?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

This study assesses the level of potential insider trading on the Saudi stock market (Tadawul) before and after the introduction of financial reforms. The level of potential insider trading is estimated by employing the market cleanliness measure (MCM) which determines the proportion of significant announcements (SAs) that were preceded by abnormal pre-announcement price movements (APPMs). The analysis was carried out using an event study approach to gauge the impact of an event on a security return. The market model is used to estimate the expected return which is subsequently compared with the actual return. The findings suggest the existence of significant abnormal returns surrounding 128 out of 1,958 unscheduled announcements made by firms listed on Tadawul from 2011 to 2020. The MCM shows that 56.36% of SAs were preceded by APPMs during the pre-financial reforms period whereas the ratio dropped to 45.2% over the post-financial reforms period. Although the findings suggest a reduction in the MCM by 11.16%, the statistics for the subsequent period was not statistically lower than the preceding period. The present study establishes a fundamental basis for tracking the efficacy of new regulations in deterring insider trading activities. This study provides empirical evidence and implications that can be taken into consideration by all parties concerned with illegal insider trading and market integrity.

Impact Statement

In view of the significance of market integrity and fairness, it is important to identify the consequences of impairments to market integrity and insufficient deterrence of insider trading. The findings of the study may be beneficial in driving regulators’ enforcement mechanisms for strengthening market surveillance and combating market misconduct by more actively implementing disciplinary actions. In addition, sequential reviews and assessments have been called for since the launch of Saudi Vision 2030 to ensure the delivery of its financial reform plans. Apart from its policy implications, the study is of interest to policymakers as it offers a foundation for regulatory bodies to determine whether further regulations are needed to strengthen regulatory performance and promote market discipline. Second, the results may be of interest to firms seeking to ensure proper functioning to accurately maintain material-sensitive information and regulate its release through appropriate channels.

1. Introduction

Information on securities markets is a motivating force for the trading operations of market participants. Unlike public information, private information provides a unique advantage for certain market participants, usually corporate insiders, who possess superior access to such information compared to other market participants (John & Lang, Citation1991; Yin & Zhao, Citation2015). The impact of private information involves being composed of material price-sensitive information. This in turn can incentivize insiders to exploit the foreknowledge of their firms’ performance and enable them to earn excess returns (Keown & Pinkerton, Citation1981; Lee, Citation2021). An extensive body of literature on illegal insider trading has documented that the financial markets are structured on trust and that the abuse of the possession of private information impairs that trust and thus raises concerns about market integrity and efficiency (Monteiro et al., Citation2007; Carvajal & Elliott, Citation2009; Dalko & Wang, Citation2016).

The prevalence of insider trading in Tadawul has raised questions about the integrity of the market and the potential effect of such practice on undermining investors’ confidence. In 2018, the Saudi Capital Market Authority (CMA) imposed 129 penalties on 249 violators of rules and regulations. Penalties for insider trading were the highest, totalling more than 86 million USD.Footnote1 In August 2021, the CMA referred a group of more than 250 individuals to the Public Prosecution charged with disclosing inside information for listed firms on social media.Footnote2 The media, however, have expressed concern over the pervasiveness of insider trading due to the abundant rumours circulating within Tadawul. These are critical issues that could discourage investors’ participations, influence the market liquidity and worsen stock price informativeness (Bhattacharya & Daouk, Citation2009; Collin‐Dufresne & Fos, Citation2015; Kim et al., Citation2019; Ahern, Citation2020).

The CMA though affirms that the Capital Market Law (CML) and its implementing regulations prohibits insider trading and considers it as a criminal offense in Saudi Arabia. The Saudi government has taken tremendous steps to develop its economy through financial reforms, broadly referred to as Saudi Vision 2030, which was adopted in 2016. The reforms plans were accompanied by a more elaborate program called the Financial Sector Development Program (FSDP). One purpose of the FSDP is to develop effective financial institutions to support the growth of the capital market and qualify Tadawul to become an advanced capital market. Therefore, the CMA has undertaken crucial initiatives that include loosening ownership limits for foreign investors to attract more investors and amending the Market Conduct Regulations (MCR) which involved extending the scope of insider trading prohibition.

Despite millions of dollars in fines imposed on insider traders along with criminal charges brought against hundreds of individuals who implicated in illegal insider trading, such ramifications have heightened concerns about integrity in Tadawul and may threaten the aim of attracting more investors. Motivated by these observations, we attempt to empirically estimate the level of potential insider trading. It may be conjectured that insider trading legislation in Tadawul lacks a sufficient mechanism to deter such misbehaviour. In other words, the low quality of institutions, weak enforcement of insider trading laws, or minimal penalties and sanctions could create space for insiders to engage in market misconduct. These are critical challenges that confront securities regulators to maintain the market discipline and promote the investors’ participations. The amount of confidence in the market can affect the amount of financing that can be raised through the stock market (Bhattacharya & Daouk, Citation2002).

The amended regulations of MCR are intended to enhance the confidence of investors and tackle market misconduct. However, there is an imperative need to understand more about market abuse in Tadawul, especially illegal insider trading, which has hitherto received little attention of empirical background research. It is, thus, the primary aim of this study to fill this gap by investigating the impact of the new regulatory amendments introduced with the financial reforms on the integrity of Tadawul with a particular focus on potential insider trading. The present study seeks to estimate and compare the market cleanliness measure (MCM) of Tadawul in the periods both before and after the introduction of the financial reforms. There is a lack of studies with respect to the estimation of possible insider trading practice in Tadawul where the most previous empirical studies on Tadawul have focused on the stock price reaction and the market efficiency. For examples, Syed and Bajwa (Citation2018) measured the impact of quarterly earnings announcements on stock prices reaction in Tadawul with the aim of testing the Efficient Market Hypothesis (EMH) and found significant abnormal returns (ARs) several days prior to the earnings announcements. Felimban et al. (Citation2018) examined the stock market response to dividend announcements in Gulf Cooperation Council (GCC) countries, including Tadawul, and suggested the information leakage before the announcements dates. However, these types of dividends and earnings announcements are often prescheduled earlier. Therefore, one may argue that the presence of ARs or information leakage before such events are motivated by informed trading of sophisticated investors that is driven by their information acquisition and/or the information provisions of sell-side analysts (Weller, Citation2018; Chen et al., Citation2020). Moreover, the ARs before the aforementioned announcements could be attributable to attentive trading on public information as shown by Alldredge and Cicero (Citation2015) or rather by the fact that the market is mostly being aware of their imminent release.

