?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

This study uses a unique dataset of transactions at the account level to construct investor networks. These networks are then analyzed to examine the role of the network centralization index in identifying the stock momentum stages. The empirical results demonstrate that the early stage strategy of purchasing winner stocks with a low centralization index and selling loser stocks with a high centralization index outperform the simple momentum strategy. Conversely, the late-stage strategy of buying winner stocks with a high centralization index and selling loser stocks with a low centralization index underperforms the simple momentum strategy. Unlike prior research, the momentum effect in the Taiwanese stock market is particularly evident with an early stage strategy. Additionally, the regression analysis shows that the interaction between past cumulative returns and the centralization index significantly influences future returns, even after controlling for liquidity and investor attention variables. The impact of arbitrage frictions on momentum profits across different holding periods was also examined, with early stage strategies proving profitable for stocks facing severe arbitrage constraints. Moreover, this study investigates the influence of investor sentiment and market state on momentum, finding that early stage strategies perform better following periods of high sentiment and up-market states. Utilizing information networks can facilitate the identification of stock momentum stages.

Impact Statement

This research advances the understanding of momentum strategies in the Taiwanese stock market by examining investor behavior through information networks. Prior studies have struggled to observe the effects of momentum in Asian markets. However, this study innovatively uses the centralization index within investor networks to identify early-stage and late-stage momentum stocks. The findings show that early-stage momentum portfolios achieve significant price continuation. In contrast, late-stage portfolios do not exhibit significant momentum. The empirical results also highlight the importance of information diffusion patterns, arbitrage constraints, and investor sentiment in driving momentum profits. By leveraging information networks, the study contributes to the literature by providing a new lens to explain momentum profits, addressing the gap in previous research on the link between information flow and momentum. The findings have significant implications for investors and researchers, as they underscore the potential of information networks as a valuable tool for understanding market dynamics and enhancing investment strategies. The research also highlights the role of word-of-mouth communication in influencing stock performance, enriching the broader discourse on information evaluation in stock markets.

1. Introduction

A major challenge in financial research is understanding the cross-sectional dynamics of price momentum (Jegadeesh & Titman, Citation1993; Citation2001; Citation2023). To account for the variation in momentum profits, Hong and Stein (Citation1999) develop a theoretical model positing that early momentum traders can achieve considerable profits by trading shortly after significant news impacts the market. Conversely, late momentum traders suffer losses by purchasing at a point when prices have responded excessively to news. Hence, identifying the momentum stage of stocks is of utmost importance for determining the profitability of momentum strategies.

Lee and Swaminathan (Citation2000) proposed the momentum life cycle hypothesis. According to their hypothesis, investors commonly neglect early winner stocks with low transaction volumes and favor early loser stocks with high volumes, thereby intensifying the momentum effect. By contrast, investors are inclined to pursue late-winner stocks with high volumes and avoid late-loser stocks with low volumes, consequently mitigating the momentum effect. While trading volume can signify investor favoritism or negligence, thus aiding in identifying a firm’s stage in the momentum life cycle, deeper insight is achievable through the examination of investor behavior in information sharing. Numerous global studies (e.g. Asness et al., Citation2013; Chui et al., Citation2010; Griffin et al., Citation2003) have found that momentum strategy performance is relatively weak in Asian markets. Accordingly, this study explores the momentum effect in the Taiwanese stock market through the lens of information networks.

This study extracts information from investor networks in order to identify the stages of stock momentum. We examine the degree of investors’ favoritism or negligence towards particular stocks by using the concentration of information diffusion among them. Ozsoylev et al. (Citation2014) propose an empirical investor network model (EIN), where a connection between two traders in the network is established if they have repeatedly engaged in trading the same stock in the same direction over a brief period of time. They also suggested that the EIN can be centralized or decentralized, representing two distinct channels of information dissemination. In a decentralized network, information is more dispersed and investors are more likely to overlook that stock. In a centralized network, information is more concentrated and investors are more likely to show favoritism towards that stock.

We utilized the centralization index, initially introduced by Freeman (Citation1979), to quantify the concentration of information diffusion within a network. Using the centralization index level of each stock’s investor network, we classify firms into centralized (low centralization index) and decentralized (high centralization index) categories. To evaluate the effectiveness of the centralization index in detecting stock momentum stages, we created strategies for both early- and late-stage momentum. The early stage strategy involves buying past winner stocks with a low centralization index and selling past loser stocks with a high centralization index. In contrast, the late-stage strategy entails buying past-winner stocks with a high centralization index and selling past-loser stocks with a low centralization index. Moreover, we apply both non-directional and directional network approaches to calculate centralization indices based on eigenvector centrality and directed degree centrality. This dual approach enables us to explore whether the effectiveness of the centralization index in identifying momentum stages is affected by the directionality of the information flow.

We examine the predictability of the centralization index for cross-sectional returns among various momentum strategies. This study consists of three parts. First, we form simple momentum portfolios by using Jegadeesh and Titman (Citation1993) procedure. Our analysis reveals an absence of notable short-term momentum profits in the Taiwanese stock market, a finding that is consistent with the results reported by Chui et al. (Citation2010). However, we observe that the early stage momentum portfolio, created by the centralization index, displays significant price continuation with an average annual return of approximately 11%, whereas the late-stage momentum portfolio exhibits no significant momentum effect. These findings hold for both eigenvector and directed degree centralization indices. Our portfolio-based approach remains robust even when accounting for value-weighted returns and alternative portfolio formation methods. Furthermore, our Fama and MacBeth (Citation1973) regression analysis indicates that after controlling for variables related to liquidity and investor attention, the interaction between past cumulative returns and the centralization index significantly impacts future stock returns.

Second, we examine whether the degree of arbitrage constraint affects momentum profits across different holding periods. To gauge the severity of arbitrage friction for each firm, we developed arbitrage friction index. Our results suggest that early stage momentum strategies created by the directed-degree or eigenvector centralization index can generate significant momentum profits for stocks facing severe arbitrage constraints. Conversely, the same strategies do not generate substantial momentum profits for stocks that experience low arbitrage friction. This finding indicates that less arbitrage activity may hinder the correction of mispricing and increase momentum profit.

Finally, we explore whether momentum can be attributed to investor sentiment or the market state. To this end, we employ Taiwan Consumer Confidence Index to differentiate between periods of high and low sentiment. We find that early stage momentum strategies tend to perform better following periods of high sentiment. This result aligns with Antoniou et al. (Citation2013) argument that momentum occurs mostly following periods of optimism because investors tend to underestimate the impact of negative news. Moreover, following Cooper et al. (Citation2004), we differentiate between varying market conditions and find that momentum profits are only substantial following upmarket states.

The uniqueness of our data and the scope of our analyses enable us to make several contributions to extant research. First, momentum effects are observed in the Taiwanese market. Prior studies by Hameed and Kusnadi (Citation2002) and Du et al. (Citation2009) do not find significant effects in Taiwan or other East Asian stock markets. Despite expanding their investigations to encompass a broader range of Asian markets, Griffin et al. (Citation2003) and Chui et al. (Citation2010) failed to identify short-term momentum effects. Identifying early stage stocks using information networks appears to be a potential solution to this challenge. Second, this study represents the first attempt to explain momentum profits using information networks. While previous literature suggests that the exchange of private information may be related to momentum, it fails to present a clear causal mechanism between information flow and momentum (e.g. Hong et al., Citation2000; Hou & Moskowitz, Citation2005; Verardo, Citation2009). Finally, our research contributes to recent studies examining the impact of information evaluation on stock markets, particularly by utilizing information networks as a model for understanding information diffusion (e.g. Colla & Mele, Citation2010; Han & Yang, Citation2013; Ozsoylev & Walden, Citation2011; Walden, Citation2019). Our analyses suggest that word-of-mouth plays a role in momentum profits.

