?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

Ghana has a lengthy history of accumulating public debt, primarily driven by the expansion of fiscal deficits. This has resulted in a persistent increase in the public debt ratio, as the country borrowed both externally and internally to stimulate economic growth and augment its capital stock. However, this trajectory has led to concerns about debt sustainability. The study examines the macroeconomic determinants of public debt accumulation in Ghana. It aims to analyse these determinants’ short- and long-term effects using the autoregressive distributed lag (ARDL) model. The study finds a positive association between merchandise trade and public debt, indicating that an increase in trade due to heavy reliance on external trade to meet domestic consumption needs leads to a rise in public debt. Furthermore, it identifies a positive relationship between gross fixed capital formation (growth) and public debt, indicating that as the economy grows and more capital is invested in fixed assets, public debt also increases. The study also reveals that higher interest payments contribute to a greater accumulation of public debt. It further demonstrates that government spending plays a crucial role in shaping the trajectory of public debt, as an increase in spending leads to an increase in public debt. The findings suggest that fiscal policies, external borrowing, trade, interest payments, and budget deficits substantially influence public debt levels in Ghana. As a result, the study highlights the need for policies that promote fiscal discipline, debt sustainability, and transparency to manage public debt effectively.

PUBLIC INTEREST STATEMENT

The growing public debt in Ghana has become a matter of great concern and has captured the attention of policymakers, economists, and citizens alike. This study explores the key factors contributing to the accumulation of public debt, including fiscal policies, borrowing practises, and economic indicators. By understanding these determinants, policymakers can develop a comprehensive understanding of the current debt situation and its implications for the Ghanaian economy. Furthermore, the study delves into possible strategies and policy recommendations to address this issue and pave the way for a sustainable future. This study is of significant public interest as it directly impacts the economic well-being and future prospects of Ghana. By addressing the challenges related to public debt, we strive to foster financial stability, promote sustainable development, and enhance the overall welfare of Ghanaian citizens.

1. Introduction

Ghana’s public debt has a long history, with various factors contributing to its accumulation (Dzawu, Citation2022). The expansion of fiscal deficits has been the primary driver behind the increase in the public debt ratio (Asiama et al., Citation2014). Ghana has borrowed both externally and internally to stimulate economic growth and augment its capital stock (Shand, Citation2020). However, this has led to a persistent increase in public debt (Ministry of Finance, Citation2021).

Ghana had no public debt record as of 1957 (Hilton, Citation2021). However, over time, the country experienced a shift from surplus budgets to deficit budgets (Ashiabor, Citation2020). Government spending also increased significantly during this period, resulting in a public debt of 25.16% of GDP by 1965 (Hilton, Citation2021). As a result of the high debt levels, Ghana was classified as a “Heavily Indebted Poor Country” (HIPC) in 2001, and the International Monetary Fund (IMF) and World Bank wrote off a significant portion of the country’s debts (Osei-Fosu, Citation2015).

Although Ghana made progress and transitioned to a lower-middle-income economy by 2008 (Schieber et al., 2012), with public debt falling from 182% in 2000 to 32% (Hilton, Citation2021), the unsustainable expansion of external debt led to a decline in the economy (Frimpong & Oteng-Abayie, Citation2006). By 2016, Ghana’s debt level had increased to 57.2% of GDP (BoG, Citation2020); as of December 2022, it represented 93.5% (IMF, Citation2023a). In addition, the COVID-19 pandemic further exacerbated the debt situation, as the government implemented expansionary fiscal policies to address the economic impact of the crisis (Aizenman & Ito, Citation2020; de Soyres et al., Citation2022).

To address the debt burden and restore debt sustainability, Ghana secured a US$3 Extended Credit Facility Arrangement from the IMF in 2023 (IMF, Citation2023a). However, the long-term effectiveness of such measures remains speculative, as they require persistent fiscal reduction and strong economic policies by the government (IMF, Citation2023b).

Given the alarming surge in public debt, there is growing concern among investors, development partners, and the Ghanaian citizenry. Ghana’s debt-to-GDP ratio is estimated to reach 98.7% by 2023, ranking the country among the top 10 nations in Sub-Saharan Africa (Myjoyonline, Citation2023). The cost of repaying outstanding debt has become more complex, and Ghana’s ability to fulfil its debt service commitments is increasingly challenging (Fitch Ratings, Citation2020; Fitch Ratings, Citation2021; Ghanaian Times, Citation2022; IMF, Citation2019; World Bank, Citation2022). The macroeconomic determinants of public debt accumulation in Ghana need to be identified to address the issue of debt sustainability (Institute of Fiscal Studies, Citation2015).

Numerous research studies have identified and rigorously evaluated the factors believed to contribute to the accumulation of debt in different time periods and countries (Brafu-Insaidoo et al., Citation2019; Drazen, Citation2000; Imbeau, Citation2004; Obeng & Sakyi, Citation2017; Swaray, Citation2005). This study revisits the macroeconomic factors that influence the level of public debt in the Ghanaian context. This study endeavours to analyse the underlying factors that influence the macroeconomic variables impacting public debt in Ghana. By analysing the causal determinants, it aims to identify the primary drivers responsible for the increasing levels of public debt in Ghana from 1970 to 2022.

To analyse the short- and long-term effects of macroeconomic determinants on public debt in Ghana, the study aims to utilise the autoregressive distributed lag (ARDL) model (Pesaran et al. in Citation2001). This model has gained recognition for its application in examining the relationship between public debt determinants in various countries, such as Nigeria (Fagbemi & Olatunde, Citation2019), Pakistan (Awan et al., Citation2015), and the Caribbean (Onafowora & Owoye, Citation2019). Its distinguishing feature is its ability to identify long- and short-term relationships among variables. Moreover, the ARDL method effectively handles small and large sample data by establishing variable integrations (Pesaran et al. in 2001). Consequently, the objective of this study is to utilise the ARDL model to analyse the short- and long-term effects of macroeconomic determinants on public debt in Ghana. Additionally, the study aims to provide potential policy implications based on the obtained results.

The study aims to provide insights into the factors contributing to Ghana’s rising public debt and offer potential policy implications based on the findings. It recognises the need for major fiscal adjustments and prudent public debt management techniques to achieve sustainable economic growth and address the challenges posed by the rising debt burden.

2. Theoretical review

The Two-Gap Model, developed by Chenery and Strout (Citation1966), explains the role of domestic savings and foreign capital in economic growth, particularly in developing countries like Ghana. These countries often face a savings and trading gap where domestic savings are insufficient for investment and export revenues do not cover import expenditures (Dang & Sui Pheng, Citation2015; Zaidi, Citation1985). As a result, international transfers, including foreign capital and exchange, are needed to bridge these gaps (Gryphon & Gryphon, Citation1978; Kirui, Citation2017). However, when foreign capital, such as foreign direct investments (FDI), is inadequate, the government resorts to borrowing to supplement its budget (Dabour, Citation2000). This model suggests that the deficit in emerging nations is necessary to achieve long-term economic growth (Nikoloski & Nedanovski, Citation2018), leading to the accumulation of foreign debt (Antwi & Atta Mills, Citation2013; Root, Citation1990).

Keynesian Economics Theory, based on the ideas of John Maynard Keynes, proposes that increasing government expenditure stimulates economic activity and spending (Elmendorf & Mankiw, Citation1999). The theory suggests that higher government spending and reduced taxes can boost demand, increasing national production or income (Wagner, Citation1911). Keynesian economics emphasises regular governmental intervention to raise aggregate demand, jobs, and output through government borrowing (Aspromourgos, Citation2018; Brown-Collier & Collier, Citation1995; Kregel, Citation1985). A rise in government debt resulting from deficit-financed fiscal policy is believed to stimulate income, money demand, and exchange rates (Fischer, Citation1993; Ncanywa et al., Citation2018). However, this theory neglects the challenges of funding budget deficits through taxes or borrowing (Pereira & Dall’acqua, Citation1991).

The Twin Deficits Phenomenon assumes that a significant government budget deficit is often associated with a large current account deficit (Duodu et al., Citation2022). Government tax cuts can lower revenue and increase the deficit, leading to higher consumption and a reduced national savings rate (Prah & Ofori, Citation2022). As a result, the country borrows more externally to meet its fiscal obligations. The twin deficits theory suggests a causal relationship between a country’s government budget and its current account balance (Miller & Russek, Citation1989). Deficit spending is considered potentially beneficial for reviving an a stagnant economy. However, critics argue that it may lead to public debt and reliance on external borrowing (Atuahene, Citation2022).

