ABSTRACT

Investment in environmental, social, and governance (ESG) significantly influences a company’s financial aspects that drive sustainability. This study sample covers the data of 981 articles obtained from the Scopus database spanning over 141 journals from 2001 to 2021 and uses quantitative bibliometric analysis to discover present and future research directions of ESG. This analysis evaluates prolific research elements, such as authors, citations, journals, institutions, countries, regions, possible links between ESG and corporate performance and trends while focusing on the environmental pillar. With the emergence of the term ESG in 2006, the number of publications on this topic has almost doubled every year since 2017. With this exponential increase in the number of publications, the world is expected to give greater consideration to the concept of ESG, including green investing, circular economy, and RE100. This study highlights the key findings during the past decade including the importance of and tendency for ESG investing and revealing the less well-specified metrics of the governance pillar compared to those of the environmental and social pillars.

1. Introduction

The global challenges currently faced by our world have led to a shift in and heightened focus on sustainable development within and outside an organization, irrespective of its function and business model. Regardless of an organization’s size, its economic, environmental, and societal impacts can no longer be neglected. The concept of socially responsible investment (SRI) was discussed around the 1960s industrialization after World War II. However, it resulted in several environmental consequences, leading to the emergence of the environmental, social, and governance (ESG) concept (Gao et al., Citation2021). The economic strength of enterprises is closely connected to sustainable development and ESG concepts.

Since the inception of the term “sustainability” over two decades ago, its definition has significantly expanded to reach almost 300 terms, as reported by Johnston et al. (Citation2007). ESG criteria, specifically, are data-driven aspects of sustainability that emphasize a company’s performance in the areas of the environment, society, and governance, all of which are measurable (Ognen et al., Citation2017). Of the three pillars of ESG, the environmental pillar addresses major environmental concerns, including carbon footprint, resource use, waste management, and toxic emissions (Jasch, Citation2006).In contrast, the social pillar focuses on major societal aspects such as community issues, workforce management, human rights, and product responsibility and the governance pillar mainly addresses policy planning, employee management, business ethics, and corporate social responsibility (Ognen et al., Citation2017).

Managers implemented major reforms in corporate governance post 2008 global financial crisis. With the gradual economic recovery, the unaddressed environmental and social issues that emerged during the crisis could no longer be neglected. In the financial sector, ESG criteria are the key factors that can significantly influence a company’s sustainability. Hence, many investors consider ESG investing as a vital approach for managing financial risks. Companies and institutions with a better ESG performance are more prone to sustainable while successfully managing goals and targets (Ognen et al., Citation2017). As a consequence, investors and other stakeholders have recently started paying more attention to ESG evaluations. They tend to seek companies’ ESG scores and are entitled to information related to long-term managerial and strategic decisions (Balluchi et al., Citation2021). As discussed by Senadheera et al. (Citation2021), the E pillar in ESG has received substantial recognition from stakeholders because it evaluates the industrial impact on the natural environment. Moreover, the comprehensive indicators described by major rate providers including Morgan Stanley Capital International (MSCI), Bloomberg, and Refinitiv for E pillar cover major themes including carbon emissions, waste management, water, and energy usage, biodiversity, raw materials, and land use. These factors significantly contribute to the total ESG score and the industries try to invest more by considering the above factors. Moreover, initiatives such as Task Force on Climate-Related Financial Disclosure (TCFD), and intergovernmental organizations such as United Nations Principles for Responsible Investment (UN PRI) and UN Global Compact, encourage companies and global leaders to make responsible and strategic investments. For example, the UN PRI defines responsible investment decisions as those incorporating ESG issues while also achieving a sustainable global financial system (PRI, Citation2021). Even during the Conference of the Parties 26 (COP 26) summit held in November 2021, it was emphasized that the governments and companies should work together to achieve the Paris climate agreements and UN Sustainable Development Goals (UN SDGs) for sustainability. In recent years, research on ESG has seen immense growth, making it challenging to understand the current trends and trajectories in ESG research. Moreover, the research gaps from past studies could be identified and can be resolved through a systematic bibliometric analysis.

Scholars have used bibliometric analyses to identify and explore the structure of a specific research field. Utilizing bibliometric analyses intends to uncover emerging trends in a specific domain and visualize the collaboration patterns in articles, journals, authors, institutions, and research constituents which ultimately helps broaden the research insights (Donthu et al., Citation2021a). Moreover, attempts have also been made at bibliometric analyses of the aspects of sustainability aspects; for example, Tang et al. (Citation2018) studied sustainability from 2009 to 2018, and Sanguankaew and Ractham (Citation2019) covered knowledge management in sustainability from 1994 to 2018.

Large quantities of unstructured data obtained through these analyses are categorized into well-established themes, enabling researchers to identify research gaps, seek novel ideas, obtain a qualitative overview, and position the findings in their respective research fields (Donthu et al., Citation2021a). Therefore, with the increase in demand for and interest in ESG research, bibliometric analyses seems necessary to gain an overall understanding of ESG analyses conducted in recent years. Considering the business management, economics, and finance sectors Gao et al. (Citation2021) mainly focused solely on business journals in their research. To provide more systematic results, this study considered the three pillars of ESG on an equal basis. Furthermore, it contributes to the literature by being the first comprehensive bibliometric analysis solely dedicated to the growing field of ESG research that includes studies outside the business field and from a larger sample than that in Gao et al. (Citation2021) on an equal basis.

This study aimed to conduct quantitative bibliometric analysis, including performance analysis with prolific research elements, such as authors, citations, journals, institutions, countries, and regions, while utilizing bibliometric analysis enhancement techniques, such as visualization (Donthu et al., Citation2021b). For this purpose, we introduced and reviewed the bibliometric analysis of ESG research as well as the methodology and techniques used to analyze the data obtained from the Scopus database. The VOSviewer software was used to dissect and categorize the data into relevant groups to enhance the visualization effects.Thereafter, we discussed the limitations associated with the bibliometric analyses and future trends in the ESG field. Importantly, the recent research topics and interests in scholars engaged in ESG were able to identify from this study. Taken together, this study aimed to enhance the understanding of ESG through bibliometrics, which could help researchers in identifying the trends in ESG and provide basic background knowledge about ESG for new researchers and investors.

