Abstract

This study aims to examine the role of digitalization in management accounting systems (DIMAS) in increasing the effectiveness of management decision-making in urban small and medium enterprises (SMEs) in a developing economy. This study also investigates the mediating role of information quality (accuracy and timeliness) and cost reduction in the relationship between DIMAS and management decision-making. This research employed primary data collected from questionnaire responses from 536 urban SMEs that implemented digitalization in a developing economy setting. The results show that DIMAS has a positive effect on the accuracy and timeliness of accounting information and cost reduction, which in turn contribute to better decision-making. The results of the mediation test reveal that the accuracy and timeliness of accounting information and cost reduction mediate the relationship between DIMAS and management decision-making. The findings of this study provide empirical evidence on the importance of digitalization for urban SMEs operating in a developing country, enabling them to survive and achieve a competitive advantage in an era of high uncertainty due to the industry 4.0 and the COVID-19 pandemic.

1. Introduction

Small and medium-sized enterprises (SMEs) have emerged as the backbone of many national economies, significantly contributing to job creation and income generation, particularly in developing nations (Al-Hattami et al., Citation2022b; Azudin & Mansor, Citation2018; Kuttner et al., Citation2022). Within the Indonesian context, SMEs have assumed critical roles in the national economy, including workforce employment, business expansion, and contribution to the national Gross Domestic Product (GDP) (Mahliza et al., Citation2017). As per the ASEAN Investment Report published in October 2022, Indonesia boasts the highest number of SMEs in the Association of Southeast Asian Nations (ASEAN) region, with 65.46 million entities. In 2021, these Indonesian SMEs managed to employ 97.0% of the country’s workforce and contributed 60.3% and 14.4% to the GDP and national exports, respectively (ASEAN Secretariat, Citation2022). In contrast, SMEs in other ASEAN countries employ between 35% and 85% of the national workforce. Notwithstanding, the GDP contribution of Indonesian SMEs lags behind that of Myanmar, where SMEs contribute as much as 69.3% to the local GDP. Likewise, in terms of export contributions, Indonesian SMEs trail behind their counterparts in Singapore (38.3%), Thailand (28.7%), Myanmar (23.7%), and Vietnam (18.7%) (ASEAN Secretariat, Citation2022). Consequently, the Indonesian government is actively promoting strategies to enhance the performance of the country’s SMEs, with one initiative being the digitalization of 30 million SMEs by 2024.

Empowerment of SMEs is a strategic imperative, given its potential to stimulate the economies of developing countries across several dimensions, including the number of business units, workforce absorption, and contribution to GDP and exports. However, SMEs often encounter development constraints owing to relatively small capital and limited resources in areas such as financing, technology, skilled labor, market access, and market information (Yoshino & Taghizadeh-Hesary, Citation2016).

Particularly in developing countries, SMEs face threats to their sustainability due to rapid changes in the external environment, including the emergence of industry 4.0 and the COVID-19 pandemic. These shifts necessitate SMEs to adapt and evolve to meet novel challenges in a sustainable manner (Al-Hattami et al., Citation2022; Ghobakhloo et al., Citation2022; Thuan et al., Citation2022). Consequently, the deployment of accurate and timely financial information to enhance strategic decision-making processes within SME management has become increasingly vital.

Industry 4.0 is a technological paradigm shift, signifying a digital revolution underpinned by advancements such as the internet of things (Ghobakhloo et al., Citation2022; Kipper et al., Citation2020). These developments could offer businesses benefits such as heightened productivity, operational efficiency, and a broader market reach. However, not all businesses, particularly SMEs, are capable of aligning their business models with the emerging Industry 4.0 paradigm. Horvath and Szabo (Citation2019) illustrate that the level of digitalization in industry 4.0 remains relatively low for SMEs, both in developed and developing countries. SMEs lag significantly behind larger corporations in terms of digital transformation, thereby leading to potential vulnerabilities and crises (Al-Hattami et al., Citation2021b; Ghobakhloo et al., Citation2022).

The COVID-19 pandemic has also introduced a dramatic rise in uncertainty for SMEs (Ghobakhloo et al., Citation2022; Tawfik et al., Citation2022; Thuan et al., Citation2022). This global health crisis has impacted businesses by drastically reducing productivity and economic growth (Al-Maliki et al., Citation2022; Almaqtari et al., Citation2023; Tawfik et al., Citation2022). The pandemic has also catalyzed digital transformation, as social distancing measures have boosted the prominence of online businesses and e-commerce across all sectors, including SMEs (Thuan et al., Citation2022). Concurrently, these circumstances have prompted businesses to upgrade their technological infrastructures, including management accounting systems (MAS) (Kumarasinghe & Haleem, Citation2020). This crisis environment fosters incentives for businesses to cultivate cognitive mechanisms and action plans, inclusive of information technology governance, to mitigate uncertainty and ensure business continuity (Almaqtari et al., Citation2023; Packard et al., Citation2017; Tawfik et al., Citation2022).

Accounting plays a crucial role in supporting management decision-making processes by recording, processing, and presenting pertinent business information. The proliferation of computers and the rapid evolution of information technology have enhanced the efficacy of accounting as a decision-making instrument (Al-Hattami, Citation2022a; Tawfik et al., Citation2022). However, the decision-making and control activities of SMEs are frequently not buttressed by relevant accounting information. Despite the escalating need for accounting information for SMEs’ management decision-making, its application is less prevalent in SMEs than in larger corporations (Kuttner et al., Citation2022; Lavia Lopez & Hiebl, Citation2015). SMEs often face difficulties in implementing a robust accounting system due to constrained financial and human resources (Kuttner et al., Citation2022; Mitter et al., Citation2022). Nevertheless, the promotion of MAS as a decision-support tool for SMEs is imperative to enhance their competitiveness amid the challenging environment precipitated by industry 4.0 and COVID-19 (Al-Hattami & Kabra, Citation2022; Almaqtari et al., Citation2023).

Our study contends that SMEs, particularly those operating in competitive urban markets, are especially susceptible to macro-level business disruptions such as industry 4.0 and the COVID-19 pandemic. SMEs could adopt digitalization in management accounting systems (DIMAS) to sustain business continuity and mitigate the adverse impacts of such disruptions. Our research seeks to explore the roles of DIMAS in facilitating the managerial decision-making process within urban SMEs operating in a developing country context. Against this backdrop, our study proposes the following research questions: (1) To what extent does DIMAS influence the quality characteristics of accounting information (specifically, accuracy and timeliness)? (2) To what extent does DIMAS contribute to cost reduction? (3) Do the quality characteristics of accounting information (accuracy and timeliness) and cost reduction mediate the effect of DIMAS on decision-making effectiveness?

Although a substantial body of research exists on accounting information systems for SMEs (Al-Hattami, Citation2022a; Al-Hattami et al., Citation2022; Almaqtari et al., Citation2023; Ghobakhloo et al., Citation2022; Tawfik et al., Citation2022; Thuan et al., Citation2022), investigations into the effectiveness of MAS for decision-making within SMEs operating in urban markets of developing economies, particularly in light of the implications of industry 4.0 and Covid-19, remain sparse. Our research aims to fill this research gap by examining the role of DIMAS in supporting managerial decision-making processes within these urban SMEs. Our study incorporates accounting information quality attributes—accuracy, timeliness, and cost reduction effectiveness—as potential mediating variables in this analysis.

This research contributes to the managerial accounting literature by exploring the role of DIMAS in the context of SMEs, entities that are highly susceptible to external factors such as the disruption caused by industry 4.0 and the COVID-19 pandemic (Al-Hattami et al., Citation2022; Kuttner et al., Citation2022; Thuan et al., Citation2022). These external events have intensified the vulnerabilities of SMEs due to their limited resources (Kuttner et al., Citation2022). As Accounting Information Systems (AIS) become increasingly crucial for SMEs in developing countries (Al-Hattami et al., Citation2022; Thuan et al., Citation2022), the digitized accounting information provided by DIMAS can play a pivotal role in mitigating crises, potentially enabling SMEs to execute strategic turnarounds, thereby increasing their survival rates. Further empirical evidence highlights the effectiveness of AIS digitalization in the era of industry 4.0 and Covid-19, in enhancing competitive advantage, augmenting productivity, and achieving time and cost savings (Al-Hattami et al., Citation2022). Previous research has primarily focused on the direct relationship between accounting systems and the effectiveness of decision-making (e.g., Al-Hattami & Kabra, Citation2022; Al-Hattami et al., Citation2022b; Thuan et al., Citation2022). This study aims to analyze the influence of information quality attributes in mediating the relationship between DIMAS and decision-making.