The remainder of this paper is organized as follows. Section 2 reviews the literature and develops our hypotheses. Section 3 describes the data and provides the summary statistics. Section 4 compares the profitability of simple momentum strategies with both early- and late-stage strategies. Section 5 conducts cross-sectional analyses and examines the impact of arbitrage limits on early stage momentum strategies. Finally, Section 6 concludes the paper.

2. Literature review and hypotheses development

Since Jegadeesh and Titman (Citation1993) documented the momentum effect in stock returns, numerous studies have explored variations in momentum profitability across countriesFootnote1 or asset classes.Footnote2 Many studies have proposed different theoretical models to explain the cross-sectional and time-series variations in momentum profits. Daniel et al. (Citation1998) suggest that short-term momentum profits result from market-delayed overreaction, while Barberis et al. (Citation1998), Hong and Stein (Citation1999), and Jegadeesh et al. (Citation2023) characterize the short-term momentum effect as a market underreaction. Numerous studies have empirically supported these theories of delayed reaction and underreaction (e.g. Chen & Lu, Citation2017; Cooper et al., Citation2004; Hong et al., Citation2000; Hong & Stein, Citation2007 Asem & Tian, Citation2010; Lee & Swaminathan, Citation2000). However, the literature still lacks a comprehensive understanding of the timing for shifts between price momentum and reversal, crucial for momentum strategy profitability. As a result, Lee and Swaminathan (Citation2000) proposed the momentum life-cycle hypothesis, explaining how momentum evolves from underreaction to overreaction throughout a cycle.

Lee and Swaminathan (Citation2000) hypothesize that trading volume illuminates the dynamics of momentum and reversals, positing that stocks undergo cycles of favoritism or negligence. They find that investors are more likely to overlook winning stocks with low turnover ratios, instead preferring early-stage losers with high turnover ratios. Their findings indicate that the returns of low-turnover winners and high-turnover losers persist strongly, but the returns of high-turnover winners and low-turnover losers exhibit weak price continuation. The former belongs to the early stage, in which momentum profits are mainly caused by investors’ underreaction to news; the latter belongs to the late stage, in which momentum profits are derived from investors’ delayed overreaction. Following this hypothesis, Liu et al. (Citation2020) employ options-implied data to identify the momentum stage of stocks, evaluating the performance of early- and late-stage momentum strategies in the US market. Furthermore, Bornholt et al. (Citation2015) and Li and Wei (Citation2016) document the applicability of the momentum life cycle hypothesis to markets in an international setting. According to their findings, identifying the momentum stages of stocks is essential for determining momentum profits.

The dissemination of information among investors can be used to identify their favoritism or negligence. Ozsoylev et al. (Citation2014) propose an empirical investor network model (EIN). Each pair of connected investors in the network indicates that they traded the same stock in the same direction many times within a small time window. They also indicated that EIN represents two channels of information dissemination. The dissemination mechanism of the decentralized network is through word-of-mouth between investors and Internet discussion boards. Another centralized dissemination channel is through different mainstream media. If the first channel drives the information network of a stock, information dissemination is more dispersed, and investors are more likely to ignore this stock. In contrast, if the second channel drives the information network of a stock, information dissemination is more concentrated, and investors are more likely to favor this stock.

The centralization index is used to measure the degree of concentration of information dissemination in the network, and it may serve as a good proxy for identifying investors’ favoritism or negligence of a certain stock. Based on the momentum life cycle hypothesis, we expect that investors are more likely to ignore low-centralization winner stocks and favor high-centralization loser stocks. This behavior amplifies the momentum effect. Conversely, investors are more likely to pay attention to high-centralization winner stocks and ignore low-centralization loser stocks. This behavior dampens the momentum effect. Thus, we developed the following hypothesis:

Hypothesis 1: Decentralized winners and centralized losers exhibit persistent and significant price continuation, while centralized winners and decentralized losers exhibit weaker price continuation.

Hypothesis 2: The momentum profit from decentralized winners and centralized losers is much higher when arbitrage friction is more severe.

Hypothesis 3: Momentum profits are more notable following periods of higher market sentiment.

3. Data and methodology

3.1. Data description

Our sample consists of all companies listed on the Taiwan Stock Exchange (TWSE) from January 2005 to December 2014. Each company included in the sample must have had at least 2 years of data available before portfolio formation. Our data primarily originate from two sources: the Taiwan Economic Journal (TEJ) and TWSE account-level intraday data. The TEJ database provides stock market price information, including closing prices, trading volumes, shares outstanding, and monthly stock returns. To ensure sufficient liquidity, we did not consider stocks with market capitalization below the 5% TWSE threshold.Footnote4 Moreover, to evaluate the historical performance of stocks and construct portfolios based on momentum strategy, it is necessary to have a minimum of 2 years of return history for each stock. Additionally, the TEJ provides us with various firm characteristics including size, book-to-market ratio, number of shareholders, and institutional ownership. Idiosyncratic volatility is the standard deviation of the market model residuals calculated from daily returns over the previous month, where daily stock returns are the dependent variable and market returns are the independent variables. In our subsequent cross-sectional analyses, we controlled for both firm characteristics and liquidity measures. Three liquidity metrics are considered: turnover rate (average monthly shares traded relative to shares outstanding), dollar volume (average monthly trading volume in dollars), and Amihud (Citation2002) illiquidity ratio (monthly average of absolute daily returns normalized by daily dollar trading volume).

We also collect comprehensive transaction records for all investors from the TWSE. This dataset includes details such as the date and time of each trade, stock ID, number of shares traded, transaction price, direction of trade (buy or sell), account ID, and trader identity. To ensure accuracy, all transaction prices are adjusted to account for dividend payments. By utilizing account-level intraday trading data, investor networks that serve as benchmarks for portfolio formation are developed.

To measure investor sentiment, we use the monthly time series of consumer confidence sentiment constructed by the Research Center for Taiwan Economic Development. We manually compiled the monthly Consumer Confidence Index reports and extracted the monthly scores of consumer confidence sentiment from the reports.Footnote5 The Taiwan Consumer Confidence Index survey is conducted via telephone interviews using computer-assisted random sampling. Participants are asked about their outlook on six economic aspects: employment opportunities, domestic economic conditions, price levels, the timing for investing in stocks, the purchasing timing for durable goods, and family financial situations. The score for each question is calculated by dividing the number of positive responses by the total number of positive and negative responses. The scores from all six questions are then combined to form the overall Consumer Confidence Index.

3.2. Network construction

Our methodology involves creating an Empirical Investor Network (EIN), a modified version of the method developed by Ozsoylev et al. (Citation2014). In this network, a connection between any two investors (i and j, where j ≠ i) signifies that these investors executed at least three trades of the same stock, in the same direction (buy or sell), within a specified time frame Δt over a month. To represent the graph of the investor network, we use an asymmetric adjacency matrix,Footnote6 A ∈ N × N, where N is the number of investors in the network. For example, the entry Aij = 1 indicates that investor i is connected with investor j, and every connected trade of investor i is always earlier than that of investor j. Conversely, the entry Aij = 0 represents that investor i is not connected with investor j.

Similar to Chung et al. (Citation2018), we employed four centrality measures. The first measure is degree centrality, introduced by Freeman (Citation1979). Degree centrality can be categorized into in-degree and out-degree measures. The indegree measure of an investor, denoted as i, indicates the amount of information received by that investor, and can be used to determine the direction of information flow. Mathematically, this can be expressed as follows:

(1)

(1)

Furthermore, an outdegree measure of investor i reflects the amount of information that he/she offers. This can be formulated as follows:

(2)

(2)

The following centrality measure is a composite of the above two measures, aimed at describing investors’ informational advantages:

(3)

(3)

The directed degree centrality measure can provide a more precise assessment of an investor’s information advantage.