2. Methodology

2.1. Overview of bibliometric approach

The Scopus database was used to gather information on authors, researchers, affiliated institutions, other organizations, and countries that have contributed to the ESG research. Information on different published items, including research articles, book chapters, conference proceedings, reviews, books, editorial issues, notes, and conference reviews, were categorized into distinct subject areas, such as mathematics, sciences, engineering, business management, economics, and finance. The published research was also grouped based on the language of publication, year of publication, number of publications in a year, and number of citations received to identify the research directions and evolving trends. The bibliometric mapping approach provides a way to visualize the direction of a research area through both performance analysis and science mapping. Techniques such as citation analysis, co-citation analysis, and bibliographic coupling were also used in this study (Donthu et al., Citation2021a). The VOSviewer software was used for visual representation.

2.2. Database selection and search terms

The Scopus database includes a more expanded spectrum of journals and a faster citation analysis than the Web of Science (WoS; Joshi, Citation2016). It also enables easy exportation of data with no manual operations and covers a wide range of papers in the fields of business, finance, and management (Aksnes & Sivertsen, Citation2019; Nawaz et al., Citation2020). On the day of analysis (29 September 2021), the search word “ESG” [TITLE-ABS-KEY (ESG)] contained 5451 documents. However, this also included some irrelevant terms related to the medical field such as “Electrically Suspended Gyroscope, Electrostatically Supported Gyroscope, Electrostatic Gyroscope, Exfoliation Syndrome Glaucoma etc” and engineering, material science, and mathematical terms, such as “ Electronic Sound Generator, Eccentric Sleeve Grinding, Electric Strain Gauge, Energy Smart Grid, Extended Superjunction Gate, Equalizer SWAP Gate”. To avoid the above mentioned irrelevant fields, the following keywords were used for searching the database: “ESG”; “Environment*” OR “Social” OR “Governance” OR “Corporate Governance”; and “invest*” OR “score*” OR “index” OR “rating provider*” OR “rate provider*” OR “sustainability” OR “sustainable”. Furthermore, the article title, abstract, and author keywords were used as strings for document searches.

2.3. Data cleaning and analysis

A total of 1,110 documents were filtered using the search keywords from 2001 to the data retrieval date (29 September 2021). Almost 50% of the documents belonged to the economic, business, or financial fields as defined by Scopus. However, some publications belonged to other research areas, such as physics and astronomy, material science, toxicology and pharmaceutics, biochemistry, genetics and molecular biology, pharmacology, medicine, and chemistry. Therefore, a manual screening was performed to remove irrelevant documents from the current study. Subsequently, 981 documents were selected and entered into a Microsoft Excel spreadsheet for next phase analysis. Publication indicators, such as the total number of available articles, corresponding author articles, first author articles, and single-author articles affiliated to different countries and institutions were applied to identify and evaluate publications’ performance (Giannoudis et al., Citation2021).

2.4. Software for visual representation

VOSviewer is a free software widely used in bibliometric research investigations to construct maps of journals, authors, citation data, and keywords that offer the viewer with visualization diagrams. The term VOS, which means the visualization of similarities, highlights the graphical representation of bibliometric maps. In addition, maps are displayed so that they are easily interpretable and understandable by the viewer (Van Eck & Waltman, Citation2010). In this study, visual network images for co-citation analysis of cited sources, cited authors, author keywords, and so on were analyzed.

3. Results and discussion

3.1. Analysis based on the number of publications

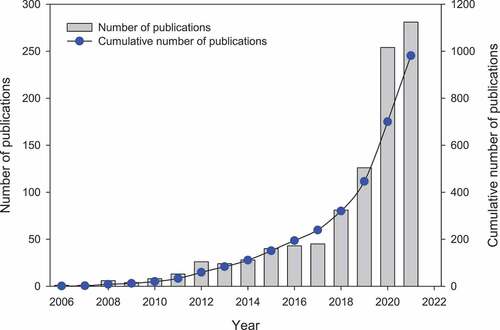

Researchers have only recently begun analyzing ESG-related aspects of sustainability because of the novelty of the term ESG. A subset of sustainability, ESG is science-based, investment-focused terminology. ESG is a combination of the words environmental, social, and governance, and was first introduced by the United Nations in 2004 in the report Who Cares Wins. Since then, starting from one publication in 2006 (Kocmanova et al., Citation2006), the interest in ESG has increased markedly over the past two decades. Kocmanova et al. (Citation2006) focused on the interrelationships among ESG performance indicators and conducted an empirical analysis that served as the basis for sustainability reporting. Additionally, the number of publications has almost doubled every year since 2017. After the 2008 financial crisis due to a year-long binge on cheap credit, corporate managers and investors paid more attention to ESG issues. Moreover, ESG evaluation results by ESG rating providers such as Thomson Reuters, MSCI, Bloomberg, and FTSE Russell directly affect the reputation and performance of corporations. Driven by this reality, researchers have developed an interest in ESG, resulting in a dramatic increase in research publications and findings. For this study, data were obtained from the Scopus database using the following keywords: “ESG” AND “Environment*” OR “Social” OR “Governance” OR “Corporate Governance” AND “invest*” OR “score*” OR “index” OR “rating provider*” OR “rate provider*” OR “sustainability” OR “sustainable”. Figure illustrates the exponential increase in the cumulative number of ESG-related publications.

Figure 1. Yearly and cumulative number of publications on ESG from 2006 to 2021.

3.2. Analysis based on document types and language of publication

As per the information obtained through the Scopus database, 981 documents were categorized into eight types (Table ). The category “Articles” had the highest number of publications. The next major shares were held by the categories “Book chapter” and “Conference papers”. However, these categories had fewer citations compared to those of the “Review” or “editorial papers.

Table 1. Categorization of articles into document types—number of publications, percentage of publications, and number of citations received

The document type “Review” constituted only 4% of the total publications, but it had the second-highest number of citations, and “Editorial” papers constituted 0.4% of the total documents. The document types “Book”, “Note”, and “Conference review” comprised 1% of the total publications with a lower number of citations.

The 981 documents were further classified according to their language of publication. Nine languages were used in the articles, with English being the most prominent (98.5%), followed by Russian (four articles). There were three publications in German, two in Chinese, and one each in Spanish, French, Japanese, Lithuanian, and Portuguese.

3.3. Analysis of citation trends

Chuang et al. (Citation2007) proposed a relationship between the publication life and the number of citations, which helps understand a research topic in accordance with the citation trends. Figure shows the trend in this relationship, where publication life is the age of the article from the date it was first published to the date of data extraction.

Figure 2. Trends in the relation between the average number of citations per publication and publication life.

Although the number of citations is related to the length of the time of publication, it is also used to assess the visibility of a certain publication. Figure shows that a document is most frequently cited in the seventh year of its publication, with a fluctuating trend thereafter. However, a steady increase in citations per article was observed up to the seventh year of publication. Notably, the number of articles increased during the analysis, with only one publication in 2006 to 281 publications in 2021.

