected purchase intention (β = 0.75, p = 0.01). The mediating mechanism of risk reduction through involvement and information search is also established. The findings suggest that customers involved in decision-making and information search are more likely to be satisfied with their purchase and experience less risk. Mortgage companies should encourage customers to be more involved and provide complete information during buying. As involved customers experience less confusion; they will make sound financial decisions and remain satisfied and loyal to the mortgage company. Using behavioral finance, policymakers could provide customers necessary nudges to improve decision-making.

PUBLIC INTEREST STATEMENT

The present study analyses customer satisfaction, knowledge, and perceived risk during mortgage buying. Several mortgage lenders face the challenge of adequately satisfying mortgage buyers. In addition, customers are reluctant to buy again from the same mortgage provider. In this context, the authors show that customer satisfaction positively affects purchase intention. The customer`s first experience with the mortgage provider must be good. Providing adequate expertise and reassurance appears to be vital to improving satisfaction. Further, knowledgeable customers are more satisfied with their mortgage provider. Due to the high product complexity in mortgages, customers perceive high risk in mortgage buying. In order to reduce perceived risk, providing mortgage buyers with clear and understandable information is crucial. The study also presents a new and integrated model to analyze customer information processing in mortgages that combines Customer Empowerment Theory and Uncertainty Reduction Theory. This model offers insights into reducing perceived risk and increasing customer knowledge during mortgage buying. The findings have implications for mortgage providers and policymakers in terms of boosting customer information search and offering default options based on demographic profiles.

1. Introduction to the study

Consumer mortgage decision-making is fraught with uncertainty, high risk, and low customer search and satisfaction. The COVID-19 pandemic has impacted customers’ housing preferences (Gamber et al., Citation2022; Liu & Su, Citation2021). Mortgages makeup 40% of a typical household’s liabilities, and poorly bought mortgages have lasting financial consequences (Agarwal et al., Citation2017; Frydman & Camerer, Citation2016). Seeking information can help customers make better decisions, reducing their risk and increasing satisfaction (Andersen et al., Citation2020, Citation2020; Kim & Ziobrowski, Citation2016; Mesly, Citation2021; Sharma et al., Citation2022; Zhang et al., Citation2021). Mortgage risk arises when households cannot accurately forecast future interest rates, property value decreases, and their ability to make payments (Kim & Ziobrowski, Citation2016; Timmons et al., Citation2022). The literature on consumer risk reduction demonstrates the importance of information in reducing perceived risk (Daugherty et al., Citation2008; Lin et al., Citation2021). Along with word-of-mouth and salesperson guidance, the Internet is a crucial source of mortgage information (Boehm & Schlottmann, Citation2020; Hochstein et al., Citation2019). van Ooijen and van Rooij (Citation2016) demonstrate that, though households can manage their daily finances, several households cannot comprehend financial risk during mortgage shopping. Hence, unprepared families face complex and risky mortgage purchases (Khan et al., Citation2022). Research into customer information search using offline and online sources is relatively new (Vinhas & Bowman, Citation2019). Recent work on the role of the Internet in consumer mortgage behavior has focused on the lending behavior of mortgage Fintechs (Fuster et al., Citation2022; Haupert, Citation2022), predicting mortgage delinquency (Chauvet et al., Citation2016), predicting mortgage demand (Carella et al., Citation2020; Pavlicek & Krištoufek, Citation2019), uptake of financial education (Chin & Williams, Citation2020), and savings from information search (Damen & Buyst, Citation2017).

However, none of these studies comprehensively examines the role of internet information search in reducing risk and enhancing mortgage satisfaction and purchase intention. According to Jefferson and Thomas (Citation2020), having access to more information is key for customers when deciding on a mortgage. High search levels empower customers to make informed decisions, but few studies have explored mortgage customer information searches (Damen & Buyst, Citation2017; Woodward & Hall, Citation2012). Because of the high stakes, customers actively seek information, as knowledge of mortgages improves customers’ risk assessment and the likelihood of buying a suitable mortgage (Bialowolski et al., Citation2022; Fornero et al., Citation2011). Hence, little is known about the mechanism to increase mortgage knowledge or reduce risk perception. When making mortgage and financial decisions, consumers often don’t have enough financial knowledge and don’t feel motivated to search for information (Damen & Buyst, Citation2017; Dawes et al., Citation2009; Nicholson et al., Citation2019; Xiao & Huang, Citation2021).

Existing research emphasizes enhancing financial literacy and reducing customer uncertainty and risk in mortgage transactions, but does not examine the underlying mechanism (Andersen et al., Citation2020; Malliaris et al., Citation2022; Woodward & Hall, Citation2012). Also, mortgage customer satisfaction research is scarce (Amin, Citation2020; Amin et al., Citation2011; Loibl et al., Citation2020; Reddy & Thanigan, Citation2022). The opaque structure of the mortgage buying process and heterogeneous stakeholders leads to less trust and satisfaction, and customers report reduced satisfaction with mortgage providers (Bhattacharya et al., Citation2021; Power, Citation2021), with several consumers quick to refinance. Only 28% of mortgage lenders met the buyers’ criteria for expertise, guidance, and communication, causing low customer satisfaction levels (Power, Citation2022a). Further, only 15% of mortgage transfer customers were willing to purchase a mortgage from the original mortgage provider (Power, Citation2022b).

Drawing on the gaps in the literature, this paper aims to address two research objectives: first, to assess the antecedents of mortgage satisfaction and purchase intention. Second, the study establishes the mechanism of consumer risk reduction during mortgage buying by assessing the mediating effect of information search and involvement in decision-making. Hence, the following questions arise: What key factors influence consumer satisfaction and purchase intention in the mortgage context (Reddy & Thanigan, Citation2022)? And, what role do information search and involvement play in mitigating perceived risk (Denegri‐Knott et al., Citation2006; Hu & Krishen, Citation2019; Santos & Gonçalves, Citation2019)? To answer the research question, the study constructs a conceptual model that integrates two crucial and complementary theories of consumer information processing: the customer empowerment theory (CET) and the uncertainty reduction theory (URT). The customer empowerment theory states that knowledge empowers customers to make autonomous decisions (Denegri‐Knott et al., Citation2006; Hu & Krishen, Citation2019). A key aspect of customer empowerment theory is customer involvement and knowledge’s role in enhancing satisfaction (Hu & Krishen, Citation2019; Wolf et al., Citation2015). Uncertainty reduction theory focuses on how buyers simplify complex and risky purchase tasks by seeking internal and external knowledge (Flavián et al., Citation2016; Kramer, Citation1999; Santos & Gonçalves, Citation2019). Uncertainty theory has recently been utilized to explain Internet search and consumer behavior (Lin et al., Citation2021; Lu & Chen, Citation2021; Santos & Gonçalves, Citation2019). This integrated model, proposed by the authors, explains the mechanism of reducing mortgage customer risk and increasing satisfaction. The authors surveyed 554 households who have recently purchased a mortgage. Since the analysis involved theory extension and testing, the partial least squares method (PLS-SEM) was used (Hair et al., Citation2019). The researchers show that knowledge significantly impacts satisfaction and purchase intention. The mechanism of risk reduction through involvement and information search is also established.

The present study contributes to the understanding of mortgage decision-making by filling several gaps in the literature. First, the study extends the current literature on mortgage knowledge, customer satisfaction, and purchase intention (Reddy & Thanigan, Citation2022; Xiao & Porto, Citation2017). Second, the authors examine how search mediates between perceived risk and mortgage product knowledge. This examination explains the underlying mechanism by which the relationship between perceived risk and mortgage knowledge is mediated through involvement and search efforts. To the author’s knowledge, no recent studies have empirically examined the risk reduction process in mortgages. There are more recent studies on risk reduction from the Internet and mobile banking environment, but none on the mortgage environment (Marafon et al., Citation2018; Mulia et al., Citation2020). The present study expands the literature related to mortgage product complexity, risk perception, information search, involvement, knowledge, and purchase outcomes of satisfaction and purchase intention by examining the mechanisms of information search by integrating customer empowerment theory and uncertainty reduction theory. This integration contributes to the theoretical development of customer information processing in mortgages and the role of information in reducing complexity and risk while improving knowledge and satisfaction.

