Figures & data

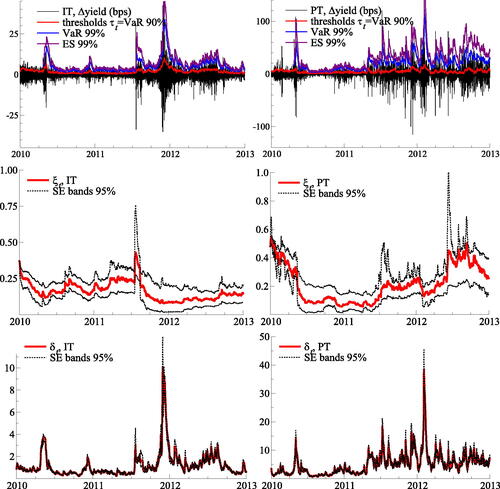

Fig. 1 News impact curves.

The first element (left panel) and second element (right panel) of st in (7) is plotted against xt for different values of ξt and δt.

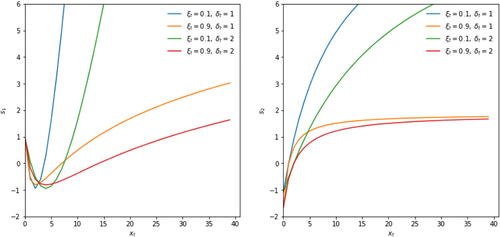

Fig. 2 Stationarity and moments regions.

Top row: the combinations of and

that satisfy A2 (left panel), and (15) for p = 2 (middle panel) and p = 4 (right panel), for an increasing number of iterations

. Bottom row: similar, but for combinations of

and

instead. Other deterministic parameters for each panel are fixed at their empirical estimates for S&P500 returns; see Section 4.1.

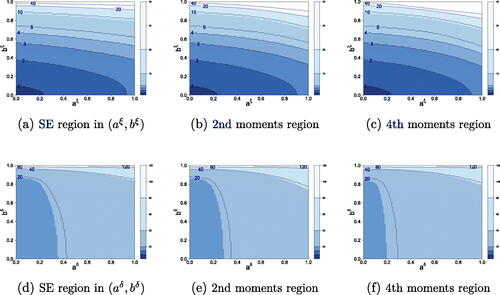

Fig. 3 Simulation results: an example.

Time series data is here generated as t

, where

and

. This is Path 3 in Section 3.1. Pseudo-true parameter values are reported in solid red. The four panels report estimates of ξt, δt, VaRt, and ESt, respectively. Median filtered values are plotted in solid black. The first two panels also indicate the lower 5% and upper 95% quantiles of the estimates (black dots). The time-varying threshold

is estimated based on the recursive specification (10) in conjunction with the objective function (18).

Table 1 RMSE outcomes for DGP1.

Table 2 Parameter estimates.

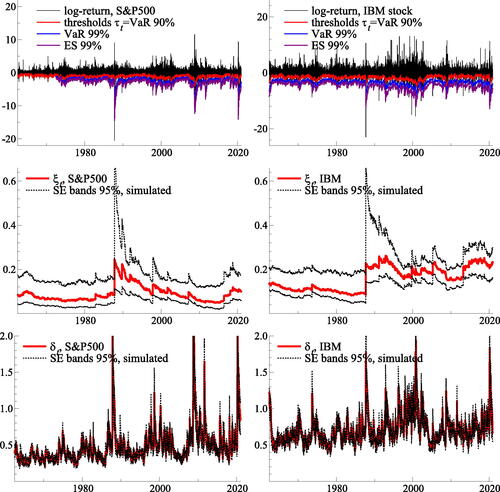

Fig. 4 Filtered tail parameters for S&P500 (left) and IBM (right) log-returns.

Top panels: daily log-returns for the S&P500 index (left) and IBM common stock (right). Middle and bottom panels: filtered tail shape (ξt, middle) and tail scale (δt, bottom) parameters. The thresholds τt are reported at a 90% confidence level; Value-at-Risk (VaR) and Expected Shortfall (ES) are plotted at an extreme 99% confidence level (top panels). The thresholds τt, VaR, and ES are mirrored at the horizontal axis to correspond to log-returns (instead of percentage losses). The estimation samples range from July 3, 1962 to December 31, 2020 for the S&P500 index, and from January 2, 1926 to December 31, 2020 for the IBM stock. The reported samples range from July 3, 1962 to December 31, 2020.

Fig. 5 The tail shape and tail scale estimates.

Top row: Five-year sovereign benchmark bond yields for Italy (IT, left column) and Portugal (PT, right column) between 2010 and 2012. Middle row: filtered tail shape (ξt) parameter. Bottom row: filtered tail scale (δt) parameter. Standard error bands are simulated at a 95% confidence level.