In addition, we utilize eigenvector centrality (Bonacich, Citation1972), which refers to the value of the primary eigenvector E. It is mathematically defined as follows:

(4)

(4)

where λ is the principal eigenvalue and the i-th entry of the eigenvector corresponds to the centrality for investor i. Specifically, the i-th component of the eigenvector represents the centrality measure for investor i. The definition of eigenvector centrality suggests that if investor i is connected to numerous other investors or a few highly influential ones, they will become more influential or centrally positioned. The representation in vector form implies that the largest eigenvalue λ corresponds to the eigenvector with the highest eigenvector centrality.

Centrality measures are used to assess an investor’s position in a network that is specific to the firm. Nonetheless, to identify central investors, another measure is required to describe the complete network structure. Hence, we employed centralization (Freeman, Citation1979) to describe the degree of centralization in a network relative to a perfectly centralized star network. Centralization is computed as the sum of the disparities in centrality divided by the maximum feasible sum of disparities in centrality, and can be represented as follows:

(5)

(5)

where the centralization index

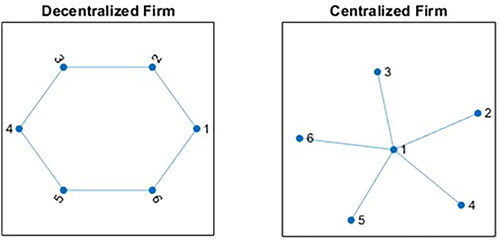

serves as a measure for quantifying the concentration of information diffusion in firm j. We employ the aforementioned centrality measures to determine the directed degree and eigenvector centralization indices for each firm. illustrates instances in which leaders are both present and absent. Investors tend to be more isolated from their peers in decentralized networks. Conversely, centralized networks feature a denser cluster of influential investors, who play a key role in relaying information to others. Similar to Chung et al. (Citation2018), we develop an investor network for each firm, classifying them as highly centralized or decentralized, based on the centralization index. Decentralized firms typically have a smaller proportion of central investors than centralized firms do, which have a greater propensity to attract the attention of other investors.

Figure 1. Illustration of decentralized versus centralized firms. Empirical investor networks delineate various network structures. Each node represents the identification code for an investor. Six investors are arbitrarily selected from distinct company-specific networks. For each connected investor pair in the network (i, j ≠ i), it represents that they traded the same stock in the same direction (buy or sell) a minimum of three times within a time window of Δt during a month. The decentralized and centralized network graphs are illustrated in the left and right figures, respectively.

With these two network structures, firms with a decentralized network structure are less effective at disseminating information, leading to a higher probability of investors overlooking their stock. Conversely, companies with centralized network structures exhibit greater efficiency in disseminating information, which can result in investors demonstrating a higher level of favoritism towards their stocks. To assess the impact of information diffusion on momentum strategies, we create portfolios using the simple momentum strategy, as well as early- and late-stage strategies. We then compare the performance of these portfolios.

3.3. Summary statistics

provides a detailed summary of the primary firm-specific variables used. The data cover the period from January 2005 to December 2014. We note that each observation in our sample is at the firm-month level, averaging around 534 monthly firms. Cross-sectional statistics were initially calculated on a monthly basis and subsequently averaged over the entire sample period. Panel A presents the time-series averages of the cross-sectional statistics, including the directed-degree and eigenvector centralization indices. Notably, both indices exhibit mean values ranging between 0 and 1, with directed-degree and eigenvector centralization indices averaging at 0.06 and 0.07, respectively. The mean and median of the centralization values are very close to each other in both directed and undirected networks. Moreover, the low values of these statistics suggest that the proportion of central investors in the network is relatively low.

Table 1. Summary statistics.

A descriptive statistical analysis of firm characteristics reveals several noteworthy insights from . First, the average value of the beta coefficient is 0.95, indicating that the stock price movements of most companies are highly correlated to market trends. Second, the average market value of the sample companies reached NT$34.15 billion, indicating that our sample mainly comes from the Taiwan Stock Exchange, where the market value generally exceeds the over-the-counter market’s average market value of NT$3.06 billion.Footnote7 Third, the average book-to-market value ratio is 0.87. This ratio, being less than 1, may reflect that the Taiwan market is predominantly led by high-tech and high-growth companies. Fourth, the average idiosyncratic volatility is 0.02, showing a minimal impact of firm-specific events on companies. Lastly, the average monthly return is 2%, but due to the inclusion of the financial crisis in the sample period, the standard deviation reached 11%, indicating a higher volatility in returns.

Panel B reports the time-series averages of the cross-sectional Pearson correlations between these variables. The table indicates a significant and positive correlation between the directed-degree and eigenvector centralization indices and variables measuring investor attention. This finding suggests that firms with higher centralization tend to attract more investor interest. Conversely, a negative relationship is observed between centralization indices and liquidity metrics, implying that firms with centralized structures may experience less liquidity than those with decentralized structures. This finding is consistent with the idea that liquidity risk is often elevated in markets with concentrated ownership or influence. Overall, our analysis underscores the significance of centralization indices for understanding the dynamics of investor attention and liquidity in stock markets.

4. Baseline results

This section focuses on testing the first hypothesis, that winner stocks with a low centralization index and loser stocks with a high centralization index exhibit pronounced price continuation. Section 4.1 presents the returns of the simple momentum strategy. Section 4.2 examines the profitability of both early- and late-stage momentum strategies and compares them to the simple momentum strategy. Section 4.3 reports an overview of annual returns for all momentum strategies. Section 4.4 outlines the empirical results of various robustness checks conducted to validate our findings.

4.1. Momentum portfolio results

Our momentum strategy is developed in accordance with the method proposed by Jegadeesh and Titman (Citation1993). The stocks are sorted at the end of each month based on their cumulative returns over the past 6 months, with the lowest returns ranking first. Subsequently, these stocks are evenly distributed into three portfolios.Footnote8 These portfolios are held for K months, where K varies by 3, 6, 9, or 12 months. To mitigate issues such as bid-ask bounce and lead-lag effects, a delay of 1 month is applied between the end of the portfolio formation period and beginning of the holding period. Stocks in the bottom third are placed in the loser portfolio, whereas those in the top third form the winner portfolio. The momentum strategy, termed MOM, involves buying a portfolio of winner stocks and selling a portfolio of loser stocks.

presents raw and risk-adjusted portfolio returns for the simple momentum strategy. These returns are calculated based on the cumulative returns over various holding periods. We use the Newey and West (Citation1987) correction for autocorrelations when computing t-statistics to account for autocorrelations caused by overlapping observations (Boudoukh et al., Citation2019; Citation2022; Hodrick, Citation1992; Valkanov, Citation2003). The winner-minus-loser portfolios across different holding periods (K = 3, 6, 9, and 12 months) are not significant. The average raw returns of the portfolios range from approximately −0.17% to 0.33%. To assess whether these return differences are attributable to systematic risk factors, we also provide monthly portfolio alphas, adjusted using the CAPM factor and the Fama and French (Citation1993) three-factor models. However, the difference in returns between the risk-adjusted winner and loser portfolios remains non-significant across different holding horizons. This result aligns with the findings of Du et al. (Citation2009) and Chui et al. (Citation2010) that the momentum effect is not pronounced in the Taiwanese market. Furthermore, portfolio returns tend to reverse for longer holding periods.

Table 2. Returns for the simple momentum strategy.

To evaluate the applicability of the momentum life cycle hypothesis in the Taiwan stock market, we assessed the performance of the turnover-based momentum strategy. Stocks are sorted into three portfolios based on their prior 6-month cumulative returns. They are further divided into terciles according to their average monthly turnover ratios over the previous 6 months. We formed an early-stage (late-stage) momentum strategy by buying winning stocks with low (high) turnover ratios and selling losing stocks with high (low) turnover ratios.

shows the time-series average of monthly returns for each strategy and provides difference tests between the early- and late-stage momentum strategies with the simple momentum strategy. The early-stage momentum strategy exhibits price persistence for a 1-month holding period, but the average monthly returns for other holding periods are not significant. The late-stage momentum strategy shows weak price reversals for most holding periods, yet the average monthly returns are mostly insignificant. Compared to the average monthly returns of the simple momentum strategy, the early-stage momentum strategy significantly outperforms the simple momentum strategy for a 1-month holding period. In contrast, there is no significant difference in average monthly returns between the late-stage momentum strategy and the simple momentum strategy. These findings indicate that in the Taiwanese stock market, stocks in early momentum portfolios show price persistence in the short term, while stocks in late momentum portfolios do not show significant price reversals. These results suggest that the interaction of turnover ratios and past cumulative returns did not generate significant momentum profits. Therefore, alternative methods to identify momentum stages may need to be explored. Consequently, we investigate the profitability of network-based momentum strategies in the subsequent subsections.