The rest of the paper is organized as follows. The literature review and the development of the hypotheses are presented next. The third section introduces the research methodology. The fourth section presents the results and discussion; the final section highlights the conclusion and limitations of the study.

2. Literature review and hypotheses development

2.1. Theoretical Background

2.1.1. Information overload and product complexity

Information overload occurs when the information load exceeds the limited cognitive capacity of the individual. Research highlights that there is a significant detrimental effect on consumer behavior due to information overload (Alba & Hutchinson, Citation1987). Overloading customers with information can slow their decision-making, lower decision quality, and increase anxiety. The complex neural mechanism of information overload is thoroughly studied by Peng et al. (Citation2021). In the presence of information overload, the central brain area continues to process the information for a time, even beyond the formal decision-making phase. This suggests cognitive agility, where the brain evaluates and compares important information beyond decision-making. However, while this adaptability showcases the brain’s capacity, it also raises questions about the cognitive burden imposed by this prolonged engagement with information. The study conducted by Pernagallo and Torrisi (Citation2022) explores the impact of consumer overload on the effectiveness of financial markets. In their work, Pernagallo and Torrisi (Citation2022) suggest that abundant knowledge can disrupt the basic principles of market balance and go against the conventional belief in informational efficiency. This observation highlights the complex interplay between the processing of information and the behavior of the market. According to Phillips-Wren and Adya (Citation2020), consumer overload has been identified as a significant stressor in consumer decision-making. Decision support systems that aim to aid customers can cause stress by overwhelming consumers with information. A paradox can arise in high-stress decision-making, where tools created to help reduce stress may actually amplify it due to the nature of the information involved. Phillips-Wren and Adya (Citation2020) suggest that it is imperative to find a middle ground between utilizing information to make well-informed decisions and avoiding the potential adverse effects of cognitive and psychological overload.

Bhutta et al. (Citation2015) state that policymakers believe that greater process transparency can empower households to make better quality decisions. As a result, policymakers mandate that more regulatory and competitive information be shared with customers (Nicholson et al., Citation2019). For example, there is an increase in mortgage comparison portals (Damen & Buyst, Citation2017; Damen & Schildermans, Citation2022; Haupert, Citation2022). However, customers who access too much market information perceive product complexity (Huang, Citation2000). Complexity and information overload increase stress, unpleasant emotions, and consumer dissatisfaction (Mick et al., Citation2004). Mortgage brokers and bankers use confusing language to sell to customers with little mortgage knowledge or experience (Woodward & Hall, Citation2012).

In the realm of financial services, such as mortgages, issues related to bank transparency and information concealment have gained prominence in recent years (Nicholson et al., Citation2019). This is particularly pertinent because mortgages exhibit two pivotal characteristics associated with complex products: firstly, they are accompanied by low levels of consumer knowledge, and secondly, there exists a significant risk of consumer exploitation by market participants (Mützel & Kilian, Citation2016). To navigate this product complexity, consumers employ strategies rooted in information processing theories, as they strive to identify diagnostic and salient product attributes that offer high informational value prior to making decisions (Mitchell, Citation1999; Mitchell & McGoldrick, Citation1996; Simon, Citation2000). Hence, customers constructively use information relevant to the type of problem they face (Bettman et al., Citation1998). However, limited research has explored the intricate relationship between product complexity and information in the mortgage context.

2.1.2. Perceived risk

One of the critical outcomes of information overload and complexity is a higher perceived risk (Hu & Krishen, Citation2019; Soto-Acosta et al., Citation2014). Perceived risk refers to the uncertainty experienced by customers when they are unable to anticipate the outcomes of their purchase (Goyal, Citation2008, pp. 332–333). Hence, product knowledge significantly mitigates risk and uncertainty by allowing customers to set accurate expectations. Further, in services, perceived risk is higher because of the experiential nature of the product (Goyal, Citation2008; Song et al., Citation2020). A meta-analysis by Li et al. (Citation2020) showed that high-risk perception and customer purchase intention are negatively correlated. Li et al. (Citation2020) discovered an effect size of − 0.239 and showed the importance of understanding how risk perception affects consumer decision-making. In their study, Holzmeister et al. (Citation2020) investigate the perception of risk associated with financial products and identify its considerable repercussions for the overall well-being of consumers. Recognising the complex and often opaque nature of financial products, Holzmeister et al. (Citation2020, p. 3987) advocate implementing “risk facts labels” on financial products to improve consumer decision-making. Holzmeister et al. (Citation2020) highlight that such “risk facts labels” would serve as a powerful tool to empower consumers and enhance their decision-making capabilities. Therefore, the perception of risk among customers substantially influences their purchase intention and behaviors. Recent research shows that perceived risk negatively influences customer satisfaction and loyalty (Hasan et al., Citation2021; Khasbulloh & Suparna, Citation2022). Hence, recent studies identify that perceived risk generally has a negative impact on customer satisfaction, loyalty, and purchase intentions.

Therefore, scholarly literature supports the notion that individuals who have made the decision to acquire a residential property should consider several approaches to minimize their perceived risk when choosing a mortgage lender. This is because after individuals have chosen a house, they cannot withdraw from the mortgage process. Understanding and mitigating consumers’ perceived risks are crucial for banks and mortgage providers to enhance customer satisfaction and bolster purchasing inclinations.

Typically, people buy mortgages after choosing a home. Therefore, those choosing a mortgage provider must find a way to lower their perceived risk because they cannot opt out (Perry & Lee, Citation2012). In the mortgage context, perceived risk relates to the variance in the mortgage provider’s performance. For example, if the bank charges an origination fee of 1.5% instead of the advertised 0.25%, this increases the cost, or if the invitation rate is 2% and the bank raises it to 4% after six months, the family budget is at risk. Consumer stress in the U.S. and U.K. mortgage markets from rate hikes is too recent and needs no documentation (Savino, Citation2022). The process of consumer risk management is constructive; customers respond to risk based on the purchasing context and personal goals (Bettman et al., Citation2008; Conchar et al., Citation2004). Consistent with Taylor’s (Citation1974) risk management model, the present study examines the importance of information search as a consumer-perceived risk reduction strategy (Chaudhuri, Citation2000).

Mitchell and McGoldrick (Citation1996) summarise the consumer risk reduction process. They propose that in high-risk decisions, customers try to increase the certainty that the decision will not fail rather than be concerned about lessening the repercussions of a poor decision. Customers increase certainty by researching information sources. Further, customers seek knowledge that either clarifies or simplifies the decision. Clarification helps the customer improve their ability to diagnose the information, whereas simplification involves following others’ advice. For example, a simplification strategy is when a customer buys a mortgage with the lowest origination fees. A clarifying technique uses the same origination fee information to analyze whether additional benefits—fast processing, fewer bank trips, and home service—are worth the fee. Because home loans are high-stakes products, customers seek a clarification strategy of increasing knowledge of the critical attributes of mortgages before deciding.

Contrary to this rational view of the customer (Bettman et al., Citation2008), contend that first-time customers overlook risk when risk probabilities cannot be decreased to zero. This means that new customers ignore risks that cannot be completely eliminated. Few customers react emotionally to perceived risk. Customers overreact to risk by focusing on safety while ignoring other information or under-react when they realize that risk probability cannot be decreased to zero. For example, the possibility of a bank raising interest rates in the next six months is non-zero for the consumer; thus, they may under-react or ignore this information but overreact to negotiable closing fees. The authors attempt to clarify this literature and understand the actual behavior of mortgage-buying customers.