3.4. Analysis of subject areas based on Scopus and journals

We now discuss an analysis of 981 documents from 141 journals that were classified into 15 subject areas in Scopus. Table shows the 10 most prominent Scopus subject areas with the number of publications and journals in each subject area. The subject area of Business, Management, and Accounting had most number of articles, followed by Econometrics, Economics, and Finance; the latter had documents distributed among all 141 journals.

Table 2. Ten most prominent Scopus subject areas with the number of publications received

The rank or importance of a journal was calculated based on the number of citations of its articles. Known as “impact factor”, it is used to identify the frequency with which an article from a particular journal is cited in a particular year.

Table shows the top 10 journals with the highest number of ESG articles published and their respective impact factors. Among these, Business Strategy and the Environment had the highest impact factor and number of articles at 36, which was 3.6% of the total documents. The Journal of Cleaner Production had the next highest impact factor. However, Sustainability had the highest number of articles related to the ESG field (11.8 %).

Table 3. Ten most prominent journals, based on the distribution of the highest number of articles

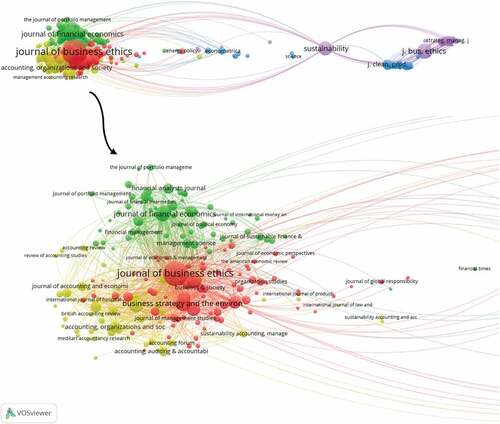

To further analyze the relationship among journals, co-citation analysis of the cited sources was conducted using the VOSviewer software. Figure illustrates the co-citation network of cited sources. A total of 282 records meet the threshold out of 16,076 sources under the condition that the least number of citations of a source equals 20.

Figure 3. Co-citation network for the cited sources using VOSviewer.

In Figure , nodes of similar color belong to the same cluster. The area of each node indicates the number of citations per document. A larger node indicates a higher number of citations A node represents a single reference per VOSviewer (Fabregat-Aibar et al., Citation2019). As depicted in Figure , the higher numbers of citations are for documents published in the Journal of Business Ethics, Journal of Financial Economics, Business Strategy and the Environment, and Sustainability.

3.5. Analysis of the documents categorized by Scopus

The highest number of ESG articles was affiliated with Sapienza Università di Roma in Italy (Table ). However, over 60% of these articles involved inter-institutional collaboration, mainly with other Italian universities. A similar pattern can also be observed for the Universidad de Zaragoza in Spain. Universidad Jaume I in Spain showed the lowest inter-institutional collaboration, whereas Ahlia University in Bahrain showed 100% collaboration with other universities in their research publications.

Table 4. Environmental, social, and governance articles categorized by affiliation

3.6. Analysis of the top 10 most productive authors

The Scopus analysis revealed that 159 authors had two or more publications. Of these, Tessa Hebb from Canada published the highest number of articles (nine articles), followed by Amina Buallay and Escrig-Olmedo (seven articles each). Analyses of the most productive authors reveal that most of the ESG-related research is conducted in Europe (e.g. Spain, Germany, and Czechia) and North America (the USA and Canada) as shown in Table .

Table 5. Top ten most productive authors in the environmental, social, and governance field

3.7. Analysis of the top 10 most frequently cited articles and the highest number of articles by country

Table lists the most cited articles in the ESG field. Prof. George Serafeim from the Harvard Business School, USA, has the highest number of cited articles published in the Strategic Management Journal. Among the top ten most popular authors, Prof. Serafeim stands out of over 12,000 business authors in the social science research network. Moreover, articles by USA authors have caught the interest of many readers as more than half of the top ten most cited articles are from the USA. Although most of the articles are published in journals from the finance and economics sectors, some are published in journals related to the field of sustainability, such as the Journal of Cleaner Production.

Table 6. Top ten most frequently cited articles

Notably, even though the Sustainability journal has the highest number of publications on ESG (Table ), none of the top ten highly cited articles have been published in this journal. In contrast, the Journal of Cleaner Production, Journal of Sustainable Finance and Investment, and Corporate Social Responsibility and Environmental Management have the highest number of publications and cited articles.

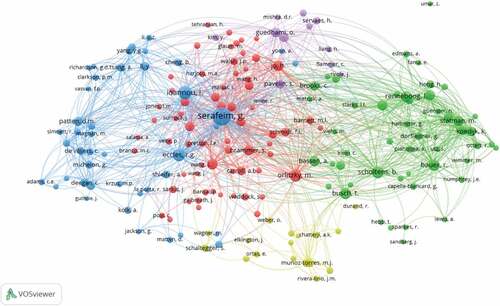

Similarly, Figure presents the co-citation network of cited authors using VOSviewer. Among 37,632 cited authors, the cluster shows 186 cited authors with a minimum of 50 citations. Serafeim, Ioannou, Eccles, and Busch were among the most prominent authors. The red, green, and blue clusters are predominant. For example, Serafime, Ioannou, and Eccles are grouped in the blue cluster, indicating that they conducted research in the same related field of study.

Figure 4. Visual representation of the cited authors’ co-citation network using VOSviewer.

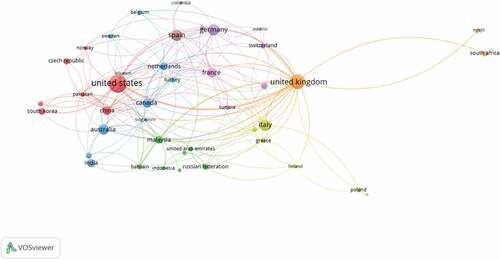

According to the countrywise research output in the ESG field (Table ), the USA leads the rankings by a significant margin with 172 articles. European countries, including the UK, Italy, Germany, Spain, and France, have produced a significant number of publications. Within the European Union, Germany has published the greatest number of articles and is among the top 5% of highly cited papers. The authors of the USA and the UK have also published many highly cited papers. Australia, China, and India in the Asia-Pacific region have also shown interest in ESG, with more than 35 publications each. However, China and India struggle to produce high-quality ESG research papers. Figure presents an overview of the cross-country co-authorship. Of the 101 countries with publications on ESG, 44 had already published a minimum of five articles. The visual diagram helps us identify collaborations among countries.