Unlike previous studies, we exclude such firms announcements and restrict our sample to unscheduled announcements. These announcements are likely to be a surprise events to the market assuming that they particularly involve a release of information in which the timing is not publicly known, and they are not easily predictable by the market participants. On the other hand, the existence of significant ARs ahead of unscheduled announcements is more likely to be driven by corporate insiders or other forms of suspicious trading activities that rely on material non-public information. This study may be the first that empirically measures the level of potential insider trading activities in Tadawul using a distinct type of major events and more recent data set during a period marked by substantial transformations in the history of Tadawul.

This paper extends the prior work of the market cleanliness methodology to answer the research question of whether the new regulatory changes were successful in reducing the occurrence of possible insider trading activities prior to firms announcements on Tadawul. We examined the research question using a sample of 1,958 unscheduled announcements released by the companies listed on Tadawul from 2011 to 2020 (the relevant period). The research hypotheses were tested by performing an event study approach to daily stock returns to examine the extent to which abnormal pre-announcement price movements (APPMs) have taken place before significant announcements (SAs). The analysis is carried out using a statistical model fitted to the time series data. The study will reveal the proportion of APPMs observed prior to SAs over the relevant period.

Our paper makes several contributions to the literature and the body of knowledge. The empirical findings of the study are important to policymakers, firms and investors. First, our paper provides a valuable contribution to the understanding of the effectiveness of insider trading laws and their enforcement in Tadawul. The study offers a foundation for regulatory bodies to determine whether additional regulations are needed to strengthen regulatory performance and promote the market discipline. Second, the results can be of interest to firms in ensuring proper function to accurately maintain material-sensitive information and regulate its release through an appropriate channel. Third, the study provides valuable insights to investors about market conditions pertaining to insider trading practises and holds value-adding in the emerging market context as well. The scope of the study is limited to examine abnormal stocks returns; however, an identified limitation involves to not examine abnormal trading volumes.

The remainder of this article is structured as follows. Section 2 proceeds with the literature review and hypothesis development. Section 3 presents the data and sample description, while Section 4 describes methodology. Section 5 presents analysis and results, and Section 6 concludes this article.

2. Literature review and hypothesis development

A number of prominent scholars in securities law and financial markets have extensively debated of whether the potential benefits of insider trading practice outweigh its drawbacks. In one hand, a vast literature has been devoted on the serious harm that insider trading does to the capital markets fairness, liquidity and stock price informativeness, thus it requires strict regulations (Bhattacharya & Daouk, Citation2002; Kwabi et al., Citation2018; Ojah et al., Citation2020). Another school of thought has argued in favour of insider trading stating that it fosters market efficiency, and it is an efficient method to compensate corporate managers for their entrepreneurial efforts (Manne, Citation1966; Carlton & Fischel, Citation1983). It is important to note that not all forms of insider trading are illegal; yet some are entirely legitimate (Shell, Citation2001; McGee, Citation2010). Although a longstanding literature debate between the opponents and proponents of insider trading prohibition, illegal insider trading is considered as a criminal conduct in many countries. As a result, most countries have established laws and legislation to prevent market misbehaviours such as insiders abusing their superior knowledge of private information (Bhattacharya & Daouk, Citation2002; La Porta et al., Citation2002, Citation2006).

2.1. Insider trading and stock return anomalies

Evidence from over three decades of insider trading investigations broadly underpins the assumption that illegal insider trading enables insiders to either gain abnormal profits or avoid potential loss by exploiting their privileged information at the expense of other investors (Kyle, Citation1985; Seyhun, Citation1986; Barclay & Warner, Citation1993; Jain et al., Citation2018; Suk & Wang, Citation2021). It has been empirically documented that the market can detect insider trading activity as such practice impounds the information into the stock price (Meulbroek, Citation1992; Bhattacharya et al., Citation2000). Drawing on firsthand observations of insider trading incidents, Meulbroek (Citation1992) revealed interesting results pertaining to 183 illegal insider trading cases charged by the U.S. Securities and Exchange Commission (SEC) from 1980 to 1989. The author discovered that 43% of price run-ups observed over the 20 days before takeover announcements. In a similar vein, Ahern (Citation2017) examined insider trading prosecutions filed by the SEC and the Department of Justice (DOJ) of the U.S. between 2009 and 2013. The author reported that the stock return average of trading on inside information gains 34.9% over 21 trading days from the original leakage date until the official public announcement of regulatory announcements whereas merger and acquisition (M&A) events yield average returns of 43% over 31 trading days leading up to the event date. These findings provide empirical evidence of the impact of insider trading on the process of security price formation.

Contrary to the massive amount of literature investigating insider trading in the U.S. and other developed capital markets, Tadawul has received very little scholarly attention. Numerous studies on Tadawul focus on the theoretical aspects of insider trading regulation, but there is little of empirical research. For instance, Syed and Bajwa (Citation2018) conducted an event study approach to test the EMH in the Tadawul by examining the stock prices reactions to 1,601 quarterly earnings announcements from 2009 to 2014. The authors designated event window comprising 21 trading day and observed significant and positive ARs in favourable of good news trend during the days leading up to the event day, particularly from day 9 to day 4 within the event window. Same event window length of 21 trading days was used by Al Qudah and Badawi (Citation2015) who tested the signaling theory to dividend announcements in Tadawul. Their findings suggest that the prices reactions to dividend announcements were not significant due to many restrictions on dividend policy in Tadawul. However, these findings are inconstant with those of Felimban et al. (Citation2018) who investigated the response of the stock market to 1,092 dividend announcements made by 299 listed firms in the GCC region from 2010 to 2015 and provided evidence indicating that the response of stock prices lends partial corroboration to the signaling hypothesis. The present study is carried out in various ways going beyond the scope of those studies. It provides more precise predictions about insider trading activities and their implications for stock price movements. This paper employs different statistical analyses and uses larger and distinguished sample of unscheduled firms announcements over a longer period which witnessed radical transformations in Tadawul.

Scholars and securities regulatory authorities attribute that the existence of significant ARs before the major firms events dates as an indicator that the events include important news about shares value and can be a signal of insider trading practices and information leakage (Jaffe, Citation1974; Olmo et al., Citation2011; Goldman et al., Citation2014; Collin‐Dufresne & Fos, Citation2015). The ARs can be estimated by conducting the event study method which probe the existence of ARs in the stock prices prior to the firms event date. The level of potential insider trading can be estimated by using the MCM which identifies the ratio of APPMs that have taken place ahead of SAs. Conceptually, the idea of the MCM is underpinned by the EMH which assumes that new information should be rapidly reflected into price changes. Interpreting the occurrence of APPMs within the context of the EMH, the implicit inference is that it violates the strong form of the EMH which supposes that asset prices reflect all public and private information. Fama (Citation1970) said, ‘strong form tests concerned with whether given investors or groups have monopolistic access to any information relevant for price formation’ (p. 383).

