Figures & data

Table 1 A summary of the robust estimators introduced in Section 2.4, where AC, CV, J, W, and WZ represent estimators proposed in Altissimoa and Corradic (Citation2003), Crainiceanu and Vogelsang (Citation2007), Jirak (Citation2015), Wu (Citation2004), and Wu and Zhao (Citation2007), respectively.

Table 2 Summary of the statistical meanings of p, q, P and their associated quantities.

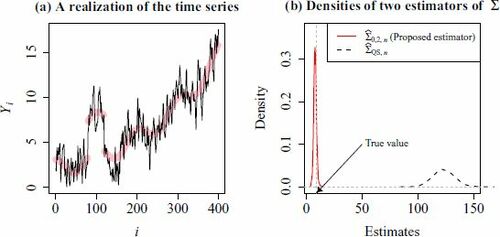

Fig. 1 (a) A typical realization of the time series with the mean function defined in (21). (b) The density functions of and

when n = 400. The true value is Σ = 9.

Fig. 2 The values of and

are plotted against n, where

denotes the MSE when the jump size ξ = 0, and

denotes the standard deviation of the MSEs across different ξ. Recall that smaller

and smaller

imply higher efficiency and robustness, respectively. Note that

is computed only when

because it requires a computationally intensive cross-validation step. Note that horizontal axis is plotted in the logarithmic scale for better visualization.

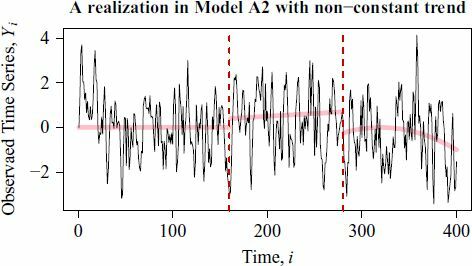

Fig. 3 Thin solid line: A realization of in Model A2 of length n = 400. Thick solid line: The nonconstant mean function

in Section 5.2. Dotted vertical lines: The change points.

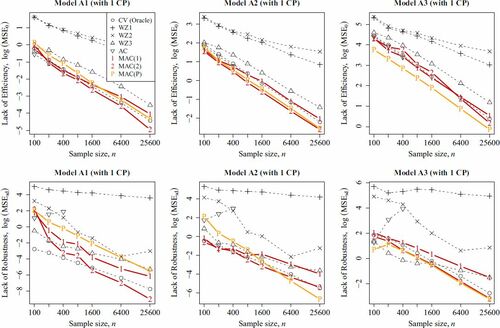

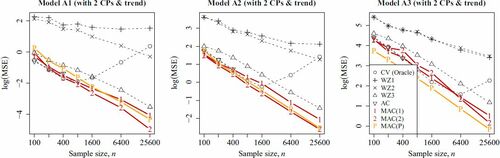

Fig. 4 The values of of different estimators are plotted against the sample size n in Models A1–A3. Here the mean function consists of nonconstant trends and multiple jumps (see Section 5.2 and ). Note that horizontal axis is plotted in the logarithmic scale.

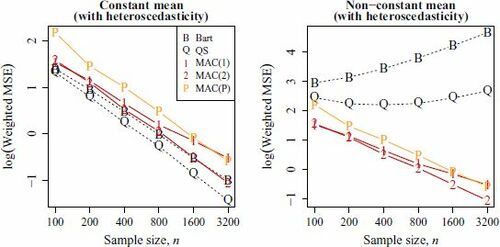

Fig. 5 The values of for

,

,

and

in the heteroscedastic case are plotted against n, where

is used, and

is defined in (16). The left and right plots show the results in the constant mean and nonconstant mean cases, respectively. Note that the horizontal axes are plotted in the logarithmic scale.

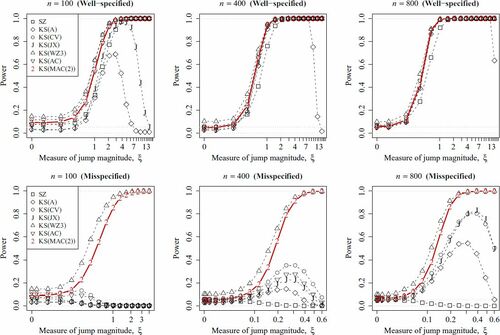

Fig. 6 The powers of the CP tests defined in Section 5.4 are plotted against the jump magnitude ξ under Model B2. The scenarios under well-specified alternative H1 and misspecified alternative are shown in the upper and lower plots, respectively. Dashed horizontal lines indicate the significance level

and zero. Note that horizontal axis is plotted in the logarithmic scale for better visualization.

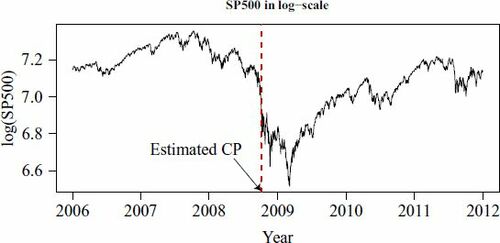

Fig. 7 Time series plot of , that is, the daily S&P 500 Index (3 January 2006–30 December 2011) in the log scale (see Section 6.1). The vertical dotted line indicates the value of

estimated by the statistic in Wu and Zhao (Citation2007). Here

is estimated by MAC(2).

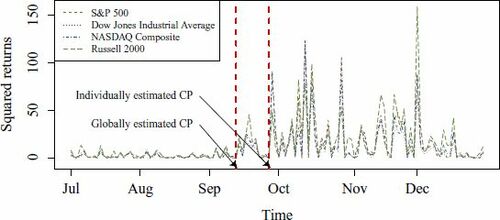

Fig. 8 The squared returns of four stock indices (1 July 2008–30 December 2008) (see Section 6.2). The two vertical lines denote the CP locations. The earlier and later CPs are detected by the multivariate and univariate CUSUM CP estimators, respectively.