Figures & data

Table 1 Empirical sizes of the tests for at 5% level based on asymptotic critical values.

Table 2 Empirical sizes of the tests for at 5% level based on bootstrap critical values.

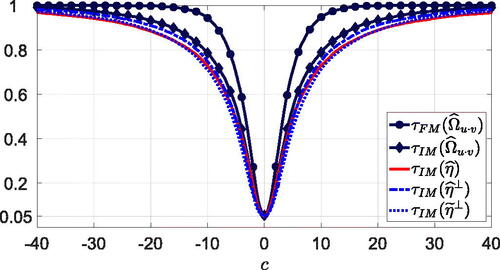

Fig. 1 Asymptotic power of the traditional and self-normalized Wald-type tests for at the nominal 5% level under local alternatives

. Note: The power curves for

and

coincide.

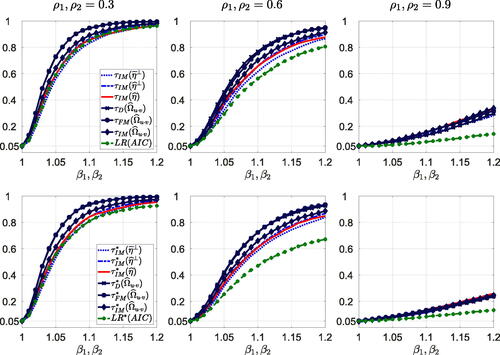

Fig. 2 Size-corrected power of the tests for at 5% level based on asymptotic critical values (top row) and bootstrap critical values (bottom row) for T = 100 and

. Note: Long-run variance parameters are estimated using the Bartlett kernel and the VAR sieve bootstrap is based on AIC.

Table 3 Realizations of test statistics for .

JBES-P-2022-0187_Revision2_Unblinded_OnlineAppendix.pdf

Download PDF (651.2 KB)Data Availability Statement

MATLAB code for empirical applications is available on www.github.com/kreichold/CointSelfNorm