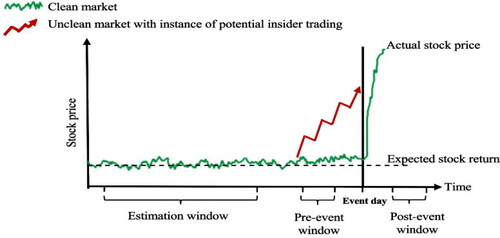

illustrates how insider trading activities influence the price movements. In a clean market, as shown by the green line, the asset price movement follows normal behaviour in the absence of new information over the estimation window leading up to the official announcement date. Once the announcement is made publicly, as indicated by the vertical line labelled as the event day, the stock price reacts instantly showing a clear spike on the event day as a result of the arrival of good news. By contrast, in an unclean market, the graph depicts that the stock price begins an upward drift, as shown by the rising red line, several days ahead of the event day during the pre-event window. In such case where the asset prices enjoyed a significant increase before the event day (i.e. APPMs), this behaviour may signal information leakage and could be a sign of insider trading activities before SAs.

Figure 1. Stock price movements with instance of insider trading.

The indication of the MCM can be estimated from the ratio of APPMs that were observed before the SAs. Subsection 4.2 describes the techniques for determining if an event is SA and preceded by APPMs. Briefly, the significant CARs over the post-event window imply that the announcement contains important news and should be considered as SA while the significant CARs across the pre-event window are indicator of the occurrence of APPMs. By contrast, the event is not considered as a SA or preceded by an APPM if no statistically significant CARs were detected over the event window being examined. The literature review establishes our research hypotheses which are formulated in a null form. This first hypothesis, denoted as assumes that the announcement has no significant impact on the distribution of CARs over the post-event window. A necessary condition to assess if APPMs have not taken place before the SAs, is the absence of significant CARs across the pre-event window as proposed in our second hypothesis, denoted as

which supposes that the announcement has no significant impact on the distribution of CARs over the pre-event window.

2.2. The role of insider trading laws

Previous academic studies have shown the significance of enforcing insider trading laws and found the legislation effects would be expected when enforcement mechanisms are enforced strictly but not merely the establishment of the laws (Bhattacharya & Daouk, Citation2009; Kwabi et al., Citation2018; Cline et al., Citation2021). Bhattacharya and Daouk (Citation2002) conducted a comprehensive survey of insider trading regulations over all countries that had stock markets at the end of 1998. The authors documented that enactment of insider trading laws alone are unlikely to be effective without strict enforcement. Chen et al. (Citation2017) found evidence that the initial enforcement of insider trading laws is positively associated with improvement in capital allocation efficiency.

Insider trading regulations have intrigued researchers who have tried to determine how insiders exploit insider trading legislation loopholes (Henning, Citation2015; Dalko & Wang, Citation2016). Alkhaldi (Citation2016) examined several insider trading cases in Tadawul and noted that those cases reviewed by the Committees for Resolution of Securities Disputes (CRSD) did not receive consistent assessment process. Alkhaldi (Citation2015) and Al-Habshan (Citation2017) addressed some instances of market misconducts in Tadawul which involve manipulation, poor transparency and insider trading cases. The authors indicated that such misconducts are due to deficiencies in the regulatory framework and inactive reactions from regulatory regime. In line with latter view, Alomari (Citation2020) scrutinised the lack of clarity presents in both legal terminology and judicial precedents pertaining to insider trading regulations in CML. The author criticized the legal definition of insider information with specific emphasis on the differentiation between ‘use’ versus ‘possession’ indicating that the central issue is concerned with ambiguity of whether the prohibition applies to engaging in trading based on material non-public information or engaging in trading while possessing such information. If the laws are properly introduced and effectively enforced, investors believe that their rights are being protected by law which in turn maintains investors’ confidence (La Porta et al., Citation2002; Citation2006).

The recent empirical studies on Tadawul, discussed in previous section, have documented the presence of significant ARs before the disclosure dates of earnings announcements as per Syed and Bajwa (Citation2018) and dividend decrease announcements (Felimban et al., Citation2018). The evidence of significant price changes before the dividend decrease announcements as well as immediately following the board meeting support Felimban et al. (Citation2018) to conclude that the GCC region markets exhibit inefficiency due to the leakage information ahead negative news announcement and the sluggish adjustment of share prices to positive news. In contrast, Alhassan et al. (Citation2019) examined the information content and the market reaction of quarterly earnings announcements of all firms listed on Tadawul for the years 2007 to 2017 and reported that stock price reactions were well-behaved due to the continuous developments in regulatory performance.

However, the media coverage of the rumours of insider trading practices, increased criminal prosecutions, and hefty penalties imposed by the CMA against insider traders has raised concerns about Tadawul’s integrity. These are critical problems that could discourage investors’ participation and pose a threat to the success of the goals related to the development of the capital market. In their empirical investigation of the impact of governance mechanisms and ownership structure on foreign investors’ decision for all non-financial firms listed in Tadawul in 2019, Bajaher et al. (Citation2022) indicated that the existing changes in governance and capital market regulations within Saudi Arabia may not be adequate in terms of inducing institutional foreign investment. Algaeed (Citation2021) suggested that the performance of the Saudi capital market with regards to its contribution and promotion towards economic development remains suboptimal. It could be argued that the weak governance of capital markets can result less capital allocation efficiency and raises investors’ concern about their investments safety.