2.1.3. Involvement

Involvement is a customer’s interest in a product class (Abdel Wahab et al., Citation2023; Dholakia, Citation1997), and the customer’s level of purchase decision involvement reflects the decision’s importance. Research has highlighted that when it comes to high-risk purchases like mortgages, perceived risk is a key factor in people’s level of involvement (Aldlaigan & Buttle, Citation2001; Bloch et al., Citation1986; Dholakia, Citation2001; Laurent & Kapferer, Citation1985). Customers cannot increase their level of knowledge if they are not involved in learning more about the product or service. While advertising relies on rote learning, customer involvement improves knowledge retention for products like mortgages, where decisions are made based on comprehensive understanding. Higher involvement enhances customer knowledge and self-persuasion efforts (Chaiken & Ledgerwood, Citation2011; Petty & Cacioppo, Citation1986; Silic & Ruf, Citation2018). So, competent consumers can acquire new insights from old facts.

2.1.4. Information search

Customer information search efforts include the perceived benefits of the search and the Internet sources visited by the customer. Perceived search benefits are about the customer’s perception that searching for more information would benefit the purchase decision and measure the subjective perceptions of the customer. Customers seek information from multiple sources, such as friends, family, third parties, and banks (Choudhary & Zhang, Citation2023; Devlin, Citation2002; Lee & Hogarth, Citation2000). The relevance of social media in augmenting customer search is underscored in a recent study conducted by Pop et al. (Citation2022). Glogovețan et al. (Citation2022) emphasize that when engaging in online purchasing, individuals are subject to several influences, including the opinions and recommendations of their social network, personal characteristics such as personality traits, and their degrees of knowledge and curiosity. The number of internet sources (Dawes et al., Citation2009) reflects the objective search effort by the customers. Customers use bank and comparison websites to find more mortgage information (Damen & Buyst, Citation2017). According to a study conducted by Laffey and Gandy (Citation2009) in the United Kingdom, comparison websites provide consumers with the convenience of efficiently comparing various products, typically arranged by price. These websites serve as a valuable resource for sellers, connecting them with potential customers who have already narrowed their preferences through comparison. According to the survey conducted for the present study, the typical consumer examined an average of 3.6 websites while deciding on a mortgage. Research by (Damen & Buyst, Citation2017) has shown that adequate customer information search leads to higher knowledge and landing a good deal.

2.1.5. Satisfaction and purchase intention

Oliver (Citation2014, p.8) defines customer satisfaction as “a customer’s judgment that a service provided a pleasurable level of fulfilment” and is related to the psychological distance between customer expectations and actual firm performance. Recent research shows that customers with a strong knowledge of financial products are satisfied (Barbu et al., Citation2021; Garrett & James Iii, Citation2013; Joo & Grable, Citation2004; Xiao & Porto, Citation2017). Customers reduce risk by buying the same product when satisfied or the competition when dissatisfied (Mitra et al., Citation1999; Torres‐Moraga et al., Citation2008). Consumer satisfaction strongly influences purchase intention (Tuu et al., Citation2011). In a recent study on home buying behavior, Dash et al. (Citation2021) found that high satisfaction leads to high purchase intention. Despite similar satisfaction levels, industry-specific purchase intentions vary (Power, Citation2021; Szymanski & Henard, Citation2001).

2.2. Theoretical underpinnings of the research model

According to Ravitch and Riggan (Citation2016), theoretical frameworks are the formal theories that address the research questions, enable the researcher to understand the phenomenon and provide a rationale for the hypothesis and methodology. For the present study, the authors use the framework of customer empowerment theory and uncertainty reduction theory to examine the role of information in reducing risk and improving consumer knowledge and satisfaction (Hu & Krishen, Citation2019; Kramer, Citation1999; Santos & Gonçalves, Citation2019). The paper builds a theoretical model to examine the determinants of customer risk reduction, satisfaction, and purchase intention in mortgage buying. Customer empowerment theory applies to the current research because it describes how customers cognitively adapt to information overload and seek helpful information before purchasing. Similarly, uncertainty reduction theory explains the customer’s motivation to seek information to reduce complexity and perceived risk. The current study context requires a model that includes consumer empowerment and uncertainty reduction to examine the interrelated factors affecting knowledge and decision satisfaction.

2.2.1. Consumer empowerment theory

Marketing information provides consumers with knowledge and enables them to make informed decisions. Policymakers are trying to arm customers with more information to help customers make better decisions (Bhutta et al., Citation2015; Denegri‐Knott et al., Citation2006; Desmond, Citation2003). Hu and Krishen (Citation2019) used consumer empowerment theory to analyze customer reviews. They use the constructs of information overload, product involvement, product knowledge, and customer satisfaction to show how consumers respond to increased levels of information. Hu and Krishen (Citation2019) recommend more research on high-risk products and risk-coping strategies. The current study builds on this gap to examine the role of these constructs in mortgage buying, which is a high-risk product (Agarwal et al., Citation2014). While Hu and Krishen (Citation2019) examine unregulated customer-written product reviews, mortgage industry information comes from three sources: regulated information like prime rates, information from marketers like advertising, and third-party information from websites or brokers (van Ooijen & van Rooij, Citation2016). Because the CET model is a comprehensive approach containing key elements that consider both customer and information characteristics, it is appropriate for this study.

2.2.2. Uncertainty reduction theory

Government banks, private banks, and large housing financing corporations compete in the Indian mortgage market with different value propositions (CRIF, Citation2021). Because of the heterogeneity of the mortgage markets, customers are uncertain about their mortgage provider performance. Therefore, customers perceive a high level of risk and try to minimize it (Lin et al., Citation2021). Uncertainty Reduction Theory (Knobloch, Citation2015; Kramer, Citation1999) predicts that customers will use both external (marketing communications or word of mouth) and internal (recall and learning) sources to get product information to reduce perceived risk (Daugherty et al., Citation2008; Lin et al., Citation2021). Because of the high stakes of high-involvement products like mortgages, customers actively seek information before buying (Bialowolski et al., Citation2022; Kramer, Citation1999). Based on Flavián et al. (Citation2016), Santos and Gonçalves (Citation2019) demonstrate how customers use a combination of online and offline information channels to reduce their service uncertainty. At the same time, Santos and Gonçalves (Citation2019) limit their analysis to consumer durables purchases but invite future research to extend it. Examining mortgage uncertainty reduction would advance the field, as mortgage buying poses significant risks for customers (Agarwal et al., Citation2014, Ijevleva & Sloka, Citation2012; Johnston, Citation2009).

2.3. Research model and hypotheses development

Figure shows the research model developed for this study, incorporating the determinants of knowledge and satisfaction during mortgage buying. The present study proposes that customers manage product complexity and perceived risk by increasing their involvement and information search, leading to higher knowledge of mortgages. Higher knowledge leads customers to higher satisfaction and purchase intentions. To understand this phenomenon in mortgages, the CET model by Hu and Krishen (Citation2019) and the URT model (Santos & Gonçalves, Citation2019) have been modified, and the proposed integrated model examines the relationship between the following variables: product complexity, perceived risk, involvement, perceived search benefits, knowledge, and satisfaction. Additionally, the authors incorporate the observed variable of the number of internet site visits. Appendix Table offers a summary of the relevant literature.

Figure 1. Theoretical framework.

