Figures & data

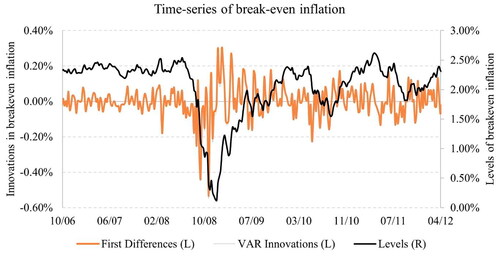

Figure 1. Innovations in Macro Variables Are Different from Levels: The Case of Breakeven Inflation

Table 1. Out-of-Sample Exposures of Mimicking Portfolios to Backward-Looking Variables

Table 2. Reliability of Macro Beta Estimates Using Different Regression Specifications: Out-of-Sample Betas with Targeted Macro Variables

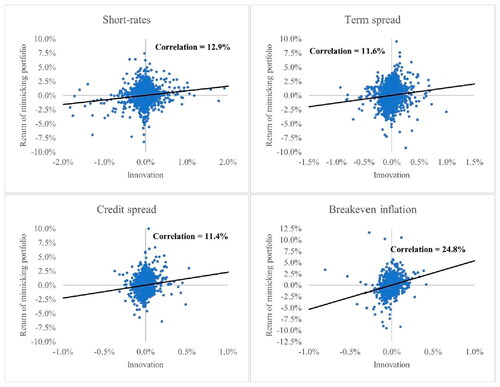

Figure 2. Relation between Returns on Macro Mimicking Portfolios and Macro Variables

Table 3. Realised Macro Exposures of Different Equity Macro Strategies

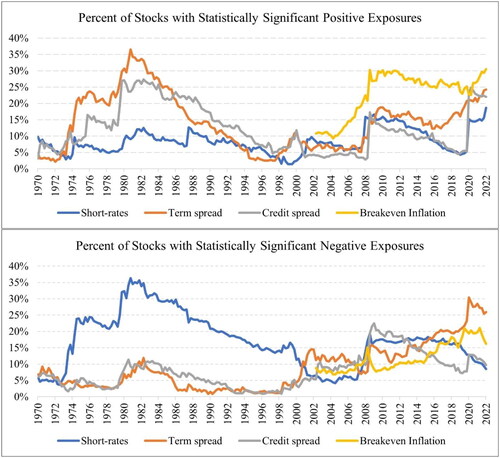

Figure 3. Percentage of Stocks with Statistically Significant Macro Exposures across Time

Table 4. Reliability of Macro Beta Estimates Using an Alternative Method to Form Mimicking Portfolios

Table 5. Ex-Ante and Realised Exposures of Equity-Style Factors

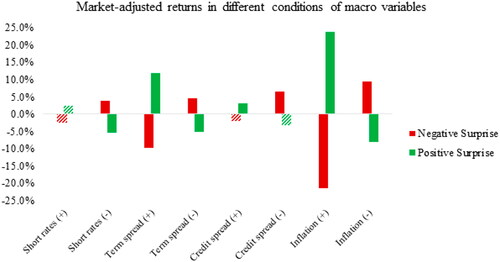

Figure 4. Conditional Relative Performance of Macro Dedicated Portfolios

Table 6. Unconditional Performance of Macro Dedicated Portfolios

Table 7. Unconditional Performance of Inflation Targeting Portfolios

Table 8. Factor Exposure Analysis of Macro Dedicated Portfolios

Table 9. Performance of Macro Dedicated Portfolios Net of Transaction Costs

Table 10. Performance of Inflation Portfolios Net of Transaction Costs