There is evidence showing that countries with stricter insider trading rules and strong enforcement have been successful in reducing insider trading activities (Bhattacharya & Daouk, Citation2002; Zhang & Zhang, Citation2018). The amended regulatory changes instituted with the financial reforms in 2016 were created to strengthen the MCR, combats market misconduct, prompts investors’ confidence and further align the market condition with global standards. The effects of these amendments on potential insider trading practices are assessed here by estimating and comparing the Tadawul’s MCM before and after the introduction of new regulatory changes. The MCM has been used by the United Kingdom’s Financial Conduct Authority (FCA) to examine the impact of the Financial Services and Markets Act (FSMA) on the level of insider trading. The FCA performed three studies of MCM for the firms listed on the UK market and provided annual updates to the measure from 2000 to 2013 (Dubow & Monteiro, Citation2006; Monteiro et al., Citation2007; Goldman et al., Citation2014). Similarly, the Australian Securities and Investments Commission (ASIC, Citation2016) and (ASIC, Citation2019) applied the MCM to assess the cleanliness of the Australian equity markets after the transfer of market supervision. Therefore, to examine whether the new regulatory changes succeeded in reducing the level of potential insider trading in Tadawul, we utilise the MCM which estimates the proportion of the SAs that were preceded by APPMs. The statistical significance of the difference is assessed by performing a z-test against the null hypothesis of being no significant changes in the ratio of APPMs between both periods. This leads to a more precise prediction as stated in our third null hypothesis, denoted as which assumes that the difference in MCM between two periods is not statistically significant.

3. Sample and data description

This study uses secondary data of firms’ public announcements and daily stock prices across all sectors in the Tadawul. The sample period spans from 2011 to 2020 and is divided into two periods. The first period covers the pre-financial reforms period which starts from April 26, 2011, to April 25, 2016. The second period encompasses the post-financial reforms period, from April 26, 2016, to April 25, 2020. The selection of this period coincides with the raft of transformations that the Tadawul has witnessed such as reducing barriers to foreign investments in 2015,Footnote3 obligating traded companies to adopt the International Financial Reporting Standards (IFRS) in 2017,Footnote4 the launch of financial reforms in 2016, and the inclusion of the Tadawul in the major global financial indices from 2018 to 2020.Footnote5 The primary source of our study data is the Market Data Premium Reports Database (MDPRD), available on the official stock exchange website (Tadawul). The Tadawul designed the E-Reference Data System which has several databases.Footnote6 One of the databases is the MDPRD which is a reliable source of information providing comprehensive historical financial data for the Saudi capital market. The data were collected by considering the selection criteria that involved restrictions imposed by data availability as outlined in the following subsection.

3.1. Selection criteria

The present study requires data on firms announcements and their related securities during the relevant period. The sample of announcements is restricted to include unscheduled firms announcements published by issuers during the relevant period. The justifications for restricting the selection to unscheduled announcements stem from their merit of being unlikely anticipated, but they are typically known by corporate insiders. Other types of firms announcements like dividends or earnings announcements were excluded because they are often prescheduled and usually subject to explicit insider trading embargo (Cohen et al., Citation2012). Importantly, when our analysis shows that APPMs occurred prior to scheduled events, one may argue that these APPMs are not driven by potential insider trading activities, but rather by the fact that the scheduled announcements are predictable. Furthermore, the process of price discovery preceding scheduled events may be attributed to the activities of sophisticated traders which are motivated by their acquisition of information and/or the information provided by sell-side analysts (Weller, Citation2018; Chen et al., Citation2020). However, APPMs that occurred before unscheduled announcements are more likely due to insider trading activities. The selection was limited to major unscheduled events that fell under the heading of ‘merger, acquisition, takeover, awarding contract’ and two subsets of unscheduled, ‘good news’ and ‘bad news’ announcements. The data set of each firm announcement was manually documented to the millisecond. This timing was critical to our analysis because if the announcement occurred outside of trading hours, the date of the announcement could be misidentified. In these cases, the following trading day was designated as the event day. The daily stock prices were in the form of adjusted closing prices. Additionally, the following selection criteria was made to arrive at a clean sample:

All firms must have been listed on Tadawul and published unscheduled announcements during the relevant period.

Each announcement must include the firm’s stock price, announcement date, time, heading, and content.

Securities of the firms must have been actively traded during the estimation and event windows (253 trading days).

Stocks that made announcements during the relevant period, including those that were later delisted, and have enough data on daily prices for the estimation window and event window were included.

The final sample collected during the relevant period consists of 1,958 unscheduled announcements. There were 761 announcements drawn from 124 companies across the pre-financial reforms period and 1,197 announcements from 178 companies over the post-financial reforms period. provides a descriptive overview of the numbers and types of announcements within the relevant period.

Table 1. Overview of the firms announcements sample during the relevant period.

4. Market cleanliness methodology

We employed the MCM developed by Dubow and Monteiro (Citation2006) on the Saudi equity market data to determine the ratio of APPMs ahead of SAs and compare the MCM before and after the introduction of financial reforms. The daily abnormal stock returns are measured by performing a standard event study methodology to stock returns and employing an Ordinary Least Square (OLS) market model following (Brown & Warner, Citation1985; MacKinlay, Citation1997; Dubow & Monteiro, Citation2006). The event study approach offers an effective method for capturing the extent to which the announcement’s value has been converted into stock prices surrounding the event being examined.

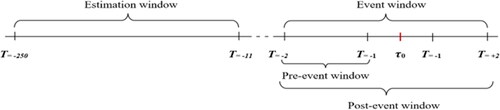

shows the timeline of the event study performed in this paper. The period involved a maximum of 253 trading days. The event day () was defined as a day on which the event occurred. There are two periods of interest for each event respective to the event day. The first period is distinguished the ‘estimation window’ which includes the first 240 trading days beginning at day −250 and ending at day −11 relative to the event day. The daily return observations within the estimation window were used to estimate the model parameters. The estimation window was kept separate from the event window to ensure that it is not contaminated by the event window. The second period is designated the ‘event window’ which consists of 5 trading days. The event window begins on day −2 and ends on day +2, and it is split into the pre-event and the post-event window. The post-event window along with the pre-event window are used to determine whether there is enough evidence to classify the event as a SA. The pre-event window is used to examine whether the APPMs have taken place prior to the event day. The reasons for the choice of the event window length can be concisely summarized as follows. First, Brooks (Citation2019) reports that the variations among models are typically minor and any errors in model specification are nearly negligible in short windows. Second, a robust short window relies on a precisely specified event date alongside that the pre-event window must be placed before the event day and should cover the time period on which abnormal trading activities are expected to have occurred (Kothari & Warner, Citation2007).

Figure 2. Timeline of the event study.