2. Literature review

2.1. Accounting information system (AIS) and digitalization in management accounting systems (DIMAS)

Management accounting plays a crucial role in facilitating effective decision-making (Harvey, Citation2007; Kumarasinghe & Haleem, Citation2020). An Accounting Information System (AIS) can be conceptualized as a specialized software application and managerial process, primarily designed to process data and supply both financial and non-financial information requisite for informed decision-making within a company (Al-Hattami et al., Citation2021a,; Al-Hattami et al., Citation2022b; Trigo et al., Citation2014). Laudon and Laudon (Citation2020) define AIS as “an interconnected assembly of components that collect (or retrieve), process, store, and disseminate information to facilitate decision-making and control in an organization.” The core components of AIS encompass hardware, software, personnel, procedures, and data. This system contributes to operationalizing and automating financial activities and generating data. AIS is the lifeline of an organization; without it, corporate activities cannot be planned, coordinated, or controlled effectively (Al-Hattami et al., Citation2021b,; Al-Hattami et al., Citation2022b; Kumarasinghe & Haleem, Citation2020; Sarwar et al., Citation2021).

The quality of AIS pertains to the system’s ability to perform the required tasks, which is judged from both technical and design perspectives (Knauer et al., Citation2020). Automation is a defining feature of AIS, thereby serving as a critical indicator of its quality (Al-Hattami & Kabra, Citation2022; Knauer et al., Citation2020). A system can be deemed automated if it performs functions or tasks that were previously executed—either partially or fully—manually, enabling data to be stored, retrieved, processed, and distributed without user intervention (Knauer et al., Citation2020). The digitalization of the management accounting system can support automation that increased operational speed, reduced errors, simplified operations, and ensured consistency. These improvements collectively enhanced the quality of AIS in supporting managerial decision-making.

Digitalization is defined as “the use of digital technologies to alter a business model and provide new revenue and value-producing opportunities; it is the process of transitioning to a digital business” (Gartner, Citation2022). Digitalization can establish and manage accounting systems at a reduced cost with advanced technological infrastructure. This evolution suggests that traditional accounting procedures, such as paper records, receipts, registration, and worksheets, will become obsolete. Digitalization offers a myriad of benefits to management in their accounting endeavors, ranging from enhanced quality, efficiency, speed, improved decision-making, and value-added potentials to newly available resources (Heimel & Müller, Citation2019). Several domains of management accounting may be influenced by digitalization, including reporting, strategy implementation and control, financial planning and analysis, competencies, roles, and organizational structure (Möller et al., Citation2020). The digitalization of management accounting has a tangible impact on how companies conduct their operations, particularly with the advent of the internet, mobile technologies, and digital economy tools (Bhimani, Citation2020; Kumarasinghe & Haleem, Citation2020).

Even though digitalization—including its implications for management accounting—has significant practical relevance, academic research on the subject remains scant (Möller et al., Citation2020). The gap between management accounting theory and practice is widening, as many entities have transitioned digitally in practice, yet empirical evidence on the effectiveness of digitalization in management accounting and control is still limited in literature (Bhimani, Citation2020; Möller et al., Citation2020).

SMEs need to undertake organizational changes in the face of digital transformation to secure their survival, sustainability, and public value creation (Almaqtari et al., Citation2023; Pham & Vu, Citation2022). Given that accounting information is used for decision-making and to reduce uncertainty (Pham & Vu, Citation2022), a management accounting system (MAS) could potentially be one of the business’ competitive advantages in the current climate. Digitalization in accounting information can be described as the method of implementing online and digital information into a company’s MAS for efficient and effective decision-making (Alnajjar, Citation2017; Pham & Vu, Citation2022). With these modern information-technology attributes, DIMAS can act as an enabler for creating, acquiring, and analyzing accounting data for value generation. The quality of accounting information is assessed by its ability to meet managers’ needs to enhance their understanding of the organizational and situational context, assist in decision-making, and monitor strategy implementation.

The implementation of DIMAS is one of the best solutions for the sustainable development of SMEs (Pham & Vu, Citation2022). DIMAS is an advanced form of AIS that includes automation, internet connectivity, big data, paperless processes, data analytics, and artificial intelligence (Mezghani & Aloulou, Citation2019; Pham & Vu, Citation2022). DIMAS makes the preparation of accounts more efficient, effective, and timely—while reducing errors—and it provides access to more detailed and updated information (Ghobakhloo et al., Citation2022). In practice, the implementation of DIMAS such as extended business reports and database management systems could be considered as the application of Industry 4.0.

2.2. SMEs in Indonesia

The SME sector plays a pivotal role in Indonesia’s economic development. The majority of the Indonesian population has a relatively low level of education, limited economic resources, and a standard of living below the average, which influences the national business sectors (Nuari, Citation2017). As per Government Regulation No.7 of 2021 concerning the Ease, Protection, and Empowerment of Cooperatives and Micro, Small, and Medium Enterprises, the SME classification is based on the size of the business’ assets and annual sales. A business entity is categorized as a small enterprise if the size of its assets is between IDR 1 billion and IDR 5 billion, excluding land and buildings, and its annual sales is between IDR 2 billion and IDR 15 billion. An entity is classified as a medium enterprise if the size of its assets is between IDR 5 billion and IDR 10 billion, excluding land and buildings, and its annual sales is between IDR 15 billion and IDR 50 billion.

The escalating business competition in Indonesia drives SMEs to enhance their performance by fostering innovation and professionalism in their operations (Pudyastuti & Saputra, Citation2021). According to the ASEAN Investment Report of 2022, the performance of Indonesian SMEs is relatively weak compared to other ASEAN countries (ASEAN Secretariat, Citation2022). As a response, the Indonesian government is urging SMEs to incorporate digitalization into their business operations (Ministry of Finance, Citation2022). The growth and development of SMEs necessitate a comprehensive and ecosystem-wide approach, encompassing six main aspects: policy, finance accessibility, market exposure, human resource capacity, mentorship, and culture. Digitalization serves as a crucial catalyst in integrating these aspects, thus accelerating the advancement of SME development programs (Ministry of Finance, Citation2022). Indonesia’s Minister of Finance, Sri Mulyani, stated that the development of the SME ecosystem and its digitalization requires a more significant private sector involvement. This involvement can take various forms, including fintech, crowdfunding, and e-commerce, which can support fledgling SMEs, expand business networks, and attract more investments (Ministry of Finance, Citation2022).

2.3. Diffusion of innovation (DOI) theory

The Diffusion of innovation (DOI) theory explains how an idea or product gains momentum and diffuses through specific social groups or systems (Rogers, Citation2010). It centers around the adoption of new ideas, behaviors, or products, highlighting the importance of treating these elements as innovations, which can be comprehended through four stages: discovery, dissemination through social systems, development, and consideration of consequences (Oirere, Citation2015).

Innovation development can manifest in various domains, such as knowledge, systems, practices, and corporate decision-making (Ndubuisi et al., Citation2017). When a company implements a new system, including digitalization, this system itself can be perceived as an innovation as it supersedes an antiquated system. Innovation is the manifestation of ideas or practices deemed new, while diffusion represents the process of communicating innovation within a social system.

Consequently, digitalization symbolizes an innovation in accounting, which can be challenging to manage and guide owing to its unstructured institutional character, extensive scope, and extended lifetime (Akande, Citation2021). In our study, digitalization is considered an independent (exogenous) variable that proxies accounting innovation. Prior literature posits that the digitalization of accounting information systems epitomizes a form of innovation that can be explained by the DOI theory (Akande, Citation2021; Kumarasinghe & Haleem, Citation2020; Thuan et al., Citation2022).