Classical economic theory views public debt negatively, considering government borrowing inefficient, harmful to prosperity, and morally wrong (Salsman, Citation2017). While some exceptions acknowledge the importance of productive government spending (Hamilton, Citation1774), classical economists generally believe that public debt hampers economic growth by reducing financial discipline and deterring private investment and foreign investors (Broner et al., Citation2014; Saungweme et al., Citation2019). Furthermore, the classical theory assumes that the economy is self-regulating (Witt, Citation1997), with mechanisms that restore it to its natural real GDP or production (Matandare, Citation2018; Snowdon & Vane, Citation2005).

3. Review of empirical studies

Numerous research studies have examined the factors behind debt accumulation in different countries and historical periods. However, the empirical literature on public debt and macroeconomic indicators has yielded conflicting results, varying depending on the timeframe and heterogeneity across countries.

Various economic variables, such as interest rates, economic growth, inflation, debt stock, budget deficit, public expenditure, the credibility of monetary policy, and openness, have been identified as potential factors influencing the trajectory of public debt (Drazen, Citation2000; Imbeau, Citation2004; Swaray, Citation2005). Atuahene’s (Citation2022) qualitative study on the Ghanaian economy found that continuous borrowing has burdened the country with public debt. The study suggests that, when managed properly, debt financing can stimulate growth and enhance an economy’s ability to service and repay its debt. However, the study also identifies three negative effects of public debt on the Ghanaian economy: “debt overhang,” “crowding out,” and default effects. These findings highlight the detrimental impact of public debt on Ghana’s GDP and investment (Atuahene, Citation2022).

Similar research conducted in Ghana (Hilton, Citation2021) confirmed the positive relationship between public debt and economic growth, aligning with Keynesian economic theory. Brafu-Insaidoo et al. (Citation2019) employed time-series econometric analysis to explore the relationship between Ghana’s public debt and macroeconomic factors. The study revealed that reduced regulatory restrictions on external borrowing, larger gaps between domestic and international interest rates, poor economic growth performance, and domestic financial deepening all contribute to increases in short-term foreign debt. However, trade openness promotes a reduction in short-term foreign debt in the short run. In contrast, multilateral development organisations’ foreign debt reduction programmes lead to a decrease in the stock of short-term foreign debt in the long run (Brafu-Insaidoo et al., Citation2019).

Obeng and Sakyi (Citation2017) used yearly time series data to investigate the impact of various factors on the expansion of government expenditure in Ghana from 1980 to 2012. Their study revealed that per capita income, tax share, population growth, the minimum wage, foreign aid, public debt, and democracy significantly influence long-term growth in government expenditure. Moreover, besides the minimum wage, these variables also serve as essential predictors of short-term government expenditure growth (Obeng & Sakyi, Citation2017).

In the context of southern Mediterranean nations, Ouhibi et al. (Citation2017) employed a simultaneous equation model to analyse the correlation between foreign direct investment, public debt, and economic development. Their findings indicated a bidirectional relationship between economic growth and foreign direct investment. In contrast, a unidirectional causal relationship exists between public debt and economic growth. The study also identified a one-way causal relationship between public debt, foreign direct investment, and economic development.

Omrane Belguith and Omrane (Citation2017) utilised the Vector Error Correction Model (VECM) technique to evaluate the primary predictors of public debt in Tunisia from 1986 to 2015. The study revealed that inflation and investment reduce public debt. In contrast, real interest rates, the budget deficit, and trade openness contribute to Tunisia’s rising public debt. The report emphasises that external borrowing from international organisations hinders the accumulation of resources for debt financing. The study suggests that sustained fiscal adjustment and a reduction in the primary deficit are necessary to mitigate debt accumulation. In Kenya, Kirui (Citation2017) examined the macroeconomic causes of public debt accumulation and found that all factors, except the real interest rate, influence public debt accumulation. Factors such as gross capital creation, exchange rates, foreign direct investment, interest payments, real GDP growth, trade openness, and the savings gap play significant roles in Kenya’s public debt accumulation.

Galiński (Citation2015) argues that higher unemployment rates lead to increased debt levels, while the structure of expenditures and revenues also affects debt levels. Swamy (Citation2015) studied 252 countries from 1980 to 2009, using the Panel Granger causality approach to assess the influence of nations’ economic, political, and income groups on debt. The findings indicate that real GDP growth, foreign direct investment, government expenditure, inflation, and population growth negatively affect debt. In contrast, trade openness, final consumption expenditure, and gross fixed capital formation have positive effects. Mupunga and Le Roux (Citation2015) investigated public debt dynamics in Zimbabwe using annual time series data from 1980 to 2012. The study revealed that unplanned political and social expenses led to considerable stock-flow adjustments, resulting in Zimbabwe’s national debt. The study also highlighted the impact of high-interest rate payments on the domestic debt portfolio and the negative effect of real interest rates on nominal GDP growth rates.

Michael (Citation2011) examined the relationship between Nigeria’s budget deficit and foreign debt burden using time-series data from 1970 to 2007. The analysis revealed a structural shift in Nigeria’s deficit and debt patterns. However, no clear causality or correlation between the variables was observed. Anoruo et al. (Citation2006) conducted a panel data analysis of 29 HIPC countries in sub-Saharan Africa from 1984 to 2000. The study found that the growth of the foreign debt to GDP ratio was significantly influenced by the real exchange rate, non-interest current account balance, economic slowdown, and interest payments. However, the study did not differentiate between internal and external factors.

In summary, extensive research has examined the causes and consequences of public debt accumulation in various countries and periods. The literature highlights the role of economic variables such as interest rates, economic growth, inflation, debt stock, budget deficit, public expenditure, and openness. The findings reveal both positive and negative effects of public debt on economic growth, government expenditure, and foreign direct investment. In addition, factors such as trade openness, investment, inflation, population growth, and fiscal adjustment emerge as significant contributors to the accumulation of public debt in different contexts.

4. Empirical methodology

4.1. Data collection and source

The relationship between public debt and associated macroeconomic variables has been extensively studied, especially within the context of three economic theories: the Keynesian growth model, the Buchanan, and the Ricardo Public Debt theories. The research incorporates significant macroeconomic factors that influence Ghana’s public debt accumulation. Previous studies, including Atuahene (Citation2022), Obeng and Sakyi (Citation2017), and Brafu-Insaidoo et al. (Citation2019), as well as theories proposed by Keynesian Economics (Blinder, Citation2008), Chenery and Strout (Citation1966), and Classical Economics (Kates, Citation2020), have highlighted the substantial impact of both domestic (internal) and external factors on the accumulation of public debt. Consequently, this study considers a comprehensive set of domestic determinants such as government spending, budget deficits, growth, gross domestic savings, and external factors like interest payments and trade as explanatory variables. The explained variable in this study is public debt. Annual data spanning from 1970 to 2022 was collected from publicly available online sources from the World Bank Development Indicators (WDI, Citation2022), Ghana’s Ministry of Finance (Ministry of Finance, Citation2022) and the Bank of Ghana (BoG, Citation2022), as presented in Table . Before conducting the ARDL bound test, the data underwent a log-transformation. The data were log-transformed before the application of the ARDL-bound test.

Table 1. Variable description and data source

4.2. Model specification

The study employed the autoregressive distributed lag (ARDL) model, initially developed by Pesaran et al. (Citation2001), to examine the long-term and short-term interactions among macroeconomic factors affecting public debt in Ghana. This methodology proves particularly valuable when analysing connections among non-stationary time series data, encompassing variables demonstrating trends or random fluctuations. The notable advantage of the ARDL approach lies in its capability to handle models involving mixed-order integration, where variables may possess different orders of integration. For instance, some variables may be integrated of order one (I(1)), indicating the presence of a unit root and non-stationarity, while others may be integrated of order zero (I(0)), suggesting stationarity. Thus, it becomes feasible to investigate relationships between variables with distinct statistical properties.

