Figures & data

Table 1. Number of audits and incidence of fraud by main audit types and in total

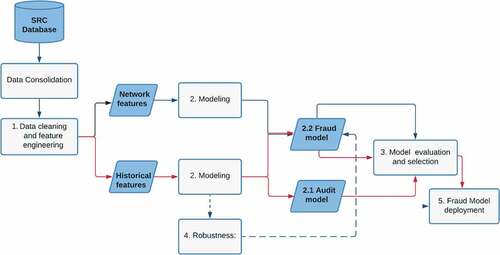

Figure 1. Fraud prediction approach using machine learning.

Table 2. Mean values of selected predictors of audit and fraud used in the study

Figure 2. Fraud distribution by taxpayer tenure (2019).

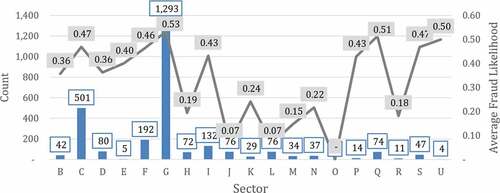

Figure 3. Fraud distribution by the taxpayer sector (NACE) of operation (2019).

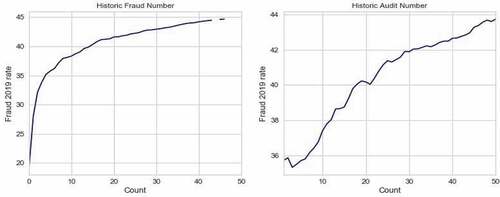

Figure 4. Effect of historical audits and frauds on probability of fraud in 2019.

Table 3. Results of Audit and Fraud classification models

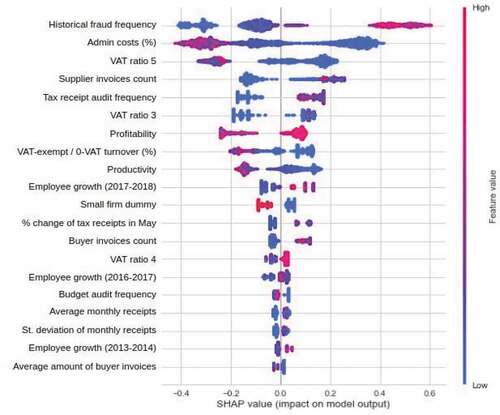

Figure 5. SHAP values for the variables used in the baseline fraud model.

Table 4. Audit model predictions and Fraud model actual accuracy by deciles

Table 5. Taxpayer’s network (supplier and buyer) characteristics used in the fraud model

Table 6. Comparison of fraud model performance with the exclusion of historical data and inclusion of taxpayer’s network information

Table A1. NACE Rev. 2 economic activity code key for

Table A2. Feature definitionsFootnote13

Table A3. Results of Audit Classification models

Table A4. Robustness: Alternative definitinos of target fraud variable