3. Research model and hypotheses development

3.1. Research model

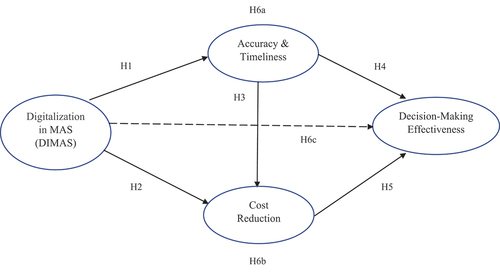

Previous research exploring the role of management accounting systems (MAS) in aiding decision-making predominantly focused on large and well-established companies (Bisbe & Malague~no, Citation2009; Kuttner et al., Citation2022; Pedroso & Gomes, Citation2020). Nonetheless, recent discourse in accounting literature has advocated for future research to probe the role of MAS and the information it provides in bolstering decision-making effectiveness within the context of SMEs (Azudin & Mansor, Citation2018; Kuttner et al., Citation2022; Pedroso & Gomes, Citation2020; Pelz, Citation2019; Sandalgaard & Nielsen, Citation2018). The present application of MAS has profited from technological advancements, which have led to increased efficiency and the availability of timely, reliable information that can guide managers in making successful decisions (Thuan et al., Citation2022). Considering the limitations of SMEs and their struggle to compete amidst the COVID-19 pandemic and Industry 4.0, the question of whether MAS can be effectively deployed by SMEs as a decision-support system warrants crucial research attention. Figure presents the research model, which is grounded in the Diffusion of Innovations theory.

Figure 1. Research model.

In this study, Digitalization in Management Accounting Systems (DIMAS) functions as an independent/exogenous variable, while attributes of accounting information quality (accuracy and timeliness) and cost reduction act as mediating variables, and decision-making effectiveness serves as a dependent/endogenous variable. The argument posited here is that DIMAS cannot directly influence decision-making effectiveness; it must instead proceed through accuracy-timeliness and cost reduction. Seventeen indicators are utilized to measure the four variables illustrated in Figure . A comprehensive explanation of the measurements and definitions of these indicators is provided in Section 4.2 and Appendix 1.

3.2. Hypotheses development

3.2.1. The relationship between digitalization in MAS (DIMAS) and accuracy-timeliness

Drawing upon the diffusion of innovation theory, digitalization could enhance company performance by augmenting the quality of information, thereby facilitating more effective managerial decision-making. For instance, Accounting Information Systems (AIS) can provide swift, integrated, secure, and effective solutions for SMEs management in planning and decision-making processes (Al-Hattami & Kabra, Citation2022; Al-Hattami et al., Citation2021b; Kumarasinghe & Haleem, Citation2020). Technology-based accounting systems, such as DIMAS, can bolster SMEs’ resilience in the current Industry 4.0 and COVID-19 environment, which is marked by volatility, uncertainty, complexity, and ambiguity (Almaqtari et al., Citation2023). Technological advancements have enabled feasible online reporting, thus simplifying access to and use of financial information for management.

This study concentrates on two key attributes of accounting information: timeliness and accuracy. Timeliness, a vital characteristic of MAS quality, indicates management’s commitment to acquiring information regularly and promptly (Pedroso & Gomes, Citation2020). Accuracy, on the other hand, reflects the extent to which the stated value in the accounting records mirrors all supporting facts (Al-Hattami et al., Citation2021a; Alsufy, Citation2019). A computerized accounting system can deliver reliable and precise information for decision-making (Alsufy, Citation2019). Accounting information, when processed and reported promptly, can significantly aid management’s decision-making process. Digitalization can automate the collection, processing, and provision of accounting information, reducing errors and thereby ensuring the quality criteria of accuracy and timeliness are met (Kumarasinghe & Haleem, Citation2020; Pedroso & Gomes, Citation2020).

Several reasons suggest that DIMAS can improve timeliness and accuracy. First, DIMAS aids in automating financial reports and information processing. Second, it can rapidly consolidate information between units and subunits, contributing to the automation of financial report production. Third, by leveraging interactive data tagging, it automates the financial reporting processes. By eliminating the need for manual data processing from various documents, SMEs can reduce the human effort spent on collecting, calculating, reviewing, checking, and interpreting financial data. Automation of the financial reporting process can diminish the risk of human error, thereby enhancing accuracy and timeliness. Additionally, automation can limit opportunities for manipulation and fraud involving accounting numbers, thus increasing the reliability and relevance of financial reports (Kim et al., Citation2013; Wu & Vasarhelyi, Citation2004). Prior research has demonstrated that digitalization in financial reporting, in the form of the Extensible Business Reporting Language (XBRL), increases the efficiency and timeliness of financial reporting (Amin et al., Citation2018; Du & Wu, Citation2018; Weissmueller & Johnson, Citation2014; Yoon & Lee, Citation2011). Digitalization in financial reporting creates synergies between internal and external reporting, leading to shorter reporting lags and more transparent financial reporting (Amin et al., Citation2018; Hwang et al., Citation2020). Consequently, the first hypothesis in its alternative form is postulated as follows:

H1:

Digitalization in the management accounting system is positively associated with the characteristics of accounting information (accuracy and timeliness).

3.2.2. The relationship between digitalization in MAS (DIMAS) and cost reduction

From the perspective of the diffusion of innovation theory, digitalization in accounting systems can improve the efficiency of internal processes, primarily realized through cost reduction. Digitalization in accounting systems aids companies in resolving long-standing issues by providing information that supports operational integration and internal control within a competitive environment. Computer-based accounting systems also assist companies in generating and maintaining data beneficial for planning, evaluating, and analyzing their operational and financial processes (Bshayreh & Hamour, Citation2020). A digitized system can deliver detailed and precise budget calculations and cost information, enabling companies to budget, control, and assess company performance more effectively and efficiently (Bataineh, Citation2018). The use of a computer-based accounting system significantly contributes to the reduction of indirect industrial costs in companies in the Jordanian chemical industry (Bshayreh & Hamour, Citation2020). Digitalization in AIS notably aids in reducing operational costs, thereby contributing to a company’s competitive advantage (Al-Hattami et al., Citation2022; Thottoli, Citation2021). Hence, the second hypothesis in its alternative form is articulated as follows:

H2:

Digitalization in the management accounting system (DIMAS) is positively associated with cost reduction.

3.2.3. The relationship between accuracy-timeliness and cost reduction

Companies can perform analysis and make informed decisions regarding production costs using accurate and timely accounting information, which are two critical characteristics of accounting information (Al-Hattami, Citation2022a; Al-Hattami et al., Citation2021b). A digitalized accounting system can offer accurate and timely budget calculations and cost information, enabling companies to quickly conduct cost analysis and make optimal decisions to enhance cost efficiency (Bataineh, Citation2018). Bshayreh and Hamour (Citation2020) demonstrate that the use of accurate accounting information has significantly reduced indirect costs. Lawal et al. (Citation2022) indicate that an accurate and timely accounting information system can assist companies in reducing costs and human errors, simplifying operations, accelerating work, and boosting the productivity of the company’s workforce. Consequently, the third hypothesis in its alternative form is formulated as follows:

H3:

The characteristics of accounting information (accuracy and timeliness) are positively associated with cost reduction.

3.2.4. The relationship between accuracy-timeliness and the effectiveness of decision-making

Accounting information that is both accurate and timely is typically characterized as high quality (Al-Hattami, Citation2022a; Al-Hattami et al., Citation2021b,; Al-Hattami et al., Citation2022b; Shagari et al., Citation2017). Such high-quality accounting information aids management in accomplishing tasks efficiently and effectively (Al-Hattami et al., Citation2022b). Previous empirical studies indicate that high-quality accounting information can augment user utilization and satisfaction in decision-making (Al-Hattami et al., Citation2022b; Owusu et al., Citation2022). In the context of developing countries, it is crucial to motivate SME management to utilize high-quality accounting information in business decision-making. Accounting information enhances SMEs’ decision-making by providing a valuable information base that enables management to respond swiftly to internal (e.g., liquidity shortage) and external threats (Kumarasinghe & Haleem, Citation2020; Lavia Lopez & Hiebl, Citation2015). The rapidity of this response can be a significant factor in securing a competitive advantage. Accounting information can be employed to manage, coordinate, and control scarce resources to surmount resource constraints (Lavia Lopez & Hiebl, Citation2015).