Furthermore, the ARDL approach enables researchers to estimate the long-term equilibrium relationship between variables and capture the short-term dynamics or adjustments towards equilibrium. Consequently, this methodology allows for evaluating the impact of changes in one variable on another variable over time, even when the variables themselves are non-stationary. The construction of the following model aimed to establish the relationship between the dependent and independent variables.

Equation (1) is then expanded linearly and formulated as in Equation (12):

After logarithmic transformation, Equation (2) is specified as follows:

Where is the total public debt in period t;

is the annual budget deficit in period t;

is the gross domestic savings in period t;

is the total government expenditure in period t;

is the growth in gross fixed capital formation in period t (investment spending in period t);

is the total interest payment for debt service in period t;

is merchandise trade in period t;

is the constant;

–

are the respective regression coefficients;

denotes the stochastic white noise, and t denotes the time period (1970–2022).

4.3. Unit root test (Test for stationarity)

Research has established that unit roots can lead to misleading outcomes in time series analysis (Granger & Newbold, Citation1974; Phillips, Citation1987). To address this issue, the AugmentedDickey—Fuller (ADF) and Phillips-Perron (PP) tests have been developed as a means to assess the stationarity of standard unit roots (Dickey & Fuller, Citation1981; Phillips, Citation1987). When most variables or series under consideration are non-stationary, unit root tests become valuable tools for determining the integration order of these variables. In the specified model (Eqn. 3), assuming the variables possess unit roots at the initial level, they can be transformed into stationary series through first differencing, denoted as I(1). In this scenario, the ADF and PP tests can be employed to examine the presence of a unit root. The typical formulation of the ADF test is represented by Equation (4).

where θ stands for the interest variable, Δ is the difference in the parameter, is the constant,

is the coefficient on a time trend,

is the lagged values of the dependent variable, δi is the coefficient of the lagged dependent variable, and

is the white noise.

4.4. Cointegration test

Cointegration occurs when variables exhibit an a stationary linear combination. This study employed the ARDL bounds test to assess the level of integration among the variables under investigation. The Johansen-Juselius cointegration test was also further estimated to ensure the results’ robustness, considering all variables exhibited integration of order I(1). The ARDL bounds test was employed as a diagnostic tool to examine the long-run relationship between the variables of interest. This test allows for determining whether a cointegrating relationship exists among the variables. Examining the bounds of the estimated model provides insights into long-term equilibrium in the system. The Johansen-Juselius test for cointegration was also conducted to strengthen the reliability of the findings. This test is particularly useful when the variables are integrated in order I(1).

Estimating the number of cointegrating vectors helps identify the long-term relationship between the variables. This approach serves as an additional verification of the results obtained through the ARDL bounds test. By employing the ARDL bounds test and the Johansen-Juselius test, this study ensures a comprehensive evaluation of the integration and cointegration levels among the variables. Such an approach enhances the robustness of the analysis. Furthermore, it provides a more reliable basis for concluding the relationships among the variables in the study.

To estimate the ARDL model, the appropriate lag length (p) is determined using criteria such as the Final Prediction Error (FPE), Akaike Information Criterion (AIC), or Schwarz Bayesian Criterion (SBC). The errors in the model should demonstrate the characteristics of white noise, indicating that they are a sequence of identically distributed and independent random variables with a constant mean and variance. Once the lag length is determined, the ARDL model is specified and estimated. The Wald test is used to verify the long-run association among the variables. The null hypothesis suggests no cointegration, while the alternative hypothesis indicates the presence of cointegration. The calculated F-statistic is compared to the lower and upper bound values. If the estimated F-statistic exceeds these bounds, it indicates the existence of cointegration.

4.5. ARDL model

When the variables exhibit cointegration as determined by the ARDL bounds test, they possess a shared stochastic trend and will grow proportionally over time. Consequently, Engle and Granger (Citation1987) suggest that an error correction model (ECM) should be constructed when a long-term relationship exists between the variables. Conversely, the vector autoregressive model (VAR) is typically preferred if the variables exhibit a short-term association. Hence, in the case of cointegration, an ECM representation can be expressed using Equationequations (4)4

4 and (Equation5

5

5 ). The lag length for the ECM is determined based on the Akaike information criterion (AIC) in this study.

In the case of cointegration, the ARDL form for the long-run relationship model is specified in Equation 4.

The short-run model, estimated with the ECM, is formulated as in Equation (5).

where represents the public debt,

denotes the residuals series from the long-run regression’s error correction term,

is the parameter for the speed of adjustment,

is the difference operator,

is the constant to

represent the regression coefficients,

represents the optimal lag orders, and

represents the number of variables in the model, which could be from 1 to k. The dependent variable is a function of its lagged values

, which becomes an exogenous variable among the lagged values of the regressors in the model.

The first part of Equation (5)

represents the short-run relationship, while indicates the long-run relationship of the model.

4.6. Model stability

Performing diagnostic tests to validate the estimated error correction model is important. These tests help determine the model’s validity and reliability. These tests include checking for serial correlation, assessing heteroscedasticity, and evaluating normality. The CUSUM and CUSUMSQ tests are used to confirm the stability of the model’s coefficients.

The first diagnostic test is for serial correlation, which checks for autocorrelation in the estimated model. If there is no correlation between disturbance terms, it indicates that the model is acceptable. However, if this assumption is violated, it suggests the presence of autocorrelation. Commonly used tests for detecting serial correlation are the Durbin-Watson statistics and the LaGrange multiplier test for serial correlation (χ2SC). The second diagnostic test focuses on assessing heteroscedasticity, which determines the reliability of the estimated model in forecasting the dependent variable. The assumption of homoscedasticity, where the variance of the residuals is constant, must be met for the model’s findings to be valid. The LaGrange multiplier test for heteroscedasticity (χ2 ARCH) is used to evaluate the presence of heteroscedasticity. The last diagnostic test is the normality test, performed on the double-log findings. Similar to other residual-based tests, the Shapiro-Wilk test of normality (χ2 normality) is used to assess the normality of the residuals.

When the results of these tests reveal that the residuals deviate from an a normal distribution and suggest the existence of serial correlation and heteroscedasticity, it implies that the conclusions drawn from the model cannot be accepted due to unreliable statistical inferences. To confirm the existence of long-run associations between variables, the study applies cumulative sum (CUSUM) and cumulative sum of squares (CUSUMSQ) tests. These tests plot the residuals of the ECM. Suppose the statistics in the plot fall within critical bounds at a 5% significant value; in that case, it suggests that the coefficients of the ARDL model are stable.

5. Results and discussions

5.1. Descriptive analysis

The study uses time series data from 1970 to 2022 to empirically investigate the effects of budget deficits, gross domestic savings, overall government expenditure, economic growth, interest payments, and trade balances on public debt accumulation in Ghana. The descriptive statistics of the study variables stated in Table specified that the Jarque-Bera tests for the entire variables used in the study are insignificant except for interest payment, which implies that all the selected variables were normally distributed except interest payment, which was not normally distributed at level The ARDL model assumes that the variables are normally distributed and free from issues like heteroscedasticity. Log-transforming variables is a common technique used in statistical analysis to improve the normality of the data distribution (Newman, Citation1993). Therefore, all the variables were log-transformed to ensure a normal distribution and improve the model’s fitness.

Table 2. Descriptive statistics

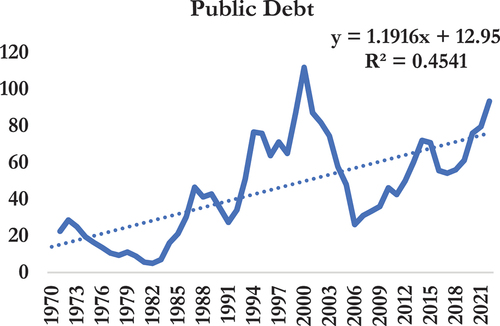

The trend in public debt accumulation shows that public debt was high in 2000 (111.95%) but afterwards showed a continuous reduction until 2006, as shown in Figure . The reduction of Ghana’s public debt between 2000 and 2006 was primarily due to the implementation of the Heavily The HIPC program was a debt relief initiative established by the International Monetary Fund (IMF) and the World Bank to assist highly indebted developing countries to lower debt burden in achieving debt sustainability. Subsequently, Ghana faced several economic challenges, including high fiscal deficits, low revenue mobilisation, global shocks (e.g., COVID-19) and increasing expenditure commitments. These challenges put pressure on the government’s finances and necessitated borrowing to meet its obligations. The trend line in Figure shows that public debt continuously increased at a rate of 1.19% each year between 1970 and 2022. The descriptive statistics further demonstrate that an average of 45.17% of debt is added annually to the public debt stock.