Table 7. Top ten countries by number of publications

Figure 5. Network analysis of co-authorship based on countries.

3.8. Author keyword analysis

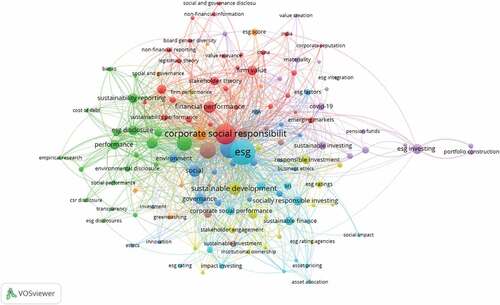

A co-occurrence analysis of the author keywords was conducted to visualize the keywords (Figure ). Of the 2,340 keywords, 131 met the threshold, wherein the minimum number of occurrences of a keyword was given as 5 in VOSviewer. According to the analysis, the term “ESG” occurred 199 times, while “corporate social responsibility” occurred 136 times. Furthermore, the terms “sustainability”, “environmental”, “corporate governance”, “social”, “CSR”, “sustainable development”, “governance”, and “financial performance” occurred most frequently in the 981 documents. Figure shows six important co-occurrences; the two major co-occurrences are around the concepts of Corporate Social Responsibility in red and ESG in blue. Both link to a large number of associated minor concepts. For instance, Corporate Social Responsibility is most prominently linked with financial performance, reflecting a preoccupation in the literature for tying corporate social responsibility with financial performance via ESG ratings. ESG is prominently tied to social and governance, and less to the environment. There seems to be a relative deficit of interest in the environmental pillar of ESG research compared to social and governance issues. This is a surprising result, given the public’s ever-increasing interest in environment-related issues. The other four co-occurrences were too scattered to draw general inferences. There is one centered on the concept of the environment in green, which involves disclosure issues. Furthermore, there are scattered themes in yellow that involve sustainable development. There are two minor themes: one in orange about ESG scores and one in purple involving sustainable investing that almost acts as a subgenre of the literature.

Figure 6. Co-occurrence analysis of author keywords.

3.9. Research foci and their developmental trends

ESG is a new concept that has evolved in the twenty-first century. It deals with the three pillars of environmental, social, and governance (Esty & Karpilow, Citation2019; Koroleva et al., Citation2020). Although the environmental pillar initially lacked substantial recognition, it has recently become a major global concern due to global warming, climate change, loss of biodiversity, and natural resource depletion. Many researchers have demonstrated how environmental aspects, mainly related to climate change, are considered in the business world, regardless of the type of industry (Clark, Citation2019; Díaz et al., Citation2021; Mercereau et al., Citation2020). Singal (Citation2014) revealed that firms in the hospitality and tourism sectors invest more in environmental programs than those in other industries with customers’ financial support. When considering the building and construction sector, major environmental pillar indicators, renewable energy, air quality, water conservation, and greenhouse gas emissions have been identified as vital aspects of financing investments (Mah, Citation2021).

As carbon dioxide emissions are a cause of concern, many industries have acknowledged that aggressive climate mitigation and carbon dioxide reduction policies can positively impact their financial profile and lead to sustainability (Cormack et al., Citation2020). Since thermal coal is a primary contributor to carbon dioxide emissions, institutional investors involved in coal combustion acknowledge strategic challenges such as replacing it with eco-friendly materials (Van De Putte et al., Citation2015). Ben Jabeur et al. (Citation2021) revealed that promoting green energy sources may help promote sustainability and mitigate climate change, and integrating ESG into oil and gas industries is more likely to lower crude oil prices. Studies also suggest that better internal governance favors the disclosure of carbon emission data revealing a positive relationship between the environmental and governmental pillars (Karim et al., Citation2021). Further, firms that act proactively regarding climate change mitigation have a higher awareness of the climate crisis and its negative impacts. Therefore, they volunteerly disclose carbon emission data (Lee et al., Citation2021).

Additionally, new frameworks for dealing with ecological sustainability that involve penalties for industries were discussed by Cho et al. (Citation2020). Scholars have constantly applied quantitative modeling tools to evaluate physical climate risk (Wiklund, Citation2021) and have studied the characteristics of metrics, such as green revenue, carbon intensity, and fossil fuel reserves (Bender et al., Citation2019). Hebb et al. (Citation2010) discussed the environmental and social impacts in the Canadian real estate market and revealed that awareness of financial impacts has raised significant interest in responsible property investments, while a research conducted by Escrig‐Olmedo et al. (Citation2013) discussed society’s perception of SRI and investors’ preferences regarding ESG criteria, and provided guidelines for approaching the Spanish market. Additionally, the importance of the E pillar in driving ESG ratings was demonstrated by Filippou and Taylor (Citation2021).

Jun (Citation2016) reflected on the importance of the governance pillar and how it helps in managerial decision making, as well as the need to address related problems promptly. However, the metrics of the governance pillar are not well-specified compared to those of the environmental and social domains (Veenstra & Ellemers, Citation2020). Furthermore, country factors, such as political issues and corruption, are not well understood when ESG data are disclosed and analyzed (Yu & Van Luu, Citation2021). Ding et al. (Citation2021) highlighted how the economy was affected during the novel coronavirus (COVID-19) pandemic due to the severe attack on health systems and the daily lives of people worldwide, and, more importantly, the need for governments’ intervention to rise from the social and economic crisis.

The weakness of the social domain can be understood thoroughly when we recognize how human rights affect sustainable development and how a journey toward sustainable development positively results in human rights (Ruggie & Middleton, Citation2019). Leins (Citation2020) highlighted the importance of responsible investments by large financial corporations that follow and accept ESG concepts. He emphasized how ESG has been transformed into a norm of responsible investments, increasing profits and adhering to social concerns over time. Moreover, Blank (Citation2019) revealed that, to date, military key performance indicators (KPI) are not offered by any of the major ESG data providers, and their findings indicate that clients request or look forward to new indicators. Engelhardt et al. (Citation2021) analyzed the association between ESG and company performance during the COVID-19 pandemic and found that the social score is a more prominent driver of lower stock volatility. Nicholls (Citation2010) suggested possible future schemes for SRI considering Weberian theory. According to research conducted during the last two decades, mainstream financial institutions lost 20–30% of their worth; however, the implementation of SRI yielded returns of approximately up to 6% during the same period. However, Van Duuren et al. (Citation2016) argued that ESG investing is more similar to fundamental investing and revealed the differences between the view point on ESG by American and European asset managers. Additionally, it has been revealed that SRI is practiced more in Europe. Further, it was identified that stakeholders and clients tend to invest more in the belief that the company works to manage its material ESG risks (Fernandez & Elfner, Citation2015). Brandstetter and Lehner (Citation2016) emphasized that investors insist ESG criteria be followed in building portfolios.