Accuracy and timeliness, as two important characteristics of accounting information, aid management in making optimal business decisions. Information technology can deliver timely and reliable accounting information, thereby enabling employees of SMEs to work with greater efficiency (Thuan et al., Citation2022). Thus, the fourth hypothesis in its alternative form is proposed as follows:

H4:

The characteristics of accounting information (accuracy and timeliness) are positively associated with the effectiveness of decision-making.

3.2.5. The relationship between cost reduction and the effectiveness of decision-making

Decision-making is the process of identifying and selecting alternative courses of action that best suit the situation’s requirements. Effective decision-making is defined as the process of choosing an alternative that can be implemented to achieve business objectives. Effective decision-making requires precision and accurate strategies that will lead to success (Kumarasinghe & Haleem, Citation2020; Obi, Citation2017). SMEs management should be encouraged to employ high-quality accounting information in business decisions. When accounting information is effectively used to improve operational efficiency, management can realize cost reduction. Cost reduction activities aim to decrease production costs by eliminating ineffective expenses or those that should not be incurred, contributing to higher profits (Kumarasinghe & Haleem, Citation2020; Nikmatullah & Widarsono, Citation2014). Accordingly, the formulation of the fifth hypothesis in its alternative form is as follows:

H5:

Cost reduction is positively associated with the effectiveness of decision-making.

Based on the research model presented in Figure , this study hypothesizes that digitalization in the management accounting system (DIMAS) can enhance the effectiveness of decision-making through the quality attribute of accounting information, specifically accuracy-timeliness and cost reduction. These elements—accuracy-timeliness and cost reduction—serve as mediating variables. Mediating variables intervene or bridge the relationship between other variables (Hair et al., Citation2016). In this scenario, a change in the exogenous/independent variable (DIMAS) affects the mediating variables, which in turn affects the endogenous/dependent variable (effectiveness of decision-making). An analysis of the strength of the relationship between the mediating variables and other variables will support conclusions about the underlying mechanism or process that underpins the causal relationship between exogenous and endogenous variables (Hair et al., Citation2016).

The research model in Figure illustrates the generative mechanism by which DIMAS can boost the effectiveness of decision-making by SMEs management. DIMAS can produce high-quality (accurate and timely) accounting information that can serve as the foundation for cost reduction. These two attributes of high-quality information represent the necessary conditions for effective decision-making. Thus, this study proposes the sixth hypothesis that DIMAS is positively and indirectly associated with the effectiveness of decision-making through the two mediating variables (as indicated by the dotted line in Figure ). DIMAS can only effectively support SME management’s decision-making if it can enhance the accuracy-timeliness of accounting information. In the end, DIMAS provides accurate and timely cost information, which should positively correlate with more effective cost reduction and, in turn, more effective management decision-making. Therefore, three hypotheses on the mediating variables are presented in their alternative forms as:

H6a:

Digitalization in the management accounting system (DIMAS) is positively and indirectly associated with the effectiveness of decision-making through accuracy-timeliness.

H6b:

Digitalization in the management accounting system (DIMAS) is positively and indirectly associated with the effectiveness of decision-making through cost reduction.

H6c:

Digitalization in the management accounting system (DIMAS) is positively and indirectly associated with the effectiveness of decision-making through accuracy-timeliness and cost reduction.

4. Methods

4.1. Population and sample selection

This study examines the implementation of digitalization in management accounting systems (DIMAS) within SMEs in one of the largest developing country, Indonesia. Questionnaire surveys were conducted to a population of urban SMEs in Indonesia that have adopted DIMAS to improve the generalization of our study. We identified 653 urban SMEs that have implemented DIMAS in the country. The identification of SMEs that have implemented DIMAS was based on initial focus group discussions with government officials, preliminary contacts made via telephone, direct visits to the SMEs’ locations, and online inquiry. The relatively small number of urban SMEs have implemented digitalization in the accounting system, despite Indonesia having the highest number of SMEs, suggests that Indonesian SMEs’ digitalization efforts are still trailing behind those of other ASEAN countries (ASEAN Secretariat, Citation2022). Questionnaires were dispatched to the identified 653 SMEs and we received 536 usable responses; equating to an 82.08% response rate. The high response rate from the sampled population (over 80%) allows us to generalize our findings to the broader population of SMEs operating in urban areas within a developing country.

4.2. Variable measurement

This study utilizes 17 indicators divided into four variables relevant to the hypotheses: digitalization in the management accounting system (DIMAS), accuracy and timeliness, cost reduction, and decision-making effectiveness. Definitions of these indicators are provided in Appendix 1. All 17 indicators delineated in Appendix 1 are assessed using a five-point Likert scale (ranging from 1, indicating strong disagreement, to 5, indicating strong agreement).

The classification of the 17 indicators into the four variables derives from definitions used in previous studies. The DIMAS variable is gauged by four indicators adopted from earlier research (Amanamah et al., Citation2016; Pham & Vu, Citation2022; Thuan et al., Citation2022). The accuracy and timeliness variable is measured by three indicators applied by Al-Hattami (Citation2022b). The measurement of cost reduction uses five indicators borrowed from Taylor (Citation2016) and Tomic et al. (Citation2018). The decision-making effectiveness variable is gauged using five indicators used by Butterfield (Citation2016) and Al-Hattami (Citation2022a). The measurement methods for all variables used in the questionnaire survey are outlined in Appendix 1. Empirical support for the classification of these indicators is provided by the results of reliability and validity tests (Tables ).

4.3. Data analysis

This study employs the Structural Equation Model approach using the Partial Least Squares (PLS-SEM) method, calculated with the Warp PLS 8.0 software. The PLS method is utilized to examine the relationships between variables that are unobserved or latent, as measured by several indicators, within a relatively complex model comprising exogenous/independent, mediating/moderating, and endogenous/dependent variables (Hair et al., Citation2016; Kock, Citation2020; Nitzl, Citation2016). The complex model being tested, which includes numerous unobserved or latent variables and indirect effects, necessitates the use of PLS-SEM, as multiple regression approaches would be unsuitable (Hair et al., Citation2016). PLS-SEM presents several advantages: (1) it avoids identification issues with small sample sizes, (2) it generally achieves high levels of statistical power with small sample sizes, and (3) it makes no assumptions about data distributions (Hair et al., Citation2016). PLS-SEM operates efficiently with small sample sizes and complex models (Hair et al., Citation2016). PLS-SEM has also been utilized in various empirical studies of accounting information systems in SMEs (e.g., Al-Hattami et al., Citation2022b, Citation2022; Thuan et al., Citation2022).

By employing PLS, the results of hypothesis testing can be simultaneously obtained by minimizing measurement and structural errors (Hair et al., Citation2016; Nitzl, Citation2016). The PLS-SEM analysis was executed in two stages: (1) evaluation of the measurement model or outer model, which explicates the relationship between latent variables and their indicators, and (2) evaluation of the structural model or inner model, which explains the relationships between latent variables or constructs (Hair et al., Citation2016).

5. Results

5.1. Sample description and interview results

The questionnaire survey was conducted both physically—by directly visiting the SME locations—and virtually—by sending a Google Form link to the SMEs’ email addresses in 2023. The study’s respondents were the accountant, management, and owners of SMEs operating in Indonesia that have implemented digitalization in the management accounting system (DIMAS) in their business processes. The response rate for the distributed questionnaires in this study was 82.08%. Details of the questionnaire survey results are presented in Table .

Table 1. Questionnaire survey results

The minimum sample size for the number of respondents is determined by multiplying the number of indicators (n) by a number between 5 and 10 (Hair et al., Citation2016). Using this method, we calculated that the minimum sample size for this study is 85 respondents since 17 indicators (that is multiplied by 5) were employed in this study (refer to Appendix 1). The final sample size for this study is 536 observations, which exceeds the minimum 85 respondents threshold and is considered sufficient for multivariate analysis. As demonstrated in Table , the scale of SMEs in the sample was predominantly small businesses, accounting for 85.45% of respondents.

Table 2. Business scale of the respondents

The target respondents of this study were owners, managers, and accountants working within SMEs, as they are likely to possess a thorough understanding of the accounting information systems implemented by their respective businesses (Al-Hattami et al., Citation2022b, Citation2022; Thuan et al., Citation2022). Table presents the demographic profile of the 536 respondents. The majority of the respondents were female (58.58%), belonged to the productive age range of 31 to 50 years old (85.91%), hold undergraduate degrees (77.61%), had between 6 to 10 years of work experience (50.37%), and occupied managerial positions (57.46%).