Figure 1. The trend in public debt in Ghana (1970–2022).

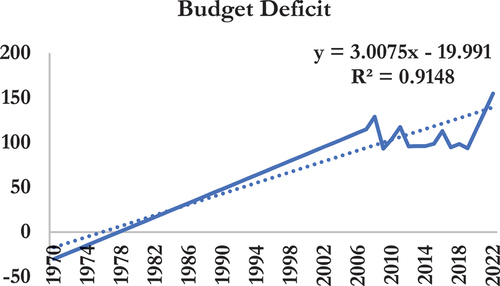

The descriptive statistics show that the budget deficit averaged 61.21%, with the highest deficit of 154.94% recorded in 2022, while the lowest deficit was noted as −30.17% in 1970, as shown in Table . The COVID-19 outbreak in 2020 caused a worldwide health emergency and had negative economic consequences globally, including in Ghana. The Ghanaian government enforced lockdowns, travel restrictions, and social distancing guidelines to control the virus’s spread. These actions had a detrimental impact on businesses, employment, and the overall economy, leading to a decline in Ghana’s GDP. The pandemic-induced economic downturn caused a significant decline in government revenue sources while expenditures increased. These combined factors contributed to Ghana’s severely impacted fiscal position, resulting in a widened fiscal deficit reaching its highest point in 2022. The trend line in Figure shows an upward fiscal fragility, with the budget deficit continuously increasing at a rate of 3.0% each year. This support the claim that increasing budget deficit is a major factor of public debt accumulation in Ghana since the government is forced to borrow to finance the gap due to low private sector activity to fill the financing gap.

Figure 2. The trend in budget deficit in Ghana (1970–2022).

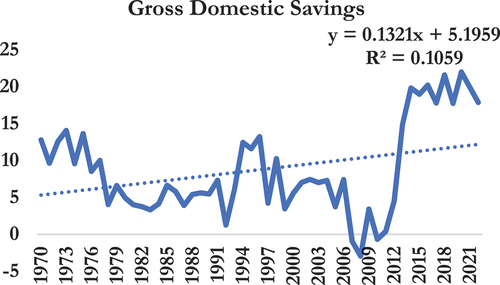

Similarly, the gross domestic savings (% GDP) during the study period peaked in 2020 (22.0%), with the lowest gross domestic savings (−2.96%) recorded in 2008. Due to low aggregate savings in Ghana, the government has limited access to domestic funds to finance its expenditures. Inadequate domestic financing forces the government to rely more on external borrowing, which often comes with higher interest rates and more stringent repayment terms, leading to increased public debt. The results in Table demonstrate an average of 8.76% aggregate savings for the period studied. The observed trend line in Figure shows a relatively low and inconsistent aggregate savings habit as gross domestic savings increase at 0.13% each year.

Figure 3. The trend in gross domestic savings in Ghana (1970–2022).

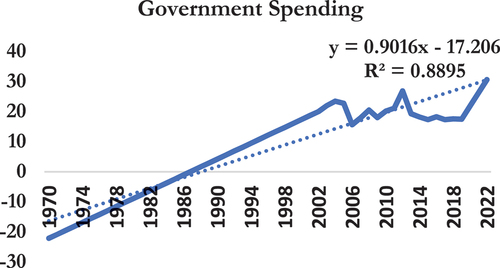

The average government expenditure was 7.14% of GDP, ranging from −22.13% in 1970 to 30.63% in 2022. The trend line of government expenditure shows the high level of government activity in financing the fiscal gap during the period, with an upward movement of 0.90% each year, as shown in Figure . The Government of Ghana’s revenue sources, such as taxes, tariffs, and fees, are inadequate to cover its expenditure requirements, forcing the government to consistently borrow to bridge the gap. Weak tax administration, low tax compliance, and an over-reliance on volatile revenue sources limit the government’s ability to generate sufficient income.

Figure 4. The trend in government expenditure in Ghana (1970–2022).

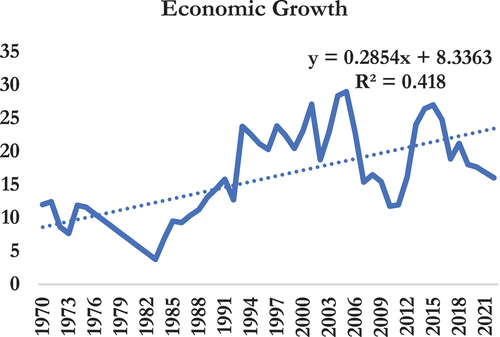

Figure displays the trend line for the productive capacity of the Ghanaian economy. The trend line shows a 0.29% annual expansion rate, implying an average yearly increase in productive capacity of 0.29%. Over the studied period, the average expansion rate was 16.04%. This suggests that the Ghanaian economy experienced consistent growth in its productive capacity throughout the studied period, albeit at a relatively modest rate of 0.29% per year. The average expansion rate of 16.04% indicates that, despite the low annual growth rate, the cumulative increase in productive capacity over the entire period was significant. This could be seen as a positive trend for the Ghanaian economy, indicating a gradual but steady improvement in its ability to produce goods and services. The implications of the trend line for productive capacity on public debt suggest that a growing and improving economy can positively affect managing and reducing public debt. The increased tax revenues, improved debt servicing capacity, and enhanced investor confidence resulting from a growing productive capacity can contribute to a more sustainable fiscal position for the government and the country.

Figure 5. The trend in growth in Ghana (1970–2022).

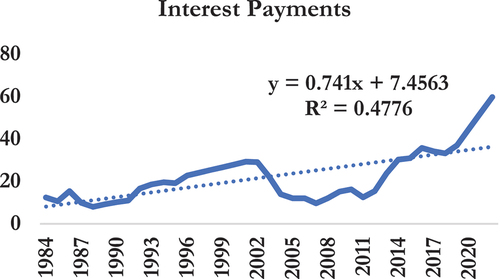

Likewise, as shown in Figure , the trend line for interest payments (% of revenue) on accumulated public debt shows the debt burden scenario of Ghana as the proportion of revenue for debt servicing continually increased by 0.74% annually over the specified time frame, reaching an all-time high in 2022 (59.8%). The descriptive statistics further suggest that an average of 22.28% of revenue is used for interest payments over the same period. Due to accumulating debt, a substantial proportion of the government’s income is allocated to servicing debt obligations, resulting in a reduced availability of funds for critical expenditures. Consequently, the government heavily depends on borrowing to sustain its operations, lacking the ability to generate ample revenue to meet its expenses and encountering challenges in fulfilling its debt obligations. This predicament compels the government to seek additional loans to repay existing debts or finance new expenditures, perpetuating a cycle of accumulating debt.

Figure 6. The trend in interest payments in Ghana (1970–2022).).

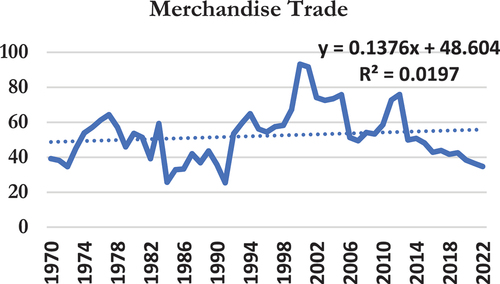

The trend line in Figure shows an increase of 0.14% in Merchandise trade (% of GDP) each year from 1970 to 2022. This suggests that Ghana’s international trade has been growing steadily. The descriptive statistics indicate that a significant portion of Ghana’s economic output is associated with international trade, averaging 52.32% of the overall economic activity. Furthermore, the country’s international trade reached an all-time high of 93.2% in 2000, implying that Ghana’s international trade as a percentage of GDP is exceptionally high, indicating a significant economic dependence on international trade. High dependence on international trade makes Ghana’s economy more vulnerable to external shocks and global economic conditions. Any disruptions in international trade, such as a decline in global demand or trade barriers imposed by other countries, can negatively impact Ghana’s economic performance. In addition, Ghana’s high dependence on international trade made its economy more vulnerable to external shocks, such as falling commodity prices in the mid-2000s and the disruptions caused by the COVID-19 pandemic. These disruptions reduced tax revenues and increased spending on social safety nets. The government incurred higher levels of public debt to manage the economic fallout. This highlights the importance for Ghana, and other countries with similar economic structures, to diversify their economies, enhance domestic production capabilities, and reduce reliance on a single sector or external trade.

