Figures & data

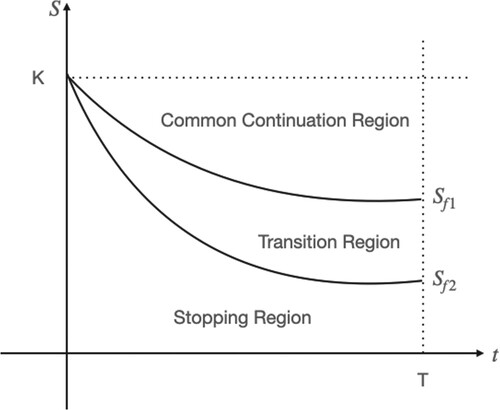

Figure 1. The option pricing domain with two optimal exercise boundaries.

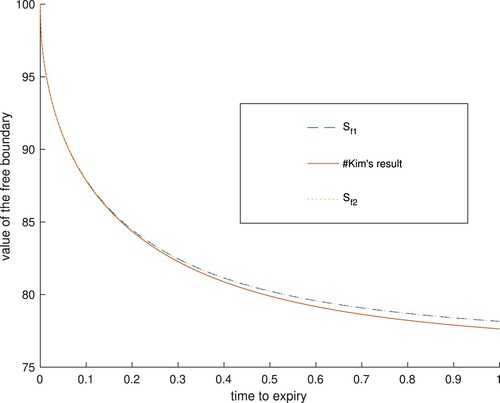

Figure 2. The optimal exercise boundaries when the regime-switching model degenerate to Black–Scholes model.

Table 1. Optimal exercise price of perpetual American puts.

Table 2. Comparison of the CPU time.

Table 3. Comparison of the CPU time.

Table 4. Comparison of the American put option price in regime 1.

Table 5. Comparison of the American put option price in regime 2.

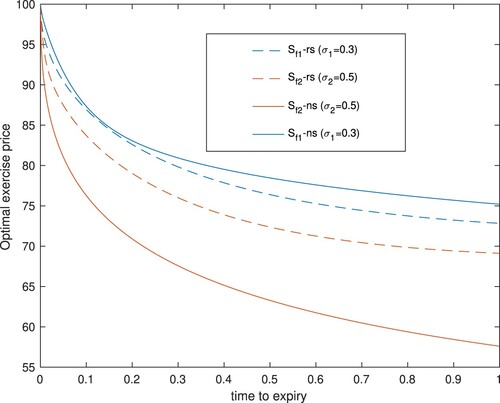

Figure 3. The optimal exercise boundaries.

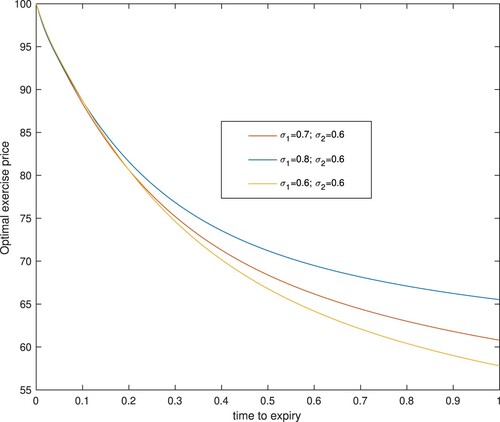

Figure 4. The optimal exercise boundaries with different volatilities().

Table 6. Parameters for regime-switching volatilities.

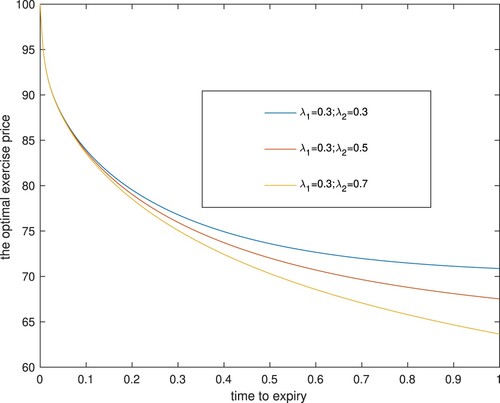

Figure 5. Two optimal exercise boundaries with different transition rates.

Table 7. Optimal exercise decision in a known state.

Table 8. Option value when the state is hidden.