4.1. Estimating abnormal return (AR)

To identify AR, the expected returns must first be obtained. We estimated the expected return using the market model which calculates the statistical relationship between the individual firm’s return and the return of the broad market index over the estimation window (−250, −11). The ARs were computed as the difference between the expected return and the actual return. The cumulative abnormal returns (CARs) for the security were calculated by summing the ARs over the event window being examined. Thereafter, the bootstrap test statistics and quantile thresholds were used to assess whether the distribution of the CARs during the event window is statistically significant. Prior to estimating the ARs, we calculated the security and the market daily returns using the logarithmic return formula due to its merits compared to arithmetic formula as explained by Hudson and Gregoriou (Citation2015; Strong, Citation1992). Note that the dividend payments were integrated into Equation (4.1), which is essential to be considered because failure to do so would have a significant negative effect on the CARs over a prolonged period. Neglecting the calculation of dividend payments could cause an underestimate in total returns that come to investors (Brooks, Citation2019). The security return was computed with consideration of dividend payments as follows:

(1)

(1)

where ln is the natural log, Pit refers to the price of security i at the end of period t, Di,t denotes the dividends paid during period t, Pit -1 is the price of security i at the end of period t – l.

The Tadawul All Share Index (TASI) is used to calculate the market return as:

(2)

(2)

where ln denotes the natural logarithm; the Rm,t refers to the index’s daily return at time t, and TASI is a proxy for the market index.

To obtain the expected return E (Ri,t) for security i on day t, an OLS market model is used to estimate the model coefficients and the residual variance by regressing the security return on the index return over the estimation window as follows:

(3)

(3)

where Ri,t is the return on security i at time t, and Rm,t denotes the return of the market portfolio across the period t (comprising 240 trading days ending 10 days before the event day); ɛi,t is the zero mean disturbance term. Parameter ß depicts how much the stock return is influenced by the overall movements of the market portfolio returns over the estimation window period. The model parameter α denotes the expected value of the security daily return after controlling for the entire market movements over the estimation window period. This model assumes that ε (the estimation error) has standard statistical properties (a zero-mean independently and identically distributed error).

After obtaining the expected return, the AR of a security on a given day is computed by subtracting the expected return, predicted by (4.3), from the actual return of security i at time t as proposed by MacKinlay (Citation1997). The AR is defined mathematically as:

(4)

(4)

Because it is possible that there might be a lot of variation in stock returns on the days that fall within the event window, it could be difficult to distinguish overall patterns as noted by Brooks (Citation2019). Such patterns can be accurately measured by calculating the time-series CARs over the event window. The CARs were computed by summing the ARs over the event window days. As explained earlier, there are two windows: the post-event and pre-event windows. The CARs over the post-event window were calculated as shown by Equation (4.5) while Equation (4.6) calculates the CARs across the pre-event window.

(5)

(5)

(6)

(6)

4.2. Bootstrap method to test CARs statistical significance

To examine whether the actual post-event CARs (−2,+2) and the actual pre-event CARs (−2,−1) are statistically significant, we employ the bootstrap method which estimates the sampling distribution using random sampling techniques with replacement. The method estimates the finite sample distribution of the sequence of ARs from the estimation window observations and compares the magnitude of the actual post-event CARs and actual pre-event CARs against their respective simulated distributions values generated by bootstrap. To this end, we performed the following steps:

Calculating the daily AR for each event over the estimation window (−250 to −11).

Drawing random sequences of five-day ARs from the estimation window, then sum them up to obtain the simulated five-day CARs

The notation * denotes to the simulated five-day CARs extracted from the bootstrap not the actual post-event CARs.

Repeating this process 50,000 times, generates 50,000 random simulated five-day CARs.

The actual post-event CARs are assumed to be statistically significant at 1% level if they are lower than or equal to the 0.5% quantile of the

Having defined the events that met the high statistical threshold, we replicated the same technique for the pre-event window CARs with two changes to investigate whether the APPMs have taken place during the pre-event window. Steps 1 and 3 were repeated by focusing only on the events that were statistically determined as SAs.

Instead of selecting five-day ARs, we draw two-day ARs at random then sum them up to calculate the simulated two-day CARs

The actual pre-event CARs are compared with the

The bootstrap technique produces detailed information regarding the distribution of the CARs over the post and pre-event windows for each event. Unlike when using analytical results, the benefit of using bootstrapping is that it enables to draw conclusions without making distributional assumptions because the distribution used is that of the real data (Brooks, Citation2019).

To test the first hypothesis, we examined whether the CARs across the post-event window are statistically significant. Under the event has no effect on the distribution of CARs over the post-event window. If the test leads to rejection of the null, the event will be classified as SA which indicates that the announcement contains significant news where the security returns have shown statistically significant reactions as a response to the event. The second hypothesis test was conducted to assess the statistical significance of CARs over the pre-event window. Under

the distribution of CARs over the pre-event window has not been influenced by the event. If the null is rejected, it suggests that the event experienced APPMs. Thus, the event will be defined as an APPM which indicates that potential insider trading activities have occurred.

The MCM is calculated as the ratio of SAs that were preceded by APPMs which is defined mathematically as:

(7)

(7)

5. Empirical analysis

The return event study analysis provides evidence of the occurrence of APPMs ahead of SAs. summarizes the results of the Tadawul’s MCM over the relevant period with the total number of the original events analysed, the events that were identified as SAs, and the events for which we observed APPMs. As indicated in Panel A of , APPMs were detected in 31 out of 55 SAs during the pre-financial reforms period. Panel B reports the measure over the post-financial reforms revealing that 73 out of 1,197 events were SAs while 33 of them exhibited APPMs.

Table 2. The market cleanliness measurements through the relevant period.

represents that the measure for the post-financial reforms period is lower than that for the preceding period. To verify and establish the statistical significance of the observed drop, a statistical test of the difference in the ratio of APPMs between the two periods was performed using a z-test computed as:

The test assumes that each event within a particular sample has the same probability of being APPMs regardless of any other explanatory variables (i.e. the chance of every event is not dependent on other events). If n1 is the number of observations in set 1, P1 is the probability of an event being an APPM Q1 = 1-P1, n 1 P 1 ≥ 5 and n 1 Q 1 ≥ 5 where P and Q = 1-P are the average ratio of both samples. shows the difference in the MCM for the post-financial reforms period compared to the pre-financial reforms period. The difference in the measure was tested at a 5% significance level. We can conclude that, despite the MCM indicated that there was a drop in the measure by11.16% after the introduction of financial reforms, we do not reject (z = 1.232, p-value = 0.109) given that the statistic shows that the difference between two periods is not statistically significant.

Table 3. The test statistics of the difference in MCM between the pre-financial reforms period and the post-financial reforms period.