Figure 7. The trend in merchandise trade of Ghana (1970–2022).

5.2. Unit root test (Test for stationarity)

Before applying the ARDL bound test, it is important to check the unit root of each variable to ensure that all variables are stationary at I(0), I(1), or both to find the bound F-statistic test. To check the integration order of each variable, the study incorporates the augmented Dickey—Fuller (ADF) and Phillips—Perron (PP) unit root tests (Said & Dickey, Citation1984). The results were evaluated by comparing the test statistics to critical values provided by MacKinnon (Citation1996). The null hypothesis of these tests assumes the presence of a unit root. A lower test statistic than the critical value indicates stationarity in the series. The ADF and PP tests, presented in Tables , demonstrate that all the variables analysed showed first-order difference stationarity at order I(1) with a significance level of 0.05. This indicates no unit root in the series for public debt, budget deficit, gross domestic savings, overall government expenditure, economic growth, interest payment, and trade balance. This suggests these variables do not exhibit persistent and non-reverting trends over time. Instead, they are likely to fluctuate around a stable level or follow a predictable pattern. Consequently, it can be concluded that these variables share the same order of stationarity, suggesting a potential long-run relationship among them.

Table 3. Augmented Dickey-Fuller (ADF) unit root test

Table 4. Phillips-Perron (PP) test

5.3. Lag selection criteria

Before conducting the ARDL bound test to determine the presence of cointegration among public debt, budget deficit, gross domestic savings, overall government expenditure, economic growth, interest payment, and trade balance, it is crucial to choose an appropriate lag order for the variables. This study utilised the optimal lag order of the vector autoregression (VAR) model to determine the suitable lag order. Table displays the results obtained from the lag selection criteria for implementing the ARDL bound test, indicating that the model performs more effectively (i.e., gives better results)with a lag of 4 compared to lags 1, 2, and 3.

Table 5. VAR lag order selection criteria

5.4. ARDL bound test for cointegration

To ascertain the long- and short-run relationships between variables, it is essential to employ the ARDL bound test (Pesaran et al., Citation2001) to confirm the presence of cointegration. The findings of the ARDL bound test, assessing the cointegration among public debt, budget deficit, gross domestic savings, overall government expenditure, economic growth, interest payment, and trade balance, are presented in Table . The computed F-statistic in the table is 8.686, surpassing the critical value of 3.61 at the 5% significance level. As a result, according to Pesaran et al. (Citation2001), the null hypothesis of no cointegrating relationship can be rejected. This indicates that public debt exhibits cointegration with budget deficit, gross domestic savings, overall government expenditure, economic growth, interest payment, and trade balance. Furthermore, these results signify a long-term relationship between the variables.

Table 6. Testing for level relationship among variables in the ARDL model

Moreover, given that all the variables have been integrated of order 1, the examination incorporates the cointegration approach introduced by Johansen and Juselius (xxx) to ensure the robustness of the prevailing long-term relationships among the variables. Table presents the empirical outcomes of Johansen’s cointegration analysis, which offer substantial evidence supporting the robustness and effectiveness of the long-run associations among the variables. The trace and max-eigenvalue tests indicate the presence of five (5) cointegrating equations at a significance level of 0.05. This finding demonstrates a long-term association within the error term, implying that all variables are cointegrated or possess a relationship over the long run. Since cointegration is established among the variables of interest, the study estimates the long-run relationship between public debt and its determinants using the Autoregressive Distributed Lag (ARDL) model. Liang and Schienle (Citation2019) propose that the Error Correction Model (ECM) is particularly suitable when there is evidence of cointegration among the variables.

Table 7. Johansen tests for cointegration

5.5. Short-run and long-run estimations

Engle and Granger (Citation1987) propose that an ECM should be constructed in the presence of a long-run relationship between variables. Consequently, an ECM was developed, wherein the error term was estimated. The estimated coefficient of the ARDL ECM confirms the presence of cointegration among variables and demonstrates a negative sign. It signifies the speed of adjustment towards long-run equilibrium following short-run shocks. This study’s estimated ECM coefficient is −1.80 and statistically significant at a 5% level. This implies that any deviation from the short-run equilibrium between variables and public debt can be rectified and restored annually at a rate of 1.80% in the long run, as illustrated in Table . After verifying the existence of a long- and short-run association between variables from the ARDL bound test, the study finds the variables’ long- and short-run parameters.

Managing public debt in Ghana presents significant challenges due to its susceptibility to various factors (Franzkowiak et al., Citation2022). The empirical results of the debt burden factors are shown in Table for a long-run association which implies that an increase in merchandise trade in Ghana can significantly increase public debt. The estimated coefficient of 0.68% indicates the expected change in public debt is associated with a 1% change in merchandise trade, holding other factors constant. This finding suggests that when Ghana’s merchandise trade expands, the country’s public debt tends to increase. This positive relationship implies that as trade in goods and services grows, it puts upward pressure on the country’s public debt. Ghana relies heavily on imported goods and products to meet domestic consumption needs. According to Aryeetey and Fenny (Citation2017), a decreasing balance of payments surplus persisted from 2010, despite a huge and increasing trade deficit, due to a current account surplus. However, the trade deficit persisted as the country imported more and more. This finding confirms the Trading Gap of Chenery and Strout’s (Citation1966) Two-Gap Economic Model, as actual export receipts by the government are less than import expenditures.

Table 8. Estimated long-run coefficients from ARDL models (53 observations from 1970 to 2022)

Even though Ghana has recorded trade surpluses in recent years, the trade-off between the impact of export and import on public debt accumulation has been a source of debate. The surplus is attributable to gold and crude oil exports, which are mostly managed and controlled by international corporations, which amass approximately 90% of the generated revenue at the expense of Ghana. This demonstrates that although Ghana boasts a trade surplus, it lacks true ownership and has had to borrow to shore up its international reserves. The findings suggest that Ghana’s heavy reliance on external trade leads to increased public debt. The government must consistently borrow to maintain its reserves and cover trade-related expenses, especially during high trade activity or trade deficits.

The Government of Ghana’s investment in fixed assets often involves financing infrastructure projects such as roads, bridges, ports, power plants, or public buildings which are expected to translate into growth. These projects require substantial upfront capital investment, which the government typically finances through borrowing. Following the study’s theoretical leanings, the findings suggest a significant positive long-run relationship between gross fixed capital formation (growth) and public debt at a 5% significance level. This implies a stable and proportional relationship between growth and public debt over the long run in the Ghanaian economy. In other words, as the economy grows and more capital is invested in fixed assets, public debt will likely increase.

The coefficient estimate of 0.22 indicates the magnitude of the impact of growth on public debt. Specifically, it suggests that a 1% increase in gross fixed capital formation (growth) is associated with a 0.22% increase in public debt. This implies that the government’s investment in fixed assets contributes to the accumulation of public debt. Similarly, Amankwah et al. (Citation2018) found that government debt negatively influences economic growth in Ghana. Baidoo et al. (Citation2021) also found that as government debt increases, it tends to have an adverse effect on the overall growth of the Ghanaian economy. Although the need to improve infrastructure in Ghana is frequently emphasised, budget allocations for capital investment routinely fall short of investment requirements. In 2016, 7.7% of the yearly budget was allocated to capital expenditures. In 2017, that amount decreased to 6.8%. 2018 it decreased to 4.7% before rising to 8.5% in 2019. This is inadequate to match the predicted $40 billion needed to expand Ghana’s road networks alone. Therefore, the government has been obliged to borrow to supplement locally generated earnings, thereby increasing the public debt.

As the government accumulates debt, it becomes obligated to pay interest and principal repayments on these borrowings. The debt servicing costs represent a significant portion of the government’s annual budget expenditure. As revenue generation falls short of covering these costs, the government is forced to borrow more or allocate a larger portion of its budget to debt servicing, leading to further debt accumulation. This is confirmed by the study findings, which suggest that debt servicing through interest payment (% of revenue) has a significant positive long-run association with public debt at a 5% significant level.