Popescu et al. (Citation2021) suggested that more stringent and upgraded science-based, open-source, and sustainability-driven assessment tools, incorporating a life-cycle perspective and measuring the positive impacts created, should be considered and given importance in ESG’s future research and reporting. Furthermore, considerations of eco-innovations in ESG (Esposito De Falco et al., Citation2021) and the application of artificial intelligence (Sætra, Citation2021) in ESG are possible as future research directions.

4. Limitations

Bibliometric analysis is a quantitative analysis of publications and paves the way for scholars to assess publications in related fields of interest. This study was based on the data retrieved from the Scopus database. Such databases as Google Scholar and the Web of Science could be considered in the future research in this field. More specific search terms to avoid manual screening of irrelevant data are key points to be considered in future studies. Although the number of citations per publication was analyzed in this study during the bibliometric analysis, there was no correlation between the quality of the research paper and the number of citations it received. Moreover, the latest technologies and methodologies in the field of ESG may not have been presented in the analyzed articles due to the lapse of time between innovation and publication (Giannoudis et al., Citation2021). Nevertheless, a bibliometric analysis aids in mapping the available literature, understanding the trends and collaborations, and helping to identify the leaders and pioneers, and their contributions to their respective fields.

5. Conclusions

Issues evolving with ESG have been seriously considered by enterprises and institutions since the 2010s, although the idea of ESG has existed for decades. For example, companies tend to publish their sustainability report in the name of “ESG report” aligning to environmental, social and governance indicators. At present, ESG contributes to a company’s sustainability and long-term operations. Therefore, it is necessary to have a clear understanding of ESG-related trends and approaches. Conducting a bibliometric analysis of ESG research is thus helpful in addressing the current knowledge gaps. Data retrieved from the Scopus database were used for further analysis. Overall, 981 publications related to ESG were published in 140 journals belonging to different research fields, such as business, economics, and the environment which were published within almost two decades (from 2001 to 2021).

Information such as the number of citations, authors, affiliations, and journals related to ESG helped to gain background knowledge on this topic. A basic bibliometric analysis indicated that the USA, Canada, and many research institutions from European countries are leading the field of ESG research, while institutes from the Asia-Pacific region have recently begun to show interest. With the exponential increase in the number of publications over time, the world is expected to give greater consideration to the concept of ESG, and the evolving research foci will benefit all economic, social, and environmental sectors. With more attention paid to ESG, there will hopefully be more contributions from the stakeholders of companies toward the mitigation of environmental issues, including carbon and toxic emissions, loss of biodiversity, global climate change, and social issues, such as healthy employee relations, gender equality, human rights, and anti-corruption. Additionally, this analysis reveals a positive correlation between disclosure of a company’s ESG information and better performance. This encourages companies to disclose more information about their ESG aspects, making ESG disclosure a popular trend.

ESG rating providers, such as Bloomberg, MSCI, and Sustainalytics, collect publicly available ESG data with their own comprehensive, unique analysis, and provide the company with an ESG score. However, owing to the different methodologies used by each rating provider, different ESG scores may coexist for a certain company. Future research can consider standardizing the scoring criteria to provide a common scoring system. Additionally, more concerns about environmental issues, including climate change, waste management, loss of biodiversity, ESG disclosure, and responsible ESG investment, with the active participation of corporate governance are possible future research directions. This analysis concludes that ESG is still an emerging field that will show drastic growth in the future, impacting sustainability.

Author contributions

Sachini Supunsala Senadheera: Data collection, Empirical Modeling, Software, Writing - Original Draft.

Richard Gregory: Writing - Review & Editing.

Jörg Rinklebe: Writing - Review & Editing.

Muhammad Farrukh: Writing - Review & Editing.

Jay Hyuk Rhee: Conceptualization, Theoretical framework, Supervision - review & editing, Funding acquisition.

Yong Sik Ok: Conceptualization, Theoretical framework, Supervision - review & editing, Funding acquisition.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Data availability statement

The authors confirm that the data supporting the findings of this study are available within the article itself. The raw data, whereas are deposited with Mendeley Data, V1, doi: 10.17632/hsdgt7rbk7.1. https://data.mendeley.com/datasets/hsdgt7rbk7

Additional information

Funding

Notes on contributors

Sachini Supunsala Senadheera

Ms. Sachini Supunsala Senadheera is a PhD scholar at the department of Environmental and Ecological Engineering at Korea University. She received her bachelor’s degree in chemical and Process Engineering in 2020. Her research focuses include environmental sustainability, carbon capture and storage and environmental remediation.

Richard Gregory

Dr. Richard Gregory graduated with a B.A. in Economics from Old Dominion University in 1988. He received an M.A. in Economics with a concentration in International Finance from Indiana University in 1990. He received his Ph. D. in Finance with a concentration in International Business from Old Dominion University in 1996. Post Ph.D. he worked as a self-employed financial consultant for start-up firms in the Research Triangle of North Carolina. Afterward he became Senior Economist for the Virginia Economic Development Partnership from 1997-2000. He was Visiting Professor of Finance at Old Dominion University from 2000-2002. He was Assistant Professor of Finance at the University of South Carolina-Upstate from 2002-2008. In between, he served as a financial consultant for various private companies. Dr. Gregory has been at East Tennessee State University since 2008. He was promoted to Associate Professor in 2013 and moved to Professor in 2018. He continues to work as a financial consultant to local and international businesses. His academic research has been published in national and international journals.

Jörg Rinklebe

Dr. Jörg Rinklebe is a Professor for Soil- and Groundwater-Management at the University of Wuppertal, Germany. His academic background covers environmental science, hazardous compounds, bioavailability of emerging contaminants, and remediation of contaminated sites. His main research is on soils, sediments, waters, plants, and their pollutions and linked biogeochemical issues with a special focus in redox chemistry. Professor Rinklebe is internationally recognized particularly for his research in the areas of biogeochemistry of trace elements in wetland soils. Professor Rinklebe published over 400 research papers, 21 were nominated in the in ISI Web of Science as “Highly Cited Papers” and 3 were nominated as “Hot Paper”. These papers have been cited more than 12,000 times in Scopus with h-index = 68. Prof Rinklebe has been selected as ISI Web of Science Globally Highly Cited Researcher in 2019, 2020 and 2021. He is serving as Editor in Chief of ”Environmental Pollution” and as Editor for Special Issues of “Journal of Hazardous Materials” and further journals. Recently, Professor Rinklebe is the President of the International Society of Trace Element Biogeochemistry (ISTEB).