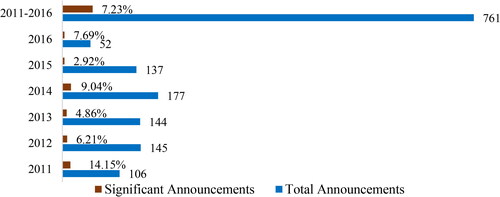

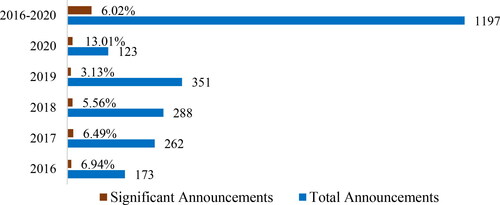

The figures displayed below show a comparison of the total number of the valid announcements analysed through the relevant period and the ratio of SAs that passed the statistical threshold of the significance level at a 1% to be considered SAs. The comparison helps to determine if an increase in SAs may have resulted from a rise in the sample size of the events assessed over each period. As shown in , the ratio of SAs in 2015 was 2.92% of 137 events, while 7.69% of the announcements were SAs from a sample of 52 events in 2016 (year ended 25th April). shows that 7.36% out of 761 events were SAs during the pre-financial reforms period, while indicates that 6.13% of a total sample of 1,197 events were SAs over the post-financial reforms period. The figures show that despite the increase in the total number of events in the post-financial reforms period compared to the prior period, the ratio of SAs is not correlated with the increase in the sample size of year-on-year events.

Figure 3. The ratio of significant announcements to the total announcements during the pre-financial reforms period.

Figure 4. The ratio of significant announcements to the total announcements during the post-financial reforms period.

The set of empirical findings reported in tests and

These Tables represent the descriptive statistics of the statistical significance level for the cumulative abnormal returns (CARs) calculated over the event window. To examine whether the CARs comprise statistically significant price movement, they are compared against the ninetieth percentile threshold of the simulated CARs of the empirical abnormal returns distribution from the estimation window period. The actual post-event window CARs are associated with the assessment to determine whether there is enough evidence to deem the events being examined as significant announcements (SAs). On the other side, the actual pre-event window CARs are used to make inferences of whether the abnormal pre-announcement price movements (APPMs) have taken place ahead of the SAs.

Table 4. The CARs of the events that were classified as SAs and preceded by APPMs during the pre-financial reforms period.

and report the number of events that met our statistical threshold for being SAs and preceded by APPMs over the pre-financial reforms and the post-financial reforms periods, respectively. In other words, these empirical findings do not permit the rejection of and

On the other hand, and show the events for which the

which assumes that the event had no impact on distribution of CARs over the post-event window was rejected; however, we found no evidence to support

concerning with the existence of statistically significant APPMs. The data reported in relate to the analysis outcomes over the pre-financial reforms periods, while the findings for the post-financial reforms period are shown in .

Table 5. The CARs of the events that were found statistically significant to be classified as SAs, but they were not preceded by APPMs during the pre-financial reforms period.

Table 6. The CARs of the events that were classified as SAs and preceded by APPMs during the post-financial reforms period.

Table 7. The CARs of the events that were found statistically significant to be classified as SAs, but they were not preceded by APPMs during the post-financial reforms period.

6. Conclusion

The study estimated the level of potential insider training in Tadawul using the MCM to examine the extent to which APPMs were detected ahead of 1,958 unscheduled announcements made by firms listed in Tadawul from 2011 to 2020. The event study approach was conducted to assess the impact of an event on stock returns. We used the market model to estimate the stock ARs. We computed the CARs and employed the bootstrapping technique to make inferences on whether the CARs during the event window being examined were statistically significant. We calculated the MCM as the ratio of firms events for which APPMs in daily stock prices were observed prior to the release of SAs.

The findings suggest that the proportion of APPMs detected ahead of SAs was lower after the introduction of financial reforms. The Tadawul’s MCM shows that 56.36% of SAs were preceded by APPMs across the pre-financial reforms period compared to 45.2% after financial reforms were passed. The analysis represents that despite there is a general improvement, as evidenced by 11.16% decline in the ratio of APPMs, the statistics for the subsequent period were not statistically lower than the preceding period. A possible explanation for this could be that the new regulatory changes introduced with financial reforms have not yet had a statistically significant effect in reducing the level of potential insider trading activities.

This study provides empirical findings with important implications for policymakers, firms, and investors. The findings could be beneficial in notifying the regulators’ enforcement mechanism to strengthen the market surveillance and combat market misconduct by implementing disciplinary actions more actively. The results alert firms to abide by CML rules and adhere the disclosures and transparency policies. Investors can benefit from the study as it supplies useful information about the market conditions regarding insider trading practices.

The scope of our study is limited to perform an event study to stock returns; however, conducting an event study to trading volumes would reinforce the return analysis. Another limitation of our analysis is the use of the OLS market model. Therefore, another direction for future research is to use several models and examine their differences. Moreover, it may be interesting to compare the reactions of scheduled announcements versus unscheduled announcements.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Notes on contributors

Abdulrhman Alqurayn

Abdulrhman Alqurayn is a lecturer at King Khalid University and a PhD candidate at Victoria University, Melbourne, Australia. He had his first degree in Business and Administration in 2011. Later on, he obtained his master’s in finance in 2016. He has worked at King Khalid University as a lecturer and a chairman of Business and Administration Department.

Nada Kulendran

Nada Kulendran is an Honorary Fellow at Victoria University, Melbourne, Australia. His area of expertise includes econometric modelling, financial markets forecasting, and volatility forecasting. He has made a sustained contribution in his area of research that resulted in the publication of research articles in high impact journals.

Ranjith Ihalanayake

Ranjith Ihalanayake is the Head of Postgraduate Courses and a Senior Lecturer in Economics and Finance in the Business School of Victoria University, Melbourne, Australia. His current research interest lies in the areas of foreign direct investment and economic growth, working capital management in small businesses and bank performance management.

Notes

1 In the 2018 Annual Report published by the CMA, Table 51 on page 158 shows the total amounts of financial penalties imposed by the CMA and the CRSD in 2018 against violators of the laws and regulations. Penalties for insider trading were the highest and were set at more 325,222,919 SR (Saudi Riyal). The report is available at https://cma.org.sa/en/Market/Reports/Documents/cma_2018_report.pdf.