Table 3. Demographic profile of the respondents

Unstructured interviews were conducted as an initial step to gather information about the application of digitalization in accounting within SMEs. These interviews served as a pilot test for the questionnaire instrument. According to the results of these interviews and questionnaire surveys, the implementation of DIMAS within SMEs primarily relies on software usage in the business process. The majority of respondents utilize custom-made software, representing 58.96% of the sample. These custom-made software solutions perform accounting functions tailored by programmers to meet the individual needs of SMEs. Respondents employing commercial accounting software comprise 41.04% of the sample. Table provides further details on the use of accounting software among the respondents.

Table 4. Details of respondents’ accounting software

In addition to the questionnaire survey, interviews were conducted with three managers of SMEs to gain preliminary insights into the implementation of DIMAS and its benefits for their businesses. All three interviewees reported that they utilized electronic data processing (EDP) software, an accounting recording system that processes transaction data using computer technology (Bodnar & Hopwood, Citation2006).

Mr. A, the first interviewee, noted that his company had been employing a computer-based accounting recording system for over a decade. He asserted that the use of such a system significantly aids in managing business finances and can enhance the company’s performance through administrative cost reductions. The second interviewee, Mrs. B, stated that her company had recently adopted a computer-based accounting recording system in 2019 due to an increase in online transactions within her SME. She stressed the continuous refinement of this digitalization to keep pace with rapid technological advancements and intense competition. Following the implementation of the computerized data recording system, Mrs. B’s company has been able to process data in a more structured, speedy, and accurate manner. The use of digitalization intensified during the COVID-19 pandemic from early 2020 to 2022. Mr. C, the third interviewee, argued that the digitalization of his current business processes was necessary due to the information technology environment, consumer expectations, and social restrictions imposed during the pandemic. He affirmed that the computer-based accounting system simplified the management of administration and finance. Mr. C also reported that his company realized the benefits of employing an accounting system, particularly when calculating inventory and preparing financial reports. He could obtain data more quickly, aiding decision-making and reducing labor costs.

5.2. Hypotheses testing results

The first stage of the PLS-SEM analysis aims to evaluate the measurement model to ensure that the criteria for construct reliability and validity are met (Hair et al., Citation2016; Kock, Citation2020). The results shown in Table confirm that construct reliability is met, with composite reliability and Cronbach’s alpha values within the acceptable range, exceeding 0.70 (Hair et al., Citation2016; Kock, Citation2020). The Average Variance Extracted (AVE) values in Table all exceed 0.50, indicating acceptable convergent validity.

Table 5. Reliability and validity test results

Table presents the results of the convergent validity analysis. The outcomes indicate that all the indicators used in this study (refer to Appendix 1) meet the loading factors criteria, which should be more than 0.70 and significant (p-values <0.01) (Hair et al., Citation2016). For instance, the indicator MAS4, one of the DIMAS measures, exhibits a high loading factor of 0.871 on other DIMAS latent variables and a low loading factor of 0.279 on the accuracy and timeliness latent variables. These values fulfill the discriminant validity criteria.

Table 6. Loading factors

Discriminant validity evaluation is also conducted by comparing the square root of AVE with the correlation between constructs (Hair et al., Citation2016; Kock, Citation2020; Nitzl, Citation2016). The results in Table confirm that the AVE square root in the diagonal column exceeds the correlation between constructs (figures in the same column), thereby meeting the discriminant validity criteria. We computed the predictive relevance indicators of this study on management accounting practice by calculating Q-squared (Table ) and effect size (Table ).

Table 7. Discriminant validity test results

Table 8. Model fit indices

Table 9. Path coefficients and p-values results

To assess the structural model, a goodness of fit analysis is performed. The results of the PLS-SEM model’s goodness of fit, presented in Table , demonstrate that all the criteria for the average path coefficient (APC), average R-square (ARS), and average adjusted R-square (AARS) have been fulfilled, implying that a causal analysis of the relationships could proceed (Kock, Citation2020). Moreover, the model doesn’t exhibit multicollinearity, meeting the average full collinearity variance inflation factor (AFVIF) criterion. Similarly, Tenenhaus GoF (GoF) and Statistical Suppression Ratio (SSR) are within acceptable limits, as shown in Table .

Following Hair et al. (Citation2016) suggestion, this study examines the Stone-Geisser’s Q2 value, indicative of the model’s out-of-sample predictive power or relevance. A PLS path model displaying high predictive relevance can precisely predict data not used in the model’s estimation (Hair et al., Citation2016). In the structural model, Q2 values larger than zero for a specific reflective endogenous latent variable indicate the path model’s predictive relevance for that dependent construct (Hair et al., Citation2016). The results from Table show that the Q2 values are 0.771, 0.648, and 0.689 for the accuracy and timeliness, cost reduction, and decision-making effectiveness variables, respectively. These values, being larger than zero, indicate this study’s predictive relevance on the effectiveness of DIMAS practice in improving decision-making effectiveness.

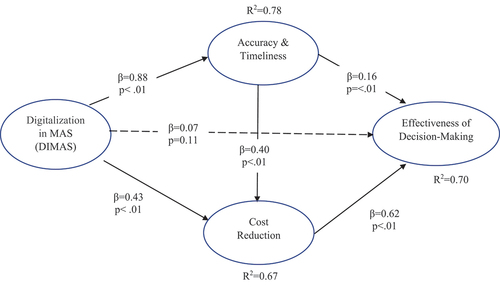

After the measurement model test results meet the statistical requirements, the structural model test is carried out to test the hypotheses. The results of the PLS-SEM structural model test are presented in Figure .

Figure 2. Results of the PLS-SEM structural model.

Table displays the path coefficient estimation results of the PLS-SEM structural model. As illustrated in Table , hypotheses H1 to H5 are supported. DIMAS positively impacts the accuracy and timeliness with a standardized coefficient of 0.885, statistically significant (p < 0.001), confirming H1. An improvement in DIMAS by one standard deviation contributes to a 0.885 increase in accuracy and timeliness. Likewise, the results support H2, as a one standard deviation increase in DIMAS can lead to a 0.431 increase in cost reduction (statistically significant with p < 0.001). The PLS-SEM results also support H3 with a standardized coefficient of 0.396, statistically significant (p < 0.001). These results support the argument that high-quality accounting information attributes (accuracy-timeliness and cost reduction) can enhance decision-making effectiveness by SMEs management. The mediating variable of accuracy and timeliness positively influences decision-making effectiveness with a standardized coefficient of 0.165, statistically significant (p < 0.001), indicating H4 is supported. The results also support H5, proposing that cost reduction positively impacts decision-making effectiveness (standardized coefficient is 0.623 and statistically significant at p < 0.001).

The study evaluates the effect size f2, enabling us to assess an independent/exogenous construct’s contribution to a dependent/endogenous latent variable’s R2 value. The results from Table indicate that the effect size of the DIMAS variable on accuracy-timeliness and cost reduction is 0.738 and 0.348, respectively. The f2 shows cutoff values of 0.02, 0.15, and 0.35, indicating that an exogenous construct has a small, medium, and large effect, respectively, on an endogenous construct (Hair et al., Citation2016). Based on these cutoff values, the DIMAS variable has a large and medium impact on two of the endogenous variables: accuracy-timeliness and cost reduction, respectively. The accuracy-timeliness and the cost reduction variables’ contribution to decision-making effectiveness is small and large effects, respectively. Overall, the effect size testing results show that the majority of independent variables exhibited in Table have medium and large effects in enhancing decision-making effectiveness.

Next, the study tests the mediation alternative hypotheses, namely H6a, H6b, and H6c. The following procedures to test the mediation hypotheses are carried out according to the PLS-SEM literature (Hair et al., Citation2016; Nitzl et al., Citation2016):

Testing the indirect effect a × b provides researchers with the information needed for testing mediation.

The strength of the indirect effect a × b determines the size of the mediation.

A bootstrap test is used to test the significance of the indirect effect a × b.

The results of the mediation hypotheses testing are presented in Table .