2.3. Hypothesis Development

2.3.1. Complexity and Perceived Risk

Product complexity is the consumer’s evaluation of the time and effort required to comprehend and use a product (Adjei et al., Citation2010; Fürst et al., Citation2023). Fürst et al. (Citation2023) emphasizes the perception of structural complexity among customers when products possess greater heterogeneity and interconnected attributes. Financial products such as mortgages are complex because they are rarely purchased but significantly impact consumer welfare (Amromin et al., Citation2018; Hochstein et al., Citation2019; Khan et al., Citation2022). Hochstein et al. (Citation2019) highlight the importance of salesperson interaction while buying complex financial products. Research shows that high perceived complexity leads customers to perceive high financial risk when purchasing financial products (Linciano et al., Citation2018; Mützel & Kilian, Citation2016; Perry & Lee, Citation2012; Van Raaij, Citation2016; Wang et al., Citation2011). Firstly, customers are not aware of the features of the mortgage product; secondly, customers tend to be apprehensive about the multiple steps involved in the mortgage process (Bhattacharya et al., Citation2021). Hence, product complexity, particularly in complex financial products like mortgages, affects customers’ ability to comprehend and use the product, leading to high perceived financial risk. Therefore, it is hypothesized that:

Hypothesis 1:

− High complexity is positively related to perceived risk.

2.3.2. Perceived Risk and Information Search

Perceived risk is an “individual’s assessment or interpretation of the riskiness of a decision.” Risk perception combines uncertainty, ignorance, and the severity of consequences (Fischhoff et al., Citation1978; Goyal, Citation2008). Mortgage customers are entering a new buying environment with limited knowledge and experience, and information overload leads them to perceive high risk (Arora et al., Citation2011; Jacoby et al., Citation1974; Malliaris et al., Citation2022; van Ooijen & van Rooij, Citation2016; Woodward & Hall, Citation2012). Customers can reduce risk by obtaining appropriate information from informal sources, such as peers or the Internet (Arora et al., Citation2011; Malliaris et al., Citation2022; Mitchell & McGoldrick, Citation1996; Zhao & Liu, Citation2021). According to Jepsen (Citation2007), there exists a correlation between the extent of internet usage and its impact on the utilization of online platforms for conducting pre-purchase information searches. Guo et al. (Citation2020) discovered a positive correlation between consumer-perceived risk, information necessity, and the extent of information search and processing.

The literature provides evidence of a positive relationship between higher perceived risk and increased search effort, as demonstrated by the findings of Srinivasan and Ratchford (Citation1991). According to Zhang and Hou (Citation2017), customers’ pre-purchase information search activity is influenced by two dimensions of perceived risk, namely functional risk and emotional risk. Customers with a heightened perception of risk are apprehensive about the lack of certainty in the decision-making process and the potential negative outcomes associated with making an unfavorable choice. Therefore, it is justifiable to anticipate that consumers will safeguard their personal interests and acquire information through informal sources, including the Internet. Therefore, an increased perception of risk prompts customers to engage in information-seeking behavior before purchasing. Therefore,

Hypothesis 2a:

− Higher perceived risk is positively related to perceived search benefits.

Hypothesis 2b:

− Higher perceived risk is positively related to the number of internet sources.

2.3.3. Perceived risk and involvement

Customers with higher risk perception, particularly in high-stakes transactions like mortgages, are more involved and committed (Aldlaigan & Buttle, Citation2001; Seabra et al., Citation2014; Su et al., Citation2021). Since customers must plan and save to buy a home and mortgage, a higher risk perception would raise their mortgage purchase involvement. Prior studies show that customer involvement increases when they perceive a high level of risk in the buying situation (Dholakia, Citation1997, Citation2001; Michaelidou & Dibb, Citation2008). A higher risk perception would increase customers’ fear of loss or regret. Consequently, customers may actively control the purchase process and try to modify it to their advantage, thereby increasing their involvement. Hence,

Hypothesis 3:

− High perceived risk is positively related to involvement.

2.3.4. Perceived search benefits and internet sources

Customers who experience more perceived benefits during the information search process are more inclined to utilize Internet sources. According to Guo (Citation2001 p 506), the process of consumer information searches is influenced by cost-benefit analysis. It may be reasonably inferred that an internet search has no direct monetary cost for users. However, users do incur costs in terms of evaluating a certain set of features and processing information in order to make an optimal selection (Jolivet & Turon, Citation2019). Research studies (Beatty & Smith, Citation1987; Singh & Jang, Citation2022; Srinivasan & Ratchford, Citation1991) have shown that higher perceived search benefits are positively related to high external search. Customers tend to utilize internet sources, including social media platforms, according to their lifestyle necessities and the degree of trust they place in such sources of information (Dabija et al., Citation2018). Customers with high perceived search benefits are keen to find product-related information as it allows them to compare the various mortgage providers easily. For customers with high perceived search benefits, the Internet is a ready source of timely, convenient, and personalized information at a low cost and offers high knowledge gain and benefits. Hence,

Hypothesis 4:

− High search benefits are positively related to the number of internet sources used.

2.3.5. Information Search and Knowledge

Customers who seek external information are more likely to report higher cognitive evaluations, thereby improving personal knowledge (Hamilton & Yao, Citation2018; Llewellyn et al., Citation2021). This influence of external information on customer understanding is called the Google effect (Ward et al., Citation2022). The Internet allows customers to construct an external transactive memory source (like a family member who remembers birthdays) (Firth et al., Citation2019). Ward et al. (Citation2022) discovered that greater Internet usage enhances customer confidence in financial decision-making. Diwanji et al. (Citation2023) emphasize that when consumers become accustomed to utilizing search engines, there is an increased propensity for them to rely on search results as a determining factor in their purchasing choices. Online information enhances customer knowledge, so customers with greater search benefits will probably have a deeper knowledge of mortgages. Customers who search for more information are more likely to learn from the various perspectives presented when they expose themselves to more information sources. Also, customers could enhance their confidence in mortgage decision-making when they access a range of sources to increase their understanding of mortgages.

Hypothesis 5a:

− High search benefits are positively related to knowledge of mortgages.

Hypothesis 5b:

− High usage of internet sources is positively related to knowledge of mortgages.

2.3.6. Involvement and knowledge

Highly involved customers, such as mortgage buyers, carefully weigh the pros and cons before purchasing (Abdel Wahab et al., Citation2023; Amarasinghe Arachchige et al., Citation2022; Park & Moon, Citation2003). High-involvement customers spend more time comparing mortgage lenders before deciding. Also, the inability to return a wrongly purchased mortgage pushes customers to be involved and knowledgeable. Hence, high involvement in buying services, such as mortgages, is correlated with higher customer product knowledge (Huang et al., Citation2014). Customers with high involvement are very focused and engaged with the mortgage purchase decision. This engagement results in customers processing and retaining more information. Involved customers can thoroughly evaluate and critically assess the presented information and carefully weigh the pros and cons of different lenders, resulting in higher knowledge. Therefore,

Hypothesis 6:

− High involvement is positively related to knowledge of mortgages.

2.3.7. Knowledge and satisfaction

According to the customer empowerment theory, greater customer knowledge leads to greater customer satisfaction (Hu & Krishen, Citation2019). Tharp et al. (Citation2020) discovered a positive relationship between financial knowledge and financial satisfaction in home buying. Using the NSMO dataset, Reddy and Thanigan (Citation2022) determined that greater mortgage knowledge leads to greater satisfaction. Increased knowledge enables customers to make more informed decisions and take control of the buying process, leading to greater satisfaction. Also, with more knowledge, customers can clearly identify their needs and formulate their expectations to increase their satisfaction. Therefore:

Hypothesis 7:

− High knowledge is positively related to satisfaction with the terms of the mortgages.

2.3.8. Satisfaction and repurchase intention

Research has established a strong relationship between satisfaction and purchase intention (Dash et al., Citation2021; Johnson et al., Citation2008; Szymanski & Henard, Citation2001; Walsh & Mitchell, Citation2010). Higher purchase intentions help mortgage companies increase their profitability (Power, Citation2022a). In the context of FinTech, Barbu et al. (Citation2021) emphasize the importance of the information experience in effectively communicating novel and beneficial information to customers. Additionally, they underscore the substantial impact of cognitive experience on customers’ purchase intention. A satisfied customer associates positive experiences with the mortgage provider and is likelier to perceive its services as valuable, leading to increased purchase intention. Additionally, satisfied customers are more likely to forgive minor issues encountered when purchasing from the mortgage provider in future purchase decisions. Based on the literature support, it is hypothesized that:

Hypothesis 8:

− High satisfaction is positively related to purchase intention.