2 The CMA’s announcement is available at https://cma.org.sa/en/Market/News/pages/CMA_N_2942.aspx.

3 The relevant information is available at https://cma.org.sa/en/Market/QFI/Pages/default.aspx.

5 The inclusion to FTSE Russell is available at https://cma.org.sa/en/MediaCenter/PR/Pages/FTSERussell.aspx, and the inclusion to MSCI emerging market is availavle at https://www.msci.com/msci-saudi-arabia-indexes.

References

- Ahern, K. R. (2017). Information networks: Evidence from illegal insider trading tips. Journal of Financial Economics, 125(1), 26–47. https://doi.org/10.1016/j.jfineco.2017.03.009

- Ahern, K. R. (2020). Do proxies for informed trading measure informed trading? Evidence from illegal insider trades. The Review of Asset Pricing Studies, 10(3), 397–440. https://doi.org/10.1093/rapstu/raaa004

- Al Qudah, A., & Badawi, A. (2015). The signaling effects and predictive powers of dividend announcements: Evidence from kingdom of Saudi Arabia. Journal of Business and Economics, 6(3), 550–557. https://doi.org/10.15341/jbe(2155-7950)/03.06.2015/012

- Algaeed, A. H. (2021). Capital market development and economic growth: an ARDL approach for Saudi Arabia, 1985–2018. Journal of Business Economics and Management, 22(2), 388–409. https://doi.org/10.3846/jbem.2020.13569

- Al-Habshan, K. (2017). Issues involving corporate transparency in the Saudi capital market. Public Administration Research, 6(2), 21–44. https://doi.org/10.5539/par.v6n2p21

- Alhassan, A., Alhomaidi, A., & Almuhtadi, B. (2019). The information content of earnings announcements: Evidence from the Saudi market. Capital Markets Authority. https://cma.org.sa/en/Market/Documents/The-Information-Content-of-Earnings-Announcements-en.pdf

- Alkhaldi, B. (2015). The saudi capital market: The crash of 2006 and lessons to be learned. International Journal of Business, Economics and Law, 8(4), 135–146.

- Alkhaldi, B. (2016). Saudi capital market: Development and challenges. Kluwer Law International B.V.

- Alldredge, D. M., & Cicero, D. C. (2015). Attentive insider trading. Journal of Financial Economics, 115(1), 84–101. https://doi.org/10.1016/j.jfineco.2014.09.005

- Alomari, Y. A. (2020). Ambiguity in Insider trading regulations: Saudi Arabia as a case study. Arab Law Quarterly, 34(4), 408–427. https://doi.org/10.1163/15730255-BJA10054

- ASIC. (2016). Review of Australian equity market cleanliness (Report No. 487). Australian Securities & Investments Commission. https://asic.gov.au/regulatory-resources/find-a-document/reports/rep-487-review-of-australian-equity-market-cleanliness/

- ASIC. (2019). Review of Australian equity market cleanliness (Report No. 623). Australian Securities & Investments Commission. https://asic.gov.au/regulatory-resources/find-a-document/reports/rep-623-review-of-australian-equity-market-cleanliness-1-november-2015-to-31-october-2018/

- Bajaher, M., Habbash, M., & Alborr, A. (2022). Board governance, ownership structure and foreign investment in the Saudi capital market. Journal of Financial Reporting and Accounting, 20(2), 261–278. https://doi.org/10.1108/JFRA-11-2020-0329

- Barclay, M. J., & Warner, J. B. (1993). Stealth trading and volatility: Which trades move prices? Journal of Financial Economics, 34(3), 281–305. https://doi.org/10.1016/0304-405x(93)90029-b

- Bhattacharya, U., & Daouk, H. (2002). The world price of insider trading. The Journal of Finance, 57(1), 75–108. https://doi.org/10.1111/1540-6261.00416

- Bhattacharya, U., & Daouk, H. (2009). When no law is better than a good law. Review of Finance, 13(4), 577–627. https://doi.org/10.1093/rof/rfp011

- Bhattacharya, U., Daouk, H., Jorgenson, B., & Kehr, C.-H. (2000). When an event is not an event: The curious case of an emerging market. Journal of Financial Economics, 55(1), 69–101. https://doi.org/10.1016/s0304-405x(99)00045-8

- Brooks, C. (2019). Introductory econometrics for finance (4th ed.). Cambridge University Press. https://doi.org/10.1017/9781108524872

- Brown, S. J., & Warner, J. B. (1985). Using daily stock returns: The case of event studies. Journal of Financial Economics, 14(1), 3–31. https://doi.org/10.1016/0304-405x(85)90042-x

- Carlton, D. W., & Fischel, D. R. (1983). The regulation of insider trading. Stanford Law Review, 35(5), 857–895. https://doi.org/10.2307/1228706

- Carvajal, A., & Elliott, J. E. (2009). The challenge of enforcement in securities markets: Mission impossible? IMF Working Papers, 09(168), 1. https://doi.org/10.5089/9781451873153.001

- Chen, Y., Kelly, B., & Wu, W. (2020). Sophisticated investors and market efficiency: Evidence from a natural experiment. Journal of Financial Economics, 138(2), 316–341. https://doi.org/10.1016/j.jfineco.2020.06.004

- Chen, Z., Huang, Y., Kusnadi, Y., & John Wei, K. C. (2017). The real effect of the initial enforcement of insider trading laws. Journal of Corporate Finance, 45, 687–709. https://doi.org/10.1016/j.jcorpfin.2017.06.006

- Cline, B. N., Williamson, C. R., & Xiong, H. (2021). Culture and the regulation of insider trading across countries. Journal of Corporate Finance, 67, 101917. https://doi.org/10.1016/j.jcorpfin.2021.101917

- Cohen, L., Malloy, C., & Pomorski, L. (2012). Decoding inside information. The Journal of Finance, 67(3), 1009–1043. https://doi.org/10.1111/j.1540-6261.2012.01740.x

- Collin‐Dufresne, P., & Fos, V. (2015). Do prices reveal the presence of informed trading? The Journal of Finance, 70(4), 1555–1582. https://doi.org/10.1111/jofi.12260

- Dalko, V., & Wang, M. H. (2016). Why is insider trading law ineffective? Three antitrust suggestions. Studies in Economics and Finance, 33(4), 704–715. https://doi.org/10.1108/SEF-03-2016-0074

- Dubow, B., & Monteiro, N. B. (2006). Measuring market cleanliness. Financial Services Authority Occasional Paper Series, (23), 1–37. https://doi.org/10.2139/ssrn.1019999

- Fama, E. F. (1970). Efficient capital markets: A review of theory and empirical work. The Journal of Finance, 25(2), 383–417. https://doi.org/10.1111/j.1540-6261.1970.tb00518.x

- Felimban, R., Floros, C., & Nguyen, A.-N. (2018). The impact of dividend announcements on share price and trading volume: Empirical evidence from the Gulf Cooperation Council (GCC) countries. Journal of Economic Studies, 45(2), 210–230. https://doi.org/10.1108/JES-03-2017-0069

- Goldman, J., Hunt, S., Minter, P., Suntheim, F., & Zaman, Q. (2014). Why has the FCAs market cleanliness statistic for takeover announcements decreased since 2009? Financial Services Authority Occasional Paper Series, (4) https://ssrn.com/abstract=2828760

- Henning, P. J. (2015). What’s so bad about insider trading law? The Business Lawyer, 70(3), 751–776.