Table 10. Results of the mediation effect test

The mediation analysis is founded on the results of the standardized (direct and indirect effect) path coefficient significance test using the PLS-SEM bootstrapping procedure (Nitzl et al., Citation2016; Hair et al., Citation2016. The test results, presented in Table , indicate that the indirect effect of DIMAS on decision-making effectiveness through accuracy-timeliness is significant with an indirect effect path coefficient of 0.247 and a p-value of < 0.001. Consequently, the H6a is supported. Similarly, we support H6b, which reveals the indirect effect of DIMAS on decision-making effectiveness through cost reduction, which is statistically significant (indirect effect path coefficient of 0.350 and a p-value <0.001). The test results show that H6c is supported, indicating that DIMAS has an indirect effect through accuracy-timeliness and cost reduction (coefficient = 0.414, p-value <0.001). The results of the PLS-SEM test in Table Panel B show that the direct effect of DIMAS on decision-making effectiveness is not statistically significant with a path coefficient of 0.066 and a p-value of 0.106. This points to the full mediation role of the two quality of accounting information variables (accuracy-timeliness and cost reduction) in the relationship between DIMAS and decision-making effectiveness (Hair et al., Citation2016; Kock, Citation2020; Nitzl et al., Citation2016; Zhao et al., Citation2010). Thus, DIMAS can only enhance the decision-making effectiveness of SMEs management if it can improve accuracy-timeliness and cost reduction. There are no other mediating variables in the relationship between DIMAS and decision-making effectiveness.

6. Discussion of results

This study aims to examine the impact of the digitalization of management accounting systems (DIMAS) by SMEs management on the quality of accounting information and decision-making. The study’s results provide empirical evidence that supports the diffusions of innovations theory, arguing that innovation in DIMAS plays a crucial role in supporting SMEs’ managerial decision-making in a developing country (Al-Hattami, Citation2022a). The empirical evidence supports H1, indicating that the use of DIMAS positively affects the accuracy and timeliness of accounting information. This finding corroborates previous research, which suggests that digitalization can automate the process of collecting, processing, and providing accounting information, reducing errors and achieving quality criteria for accuracy and timeliness (Al-Hattami et al., Citation2021b; Almaqtari et al., Citation2023; Kumarasinghe & Haleem, Citation2020; Pedroso & Gomes, Citation2020).

The study’s empirical results also support H2, suggesting that DIMAS can provide detailed and accurate budget calculations and cost information, enabling companies to budget, control, and evaluate company performance more effectively and efficiently (Al-Hattami & Kabra, Citation2022; Bataineh, Citation2018; Kumarasinghe & Haleem, Citation2020).

The results also show that high-quality (accurate and timely) accounting information improves decision-making effectiveness. This empirical evidence emphasizes the essential role of high-quality accounting information in assisting SMEs management in efficiently and effectively completing tasks. The study’s empirical evidence also supports previous research findings, indicating that high-quality accounting information can provide a basis for SMEs management when making economic decisions (Al-Hattami et al., Citation2022b; Almaqtari et al., Citation2023; Lavia Lopez & Hiebl, Citation2015; Owusu et al., Citation2022; Thuan et al., Citation2022).

The mediation effect testing results, as conducted through PLS-SEM, demonstrate that DIMAS does not directly influence the effectiveness of decision-making. Rather, it must interact with two attribute variables of high-quality accounting information: accuracy and timeliness, along with cost reduction. This analysis provides empirical evidence that high-quality accounting information and cost reduction serve as full mediators in this relationship. Consequently, DIMAS can only effectively support decision-making processes in SME management by simultaneously enhancing the accuracy and timeliness of accounting information and facilitating cost reduction. This empirical evidence corroborates previous research advocating the significance of high-quality accounting information in improving SME management’s decision-making processes (Al-Hattami, Citation2022a; Al-Hattami & Kabra, Citation2022; Owusu et al., Citation2022). The implications of this study are paramount, especially within the current competitive landscape where SMEs strive for survival. DIMAS could be instrumental in achieving sustainable competitiveness (Almaqtari et al., Citation2023; Kumarasinghe & Haleem, Citation2020; Monteiro & Cepêda, Citation2021). DIMAS supports a decision-making process that yields swift, integrated, secure, and effective solutions, thereby fostering greater resilience among SMEs (Al-Matari et al., Citation2022; Almaqtari et al., Citation2023; Thuan et al., Citation2022).

7. Conclusions

7.1. Conclusion

The present study concludes that digitalization in the management accounting system (DIMAS) for SMEs can enhance information quality attributes (accuracy and timeliness) and promote cost reduction. Furthermore, these two mediating variables bolster the effectiveness of SME management’s decision-making processes. Our findings indicate that DIMAS can automate the procedure of financial statement preparation, consolidate reports across business units, and reduce the risk of human errors, thereby leading to improved accuracy and timeliness of accounting information.

Our results demonstrate that high-quality accounting information is utilized by management to enhance decision-making effectiveness and mitigate costs. We find that DIMAS does not directly support SMEs management’s decision-making. Rather, DIMAS can only augment effective decision-making through attributes of accounting information (accuracy and timeliness) and cost reduction. These two variables fully mediate the relationship between DIMAS and the effectiveness of SME management’s decision-making.

7.2. Implications (theory and practice)

This paper provides significant theoretical and practical implications. To the best of our knowledge, there is a lack of empirical studies investigating the impact of the digitalization of management accounting systems on effective decision-making for SMEs in a competitive urban business environment within a developing country. The empirical evidence from this study underscores the importance of digitalization for urban SMEs in enhancing the quality of accounting information and managerial decision-making in the face of business disruptions. Additionally, this study extends prior management accounting research by providing empirical evidence on the mediating role of accounting information quality.

In terms of practical implications, our findings should encourage urban SMEs, still reliant on manual management accounting systems, to transition towards digitalized systems. The empirical evidence from our study demonstrates that urban SMEs management can leverage DIMAS to obtain accurate and timely information for effective and efficient decision-making, thus minimizing the adverse effects of business disruptions. Government policymakers could utilize the findings of this study to provide support for SMEs operating in urban areas, enabling them to compete, sustain, and expand their business operations. Our study reveals that the adoption of digitalization for management accounting systems among urban SMEs is currently limited, primarily due to the substantial implementation cost. Presently, only SMEs with sufficient financial resources have embraced DIMAS and consequently reaped the benefits of digitalization. Therefore, without external support, the majority of urban SMEs in developing economies would have limited opportunities to adopt DIMAS and reap its benefits as outlined in this study. Hence, governments could support urban SMEs by incentivizing investments in DIMAS implementation, providing free software, subsidies, lines of credit, low-interest loans, tax relief, or training workshops for select SMEs showing high growth potential.

7.3. Limitation and future research

The results of this study might be influenced by personal bias and judgment error bias inherent in questionnaire survey research. We attempted to mitigate this bias by employing anonymous responses and reversing the order of the survey questions. Future research could expand the sample to other research settings, such as SMEs in developed economies or SMEs operating in rural areas. Future studies should also examine the digital transformation process for SMEs, as it involves more than mere technological change but also changes in the organization, its offerings, and its market engagement. Digital transformation is not just about technology but encompasses leadership, culture, organization, operations, and innovation (Armstrong & John Lee, Citation2021). Future research could also investigate the impact of digitalization on financial reports prepared according to SME accounting standards and their audit quality.

Declaration of AI and AI-assisted technologies in the writing process

During the preparation of this work, the author(s) used OpenAI ChatGPT for proofreading purposes. After using this tool/service, the author(s) reviewed and edited the content as needed and take(s) full responsibility for the content of the publication.

Disclosure statement

No potential conflict of interest was reported by the author(s).

References

- Akande, O. O. (2021). Computerized accounting system and performance of u entrepreneurs in South Western Nigeria. International Journal of Management and Applied Science, 3(2), 90–22.

