Figures & data

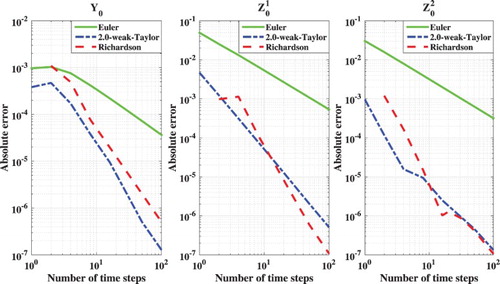

Figure 1. SABR example.

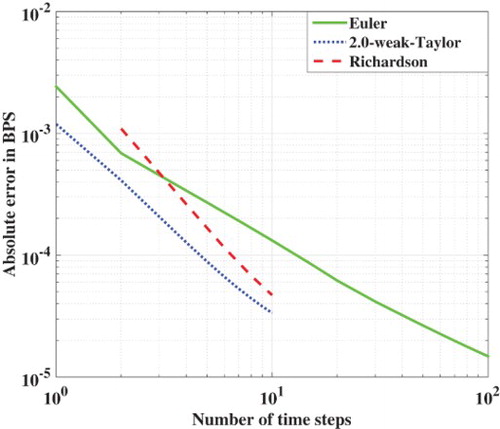

Table 1. Number of time steps and CPU time needed to obtain an absolute error of 1 or 0.5 basis points in the Black implied volatility for the Euler (with and without Richardson extrapolation) and 2.0-weak-Taylor schemes.

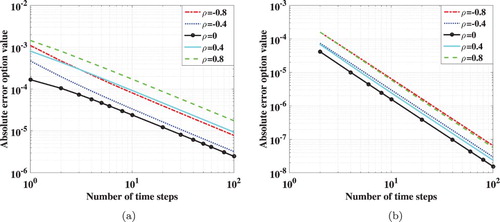

Figure 2. The Heston model with different correlations: (a) the Euler–Maruyama scheme and (b) Richardson extrapolation on the Euler results.

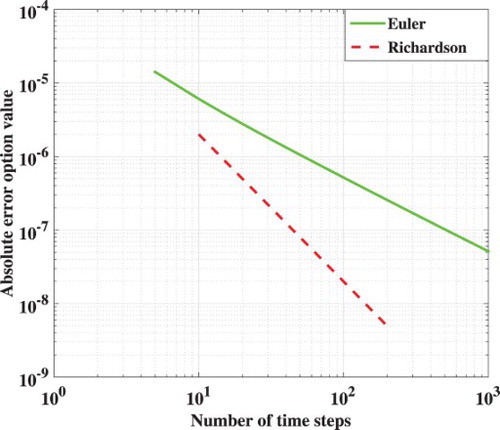

Figure 3. Heston Bermudan put with 5 early-exercise dates.

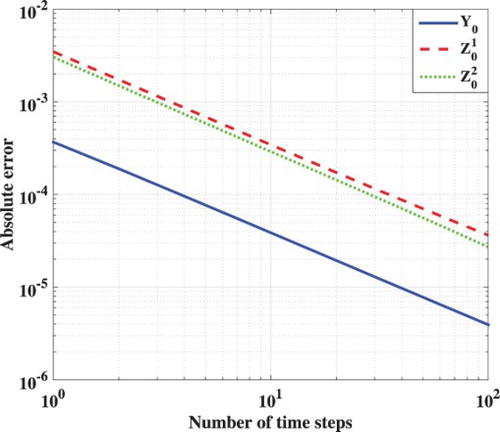

Figure 4. Geometric basket call option with the Euler scheme.

Figure 5. Spread option with the Euler scheme and CEV FSDEs (Equation52(47)

(47) ).

![Figure 5. Spread option with the Euler scheme and CEV FSDEs (Equation52(47) Zm1,Δ(x)=1Δtθ2Em[Ym+1Δ(Xm+1Δ)ΔWm+11]−1−θ2θ2Em[Zm+11,Δ(Xm+1Δ)+ρZm+12,Δ(Xm+1Δ)]+1−θ2θ2Em[f(tm+1,Λm+1Δ(Xm+1Δ))ΔWm+11]−ρZm2,Δ(x),(47) ).](/cms/asset/10a59364-b198-4651-882c-74aab787e1a0/gcom_a_1290438_f0005_c.jpg)

Figure 6. SABR example.