Table 3. Returns for the turnover-based momentum strategies.

4.2. Profitability analysis of the early-stage strategies

To construct portfolios of stocks with high and low past returns, we further divide these portfolios into three subgroups based on their network centrality indices. The early stage directed-degree (DD) strategy entails purchasing winner stocks with a low directed-degree centralization index and selling loser stocks with a high directed-degree centralization index. Similarly, the early stage eigenvector strategy (EIG) involves buying winner stocks with a low eigenvector centralization index and selling loser stocks with a high eigenvector centralization index.

presents the average monthly returns and t statistics for the directed-degree and eigenvector early-stage momentum strategies over holding periods of 3, 6, 9, and 12. The directed-degree momentum strategy yields an average monthly return of 0.98% with a t-statistic of 2.26 for a 1-month period. We also calculate risk-adjusted returns relative to the CAPM and the Fama and French (Citation1993) three-factor models. The alpha for the three-factor model stands at 1.04% monthly with a t-statistic of 2.62, aligning closely with the CAPM alphas. These alphas are statistically significant across the 3-, 6-, 9-, and 12-month holding periods. Beyond the directed-degree strategy, the eigenvector strategy produces significant returns for up to 12 months. For example, over 6 months, stocks with low eigenvector centrality outperform those with high centrality by 0.85% monthly or approximately 10% annually. This pattern holds for other holding durations. The CAPM alphas ranged from 0.82% to 0.95% per month across the holding horizons. The Fama-French three-factor alphas are comparable to, but slightly smaller in magnitude than, those of the CAPM alphas. Compare these results with those of the turnover-based momentum strategies in Section 4.1. We find that under all different holding period settings, both the magnitude and statistical significance of average returns of the network-based early-stage momentum strategies are superior to the turnover-based early-stage momentum strategy.

Table 4. Returns for the early-stage momentum strategies.

further compares the performance of various momentum strategies. We assess the performance differential between the directed-degree momentum strategy and the simple momentum strategy, with the former consistently outperforms across multiple holding periods. Similarly, the eigenvector momentum strategy demonstrates superior returns compared to the simple momentum strategy. Our study employs two network centralization measures to construct these momentum strategies. To determine which strategy has higher performance, we also conduct a differential test between the directed-degree and eigenvector momentum strategies. The results show no significant difference in returns between the two strategies, supporting the notion that directed-degree and eigenvector centralization provide interchangeable information for identifying momentum stages.

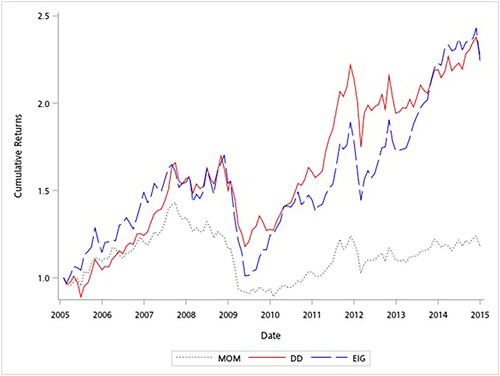

illustrates the compound returns of the various strategies from January 2005 to December 2014, starting with an initial investment of $1. Strategies include momentum, directed-degree momentum, and eigenvector momentum, with monthly portfolio rebalancing excluding transaction costs. The momentum strategy demonstrates negligible growth, maintaining a value near $1. Conversely, the directed-degree and eigenvector momentum strategies exhibited pronounced growth trends, culminating in $2.48 and $2.38, respectively. Notably, during the global financial crisis, all strategies experienced heightened volatility and momentum crashes (Daniel & Moskowitz, Citation2016), particularly the simple momentum strategy.

Figure 2. Compound returns for the momentum and centralization momentum strategies. Time-series patterns of compound monthly returns for the momentum (MOM; dotted line), directed-degree momentum (DD; solid line), and eigenvector momentum (EIG; dashed line) strategies. All stocks are ranked in ascending order at the end of each month based on their past-6-month cumulative returns. The stocks in the bottom one-third are assigned to the loser portfolio and those in the top one-third are assigned to the winner portfolio. The MOM represents a zero-investment portfolio that longs the winner portfolio and shorts the loser portfolio. The stocks in the winner and loser portfolios are further sorted into three subgroups based on their centralization index values: high, middle, and low centralization portfolios. DD represents a zero-investment portfolio that longs winners with low-directed-degree centralization and shorts losers with high-directed-degree centralization. EIG represents a zero-investment portfolio that longs winners with low eigenvector centralization, and shorts losers with high eigenvector centralization. The sample period is from January 2005 to December 2014.

The results summarized above provide several key insights. First, the simple momentum strategy has a negligible impact in terms of both magnitude and statistical significance. Second, early stage momentum strategies consistently outperform simple momentum strategies across various holding periods (K = 1, 3, 6, 9, and 12). This finding is consistent with our main hypothesis that stocks demonstrate significant and persistent price continuation in their early stages.

4.3. Profitability analysis of the late-stage strategies

presents the average monthly returns for the late-stage strategies. The late-stage directed-degree strategy (LDD) involves purchasing winner stocks with a high directed-degree centralization index and selling loser stocks with a low directed-degree centralization index. Similarly, the late-stage eigenvector strategy (LEIG) involves buying winners with a high eigenvector centralization index and selling losers with a low eigenvector centralization index. If centralization indices can facilitate the identification of momentum stages in stocks, it is hypothesized that the LDD and LEIG strategies will underperform compared with the simple momentum strategy. reveals that the returns for the LDD and LEIG strategies lack statistical significance throughout all the specified holding periods, suggesting a lack of noticeable price momentum or reversal. Furthermore, the performance of these strategies is compared with that of the simple momentum strategy in terms of return differentials. The differentials are consistently negative and statistically significant across all holding periods, except for the 12-month interval, where they are not significant. These findings imply that LDD and LEIG strategies could be instrumental in identifying stocks in the late stages of their momentum cycle.

Table 5. Returns for the late-stage momentum strategies.

4.4. Fama–MacBeth regressions

We employed a portfolio-based approach in the previous analyses to evaluate the predictability of future returns across various trading strategies. However, the interaction between cumulative past returns and the centralization index fails to consider additional variables that might significantly forecast future returns. To determine the influence of the interaction effect of cumulative past returns and the centralization index on future returns, we incorporate this interaction term in our estimation of the Fama–MacBeth regression models:

(6)

(6)

where the dependent variable is the return in the subsequent holding period.

represents the cumulative returns of firm i over the past 6 months, excluding the current month’s return.

is the centralization index of firm i. For stocks whose cumulative returns are in the top 50 percentile,

equals

for those in the bottom 50 percentile,

equals

The model incorporates both directed-degree and eigenvector centralization indices. Moreover,

represents a vector of explanatory variables that correlate with firm characteristics, including CAPM beta (β), the natural logarithm of market capitalization (ln(Size)), the book-to-market ratio (B/M), and the current 1-month return (Ret).

is a vector of investor attention variables, such as institutional ownership and number of shareholders. The liquidity vector (

) includes the natural logarithm of Amihud (Citation2002) illiquidity (ln(Illiquidity)), natural logarithm of turnover rate (ln(Turnover)), and natural logarithm of dollar volume (ln(Dvolume)). The error term is denoted by

For accuracy in our findings, t statistics are adjusted for heteroskedasticity and autocorrelation using Newey and West (Citation1994) method.

displays the mean coefficients from the Fama–MacBeth regressions, calculated using alternative specifications that incorporate varying combinations of control variables from EquationEq. (6)(6)

(6) . The coefficient of the interaction term was particularly significant. Our analysis reveals that when accounting for their interaction terms, neither cumulative returns nor the centralization index alone show substantial predictive power for future returns. This aligns with earlier findings on the limited predictability of centralization indices and the modest efficacy of the simple momentum strategy. To mitigate the influence of stock characteristics on the momentum and centralization indices, we include common firm characteristics, investor attention variables, and liquidity metrics in our regression models. Notably, the significance of the coefficients of the interaction term persisted even after the inclusion of these variables. Consequently, the results of the Fama–MacBeth regressions indicate that the interaction between past cumulative returns and the centralization index significantly contributes to the effectiveness of our proposed strategy.