- Al-Hattami, H. M. (2022a). Impact of AIS success on decision-making effectiveness among SMEs in less developed countries. Information Technology for Development, 1–21. https://doi.org/10.1080/02681102.2022.2073325

- Al-Hattami, H. M., Abdullah, A. A. A. H., Kabra, J. D., Alsoufi, M. A., Gaber, M. M., & Shuraim, A. M. (2022b). Effect of AIS on planning process effectiveness: A case of SMEs in a less developed nation. The Bottom-Line, 35(2/3), 33–52. https://doi.org/10.1108/BL-01-2022-0001

- Al-Hattami, H. M., Hashed, A. A., Alnuzaili, K. M. E., Maged, A., Alsoufi, Z., Alnakeeb, A. A., & Rageh, H. (2021a). Effect of risk of using computerized AIS on external auditor’s work quality in Yemen. International Journal of Advanced and Applied Sciences, 8(1), 75–81. https://doi.org/10.21833/ijaas.2021.01.010

- Al-Hattami, H. M., Hashed, A. A., & Kabra, J. D. (2021b). Effect of AIS success on performance measures of SMEs: Evidence from Yemen. International Journal of Business Information Systems, 36(1), 144–164. https://doi.org/10.1504/IJBIS.2021.112399

- Al-Hattami, H. M., & Kabra, J. D. (2022). The influence of accounting information system on management control effectiveness: The perspective of SMEs in Yemen. Information Development, 02666669221087184. https://doi.org/10.1177/02666669221087184

- Al-Hattami, H. M., Senan, N. A. M., Al-Hakimi, M. A., & Azharuddin, S. (2022). An empirical examination of AIS success at the organizational level in the era of COVID-19 pandemic. Global Knowledge, Memory & Communication. https://doi.org/10.1108/GKMC-04-2022-0094

- Al-Maliki, H. S. N., Salehi, M., & Kardan, B. (2022). The effect of COVID-19 on risk-taking of small and medium-sized, family and non-family firms. Journal of Facilities Management. https://doi.org/10.1108/JFM-09-2021-0105

- Almaqtari, F., Farhan, N., Al-Hattami, H. M., & Elsheikh, T. (2023). The moderating role of information technology governance in the relationship between board characteristics and continuity management during the COVID-19 pandemic in an emerging economy. Humanities and Social Sciences Communications, 10(1). https://doi.org/10.1057/s41599-023-01552-x

- Al-Matari, A. S., Amiruddin, R., Aziz, K. A., & Al-Sharafi, M. A. (2022). The impact of dynamic accounting information system on organizational resilience: The mediating role of business processes capabilities. Sustainability, 14(9), 1–22. https://doi.org/10.3390/su14094967

- Alnajjar, M. I. M. (2017). Impact of accounting information system on organizational performance: A study of SMEs in the UAE. www.researchgate.net/publication/324062452.

- Alsufy, F. J. H. (2019). The effect of speed and accuracy in accounting information systems on financial statements content in Jordanian commercial banks. International Journal of Business & Management, 14(8), 160–166. https://doi.org/10.5539/ijbm.v14n8p160

- Amanamah, R. B., Morrison, A., & Asiedu, K. (2016). Computerized accounting systems usage by small and medium scale enterprises in Kumasi Metropolis, Ghana. Research Journal of Finance and Accounting, 7(16), 16–29.

- Amin, K., Eshleman, J. D., & Feng, C. (2018). The effect of the SEC’s XBRL mandate on audit report lags. Accounting Horizons, 32(1), 1–27. https://doi.org/10.2308/acch-51823

- Armstrong, A., & John Lee, G. (2021). Introduction to digital business. South Africa in 2021 by Silk Route Press.

- ASEAN Secretariat. (2022, October). ASEAN Investment report 2022 - pandemic recovery and Investment facilitation.

- Azudin, A., & Mansor, N. (2018). Management accounting practices of SMEs: The impact of organizational DNA, business potential and operational technology. Asia Pacific Management Review, 23(3), 222–226. https://doi.org/10.1016/j.apmrv.2017.07.014

- Bataineh, A. (2018). The effect of using computerized accounting information systems on reducing production costs in Jordanian pharmaceutical companies. International Journal of Business and Management Invention, 7(7), 1–10.

- Bhimani, A. (2020). Digital data and management accounting: Why we need to rethink research methods. Journal of Management, 31(1–2), 9–23. https://doi.org/10.1007/s00187-020-00295-z

- Bisbe, J., & Malague~no, R. (2009). The choice of interactive control systems under different innovation management modes. European Accounting Review, 18(2), 371–405. https://doi.org/10.1080/09638180902863803

- Bodnar, H. G., & Hopwood, W. S. (2006). Accounting information systems (Ninth Edition ed.). Andi.

- Bshayreh, M. M., & Hamour, A. M. A. (2020). The role of accounting information systems in reducing indirect industrial costs. Academy of Accounting & Financial Studies Journal, 24(5), 1–10.

- Butterfield, E. (2016). Managerial decision making and management accounting information. University of Applied Sciences.

- Du, H., & Wu, K. (2018). XBRL mandate and timeliness of financial reporting: Do XBRL filings take longer? Journal of Emerging Technologies in Accounting, 15(1), 57–75. https://doi.org/10.2308/jeta-52094

- Gartner, G. (2022). Retrieved December 15, 2022, from https://www.gartner.com/en/information-technology/glossary/digitalization

- Ghobakhloo, M., Iranmanesh, M., Vilkas, M., & Grybauskas, A. (2022). Drivers and barriers of industry 4.0 technology adoption among manufacturing SMEs: A systematic review and transformation roadmap. Journal of Manufacturing Technology Management, 33(6), 1029–1058. https://doi.org/10.1108/JMTM-12-2021-0505

- Hair, J. F., Jr., Tomas, G., Hult, M., Ringle, C. M., & Sarstedt, M. (2016). A primer on partial least squares structural equation modeling (2nd ed.). SAGE Publications.

- Harvey, J. (2007). Effective decision making. The Chartered Institute of Management Accountants.

- Heimel, J., & Müller, M. (2019). Controlling 4.0. In M. Erner (Ed.), Management 4.0 – Unternehmensführung im digitalen Zeitalter (pp. 389–430). Springer.

- Horvath, D., & Szabo, R. Z. (2019). Driving forces and barriers of industry 4.0: Do multinational and small and medium-sized companies have equal opportunities? Technological Forecasting and Social Change, 146, 119–132. https://doi.org/10.1016/j.techfore.2019.05.021

- Hwang, S., No, W. G., & Kim, J. (2020). XBRL mandate and timeliness of financial reporting: The effect of internal control problems. Journal of Accounting, Auditing & Finance, 36(3), 667–692. https://doi.org/10.1177/0148558X20929854

- Kim, J. J., Kim, W., & Lim, J. (2013, April 25–27). Does XBRL adoption constrain managerial opportunism in financial reporting? Evidence from mandated U.S. filers. Proceedings of the University of Kansas International Conference on XBRL, Anaheim, CA.

- Kipper, L. M., Furstenau, L. B., Hoppe, D., Frozza, R., & Iepsen, S. (2020). Scopus scientific mapping production in industry 4.0 (2011–2018): A bibliometric analysis. International Journal of Production Research, 58(6), 1605–1627. https://doi.org/10.1080/00207543.2019.1671625

- Knauer, T., Nikiforow, N., & Wagener, S. (2020). Determinants of information system quality and data quality in management accounting. Journal of Management Control, 31(1–2), 97–121. https://doi.org/10.1007/s00187-020-00296-y

- Kock, N. (2020). WarpPLS 7.0 user manual. ScriptWarp Systems.

- Kumarasinghe, W. S., & Haleem, A. (2020). The impact of digitalization on business models with special reference to management accounting in small and medium enterprises in Colombo district. International Journal of Scientific and Technology Research, 9(3), 6654–6665.

- Kuttner, M., Mayr, S., Mitter, C., & Duller, C. (2022). Impact of accounting on reorganization success: Empirical evidence from bankrupt SMEs. Journal of Accounting & Organizational Change, 19(6), 24–45. https://doi.org/10.1108/JAOC-06-2021-0080

- Laudon, J. P., & Laudon, K. C. (2020). Management information systems: Managing the digital firm. Pearson Education.

- Lavia Lopez, O., & Hiebl, M. R. (2015). Management accounting in small and medium-sized enterprises: Current knowledge and avenues for further research. Journal of Management Accounting Research, 27(1), 81–119. https://doi.org/10.2308/jmar-50915

- Lawal, A., Mohamed, R., Abdalla, H., El Kelish, W. W., & Lasyoud, A. A. (2022). The role of accounting information systems in firms’ performance during the COVID-19 pandemic. Journal of Governance & Regulation, 11(1), 45–54. https://doi.org/10.22495/jgrv11i1art5

- Mahliza, F., Priatna, W. B., & Burhanuddin, B. (2017). The influence of family and economic environment on the performance of tofu businesses in Bogor Regency. Journal of Indonesian Agribusiness, 4(1), 17–26. https://doi.org/10.29244/jai.2016.4.1.17-26

- Mezghani, K., & Aloulou, W. (2019). Business transformations in the era of digitalization. Berrett- Koehler.