2.3.9 The mediating role of involvement and information search

Existing literature shows that customers might reduce their perceived risk by becoming more involved in purchasing decisions or searching for more information (Daugherty et al., Citation2008; Dholakia, Citation2001; Lin et al., Citation2021). At a neurological level, when faced with high situational involvement, customers experience perceived risk first as anxiety and subsequently as cognitive inferences (Bettman et al., Citation2008; LeDoux, Citation1994; Zajonc & Markus, Citation1982). By increasing involvement, consumers reduce perceived risk. Higher involvement leads to customers gathering diagnostic knowledge about the brands and attributes (Dholakia, Citation2001). Hence, it is likely that involvement can be a mechanism for customers to reduce perceived risk through knowledge acquisition. Similarly, information-search is a risk-reducing technique for consumers in high-risk situations, and the information-search intensity is strongly related to higher risk reduction (Conchar et al., Citation2004; Dowling & Staelin, Citation1994; Zuschke, Citation2020). Beatty and Smith (Citation1987) observed that customers with higher perceived risk conduct more searches when purchasing complex products.

Hence, consumers reduce risk by finding helpful information about the attributes, leading to higher knowledge. Consistent with the customer uncertainty reduction theory, accumulated knowledge reduces customer uncertainty. Thus, involvement and information search serve as distinct paths to reducing risk. However, it may be impossible to draw clear boundaries between the two types of risk reduction, as individual customers may use greater involvement or information search to reduce their perceived risk. Also, no formal limitation or compulsion prevents the customer from switching between these two risk-mitigating strategies. Therefore, it is not the purpose of the study to draw boundaries around the risk mitigation strategy. Instead, the authors suggest that both risk-reducing strategies are parallel mediators of the impact of perceived risk on consumer knowledge about mortgages. Hence, it is proposed that:

Hypothesis 9a:

− Perceived search benefits mediate the relationship between perceived risk and knowledge.

Hypothesis 9b:

− Involvement mediates the relationship between perceived risk and knowledge.

3. Research Methodology

The study aims to examine the mechanism of customer risk reduction and the antecedents of mortgage satisfaction and purchase intention by providing empirical evidence of the relationships. In this study, it has been ontologically postulated that consumer perceptions, attitudes, and knowledge about mortgages result from the customer’s experience of buying a mortgage and are held in an intangible form. Given the lack of public disclosure regarding customers’ mortgage purchasing process, it is deemed appropriate to conduct a survey in order to ascertain their respective experiences. The survey technique facilitates the confidential sharing of customers’ mortgage buying experiences. The utilization of a theory testing approach such as PLS-SEM in the examination of consumer response data enables researchers to uncover multivariate relationships among several variables and address the research questions at hand.

3.1. Data collection and sampling

The study focuses on the behavioral patterns exhibited by mortgage customers. Consequently, a representative sample of customers who have recently purchased mortgages in various regions of India was carefully chosen. A cross-sectional survey was conducted, wherein a sample of mortgage customers was solicited to participate and respond to a structured questionnaire. The survey was conducted between June and August 2022. A professional research agency was engaged to collect data from customers living across 190 Indian postal codes. Two thousand two hundred mortgage loan customers from the past three years were identified. Of these customers, only 765 clients could be reached for the survey. A survey questionnaire was completed by a total of 554 participants, indicating a response rate of 72.4%. This response percentage can be considered satisfactory (Kato & Miura, Citation2021). The field representatives established personal contact with each participant and administered the survey at their business or residential address. Table provides the demographic details of the sample. The male participants constituted 65.9% of the sample, while the female participants accounted for 33.2% of the overall sample. The proportion of salaried consumers in the whole sample was 70.4%, while self-employed individuals accounted for 29.2% of the sample. Regarding the property types for which mortgages were obtained, it was found that 8.5% of respondents purchased detached houses, while 63.2% opted for flats or condominiums. This indicates that a substantial proportion of the sample population resides in apartment-style dwellings, consistent with recent trends in the real estate market. Additionally, 14.8% of respondents chose home extensions, while 13.5% acquired plots of land. The average loan amount observed in the study was 28.1 lakhs (equivalent to 2.8 million rupees), with the minimum loan amount recorded at two lakhs (0.2 million rupees) and the maximum loan amount reaching 150 lakhs (15 million rupees). The average loan-to-value ratio is 0.61, indicating that, on average, consumers obtain a loan amount that is 61% of the property’s appraised value. A recent report by an Indian credit bureau shows that the average loan size was 28 lakhs, age was 35 and purchased mainly by salaried customers (CRIF, Citation2021). Hence, the study sample truly represents Indian mortgage buyers.

Table 1. Demographic profile

3.2. Measures

The researchers used established scales from the literature, with necessary modifications for the mortgage context. Perceived risk is the state of uncertainty that customers feel when they cannot predict what will happen with their mortgage purchases and was measured using a 5-item scale derived from (DelVecchio & Smith, Citation2005). Researchers gauged involvement using a 3-item scale created by Kim and Sung in 2009. The scale measured the importance that customers placed on their purchases. Knowledge was measured using a 5-item scale developed by (Laroche et al., Citation2005), and this scale serves as a metric for assessing customers’ knowledge of mortgages. Product complexity measuring the level of complexity which customers encountered in mortgage purchases was measured using the 2-item scale adopted from (Heitmann et al., Citation2007). The measurement of perceived search benefits, denoting the benefits customers derive from information search, was conducted utilizing a 4-item scale developed by Srinivasan and Ratchford in 1991. The number of internet sources was measured as a continuous variable using a unidimensional scale and measured the objective search effort of the customers (Dawes et al., Citation2009). Mortgage satisfaction was measured from the 5-item scale employed by the National Survey of Mortgage Origination (NSMO) and measures customer satisfaction with the mortgage process (Critchfield et al., Citation2019). Purchase intention refers to customers’ willingness to buy mortgages from the same bank and was measured with a 6-item scale adopted from (D’Souza et al., Citation2021). All scales, with the exception of the number of internet sources, represent latent constructs, while the latter is an observed variable. The customer responses were recorded using a 5-point Likert scale. An overview of the descriptive data for the surveyed items is presented in Appendix Table . Furthermore, Table below exhibits the items utilized in the survey, along with their respective loadings.

Table 2. Factor loadings and reliability assessment

4. Analysis and results

4.1. Data analysis

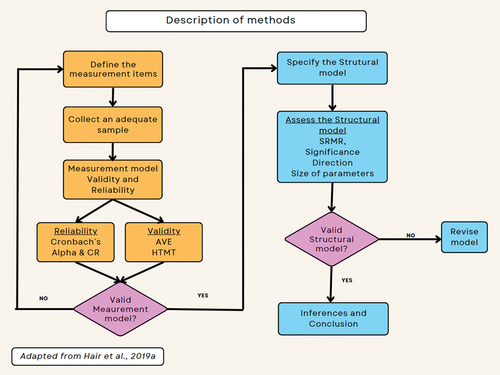

The present study used PLS-SEM (Partial Least Squares Structural Equation Modeling), as implemented in SmartPLS (Hair et al., Citation2019). PLS-SEM excels in handling complex survey datasets, offering support for conducting exploratory and confirmatory analyses. PLS-SEM is an excellent tool for structural modeling as it allows the researcher to understand intricate relationships within the research constructs, thereby providing accurate and nuanced insights into the phenomenon. The (PLS-SEM) methodology undertakes the estimation of latent construct scores and structural model path coefficients through a two-step process. Therefore, PLS-SEM results are analyzed in two phases: initially, the latent constructs undergo assessment for validity and reliability, followed by the examination of regression weights and the significance of correlations, which are based on path coefficients. Evaluating the significance of the relationships is a test of the plausibility of the hypotheses proposed by the researcher. Because the PLS-SEM technique processes multiple endogenous and exogenous variables simultaneously, this technique is appropriate for analyzing the antecedents of mortgage satisfaction and purchase intention (Hair et al., Citation2019). Further, PLS-SEM is a technique that allows for extending theories in complex fields, such as mortgage buying (Hair et al., Citation2019). Appendix Figure summarizes the methodology adopted in the present study.