This outcome implies that a 1% increase in interest payments is associated with a 0.53% increase in public debt. This indicates that higher interest payments contribute to a greater accumulation of public debt over the long term. Bawumia’s (Citation2015) findings align with this outcome, revealing a similar pattern wherein Ghana’s public debt expansion was attributed to the escalating debt servicing burden. The indication is that when the government’s revenue generation falls short of covering the debt servicing costs, it faces two options: borrowing more or allocating a larger portion of its budget to debt servicing. In both cases, this leads to a further accumulation of debt.

The Institute of Fiscal Studies (Citation2015) reported that interest payment had become a major factor behind the country’s fiscal deterioration, besides wages and salaries, requiring serious attention. According to Fitch Ratings (Citation2015), the country’s interest burden is the highest amongst its rated sub-Saharan African countries. As a result, Ghana’s economy experienced recent downgrades by prominent international credit rating agencies like Fitch Ratings in 2022. These downgrades were primarily linked to the country’s inability to generate sufficient revenue to fulfil its debt obligations.

Government debt stands at approximately 535% of government revenue, which is significantly higher than the 304% observed in economies with similar credit ratings, according to Fitch Ratings in 2021. Fumey et al. (Citation2022) state that the presence of statutory payments in the budget, over which the government has no control, poses challenges to its ability to achieve its goals without borrowing. The country’s overall revenues and grants are primarily consumed by debt servicing and staff compensation. In 2020, around 70% of the revenue was dedicated to loan repayment, including interest and amortisation. This figure is close to the 72% recorded when the country joined the programme for Heavily Indebted Poor Countries (HIPC) in 2000.

Credendo (Citation2022) reported that in 2020, decisive actions to mitigate the impact of the COVID-19 pandemic helped the business environment and households but came with a major fiscal cost. Public interest payments in 2020 absorbed half of that year’s total public revenues, further aggravating concerns over Ghana’s public debt sustainability, which has been at “high risk of debt distress” according to the IMF’s Debt Sustainability Analysis (DSA) for years. In 2021, the interest burden reached more than 50% of public revenues, the second-highest ratio in the world following Sri Lanka. Without a significant increase in revenues, the burden of these interest payments could spark a debt crisis in the near term. Overall, the results support the notion that higher interest payments contribute to a further increase in public debt.

The study suggests a statistically negative significant long-run relationship between budget deficit on public debt at a 5% level of significance. This outcome implies that when the government increases its budget deficit by 1%, the country’s public debt decreases by 0.38% in the long run. This implies that the government’s borrowing through the budget deficit effectively reduces the overall public debt burden. This might seem counterintuitive initially, but it can be explained by considering the potential effects of the government’s budget deficit financing on economic growth and fiscal sustainability in the long run. The findings support the Keynesian economic theory (Thirlwall, Citation1987), which suggests that government deficit financing can be useful in specific economic situations, particularly during recessions or periods of low aggregate demand to stimulate economic growth.

In the long term, budget deficits may stimulate economic growth through increased government spending, leading to higher tax revenues and improved economic conditions. As a growing economy, Ghana can generate higher income levels and increased tax revenues, which can help reduce the public debt burden over time. Additionally, policymakers have implemented measures to address fiscal imbalances and improve the sustainability of public finances, such as implementing structural reforms or pursuing fiscal consolidation measures. For instance, the promulgation of the Fiscal Responsibility Act 2018 (Act 982) aimed at promoting fiscal discipline and controlling public debt. It provides a framework for managing government finances, emphasising responsible spending, debt sustainability, and transparency. The Act sets targets for reducing the debt-to-GDP ratio. In addition, it limits the amount of debt the government can accumulate. This helps prevent excessive borrowing and mitigate the risks of high debt levels.

However, the economic doldrum from the impact of COVID-19 led to the suspension of the Act, as fiscal revenues fell short of planned expenditures leading to increased borrowing and debt accumulation. Consequently, Ghana could not meet its debt obligations, resulting in a severe financial and economic situation. In 2020, decisive actions to mitigate the impact of the COVID-19 pandemic helped the business environment and households but came with a major fiscal cost. As a result, the fiscal deficit amounted to more than 15% of GDP, further aggravating concerns over Ghana’s public debt sustainability, which has been at “high risk of debt distress” according to the IMF’s Debt Sustainability Analysis (DSA). In 2021, the budget deficit reached double digits again, pushing the gross public debt stock to 81.8% of GDP (567.9% of public revenue). By 2022, the country’s debt had risen significantly due to borrowing to finance infrastructure projects and budget deficits.

As a result, Ghana sought assistance from the International Monetary Fund (IMF) to address its fiscal imbalances and implement structural reforms (Amponsah, Citation2015). Under the IMF programme, Ghana implemented several measures to restore fiscal discipline and debt sustainability. Additionally, Ghana restructured its domestic debt repayment as part of its IMF conditionalities, implying that the country took steps to renegotiate the terms of its domestic debt, such as extending maturity dates, reducing interest rates, or adjusting payment schedules. Such restructuring efforts were pursued to enhance debt sustainability and create more manageable repayment obligations.

The study further indicates a statistically significant positive long-term relationship between government spending and public debt at a 5% significance level. The positive and significant coefficient indicates that the relationship between government spending and public debt is not merely due to chance but reflects a meaningful association. The findings suggest that when the Government of Ghana increases its spending by 1%, it leads to a 0.24% increase in the country’s public debt in the long run. This implies that government spending is crucial in shaping Ghana’s public debt trajectory. When the government decides to increase its spending, it incurs additional costs that contribute to accumulating public debt over time. The current findings align with the results of prior studies (Asiama et al., Citation2014; Frimpong & Oteng-Abayie, Citation2006; Owusu‐Nantwi & Erickson, Citation2016) conducted on a similar topic.

This convergence in findings across studies adds credibility to Ghana’s observed relationship between government spending and public debt. The Government of Ghana consistently spends more than its revenue, which results in a budget deficit. To cover this deficit, the government borrows money by issuing treasury bills, bonds, or obtaining loans from international financial institutions. These borrowings contribute to the accumulation of public debt. Also, governments often invest in infrastructure projects such as roads, schools, hospitals, and energy facilities to promote economic growth and improve living standards. While these investments are important for long-term development, they often require substantial funding.

The government relies heavily on borrowing to finance these projects without generating sufficient revenue or controlling expenses, leading to a significant increase in public debt. Furthermore, the government provides subsidies or implements social programmes to support vulnerable populations, stimulate economic sectors, or promote social welfare. These initiatives, such as education subsidies, healthcare programmes, or cash transfer schemes, require financial resources. Consequently, the government cannot fund them adequately from its revenue sources and resorts to borrowing, contributing to debt accumulation.

The findings reveal that the relationship between domestic savings and public debt is non-significant in the long run. This implies that over an extended period, increasing domestic savings does not have a meaningful effect on public debt in Ghana. However, the observed 1% increase in domestic savings potentially increasing public debt by 0.05%, in the long run, may imply that there might be some impact of domestic savings on public debt, although not significant in the long run. Therefore, in the long run, the non-significant impact implies that domestic savings alone do not favourably affect the dynamics of Ghana’s public debt in the long run. This finding is consistent with Nneka and Ubah (Citation2021).

As the preliminary findings of this study have shown, other factors, such as government spending, external borrowing, fiscal policies, trade, interest payments, and budget deficits, have a more substantial influence on public debt levels. This implies that changes in domestic savings alone do not significantly impact the level of public debt over an extended period, given the Ghanaian context. This suggests other mechanisms through which domestic savings indirectly affect public debt in the long run.

Savings rates in Sub-Saharan Africa (SSA) countries exhibit a general trend of being low, both in the government and private sectors. However, there are notable variations among nations. For example, despite Ghana’s classification as a lower-middle-income economy, its savings performance falls short compared to its West African counterparts like Nigeria and Cote d’Ivoire. These dissimilarities can be attributed to a combination of sociocultural and political-economic factors. Notably, Ghana experienced a banking sector clean-up in 2017 that resulted in the loss of savings for a significant portion of the population. This event has potentially had a profound impact on the savings culture within the country. Consequently, households and businesses may view traditional bank accounts as insecure, opting instead to save their funds in unconventional locations (Ackah & Lambon-Quayefio, Citation2020). These factors could explain why domestic savings is insignificant in impacting public debt.