Table 6. Fama–MacBeth cross-sectional regressions with centralization index.

4.5. Long-horizon portfolio returns

Our empirical analysis demonstrates that price reversals do not occur within the first year of holding an early stage momentum portfolio. This section delves into the returns following the holding period of both momentum and early stage portfolios, examining the possibility of price reversal post-portfolio formation. We define years 2, 3, 4, and 5 as the annual returns for four consecutive 1-year periods following portfolio formation. These annual portfolio returns are calculated by taking the average of the annual holding-period returns for the stocks in each portfolio, with each stock having equal weight.

presents the annual returns for various momentum strategies across holding periods ranging from 2 to 5 years post-formation. As shown in , the simple momentum strategy results in notably negative returns in Year 3, with returns becoming insignificant in the subsequent holding periods. By contrast, neither the directed degree nor the eigenvector momentum strategy demonstrates significant price reversals until Year 5. This suggests that the returns for these two early stage momentum strategies undergo reversals later than the simple momentum strategy.

Table 7. Post-holding-period returns for the various momentum strategies.

4.6. Robustness checks

In this subsection, we present a set of rigorous robustness checks for baseline analysis. Firstly, we verified whether varying the sample periods significantly impacted the empirical results of the traditional momentum strategy. This study updated the monthly stock returns and three-factor data from 2015 to 2023 to analyze the profitability of a simple momentum strategy during this period. shows the raw and risk-adjusted returns of portfolios using a simple momentum strategy between 2015 and 2023. From these empirical results, we observed that the raw returns of winner stocks were slightly greater than those presented in (sample period 2005–2014), while the returns of loser stocks were not statistically significant across all holding horizons. Similar to the findings in , the returns of momentum portfolios (winner minus loser) across different holding periods are also insignificant. The average raw returns of these portfolios range from 0.13% to 0.71%. Even after accounting for CAPM and the Fama and French (Citation1993) three-factor model, the risk-adjusted returns of the momentum portfolios remain insignificant. This result reconfirms that, even with the most current sample data, the traditional momentum strategy in the Taiwan stock market seems to be unable to generate significant momentum profits.

Table 8. Returns for the simple momentum strategy in the interval of 2015–2023.

Secondly, we verified whether varying the sample periods significantly impacted the empirical results of the network-based momentum strategies. Due to the restrictions on the Personal Data Protection Act, we could not update the most recent investor trading data to examine the profitability of network-based momentum strategies. Therefore, we divided the 10-year period into two sub-periods of 5 years each: 2005 to 2009 and 2010 to 2014, reassessing the stability and profitability of early-stage momentum strategies. presents the average monthly returns of early-stage momentum strategies within these two sub-periods. Comparing the results of Panel A (2005 to 2009) with Panel B (2010 to 2014), the performance of both directed-degree and eigenvector momentum strategies during the period of 2010 to 2014 is generally better than that of 2005 to 2009, which might be related to the influence of the financial crisis. Despite the impact of the financial crisis, early-stage momentum strategies still perform significantly better than the simple momentum strategy during the period from 2005 to 2009. Results in Panel B further confirm that, from 2010 to 2014, the average raw returns of early-stage momentum strategies are significantly superior to the simple momentum strategy for different holding periods. Moreover, testing the return differences between the directed-degree and eigenvector momentum strategies across different sample periods indicates no significant difference in average returns between the two strategies, further supporting the view that directed-degree and eigenvector centralization provide interchangeable information for identifying momentum stages.

Table 9. Returns for the early-stage momentum strategies in split intervals of 2005–2009 and 2010–2014.

The empirical results show that, across different subperiods, network-based momentum strategies yield significant profits, indicating a stable price continuation phenomenon. Furthermore, selecting stock market data from 2005 to 2014 would be ideal. During this period, market participants in the Taiwan stock market did not encounter significant shocks, such as changes in the national political landscape or disease outbreaks.Footnote9 Choosing this period as the sample timeframe allows for the exclusion of these contextual factors, enhancing the external validity of our research to other stock markets.

Thirdly, reports the value-weighted average returns and t statistics for a variety of momentum strategies with distinct holding periods ranging from K = 1, 3, 6, 9, and 12. Notably, for K = 1, the average raw return for the directed-degree (eigenvector) momentum strategy is 1.06% (0.91%) per month, with a t-statistic of 2.20 (1.96). Although the results are generally similar to our baseline findings, some robustness test results are comparatively weak and statistically insignificant. These results also imply that momentum profits are much stronger for small stocks than for large stocks, which is likely due to the high transaction costs and low liquidity of small stocks, which make it difficult to take advantage of arbitrage opportunities (Baker & Wurgler, Citation2006; Citation2007).Footnote10 Furthermore, difference tests indicate that early-stage momentum strategies tend to perform more favorably than simple momentum strategies over different holding horizons.

Table 10. Value-weighted returns for the various momentum strategies.

Finally, to ensure the robustness of our main findings, we conduct additional tests by altering the ranking benchmark to past-3-month cumulative returns and constructing portfolio holdings with different holding periods.Footnote11

reports the mean monthly returns across various momentum strategies, where stocks are sorted by 3-month cumulative returns. Our main findings remain stable. Both the directed-degree and eigenvector momentum strategies perform better than the simple momentum strategy under different holding horizons. Our results remain robust when value-weighted returns and alternative means of constructing portfolios are used.

Table 11. Returns for an alternative momentum strategy.

5. Further analysis of the information-diffusion effect

This section investigates the influence of arbitrage constraints and investor sentiment on the predictability of early stage momentum strategies.

5.1. Limits to arbitrage and momentum profits

Several studies (e.g. Gromb & Vayanos, Citation2010; Shleifer & Vishny, Citation1997) report that cross-sectional anomalies are more pronounced in firms with more severe arbitrage restrictions. The persistence of the momentum effect is attributed to arbitrage constraints that hinder price correction in the market. Moreover, momentum profits stemming from mispricing rather than risk premiums are amplified in firms facing greater arbitrage frictions. Consequently, this study analyzes the effect of arbitrage impediments on the returns of momentum strategies.

To examine the relationship between arbitrage friction and the performance of early-stage momentum strategies, we developed an arbitrage-friction index through principal components analysis,Footnote12 incorporating six firm-specific characteristics: idiosyncratic volatility, bid-ask spread, Amihud’s illiquidity measure, institutional ownership, shareholder count, and trading volume.Footnote13 This approach follows the methodologies Baker and Wurgler (Citation2006) and Schmeling (Citation2009) established. The process involves standardizing the characteristics to zero mean and unit variance, estimating the first principal component based on these variables and their lags, resulting in a 12-factor preliminary index. We refine this by focusing on the first principal component of the six variables’ correlation matrix, selecting leads or lags with the highest correlation for each variable, and adjusting the coefficients to standardize the index’s variance. After establishing the arbitrage-friction index, stocks are separated into two groups: high and low arbitrage friction, using the index’s median for separation. Using the dichotomy method, we further divide each group into four portfolios based on their past cumulative returns and centralization index. This segmentation approach is applied to both directed degree and eigenvector momentum strategies.

presents the findings of our early stage momentum strategies in relation to arbitrage friction. Our results demonstrate that both directed-degree and eigenvector momentum strategies yield substantial momentum returns through all holding durations for stocks with severe arbitrage restrictions, whereas low-arbitrage friction stocks do not exhibit comparable gains. The last two columns display the differential returns of the two strategies under conditions of high and low arbitrage constraints. Companies with severe arbitrage constraints exhibit greater momentum returns across all holding periods except for the 12-month period. Our results reveal that reduced arbitrage activity may hinder the correction of mispricing, thus increasing momentum profit.

