Figures & data

Table 1. Descriptive Statistics of the returns.

Table 2. Parameter estimates for cDCC model based on multivariate Student distribution.

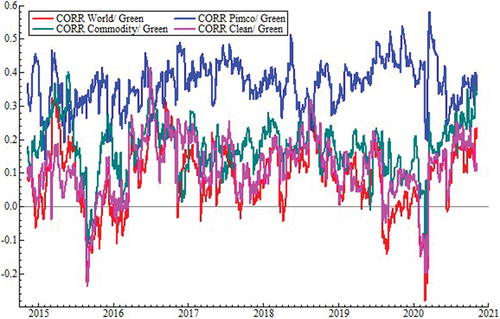

Figure 1. Dynamic conditional correlations.

Table 3. DCC, Hedge ratios and optimal portfolio weights summary statistics.

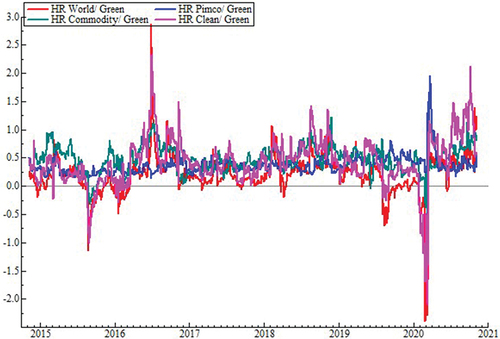

Figure 2. Optimal hedge ratios.

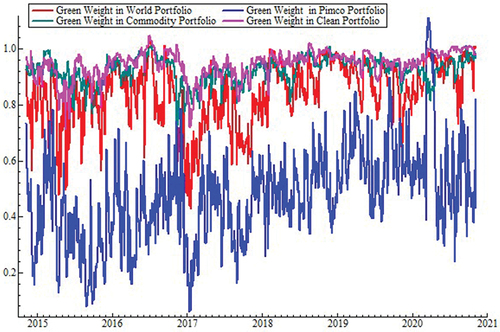

Figure 3. Optimal green bond weights.

Table 4. Portfolios’ average risk/downside risk reduction and utility gain improvement.