4.1.1. Measurement model

The evaluation of reliability in the context of structural equation modeling refers to the examination of the consistency and stability of the measurement instruments employed to capture latent constructs (Hair et al., Citation2019). Reliability is evaluated using internal validity and composite reliability tests (Henseler et al., Citation2016). The evaluation of internal validity, as measured by Cronbach’s alpha, measures the extent to which the indicators within a latent construct reliably capture exactly the same underlying psychological concept. The Cronbach’s alpha coefficient exceeded 0.6 for all latent constructs, thus demonstrating an adequate degree of internal validity. Composite reliability offers an assessment of the extent to which the observed indicators accurately represent the actual scores of the latent construct. In this study, the latent variables have composite reliability values above 0.7 (Hair et al., Citation2019; Peterson & Kim, Citation2013). Hence, the measurement model proposed by the authors has high reliability. The authors use Harman’s single-factor test to check common method bias (Podsakoff et al., Citation2003). Single-factor extraction was 19.7%, well below the 50% criterion, indicating no common method bias.

Guide and Ketokivi (Citation2015) propose that it is imperative for researchers to establish causality prior to undertaking the study. Reverse causality occurs when the anticipated cause-and-effect relationship is contrary to the initial hypothesis. The concept of reverse causality holds significant relevance in the field of structural equation modeling. In order to address this concern, Kock (Citation2022) recommends employing the Nonlinear Bivariate Causality Direction Ratio (NLBCDR) approach as a means to ascertain causality. According to Kock (Citation2022), it is recommended that the ratio be equal to or greater than 0.7. The researchers tested the Nonlinear bivariate causality direction ratio (NLBCDR) and found that the NLBCDR value was 0.80, indicating that reverse causality was not an issue. Moreover, the model’s R2 value of 56.4% indicates a strong relationship between the variables. Additionally, the Tenenhaus Goodness-of-Fit (GoF) measure is 0.382, the Simpson’s paradox ratio and the Statistical suppression ratio are both 1.000, indicating that there is no evidence of causality being a concern in this study.

The assessment of convergent and discriminant validity in PLS-SEM is paramount as it guarantees the accurate representation of the latent constructs by the measurement instruments and facilitates their differentiation from each other. Convergent validity is “the degree to which two measures of the same concept are correlated” (Hair et al., Citation2019, p 162). Convergent validity is the evaluation of the degree to which the items intended to measure a particular concept exhibit strong intercorrelations. Convergent validity is assessed using average variance extracted (AVE), the mean of all the squared loadings associated with a construct (Hair et al., Citation2019). A higher average extracted variance (AVE) value indicates more convergent validity, suggesting that the indicators collectively demonstrate an excellent representation of the underlying construct. Table shows that AVE is above 0.5 for all constructs, establishing convergent validity (Fornell & Larcker, Citation1981).

Table 3. Convergent validity- Fornell Larcker Table

Discriminant validity evaluates the “degree to which two conceptually similar concepts are distinct” (Hair et al., Citation2019, p162). Discriminant validity evaluates whether the magnitude of the correlation between indicators within a specified construct surpasses the correlation observed among indicators from different constructs. The Fornell-Larcker criterion has conventionally been employed for establishing discriminant validity. However, contemporary advancements in PLS-SEM methodology advocate for the evaluation of discriminant validity by utilising the bootstrap HTMT (hetereotrait-monotrait ratio) table (Hair et al., Citation2019; Henseler et al., Citation2015). HTMT is the “mean value of the indicator correlations across constructs relative to the mean of the average correlations of indicators measuring the same construct” (Hair et al., Citation2019, p 776). According to the findings presented in Table , it can be observed that the bootstrapped HTMT values, which are below the threshold of 0.9, provide evidence in support of discriminant validity (Henseler et al., Citation2015).

Table 4. Discriminant validity—bootstrapped HTMT values

The assessment of the measurement model provides confirmation that the constructs exhibit internal consistency and possess adequate discriminant validity, thereby establishing the foundation for the subsequent analysis of the structural model.

4.1.2. Structural Model Evaluation

The partial least squares approach (PLS-SEM) is a variance-based technique that allows the researcher to study the complex relationship between multiple variables simultaneously (Chin, Citation1998; Hair et al., Citation2019). The standardized root mean square residual (SRMR) is a statistical measure used to assess the goodness-of-fit of a structural model (Hu & Bentler, Citation1999). It quantifies the disparity between the observed covariance matrix and the covariance matrix predicted by the model. A smaller standardized root mean square residual (SRMR) score suggests a stronger alignment between the model and the observed data. The estimated model had an SRMR value of 0.043, which is lower than the SRMR of 0.08 proposed by Hu and Bentler (Citation1999). Multicollinearity manifests itself as the existence of strong correlations between two or more predictor variables, leading to potential difficulties in precisely estimating and analyzing relationships within the model. The Variance Inflation Factor (VIF) is a statistical metric employed for assessing the existence of multicollinearity among predictor variables within a specified model. As the VIF (Variation Inflation Factor) in the present study is below 3.0, there is no multicollinearity (Hair et al., Citation2019). The model R2 of 56.4% demonstrates a significant effect (Hair et al., Citation2019).

Bootstrapping is a resampling approach that is utilized within the context of Partial Least Squares Structural Equation Modeling (PLS-SEM). Its primary objective is to evaluate the reliability and statistical significance of multiple model parameters. The parameters encompass path coefficients, loadings, and correlations pertaining to latent variables. In the current investigation, the technique of bootstrapping was utilized to evaluate the statistical significance of the path coefficients within the structural model (Hair et al., Citation2019; Henseler, Citation2020). Table indicates the bootstrapped path coefficients. Six of the ten proposed hypotheses were accepted.

Table 5. Hypothesis testing

The findings from the PLS-SEM analysis, as presented in Table , provide evidence in favor of the relationships proposed in six hypotheses, while four hypotheses were not supported. The perceived risk is considerably influenced by the complexity of the product, as indicated by H1 (β = 0.511). The hypothesis H2a did not receive support in the study, however H2b (β = 0.126) received support. The influence of perceived risk on the probability of utilizing internet sources was shown to be significant. The hypothesis H3, which posited a positive relationship between perceived risk and involvement, did not receive empirical support. The fourth hypothesis (H4), which posits that an increase in perceived search benefits leads to a usage of higher number of Internet sources, was not substantiated by the findings of this study. The study investigated the impact of information search on knowledge through the examination of Hypotheses H5a and H5b. The results indicate that H5a is supported (β = 0.126), but H5b is not supported. The hypothesis H6, which suggests that more consumer involvement has a favorable impact on mortgage knowledge, is supported (β = 0.559). The study supports H7, which proposed that an increase in customer knowledge positively impacts customer satisfaction (β = 0.105). Furthermore, H8, which proposed that greater levels of customer satisfaction lead to an increase in purchase intention, is also supported (β = 0.753).

Subsequently, the researchers conducted a mediation analysis in order to elucidate the underlying mechanisms responsible for the reduction of perceived risk. The mediation test is employed to assess if the mediator modifies the effect of the constructs that are posited to mediate. The authors use the bootstrapping procedure of PLS-SEM, which gives more accurate results than PROCESS (Hair et al., Citation2021; Nitzl et al., Citation2016; Sarstedt et al., Citation2020). Table presents the results indicating that two of the three mediating relationships are statistically significant. Specifically, the findings demonstrate that involvement (H9a) and perceived search benefits (H9b) act as parallel mediators, fully mediating the relationship between perceived risk and consumer knowledge (Hair et al., Citation2021; Sarstedt et al., Citation2020).