Table 12. Limits to arbitrage and momentum returns.

5.2. Sentiment and momentum profits

We conduct a final test to investigate the impact of time-series variations on the performance of early stage momentum strategies. Antoniou et al. (Citation2013) suggest that following periods of high sentiment, investors become excessively optimistic about stock prices, whereas, following periods of low sentiment, they become excessively pessimistic, leading to cognitive dissonance and decelerated diffusion of negative and positive signals, respectively. In a related vein, Cooper et al. (Citation2004) demonstrate that investors are influenced by market conditions and alter their self-attribution bias and risk preferences accordingly, indicating that momentum profits are contingent on market conditions. Momentum profits are likely to be more substantial following upmarket periods. We suggest that a similar occurrence occurs with investor self-attribution bias and that early stage momentum strategies are affected by changing market conditions.

We conducted a test to investigate whether time-series variations affect the profitability of network-based momentum strategies. Following Antoniou et al. (Citation2013), who argue that investor sentiment is driven by periods of optimism and pessimism that impede the timely diffusion of signals, we applied the methodology of Wang et al. (Citation2021), using the Taiwan Consumer Confidence IndexFootnote14 to measure market sentiment and categorize the sample period into high- and low-sentiment periods.

Since we follow the methodology of Jegadeesh and Titman (Citation1993) to create overlapping momentum portfolios, we employ the classification technique of Antoniou et al. (Citation2013) to identify periods of high and low sentiment. Specifically, we classify each formation period as optimistic or pessimistic based on a weighted rolling average of the Consumer Confidence Index over the 3 months before the formation period’s end, assigning weights of 3, 2, and 1 to the sentiment scores of the last 3 months, respectively. A formation period is considered optimistic (or pessimistic) if its rolling average ranks in the top (or bottom) 30th percentile of our sentiment time series. Given the overlapping nature of our portfolios, each holding period includes stocks from several formation periods with different sentiments. To determine the average sentiment, we aggregate the counts of optimistic and pessimistic periods. If all formation periods in a holding month are either optimistic or pessimistic, the month is labeled accordingly; otherwise, it is deemed to reflect a ‘mild’ sentiment. We further investigate whether the momentum profits for each sentiment period differ from zero by regressing the time series of the average monthly returns on three dummy variables (optimism, mildness, and pessimism) without an intercept. Finally, we test whether the average returns following optimistic periods differ from those following pessimistic periods by regressing the time-series average monthly returns on optimism and mildness dummy variables with an intercept.

presents the average monthly returns generated by the directed-degree and eigenvector momentum strategies across high- and low-sentiment periods. Our findings indicate that network-based strategies tend to outperform high-sentiment periods, particularly for shorter holding periods. Notably, when K = 1, the directed-degree and eigenvector momentum strategies generated substantial monthly profits of 1.40% and 1.36%, respectively, following optimistic periods. In contrast, these profits decline sharply to 0.57% and 0.09%, respectively, following pessimistic periods. The observed differences in profitability remain statistically significant for K less than 9 months.

Table 13. Sentiment variation and momentum returns.

We explore whether momentum profits are influenced significantly by varying market conditions. To this end, we adopt Cooper et al. (Citation2004) method for classifying market conditions. Specifically, we classify the market condition as either ‘UP’ or ‘DOWN’ depending on whether the value-weighted market return for the 3-year period before the start of the holding period is positive or negative, respectively. shows the average monthly returns for these market states. Our findings suggest that momentum profits are significant only after UP states, which is consistent with Cooper et al. (Citation2004). Conversely, momentum profits are mostly insignificant following down states, except for the 12-month holding period. In general, our results indicate that momentum profits are highly susceptible to time variation.

Table 14. Market states and momentum returns.

6. Conclusion

This study sheds new light on the momentum effect within the Taiwanese stock market by dissecting the role of information networks in determining the momentum stages and subsequent profitability. We employ the centralization index derived from empirical investor networks to measure the level of information diffusion concentration that could potentially influence investors’ biases towards or against specific stocks.

The results of our study support the momentum life-cycle hypothesis proposed by Lee and Swaminathan (Citation2000), revealing that the early stage momentum portfolio exhibits strong price continuation, whereas the late-stage momentum portfolio does not demonstrate a significant momentum effect. These findings hold for both eigenvector and directed degree centralization indices. The results remain robust when value-weighted returns and alternative portfolio construction methods are used. Furthermore, the interaction between past cumulative returns and the centralization index significantly impacts future stock returns, even after controlling for liquidity- or investor-attention-related variables.

Our study further extends momentum analysis by incorporating arbitrage constraints and investor sentiment. We demonstrate that early stage momentum profits are enhanced in the presence of severe arbitrage constraints, indicating that less efficient correction of mispricing under such conditions amplifies momentum returns. Moreover, early stage momentum strategies tend to perform better following high-sentiment periods, particularly when holding a portfolio for a short period. This effect is also confirmed to be more pronounced following upmarket conditions, offering evidence that market states influence the magnitude of momentum profit.

This study provides a novel examination of the influence of network centralization on momentum profits, a perspective that has not yet been thoroughly examined in prior research. Through our analysis, we rigorously establish the critical importance of information networks in shaping momentum-investment strategies. Our analysis substantiates the pivotal role of information networks in momentum investing strategies and offers new insights into the conditions that facilitate or impede momentum profit. Our findings can be helpful to investors and market participants in making investment decisions.

Author contributions statement

Wen-Rang Liu: Conceptualization, Methodology, Software, Formal analysis, Validation, Writing – original draft, Writing – review & editing.

Data availability statement

The data that support the findings of this study are available on request from the corresponding author, W.R. Liu, upon reasonable request. The data are not publicly available due to the presence of information that may compromise privacy.

Disclosure statement

No potential conflict of interest was reported by the author.

Additional information

Funding

Notes on contributors

Wen-Rang Liu

Dr. Wen-Rang Liu is an Assistant Professor in the Department of Finance at the National Yunlin University of Science and Technology, Taiwan. His primary research interests lie in empirical asset pricing, derivatives markets, and investment strategies.

Notes

1 Rouwenhorst (Citation1998), Griffin et al. (Citation2003), Chui et al. (Citation2010), Asness et al. (Citation2013), Israel and Moskowitz (Citation2013), Li and Wei (Citation2016), Chang et al. (Citation2018), Berggrun et al. (Citation2020), Gao et al. (Citation2020), and Goyal et al. (Citation2023) find momentum effects in the international stock markets.

2 John and Derek (Citation2003) and Menkhoff et al. (Citation2012) document momentum profits in foreign currency markets, Bhojraj and Swaminathan (Citation2006) in equity indices, Erb and Harvey (Citation2006) and Benavides Rosales (Citation2017) in commodity markets, and Jostova et al. (Citation2013) and Ho and Wang (Citation2018) in bonds. Asness et al. (Citation2013) find significant momentum profits in individual stocks, stock indices, commodities, and bond markets.

3 We express our gratitude to an anonymous reviewer for providing this highly insightful argument.

4 Screening criteria are devised in alignment with those of Hong et al. (Citation2003). To ensure the robustness of our findings, we test the results to varying cutoff thresholds.