In the short run, the coefficient of macroeconomic factors such as trade, growth, interest payment, and budget deficit significantly influence public debt. The results shown in Table indicate that, in the short run, an increase in trade in Ghana leads to a decrease in public debt. In this case, the estimated coefficient of −0.96 indicates that a 1% increase in trade will cause a 0.96% reduction in public debt in the short run. This negative coefficient suggests an inverse relationship between trade and public debt in Ghana. It implies that as trade expands, the associated economic benefits, such as increased exports or foreign investment, lead to higher revenue generation, reducing the need for borrowing and consequently lowering public debt. However, these findings contradict the long-run estimates, which show that increased trade stimulates debt accumulation. Therefore, despite the recorded trade surplus in recent times, it has not significantly impacted debt reduction in the long run in Ghana.

Table 9. Estimated short-run coefficients from ARDL models (53 observations from 1970 to 2022)

This suggests that despite the trade surplus, Ghana’s overall debt level has not been significantly influenced by this surplus over an extended period. In other words, the trade surplus has not contributed significantly to reducing the country’s debt burden. Therefore, the findings imply that while Ghana may have had a trade surplus in recent times, other factors or economic challenges may be contributing to the country’s ongoing debt accumulation, suggesting that the trade surplus alone has not been sufficient to address the debt situation in the long run. This could explain why Ghana’s trade surpluses in recent years, such as the $1.107 billion recorded at the end of the 2021 fiscal year, according to the Bank of Ghana’s Summary of Economic and Financial Data, have not resulted in public debt reduction.

In the short run, an increase of 1% in interest payments in Ghana leads to a decrease of 0.48% in public debt. This suggests that higher interest payments may act as a disincentive for the government to accumulate additional debt in the short term. On the other hand, in the long run, the estimates reveal that interest payments accumulate public debt. This indicates that over an extended period, the impact of higher interest payments outweighs the short-term disincentive effect. This could be due to compounding interest, limited fiscal discipline, or other macroeconomic factors that lead to debt accumulation despite interest payments. To find common ground, it is important to recognise that the short-term and long-term dynamics of interest payments on public debt can differ. In the short run, higher interest payments may serve as a deterrent, encouraging the government to be more cautious in accumulating debt. However, in the long run, the burden of interest payments can outweigh the initial disincentive effect and contribute to the accumulation of public debt.

The study found that a 1% increase in economic growth leads to a 0.41% increase in public debt. This means that when the economy experiences short-term growth, there is a slight increase in the accumulation of public debt. It suggests that governments tend to borrow more during periods of economic expansion to finance various projects or provide stimulus. The study also revealed that over the long term, economic growth contributes to the accumulation of public debt. This indicates that sustained economic growth can lead to a continuous increase in public debt levels. The reasons for this could include increased government spending, investment in infrastructure, or other factors that require borrowing. While economic growth is generally seen as beneficial, it also has implications for public debt. The Government of Ghana often borrows during periods of economic expansion to stimulate further growth or address various needs leading to increased debt accumulation.

In 2016, there was a notable deviation in government spending, surpassing the projected GDP by 3.9%. However, expenditures consistently fell short of the set targets in subsequent periods. Unfortunately, the levels of revenue generated did not match the initial projections. This shortfall in government revenue resulted in recurring fiscal deficits, leading to debt accumulation over several years and increased expenses for servicing that debt. In the short run, it is observed that a 1% increase in the budget deficit leads to a 0.44% increase in public debt in Ghana. This suggests that in the immediate period following a budget deficit, the government relies on borrowing to finance its expenditures, increasing the public debt. This relationship is statistically significant at a 5% level, indicating a relatively strong correlation between budget deficits and public debt in the short term.

On the other hand, the long-run estimates indicate a different relationship between budget deficits and public debt. The estimates suggest that budget deficits reduce Ghana’s public debt over an extended period. Recognising the distinction between short-run and long-run dynamics is important to find common ground between these contrasting results. In the short run, budget deficits may contribute to an increase in public debt, reflecting the immediate impact of borrowing to finance expenditures. However, budget deficits can lead to economic growth and improved fiscal sustainability in the long run, reducing public debt over time.

This implies that increasing debt to finance the deficit has short-term and long-term implications for Ghana. The government can continue funding essential services and infrastructure projects in the short term. However, accumulating too much debt has led to concerns about the country’s ability to repay its obligations, resulting in higher interest rates on future borrowing. Additionally, the private sector in Ghana is experiencing considerably low economic activity. As a result, it cannot adequately fund the budget deficit, presenting challenges for the government in managing its fiscal situation. Hence, the private sector is not generating sufficient revenue and profits, which results in lower tax revenues for the government, reducing the funds available to cover the budget deficit. As a result, it becomes challenging for the government to rely on private sector funding alone to cover the deficit. Therefore, the government must fill the financing gap by increasing its debt.

In the short run, the study suggests that government spending does not significantly impact public debt. Several factors may influence this finding. In the short term, government spending can stimulate economic growth, increase aggregate demand, and create jobs. This can lead to higher tax revenues and reduced reliance on debt financing, resulting in a smaller immediate impact on public debt. Additionally, other short-term factors, such as favourable economic conditions, temporary revenue surpluses, or external assistance, may mitigate the impact of government spending on public debt. On the other hand, in the long run, the study reveals that government spending significantly affects increasing public debt. Over time, continued government expenditure without corresponding revenue generation or fiscal discipline has contributed to persistent budget deficits and Ghana’s public debt accumulation.

The findings further show that domestic savings did not have a short-run significant impact on public debt. This suggests that, in the immediate term, changes in domestic savings do not have a noticeable effect on public debt levels. However, the observed 1% increase in domestic savings potentially reducing public debt by 0.14% in the short run may imply that there might be some impact of domestic savings on public debt, although not significant in the short run. This finding is expected and supports Chenery & Strout’s (Citation1967) economic reasoning regarding the necessity for higher savings, which invariably reduces the government’s debt burden. In domestic savings, the theory suggests that if households and businesses increase their savings, more funds will be available for investment. With higher domestic savings, the supply of loanable funds increases, which can help meet the government’s borrowing needs without causing a significant increase in interest rates. The results are similar to existing studies of Poterba and Summers (Citation1987), Akram (Citation2011), and Shah and Pervin (Citation2012).

5.6. Residual diagnostics tests

Table displays diagnostic tests for residual analysis of the model. The ARDL model yielded an R-square value of 0.8829, indicating a reasonably good fit. The absence of autocorrelation in the residuals (or errors) was confirmed by the Durbin-Watson statistics value of 2.06. Moreover, the root mean square error (RMSE) of 0.1310 suggests a strong model fit to the data, with smaller prediction errors. The projected Ramsey reset test (χ2 Ramsey reset) confirmed the correctness of the functional form of the estimated model. Furthermore, the LaGrange multiplier test for heteroscedasticity (χ2 ARCH) resulted in a value of 2.670 (P-value = 0.1022), indicating no significant evidence of heteroscedasticity. Similarly, the LaGrange multiplier test for serial correlation (χ2SC) yielded a value of 0.169 (P-value = 0.6810), indicating no substantial presence of serial correlation. Additionally, the Shapiro-Wilk test of normality (χ2 Normality) obtained a chi-square value of 0.962 (P-value = 0.534), satisfying the assumption of normality of errors. Consequently, the diagnostic tests for serially uncorrelated errors, normality, and heteroscedasticity were all satisfied at a 5% significance level.

Table 10. Diagnostic tests

5.7. Stability check

Every economy experiences structural changes that make it extremely difficult for a nation, industry, or market to function. Significant economic advancements can prompt these changes and are often driven by innovation. The dynamism within the system is crucial in bringing about fundamental change. Various factors can contribute to structural transformation, such as technological advancements, new economic trends, global shifts in labour and capital markets, changes in resource availability, shifts in supply and demand, and changes in the political environment. In addition to these factors, other reasons frequently triggering structural change include new economic advancements, global shifts in labour and capital markets, and adjustments in resource availability due to conflict or natural disasters.