Muhammad Farrukh

Dr. Muhammad Farrukh is currently working at the Department of Economics, Shenzhen MSU-BIT, Shenzhen, China. His area of research revolves around entrepreneurship, Intrapreneurship, and Industrial-organizational psychology. His publications appear in ABS and ABDC-listed journals.

Jay Hyuk Rhee

Dr. Jay Hyuk Rhee is a Professor at the School of Business Administration, Korea University, Seoul, Korea. Prof. Rhee serves as the Head of the Sustainability Management Research Group (a corporate management research institute at Korea University) since 2019 and the Director of Korea University Social Enterprise Center. Prof. Rhee’s main research areas cover global management, management strategy, and sustainability including ESG, CSR, and SDG. He has received a number of awards and honors, including the Stone Tower Research Award in 2020 at Korea University, Korea University Seok-Top Lecture Awards, KUBS Teaching Award, Korea University Graduate School of Business Management Research Course Excellence Lecture Award. Prof. Rhee is the founding member and member of the Institute for Sustainable Economy and Society. He has served as a member of many government institutes including the National Pension Fund Trustee Responsibility Specialized Committee, Special Committee for Win-Win Cooperation Division, Ministry of SMEs, Startups, Corporate Governance Committee of the Korea Corporate Governance Service and Social Welfare Community Chest of Korea and Sharing Culture Research Center.

Yong Sik Ok

Dr. Yong Sik Ok is a Full Professor and global research director at Korea University in Seoul, Korea. His academic background covers waste management, the bioavailability of emerging contaminants, and bioenergy and value-added products (such as biochar). Further, Professor Ok has experience in fundamental soil science and the remediation of various contaminants in soils and sediments. In 2019, he became the first Korean to be selected as an HCR in the field of Environment and Ecology. He maintains a worldwide professional network by serving as an Editor (former Co-Editor) of Critical Reviews in Environmental Science and Technology, Editor of Environmental Pollution, member of the editorial advisory board of Environmental Science & Technology and editorial boards of Renewable and Sustainable Energy Reviews, Chemical Engineering Journal, Chemosphere, Journal of Analytical and Applied Pyrolysis, and Environmental Science: Water Research & Technology with several other top journals. He currently serves as Director of the Sustainable Waste Management Program for the Association of Pacific Rim Universities (APRU) and Co-President of the International ESG Association. Prof. Ok also hosted the first Nature conference among South Korean universities in Seoul in 2021 on waste management and valorization for a sustainable future together with Chief Editors of Nature Sustainability.

References

- Academic Accelerator, 2021. https://academic-accelerator.com/

- Aksnes, D. W., & Sivertsen, G. (2019). A criteria-based assessment of the coverage of Scopus and web of science. Journal of Data and Information Science, 4(1), 1–15. https://doi.org/10.2478/jdis-2019-0001

- Atkins, J., & Maroun, W. (2015). Integrated reporting in South Africa in 2012: Perspectives from South African institutional investors. Meditari Accountancy Research, 23(2), 197–221. https://doi.org/10.1108/MEDAR-07-2014-0047

- Balluchi, F., Lazzini, A., & Torelli, R. (2021). Credibility of environmental issues in non-financial mandatory disclosure: Measurement and determinants. Journal of Cleaner Production, 288, 125744. https://doi.org/10.1016/j.jclepro.2020.125744

- Bender, J., Bridges, T. A., & Shah, K. (2019). Reinventing climate investing: Building equity portfolios for climate risk mitigation and adaptation. Journal of Sustainable Finance and Investment, 9(3), 191–213. https://doi.org/10.1080/20430795.2019.1579512

- Ben Jabeur, S., Khalfaoui, R., & Ben Arfi, W. (2021). The effect of green energy, global environmental indexes, and stock markets in predicting oil price crashes: Evidence from explainable machine learning. Journal of Environmental Management, 298, 113511. https://doi.org/10.1016/j.jenvman.2021.113511

- Blank, H. D. (2019). Corporate treatment of veterans as an ESG factor and a potential source of incremental returns. Review of Business, 39(1), 75–93. https://vetsindexes.com/wp-content/uploads/2020/09/Corporate-Tratment-of-Veterans-as-an-ESG.pdf.

- Brandstetter, L., & Lehner, O. M. (2016). Opening the market for impact investments: The need for adapted portfolio tools. Routledge Handbook of Social and Sustainable Finance, 5 (2), 448–462. Routledge. https://doi.org/10.1515/erj-2015-0003

- Brooks, C., & Oikonomou, I. (2018). The effects of environmental, social and governance disclosures and performance on firm value: A review of the literature in accounting and finance. British Accounting Review, 50(1), 1–15. https://doi.org/10.1016/j.bar.2017.11.005

- Cheng, B., Ioannou, I., & Serafeim, G. (2014). Corporate social responsibility and access to finance. Strategic Management Journal, 35(1), 1–23. https://doi.org/10.1002/smj.2131

- Cho, H. J., Lehner, O. M., & Nilavongse, R. (2020). Combining financial and ecological sustainability in bank capital regulations. Journal of Applied Accounting Research, 22(3), 423–435. https://doi.org/10.1108/JAAR-10-2020-0221

- Chuang, K. Y., Huang, Y. L., & Ho, Y. S. (2007). A bibliometric and citation analysis of stroke-related research in Taiwan. Scientometrics, 72(2), 201–212. https://doi.org/10.1007/s11192-007-1721-0

- Clark, C. (2019). Climate change scenario analysis for public market investors. Journal of Applied Corporate Finance, 31(2), 118–123. https://doi.org/10.1111/jacf.12353

- Cormack, C., Donovan, C., Köberle, A., & Ostrovnaya, A. (2020). Estimating financial risks from the energy transition: Potential impacts from decarbonization in the European power sector. Journal of Energy Markets, 13(4), 1–49. https://doi.org/10.21314/JEM.2020.209

- Cucari, N., Esposito De Falco, S., & Orlando, B. (2018). Diversity of board of directors and environmental social governance: Evidence from Italian listed companies. Corporate Social Responsibility and Environmental Management, 25(3), 250–266. https://doi.org/10.1002/csr.1452

- Díaz, V., Ibrushi, D., & Zhao, J. (2021). Reconsidering systematic factors during the Covid-19 pandemic – The rising importance of ESG. Finance Research Letters, 38(C), 101870. https://doi.org/10.1016/j.frl.2020.101870