5 The center and the report can be accessed through the following URL: http://rcted.ncu.edu.tw/.

6 Ozsoylev et al. (Citation2014) only consider a unidirectional network model. Because we propose that investor trading activities and information diffusion have leading and lagged relationships with each other, we also consider a directional network model.

7 This descriptive statistic is calculated based on the historical statistics of listed stocks provided by the Taipei Exchange (https://www.tpex.org.tw/web/).

8 We divide the stocks into 3 rather than 10 equal groups as Jegadeesh and Titman (Citation1993) do due to the smaller sample size of the Taiwan stock market.

9 How investors anticipate Taiwan’s future may affect their choices and timing of trading to some extent. It is difficult to exclude the impact of contextual factors, such as political risk, on investors’ trading behavior when examining the momentum effect. We expect this influence to become even more pronounced with the US-China tension; rumors and speculations that the US and China may engage in a proxy war in Taiwan have been circulating in the market in recent years. This fear of potential conflicts stimulates Taiwan’s stock market. Furthermore, investor trading behavior and information dissemination behavior have also changed since the outbreak of the COVID-19 pandemic.

10 We thank an anonymous referee for providing this valuable input.

11 In the untabulated results, we verify that findings similar to the baseline results can be obtained if past-9-month or past-12-month cumulative returns are used as the ranking benchmark.

12 We thank an anonymous referee for providing this great suggestion.

13 For firm characteristic variables that are negatively correlated with arbitrage frictions, such as institutional ownership, number of shareholders, and dollar trading volume, we add a negative sign.

14 Prior research, notably Yu and Yuan (Citation2011), Antoniou et al. (Citation2013), and Antoniou et al. (Citation2016), has extensively employed the investor sentiment index by Baker and Wurgler (Citation2006) and Baker & Wurgler (Citation2007) to identify different market sentiment periods. However, this index, based on the American market, is unsuitable for our analysis of the Taiwanese market. Wang et al. (Citation2021)’s empirical findings suggest that the consumer confidence index effectively reflects investor sentiment. Thus, our study adopts the monthly Consumer Confidence Index as our sentiment measure. We are grateful for an anonymous reviewer’s recommendation.

References

- Amihud, Y. (2002). Illiquidity and stock returns: Cross-section and time-series effects. Journal of Financial Markets, 5(1), 31–56. https://doi.org/10.1016/S1386-4181(01)00024-6.

- Antoniou, C., Doukas, J. A., & Subrahmanyam, A. (2013). Cognitive dissonance, sentiment, and momentum. Journal of Financial and Quantitative Analysis, 48(1), 245–275. https://doi.org/10.1017/S0022109012000592

- Antoniou, C., Doukas, J. A., & Subrahmanyam, A. (2016). Investor sentiment, beta, and the cost of equity capital. Management Science, 62(2), 347–367. https://doi.org/10.1287/mnsc.2014.2101

- Asem, E., & Tian, G. Y. (2010). Market dynamics and momentum profits. Journal of Financial and Quantitative Analysis, 45(6), 1549–1562. https://doi.org/10.1017/S0022109010000542

- Asness, C. S., Moskowitz, T. J., & Pedersen, L. H. (2013). Value and momentum everywhere. The Journal of Finance, 68(3), 929–985. https://doi.org/10.1111/jofi.12021

- Baker, M., & Wurgler, J. (2006). Investor sentiment and the cross-section of stock returns. The Journal of Finance, 61(4), 1645–1680. https://doi.org/10.1111/j.1540-6261.2006.00885.x

- Baker, M., & Wurgler, J. (2007). Investor sentiment in the stock market. Journal of Economic Perspectives, 21(2), 129–151. https://doi.org/10.1257/jep.21.2.129

- Barberis, N., Shleifer, A., & Vishny, R. (1998). A model of investor sentiment. Journal of Financial Economics, 49(3), 307–343. https://doi.org/10.1016/S0304-405X(98)00027-0

- Benavides Rosales, E. (2017). Time-series and cross-sectional momentum and contrarian strategies within the commodity futures markets. Cogent Economics & Finance, 5(1), 1339772. https://doi.org/10.1080/23322039.2017.1339772

- Berggrun, L., Cardona, E., & Lizarzaburu, E. (2020). Profitability of momentum strategies in Latin America. International Review of Financial Analysis, 70, 101502. https://doi.org/10.1016/j.irfa.2020.101502

- Bhojraj, S., & Swaminathan, B. (2006). Macromomentum: Returns predictability in international equity indices. The Journal of Business, 79(1), 429–451. https://doi.org/10.1086/497416

- Bonacich, P. (1972). Factoring and weighting approaches to status scores and clique identification. The Journal of Mathematical Sociology, 2(1), 113–120. https://doi.org/10.1080/0022250X.1972.9989806

- Bornholt, G. N., Dou, P., & Malin, M, Griffith University, Australia. (2015). Trading volume and momentum: The international evidence. Multinational Finance Journal, 19(4), 267–313. https://doi.org/10.17578/19-4-2

- Boudoukh, J., Israel, R., & Richardson, M. (2019). Long-horizon predictability: A cautionary tale. Financial Analysts Journal, 75(1), 17–30. https://doi.org/10.1080/0015198X.2018.1547056

- Boudoukh, J., Israel, R., & Richardson, M. (2022). Biases in long-horizon predictive regressions. Journal of Financial Economics, 145(3), 937–969. https://doi.org/10.1016/j.jfineco.2021.09.013

- Chang, R. P., Ko, K.-C., Nakano, S., & Rhee, G. S. (2018). Residual momentum in Japan. Journal of Empirical Finance, 45, 283–299. https://doi.org/10.1016/j.jempfin.2017.11.005

- Chen, Z., & Lu, A. (2017). Slow diffusion of information and price momentum in stocks: Evidence from options markets. Journal of Banking & Finance, 75, 98–108. https://doi.org/10.1016/j.jbankfin.2016.11.010

- Chui, A. C. W., Titman, S., & Wei, K. C. J. (2010). Individualism and momentum around the world. The Journal of Finance, 65(1), 361–392. https://doi.org/10.1111/j.1540-6261.2009.01532.x

- Chung, S.-L., Liu, W., Liu, W.-R., & Tseng, K. (2018). Investor network: Implications for information diffusion and asset prices. Pacific-Basin Finance Journal, 48, 186–209. https://doi.org/10.1016/j.pacfin.2018.02.004

- Colla, P., & Mele, A. (2010). Information linkages and correlated trading. Review of Financial Studies, 23(1), 203–246. https://doi.org/10.1093/rfs/hhp021

- Cooper, M. J., Gutierrez, R. C., Jr., & Hameed, A. (2004). Market states and momentum. The Journal of Finance, 59(3), 1345–1365. https://doi.org/10.1111/j.1540-6261.2004.00665.x

- Daniel, K., Hirshleifer, D., & Subrahmanyam, A. (1998). investor psychology and security market under- and overreactions. The Journal of Finance, 53(6), 1839–1885. https://doi.org/10.1111/0022-1082.00077

- Daniel, K., & Moskowitz, T. J. (2016). Momentum crashes. Journal of Financial Economics, 122(2), 221–247. https://doi.org/10.1016/j.jfineco.2015.12.002

- Du, D., Huang, Z., & Liao, B-s (2009). Why is there no momentum in the Taiwan stock market? Journal of Economics and Business, 61(2), 140–152. https://doi.org/10.1016/j.jeconbus.2008.06.001

- Erb, C. B., & Harvey, C. R. (2006). The strategic and tactical value of commodity futures. Financial Analysts Journal, 62(2), 69–97. https://doi.org/10.2469/faj.v62.n2.4084

- Fama, E. F., & French, K. R. (1993). Common risk factors in the returns on stocks and bonds. Journal of Financial Economics, 33(1), 3–56. https://doi.org/10.1016/0304-405X(93)90023-5

- Fama, E. F., & MacBeth, J. D. (1973). Risk, return, and equilibrium: Empirical tests. Journal of Political Economy, 81(3), 607–636. https://doi.org/10.1086/260061