Table 6. Bootstrap test of mediation

5. Discussion of Results

The results show that increasing consumer knowledge, involvement, and information search while reducing perceived risk increases consumer purchase intent and satisfaction with mortgages. The findings echo previous work focused on financial literacy (Xiao & Porto, Citation2017), providing trusted advice (Argento et al., Citation2019) and trusted websites (Damen & Buyst, Citation2017; Nicholson et al., Citation2019), thereby contributing to the theories of uncertainty reduction and consumer empowerment.

This study examined two related research objectives: 1) the antecedents of customer satisfaction and purchase intent in mortgages and 2) the mechanism of perceived risk reduction. To address the objectives, a conceptual model based on the uncertainty reduction theory and customer empowerment theory was developed (Hu & Krishen, Citation2019; Santos & Gonçalves, Citation2019). A detailed evaluation of the results follows.

The first hypothesis (H1), proposing that higher product complexity positively affects perceived risk, is supported. This result is consistent with prior studies (Linciano et al., Citation2018; Perry & Lee, Citation2012; Van Raaij, Citation2016) highlighting customer confusion and cognitive challenges when buying mortgages. The large effect size reiterates that mortgage buyers need financial education or counseling to lower risk perception (Argento et al., Citation2019; Xiao & Porto, Citation2017). This result supports the view that customers are overwhelmed by the complex attributes to consider when purchasing mortgages. Customers may be confused and unable to evaluate options clearly, leading them to perceive high levels of risk.

The second hypothesis (H2a and H2b) proposed that perceived risk positively affects perceived search benefits and internet sources. H2a is not supported, and customers with high perceived risk appear to emphasize seeking mortgage information negatively. Jacoby et al. (Citation1974) emphasized that in complicated product markets like mortgages, new customers are reluctant to invest time or cognitive effort in gathering information, and the results confirm this view. The results support H2b that customers with a high perceived risk visit more websites (Hu & Krishen, Citation2019; Soto-Acosta et al., Citation2014). There is an inconsistency in customer search behavior- higher objective search behavior and less subjective search intentions. This may be attributed to the “Google effect,” when users minimize their effort to enhance internal financial knowledge because of the presence of external information (Ward et al., Citation2022).

The third hypothesis (H3) proposes that higher perceived risk positively influences involvement and is not supported. This finding contradicts certain previous studies (Dholakia, Citation1997; Michaelidou & Dibb, Citation2008; Seabra et al., Citation2014) but aligns with Bettman et al. (Citation2008), who believe first-time purchasers underestimate risk. The underestimation diminishes involvement in the purchase decision. Low housing and mortgage insurance penetration (1%) in India shows customers’ disregard for risk (Khanna, Citation2017; Tiwari, Citation2001). Instead of managing risk cognitively, consistent with Bauer (Citation2001), customers may emotionally manage perceived risk by making hasty choices to escape the traumatic experience (Bauer, Citation2001; Bettman et al., Citation2008; Conchar et al., Citation2004). Consistent with prospect theory, research by Markett et al. (Citation2016) and Mellers et al. (Citation2021) has shown that loss aversion can cause customers to experience emotional pain, and the fear of the consequences of a poorly purchased mortgage can further increase consumer anxiety. McKinsey & Company finds that mortgage customers rate reassurance as the most important factor in the mortgage buying process (Bhattacharya et al., Citation2021).

The fourth hypothesis (H4) proposes that higher perceived search behavior positively influences the number of Internet sources used. The hypothesis is rejected, and there is no relationship as proposed in existing literature (Srinivasan & Ratchford, Citation1991). The results support the view that customers interested in searching for mortgage information seek sources other than the Internet. Prior studies highlight the importance of gathering mortgage information from professionals—real estate agents, bank employees (Devlin, Citation2002), family, and friends (Lee & Hogarth, Citation2000). The complex nature of mortgages forces customers to seek trustworthy or professional information sources. The personalized nature of interactions with experts or trusted family and friends may play a more significant role in enhancing mortgage knowledge than the impersonal Internet. Deloitte (Citation2016) emphasizes how customers use mortgage agents as “navigators” through the mortgage buying process.

The fifth hypothesis (H5a and H5b) proposed that higher perceived search benefits and the number of internet sources positively influence customer knowledge. While perceived search benefits significantly influence knowledge, increasing internet source usage does not result in increased knowledge. These findings support the view that information, instead of empowering customers, must be overloading them—exposure to internet sources did not convert into adequate knowledge. Customers’ knowledge seems to expand as they search from multiple sources- bank, real estate, and family sources. This result fits into the quantity-quality debate of consumer information (Fürstenau et al., Citation2016; Yoo et al., Citation2019), where the quality of the information is superior to the quantity/number of sources consulted. This finding shows that banks and regulators should prioritize providing customers with quality information over quantity (Nicholson et al., Citation2019). There continues to exist a trust gap between customers and financial service providers (Sapienza & Zingales, Citation2021). In this context, mortgage providers can increase trust and confidence by providing quality information to reduce customers’ perceived risk. Further, well-informed customers would make on-time payments and pose fewer compliance risks for banks.

The sixth hypothesis (H6), proposing that higher involvement positively influences customer mortgage knowledge, is supported. This result confirms that involved customers are more knowledgeable (Celsi & Olson, Citation1988). This is due to increased elaboration because of the exertion of cognitive resources and willingness to attend to market information (Celsi & Olson, Citation1988; Petty & Cacioppo, Citation1986). As predicted by uncertainty reduction theory, higher involvement leads to higher customer knowledge. Highly involved customers pay focused attention to the information presented, thereby enhancing their knowledge of mortgages (Amarasinghe Arachchige et al., Citation2022). Further, by interacting closely with mortgage personnel, involved customers can gather more details about the features and process of mortgage loans than less involved customers.

The seventh hypothesis (H7) proposes that higher customer knowledge positively influences customer satisfaction and is supported (β = 0.105). These results suggest customer satisfaction results from mortgage knowledge, consistent with recent studies (Reddy & Thanigan, Citation2022). Customers with a more robust knowledge of mortgages may be able to negotiate favorable terms with mortgage providers while understanding the implications of those terms on their welfare. Contrarily, customers with less knowledge may be more vulnerable to predatory lending practices or may make decisions that are not in their best interest (Agarwal et al., Citation2014). Overall, having a good knowledge of mortgages would help customers to make better choices and to be more satisfied with the service they receive from their mortgage provider.

The eighth hypothesis (H8) proposes that higher customer satisfaction positively influences purchase intention and is supported (β = 0.753). These results align with recent studies on home buying satisfaction and purchase intention (Dash et al., Citation2021). When customers have a satisfying buying experience when purchasing a mortgage, they believe it is because of the mortgage provider’s competence and brand reputation. This leads customers to trust the brand and develop loyalty (Bhattacharya et al., Citation2021).

The authors examined the mediating relationships to gain insight into the underlying risk reduction mechanism. The authors find that perceived search benefits and involvement competitively mediate perceived risk. This suggests that higher perceived search benefits and involvement suppress perceived risk (Zhao et al., Citation2010). So, involvement and perceived search benefits are the parallel mediators of perceived risk and knowledge. The outcome of the parallel mediation test foregrounds the various approaches to help households reduce their perceived risk. These findings suggest that perceived risk reduces when customers are involved in the purchase decision. Mortgage counseling is an excellent approach to increasing purchase decision involvement (Argento et al., Citation2019). Also, increasing customers’ perception of search benefits can reduce customer perceived risk. This is consistent with Singh and Jang (Citation2022), who show that each information channel has associated search benefits that enhance customer purchase intention and satisfaction. This is consistent with the conceptualizations of both the uncertainty reduction theory and customer empowerment theory, which offer complementary and parallel theoretical explanations of the process of risk reduction by customers.