- Ding, W., Levine, R., Lin, C., & Xie, W. (2021). Corporate immunity to the COVID-19 pandemic. Journal of Financial Economics, 141(2), 802–830. https://doi.org/10.1016/j.jfineco.2021.03.005

- Donthu, N., Kumar, S., Mukherjee, D., Pandey, N., & Lim, W. M. (2021a). How to conduct a bibliometric analysis: An overview and guidelines. Journal of Business Research, 133 (C), 285–296. https://doi.org/10.1016/j.jbusres.2021.04.070

- Donthu, N., Kumar, S., & Pandey, N. (2021b). A retrospective evaluation of Marketing Intelligence and Planning: 1983–2019. Marketing Intelligence and Planning, 39(1), 48–73. https://doi.org/10.1108/MIP-02-2020-0066

- Engelhardt, N., Ekkenga, J., & Posch, P. (2021). ESG ratings and stock performance during the covid-19 crisis. Sustainability (Switzerland), 13(13), 7133. https://doi.org/10.3390/su13137133

- Escrig‐Olmedo, E., Muñoz‐Torres, M. J., & Fernández‐Izquierdo, M. Á. (2013). Sustainable development and the financial system: Society’s perceptions about socially responsible investing. Business Strategy and the Environment, 22(6), 410–428. https://doi.org/10.1002/bse.1755

- Esposito De Falco, S., Scandurra, G., & Thomas, A. (2021). How stakeholders affect the pursuit of the environmental, social, and governance. Evidence from innovative small and medium enterprises. Corporate Social Responsibility and Environmental Management, 28(5), 1528–1539. https://doi.org/10.1002/csr.2183

- Esty, D. C., & Karpilow, Q. (2019). Harnessing investor interest in sustainability: The next frontier in environmental information I regulation. Yale Journal on Regulation, 36(2), 625–692. https://openyls.law.yale.edu/bitstream/handle/20.500.13051/8291/36_JREG_625_Esty.pdf?sequence=2.

- Fabregat-Aibar, L., Barberà-Mariné, M. G., Terceño, A., & Pié, L. (2019). A bibliometric and visualization analysis of socially responsible funds. Sustainability (Switzerland), 11(9), 2526. https://doi.org/10.3390/su11092526

- Fatemi, A., Glaum, M., & Kaiser, S. (2018). ESG performance and firm value: The moderating role of disclosure. Global Finance Journal, 38(C), 45–64. https://doi.org/10.1016/j.gfj.2017.03.001

- Fernandez, R., & Elfner, N. (2015). ESG integration in corporate fixed income. Journal of Applied Corporate Finance, 27(2), 64–72. https://doi.org/10.1111/jacf.12119

- Filippou, I., & Taylor, M. P. (2021). Pricing ethics in the foreign exchange market: Environmental, social and governance ratings and currency premia. Journal of Economic Behavior and Organization, 191, 66–77. https://doi.org/10.1016/j.jebo.2021.08.037

- Friede, G., Busch, T., & Bassen, A. (2015). ESG and financial performance: Aggregated evidence from more than 2000 empirical studies. Journal of Sustainable Finance and Investment, 5(4), 210–233. https://doi.org/10.1080/20430795.2015.1118917

- Gao, S., Meng, F., Gu, Z., Liu, Z., & Farrukh, M. (2021). Mapping and clustering analysis on environmental, social and governance field a bibliometric analysis using scopus. Sustainability (Switzerland), 13(13), 7304. https://doi.org/10.3390/su13137304

- Giannoudis, P. V., Chloros, G. D., & Ho, Y. S. (2021). A historical review and bibliometric analysis of research on fracture nonunion in the last three decades. International Orthopaedics, 45(7), 1663–1676. https://doi.org/10.1007/s00264-021-05020-6

- Hebb, T., Hamilton, A., & Hachigian, H. (2010). Responsible property investing in Canada: Factoring both environmental and social impacts in the Canadian real estate market. Journal of Business Ethics, 92(1), 99–115. https://doi.org/10.1007/s10551-010-0636-5

- Jasch, C. (2006). Environmental management accounting (EMA) as the next step in the evolution of management accounting. Journal of Cleaner Production, 14(14), 1190–1193. https://doi.org/10.1016/j.jclepro.2005.08.006

- Johnston, P., Everard, M., Santillo, D., & Robèrt, K. H. (2007). Reclaiming the definition of sustainability. Environmental Science and Pollution Research, 14(1), 60–66. https://doi.org/10.1065/espr2007.01.375

- Joshi, A. (2016). Comparison between Scopus ; ISI web of science. Journal Global Values , VII(1), 1–11. https://www.researchgate.net/profile/Aditi-Joshi-10/publication/318258303_COMPARISON_BETWEEN_SCOPUS_ISI_WEB_OF_SCIENCE/links/595f16440f7e9b8194b72d3d/COMPARISON-BETWEEN-SCOPUS-ISI-WEB-OF-SCIENCE.pdf?_sg%5B0%5D=xtnRHPojzghEiFKnOowLknjF01MHrMw7pO44CLy7C7PEIyp6870c1PDGIGv0EKc992BT0lQ9zZmSyPNGYm3JYQ.02YYZ82vdiiMAxpG6z_7HnX18gRoUHUHJ31f8YrYhg7Kd5WZZu_aGgkiLlmpSnDIq46bqemQjTiUmCr2CQ6aQw&_sg%5B1%5D=CL7SfQlE9FbNZqv89K4-wx6a-arg0bPwz_lNn3qbeC1pbNsQPxYDPqcWsww_iYYpSErsS6tLvp4_ysnKovwaS1ViAJTXWX566_wNLwnRvHhs.02YYZ82vdiiMAxpG6z_7HnX18gRoUHUHJ31f8YrYhg7Kd5WZZu_aGgkiLlmpSnDIq46bqemQjTiUmCr2CQ6aQw&_iepl=).

- Jun, H. (2016). Corporate governance and the institutionalization of socially responsible investing (SRI) in Korea. Asia Pacific Business Review, 22(3), 487–501. https://doi.org/10.1080/13602381.2015.1129770

- Karim, A. E., Albitar, K., & Elmarzouky, M. (2021). A novel measure of corporate carbon emission disclosure, the effect of capital expenditures and corporate governance. Journal of Environmental Management, 290, 112581. https://doi.org/10.1016/j.jenvman.2021.112581

- Kocmanova, A., Nemecek, P., & Simberova, I. (2006). Qualitative relationships between the environmental, social and governance (ESG) performance indicators for supporting the decision-making. WMSCI 2006 - The 10th World Multi-Conference on Systemics, Cybernetics and Informatics, Jointly with the 12th International Conference on Information Systems Analysis and Synthesis, ISAS 2006 - Proc., 1.