- Freeman, L. C. (1979). Centrality in social networks conceptual clarification. Social Networks, 1(3), 215–239. https://doi.org/10.1016/0378-8733(78)90021-7

- Gao, Y., Guo, B., & Xiong, X. (2020). Signed momentum in the Chinese stock market. Pacific-Basin Finance Journal, 68, 101433. https://doi.org/10.1016/j.pacfin.2020.101433

- Goyal, A., Jegadeesh, N., & Subrahmanyam, A. (2023). Empirical Determinants of Momentum: A Perspective From International Data. Available at SSRN 4012902. https://doi.org/10.2139/ssrn.4012902

- Griffin, J. M., Ji, X., & Martin, J. S. (2003). Momentum investing and business cycle risk: Evidence from pole to pole. The Journal of Finance, 58(6), 2515–2547. https://doi.org/10.1046/j.1540-6261.2003.00614.x

- Gromb, D., & Vayanos, D. (2010). Limits of arbitrage. Annual Review of Financial Economics, 2(1), 251–275. https://doi.org/10.1146/annurev-financial-073009-104107

- Hameed, A., & Kusnadi, Y. (2002). Momentum strategies: Evidence from Pacific Basin stock markets. Journal of Financial Research, 25(3), 383–397. https://doi.org/10.1111/1475-6803.00025

- Han, B., & Yang, L. (2013). Social networks, information acquisition, and asset prices. Management Science, 59(6), 1444–1457. https://doi.org/10.1287/mnsc.1120.1678

- Ho, H.-C., & Wang, H.-C. (2018). Momentum lost and found in corporate bond returns. Journal of Financial Markets, 38, 60–82. https://doi.org/10.1016/j.finmar.2017.10.003

- Hodrick, R. J. (1992). Dividend yields and expected stock returns: Alternative procedures for inference and measurement. Review of Financial Studies, 5(3), 357–386. https://doi.org/10.1093/rfs/5.3.351

- Hong, D., Lee, C., & Swaminathan, B. (2003). Earnings momentum in international markets. Available at SSRN 390107. https://doi.org/10.2139/ssrn.390107

- Hong, H., Lim, T., & Stein, J. C. (2000). Bad news travels slowly: Size, analyst coverage, and the profitability of momentum strategies. The Journal of Finance, 55(1), 265–295. https://doi.org/10.1111/0022-1082.00206

- Hong, H., & Stein, J. C. (1999). A unified theory of underreaction, momentum trading, and overreaction in asset markets. The Journal of Finance, 54(6), 2143–2184. https://doi.org/10.1111/0022-1082.00184

- Hong, H., & Stein, J. C. (2007). Disagreement and the stock market. Journal of Economic Perspectives, 21(2), 109–128. https://doi.org/10.1257/jep.21.2.109

- Hou, K., & Moskowitz, T. J. (2005). Market frictions, price delay, and the cross-section of expected returns. Review of Financial Studies, 18(3), 981–1020. https://doi.org/10.1093/rfs/hhi023

- Israel, R., & Moskowitz, T. J. (2013). The role of shorting, firm size, and time on market anomalies. Journal of Financial Economics, 108(2), 275–301. https://doi.org/10.1016/j.jfineco.2012.11.005

- Jegadeesh, N., Luo, J., Subrahmanyam, A., & Titman, S. (2023). Momentum and short-term reversals: Theory and evidence. Available at SSRN: https://ssrn.com/abstract=4069575.

- Jegadeesh, N., & Titman, S. (1993). Returns to buying winners and selling losers: Implications for stock market efficiency. The Journal of Finance, 48(1), 65–91. https://doi.org/10.1111/j.1540-6261.1993.tb04702.x

- Jegadeesh, N., & Titman, S. (2001). Profitability of momentum strategies: An evaluation of alternative explanations. The Journal of Finance, 56(2), 699–720. https://doi.org/10.1111/0022-1082.00342

- Jegadeesh, N., & Titman, S. (2023). Momentum: Evidence and insights 30 years later. Pacific-Basin Finance Journal, 82, 102202. https://doi.org/10.1016/j.pacfin.2023.102202

- John, O., & Derek, W. (2003). Do momentum-based strategies still work in foreign currency markets? Journal of Financial and Quantitative Analysis, 38(2), 425–447.

- Jostova, G., Nikolova, S., Philipov, A., & Stahel, C. W. (2013). Momentum in corporate bond returns. Review of Financial Studies, 26(7), 1649–1693. https://doi.org/10.1093/rfs/hht022

- Lee, C. M. C., & Swaminathan, B. (2000). Price momentum and trading volume. The Journal of Finance, 55(5), 2017–2069. https://doi.org/10.1111/0022-1082.00280

- Li, F. W., & Wei, K.-C. (2016). Momentum life cycle around the world and beyond. Available at SSRN: https://ssrn.com/abstract=2565305.

- Liu, M.-Y., Chuang, W.-I., & Lo, C.-L. (2020). Options-implied information and the momentum cycle. Journal of Financial Markets, 53, 100565. https://doi.org/10.1016/j.finmar.2020.100565

- Menkhoff, L., Sarno, L., Schmeling, M., & Schrimpf, A. (2012). Currency momentum strategies. Journal of Financial Economics, 106(3), 660–684. https://doi.org/10.1016/j.jfineco.2012.06.009

- Newey, W. K., & West, K. D. (1987). Hypothesis testing with efficient method of moments estimation. International Economic Review, 28(3), 777–787. https://doi.org/10.2307/2526578

- Newey, W. K., & West, K. D. (1994). Automatic lag selection in covariance matrix estimation. The Review of Economic Studies, 61(4), 631–653. https://doi.org/10.2307/2297912

- Ozsoylev, H. N., & Walden, J. (2011). Asset pricing in large information networks. Journal of Economic Theory, 146(6), 2252–2280. https://doi.org/10.1016/j.jet.2011.10.003

- Ozsoylev, H. N., Walden, J., Yavuz, M. D., & Bildik, R. (2014). Investor networks in the stock market. Review of Financial Studies, 27(5), 1323–1366. https://doi.org/10.1093/rfs/hht065

- Pontiff, J. (1996). Costly arbitrage: Evidence from closed-end funds. The Quarterly Journal of Economics, 111(4), 1135–1151. https://doi.org/10.2307/2946710

- Rouwenhorst, K. G. (1998). International momentum strategies. The Journal of Finance, 53(1), 267–284. https://doi.org/10.1111/0022-1082.95722

- Schmeling, M. (2009). Investor sentiment and stock returns: Some international evidence. Journal of Empirical Finance, 16(3), 394–408. https://doi.org/10.1016/j.jempfin.2009.01.002

- Shleifer, A., & Vishny, R. W. (1997). The limits of arbitrage. The Journal of Finance, 52(1), 35–55. https://doi.org/10.1111/j.1540-6261.1997.tb03807.x

- Valkanov, R. (2003). Long-horizon regressions: Theoretical results and applications. Journal of Financial Economics, 68(2), 201–232. https://doi.org/10.1016/S0304-405X(03)00065-5

- Verardo, M. (2009). Heterogeneous beliefs and momentum profits. Journal of Financial and Quantitative Analysis, 44(4), 795–822. https://doi.org/10.1017/S0022109009990214

- Walden, J. (2019). Trading, profits, and volatility in a dynamic information network model. The Review of Economic Studies, 86(5), 2248–2283. https://doi.org/10.1093/restud/rdy058

- Wang, W., Su, C., & Duxbury, D. (2021). Investor sentiment and stock returns: Global evidence. Journal of Empirical Finance, 63, 365–391. https://doi.org/10.1016/j.jempfin.2021.07.010

- Yu, J., & Yuan, Y. (2011). Investor sentiment and the mean–variance relation. Journal of Financial Economics, 100(2), 367–381. https://doi.org/10.1016/j.jfineco.2010.10.011