6. Contributions, Limitations, and Conclusion

6.1. Theoretical contributions

Using the theoretical lens of consumer empowerment (Hu & Krishen, Citation2019) and uncertainty reduction (Knobloch, Citation2015; Kramer, Citation1999; Santos & Gonçalves, Citation2019), the present study examines the mechanism of consumer risk reduction and satisfaction enhancement during mortgage buying. The study makes three contributions to the literature. First, by examining the parallel mediating effects of involvement, perceived search benefits, and the number of internet sources, this study integrates the information search literature presented in customer empowerment theory and uncertainty reduction theory (Hu & Krishen, Citation2019; Santos & Gonçalves, Citation2019). While Hu and Krishen (Citation2019) employed involvement as the only mediator, the current work investigates three mediators. By assessing the effect of three mediating variables in parallel, this study provides a robust profile of the underlying mechanisms of risk reductions in mortgage purchases. Second, it enumerates the role of knowledge in increasing satisfaction and purchase intent and is consistent with recent studies highlighting the importance of assessing consumer satisfaction (Dash et al., Citation2021; Hu & Krishen, Citation2019; Reddy & Thanigan, Citation2022; Xiao & Porto, Citation2017). Third, the antecedents of consumer knowledge, including the influence of customer involvement and search, are presented (Celsi & Olson, Citation1988; Damen & Buyst, Citation2017; Petty & Cacioppo, Citation1986; Woodward & Hall, Citation2012).

6.2. Managerial and policy implications

This study highlights the critical components of reducing perceived risk and increasing purchase intent from an applied perspective. Most mortgage company managers want to boost customer satisfaction and purchase intent. The results imply that customers who decide based on adequate information and knowledge are more inclined to have a strong and satisfying relationship with the lender and are less likely to refinance with a competitor (Reddy & Thanigan, Citation2022). The findings imply that a higher level of knowledge results from greater customer involvement and search intent. To encourage engagement, mortgage companies should require their customers to spend more time with the mortgage advisor.

These findings have two important implications for Indian policymakers and mortgage companies. First, as the Indian mortgage market is poised for higher growth due to younger customers entering the market, policymakers could nudge mortgage companies to provide higher information disclosures to customers (Nicholson et al., Citation2019). Better disclosures could be accomplished through detailed mortgage comparison charts (Nicholson et al., Citation2019) or by presenting essential loan information in an easily understandable format (Lacko & Pappalardo, Citation2010; Musa et al., Citation2021). Secondly, mortgage companies could provide customers with brochures and easily navigable, interactive webpages that aid mortgage research and knowledge gain. This would increase customer satisfaction by boosting confidence in the mortgage company.

With relevant knowledge, consumers make informed decisions, claims the consumer empowerment theory. However, the study finds that more information improves customer decision-making only if customers actively search for it. Basic financial knowledge is inadequate for customers to comprehend risky products like mortgages (van Ooijen & van Rooij, Citation2016). So, mortgage-related information must be provided in a straightforward manner for customers to comprehend (Nicholson et al., Citation2019). Mortgages are not one-size-fits-all; therefore, policymakers should encourage buyers to shop around (Damen & Buyst, Citation2017).

6.3. Limitations and scope of future work

While this study examines the antecedents of customer purchase intention and the mechanism of risk reduction in mortgage purchase, there are several exciting streams that future work could unravel. The potential bi-directionality of the perceived risk-involvement relationship can be explored. While the present study follows the lead of Laurent and Kapferer (Citation1985), other directions provided by Dholakia (Citation2001) can be examined. Emotional responses to perceived risk might be examined. Perceived risk induces anxiety, and examining anxiety could offer alternative explanations of risk reduction, as sometimes emotional regulation may be more important than cognitive approaches (Bettman et al., Citation2008). Academics could study the relationship between search and knowledge acquisition, especially the “Google effect” (Ward et al., Citation2022). As customers replace internal memory with internet sources, the “Google effect” offers exciting avenues. Ethnomethodological approaches could study consumer knowledge as embodied knowledge (Llewellyn et al., Citation2021). Studies could focus on how frontline mortgage personnel assess consumer knowledge and aid in remedying the gaps (Llewellyn et al., Citation2021).

Further, researchers can use experimental studies to examine the temporal sequence of causation between the variables such as involvement and knowledge or knowledge and satisfaction and purchase intent. The mediating mechanisms showcased in this study apply to the mortgage context. Examining these mediators in the context of other financial products such as equity, FinTech products, or other loan products would provide a more comprehensive validation of the current study.

Finally, a key limitation of this Indian study is its generalizability to other countries. The findings and conclusions may not apply to different economic, demographic or social contexts, limiting the study`s external validity. In 2022, India’s mortgage debt to GDP ratio was only 14.3%, significantly lower than that of advanced economies. Researchers in advanced economies could conduct further investigations to explore the applicability of the factors identified by the authors.

7. Conclusions

The study reveals the outcomes of an analysis of mortgage consumer decision-making, focusing on purchase intent, satisfaction, and perceived risk. The results confirm that satisfaction with the mortgage process positively influenced purchase intention. Customers who are satisfied with the buying process have developed a positive attitude towards the home loan provider based on the positive experience and are more willing to buy from the same provider. Therefore, it is crucial for mortgage providers to strive to enhance customer satisfaction and to monitor and improve it to drive purchase intent continuously. Second, customers with a stronger knowledge of mortgages were more satisfied with their mortgage provider. This could be because knowledgeable customers can make informed decisions about the type of mortgage and lender that best suits their needs. In addition, better-informed customers are more likely to negotiate favorable terms with their mortgage provider and understand the implications of those terms. Third, customers with high product complexity assessed mortgage purchase risk as high. Mortgages are complex products with several characteristics difficult for customers to understand. Product complexity impairs the customer’s ability to understand and develop product expertise, thereby increasing perceived risk. As such, mortgage providers must provide clear and detailed information about their products to make it easier for customers to understand mortgages, which can help reduce the perceived risk associated with the purchase. Finally, the present study establishes the parallel mediation effect of information search and purchase decision involvement on the relationship between perceived risk and knowledge to identify the mechanism for risk reduction and knowledge augmentation. By understanding how information search and purchase decision involvement impact perceived risk and knowledge, this study provides insights into effectively reducing perceived risk and increasing customer knowledge. This can lead to more informed purchasing decisions and greater consumer satisfaction.

Theoretically, the present paper has implications for extending existing consumer information process theories. The authors integrate the Customer Empowerment Theory (CET), which articulates how customers cope with cognitive overload, with Uncertainty Reduction Theory (URT), which addresses the role of involvement and information search in knowledge enhancement. This new and integrated model provides evidence about the process of consumer knowledge enhancement and risk reduction while purchasing mortgages.

In management and policy terms, the findings of this study also have implications for mortgage providers and regulators. Research in behavioral finance articulates the need for policymakers to provide customers with the right nudges or carefully chosen defaults (Thaler & Sunstein, Citation2009). In the case of mortgages, nudges to customers to boost their search efforts might result in better contract terms for households. Also, providing selected “default options” in mortgage contracts based on demographic profiles may lower the risk for mortgage-buying customers (Sunstein, Citation2013, Citation2017).

Thereby, this study contributes to the continuing research on boosting consumer knowledge and satisfaction while reducing risk perceptions. As it is found that customer engagement and information search act in tandem to lower perceived risk and increase customer knowledge (Hu & Krishen, Citation2019; Knobloch, Citation2015; Lu & Chen, Citation2021), this study focuses on the mechanism through which risk can be reduced by using marketing communication tactics.

Participant consent

The participants of this study did not give written consent for their data to be shared publicly, so due to the sensitive nature of the research, supporting data is not available.

Disclosure statement