Figures & data

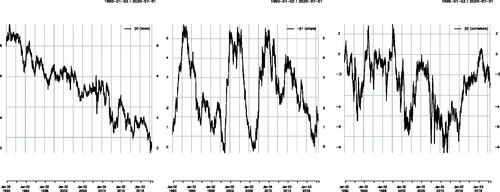

Figure 1. Yield Curve’s Level (Left Panel), Slope (Middle) and Curvature (Right Panel) Nelson–Siegel Model Parameters Estimated from Bond Prices, Assuming a Fixed Shape Parameter Equal to = 1.37 = 1/(12 × 0.0609) as in Diebold and Li (Citation2006)

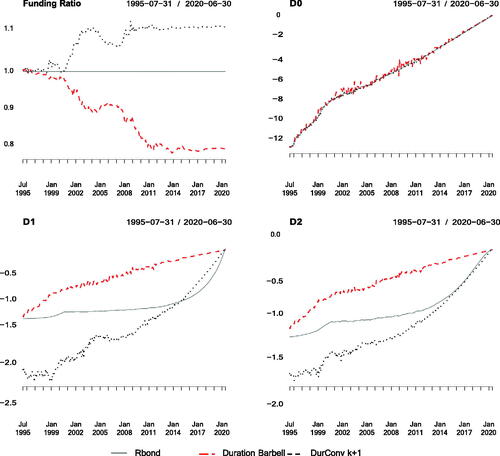

Figure 2. Funding Ratio and First-Order Sensitivities to the NS Factors of the Retirement Bond (Continuous Line), the Duration Barbell (Dashed Line), and the Duration-Convexity (Dotted Line) strategies implemented with k + 1 Bonds, Where k Is the Number of Factor Sensitivities Matched by the Strategy (2 and 3 for the Duration and Duration-Convexity Strategies, Respectively)

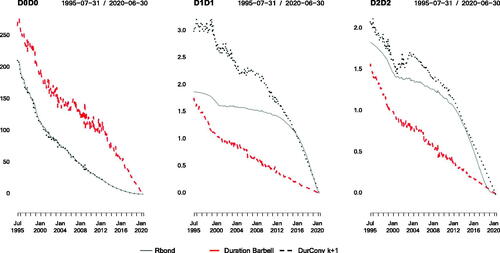

Figure 3. Second-Order Sensitivities to the NS Factors of the Retirement Bond (Continuous Line), the Duration Barbell (Dashed Line) and the Duration-Convexity (Dotted Line) Strategies Implemented with k + 1 Bonds, Where k Is the Number of Factor Sensitivities Matched by the Strategy (2 and 3 for the Duration and Duration-Convexity Strategies, Respectively)

Table 1. Number of Constituents (NC), Median and Maximum Leverage (Med Lev, Max Lev), Final Funding Ratio (FR.Final), Funding Ratio Median Absolute Deviation (FR.MEAD) and Maximum Absolute Deviation (FR.MAAD), and Average One-Way Monthly Turnover (TO) of Hedging Strategies Matching the Retirement Bond Yield Curve Factor Sensitivities Rebalanced Monthly

Table 2. Summary of Deviations in NS Factor Sensitivities of Hedging Strategies Relative to the Retirement Bond

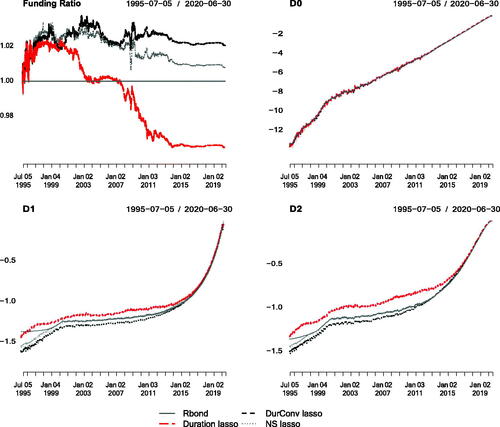

Figure 4. Funding Ratio and First-Order Sensitivities to the NS Factors of the Retirement Bond (Continuous Line), and the Hedging Strategies Implemented with All the Bonds Available and with a Lasso Regularization that Restricts the Gross Leverage below Three at All Times

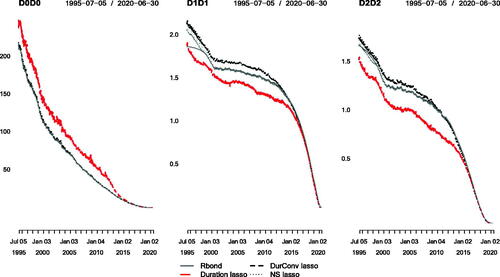

Figure 5. Second-Order Sensitivities to the Three NS Factors of the Retirement Bond, and of the Hedging Strategies Implemented with All the Bonds Available and with a Lasso Regularization that Restricts the Gross Leverage below Three at All Times

Table 3. Summary of Deviations in NS Factor Sensitivities of Long-Only Hedging Strategies Relative to the Retirement Bond