Figures & data

Table 1. List of methods used with abbreviations, marker symbol used in figures, references, and whether the MATLAB-implementation makes use of parallellism.

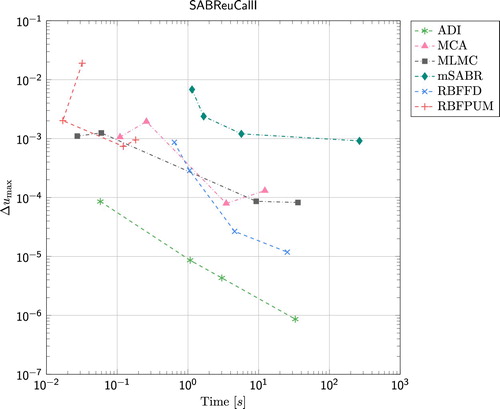

Figure 1. Results for the European call option under the SABR model, Parameter Set I. The reference values for ,

are given by 0.221383196830866, 0.193836689413803, and 0.166240814653231.

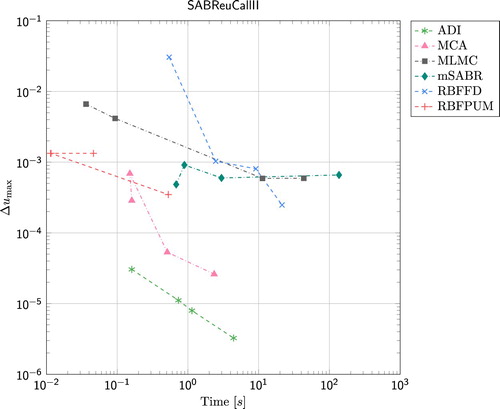

Figure 2. Results for the European call option under the SABR model, Parameter Set II. The reference values for ,

are given by 0.052450313614407, 0.046585753491306, and 0.039291470612989.

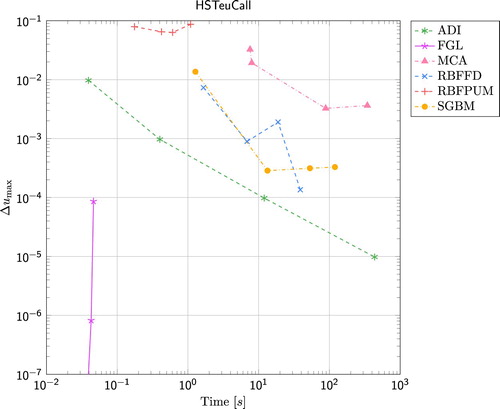

Figure 3. Results for the European call option under the Heston model. The reference values for , 100, and 125 are given by 0.908502728459621, 9.046650119220969, and 28.514786399298796.

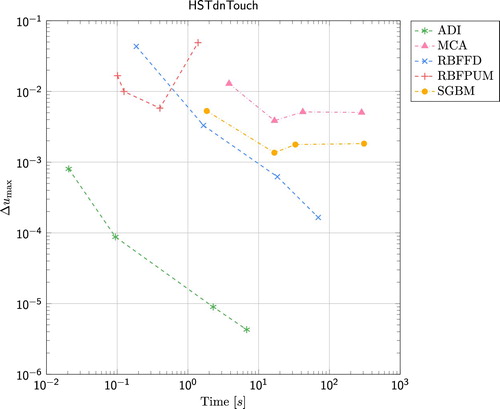

Figure 4. Results for the Double-no-touch option under the Heston model. The reference values for , 100, and 125 are given by 0.834539127387590, 0.899829293208866, and 0.668399975738358.

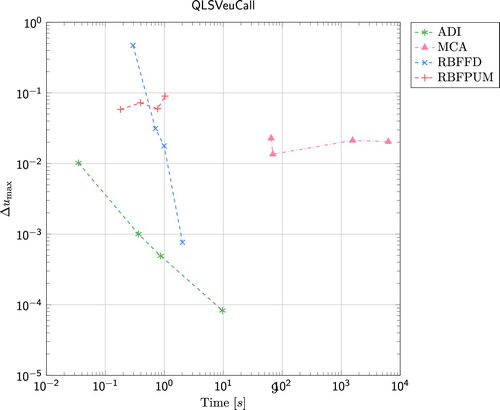

Figure 5. Results for the European call option under the QLSV model. The reference values for , 100, and 125 are given by 0.527472759419533, 8.902347915743665, and 29.159828965633729.

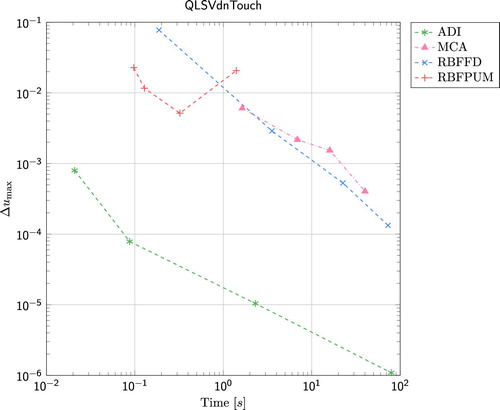

Figure 6. Results for the Double-no-touch option under the QLSV model. The reference values for , 100, and 125 are given by 0.933800903110254, 0.914799140676374, and 0.592983062889906.

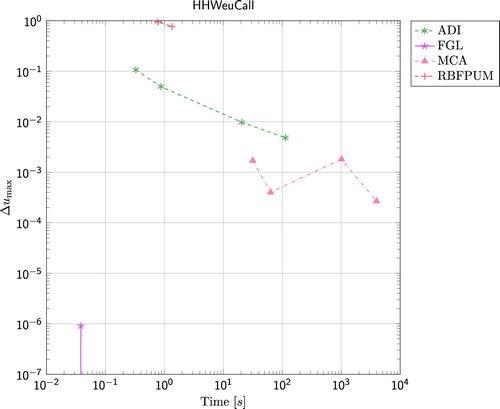

Figure 7. Results for the European call option under the HHW model. The reference values for , 100, and 125 are given by 35.437896876285350, 54.728065308229503, and 75.397596834993621.