Ghana has experienced other instances of structural change. One such instance was the discovery of oil reserves in the country, which led to a significant transformation in its economy. The development of the oil industry brought about changes in investment patterns, job opportunities, and the overall economic landscape of Ghana. Furthermore, Ghana has also faced structural changes due to shifts in global commodity prices. Fluctuations in the prices of key exports, such as cocoa, gold, and timber, have impacted the country’s economy. These price changes have necessitated adjustments in production strategies, trade patterns, and government policies to ensure economic stability and growth.

Consequently, the general economic outlook for Ghana seemed optimistic. Nevertheless, in 2020, the nation experienced a severe economic setback triggered by the global COVID-19 pandemic. As a result, the real GDP per capita plummeted to its lowest point since 2007. The COVID-19 crisis disrupted economic activities, risking global progress in promoting shared prosperity and reducing poverty.

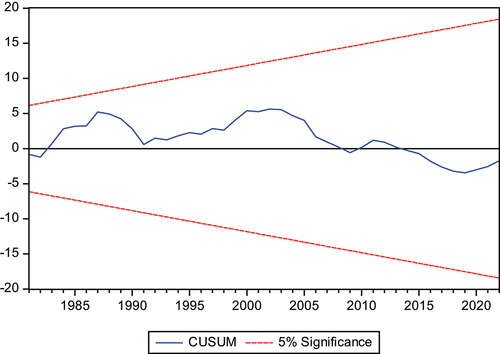

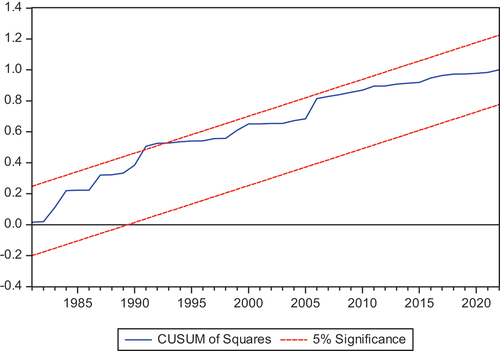

Considering these structural changes and their influence on economic parameters is crucial when analysing macroeconomic data. Therefore, employing techniques like the CUSUM and CUSUMSQ tests becomes important to verify the stability of regression coefficients and ensure the robustness of estimates. These tests can swiftly identify even the slightest variations from the mean values, helping to highlight structural changes in the model over time. Furthermore, one can determine if structural breaks have occurred by analysing the cumulative total lines and comparing them to the lower and upper critical levels. The result of the CUSUM (Figure ) and CUSUMSQ (Figure ) tests in the case of Ghana suggests that the coefficients in the model are persistent across time, indicating robust estimation and consistency in the regression model.

Figure 8. plot of CUSUM for coefficients’ stability of ARDL model. Source: authors’ estimates from data 1970–2022.

Figure 9. plot of CUSUMSQ for coefficients’ stability of ARDL model. Source: authors’ estimates from data 1970–2022.

6. Conclusion and policy implications

Based on the study findings, several conclusions can be drawn regarding the relationship between various factors and public debt in Ghana.

Firstly, the study confirms the presence of a long-run relationship between variables, indicating that an error correction model (ECM) should be constructed to account for short-run dynamics. The estimated coefficient of the ECM suggests that any deviation from the short-run equilibrium between variables and public debt can be rectified and restored annually at a rate of 1.80% in the long run.

The findings reveal that Ghana’s heavy reliance on external trade increases public debt. An increase in merchandise trade in Ghana significantly increases public debt, indicating a positive relationship between trade and public debt. This implies that as trade in goods and services grows, it puts upward pressure on the country’s public debt.

Investment in fixed assets, such as infrastructure projects, contributes to the accumulation of public debt. There is a significant positive long-run relationship between gross fixed capital formation (growth) and public debt, implying that as the economy grows and more capital is invested in fixed assets, public debt also increases.

Interest payments represent a significant portion of the government’s annual budget expenditure. As a result, higher interest payments contribute to further accumulating public debt over the long term. This suggests that when the government’s revenue generation falls short of covering the debt servicing costs, it may borrow more or allocate a larger portion of its budget to debt servicing, leading to further debt accumulation.

The study also reveals a negative significant long-run relationship between the budget deficit and public debt. But conversely, an increase in the government’s budget deficit leads to a decrease in public debt in the long run. The potential positive effects of government deficit financing on economic growth and fiscal sustainability can explain this counterintuitive relationship.

Domestic savings alone do not significantly impact the level of public debt in the long run in Ghana. Other factors, such as government spending, external borrowing, fiscal policies, trade, interest payments, and budget deficits, substantially influence public debt levels.

Policy implications can be drawn from these findings. Firstly, Ghana should focus on diversifying its economy and reducing its dependence on external trade to mitigate the impact of trade-related public debt accumulation. This could involve promoting domestic industries and reducing reliance on imported goods.

The government should carefully manage its investment in fixed assets and ensure that the expected economic benefits outweigh the increase in public debt. This may involve prioritising infrastructure projects based on their long-term economic growth and revenue generation potential.

Efforts should be made to reduce the burden of interest payments on public debt. This could include exploring options for refinancing or renegotiating debt terms to reduce interest rates and extend repayment periods. Additionally, measures should be taken to improve revenue generation and reduce reliance on borrowing to cover debt servicing costs.

The government should continue to monitor and manage budget deficits effectively. While deficit financing can be useful in certain economic situations, it should be accompanied by measures to stimulate economic growth and ensure fiscal sustainability. Careful budget planning and implementation are crucial to avoid excessive borrowing and the accumulation of public debt.

The government should create an enabling environment for savings and investment to promote domestic savings. This could involve implementing policies encouraging savings, improving financial literacy, and addressing any structural barriers hindering savings mobilisation.

The findings suggest Ghana needs a comprehensive and balanced approach to managing its public debt. This includes promoting economic diversification, prioritising infrastructure investments, managing interest payments, and ensuring responsible fiscal management. By implementing these policies, Ghana can work towards achieving debt sustainability and long-term economic growth.

Acknowledgments

The author sincerely thanks the editorial board and anonymous reviewers for their invaluable suggestions.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Data availability statement

The online repositories listed below provide access to all the pertinent data utilised for the analysis:

(1) Ghana Ministry of Finance and Economic Planning (https://mofep.gov.gh/public-debt/debt-data): This website provides access to debt data for Ghana. One can access data on public debt, including debt levels, composition, and servicing.

(2) Bank of Ghana (https://www.bog.gov.gh/economic-data/): The website of the Bank of Ghana offers economic data for Ghana. It includes a wide range of information, such as monetary indicators, exchange rates, inflation rates, balance of payments, and other macroeconomic data. The central bank of Ghana maintains this repository.

(3) World Bank (https://data.worldbank.org/country/GH): The World Bank’s website provides data on various aspects of Ghana’s economy and development. It covers various indicators, including economic, social, and environmental data. In addition, you can access information about GDP, poverty rates, education, health, infrastructure, and more.

Additional information

Notes on contributors

Ibrahim Musah

Ibrahim Musah is a practicing Development Planner and Economic Development Policy Analyst at the National Development Planning Commission of Ghana. He holds a bachelor’s degree in Development Management from the University for Development Studies, Ghana, and a master’s in Development Policy and Planning with Economic Development Policy as his specialization from the Kwame Nkrumah University of Science and Technology, Ghana. He is at present on his PhD programme in Planning at the Kwame Nkrumah University of Science and Technology, Ghana. Mr. Musah specializes in Econometric research; Data Analytics; Monitoring and Evaluation (M&E); Policy Analysis; and Local Economic Development (LED). His research interests focus on Economic Analysis, Macroeconomics, Micro-Economics, International Trade and Development Economics.

References

- Ackah, C., & Lambon-Quayefio, M. P. (2020). Confronting low domestic savings in Africa. Retrieved December 11, 2022. Available at: https://isser.ug.edu.gh/confronting-low-domestic-savings-africa

- Aizenman, J., & Ito, H. (2020). US macro policies and global economic challenges (no. w28232). National Bureau of Economic Research.

- Akram, N. (2011). Impact of public debt on the economic growth of Pakistan. The Pakistan Development Review, 50(4II), 599–29. https://doi.org/10.30541/v50i4IIpp.599-615

- Amankwah, G., Ofori-Abebrese, G., & Kamasa, K. (2018). An empirical analysis of the sustainability of public debt in Ghana. Theoretical Economics Letters, 8(11), 2038.