- Koroleva, E., Baggieri, M., & Nalwanga, S. (2020). Company performance: Are environmental, social, and governance factors important? International Journal of Technology, 11(8), 1468–1477. https://doi.org/10.14716/ijtech.v11i8.4527

- Lee, J., Kim, S., & Kim, E. (2021). Voluntary disclosure of carbon emissions and sustainable existence of firms: With a focus on human resources of internal control system. Sustainability (Switzerland), 13(17), 9955. https://doi.org/10.3390/su13179955

- Leins, S. (2020). ‘Responsible investment’: ESG and the post-crisis ethical order. Economy and Society, 49(1), 71–91. https://doi.org/10.1080/03085147.2020.1702414

- Mah, S. K. (2021). Earth, wind, and fire: Pace plays a vital ESG role. Journal of Structured Finance, 26(4), 73–85. https://doi.org/10.3905/JSF.2021.26.4.073

- Mercereau, B., Neveux, G., Sertã, J. P. C. C., Marechal, B., & Tonolo, G. (2020). Fighting climate change as a global equity investor. Journal of Asset Management, 21(1), 70–83. https://doi.org/10.1057/s41260-020-00150-9

- Nawaz, K., Saeed, H. A., & Sajeel, T. A. (2020). Covid-19 and the State of research from the perspective of psychology. International Journal of Business and Psychology, 2(1), 35–44. https://ijbpsy.com/wp-content/uploads/2020/08/IJBPSY2020-kalsoom-1.pdf.

- Nicholls, A. (2010). The institutionalization of social investment: The interplay of investment logics and investor rationalities. Journal of Social Entrepreneurship, 1(1), 70–100. https://doi.org/10.1080/19420671003701257

- Nofsinger, J., & Varma, A. (2014). Socially responsible funds and market crises. Journal of Banking and Finance, 48(C), 180–193. https://doi.org/10.1016/j.jbankfin.2013.12.016

- Nollet, J., Filis, G., & Mitrokostas, E. (2016). Corporate social responsibility and financial performance: A non-linear and disaggregated approach. Economic Modelling, 52(B), 400–407. https://doi.org/10.1016/j.econmod.2015.09.019

- Ognen, R., Thomson, T., & Scores, R. E. (2017). Thomson Reuters ESG Scores.

- Popescu, I. S., Hitaj, C., & Benetto, E. (2021). Measuring the sustainability of investment funds: A critical review of methods and frameworks in sustainable finance. Journal of Cleaner Production, 314, 128016. https://doi.org/10.1016/j.jclepro.2021.128016

- PRI. (2021) . What are the principles for responsible investment?

- Ruggie, J. G., & Middleton, E. K. (2019). Money, millennials and human rights: Sustaining ‘sustainable investing’. Global Policy, 10(1), 144–150. https://doi.org/10.1111/1758-5899.12645

- Sætra, H. S. (2021). A framework for evaluating and disclosing the ESG related impacts of ai with the sdgs. Sustainability (Switzerland), 13(15), 8503. https://doi.org/10.3390/su13158503

- Sanguankaew, P., & Ractham, V. V. (2019). Bibliometric review of research on knowledge management and sustainability, 1994-2018. Sustainability (Switzerland), 11(16), 4388. https://doi.org/10.3390/su11164388

- Senadheera, S. S., Withana, P. A., Dissanayake, P. D., Sarkar, B., Chopra, S. S., Rhee, J. H., & Ok, Y. S. (2021). Scoring environment pillar in environmental, social, and governance (ESG) assessment. Sustainable Environment, 7(1), 1960097. https://doi.org/10.1080/27658511.2021.1960097

- Singal, M. (2014). The link between firm financial performance and investment in sustainability initiatives. Cornell Hospitality Quarterly, 55(1), 19–30. https://doi.org/10.1177/1938965513505700

- Tang, M., Liao, H., Wan, Z., Herrera-Viedma, E., & Rosen, M. A. (2018). Ten years of Sustainability (2009 to 2018): A bibliometric overview. Sustainability (Switzerland), 10(5), 1655. https://doi.org/10.3390/su10051655

- Van De Putte, A., Proctor, J., Blankenship, M., Kelimbetov, K., Turner, A., Njagulj, A., & Wu, H. (2015). Assessing the investability of thermal coal over the next 20 years. Journal of World Energy Law and Business, 8(5), 398–424. https://doi.org/10.1093/jwelb/jwv021

- Van Duuren, E., Plantinga, A., & Scholtens, B. (2016). ESG integration and the investment management process: Fundamental investing reinvented. Journal of Business Ethics, 138(3), 525–533. https://doi.org/10.1007/s10551-015-2610-8

- Van Eck, N., & Waltman, L. (2010). Software survey: VOSviewer, a computer program for bibliometric mapping. scientometrics, 84(2), 523–538. https://doi.org/10.1007/s11192-009-0146-3

- Veenstra, E. M., & Ellemers, N. (2020). ESG indicators as organizational performance goals: Do rating agencies encourage a holistic approach? Sustainability (Switzerland), 12(24), 10228. https://doi.org/10.3390/su122410228

- Wang, Z., & Sarkis, J. (2017). Corporate social responsibility governance, outcomes, and financial performance. Journal of Cleaner Production, 162, 1607–1616. https://doi.org/10.1016/j.jclepro.2017.06.142

- Wang, Z., Sarkis, J., & D. Huaccho Huatuco, Jairo Rafael Mo, L. (2013). Investigating the relationship of sustainable supply chain management with corporate financial performance. International Journal of Productivity and Performance Management, 62(8), 871–888. https://doi.org/10.1108/IJPPM-03-2013-0033

- Wiklund, S. (2021). Evaluating physical climate risk for equity funds with quantitative modelling–how exposed are sustainable funds? Journal of Sustainable Finance and Investment, 1–26. https://doi.org/10.1080/20430795.2021.1894901

- WOS, 2021.Web of Science. https://www-webofscience-com-ssl.oca.korea.ac.kr/wos/woscc/advanced-search

- Yu, E. P., & Van Luu, B. (2021). International variations in ESG disclosure – Do cross-listed companies care more? International Review of Financial Analysis, 75(C), 101731. https://doi.org/10.1016/j.irfa.2021.101731