Figures & data

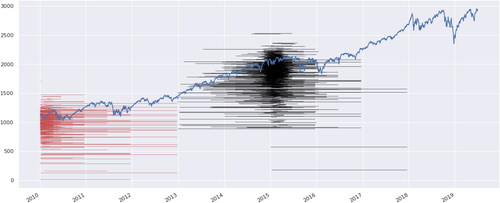

Fig. 1 A sample of the obtained put options along with the underlying’s (S&P 500) price process in blue. Only options that have a trading volume of more than 1000 on some trading day are included. Each red (black) line segment represents a put option that had price quotes within the first quarter of 2010 (2015). The corresponding strike is indicated as the value on the y-axis. Small random vertical shifts are added to increase the visibility of the options.

Table 1 This table presents a (simplified) preview of one of the four processed datasets.

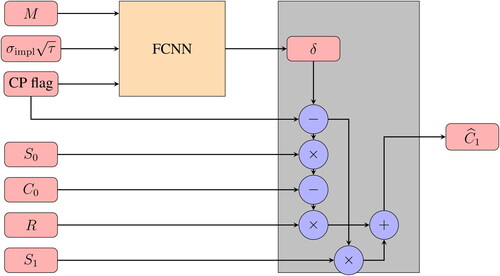

Fig. 2 A schematic graph of HedgeNet. The features are transformed into a hedging position by a fully connected feed-forward neural network (FCNN). The additional input is used to compute the value of the replicating portfolio.

Fig. 3 A detailed schematic presentation of HedgeNet. Recall that and

are moneyness and square root of total implied variance. “CP flag” is a Boolean flag for the option type; it equals 1 for puts and 0 for calls. Next, S0 and S1 are the underlying’s prices at the beginning and end of the hedging period, C0 denotes the option price at the beginning of the period, and

denotes the replication value. Finally,

is the risk-free overnight return.

Table 2 Performance of the linear regressions and ANNs on the S&P 500 dataset.

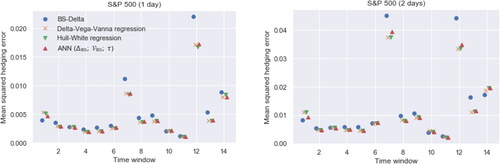

Fig. 4 MSHEs of four different statistical models for the hedging ratio across all 14 time windows in the S&P 500 dataset, for the one-day (left) and two-day (right) hedging period. The in-sample sets for periods 7 and 12 range from 2013 to the first half of 2015 and the second half of 2015 to 2017, respectively. The test data for the 7th time window fall exactly in the 2015–16 selloff. The test data for the 12th time window contain the first week of February 2018, where the S&P 500 experienced a 10% drop; see also .

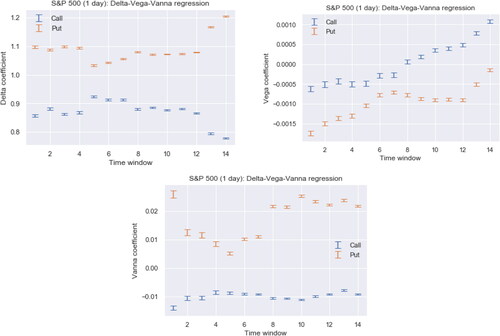

Fig. 5 The coefficients in the Delta-Vega-Vanna regression for each of the 14 time windows in the S&P 500 dataset. The top and bottom of each line segment are the point estimate plus/minus two standard errors. These numbers correspond to the one-day hedging period. The coefficient plots for the two-day hedging periods (not displayed here) look very similar; in particular, the Vanna coefficients for calls are again stable. However, the Vanna coefficients for puts and the Vega coefficients for calls and puts are slightly more fluctuating.

Table 3 Performance of the benchmarks and ANNs on the Euro Stoxx 50 dataset, when the in-sample and out-of-sample are split into one time window.

Table 4 Coefficients of Delta-Vega-Gamma-Vanna regression for each sensitivity on the Euro Stoxx 50 dataset.

Table 5 Performance of the “fixed” hedging strategy on the S&P 500 and Euro Stoxx 50 datasets.