Figures & data

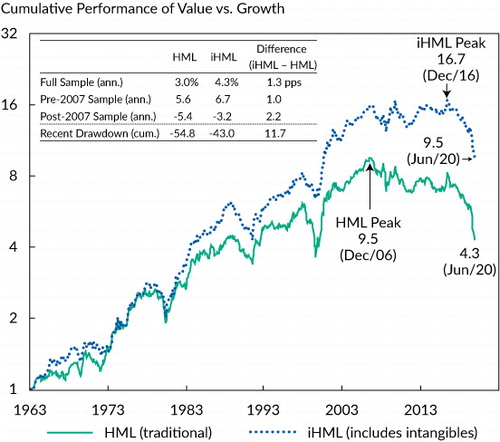

Table 1. Major Factor Performance, US Stocks

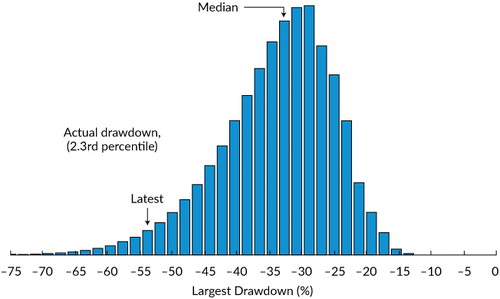

Table 2. US Value Stocks vs. US Growth Stocks: Worst Value Drawdowns, July 1963–June 2020

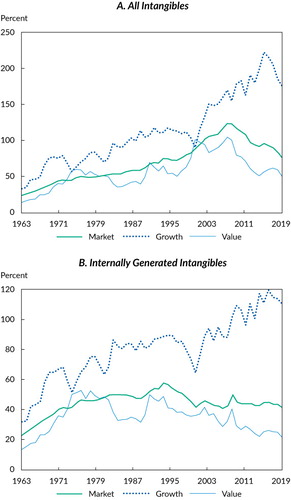

Notes: Panel A displays the ratio of all intangibles (capitalized R&D and 30% of SG&A plus acquired intangibles) to the tangible part of the book value of equity (the book value of equity minus acquired intangibles). Panel B displays the ratio of internally generated intangibles (capitalized R&D and 30% of SG&A) to the book value of equity.

Sources: Research Affiliates, LLC, using data from CRSP/Compustat; Peters and Taylor (2017).

Sources: Research Affiliates, LLC, using data from CRSP/Compustat.

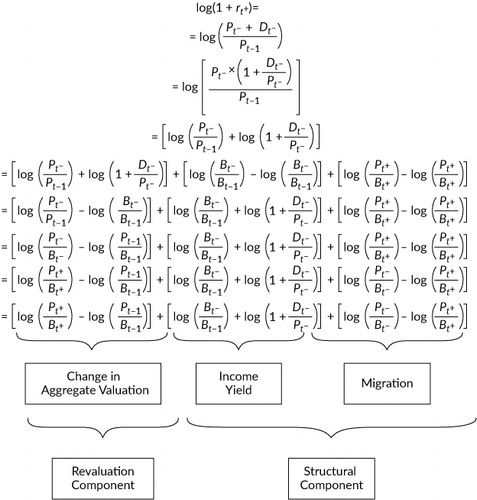

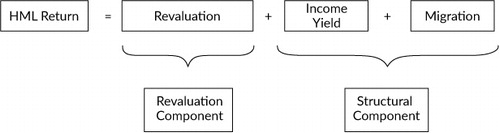

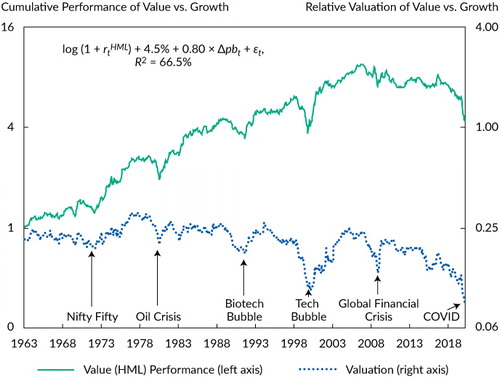

Table 3. Attribution of Value Factor Returns

Notes: We computed the relative valuations each month by

constructing a monthly rebalanced version of HML. The signal is the book value

of equity from a fiscal year that ended at least six months earlier divided by

the market value of equity lagged by six months. This signal matches the signal

of the annually rebalanced HML: When HML was rebalanced at the end of June in

year t, the book value of equity is from the fiscal year that

ended in year t – 1 and the market value is from December

of year t – 1. Our monthly version of HML matches the

standard HML’s valuations at the rebalancing points while still tracing

out valuations at a monthly frequency. Moreover, because most US companies have

December fiscal year-ends, the value factor (HML) becomes predictably cheaper

at the June rebalancing date. This rebalancing effect then dissipates over the

following year. We removed the resulting seasonalities from valuations by

subtracting the calendar month–specific (e.g., February) mean valuation and

adding back the unconditional mean valuation. An alternative method for constructing

a timely measure of value (and valuations) is the “HML devil,” which

divides the lagged book value of equity by the current price (Asness and Frazzini

2013). The

is HML return, and

is the change in the logarithm of the price-to-book ratio.

Sources: Research Affiliates, LLC, using data from CRSP/Compustat.

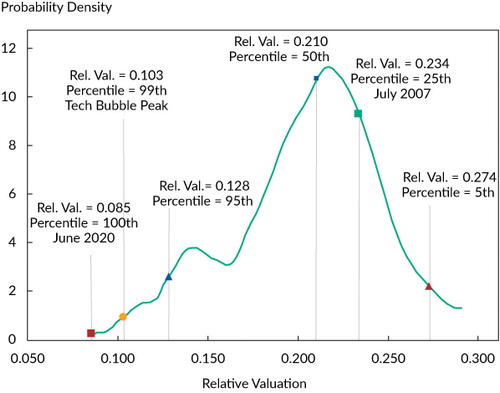

Table 4. Performance of Alternative Value Definitions: US Stocks

Notes: We estimated the theoretical distribution of valuations using kernel density estimation. We took the realized distribution of valuations from and used the Epanechnikov (parabolic) kernel with optimal bandwidth. This method can be considered to fit a smooth “density” over the historical histogram of valuations; it fills the gaps and makes educated guesses about the distribution outside the highest and lowest historical valuations. We have also placed the July 2007 and June 2020 relative valuations in this distribution plot.

Sources: Research Affiliates, LLC, using data from CRSP/Compustat.

Table 5. Scenario Analysis: Forward-Looking Expected Return, Conditional on Revaluation

Note: Bootstrap simulations are drawn from US HML returns for July 1963–December 2006.

Sources: Research Affiliates, LLC, using CRSP/Compustat data.

Table B1. HML vs. iHML Spanning Tests: US Market, July 1963–June 2020 (t-statistics in parentheses)