- Ministry of Finance. (2022). Retrieved December 15, 2022, from https://www.kemenkeu.go.id/informasi-publik/publikasi/berita-utama/Digitalisasi-Penting-Bagi-Pengembangan-UMKM

- Mitter, C., Postlmayr, M., & Kuttner, M. (2022). Risk management in small family firms: Insights into a paradox. Journal of Family Business Management, 12(2), 237–250. https://doi.org/10.1108/JFBM-06-2020-0051

- Möller, K., Schäffer, U., & Verbeeten, F. (2020). Digitalization in management accounting and control: An editorial. Journal of Management Control, 31(1–2), 1–8. https://doi.org/10.1007/s00187-020-00300-5

- Monteiro, A., & Cepêda, C. (2021). Accounting information systems: Scientific production and trends in research. Systems, 9(3), 67. https://doi.org/10.3390/systems9030067

- Ndubuisi, A. N., Chidoziem, A. M., & Cinyere, O. B. (2017). Comparative analysis of computerized accounting system and manual accounting system of quoted microfinance banks (MFBs) in Nigeria. International Journal of Academic Research in Accounting, Finance and Management Sciences, 7(2). https://doi.org/10.6007/IJARAFMS/v7-i2/2787

- Nikmatullah, M. I., & Widarsono, A. (2014). Analysis of the implementation of cost reduction in increasing profits (studies at rural banks in west java). Journal of Accounting & Finance Research, 2(2), 352–363 https://doi.org/10.17509/jrak.v2i2.6590.

- Nitzl, C. (2016). The use of partial least squares structural equation modelling (PLS-SEM) in management accounting research: Directions for future theory development. Journal of Accounting Literature, 37(1), 19–35. https://doi.org/10.1016/j.acclit.2016.09.003

- Nitzl, C. J., Roldon, J., & Cepeda, G. (2016). Mediation analysis in partial least squares path modeling. Industrial Management & Data Systems, 116(9), 1849–1864. https://doi.org/10.1108/IMDS-07-2015-0302

- Nuari, A. R. (2017). The importance of small and medium enterprises (SMEs) to Drive economic growth in Indonesia. Paper presented at the National Seminar on Multidisciplinary Sciences.

- Obi, J. N. (2017). Effective decision-making and organizational goal achievement in a depressed economy. International Journal of Research and Development Studies, 8(1), 1–21.

- Oirere, A. N. (2015). Effect of Innovation on Financial Performance of Small and Medium Manufacturing Enterprises in Nairobi County [ Thesis]. University of Nairobi.

- Owusu, A., Akpe-Doe, C. E., & Taana, I. H. (2022). Assessing the effectiveness of E-government services in Ghana: A case of the registrar general’s department. International Journal of Electronic Government Research, 18(1), 1–23. https://doi.org/10.4018/IJEGR.289827

- Packard, M. D., Clark, B. B., & Klein, P. G. (2017). Uncertainty types and transitions in the entrepreneurial process. Organization Science, 28(5), 840–856. https://doi.org/10.1287/orsc.2017.1143

- Pedroso, E., & Gomes, C. F. (2020). The effectiveness of management accounting systems in SMEs: A multidimensional measurement approach. Journal of Applied Accounting Research, 21(3), 497–515. https://doi.org/10.1108/JAAR-05-2018-0059

- Pelz, M. (2019). Can management accounting be helpful for young and small companies? Systematic review of a paradox. International Journal of Management Reviews, 21(2), 256–274. https://doi.org/10.1111/ijmr.12197

- Pham, Q. H., & Vu, K. P. (2022). Digitalization in small and medium enterprise: A parsimonious model of digitalization of accounting information for sustainable innovation ecosystem value generation. Asia Pacific Journal of Innovation and Entrepreneurship, 16(1), 2–37. https://doi.org/10.1108/APJIE-02-2022-0013

- Pudyastuti E., & Saputra A. (2021). Efforts to increase the competitive advantage of micro, small and medium enterprises (MSMEs) in Medan city during the COVID-19 pandemic. Journal of Indonesian Business Innovation and Management, 04(3), 437–449. https://doi.org/10.31842/jurnalinobis.v4i3.195

- Rogers, E. M. (2010). Diffusion of innovations. Simon and Schuster.

- Sandalgaard, N., & Nielsen, C. (2018). Budget emphasis in small and medium-sized enterprises: Evidence from Denmark. Journal of Applied Accounting Research, 19(3), 351–364. https://doi.org/10.1108/JAAR-08-2016-0087

- Sarwar, M. I., Iqbal, M. W., Alyas, T., Namoun, A., Alrehaili, A., Tufail, A., & Tabassum, N. (2021). Data vaults for blockchain-empowered accounting information systems. IEEE Access, 9, 117306–117324. https://doi.org/10.1109/ACCESS.2021.3107484

- Shagari, S. L., Abdullah, A., & Mat Saat, R. (2017). Accounting information systems effectiveness: Evidence from the Nigerian banking sector. Interdisciplinary Journal of Information, Knowledge, and Management, 12, 309–335. https://doi.org/10.28945/3891

- Tawfik, O. I., Durrah, O., Hussainey, K., & Elmaasrawy, H. E. (2022). Factors influencing the implementation of cloud accounting: Evidence from small and medium enterprises in Oman. Journal of Science and Technology Policy Management, 14(5), 859–884. https://doi.org/10.1108/JSTPM-08-2021-0114

- Taylor, T. P. (2016). Performance Measurement in Global Product Development: The selection and application of key performance indicators. Research output: Book/Report [ Ph.D. thesis].

- Thottoli, M. M. (2021). Knowledge and use of accounting software: Evidence from Oman. Journal of Industry-University Collaboration, 3(1), 2–14. https://doi.org/10.1108/JIUC-04-2020-0005

- Thuan, P. Q., Khuong, N. V., Anh, N. D. C., Hanh, N. T. X., Thi, V. H. A., Tram, T. N. B., & Han, C. G. (2022). The determinants of the usage of accounting information systems toward operational efficiency in industrial revolution 4.0: Evidence from an emerging economy. Economies, 10(4), 83. https://doi.org/10.3390/economies10040083

- Tomic, I., Tesic, Z., Kuzmanovic, B., & Dan Tomic, M. (2018). An empirical study of employee loyalty, service quality, cost reduction and company performance. Economic Research-Ekonomska Istraživanja, 31(1), 827–846. https://doi.org/10.1080/1331677X.2018.1456346

- Trigo, A., Belfo, F., & Estébanez, R. P. (2014). Accounting information systems: The challenge of the real-time reporting. Procedia Technology, 16, 118–127. https://doi.org/10.1016/j.protcy.2014.10.075

- Weissmueller, R. J., & Johnson, G. G. (2014). Impact of using XBRL in 10K and 10Q filings with the SEC: Evidence of increased timeliness in reporting. International Journal of Business Research and Information Technology, 1(1), 45–59.

- Wu, J., & Vasarhelyi, M. (2004). XBRL: A new tool for electronic financial reporting. In Anandarajan, M., Anandarajan, A., & Srinivasan, C.A. (Eds.), Business intelligence techniques (pp. 73–92). Springer.

- Yoon, S. W., & Lee, C. (2011). The effects of mandatory XBRL filings on the timeliness of financial reporting: Early evidence. Pan-Pacific Journal of Business Research, 2(1), 104–123.

- Yoshino, N., & Taghizadeh-Hesary, F. (2016). Major challenges facing small and medium-sized enterprises in Asia and solutions for mitigating them. ADBI working paper series. Asian Development Bank Institute.

- Zhao, X., Lynch, J. G., & Chen, Q. (2010). Reconsidering Baron and Kenny: Myths and truths about mediation analysis. Journal of Consumer Research, 37(2), 197–206. https://doi.org/10.1086/651257