- Hudson, R. S., & Gregoriou, A. (2015). Calculating and comparing security returns is harder than you think: A comparison between logarithmic and simple returns. International Review of Financial Analysis, 38, 151–162. https://doi.org/10.1016/j.irfa.2014.10.008

- Jaffe, J. F. (1974). Special information and insider trading. The Journal of Business, 47(3), 410–428. https://doi.org/10.1086/295655

- Jain, S., Agarwalla, S. K., Varma, J. R., & Pandey, A. (2018). Informed trading around earnings announcements—Spot, futures, or options? Journal of Futures Markets, 39(5), 579–589. https://doi.org/10.1002/fut.21983

- John, K., & Lang, L. H. (1991). Insider trading around dividend announcements: Theory and evidence. The Journal of Finance, 46(4), 1361–1389. https://doi.org/10.1111/j.1540-6261.1991.tb04621.x

- Keown, A. J., & Pinkerton, J. M. (1981). Merger announcements and insider trading activity: An empirical investigation. The Journal of Finance, 36(4), 855–869. https://doi.org/10.1111/j.1540-6261.1981.tb04888.x

- Kim, D., Ng, L., Wang, Q., & Wang, X. (2019). Insider trading, informativeness, and price efficiency around the world. Asia-Pacific Journal of Financial Studies, 48(6), 727–776. https://doi.org/10.1111/ajfs.12278

- Kothari, S. P., & Warner, J. B. (2007). Econometrics of event studies. In Handbook of empirical corporate finance. (pp. 3–36): Elsevier. https://doi.org/10.1016/B978-0-444-53265-7.50015-9

- Kwabi, F. O., Boateng, A., & Adegbite, E. (2018). The impact of stringent insider trading laws and institutional quality on cost of capital. International Review of Financial Analysis, 60, 127–137. https://doi.org/10.1016/j.irfa.2018.07.011

- Kyle, A. S. (1985). Continuous auctions and insider trading. Econometrica, 53(6), 1315–1335. https://doi.org/10.2307/1913210

- La Porta, R., Lopez‐de‐Silanes, F., & Shleifer, A. (2006). What works in securities laws? The Journal of Finance, 61(1), 1–32. https://doi.org/10.1111/j.1540-6261.2006.00828.x

- La Porta, R., Lopez‐de‐Silanes, F., Shleifer, A., & Vishny, R. (2002). Investor protection and corporate valuation. The Journal of Finance, 57(3), 1147–1170. https://doi.org/10.1111/1540-6261.00457

- Lee, J. (2021). Information asymmetry, mispricing, and security issuance. The Journal of Finance, 76(6), 3401–3446. https://doi.org/10.1111/jofi.13066

- MacKinlay, A. C. (1997). Event studies in economics and finance. Journal of Economic Literature, 35(1), 13–39. https://www.jstor.org/stable/2729691

- Manne, H. G. (1966). Insider trading and the stock market. Free Press.

- McGee, R. W. (2010). Analyzing insider trading from the perspectives of utilitarian ethics and rights theory. Journal of Business Ethics, 91(1), 65–82. https://doi.org/10.1007/s10551-009-0068-2

- Meulbroek, L. K. (1992). An empirical analysis of illegal insider trading. The Journal of Finance, 47(5), 1661–1699. https://doi.org/10.1111/j.1540-6261.1992.tb04679.x

- Monteiro, N. B., Zaman, Q., & Leitterstorf, S. (2007). Updated measurement of market cleanliness. SSRN Electronic Journal, (25), 3–60. https://doi.org/10.2139/ssrn.1011212

- Ojah, K., Muhanji, S., & Kodongo, O. (2020). Insider trading laws and price informativeness in emerging stock markets: The South African case. Emerging Markets Review, 43, 100690. https://doi.org/10.1016/j.ememar.2020.100690

- Olmo, J., Pilbeam, K., & Pouliot, W. (2011). Detecting the presence of insider trading via structural break tests. Journal of Banking & Finance, 35(11), 2820–2828. https://doi.org/10.1016/j.jbankfin.2011.03.013

- Seyhun, H. N. (1986). Insiders’ profits, costs of trading, and market efficiency. Journal of Financial Economics, 16(2), 189–212. https://doi.org/10.1016/0304-405x(86)90060-7

- Shell, G. R. (2001). When is it legal to trade on inside information? MIT Sloan Management Review, 43(1), 89–89.

- Strong, N. (1992). Modelling abnormal returns: a review article. Journal of Business Finance & Accounting, 19(4), 533–553. https://doi.org/10.1111/j.1468-5957.1992.tb00643.x

- Suk, I., & Wang, M. (2021). Does target firm insider trading signal the target’s synergy potential in mergers and acquisitions? Journal of Financial Economics, 142(3), 1155–1185. https://doi.org/10.1016/j.jfineco.2021.05.038

- Syed, A. M., & Bajwa, I. A. (2018). Earnings announcements, stock price reaction and market efficiency–The case of Saudi Arabia. International Journal of Islamic and Middle Eastern Finance and Management, 11(3), 416–431. https://doi.org/10.1108/IMEFM-02-2017-0044

- Weller, B. M. (2018). Does algorithmic trading reduce information acquisition? The Review of Financial Studies, 31(6), 2184–2226. https://doi.org/10.1093/rfs/hhx137

- Yin, X., & Zhao, J. (2015). A hidden Markov Model approach to information-based trading: Theory and applications. Journal of Applied Econometrics, 30(7), 1210–1234. https://doi.org/10.1002/jae.2412

- Zhang, I. X., & Zhang, Y. (2018). Insider trading restrictions and insiders’ supply of information: Evidence from earnings smoothing. Contemporary Accounting Research, 35(2), 898–929. https://doi.org/10.1111/1911-3846.12419